Japan Artificial Intelligence (AI) Optimised Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

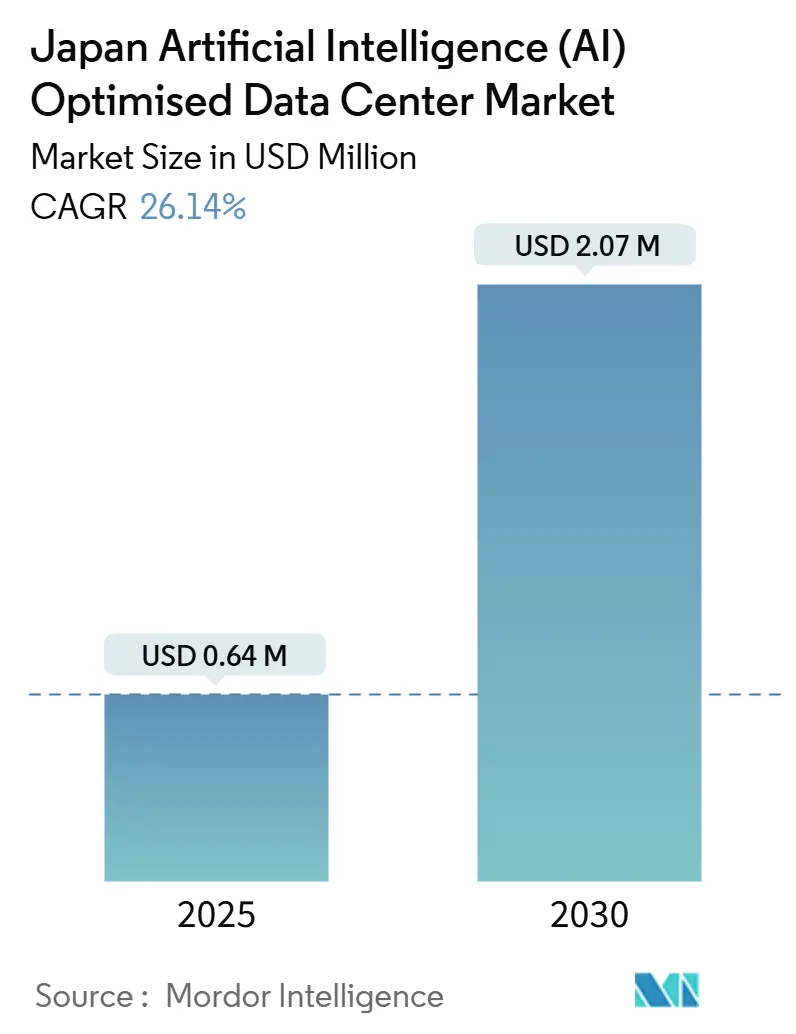

| Market Size (2025) | USD 0.64 Billion |

| Market Size (2030) | USD 2.07 Billion |

| Growth Rate (2025 - 2030) | 26.14% CAGR |

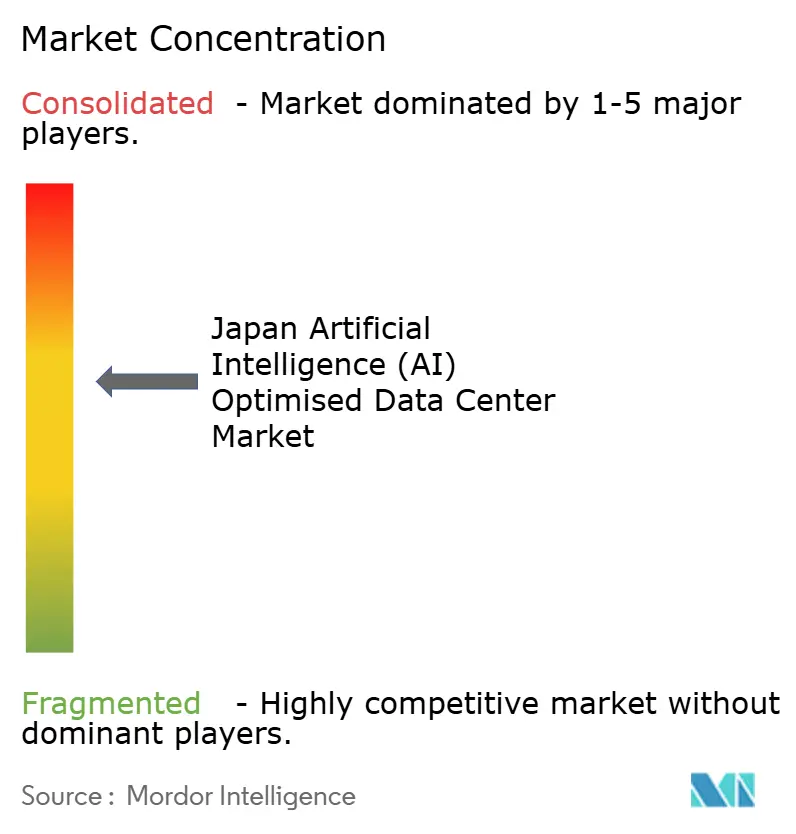

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Artificial Intelligence (AI) Optimised Data Center Market Analysis by Mordor Intelligence

The Japan artificial intelligence data center market size stands at USD 0.64 billion in 2025 and is projected to reach USD 2.07 billion by 2030, registering a 26.14% CAGR. High-density generative-AI workloads, a USD 10 billion national smart-city stimulus, and a USD 29.4 billion wave of hyperscaler capital are reshaping facility designs, cooling choices, and regional site selection. Operators are pivoting toward liquid cooling, 40-80 kW rack densities, and silicon-photonics switching to handle 10-fold compute growth while keeping PUE below 1.3. Public-private partnerships under the Digital Garden City Initiative reduce investment risk and accelerate secondary-city builds. Meanwhile, yen weakness inflates imported hardware costs, but it also encourages local manufacturing of cooling components and optical modules, subtly shifting the supply chain balance toward domestic vendors.

Key Report Takeaways

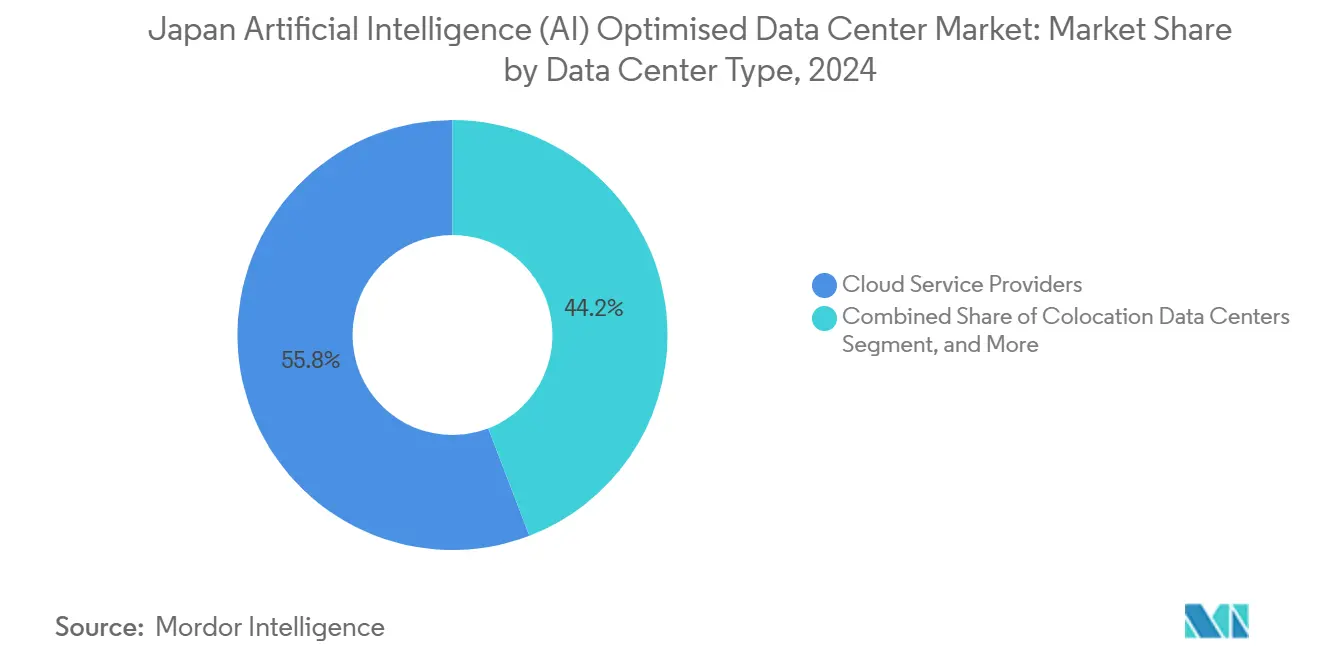

- By data-center type, cloud service providers led with 55.82% revenue share in 2024 in the Japan artificial intelligence data center market; colocation facilities are forecast to expand at a 28.23% CAGR through 2030.

- By component, software held 45.83% of the Japan artificial intelligence data center market share in 2024, while hardware infrastructure is advancing at a 27.67% CAGR to 2030.

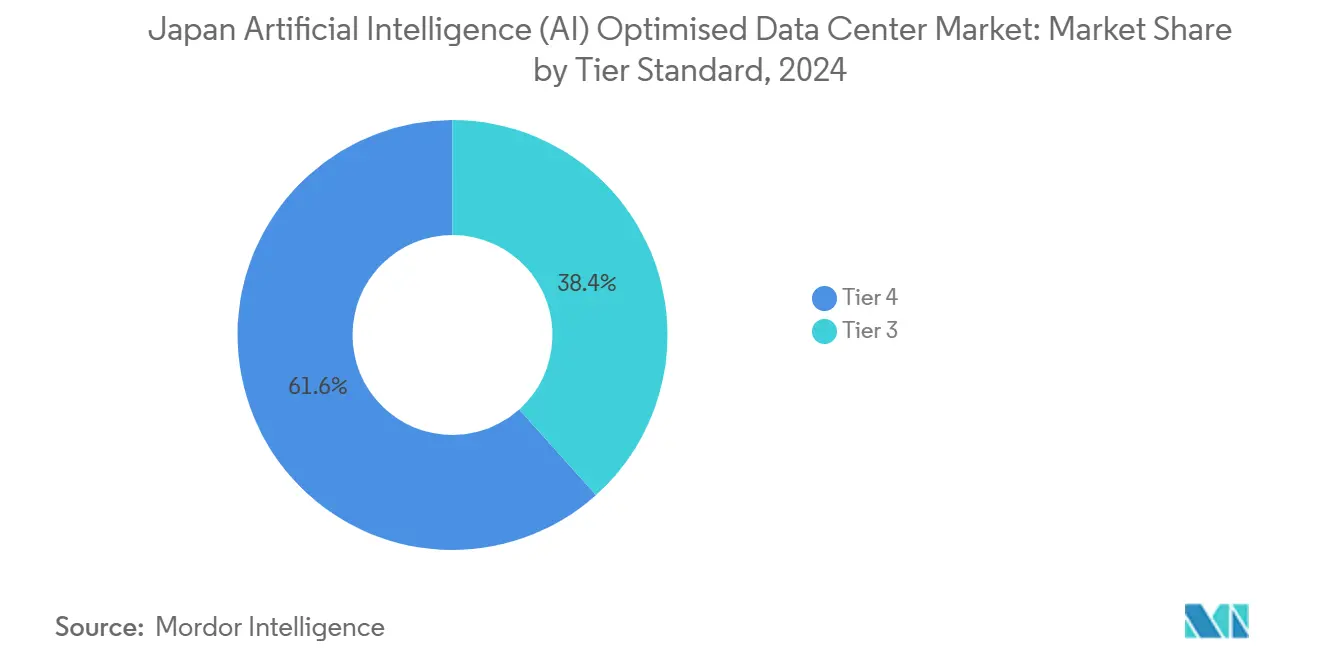

- By tier standard, Tier 4 captured 61.63% of the Japan artificial intelligence data center market size in 2024, yet Tier 3 is projected to accelerate at 28.77% CAGR between 2025-2030.

- By end-user industry, IT and ITES commanded 33.82% demand in 2024 in the Japan artificial intelligence data center market; Internet and digital media is rising fastest at 27.45% CAGR through 2030.

Global valuation is built by aggregating outputs from multiple countries and regions, with Japan being one of the contributors. Our global artificial intelligence (ai) data center market size represents that cumulative total.

Japan Artificial Intelligence (AI) Optimised Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative-AI/HPC compute boom | +6.5% | National, concentrated in Tokyo-Osaka corridor | Medium term (2-4 years) |

| Edge-to-core AI-ready colocation demand | +5.2% | National, with early gains in Kanagawa, Kobe, Ishikari | Long term (≥ 4 years) |

| Government Digital Garden City Initiative funding | +4.8% | National, priority zones in smart cities | Medium term (2-4 years) |

| Rapid adoption of silicon photonics switches | +3.1% | National, led by NTT IOWN deployment | Long term (≥ 4 years) |

| Carbon-free energy PPAs by hyperscalers | +2.8% | National, renewable-rich prefectures prioritized | Long term (≥ 4 years) |

| AI-based DCIM lowers OPEX | +2.0% | National, enterprise and colocation focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Generative-AI/HPC compute boom

NVIDIA’s partnership with SoftBank to deploy 25 AI exaflops shows how quickly compute density expectations are climbing, forcing rack-level power budgets from 10 kW to 80 kW.[1]NVIDIA Corporation, “SoftBank and NVIDIA to Build AI Factory,” nvidia.com Operators retrofit legacy halls with cold-plate and immersion solutions, while new builds integrate rear-door heat exchangers from the outset. KDDI and Sharp shifted a former LCD factory into Asia’s largest AI facility and demonstrated that brownfield assets can meet next-gen power and cooling demands without Tokyo land premiums. Government grants covering up to 30% of advanced-cooling capex further accelerate adoption. Enterprises outside the hyperscale core, such as research agencies running ABCI 3.0, are mirroring these design choices, broadening market depth. As a result, the Japan artificial intelligence data center market now prices projects on watts per rack rather than square footage, changing valuation norms.

Edge-to-core AI-ready colocation demand

Japan’s rail-linked, multi-core urban layout makes 5-millisecond latency a hard ceiling for autonomous factories and smart-intersection analytics.[2]Equinix, “AI-Ready Facilities in Japan,” equinix.com Colocation firms are planting 10-20 MW edge pods in Kanagawa and Kobe, bundling pre-installed direct fiber routes to core cloud regions, liquid cooling, and GPU-optimized power trees. This turnkey model attracts manufacturers migrating from on-premises rooms that cannot host 40 kW racks or support 415 V power backbones. Society 5.0 statutes further nudge industries to process data within prefectural boundaries, making these pods regulatory compliance enablers. As capsules fill, operators are layering AI-specific managed services, boosting average monthly recurring revenue per rack by up to 40% compared with legacy colocation. The virtuous cycle feeds land acquisition outside the overheated Tokyo–Osaka corridor and helps distribute the Japan artificial intelligence data center market toward regional economies.

Digital Garden City Initiative funding

The USD 10 billion Digital Garden City kitty offers subsidies that cover site preparation, renewable tie-ins, and flood-mitigation works.[3]Cabinet Office Japan, “Digital Garden City Initiative,” cao.go.jp Municipalities compete by lowering property taxes and waiving height restrictions for mega-halls. Projects must hit PUE less than or equal to 1.3 and source 50% green power by 2030, steering builders toward on-site solar plus Hokkaido wind PPAs. These conditions have turned Ishikari into a data-center cluster within two fiscal years despite its remote location. Operators benefit from fast-tracked environmental impact reviews that can shave six months off build schedules, a crucial advantage when GPU demand cycles reset every 18 months. The program also requires facilities to host community digital-skills labs, aligning public image with local employment promises and ensuring political momentum behind continued funding.

Rapid silicon-photonics switch adoption

NTT’s IOWN platform pushes 800 Gbps per channel with sub-microsecond latency, eliminating electronic-optical bottlenecks that throttle multi-GPU training clusters.[4]NTT Corporation, “IOWN Roadmap,” ntt.com Early roll-outs in Tokyo showed power savings near 75%, translating into operating-expense reductions large enough to offset higher upfront optics costs within three years. NTT is licensing designs to colocation providers, creating de facto interoperability standards across the Japan artificial intelligence data center market. Government semiconductor revival grants subsidize local photonic wafer fabs, cutting import exposure. Operators pairing optical backplanes with liquid cooling gain roughly 12% headroom on rack densities, postponing the need for expensive floor-plate expansions. This technology leap makes network fabric a new site-selection criterion, alongside power and fiber, influencing how regional campuses market themselves to hyperscaler tenants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of land and power in Tokyo/Osaka | -3.4% | Tokyo-Osaka metropolitan corridor | Short term (≤ 2 years) |

| Rising liquid-cooling capex and skill gap | -2.9% | National, acute in tier-2 cities | Medium term (2-4 years) |

| Grid-capacity permitting delays | -2.1% | National, concentrated in urban zones | Medium term (2-4 years) |

| Yen depreciation inflating imported HW | -1.8% | National, import-dependent facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarcity of land and power in Tokyo/Osaka

Vacant, flood-safe industrial plots inside Tokyo’s 23 wards have fallen by 40% since 2024, forcing auction prices past USD 8,000 per m². Grid operators warn that allocating the 20-50 MW blocks required by AI campuses now involves multi-year substation upgrades. This scarcity lengthens build timelines and nudges developers toward Kanagawa ports or Saitama brownfields, lengthening fiber back-haul paths and adding latency penalty cushions to SLA calculations. Some smaller players exit the market rather than absorb land premiums, pushing consolidation that concentrates bargaining power with incumbent landlords. Government land-reclamation projects may ease pressures after 2027, but until then the constraint clips near-term capacity adds in the Japan artificial intelligence data center market.

Rising liquid-cooling capex and skill gap

Direct-to-chip and immersion systems cost 3-4 times more than legacy CRAH deployments, elevating project IRR hurdles. Certified technicians earn 30-40% wage premiums, and only a handful of vocational programs teach pump-loop balancing or dielectric-fluid maintenance. Projects in tier-2 cities like Kobe experience commissioning delays of up to six months while hunting for specialized contractors. Operators respond with in-house academies, but the talent pipeline will take years to normalize. Consequently, capital-rich firms capture early mover advantage, skewing competition until the skill gap narrows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Hyperscalers Drive Colocation Surge

Colocation capacity represented 28.23% CAGR through 2030, outpacing all other deployment models as enterprises seek turnkey AI racks without running power or cooling plants. The Japan artificial intelligence data center market benefits because colocation offerings bundle 400 Gbps cross-connects into hyperscale cloud exchanges, giving tenants GPU-to-GPU latency under 1 millisecond. Service-level differentiation now centers on how many kilowatts per rack a provider can guarantee, not just floor footage. To compress deployment cycles, colocation operators pre-approve standard 15-rack AI pods with immersed NVIDIA GB200 clusters, slashing customer deployment lead times to six weeks.

Cloud service providers still hold 55.82% share in 2024, thanks to Microsoft, AWS, and Oracle’s USD 26 billion combined commitments. These hyperscalers vertically integrate power sourcing, optical fabrics, and ML ops teams, reinforcing control over AI PaaS layers. Yet they increasingly lease satellite halls from domestic telcos, illustrating a hybrid procurement model that keeps expansion flexible. Enterprise-owned on-premises rooms retain niche roles for sovereignty-sensitive workloads but cede growth momentum to shared capacity. Overall, the shift enlarges the addressable base of the Japan artificial intelligence data center market by drawing in mid-sized firms that previously lacked capex for AI hardware.

By Component: Hardware Investment Accelerates

Software’s 45.83% market share in 2024 reflected early-stage AI pilot runs, but the hardware slice is scaling fastest at 27.67% CAGR as production-stage models demand dedicated GPU clusters and 800 Gbps fabrics. Liquid-cooling skids, busways, and battery-less UPS lines now absorb over half of new-build spend, pushing per-MW capex to USD 12-15 million. The Japan artificial intelligence data center market size tied to hardware could top USD 1.4 billion by 2030 if current ratios persist. Vendors respond with modular slurry-loop kits and sub-floor coolant distribution rails, reducing field-install hours by 30% and partly offsetting higher material costs.

Services revenue rises steadily as enterprises outsource design, deployment, and optimization. Managed service firms guarantee rack-level availability, relieve customers of maintenance risk, and monetize AI-ready white glove support. Meanwhile, software spend migrates from experimentation toward inference orchestration and data-governance tooling, reflecting maturating use cases such as multimodal customer-service agents. The balanced stack underscores that the Japan artificial intelligence data center industry is no longer a pure cloud-software play; physical infrastructure now anchors value creation.

By Tier Standard: Tier 3 Gains Ground

Tier 4 retained 61.63% share in 2024, underscoring Japan’s zero-downtime corporate ethos. Yet Tier 3 sites book the highest 28.77% CAGR because many AI inference tasks tolerate brief maintenance windows when ownership costs drop accordingly. Operators package N+1 redundant power, liquid-cooling loops with dual pumps, and 24-hour refill reserves to emulate Tier 4 resilience at lower price points. Financial regulators still mandate Tier 4 for trading platforms, but manufacturers accept Tier 3 for production quality-control AI, widening the customer base.

The strategy doubles regional expansion: Tier 3 designs fit on smaller plots and need less power plant redundancy, making them viable in suburban industrial areas where Tier 4’s dual-utility feed requirement is impractical. This gradient approach also lets operators mix tiers within a campus, allocating coresidence AI dev environments to Tier 3 pods while reserving Tier 4 rooms for mission-critical inference. The tier mix increases utilization and enhances the Japan artificial intelligence data center market’s overall capital efficiency.

By End-user Industry: Media Sector Accelerates

IT/ITES captured 33.82% uptake in 2024 because system integrators and SaaS vendors were first to refactor code for GPUs. The Internet and digital-media vertical, however, is sprinting at 27.45% CAGR on the back of generative-video channels, real-time game streaming, and AI-driven subtitle localization. GPU inference farm contracts from anime studios and OTT platforms are often multiyear, raising forward coverage for capacity planners. Japan’s privacy-conscious banks expand AI fraud-detection clusters, while automotive suppliers push edge inference nodes into factory lines, creating dovetail demand at colocation edge sites.

Healthcare, encouraged by relaxed data-anonymization laws, pilots federated-learning models for medical imaging, boosting GPU hour consumption but requiring domestic hosting to satisfy patient-data laws. Defense agencies carve sovereign capacity zones within domestic telco campuses, melding national-security oversight with hyperscaler toolchains. The diversification means no single vertical can dominate capacity negotiations, preserving competitive balance in the Japan artificial intelligence data center market.

Geography Analysis

Tokyo owns roughly 45% of installed AI capacity, buoyed by dense enterprise headquarters and multiple undersea-cable landings. Osaka adds 25%, serving Kansai’s industrial belt and acting as primary disaster-recovery site. These metros face escalating real-estate costs and grid constraints that slow near-term megawatt adds. Consequently, Kanagawa and Saitama are becoming spillover beneficiaries, offering sub-40 km latency into central Tokyo while granting cheaper land leases and deferred urban-planning fees.

Farther afield, Ishikari in Hokkaido is gaining traction with cool ambient temperatures that shave 4-5 percentage points off annualized PUE. Sakura Internet’s JPY 100 billion (USD 640 million) GPU build exemplifies the climatic advantage and sets a benchmark for renewable-energy integration via surplus wind farms. Kyushu promotes solar-plus-battery hybrids, but typhoon resilience raises structural-engineering costs, producing a mixed investment calculus. Overall, diversification spreads risk across seismic zones, aligns with Society 5.0 disaster-continuity mandates, and extends the Japan artificial intelligence data center market footprint into regions once peripheral to the digital economy.

International hyperscalers now design triple-region Japan topologies, pairing Tokyo and Osaka cores with a northern or southern satellite for redundancy and data-sovereignty compliance. Prefectural governments sweeten these deals with expedited fiber-easement approvals and tax abatements tied to local hiring quotas. Over the forecast period, secondary markets could collectively command up to 35% of national AI rack capacity, diluting the primacy of the traditional Tokyo-Osaka corridor while sustaining national resiliency goals.

Coverage of the artificial intelligence (ai) data center market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America, South America, and Europe, alongside detailed country-level intelligence for Indonesia, Singapore, United States, Brazil, Germany, and Thailand, each shaped by local operating conditions.

Competitive Landscape

Collaboration defines competition: Microsoft anchors new builds on NTT leased fiber, AWS teams with KDDI for edge pop sites, and Oracle co-locates in SoftBank’s physical shells, avoiding regulatory frictions while accelerating ramp-ups. Top five operators command around 60% aggregate share, indicating a moderately concentrated field that still leaves room for niche challengers. Differentiation hinges on proprietary technology stacks, NTT’s IOWN optical mesh, Microsoft’s custom phase-change immersion, and AWS’s Graviton-integrated GPU cards all create switching costs that preserve margins.

Domestic telcos leverage right-of-way privileges to fast-track trunk-fiber extensions, an advantage that foreign hyperscalers willingly compensate for through revenue-share agreements. Edge specialists such as Telehouse Japan carve 5-10 MW micro-sites adjacent to manufacturing zones, using local customer intimacy as a moat. Meanwhile, AI DCIM analytics become table stakes: operators without automated thermal prediction face price discounts in RFPs. Sustainability credentials further tilt bids; facilities signing 100% renewable PPAs win regulatory goodwill and face lower municipal scrutiny. Overall, technical innovation outweighs raw floor-plate scale as the decisive factor in the Japan artificial intelligence data center market.

Japan Artificial Intelligence (AI) Optimised Data Center Industry Leaders

Equinix, Inc.

MC Digital Realty Co., Ltd.

KDDI Corporation (Telehouse)

Colt Data Centre Services (Colt Group S.A.)

NTT Global Data Centers Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SoftBank acquired Sharp’s former LCD panel plant in Sakai, Osaka, for approximately $676 million. The company plans to transform the facility into a large-scale AI data center with an initial power capacity of 150 megawatts, scalable up to 400 megawatts. Operations are expected to commence in 2026, aiming to support advanced AI workloads and services

- January 2025: Microsoft Japan completed its USD 2.9 billion AI and cloud build-out, adding three liquid-cooled regions connected to Azure OpenAI services.

- December 2024: Oracle closed an USD 8 billion two-region expansion with NVIDIA H100/H200 GPU zones.

- November 2024: AWS Japan launched phase one of a USD 15.5 billion roll-out, adding three AI-optimized zones with 400 Gbps fabrics.

Japan Artificial Intelligence (AI) Optimised Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

What is the projected value of the Japan artificial intelligence data center market in 2030?

It is forecast to reach USD 2.07 billion, expanding at a 26.14% CAGR.

Which deployment model is growing fastest?

Colocation data centers show a 28.23% CAGR as enterprises outsource high-density AI infrastructure.

Why are Tier 3 facilities gaining traction?

They balance cost and reliability, registering the highest 28.77% CAGR as many AI workloads can tolerate brief maintenance windows.

Which geographic areas beyond Tokyo and Osaka are attracting new builds?

Kanagawa, Kobe, and Ishikari prefectures are emerging destinations due to land availability, cooler climates, and renewable-energy access.

How are hyperscalers addressing sustainability requirements?

Companies like AWS and Google sign multi-hundred-megawatt PPAs, enabling facilities to reach 100% renewable energy targets and lower PUE below 1.3.

Page last updated on: