Malaysia Artificial Intelligence (AI) Optimised Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

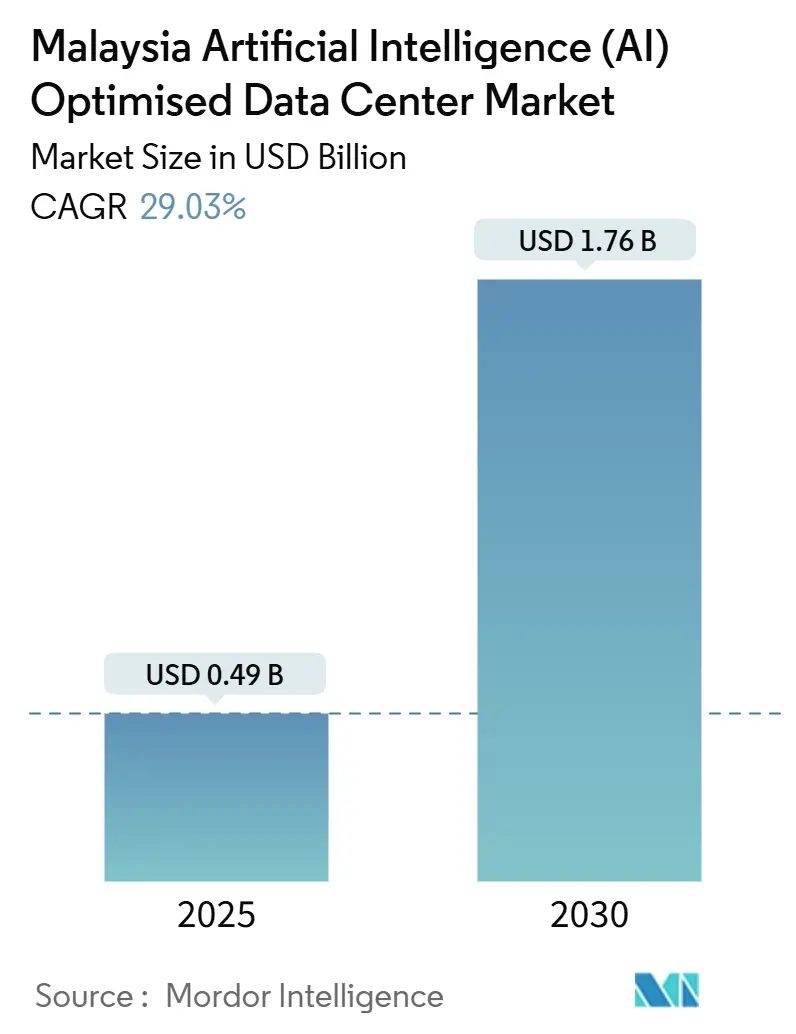

| Market Size (2025) | USD 0.49 Billion |

| Market Size (2030) | USD 1.76 Billion |

| Growth Rate (2025 - 2030) | 29.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Artificial Intelligence (AI) Optimised Data Center Market Analysis by Mordor Intelligence

Malaysia AI data center market size stood at USD 0.49 billion in 2025 and, supported by a forecast CAGR of 29.03%, is projected to cross USD 1.76 billion by 2030. Powerful hyperscaler capital inflows, streamlined government incentives, and Singapore spill-over demand position the nation as Southeast Asia’s next-generation AI hub. Johor’s 1,600 MW installed IT capacity, Cyberjaya’s dense interconnection ecosystem, and rising submarine-cable bandwidth reinforce Malaysia’s regional competitiveness. Intensified competition between Tier III and Tier IV facilities is compressing construction timelines as operators race to satisfy GPU-dense workloads. Meanwhile, power-purchase agreements (PPAs) and direct-to-chip liquid cooling point toward greener, higher-density deployments. Finally, talent shortages and rising land costs temper near-term optimism yet also accelerate consolidation among well-capitalized providers.

Key Report Takeaways

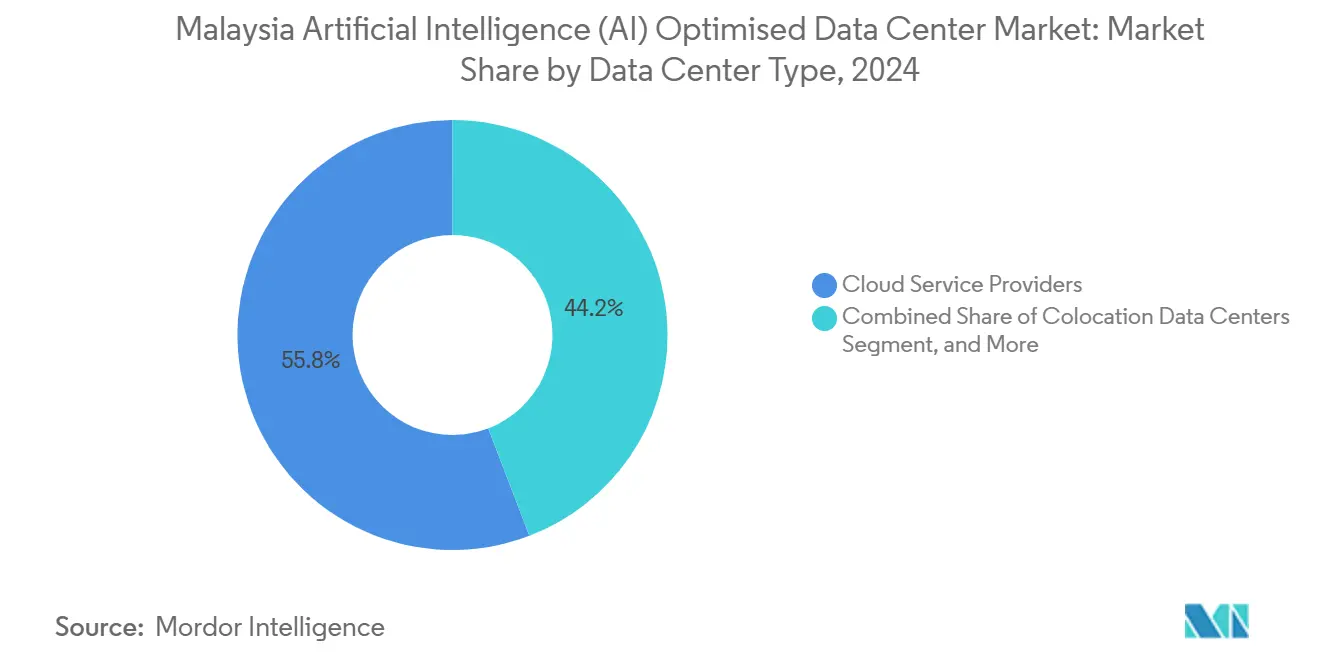

- By data-center type, Cloud Service Providers led with 55.82% of Malaysia AI data center market share in 2024; Colocation is advancing at 31.23% CAGR through 2030.

- By component, Software commanded 45.83% share of Malaysia AI data center market size in 2024, while Hardware is expanding at 30.67% CAGR to 2030.

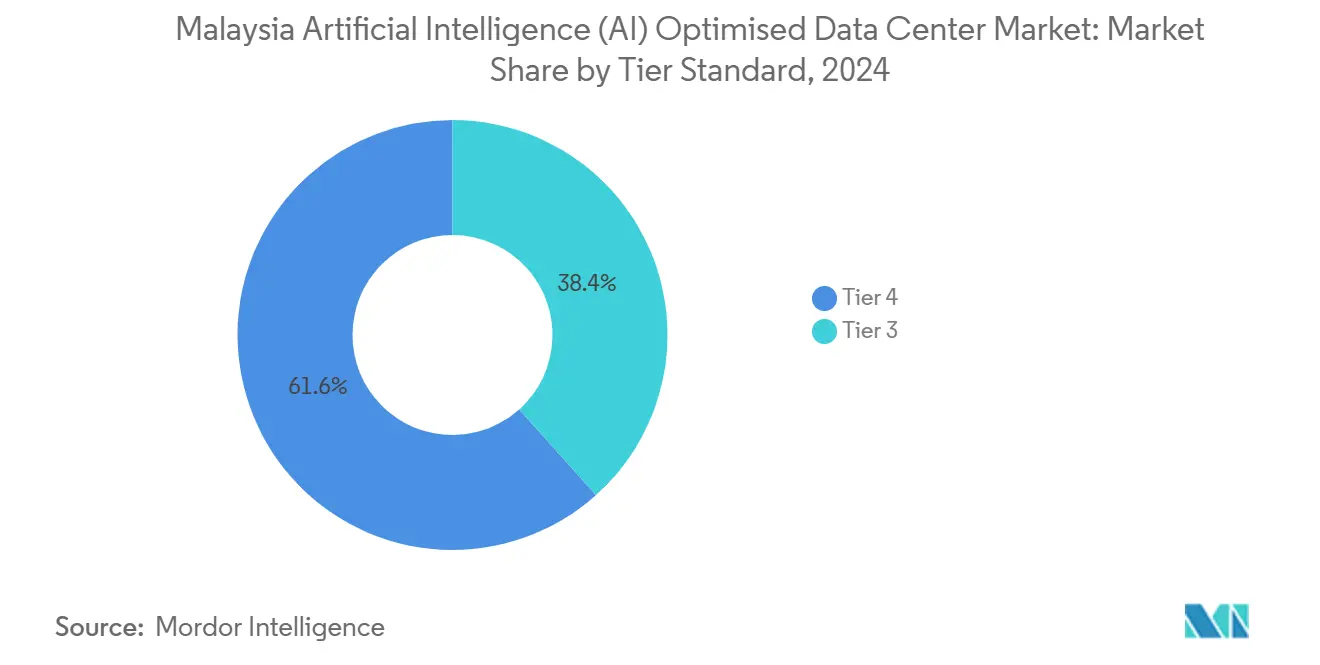

- By tier, Tier IV facilities held 61.63% share of Malaysia AI data center market size in 2024; Tier III is growing at 31.77% CAGR through 2030.

- By end-user, IT and ITES controlled 33.82% of Malaysia AI data center market share in 2024, whereas Internet and Digital Media is rising at 30.45% CAGR to 2030.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of Malaysia. The artificial intelligence (ai) data center market share in our global report expresses these relative weights.

Malaysia Artificial Intelligence (AI) Optimised Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscaler capital inflow into Cyberjaya and Johor | +8.5% | Johor, Klang Valley/Cyberjaya | Medium term (2-4 years) |

| Government incentives (MyDIGITAL, Green Lane Pathway) | +6.2% | Global | Short term (≤ 2 years) |

| Surging AI-workload density across BFSI and telecom sectors | +5.8% | National, with early gains in Kuala Lumpur, Johor Bahru, Penang | Medium term (2-4 years) |

| Submarine-cable and 5G upgrades improving international latency | +4.3% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Singapore spill-over demand for ultra-low-latency AI clusters | +7.1% | Johor, with secondary benefits to Klang Valley | Short term (≤ 2 years) |

| Corporate-renewable PPAs (CRESS) unlocking green AI campuses | +3.8% | National, with concentration in Johor and Selangor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyperscaler Capital Inflow Transforms Regional Infrastructure Dynamics

Record pledges, Google USD 2 billion, Microsoft USD 2.2 billion, AWS USD 6.2 billion, Oracle USD 6.5 billion, are shifting Malaysia from conventional hosting toward AI-native campuses with rack densities above 40 kW. Vantage’s 256 MW Cyberjaya build includes a dedicated 275 kV substation, underscoring the need for high-capacity grid tie-ins. Capital clustering lowers interconnection costs yet tightens competition for skilled engineers and utilities.

Government Incentives Accelerate Market Entry Through Regulatory Streamlining

The Digital Investment Office cuts permit cycles to 18-24 months, while the Green Lane Pathway slashes grid-connection lead-time to 12 months. TM Global scheduled Phase 2 expansions within 18 months of announcement, illustrating the benefit to hyperscalers.[1]TM Global, “TM Global Expands Data Centres in Cyberjaya and Johor to Strengthen Nation's Digital Transformation,” tmglobal.com.my Rapid approvals, however, inflate M&E contractor rates and squeeze smaller developers.

AI Workload Density Surge Reshapes BFSI and Telecom Infrastructure Requirements

More than 80% of Malaysian banks deploy AI for fraud detection and analytics, yet Bank Negara’s data-sovereignty rules require on-shore hosting. Concurrently, 5G coverage exceeding 80% of populated areas enables sub-10 ms edge inference, driving hybrid core-edge architectures. These trends multiply total compute demand across backbone and edge nodes.

Submarine Cable Upgrades Position Malaysia as Asia-Pacific Connectivity Hub

The Asia Link Cable’s 24 Tbps and SEA-ME-WE 6’s 100 Tbps designs anchor Malaysia’s role in regional AI traffic flows.[2]TM, “TM Joins Asia Link Cable System Consortium,” tm.com.my TM’s new Kuala Sedili landing cuts Singapore-Malaysia latency by 15-20%, supporting distributed model training. The forthcoming Candle system will further extend Japan-ASEAN throughput.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating power and cooling load threatening PUE targets | -4.2% | National, with acute pressure in Johor and Cyberjaya | Short term (≤ 2 years) |

| High capex and land-bank costs in primary hubs | -3.8% | Johor, Klang Valley/Cyberjaya | Medium term (2-4 years) |

| Carbon-footprint scrutiny and upcoming sustainability mandates | -2.9% | Global, with regulatory focus in Selangor and Johor | Long term (≥ 4 years) |

| Shortage of AI-specialised data-center talent | -3.1% | National, with skills gaps most acute in Kuala Lumpur and Johor Bahru | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Power and Cooling Load Escalation Challenges Efficiency Targets

AI racks consume 40-60 kW, outstripping legacy designs of 8-12 kW. AirTrunk’s direct-to-chip cooling cuts energy 23% yet raises capex. Water demand is projected at 808 million L/day versus 142 million L supply, prompting regulators to mandate alternative-cooling studies.

AI-Specialized Talent Shortage Constrains Operational Scaling

GPU-cluster, liquid-cooling, and high-frequency networking skills remain scarce, with Singapore wage premiums luring technicians abroad. Importing expertise inflates OPEX for smaller players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation Momentum Challenges Cloud Dominance

Colocation captured 31.23% CAGR through 2030 as enterprises sought hybrid deployments, although Cloud Service Providers kept 55.82% Malaysia AI data center market share in 2024. Malaysia AI data center market size for colocation is projected to scale rapidly as financial institutions pivot to data-residency-compliant hybrid models. Colocation operators leverage carrier-neutral fabrics enabling private connectivity to hyperscale clouds, thereby reducing latency and egress fees. TM Global’s Klang Valley upgrades and Equinix’s Johor–Cyberjaya dual metro illustrate strategic positioning for interconnection revenues.

Simultaneously, the Cloud segment maintains growth via direct hyperscaler builds that internalize future-proof design. AWS, Google, and Microsoft collectively anchor more than USD 10 billion in capital commitments, reinforcing scale advantages yet pressuring wholesale pricing structures.[3]Okoone Spark, “AWS Expands Asia Pacific Presence,” okoone.com Edge and on-premises micro-facilities remain niche, handling ultra-low-latency or regulated workloads.

By Component: Hardware Upgrades Define Spending Priorities

Hardware expanded at 30.67% CAGR, narrowing the 2024 lead held by Software (45.83% share). GPU cards, high-bandwidth memory, and rack-level liquid cooling dominate procurement budgets, driving multi-year refresh cycles distinct from traditional server uplifts. Malaysia AI data center market size for hardware elements is expected to surge as operators migrate toward 40 kW-plus rack densities. YTL Power’s NVIDIA GB200 Grace Blackwell deployment illustrates a shift toward exascale clusters that demand specialized power distribution and heat-dissipation designs.

In parallel, Software revenue remains anchored in AI frameworks and orchestration platforms that optimize distributed training. Services revenue grows steadily, fueled by managed operations and AI optimization consulting as enterprises seek performance tuning and energy efficiency.

By Tier Standard: Tier III Ascendancy Balances Cost and Resilience

Tier IV retained 61.63% market share in 2024, yet Tier III is scaling at 31.77% CAGR as operators prioritize cost efficiency. Malaysia AI data center market share for Tier III is expected to widen because AI applications often tolerate brief interruptions through checkpointing. AirTrunk’s 1.15 PUE JHB1 demonstrates how Tier III+ can achieve best-in-class efficiency without full Tier IV redundancy.

Developers continue to target Tier IV for sovereign or mission-critical applications in finance and healthcare. Nonetheless, rising capex and energy concerns are compelling many to adopt Tier III designs supplemented by distributed redundancy at network level.

By End-user Industry: Digital Media Outpaces IT and ITES Growth

IT and ITES controlled 33.82% of Malaysia AI data center market size in 2024, driven by continued software development and back-office outsourcing. Yet Internet and Digital Media exhibits 30.45% CAGR, reflecting demand for generative content, real-time streaming, and game rendering. Streaming companies leverage AI for recommendation engines and scene-level metadata generation, requiring low-latency inference. Malaysia’s position as a content-localization hub for Bahasa-speaking audiences underpins this expansion.

Concurrent growth in BFSI and Healthcare sustains baseline demand, while Telecom leverages AI for self-optimizing networks. Manufacturing uses predictive analytics for quality control, necessitating edge-linked GPUs. Government and Defense deployments emphasize data sovereignty, reinforcing domestic facility usage.

Geography Analysis

Johor led the Malaysia AI data center market in 2024, hosting 72 of 101 active sites and exceeding 1,600 MW IT capacity. Proximity to Singapore enables sub-5 ms cross-border latency, making Johor attractive for AI inference spill-over workloads. AirTrunk, Equinix, and the TM-Singtel JV each anchor large campuses in Iskandar Puteri, benefiting from dedicated submarine-cable landings that cut transit costs by 20-30%.

Klang Valley/Cyberjaya remains Malaysia’s historical technology corridor, combining mature fiber grids with federal incentives. Google’s USD 2 billion Elmina Business Park project and Vantage’s 256 MW Cyberjaya campus reaffirm its relevance. Grid-upgrade requirements, however, may limit rapid hyperscale expansion compared with Johor’s greenfield availability.

Penang’s semiconductor hub provides a niche cluster for AI-hardware testing and lower-cost colocation. Limited high-voltage capacity restrains hyperscaler scale, yet strong supply-chain ties support specialty workloads. East Malaysia’s Sarawak prospects rise with SEA-H2X cable landing and PPTEL’s Tier IV build, positioning the region as a future gateway for North Asia–Indonesia traffic. Expect secondary-market momentum as land and power scarcity in primary hubs pushes developers outward during 2025-2030.

Mordor Intelligence examines the artificial intelligence (ai) data center market across diverse other regional markets as well, including South America, Europe, and Asia, while also offering granular country-level perspectives for Singapore, Thailand, Chile, France, Australia, and Saudi Arabia and more.

Competitive Landscape

The Malaysia AI data center market features moderate concentration. Hyperscalers such as AWS, Google, Microsoft, and Oracle pursue self-builds while continuing to lease wholesale blocks, pressuring incumbent colocation pricing. Domestic champions TM Global and YTL Power leverage state relationships to fast-track approvals and renewable PPAs. International colos like Equinix and NTT add carrier-dense sites, amplifying interconnection competitiveness.

Strategic moves center on sustainability and high-density engineering. YTL’s 300-plus exaflops NVIDIA supercomputer flags Malaysia’s global-scale ambitions. AirTrunk pioneered direct-to-chip cooling, reducing energy use 23% at JHB. The TM-Singtel JV offers a cross-border platform, enabling load shifting to optimize cost and regulatory exposure.

White-space opportunities arise in GPU-as-a-Service, immersion-cooling consultancies, and carbon-offset trading tied to PPAs. As capex escalates, consolidation is likely, with resource-rich players absorbing smaller facilities that cannot afford liquid-cooling retrofits.

Malaysia Artificial Intelligence (AI) Optimised Data Center Industry Leaders

YTL Power International Berhad (YTL Data Center Park)

Keppel Data Centres Holdings Pte Ltd (Malaysia Ops)

Telekom Malaysia Berhad (Telekom Malaysia TM One)

NTT Global Data Centers Malaysia Sdn Bhd

Bridge Data Centres Malaysia Sdn Bhd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Wiwynn has partnered with Malaysia's YTL Group to develop a 600MW AI data center complex in Johor, with the first 100MW phase already operational. This collaboration marks Wiwynn's expansion into sovereign AI infrastructure, a growing segment driven by the need for localized data processing amidst geopolitical tensions. The project, co-developed with NVIDIA, will utilize advanced AI technologies, including NVIDIA's SuperPOD architecture, and represents a shift from traditional server manufacturing to full-scale AI cluster integration. Johor, a strategic hub for Southeast Asia's data center growth, now hosts over 20 operational centers, with YTL's site set to further enhance the region's access to cutting-edge AI capabilities.

- November 2024: VCI Global has secured a USD 30 million investment from Alumni Capital to develop its AI Computing Center (AICC) in Kuala Lumpur, Malaysia, which will house 512 Nvidia H200 Tensor Core GPUs. The first phase of the data center is expected to be completed by Q1 2025, aiming to serve global customers, particularly in Southeast Asia, and foster innovation in AI cloud computing.

- November 2024: TM Global announced 20 MW Phase 2 expansions at Klang Valley and Iskandar Puteri facilities, targeting Tier III and LEED Silver standards.

- September 2024: OMS Group committed USD 300 million to Project MIST subsea cable and quartet of landing stations across ASEAN.

Malaysia Artificial Intelligence (AI) Optimised Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

How big is Malaysia’s AI data center market today?

Malaysia AI data center market size reached USD 0.49 billion in 2025 and is on track for USD 1.76 billion by 2030 at a 29.03% CAGR.

Which segment is growing the fastest?

Colocation facilities are advancing at 31.23% CAGR through 2030 as enterprises embrace hybrid AI deployments that combine sovereign control with cloud connectivity.

Why is Johor attracting so many data centers?

Johor offers proximity to Singapore, 1,600 MW installed IT capacity, competitive land incentives, and submarine-cable landings that cut latency costs for cross-border AI workloads.

What technologies are driving new data center builds?

GPU-dense racks, direct-to-chip liquid cooling, on-site renewable PPAs, and 275 kV high-voltage grid tie-ins are central to AI-ready campus designs.

How are sustainability goals influencing the sector?

Malaysia’s 70% renewable-energy target and emerging PUE regulations are pushing operators toward solar PPAs, reclaimed-water cooling, and immersion or liquid-cooling systems to meet ESG requirements.

Page last updated on: