Singapore Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

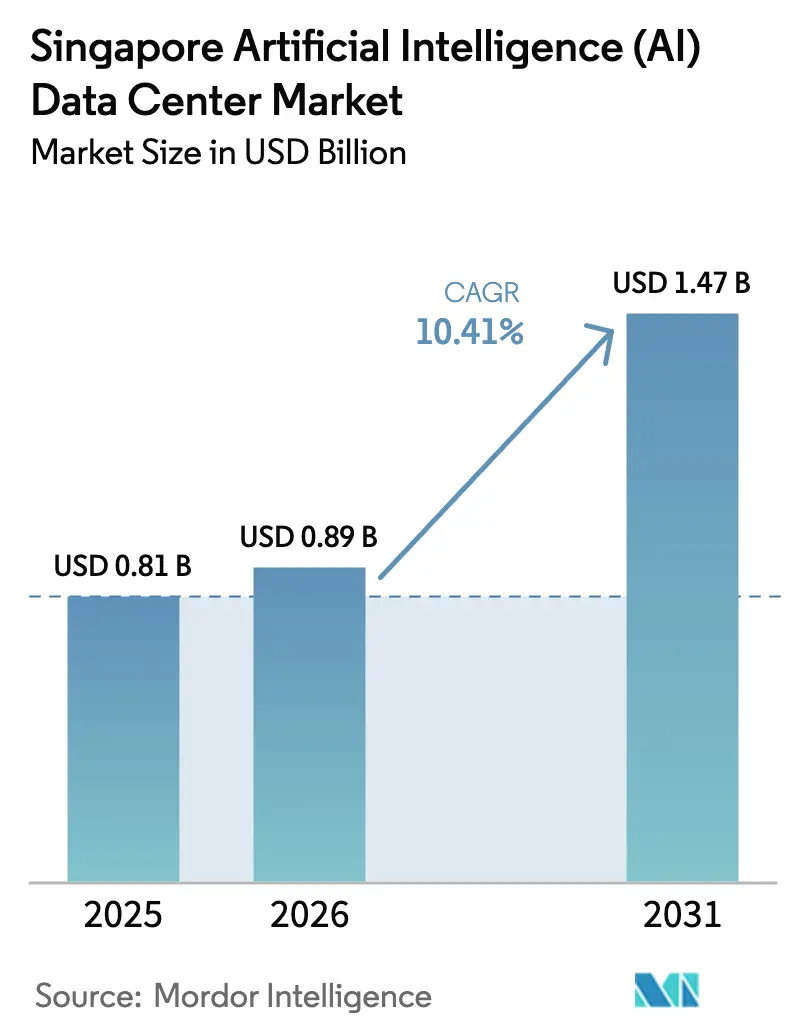

| Base Year Market Size (2025) | USD 0.81 Billion |

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.47 Billion |

| Growth Rate (2026 - 2031) | 10.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The Singapore artificial intelligence data center market size was valued at USD 0.81 billion in 2025 and estimated to grow from USD 0.89 billion in 2026 to reach USD 1.47 billion by 2031, at a CAGR of 10.41% during the forecast period (2026-2031). Strong demand for sovereign AI compute, a government-backed 300 MW power release, and sub-1% colocation vacancy rates underpin the expansion. Operators respond with liquid- and immersion-cooling retrofits that support power densities above 20 kW per rack, turning Singapore’s land scarcity into an innovation catalyst. Sustainability rules PUE ≤ 1.30 and WUE ≤ 2.0 reshape capital‐allocation decisions, linking new capacity approvals to demonstrable energy-efficiency gains. Cross-border campuses in Johor and Batam complement island facilities, allowing workloads to swing between low-latency Singapore cores and cost-optimized regional nodes.

Key Report Takeaways

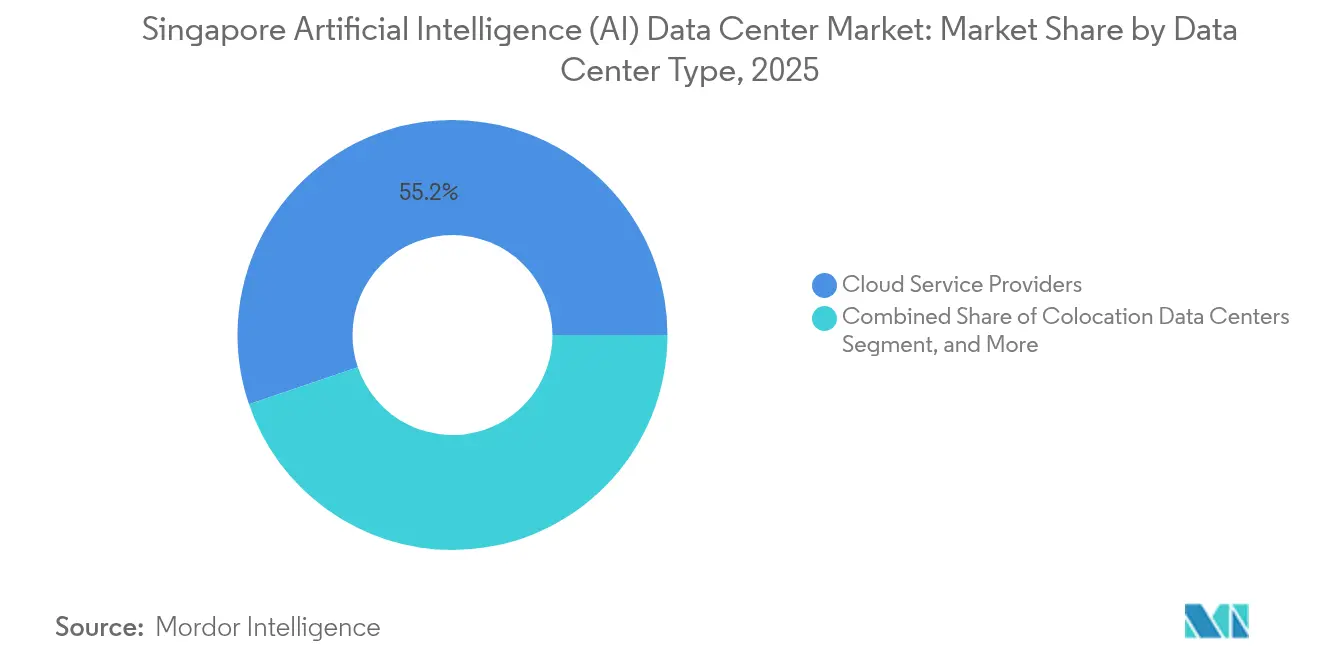

- By data center type, Cloud Service Providers led the Singapore artificial intelligence data center market with 55.22% of the market share in 2025, while Colocation Data Centers are forecasted to expand at a 11.78% CAGR through 2031.

- By component, Software accounted for 45.43% of the Singapore artificial intelligence data center market size in 2025, whereas Hardware is projected to grow at an 11.28% CAGR to 2031.

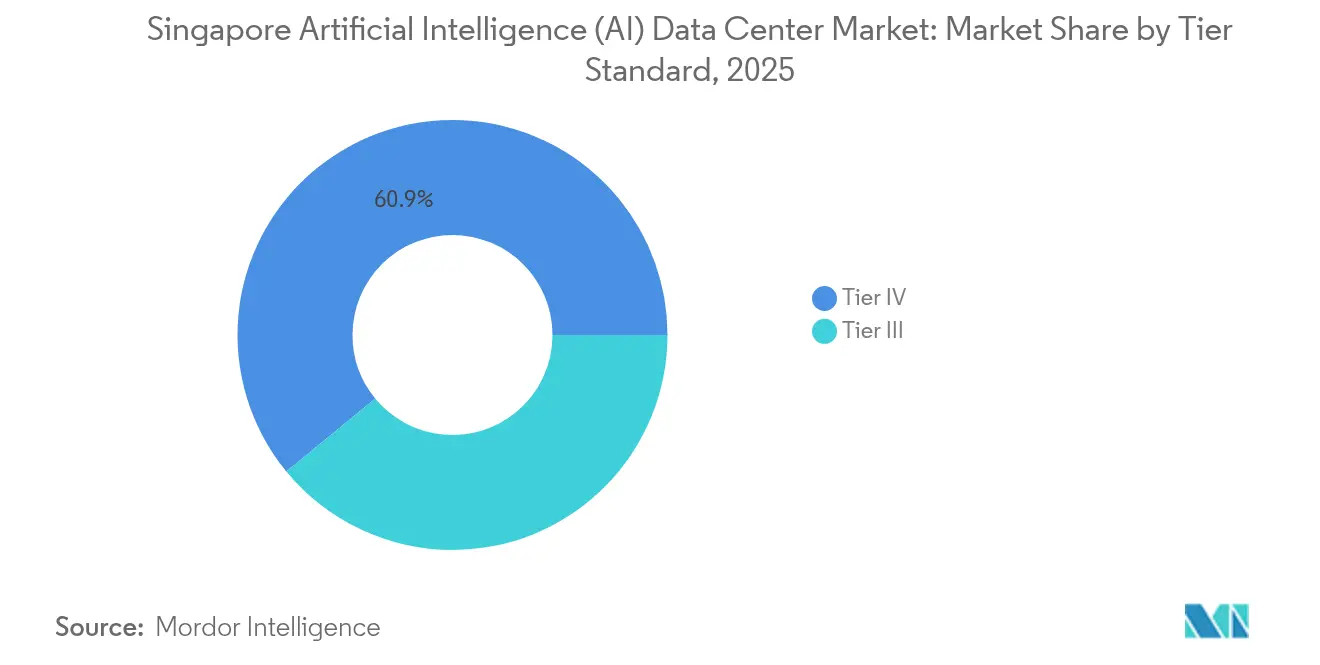

- By tier standard, Tier IV facilities held a 60.94% share of the Singapore artificial intelligence data center market size in 2025; Tier III is expected to register the highest CAGR at 12.21% over the same horizon.

- By end-user industry, IT and IT-enabled services captured 33.27% of the 2025 revenue of the Singapore artificial intelligence data center market, while the Internet and Digital Media segment is advancing at a 11.02% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Future direction is shaped by developments occurring across multiple countries and regions, with Singapore contributing to the overall trajectory. The outlook on worldwide artificial intelligence (ai) data center market reflects how these are expected to evolve collectively.

Singapore Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in AI-driven Power-Density Requirements | +2.8% | Singapore core, spillover to Johor-Batam | Medium term (2-4 years) |

| Exploding GPU Imports and Local AI Cloud Offerings | +2.1% | Singapore hub with regional distribution | Short term (≤ 2 years) |

| Government Green DC Roadmap and 300 MW Power Release | +1.9% | National, concentrated in Jurong West cluster | Medium term (2-4 years) |

| Regional Hub Status and Sub-1% Vacancy (Colocation) | +1.5% | Singapore core with cross-border arbitrage | Long term (≥ 4 years) |

| Liquid-/Immersion-Cooling Cost Break-throughs | +1.3% | Tropical Asia Pacific markets, Singapore leadership | Medium term (2-4 years) |

| Cross-Border Johor-Batam-SG "Tri-Hub" Campus Build-outs | +1.0% | Singapore-Malaysia-Indonesia corridor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in AI-driven Power-Density Requirements

AI workloads exceeding 20 kW per rack force a re-think of thermal design and electrical distribution. ST Engineering’s SGD 120 million Jalan Boon Lay project features proprietary secondary-loop liquid systems, ensuring a PUE of 1.25 even in 32 °C ambient temperatures.[1]ST Engineering, “ST Engineering Breaks Ground on Fourth Singapore Data Centre,” stengg.com Operators unable to retrofit legacy halls face stranded assets, leading to accelerated secondary market transactions that repurpose space for edge or disaster recovery functions. Rising rack densities also reshape rental economics, prompting a shift from per-square-foot to per-kilowatt pricing. Financiers view high-density designs as future-proof, channeling capital toward builders that can certify 30 kW-ready halls.

GPU Imports and Local AI Cloud Roll-outs

Preferential tariff regimes and free-trade zone logistics make Singapore the primary point of entry for GPU boards destined for ASEAN. Local cloud providers bundle those accelerators into GPU-as-a-Service offerings, reducing deployment lead times from months to days. System integrators colocate staging labs within tax-advantaged logistics parks, enabling on-site firmware flashing and burn-in before racks are shipped to production floors. The rapid fulfillment cycle appeals to start-ups and mid-caps that lack procurement muscle, stimulating demand spikes each quarter when new GPU SKUs are release. Hardware vendors reciprocate by allocating early-access inventory to Singapore operators that commit to regional showcase deployments.

Government Green DC Roadmap and 300 MW Power Release

The Infocomm Media Development Authority (IMDA) and the Energy Market Authority (EMA) allocated 300 MW of fresh DC power in 2024, contingent on operators meeting best-in-class efficiency benchmarks.[2]Infocomm Media Development Authority, “Pilot Data Centre Call for Application—Capacity Allocation Announcement,” imda.gov.sg An additional 200 MW remains in reserve for applicants who demonstrate the use of renewable-energy credits or district cooling. The roadmap effectively shifts the focus of competition from raw megawatt accumulation to achieving energy productivity. Facility blueprints now integrate 26 °C supply-air designs, hot-aisle enclosures, and on-site waste-heat reuse for district heating pilots. Established players with strong balance sheets absorb the higher capex, whereas smaller entrants gravitate toward joint ventures that pool sustainability expertise.

Regional Hub Status and Sub-1% Vacancy (Colocation)

Persistent vacancy below 1% keeps Singapore rack rates at a 35–50% premium over regional peers, yet enterprises accept the markup for latency-sensitive applications. Hyperscalers pre-lease entire halls two years before practical completion, crowding out short-cycle retail deals. The supply squeeze pushes second-tier workloads into Johor and Batam, giving rise to a two-station operating model where Singapore hosts master data sets and regional sites house replicas. Colocation landlords capitalize on the scarcity by upselling cross-connects, direct cloud on-ramps, and managed interconnection fabrics that stitch the tri-hub together.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land and Grid-Power Scarcity on the Island | -2.3% | Singapore core, driving cross-border expansion | Long term (≥ 4 years) |

| Stringent PUE ≤ 1.30 and WUE ≤ 2.0 Compliance Costs | -1.8% | National, affecting all new developments | Medium term (2-4 years) |

| Intensifying Cost Competition from Johor and Batam | -1.4% | Singapore-Malaysia-Indonesia corridor | Medium term (2-4 years) |

| Skilled AI/HPC Talent Shortage Drives Opex Up | -1.1% | Singapore core with regional talent competition | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Land and Grid-Power Scarcity on the Island

Only 728 km² of territory and finite substation capacity limit the development of additional greenfield sites. Prime industrial parcels routinely command SGD 2,000 per square meter, up 18% since 2024, compressing pro forma returns. Grid-connection queues stretch to 36 months, forcing developers to pursue gas turbine-based private networks as interim solutions. These bottlenecks channel growth into multi-story designs and out-of-country satellite campuses. Firms cultivating energy arbitrage agreements with Malaysia’s TNB or Indonesia’s PLN gain a decisive lead in meeting near-term capacity requests.

Stringent PUE ≤ 1.30 and WUE ≤ 2.0 Compliance Costs

Singapore Green Building Council’s Green Mark 2024 framework compels operators to budget 15–20% extra capex for advanced thermal controls and gray-water recycling.[3]Singapore Green Building Council, “Green Mark 2024 for Data Centres,” sgbc.sg Achieving WUE targets in humid climates encourages builders to adopt closed-loop adiabatic systems, which often carry premium maintenance contracts. Smaller providers struggle to secure project financing without green-bond qualification, effectively tightening market entry. Over time, however, the energy-cost savings partially offset the higher build price, rewarding early adopters with lower operating expense profiles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Cloud Dominance Drives Colocation Growth

Cloud Service Providers held 55.22% of the Singapore artificial intelligence data center market share in 2025, benefiting from more than USD 14 billion in hyperscale investment aligned with the city-state’s digital gateway role. Their footprint anchors multi-tenant ecosystems that funnel enterprise traffic through dedicated on-ramps and content-delivery nodes. The segment’s growth, however, converges toward single-digit rates as land-power constraints bite. Enterprises seeking regulatory control and predictable costs pivot toward carrier-neutral colocation, spurring a 11.78% CAGR that outpaces overall market momentum and reallocates white-space mix toward wholesale suites.

Hybrid cloud architectures dominate procurement dialogues: local banks maintain Tier IV vaults for customer data, burst into the public cloud for non-sensitive computing, and pivot to Johor or Batam for budget-sensitive AI training. Colocation landlords enhance their value propositions with modular, powered-shell expansions that guarantee delivery within six months, outpacing hyperscaler cycle times. Edge-oriented micro-sites appear near 5G aggregation hubs, serving AR/VR and autonomous vehicle tests that cannot tolerate backhaul jitter. The resulting lattice of core, near-edge, and cross-border nodes sustains workload distribution flexibility, a key selling point as AI application patterns evolve.

By Component: Hardware Acceleration Challenges Software Leadership

Software solutions spanning machine-learning platforms, optimized containers, and orchestration stacks commanded 45.43% share of the Singapore artificial intelligence data center market size in 2025, reflecting the city’s deep pool of developers and start-ups serving multilingual ASEAN audiences. Licensing revenue is sticky, underwritten by long-term contracts from financial, healthcare, and public-sector clients that prize on-prem inference. Yet hardware outstrips software in incremental growth, clocking an 11.28% CAGR as liquid-cooling certifications spur mass GPU deployments.

STT GDC’s March 2025 enrollment in NVIDIA’s DGX-Ready program validates in-rack liquid heat-exchangers and positions the operator for premium AI cluster hosting. Switchgear vendors bundle full-stack solutions that combine 415 V busways, rear-door heat exchangers, and immersion baths, addressing Singapore’s humidity challenges without derating. Power and cooling infrastructure spending scales in tandem, as transformers, UPS modules, and harmonic filters upgrade to handle fluctuating AI load profiles. Managed services providers capture recurring revenue by optimizing GPU cluster utilization, driving a service-layer CAGR that parallels hardware adoption.

By Tier Standard: Tier IV Resilience Meets Tier III Efficiency

Tier IV halls controlled 60.94% of installed IT power in 2025, catering to finance and government workloads that mandate 99.995% availability and concurrent maintainability. Triple-feed power rooms, 2 N+1 mechanical redundancy, and on-site fuel reserves typify the architecture. That resilience adds 30–40% capex and 15% higher opex compared with Tier III equivalents, prompting cost-sensitive AI tenants to accept slightly lower SLA tiers. Consequently, Tier III capacity grows at a 12.21% CAGR, gradually eroding the dominance of fault-tolerant builds.

Technological convergence narrows the practical reliability gap: advanced battery-energy-storage systems provide instantaneous ride-through, while software-defined power automates load shedding during utility disturbances. Equinix’s SG6, classified as Tier III, integrates rear-door liquid heat exchangers and on-site solar PPAs to meet both sustainability and uptime obligations. Operators highlight predictive-maintenance analytics and AI-driven incident response as intangible layers that compensate for reductions in mechanical redundancy. This shift reframes the resilience conversation from hardware-centric to software-augmented reliability.

By End-user Industry: IT Leadership Faces Digital-Media Challenge

IT and IT-Enabled Services absorbed 33.27% of demand in 2025, relying on Singapore’s multilingual workforce and pro-business policies to export SaaS across ASEAN. Large system integrators house DevSecOps pipelines in-country to satisfy banking data-residency rules, then deploy finished applications through regional edge nodes. Digital media providers, however, exhibit the fastest trajectory, with an 11.02% CAGR, as video-on-demand, cloud gaming, and short-form content consumption increase across Indonesia, Vietnam, and the Philippines.

Streaming platforms localize encoding farms in Singapore for rights management and near-origin caching, while offloading archival libraries to Johor for cost containment. Telecom operators monetize 5G slices by colocating MEC nodes inside Tier III sites, bundling them with GPU inference for real-time language translation and immersive sports feeds. BFSI institutions continue to explore private LLMs, anchoring secure enclaves within Tier IV vaults to align with the Cybersecurity (Amendment) Act 2024 requirements. Healthcare providers pilot federated learning schemes that maintain patient confidentiality while accessing pooled model improvements, further diversifying end-user demand profiles.

Geography Analysis

Singapore has more than 70 data centers, totaling 1.4 GW, which account for 7% of the nation's electricity consumption and 82% of ICT sector emissions. The government couches the 300 MW release within an efficiency mandate, effectively converting sustainability into a competitive moating mechanism. Operators with proven liquid-cooling track records secure earlier access to the limited-power pool, allowing them to command premium rack rates on launch.

Cross-border expansion reshapes geographic economics. AirTrunk’s 150 MW Johor campus and Nxera’s 64 MW Iskandar Puteri build achieve land cost savings upwards of 60%, yet maintain sub-10 ms latency to Singapore’s CBD. Submarine fiber pairs ring the corridor, underpinning active-active designs where real-time inference sits on-island while GPU training migrates offshore. Princeton Digital Group’s USD 5 billion regional program underscores the financing advantage that Singapore-headquartered entities wield in capital markets.

The resulting topology casts Singapore as the orchestration control plane that governs disaggregated compute spread across ASEAN. IMDA initiatives to harmonize data-classification norms with Malaysia’s MCMC and Indonesia’s KOMINFO lower regulatory friction in hybrid workload placement. As regional peers ramp up indigenous capacity, Singaporean operators differentiate themselves through compliance services, inter-platform latency SLAs, and multi-cloud access marketplaces. This strategic posture maintains the island’s role as a digital gateway, even as the raw megawatt share gradually diminishes.

Analysis of the artificial intelligence (ai) data center market by Mordor Intelligence spans multiple other regional evaluations across Asia, Middle East and Africa, and North America, supported by country-level insights for Australia, India, United Arab Emirates, Canada, Saudi Arabia, and Mexico, wherein local market conditions keep varying from one country to another.

Competitive Landscape

High capital intensity, scarce land, and demanding regulations result in a moderately concentrated field, where the top five operators collectively control approximately 68% of the installed IT power. STT GDC, Equinix, Digital Realty, Singtel’s Nxera, and Keppel DC REIT dominate new-build allocations. Competition centers on sustainability credentials and cross-border partnerships rather than price alone. STT GDC closed a SGD 1.75 billion funding round led by KKR in June 2024, earmarking the proceeds for GPU-ready expansions and renewable energy procurement.

Equinix partnered with the National University of Singapore in February 2025 to open a USD 4 million Co-Innovation Facility that prototypes cooling solutions for tropical climates. The initiative positions Equinix as a technology thought leader and secures early-mover insights into the adoption curves of liquid immersion. Princeton Digital Group leverages a regional land-banking strategy, acquiring Singapore’s SG3 asset from Yahoo and adjacent plots in Johor to provide contiguous 200 MW corridors.

Regulatory evolution shapes competitive moats: The Cybersecurity (Amendment) Act 2024 labels data centers as “foundational digital infrastructure,” subjecting operators to periodic cyber-resilience audits. Providers with ISO 22301, PCI-DSS, and MAS-TRM compliance histories convert that governance overhead into a sales advantage, particularly with finance, healthcare, and public-sector tenants. Smaller entrants focus on niche plays, such as edge micro-pods or AI model tuning services, to avoid head-to-head battles with incumbents.

Singapore Artificial Intelligence (AI) Data Center Industry Leaders

ST Telemedia Global Data Centres Ltd.

Equinix, Inc.

Digital Realty Trust, Inc.

Keppel DC REIT Management Pte. Ltd.

AirTrunk Operating Pte. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: STT GDC achieved NVIDIA DGX-Ready Data Center Program certification, unlocking premium AI workload hosting opportunities.

- February 2025: Equinix and the National University of Singapore have launched a USD 4 million Co-Innovation Facility at the upcoming SG6 site to develop sustainable cooling solutions.

- November 2024: Equinix broke ground on SG6 with an initial USD 260 million investment, featuring liquid cooling and renewable-energy PPAs with Sembcorp Industries.

- October 2024: GDS International secured a 39,978 m² plot at Jalan Buroh for its maiden Singapore facility, which is slated for operation in Q4 2026.

Singapore Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and IT-Enabled Services |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and IT-Enabled Services | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

How large is the Singapore artificial intelligence data center market in 2026?

The market stands at USD 0.89 billion in 2026 and is tracking toward USD 1.47 billion by 2031.

What is driving new capacity approvals on the island?

IMDA’s 300 MW power release ties allocations to strict PUE ≤ 1.30 and WUE ≤ 2.0 targets, making energy efficiency the key gatekeeper.

Which data center type is growing fastest?

Colocation facilities are expanding at a 11.78% CAGR as enterprises seek sovereign AI compute without hyperscaler lock-in.

How are operators coping with land scarcity?

They adopt multi-story high-density designs in Singapore and build satellite campuses in Johor and Batam to balance cost and latency.

Why are Tier III builds gaining traction?

Advances in liquid cooling and software-defined power narrow reliability gaps, offering 30–40% lower capex compared with Tier IV halls.

Which end-user segment is forecast to surge?

Internet and Digital Media workloads lead growth at an 11.02% CAGR on the back of streaming, gaming, and social media demand.

Page last updated on: