India Artificial Intelligence (AI) Optimised Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

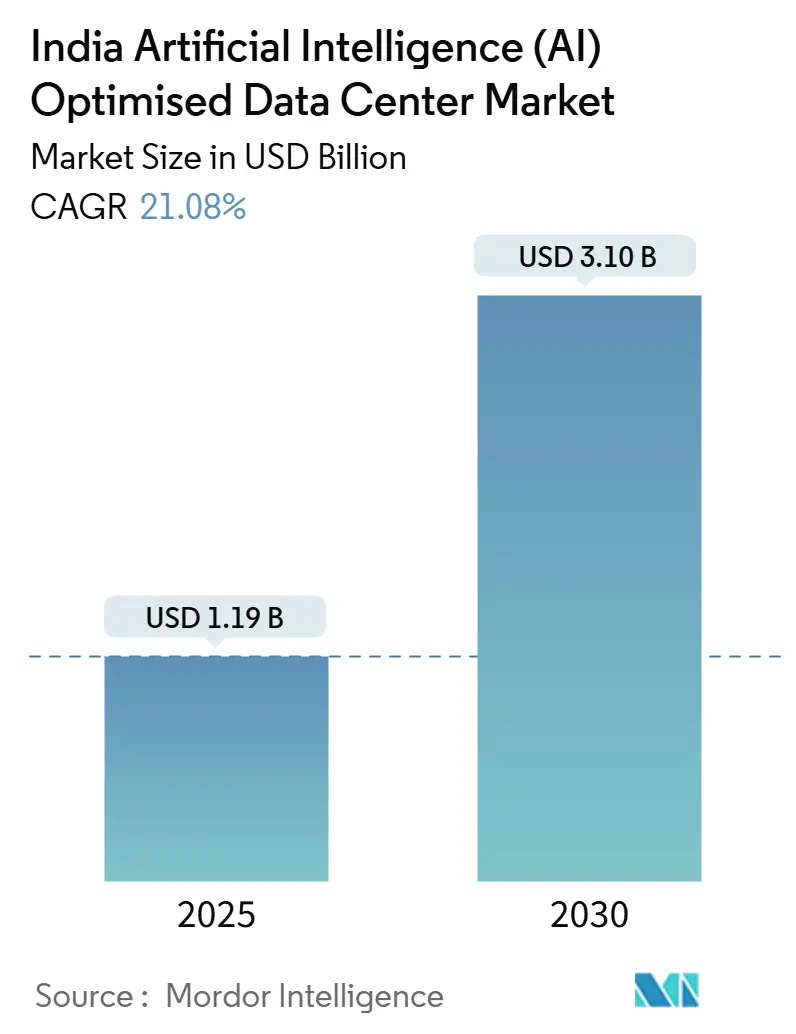

| Market Size (2025) | USD 1.19 Billion |

| Market Size (2030) | USD 3.10 Billion |

| Growth Rate (2025 - 2030) | 21.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Artificial Intelligence (AI) Optimised Data Center Market Analysis by Mordor Intelligence

The India artificial intelligence data center market size is valued at USD 1.19 billion in 2025 and is projected to reach USD 3.10 billion by 2030, reflecting a 21.08% CAGR. Energy-efficient AI hardware demand, mandatory data-localization, and hyperscale region roll-outs along the Mumbai-Bangalore corridor are accelerating capital expenditure in next-generation facilities that routinely draw 30 kW or more per rack. Enterprises increasingly treat sovereign data processing as a strategic capability rather than a cost center, and this mindset fuels sustained outlays on Tier IV sites backed by renewable-rich power purchase agreements. Competitive intensity is highest where submarine cable connectivity, cloud availability zones, and state incentives intersect, prompting aggressive land banking by both global hyperscalers and domestic colocation specialists. The India artificial intelligence data center market continues to benefit from inter-related policy initiatives such as the IndiaAI Mission, Production Linked Incentive scheme, and National 5G/6G Mission, each of which pushes AI workloads deeper into enterprise and public-sector operations.

Key Report Takeaways

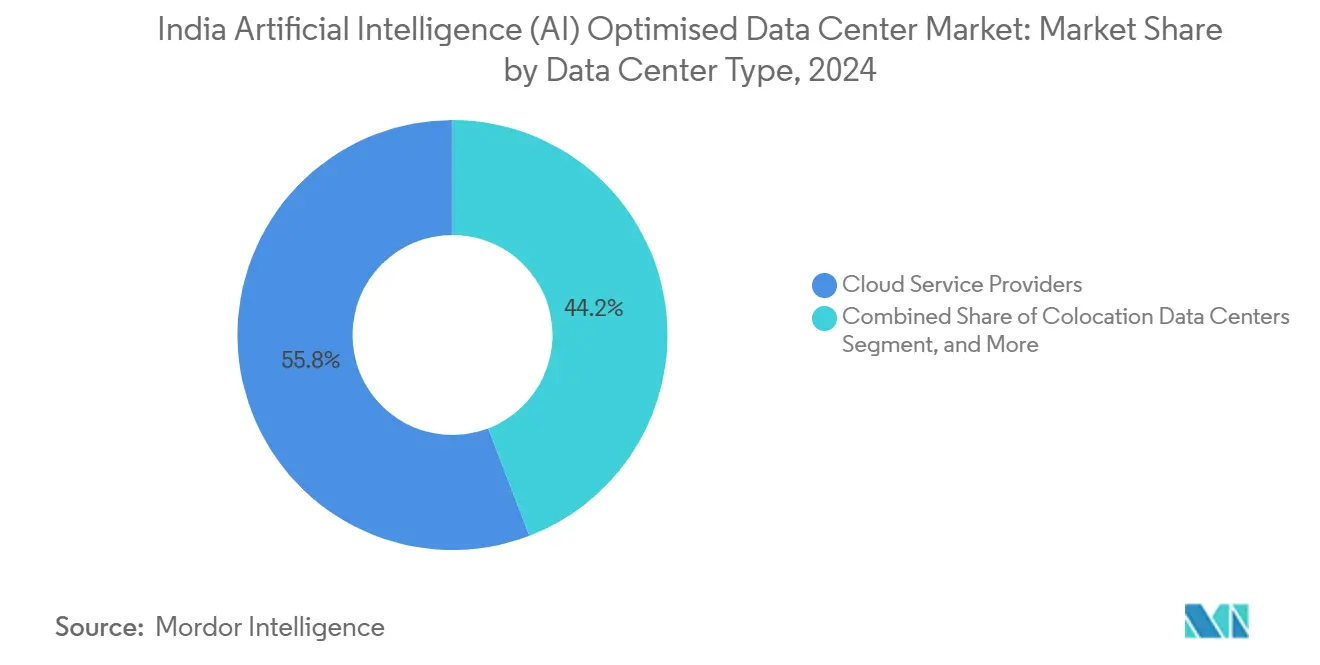

- By data center type, cloud service providers led with 55.82% revenue share in 2024 in the India artificial intelligence data center market, while colocation facilities are projected to expand at a 22.67% CAGR through 2030.

- By component, software maintained 45.83% share of the India artificial intelligence data center market size in 2024, whereas hardware investment is advancing at a 22.23% CAGR to 2030.

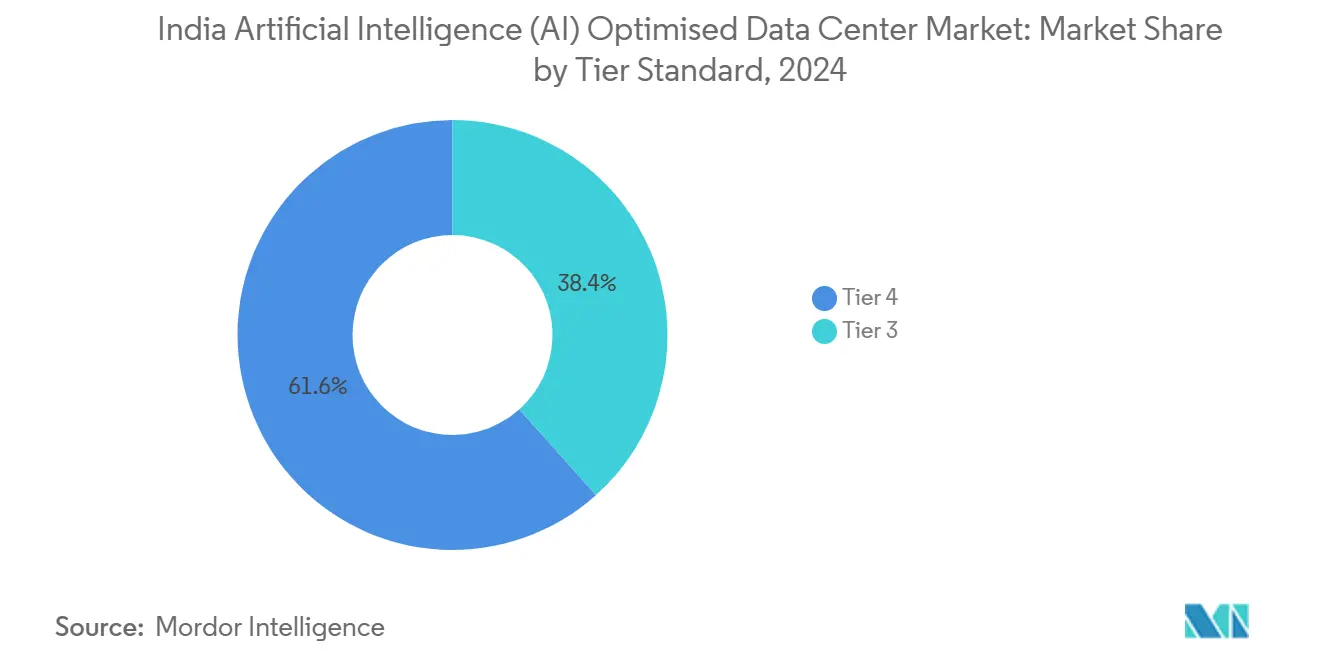

- By tier standard, Tier IV sites accounted for 61.63% of the India artificial intelligence data center market share in 2024, yet Tier III deployments exhibit the highest 23.44% CAGR through 2030.

- By end-user industry, IT and ITES held 33.82% share in 2024 in the India artificial intelligence data center market, while internet and digital media workloads are rising at a 22.45% CAGR to 2030.

Companies active in India may frequently operate across several geographies, linking regional presence to global strategy. Mordor Intelligence captures the entire market landscape of the global artificial intelligence (ai) data center industry and how these positions are distributed.

India Artificial Intelligence (AI) Optimised Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid hyperscale cloud-region roll-outs along Mumbai-Bangalore corridors | +4.2% | Mumbai, Bangalore, Pune, Chennai | Medium term (2-4 years) |

| Mandatory data-localisation under Digital Personal Data Protection Act | +3.8% | National, concentrated in Tier-1 metros | Short term (≤ 2 years) |

| National 5G/6G mission creating edge-AI inference demand across 28 states | +3.1% | National, early gains in Delhi, Mumbai, Bangalore | Medium term (2-4 years) |

| Abundant solar and wind PPAs in Rajasthan and Karnataka enabling low-carbon GPU farms | +2.9% | Rajasthan, Karnataka, Tamil Nadu | Long term (≥ 4 years) |

| Government incentives (PLI, Data-Centre Policy) slashing capex for liquid-cooled AI halls | +2.7% | National, priority in designated zones | Short term (≤ 2 years) |

| Semiconductor and AI-chip fabrication push spurring heterogeneous compute racks | +1.9% | Gujarat, Karnataka, Assam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyperscale Infrastructure Expansion Drives Market Acceleration

Mumbai-Bangalore has emerged as the nation’s AI backbone because fiber proximity, cloud region density, and readily accessible solar-wind PPAs converge inside a 1,200 km stretch. Microsoft earmarked USD 3.7 billion through 2025 for three Azure regions equipped with advanced GPU clusters tailored to generative models.[1]Microsoft News Center India, “Microsoft Announces Comprehensive AI Skilling Initiative and Major Infrastructure Investments,” news.microsoft.com Amazon followed by extending Local Zones into eight cities, giving developers low-latency ingress to model-training pipelines that cannot tolerate more than 10 milliseconds delay. Those roll-outs generate follow-on demand for the India artificial intelligence data center market as colocation firms such as NTT and STT deploy adjacent halls to capture spillover capacity. The corridor’s clustering effect reinforces landlord pricing power, and yet secondary metros imitate the template, illustrating how hyperscale moves set the pace for supporting providers.

Data Sovereignty Mandates Reshape Infrastructure Investment Patterns

The Digital Personal Data Protection Act 2023 compels sensitive personal-data processing to remain on sovereign soil, turning compliance into a non-negotiable siting criterion.[2]Ministry of Electronics and Information Technology, “Digital Personal Data Protection Act 2023,” meity.gov.in Global banks, insurers, and health-tech firms expand domestic AI racks even during macro-economic slowdowns because offshoring is no longer an option. The India artificial intelligence data center market thus enjoys an insulation against external headwinds uncommon in many emerging technology segments. Legal certainty around localization also eases project-finance underwriting, letting operators raise multi-tranche debt at lower coupons on the expectation that AI capacity utilization will stay above 85% for regulated sectors.

Edge Computing Proliferation Expands Geographic Footprint

5G densification under the National 5G/6G Mission enables real-time AI experiences that cannot afford round-trip latency to Tier-1 metros.[3]Department of Telecommunications, “National Broadband Mission,” dot.gov.in Telecom majors Reliance Jio and Bharti Airtel are commissioning 100-500 rack edge nodes in Tier-2 cities such as Jaipur, Lucknow, and Coimbatore, aiming to keep inference close to end users for autonomous mobility pilots and Industry 4.0 use cases. This pivot increases the total addressable rack count well beyond traditional metro limits and lifts the India artificial intelligence data center market penetration among small-to-mid enterprises that previously lacked local AI services.

Renewable Energy Integration Enables Sustainable AI Computing

GPU farms can draw 50 MW or more, and operators increasingly bundle green PPAs to mitigate both cost and carbon intensity. Karnataka’s 13 GW renewable base and Rajasthan’s wind-solar hybrids allow AI halls to promise sub-0.2 kg CO₂/kWh footprints, meeting hyperscalers’ Scope 3 reduction targets.[4]Karnataka Renewable Energy Development Limited, “Renewable Energy Capacity and Projects,” kredl.karnataka.gov.in Adani’s USD 4 billion portfolio in these states showcases how integrated utility ownership and immersion cooling can reduce lifetime energy expenditure by up to 30% versus grid-only peers. The sustainability differentiator is now a sales prerequisite, meaning renewable leaders enjoy higher pre-leasing velocity than fossil-dependent rivals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion in Mumbai-Pune and NCR limiting new power connections | -2.1% | Mumbai, Pune, Delhi, Gurgaon, Noida | Short term (≤ 2 years) |

| Land-acquisition delays and zoning hurdles in Tier-1 metros | -1.8% | Mumbai, Delhi, Bangalore, Chennai | Medium term (2-4 years) |

| High import duties on advanced immersion-cooling fluids and hardware | -1.3% | National | Short term (≤ 2 years) |

| Shortage of certified thermal-management talent for above 30 kW/rack designs | -1.1% | National metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Power Grid Constraints Limit Metro Expansion Capacity

Maharashtra’s distribution utility reports 18-24-month lead times for new connections topping 10 MW, effectively pausing fresh approvals for GPU-dense sites in Mumbai and Pune. AI halls need 15-30 kW per rack, sextuple the draw of legacy clouds, inflating the transformer and feeder requirements that utilities struggle to accommodate. In the interim, developers redirect capex toward Hyderabad-Chennai where reserve margins and open-access renewables remain available, but they forgo the immediate ecosystem benefits of Tier-1 metros.

Regulatory and Zoning Complexities Slow Development Timelines

Securing 50-acre contiguous parcels inside Coastal Regulation Zones near Mumbai can extend project timetables to 48 months, raising interest-during-construction costs by double digits. The India artificial intelligence data center market therefore rewards incumbents with government-relations acumen and brownfield inventories, while new entrants confront a steeper curve. Zoning delays compel some hyperscalers to pivot toward multi-story vertical campuses that fit within urban parcels yet incur higher per-rack build costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation Surge Challenges Cloud Dominance

Cloud providers controlled 55.82% of the India artificial intelligence data center market in 2024, but colocation revenue is compounding at 22.67% CAGR, a pace that compresses the gap annually. Financial institutions, healthcare systems, and SaaS vendors pursue hybrid topologies, keeping mission-critical AI models in dedicated cages while bursting to cloud for episodic training, to balance compliance and flexibility. CtrlS, Yotta, and NTT pre-install liquid-cooling manifolds, direct cross-connects, and GPU-as-a-Service catalogs that let tenants spin specialized clusters inside 24 hours. This one-stop convenience underpins price premiums as high as 18% relative to generic wholesale space.

Second-order effects cascade through supply chains: more pre-fabricated modular halls ship to India than any other APAC country except China, reflecting operators’ need for speed. Colocation’s ascent also redistributes bargaining power toward enterprises able to negotiate energy pass-through contracts and renewable matching. As these trends mature, the India artificial intelligence data center market records an uptick in three-party joint ventures where landowners, infrastructure funds, and colocation specialists divide risk pools, a model likely to accelerate beyond 2027.

By Component: Hardware Investment Accelerates Despite Software Leadership

Software platforms held 45.83% share in 2024, sustained by revenue from orchestration, monitoring, and AI-operations stacks licensed on per-core metrics. Yet hardware outlays are climbing 22.23% CAGR as every incremental teraflop requires denser racks, advanced PDUs, and liquid-to-chip heat exchangers. Power infrastructure lines alone, UPS, switchgear, busways, now represent 22-25% of total shell-and-core budgets for GPU halls, compared with 12% five years earlier. Immersion cooling fluid import duties raise capex by 8-10%, but operators reclaim the delta via lower energy spend, quick payback periods of 18-24 months, and ESG-linked financing at preferential coupons.

Services revenue rises in tandem because few domestic enterprises maintain in-house AI ops skills. Managed service firms bundle model optimization, inference scripting, and auto-scaling policies, taking over tasks traditionally assigned to DevOps teams. The India artificial intelligence data center market thus nurtures a vibrant ecosystem of integrators and specialists that monetize the complexity gap between older air-cooled estates and next-generation liquid systems.

By Tier Standard: Edge Computing Drives Tier III Acceleration

Tier IV dominated with 61.63% share in 2024, reflecting BFSI and healthcare’s zero-tolerance stance on downtime. Nevertheless, Tier III racks are set to grow 23.44% CAGR because distributed edge nodes often accept 99.982% availability when weighed against 25-30% capex savings. Telecom operators outfit micro-facilities near 5G base-stations to crunch computer-vision workloads for smart-factory clients. Retail chains adopt Tier III for in-store recommendation engines that lose minimal revenue if offline for a few minutes yearly.

These dynamics split investment lanes: large campuses near landing stations preserve Tier IV standards for national-scale AI model training, whereas Tier III nodes proliferate along highways, industrial parks, and campuses to localize inference. Over time, multi-tier portfolios will characterize the India artificial intelligence data center market, mirroring how cloud players deploy both region cores and edge POPs.

By End-user Industry: Digital Media Transformation Accelerates Adoption

IT and ITES users commanded 33.82% share in 2024, but Digital Media workloads are rising 22.45% CAGR as streaming platforms, gaming publishers, and social networks chase personalized engagement. Video transcoding pipelines shift to AI-assisted compression, multiplying compute-hour consumption. Generative engines produce localized clips, thumbnails, and even dialogue dubs, escalating GPU leasing. BFSI keeps adding racks for fraud models and real-time credit underwriting, while Healthcare invests in multi-modal diagnostic algorithms that fuse radiology, genomics, and EHRs.

Industrial IoT joins the fray as automotive, textile, and pharma plants retrofit high-bandwidth sensors. Predictive maintenance AI reduces unscheduled downtime by up to 40%, a saving that offsets colocation premiums in under 18 months. Government programs, smart cities, traffic analytics, and crowd-management, bundle public-private procurement, ensuring further diversification of the India artificial intelligence data center market revenue streams.

Geography Analysis

Mumbai-Bangalore accounts for roughly 65% of operational AI megawatts today, owing to dual submarine cable gateways, entrenched developer clusters, and renewable open-access schemes that price solar-wind hybrids at INR 3.1–3.3 per kWh (USD 0.037–0.039 per kWh). Financial services anchor Mumbai’s rack absorption, whereas Bangalore captures SaaS, gaming, and AI research tenants that value proximity to India’s largest tech talent pool. Microsoft’s additional USD 1.2 billion pledge in January 2025 underscores confidence in the corridor’s network and policy stability.

NCR holds 18% share despite grid congestion. Ministries insist on local data processing for e-governance, identity, and defense workloads, compelling developers to pursue creative solutions such as direct-current micro-grids and in-building fuel cells to bypass feeder limitations. Satellite towns, Greater Noida, Manesar, offer cheaper land and fewer zoning hurdles, marginally shifting heat maps while preserving Delhi adjacency for policy liaison.

Hyderabad-Chennai and Pune-Ahmedabad corridors surge at 25–30% CAGR as land price elasticity and renewable add-on clauses entice green-field entrants. Hyderabad’s pharma heartlands demand AI for molecule screening; Chennai’s auto OEMs digitalize factories; Pune’s engineering firms adopt edge analytics. Each geography also benefits from dedicated fiber spurs into submarine landing stations, narrowing bandwidth cost gaps with Mumbai.

The artificial intelligence (ai) data center market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Middle East and Africa, North America, and South America, along with detailed country-level analysis for Japan, Malaysia, South Africa, Canada, Chile, and France.

Competitive Landscape

The top five operators, Microsoft, Amazon, Google, NTT, and STT, together control near-45% capacity, giving the India artificial intelligence data center market a moderate consolidation profile. Hyperscalers differentiate via custom AI accelerators (e.g., AWS Trainium, Google TPU) embedded into IaaS offerings, whereas domestic specialists emphasize sovereign hosting and enterprise hand-holding. Reliance Jio teams with NVIDIA for a 10,000-GPU supercomputer to seed India-language LLMs, leveraging telco fiber and consumer data reservoirs.

STT and CtrlS upgrade existing halls with rear-door heat exchangers and immersion pods to compete on PUE and rack density metrics without incurring green-field delays. Adani leverages its utility portfolio, offering “renewables-as-a-service” bundles alongside colocation whitespace to attract ESG-driven tenants. Telecom operators, once bandwidth vendors, now bundle edge nodes, content delivery, and AI acceleration, expanding the addressable share of wallet. The landscape is fluid; new chip-fabrication incentives may give vertically integrated conglomerates such as the Tata Group an advantage in supplying AI modules domestically, reducing import friction.

A vibrant vendor ecosystem of thermal-management, power electronics, and modular-construction suppliers thrives under this competitive churn. Schneider Electric, Vertiv, and Siemens localize manufacturing lines to skip import duties, aligning with PLI credits and offering rapid shipment lead times.

India Artificial Intelligence (AI) Optimised Data Center Industry Leaders

NTT GDC India

STT GDC India

CtrlS Datacenters Ltd.

Yotta Infrastructure Solutions LLP

Nxtra Data Limited (Bharti Airtel)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: India’s first AI data center park is being developed in Sector-22, Nava Raipur, by RackBank Datacenters Pvt Ltd. The project spans 5.5 hectares and includes a 2.7-hectare Special Economic Zone. It will feature GPU-based high-end computing infrastructure, starting with a 5 MW capacity in its first phase, scalable up to 150 MW. With an investment of ₹2,000 crore, the initiative is expected to generate 500 direct and 1,500 indirect jobs, prioritizing local employment. The park will integrate advanced systems such as GPU computing, AI workflows, data processing, and broadcast-level streaming, setting a benchmark in India’s digital infrastructure.

- January 2025: Microsoft announced plans to invest USD 3 billion in cloud and AI infrastructure in India, including the establishment of new data centers. This investment highlights the growing demand for AI processing capabilities and is expected to strengthen India's AI ecosystem, positioning the country as a key player in the global AI market.

- December 2024: Adani Group completed the first phase of its USD 4 billion data center investment plan with the inauguration of a 50 MW AI-optimized facility in Karnataka powered entirely by solar energy, featuring immersion cooling technology for GPU-dense deployments.

- November 2024: Amazon Web Services launched four new Local Zones across Chennai, Hyderabad, Kolkata, and Pune to support edge AI applications, representing a USD 800 million infrastructure expansion targeting sub-10 millisecond latency requirements.

India Artificial Intelligence (AI) Optimised Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITeS |

| Internet and Digital Media |

| Telecom Operators |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITeS | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

What is the current valuation of the India artificial intelligence data center market?

The market stands at USD 1.19 billion in 2025, with projections indicating USD 3.10 billion by 2030.

How fast is the India artificial intelligence data center market expected to grow?

Revenue is forecast to increase at a 21.08% CAGR between 2025 and 2030, driven by data localization mandates and hyperscale cloud expansions.

Which data center type is growing the fastest?

Colocation facilities are expanding at a 22.67% CAGR, outpacing cloud region growth as enterprises pursue hybrid AI deployments.

Why are Tier III sites gaining traction despite Tier IV dominance?

Tier III solutions offer cost advantages of up to 30% and sufficient 99.982% uptime for distributed edge AI workloads, supporting a 23.44% CAGR.

Which end-user verticals are driving new demand?

Internet and Digital Media companies are leading with a 22.45% CAGR, followed by BFSI and Healthcare adopting AI for compliance and diagnostic needs.

Page last updated on: