Asia-Pacific Artificial Intelligence (AI) Optimised Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

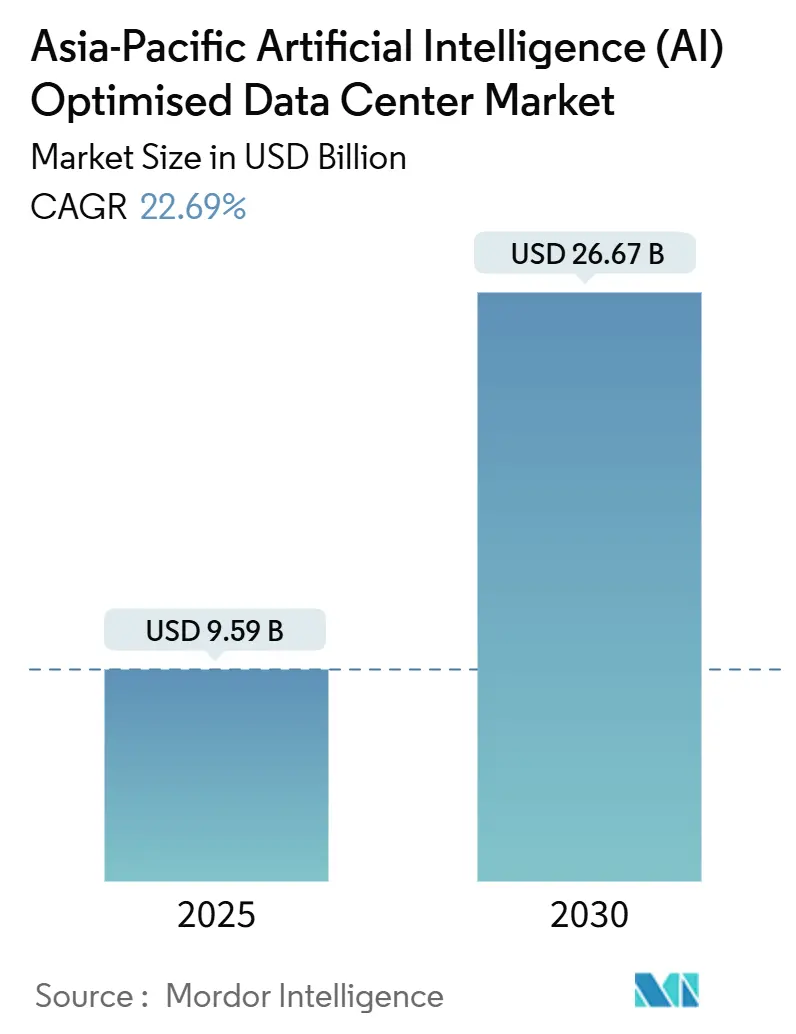

| Market Size (2025) | USD 9.59 Billion |

| Market Size (2030) | USD 26.67 Billion |

| Growth Rate (2025 - 2030) | 22.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Artificial Intelligence (AI) Optimised Data Center Market Analysis by Mordor Intelligence

The Asia-Pacific artificial intelligence data center market is valued at USD 9.59 billion in 2025 and, at a 22.69% CAGR, is forecast to reach USD 26.67 billion by 2030, underscoring the strongest five-year expansion yet seen in regional digital infrastructure spending. Hyperscale cloud operators continue to anchor demand, but sovereign-AI legislation, export-control uncertainty, and the heat-density jump tied to generative-AI workloads are redefining site location, cooling choices, and power procurement strategies. Over the next five years, liquid-cooling retrofits are expected to outpace new air-cooled halls, while colocation pre-leasing terms lengthen as banks and public-sector agencies race to secure domestic GPU capacity. Regional power-purchase agreements increasingly attach renewable-energy guarantees to hedge transformer shortfalls in Tier-2 Indian cities, and talent premiums for AI-qualified infrastructure engineers remain 35–50% above legacy roles, cementing labor availability as a board-level risk factor. As a result, operators that can pair sovereign-cloud certifications with advanced cooling and dedicated megawatt blocks stand to gain the largest share of the next growth wave.

Key Report Takeaways

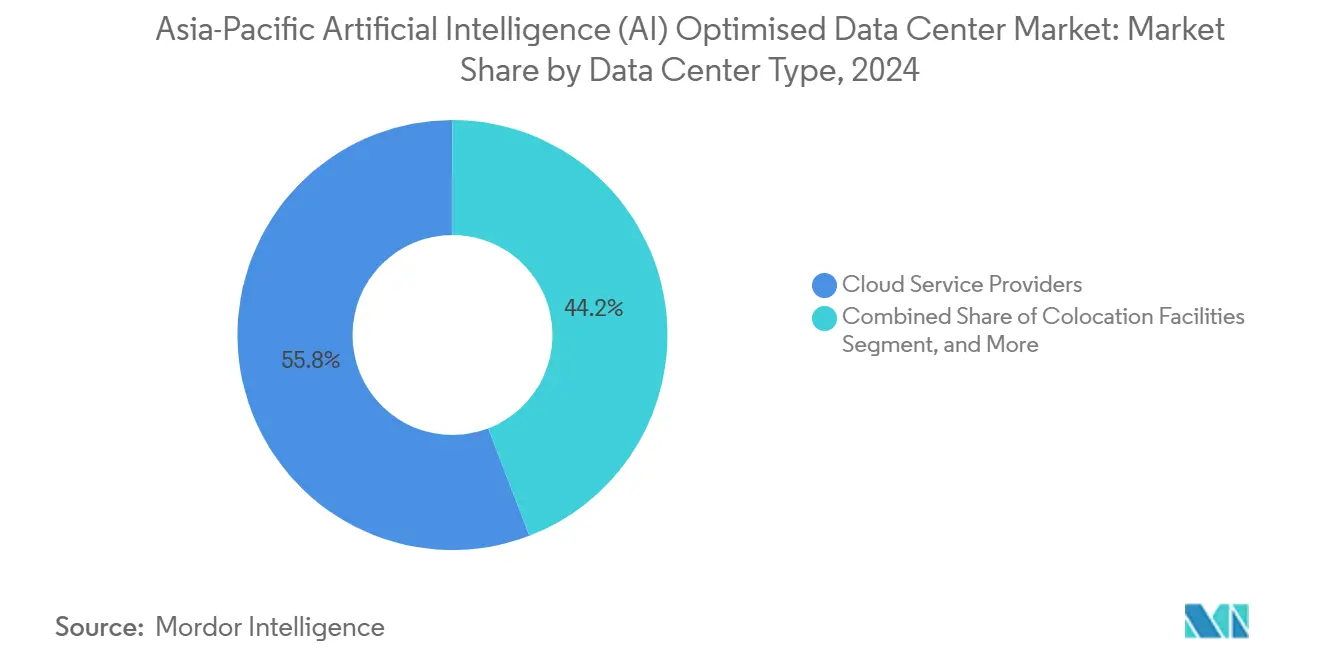

- By data center type, hyperscale cloud providers led with a 55.82% Asia-Pacific artificial intelligence data center market share in 2024, while colocation facilities are on track for a 24.23% CAGR through 2030.

- By component, software held 45.83% of the Asia-Pacific artificial intelligence data center market size in 2024, whereas hardware infrastructure is projected to expand at 23.67% CAGR to 2030.

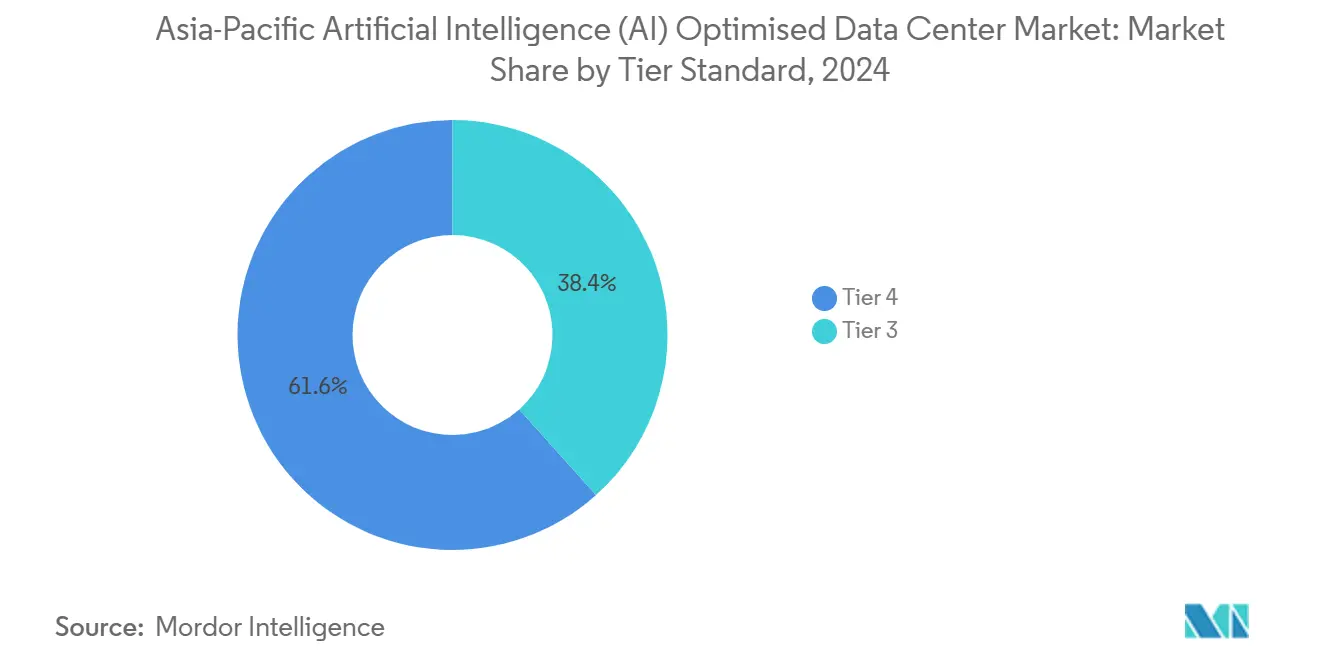

- By tier standard, Tier IV installations commanded 61.63% share of the Asia-Pacific artificial intelligence data center market size in 2024; Tier III facilities are advancing at a 24.77% CAGR.

- By end-user industry, IT and ITES accounted for 33.82% of the Asia-Pacific artificial intelligence data center market size in 2024, while internet and digital media posts the highest 23.45% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Asia representing one of the more structurally developed among them. The global report on artificial intelligence (ai) data center market by Mordor Intelligence reflects how these regional layers combine into a single system.

Asia-Pacific Artificial Intelligence (AI) Optimised Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale cloud build-outs in Southeast Asia | +4.2% | Southeast Asia core, spill-over to India | Medium term (2-4 years) |

| Government-backed AI compute subsidies in China and South Korea | +5.8% | China and South Korea, policy contagion to ASEAN | Short term (≤ 2 years) |

| AI-led retrofit of brownfield facilities to liquid cooling | +3.1% | Global, concentrated in coastal mega-sites | Medium term (2-4 years) |

| Surging generative-AI inference traffic at telecom edge nodes | +2.9% | APAC core, early gains in Japan, Singapore | Short term (≤ 2 years) |

| On-prem GPU clusters by Japanese keiretsu manufacturers | +1.8% | Japan-centric, limited regional spillover | Long term (≥ 4 years) |

| Sovereign-AI mandates accelerating ASEAN colo pre-leasing | +4.5% | ASEAN markets, regulatory influence expanding | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-backed AI compute subsidies drive infrastructure acceleration

South Korea’s USD 7 billion AI program, aimed at strengthening the artificial intelligence-optimised data center ecosysyem, 400% above prior infrastructure budgets, directs 60% of funds to domestic capacity additions, compressing build timelines to less than 18 months. China’s requirement that 80% of AI-training workloads remain onshore by 2026 has produced the region’s highest colocation pre-lease rates and propelled GPU inventory stockpiling to hedge export-control risk. Across ASEAN, similar mandates lift sovereign-cloud premiums by 25–30%, especially in Singapore, where certified facilities already command the lowest vacancy in Asia.

Hyperscale cloud build-outs reshape Southeast Asian infrastructure

Google’s USD 3 billion plan for Thailand and Malaysia confirms the power-grid advantage these markets hold over legacy hubs, while Microsoft’s USD 1.7 billion Indonesian sovereign-cloud region positions the company ahead of Jakarta’s 2025 data-localization deadline. Each hyperscaler requires parcel-level transformer blocks of 100 MW or more, incentivizing industrial-park locations that can bypass urban grid queues.

AI-led retrofit of brownfield facilities to liquid cooling

Generative-AI racks run 3–4 times hotter than conventional servers, forcing operators to pursue direct-to-chip cooling to hold PUE below 1.3. NTT reports that 40% of all new Japanese capacity commissioned in 2024 already integrates liquid cooling. Retrofit economics favor brownfield halls with sufficient floor load and busway headroom, cutting per-rack energy use by 15–20% and doubling density without greenfield lead-time.

Surging generative-AI inference traffic at telecom edge nodes

5G multi-access edge compute rollouts are shifting AI inference closer to users, trimming latency and offloading backbone bandwidth. Japan and Singapore are first movers, each layering small-footprint GPU clusters inside carrier hotels to serve real-time translation, immersive retail, and AR navigation services. The strategy frees hyperscale regions for training tasks while generating new micro-colocation demand curves.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute transformer-grade power shortages in Tier-2 Indian cities | -2.1% | India Tier-2 cities, grid infrastructure gaps | Short term (≤ 2 years) |

| ASIC/GPU export controls impacting supply lead-times | -3.4% | China primary, secondary effects across APAC | Medium term (2-4 years) |

| Rising seawater-intake restrictions on coastal mega-sites | -1.6% | Coastal facilities in Singapore, Japan, Australia | Long term (≥ 4 years) |

| Talent crunch for AI-optimized DC-IM software engineers | -2.8% | Regional, acute in Singapore, Seoul, Tokyo | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Power-infrastructure shortages constrain Tier-2 city expansion

In Pune, Hyderabad, and Chennai, grid allocations trail data-center demand by up to 40%, pushing connection waits beyond 18 months and forcing developers into higher-cost renewable PPA structures. Although green power softens emissions profiles, added capex inflates project IRR hurdles by as much as 300 basis points.

ASIC/GPU export controls impact supply lead-times

Curbs on advanced accelerators lengthen delivery windows to 6–12 months, prompting Chinese firms to lift on-prem order volumes by 180% year on year. Japanese buyers now diversify toward domestic chipmakers offering 60–70% of top-tier performance at 40% lower cost, but at the expense of software-stack fragmentation and validation delays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation growth eclipses historical norms

Colocation facilities captured 28.35% of spend yet will expand at 24.23% CAGR, eclipsing hyperscale’s growth as sovereign-AI rules make domestic rack control mandatory for banks, insurers, and government ministries. Hyperscalers retain a 55.82% lead, but their Asia-Pacific artificial intelligence data center market share has plateaued as on-prem and edge nodes proliferate. Colocation operators that pre-provision liquid cooling and 20+ MW transformer blocks win outsized pre-leases, particularly in Singapore and Kuala Lumpur where land caps limit greenfield scale. Enterprise and edge deployments, favored by Japanese keiretsu, absorb export-control risk by retaining physical GPU custody. The Asia-Pacific artificial intelligence data center market size tied to enterprise on-prem nodes will cross USD 3 billion by 2030, reflecting a sustained diversification away from public cloud. Over the forecast horizon, hyperscaler build-outs are expected to consolidate around five power-rich corridors, cementing their role in training workloads while offloading latency-critical inference to edge colo pods.

Across 2025-2030, hyperscaler expansion pledges, Microsoft’s USD 2.9 billion in Japan and Google’s USD 3 billion in mainland Southeast Asia, lift the segment’s historic 18.4% CAGR to 21.8%. Providers that integrate submarine-cable landing rights with direct GPU capacity create a defensible moat against domestic competitors. Meanwhile, the Asia-Pacific artificial intelligence data center market continues to reward colocation groups that obtain AI-governance stamps and bundle low-latency interconnect fabrics, allowing tenants to stitch private clusters to hyperscale GPUs when export limits relax.

By Component: Hardware surge arrives as AI moves from pilot to production

Software still commands 45.83% of 2024 spend because model frameworks, orchestration layers, and observability platforms remain foundational for AI buildout. Yet hardware, the fastest rising slice at 23.67% CAGR, is forecast to top USD 10 billion of Asia-Pacific artificial intelligence data center market size by 2030, propelled by the pivot from cloud-based experimentation to at-scale inference clusters that stress rack density thresholds. Operators now reserve more than half of 2025-capex for cooling loops, busways, and medium-voltage switchgear that can sustain thermals above 40 kW per rack.

Power and cooling swallows the largest hardware outlay; each GPU rack draws up to 10× the current of a CPU rack, pushing many halls to 30 MVA utility feeds. Liquid-cooling procurement alone is growing at 35% annually in Japan, raising the country’s Asia-Pacific artificial intelligence data center market share inside the hardware category. Services, representing 31.52% of spend, are skewing toward managed offerings as customers outsource tuning of replicas, gradient checkpoints, and energy-aware scheduling. Professional-services growth lags as hyperscalers internalize design skills and smaller providers rely on reference architectures from vendors like Schneider Electric. Across the region, supply-chain constraints in GPUs and network fabric cause operators to hold three-month inventory buffers, tying up working capital but ensuring deployment continuity.

By Tier Standard: Tier III momentum builds at the edge

Tier IV halls still dominate with 61.63% share because AI-training downtime can erase weeks of compute work and spill into model-retraining budgets. Even so, Tier III venues, forecast at a 24.77% CAGR, capture fresh demand for inference, where brief disruptions can be absorbed through traffic routing and micro-batch rescheduling. The Asia-Pacific artificial intelligence data center market size linked to Tier III footprints will top USD 6 billion by 2030, aided by edge deployments in telecom exchanges and metro fiber shelters.

China’s sovereign-AI workloads continue to insist on Tier IV redundancy, but Southeast Asia relaxes to Tier III levels that trade five-nines for quicker build times and 18–20% lower capex. Japan’s regulators now accept modular Tier III pods inside factories to shorten semiconductor design loops. Meanwhile, Tier IV growth inches higher to 22.1% CAGR as capital-rich hyperscalers double-stack liquidity agreements with suppliers to secure switchgear and chillers 12 months in advance. The Asia-Pacific artificial intelligence data center market share split between tiers will narrow, yet both remain indispensable: one for uninterrupted training and the other for latency-sensitive inference at the network edge.

By End-user Industry: Internet and Digital Media rockets ahead

IT and ITES held 33.82% of 2024 outlays thanks to early adoption of continuous integration pipelines and automated test frameworks powered by large-language models. By contrast, Internet and Digital Media grows at 23.45% CAGR, lifted by real-time content generation, recommendation engines, and immersive social experiences that require millisecond-grade inference. The Asia-Pacific artificial intelligence data center industry is witnessing telecoms allocate 18.7% of spend toward multi-access edge nodes to enable computer-vision AR overlays for 5G subscribers.[1]GSMA Future Networks Team, “Multi-access edge computing overview,” GSMA, gsma.com

BFSI’s 15.2% share is sticky because risk and compliance teams must host fine-tuning cycles inside national borders, pushing sovereign-cloud premiums upward. Healthcare and Life Sciences add 22.8% CAGR by harnessing generative AI in drug discovery and radiology triage, often under hospital-grade privacy rules.[2]Health-Tech Editors, “AI accelerates drug discovery and imaging,” Nature Medicine, nature.com Manufacturing use cases cluster around predictive maintenance and inline defect detection, requiring controller-edge integration that favors on-prem clusters within factories. Government and Defense, though smaller, enjoy priority access to transformer blocks and water rights, ensuring facilities achieve readiness ahead of civilian counterparts.

Geography Analysis

China dominates the Asia-Pacific artificial intelligence data center market with 42.74% share in 2024, shielded by directives that 80% of training workloads remain onshore by 2026. Annual growth accelerates to 22.3% as export-control headwinds spur 180% year-over-year spikes in domestic GPU deployments. Beijing-backed liquid-cooling mandates for halls above 10 MW trigger retrofit booms across legacy campuses, sustaining the country’s outsized CAPEX run-rate.

Japan, at 21.3% share, leverages record foreign direct investment, Oracle’s USD 8 billion and Microsoft’s USD 2.9 billion, to cement its role as the region’s most advanced cooling lab. National fast-track approvals for PUE below 1.3 halls allow projects to break ground within 90 days, and keiretsu stakeholders add USD 2 billion in on-prem clusters to secure design IP.

South Korea posts the region’s fastest 26.61% CAGR on the back of a USD 7 billion AI stimulus focused on domestic capacity grants and tax credits. The telecom regulator’s 2025 edge-compute mandate further tilts spend toward distributed 5G nodes, creating parallel demand tracks for hyperscale and micro-colo operators.

India’s 18.9% share remains capped by transformer bottlenecks and grid queuing in Tier-2 metros, yet renewable PPAs and land banking along coastal corridors keep long-term prospects intact. Australia and New Zealand jointly hold 8.4% share, courting investors with sovereign-cloud carve-outs aimed at defense and health agencies.[3]Claire Jones, “Australia sovereign cloud AI infrastructure,” Australian Financial Review, afr.com Singapore, though only 6.1% by revenue, wields outsized regulatory influence; its AI governance framework now serves as the certification template across ASEAN. Remaining Southeast Asian nations exploit hyperscaler capex pushes to leapfrog legacy infrastructure, positioning the corridor as the world’s highest-growth adjacency for AI workloads.

Mordor Intelligence provides coverage of the artificial intelligence (ai) data center market across other key regional markets, including Middle East and Africa, North America, and South America, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to China, Japan, Malaysia, Indonesia, Singapore, and Thailand incorporating local coverage and market participation, as required.

Competitive Landscape

Asia-Pacific artificial intelligence data center market concentration is moderate as hyperscalers, regional telcos, and independent colocation firms pursue overlapping strategies. Alibaba Cloud, Tencent Cloud, AWS, and Microsoft continue to bundle cloud services with owned real estate, but rising data-residency rules enable domestic champions like NTT Global Data Centers and STT GDC to defend share via compliance certifications and pre-installed liquid-cooling loops.

Strategic moves include Microsoft’s sovereign-cloud tie-ups with Thai ministries, Oracle’s Tokyo-Osaka megacluster optimized for 40 kW-rack AI, and STT GDC’s USD 800 million buyout of Indian halls already equipped for GPU densities above 30 kW. Technology alliances deepen: Schneider Electric and Vertiv provide closed-loop cooling skids, while NVIDIA and Huawei jockey for accelerator design-wins amid export restrictions. Operators with in-house liquid-cooling IP capture premium rents and can defer brownfield write-offs by doubling rack density without enlarging footprints.

The talent crunch shapes M&A logic; firms view engineering headcount as a scarce asset and pay acquisition premiums for teams that can integrate direct-to-chip cooling, AI workload schedulers, and energy-adaptive DC-IM software. Competitive intensity also rises at the edge, where NTT and Singtel leverage fiber access rights to deploy micro-colo pods that bind 5G RAN sites to GPU accelerators, thus reducing last-mile latency for AR and gaming workloads. Overall, the market rewards players capable of uniting compliance assurance, high-density cooling, and energy resilience inside a single commercial offering.

Asia-Pacific Artificial Intelligence (AI) Optimised Data Center Industry Leaders

NVIDIA Corporation

Huawei Technologies Co., Ltd.

Sunbird Software, Inc.

Delta Electronics

Daikin Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Alibaba Cloud unveiled its newest addition to the "Qwen series" of artificial intelligence models. This launch comes amid intensifying competition in China's large language model arena, especially after the notable "DeepSeek moment." The newly introduced model, "Qwen2.5-Omni-7B," boasts multimodal capabilities, allowing it to handle diverse inputs such as text, images, audio, and video. In return, it generates instantaneous text and natural speech outputs.

- February 2025: Daikin has unveiled its latest offering, the Pro-C Computer Room Air Handler (CRAH), bolstering its Data Center product lineup. Tailored to cater to diverse cooling requirements of Data Centers, the unit boasts an enhanced design and sophisticated control mechanisms.

- January 2025: Microsoft added USD 1.5 billion to Thailand’s AI buildout, introducing sovereign-cloud zones for finance and public-sector clients.

- December 2024: Oracle opened the first USD 8 billion tranche of Japan GPU halls in Tokyo and Osaka with 40 kW liquid-cooled racks.

Asia-Pacific Artificial Intelligence (AI) Optimised Data Center Market Report Scope

The term "Artificial Intelligence (AI) in data centers delves into the integration of diverse AI technologies, spanning machine learning, deep learning, natural language processing, and computer vision into the operations of data centers. These operations encompass a spectrum of components, from infrastructure and energy management to storage, networking, cybersecurity, and facility automation.

Asia-Pacific Artificial Intelligence (AI) Data Center Market Report is Segmented by Data Center Type (CSP Data Centers, Colocation Data Centers, and Others(Enterprise and Edge), by Component (Hardware(Power, Cooling, IT Equipment, and Others), Software Technology (Machine Learning, Deep Learning, Natural Language Processing, and Computer Vision)), and Services, and by Country (China, India, Japan, Malaysia, Australia, Singapore, Indonesia, Thailand, South Korea, and Rest of Asia-Pacific). The Market Sizes and Forecasts are Provided in Values (USD) for all the Above Segments.

| Cloud Service Providers |

| Colocation Facilities |

| Enterprise / On-Prem / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| China |

| Japan |

| India |

| Malaysia |

| South Korea |

| Singapore |

| Rest of Asia-Pacific |

| By Data Center Type | Cloud Service Providers | |

| Colocation Facilities | ||

| Enterprise / On-Prem / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

| By Country | China | |

| Japan | ||

| India | ||

| Malaysia | ||

| South Korea | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What growth rate is forecast for the Asia-Pacific artificial intelligence data center market through 2030?

The market is projected to expand at a 22.69% CAGR, reaching USD 26.67 billion by 2030.

Which segment grows fastest within Asia-Pacific AI data centers?

Colocation facilities lead with a 24.23% CAGR as sovereign-AI rules drive domestic rack demand.

Why are liquid-cooling retrofits accelerating in Asia-Pacific GPU halls?

Generative-AI racks generate 3–4× the heat of traditional servers, and liquid cooling keeps PUE below 1.3 while doubling rack density.

Which country delivers the highest growth pace?

South Korea posts the strongest 26.61% CAGR, backed by USD 7 billion in AI-specific data-center incentives.

How do export controls influence regional AI infrastructure strategies?

Restrictions lengthen GPU lead-times to 6–12 months, pushing Chinese and Japanese firms to stockpile accelerators and favor on-prem clusters.

Page last updated on: