China Artificial Intelligence (AI) Optimised Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

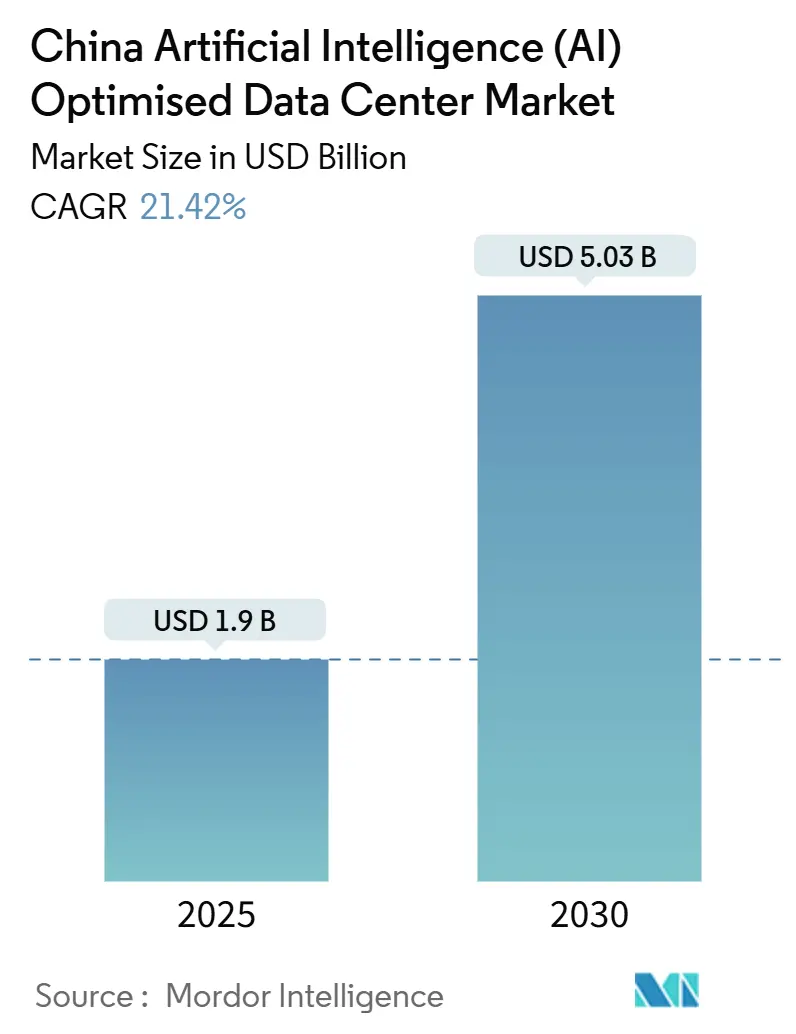

| Market Size (2025) | USD 1.9 Billion |

| Market Size (2030) | USD 5.03 Billion |

| Growth Rate (2025 - 2030) | 21.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Artificial Intelligence (AI) Optimised Data Center Market Analysis by Mordor Intelligence

The China artificial intelligence data center market size is presently valued at USD 1.90 billion, and it is forecast to reach USD 5.03 billion by 2030 on the back of a 21.42% CAGR. The growth is propelled by state-backed AI initiatives, mandatory data-sovereignty compliance, and the accelerated roll-out of domestic AI accelerators that favor heterogeneous compute architectures. Liquid-cooled, high-density GPU clusters are becoming the design default as providers chase power-usage-effectiveness (PUE) targets below 1.2. Colocation adoption is rising quickly because enterprises are trimming capital budgets while still demanding access to the newest AI hardware. Parallel investments in renewable-energy integration and western-province build-outs align with the national “East Data West Computing” plan, which pushes workloads toward low-carbon energy hubs. Competitive intensity is moderate: hyperscalers such as Alibaba Cloud, Tencent Cloud, and Huawei Cloud dominate, yet regional specialists carve out share with edge and green-power propositions.

Key Report Takeaways

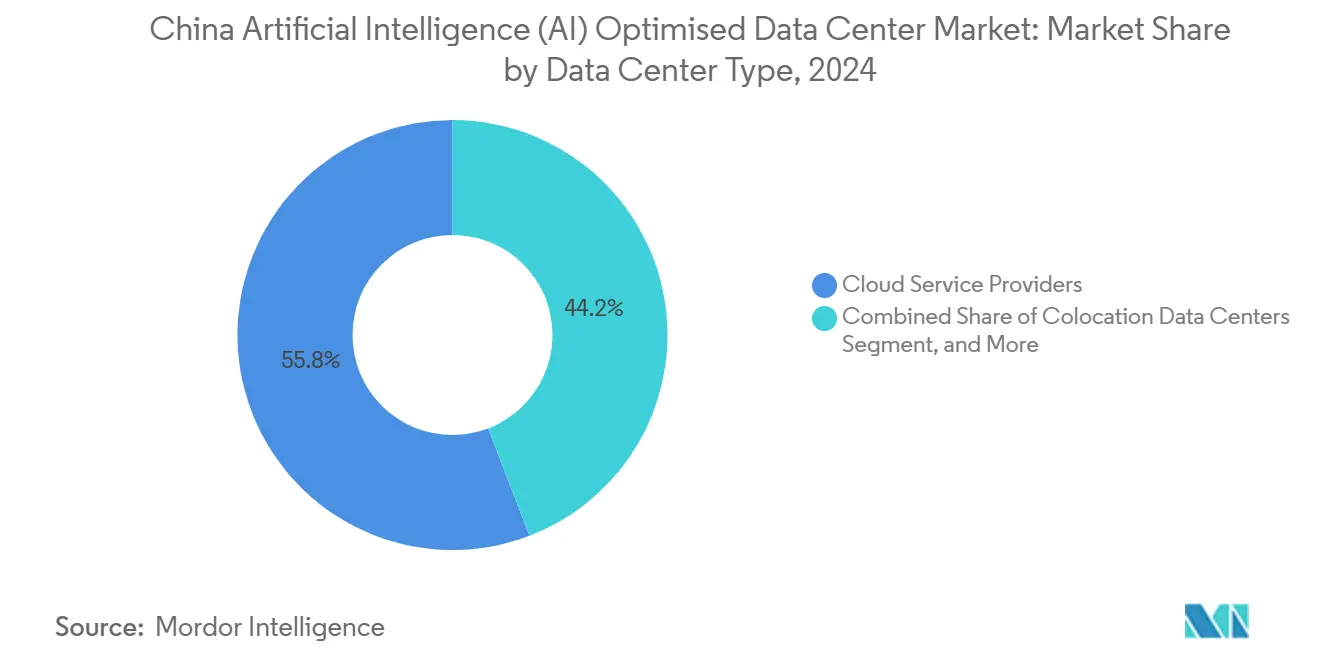

- By data-center type, Cloud Service Providers led with 55.82% of China artificial intelligence data center market share in 2024, while Colocation Data Centers are advancing at a 23.23% CAGR through 2030.

- By component, software accounted for 45.83% of the China artificial intelligence data center market size in 2024; hardware is projected to expand at a 22.67% CAGR between 2025-2030.

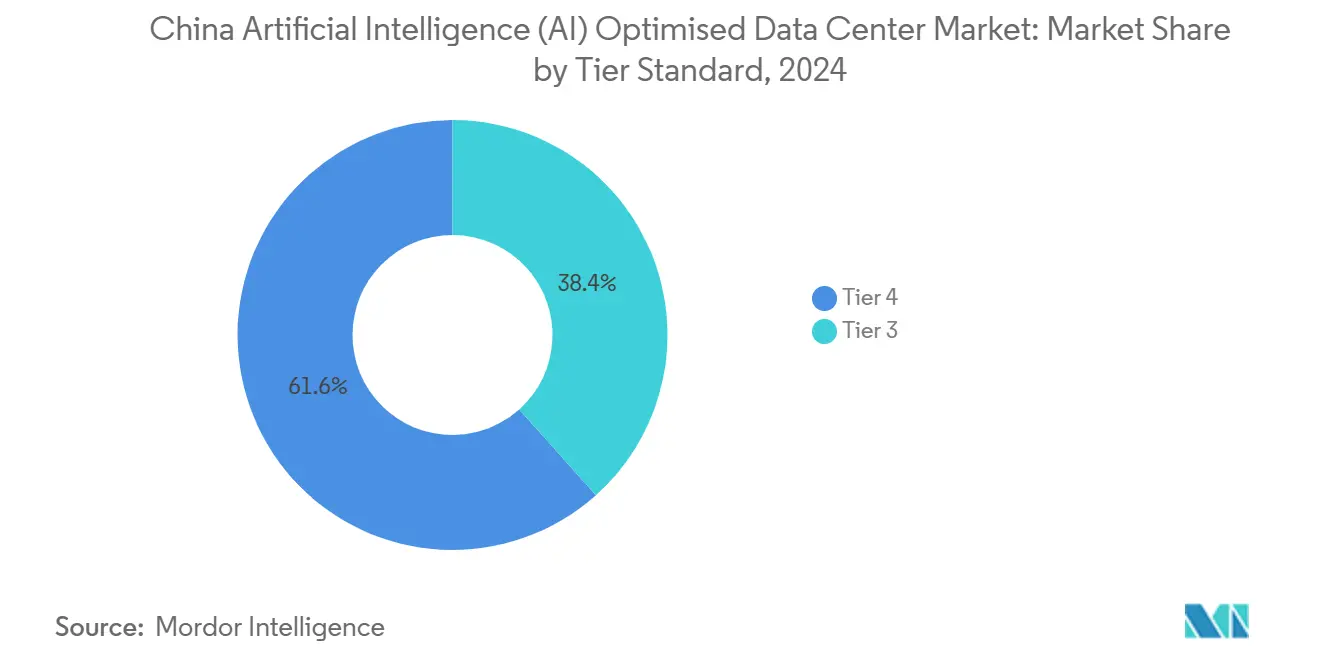

- By tier standard, Tier IV facilities held 61.63% revenue share in 2024 in China artificial intelligence data center market, whereas Tier III deployments post the fastest 23.77% CAGR to 2030.

- By end-user industry, IT and ITES captured 33.82% of the China artificial intelligence data center market size in 2024; Internet and Digital Media is the quickest-growing segment at 22.45% CAGR through 2030.

China contributes to a system defined not by any single country or region but by the interaction of many. The global artificial intelligence (ai) data center market data by Mordor Intelligence represents that combined structure.

China Artificial Intelligence (AI) Optimised Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid deployment of high-density GPU clusters by Chinese hyperscalers | +4.2% | National, concentrated in East and North China | Medium term (2-4 years) |

| Government subsidies and green-DC incentives in Tier-2 cities | +3.8% | Southwest and Northwest China primarily | Long term (≥ 4 years) |

| Surge in proprietary AI silicon driving heterogeneous compute demand | +3.5% | National, with manufacturing hubs in East China | Medium term (2-4 years) |

| Mandatory data-sovereignty rules repatriating AI workloads | +2.9% | National, strongest enforcement in tier-1 cities | Short term (≤ 2 years) |

| Expansion of ultra-low-latency 5G edge zones for real-time AI inference | +2.1% | East and South China initially, expanding nationwide | Medium term (2-4 years) |

| Aggressive PUE targets pushing liquid-cooling retrofits | +1.8% | National, prioritizing Beijing-Tianjin-Hebei region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid deployment of high-density GPU clusters by Chinese hyperscalers

Hyperscale cloud providers have redesigned server halls for domestic AI accelerators that already power almost half of large-language-model (LLM) training tasks. Huawei alone has rolled out 2,500 petaflops of AI compute across 20 cities, and its Ascend 910B chips require liquid cooling and custom interconnects that differ from legacy GPU layouts. The shift is steering operators toward heterogeneous racks that pair multiple accelerator types inside the same power domain to guarantee supply continuity. Operators report 30-40% energy savings once immersion or cold-plate systems replace air cooling, freeing energy headroom for additional compute.[1]Huawei Technologies, “计算2030,” Huawei, huawei.com

Government subsidies and green-DC incentives in tier-2 Chinese cities

The National Development and Reform Commission (NDRC) offers land, tax, and low-rate financing packages to data-center projects that co-locate with renewable-generation assets. Qinghai’s plan to lift photovoltaic self-consumption limits from 40 MW to 100 MW for single campuses illustrates how western provinces compete for AI workloads.[2]Qinghai Provincial People’s Congress, “关于清洁能源与算力融合发展的建议,” qhrd.gov.cn The policy widens source-grid-load-storage integration zones to 500 km, enabling operators in Xining or Yushu to tap hydro-solar hybrids and achieve >80% green-power utilization mandated for 2025 builds.[3]National Development and Reform Commission, “关于新增算力布局的指导意见,” ndrc.gov.cn

Surge in proprietary AI silicon driving demand for heterogeneous compute racks

Huawei Ascend, Baidu Kunlun, Cambricon, and Biren chips each impose unique power-draw and cooling envelopes, obliging facilities to adopt open-sled rack formats and programmable power-distribution units. Supply-chain uncertainties from foundry-yield variability push operators to diversify chip sourcing and over-provision capacity buffers. Software orchestration layers must juggle distinct toolchains while sustaining the low-latency, high-bandwidth links vital for distributed AI training.

Mandatory data-sovereignty rules repatriating AI workloads to domestic facilities

Security assessments for cross-border transfers now cover personal, financial, and public-sector datasets, forcing multinational firms to anchor AI workloads in mainland facilities. Sovereign-cloud offerings that bundle compliance audits, encryption key-management, and localized support gain preference among regulated industries. Distributed edge nodes ensure that inference for global apps stays inside Chinese territory without breaching latency budgets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National energy-consumption caps limiting new permits in Beijing-Tianjin-Hebei | -2.8% | Beijing-Tianjin-Hebei region specifically | Short term (≤ 2 years) |

| US GPU-export curbs lengthening AI-accelerator supply cycles | -2.1% | National, affecting all major operators | Medium term (2-4 years) |

| Grid instability in western provinces complicating large-scale AI DC siting | -1.4% | Northwest and Southwest China primarily | Long term (≥ 4 years) |

| Rising water-scarcity penalties discouraging evaporative-cooling adoption | -0.9% | North China and western regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National energy-consumption caps limiting new permits in Beijing-Tianjin-Hebei

Local governments froze large-scale data-center approvals to meet dual-carbon targets, squeezing supply in China’s most lucrative rack market. Existing operators leverage efficiency retrofits and edge offloading to maximize authorized energy envelopes. Capacity scarcity lifts pricing premiums 20-30% above unconstrained provinces and accelerates migration of batch training jobs to western hubs.[4]Beijing Municipal Data Bureau, “培育壮大绿色算力,” data.beijing.gov.cn

US GPU-export curbs lengthening AI-accelerator supply cycles

Export controls doubled procurement lead times to 6-12 months, compelling providers to lock in demand forecasts and maintain higher inventory buffers. Dual-sourcing strategies pair restricted foreign accelerators with domestic alternatives that now reach 80% of flagship performance. The policy accelerates capital allocation toward home-grown chip ecosystems but reduces short-term procurement flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation Drives Infrastructure Sharing

Colocation facilities captured 23.23% of new capacity additions in 2024 and are forecast to outpace the wider China artificial intelligence data center market at a 23.23% CAGR. The pivot reflects budgets shifting from capital expenditure to predictable operating expense as enterprises prioritize rapid access to AI-ready racks and advanced cooling. Cloud Service Providers still dominate overall installed capacity with 55.82% China artificial intelligence data center market share, underwritten by hyperscalers’ vertically integrated cloud-to-chip stacks.

Enterprises increasingly mix colocation nodes with public-cloud control planes to sidestep Beijing energy-permit constraints while preserving low-latency interconnects for real-time inference. Providers such as GDS Holdings pre-install liquid-cooled AI pods, enabling customers to spin up 8-GPU blocks within days. The China artificial intelligence data center market size for colocation deployments is projected to more than triple by 2030 as regulatory complexity and technology refresh cycles shorten.

By Component: Hardware Acceleration Drives Infrastructure Transformation

Hardware spending will expand at a 22.67% CAGR, faster than the broader China artificial intelligence data center market, as generative-AI training pushes rack power envelopes past 30 kW. Although Software held 45.83% revenue share in 2024, the shift toward proprietary AI silicon and low-latency fabrics elevates server, network, and cooling outlays.

Power-delivery and cooling subsystems collectively represent the fastest-growing hardware slice, mirroring PUE mandates and rack-density trends. High-bandwidth memory, silicon photonics, and 800 Gbps switches enter mainstream bill-of-materials lists. Services revenue follows hardware complexity: integration firms bundle chip-level tuning, workload migration, and compliance documentation as managed offerings, sustaining a steady mid-teens CAGR inside the China artificial intelligence data center industry.

By Tier Standard: Tier III Gains Ground Through Cost Optimization

Tier IV remained the preferred choice for mission-critical AI model training, accounting for 61.63% of 2024 capacity. Yet Tier III is forecast to post a brisk 23.77% CAGR, narrowing the gap as checkpointing, distributed training, and redundancy features built into software temper outage risk. The China artificial intelligence data center market size tied to Tier III is expected to nearly quintuple by 2030.

Operators realize 30-40% capex savings by downgrading one redundancy level without sacrificing customer service-level agreements for less latency-sensitive tasks. Regulators have clarified tier-classification criteria, giving enterprises a transparent risk-budgeting framework and allowing edge-zone sites to standardize on Tier III with regional grid-backup overlays.

By End-user Industry: Digital Media Accelerates AI Adoption

Digital-media platforms register the highest growth velocity at 22.45% CAGR, narrowing the lead held by IT and ITES, which commanded 33.82% China artificial intelligence data center market share in 2024. Video-generation workflows, personalized feeds, and real-time moderation demand GPU-dense clusters and high-throughput object-storage arrays.

Manufacturing and Industrial IoT deployments emphasize edge inference for quality control and predictive maintenance, spawning micro-data-center footprints inside factory grounds. BFSI and Healthcare maintain steady double-digit growth as regulatory-compliant sovereign-cloud services mature, while Government and Defense workloads gravitate toward domestic silicon stacks for security assurances mandated by national policy.

Geography Analysis

East China remains the largest regional contributor to the China artificial intelligence data center market size, thanks to dense enterprise footprints, skilled labor pools, and mature connectivity. Strict land-use and energy caps motivate upgrades to liquid cooling and 2-story rack arrangements that add capacity without breaching allocated megawatts. The region also acts as a control plane for AI compute executed in western provinces via low-latency UHV lines.

North China, anchored by Beijing-Tianjin-Hebei, commands premium pricing because capacity additions lag demand under regional carbon quotas. Operators push PUE values below 1.15 through heat-recovery loops that feed municipal heating grids, while edge nodes in neighboring provinces handle overflow batch training.

South China, notably Guangdong, leverages manufacturing synergies to adopt AI for supply-chain optimization. Proximity to Hong Kong supports hybrid architectures that segregate international workloads from domestic data, a compliance pattern gaining traction among export-oriented enterprises.

Southwest provinces such as Sichuan and Guizhou capture hyperscale builds with abundant hydro-power and cooler climates that favor free-air economization. Local authorities streamline permits, grant land concessions, and guarantee renewable-energy allocation, helping the sub-region post the highest installed-rack growth rate nationwide. Northwest hubs in Ningxia mirror these advantages but battle grid-stability concerns that call for integrated storage solutions.

Northeast China lags in absolute capacity but presents growth optionality as provincial governments court digital infrastructure to revitalize industrial bases. Improved fiber backbones and preferential tariffs are beginning to attract second-wave operators aiming to diversify geographic risk.

The artificial intelligence (ai) data center market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Middle East and Africa, North America, and South America. This is complemented by country-specific insights for Malaysia, Indonesia, South Africa, Canada, Chile, and Singapore, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Market concentration remains moderate: The top three hyperscalers, Alibaba Cloud, Tencent Cloud, and Huawei Cloud, maintain a significant share of deployed AI racks. However, this dynamic creates opportunities for regional colocation specialists and telecom-affiliated players to carve out their niches. These market leaders differentiate themselves through vertically integrated solutions that combine domestic AI chips, orchestration stacks, and low-carbon power-purchase agreements. Huawei has advanced its Ascend-centric server line with in-rack liquid loops and programmable network fabrics, while Alibaba is piloting custom silicon photonic interconnects to accelerate training times for trillion-parameter models.

Regional providers, such as Shanghai AtHub, are leveraging their expertise in retrofitting legacy halls. By deploying immersion baths, they achieve PUE levels below 1.2 without incurring the costs associated with greenfield developments. Meanwhile, telecom operators like China Mobile and China Telecom are utilizing their extensive nationwide fiber infrastructure, exchange nodes, and 5G MEC sites to deliver bundled distributed inference services.

Over the past year, strategic initiatives have included securing multi-year renewable-energy procurement agreements, establishing joint ventures with provincial governments to develop hydro-powered campuses, and filing patents for AI-optimized rack designs that incorporate on-board phase-change cooling plates. The competitive landscape is increasingly shaped by the need to align with domestic silicon roadmaps and to ensure compliance with evolving data-sovereignty regulations.

China Artificial Intelligence (AI) Optimised Data Center Industry Leaders

Alibaba Cloud

Tencent Cloud

Huawei Cloud

Baidu AI Cloud

GDS Holdings Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: China has launched the first-ever commercial underwater data center off the coast of Hainan Province. This facility, leveraging the ocean's natural cooling properties, significantly reduces energy consumption while housing over 400 high-performance servers capable of processing more than 7,000 AI queries per second. This development marks a groundbreaking step in sustainable AI infrastructure.

- March 2025: China's AI data center industry is facing significant challenges as many facilities remain underutilized. Up to 80% of newly built computing resources are idle, with operators struggling to attract clients for GPU rentals. Nvidia H100 server rental prices have dropped to 75,000 yuan per month, reflecting a sharp decline in demand. The shift in AI trends, driven by reasoning models like DeepSeek's R1, has altered infrastructure requirements, leaving many data centers ill-equipped to meet current needs. Some facilities are choosing to remain idle to avoid further financial losses, and there is speculation that the Chinese government may intervene to address the growing issues in the sector.

- January 2025: Huawei detailed a roadmap for Z-FLOPS-class clusters requiring petabyte-scale memory extensions and 30× interconnect bandwidth increases to support next-generation generative models.

- July 2024: The NDRC, MIIT, and National Energy Administration released the Data Center Green Low-Carbon Development Special Action Plan, mandating above 80% green-power use for new hub-node sites.

China Artificial Intelligence (AI) Optimised Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications. Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises /Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardwares | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises /Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardwares | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

How large is the China artificial intelligence data center market in 2025?

The market is valued at USD 1.90 billion in 2025 and is projected to reach USD 5.03 billion by 2030.

What is the expected CAGR for Chinese AI data centers through 2030?

The compound annual growth rate stands at 21.42% for the 2025-2030 period.

Which segment is growing fastest within Chinese AI data centers?

Colocation facilities post the highest growth at a 23.23% CAGR, reflecting enterprise appetite for shared AI infrastructure.

Why are western Chinese provinces attracting new AI data centers?

Abundant renewable energy, favorable land policies, and government incentives align with the “East Data West Computing” strategy.

How are energy-efficiency regulations shaping data-center design?

Mandated PUE targets below 1.2 are accelerating liquid-cooling retrofits and boosting demand for high-density, energy-efficient rack solutions.

Page last updated on: