United States Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

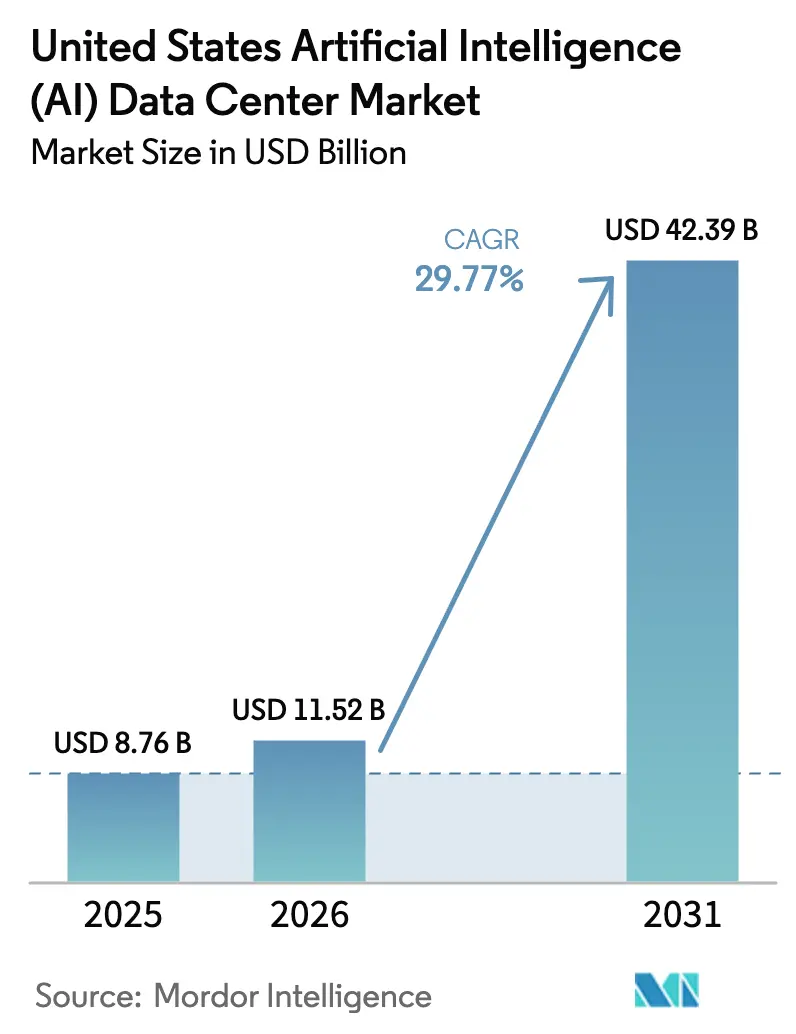

| Base Year Market Size (2025) | USD 8.76 Billion |

| Market Size (2026) | USD 11.52 Billion |

| Market Size (2031) | USD 42.39 Billion |

| Growth Rate (2026 - 2031) | 29.77% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The United States Artificial Intelligence Data Center Market size is projected to expand from USD 8.76 billion in 2025 and USD 11.52 billion in 2026 to USD 42.39 billion by 2031, registering a CAGR of 29.77% between 2026 to 2031.

Explosive generative-AI workloads are boosting rack power densities above 100 kilowatts, reshaping electrical distribution and liquid-cooling design. Hyperscale cloud providers continue to dominate capacity additions through multi-billion-dollar self-build programs, while the colocation segment enjoys the fastest growth as enterprises look for turnkey AI-ready space. Hardware outlays, especially for GPU clusters and high-bandwidth networks, are expanding faster than software spending as operators race to deploy next-generation accelerators. Strict uptime requirements keep Tier IV facilities in the lead, and tax incentives plus renewable-energy availability are shifting new builds toward secondary metros with larger power headroom.

Key Report Takeaways

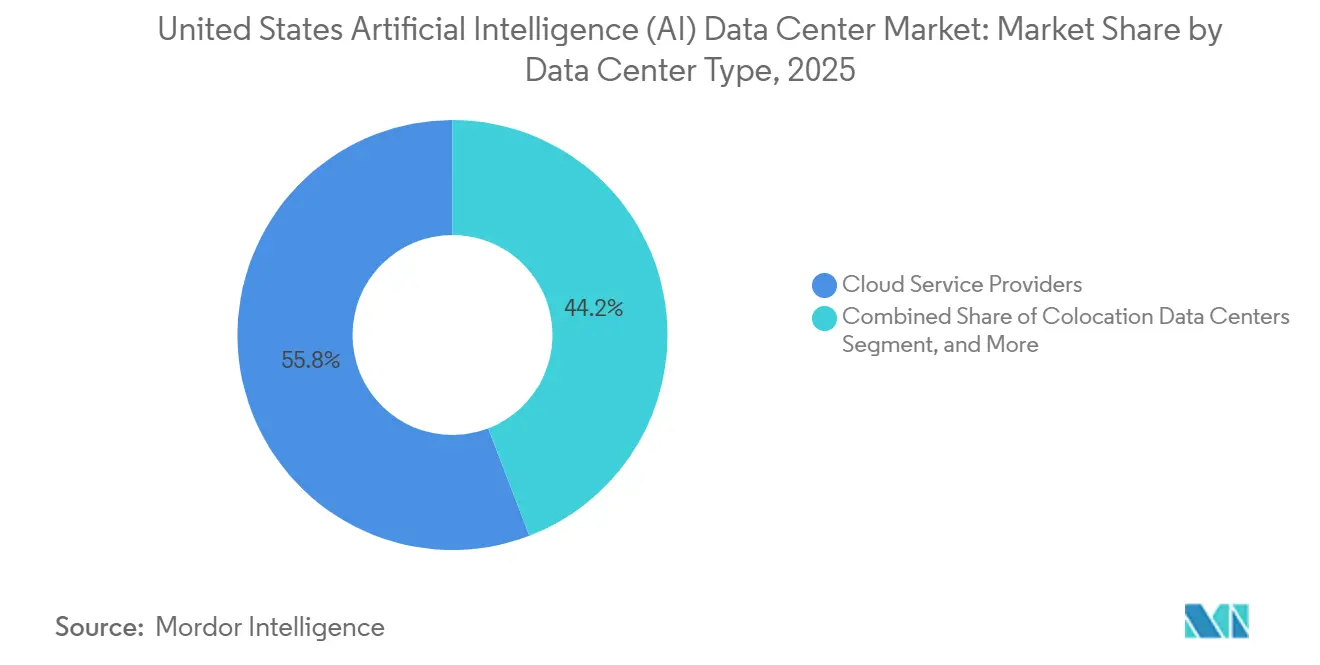

- By data center type, cloud service providers held 55.82% of United States artificial intelligence data center market share in 2025, whereas the colocation segment is projected to post a 31.22% CAGR to 2031.

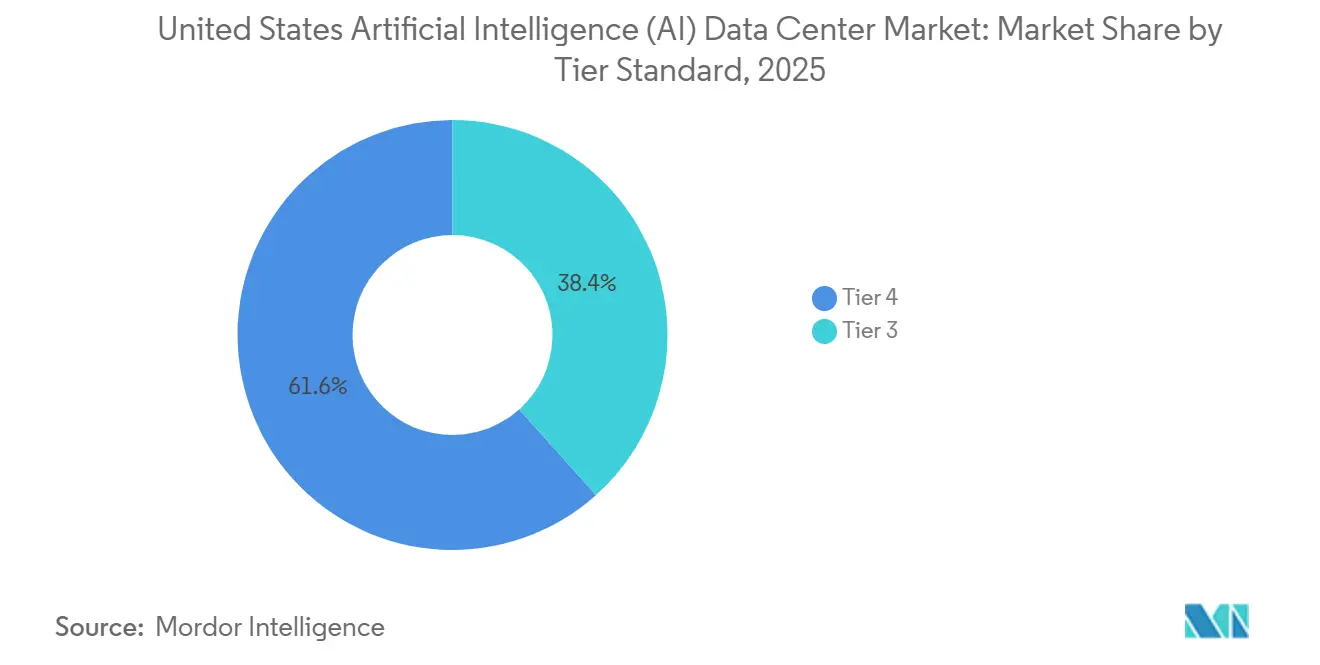

- By tier standard, Tier IV facilities captured 61.63% revenue share in 2025 in the United States artificial intelligence data center market; Tier III is forecast to expand at 32.09% CAGR during 2026-2031.

- By component, software commanded 45.83% of United States artificial intelligence data center market size in 2025; hardware spending is poised to grow at 30.56% CAGR through 2031.

- By end-user industry, IT and ITES accounted for 33.82% share of the United States artificial intelligence data center market size in 2025, while Internet and digital media is projected to record a 30.88% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Relative standing becomes clear only when country-level and regional contributions are evaluated alongside one another at a global level. Mordor Intelligence's artificial intelligence (ai) data center market share coverage captures this comparative structure.

United States Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Generative-AI GPU Cluster Build-outs by US Hyperscalers | +8.2% | National, concentrated in Virginia, Texas, Oregon | Medium term (2-4 years) |

| US CHIPS Act Incentives Accelerating Domestic AI-Chip Supply Chain | +4.1% | National, focused on Arizona, Ohio, New York | Long term (≥ 4 years) |

| AI-Optimised Edge Deployments Supporting 5G and Autonomous-Vehicle Roll-outs | +3.7% | Urban metros, automotive corridors | Medium term (2-4 years) |

| Corporate Net-Zero Mandates Pushing AI-Enabled Energy Optimisation | +2.9% | Global, early adoption in California, Washington | Long term (≥ 4 years) |

| Secondary Markets Offering Low-Latency + Renewable PPAs for AI Facilities | +2.3% | APAC core, spill-over to secondary US metros | Short term (≤ 2 years) |

| FERC Order 2222 Enabling AI-Data-Center Demand-Response Revenues | +1.8% | National, grid-constrained regions prioritized | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Generative-AI GPU Cluster Build-outs by US Hyperscalers

Microsoft has earmarked USD 80 billion for Azure AI capacity, while Amazon is investing USD 100 billion in new AI-specific data centers. Both projects hinge on thousands of H100 GPUs, each drawing a 700-watt TDP.[1]Microsoft Corp., “Stargate AI Infrastructure Initiative,” microsoft.com NVIDIA logged USD 30.8 billion data-center revenue in fiscal 2025 as orders for clusters exceeding 100,000 GPUs rolled in. Rack densities near 150 kilowatts require full liquid cooling and re-engineered busways. Google’s Tensor Processing Units and Amazon’s Trainium chips illustrate an in-house silicon path that trims reliance on external GPU vendors. Meta’s USD 65 billion AI build through 2025 covers 600,000 H100-class accelerators and pushes spill-over demand to colocation facilities.

US CHIPS Act Incentives Accelerating Domestic AI-Chip Supply Chain

The CHIPS and Science Act’s USD 52.7 billion pool is steering advanced-node fabs toward Arizona, Ohio, and New York.[2]U.S. Department of Commerce, “TSMC Arizona Preliminary Terms,” commerce.gov Intel secured USD 8.5 billion to scale leading-edge output, while TSMC obtained USD 6.6 billion for its Arizona complex. Amkor won USD 407 million for advanced packaging that supports AI accelerators, and Micron committed USD 15 billion to high-bandwidth memory capacity in New York. Export-control rules are tightening premium AI chip shipments abroad, giving U.S. data-center builders preferential access.

AI-Optimized Edge Deployments Supporting 5G and Autonomous-Vehicle Roll-outs

Autonomous-driving test corridors in Michigan, California, and Arizona need sub-10 millisecond latency, which pushes AI compute to local edge sites. Verizon’s USD 10 billion 5G program includes Jetson-equipped edge nodes for vehicle-to-everything communications. Amazon’s Wavelength zones embed AWS resources inside carrier networks to shorten data paths for augmented reality and analytic workloads. Tesla’s Dojo cluster, although proprietary, is influencing industry rack-level cooling blueprints. Qualcomm’s Snapdragon embedded AI is extending distributed inference into transportation and smart-city infrastructure.

Corporate Net-Zero Mandates Pushing AI-Enabled Energy Optimization

Microsoft targets carbon negativity by 2030 and has cut portfolio-wide PUE below 1.12 using reinforcement-learning models for cooling. Google’s AI-driven airflow tuning delivers 30% energy savings against legacy baselines.[3]Google LLC, “Cloud TPU v5p Launch,” google.com Meta has procured 12 gigawatts of renewable power and employs machine-learning dispatch to match intermittent supply with GPU loads. Amazon’s Climate Pledge accelerates renewables plus AI-based demand forecasts that flatten load curves. SEC climate-risk disclosure proposals are prompting enterprises to adopt AI energy-management platforms that surface defensible carbon-reduction metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled Workforce for High-Density AI Operations | -3.8% | National, acute in Silicon Valley, Austin | Short term (≤ 2 years) |

| Grid Congestion and Power-Allocation Moratoria in Key Metro Areas | -4.2% | Northern Virginia, Phoenix, Silicon Valley | Medium term (2-4 years) |

| Escalating Water-Usage Restrictions in Drought-Prone States | -2.1% | California, Arizona, Nevada, Texas | Long term (≥ 4 years) |

| High Opex for AI-Centric Liquid-Cooling Retrofits in Brownfield Sites | -1.9% | Legacy data center markets nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Workforce for High-Density AI Operations

The United States faces more than 200,000 unfilled positions across GPU cluster administration, immersion-cooling maintenance, and machine-learning engineering. NVIDIA’s Deep Learning Institute trained 500,000 professionals in 2024 yet cannot match demand. Only a few thousand technicians hold immersion or cold-plate certifications, slowing deployment timelines for large-scale retrofits. Compensation premiums that run 40-60% above generic IT roles squeeze smaller operators. Industry-college partnerships are ramping curricula, though graduates will enter the workforce only gradually through 2031.

Grid Congestion and Power-Allocation Moratoria in Key Metro Areas

Loudoun County froze new permits due to transformer shortages, disrupting projects in the world’s largest data center cluster. Phoenix requires up to 18 months for interconnection requests exceeding 50 megawatts, which delays hyperscale timelines. California ISO issued multiple summer energy emergency alerts, forcing operators to curtail discretionary loads. ERCOT hit record peaks beyond 85 gigawatts in 2024, spurring data-center demand-response programs that rely on on-site batteries and backup-generation fleets. Transmission upgrades often exceed a 3-year lead time, limiting near-term expansion in prime fiber corridors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Hyperscaler Investment Dominates but Colocation Surges

Cloud service providers held 55.82% of United States artificial intelligence data center market share in 2025, grounded in massive internal builds such as Microsoft’s USD 80 billion and Amazon’s USD 100 billion commitments. The colocation slice is forecast to rise at a 31.22% CAGR as enterprises rent GPU-ready halls that support 150 kilowatt racks without upfront capex.

Hyperscalers leverage custom silicon and software stacks to squeeze performance per watt and manage asset sweat cycles. Colocation specialists differentiate through flexible contract terms and regional diversification that skirts grid bottlenecks. Enterprise and edge sites remain smaller in value but play a strategic latency role for autonomous-vehicle feeds and smart-manufacturing loops.

By Component: Software Leads Today, Hardware Accelerates Tomorrow

Software technology commanded 45.83% market share in 2025, encompassing machine learning frameworks, deep learning platforms, natural language processing tools, and computer vision applications that orchestrate AI workload distribution across distributed computing resources. Intel's oneAPI toolkit and NVIDIA's CUDA ecosystem dominate AI software infrastructure, while open-source alternatives including PyTorch and TensorFlow gain enterprise adoption for cost optimization and vendor independence. Hardware components capture the fastest growth trajectory at 30.56% CAGR through 2031, driven by massive GPU cluster deployments requiring specialized power distribution, liquid cooling systems, and high-bandwidth networking infrastructure capable of supporting 400-gigabit Ethernet connections between compute nodes.

Services represent the smallest component segment but demonstrate critical importance for AI data center operations, with managed services providers offering specialized expertise in GPU cluster optimization, workload orchestration, and performance monitoring. Professional services encompass system integration, custom AI model deployment, and regulatory compliance consulting, particularly valuable for enterprises lacking internal AI infrastructure expertise.

By Tier Standard: Tier IV Retains Majority, Tier III Gains Momentum

Tier IV data centers maintained a 61.63% market share in 2025, as AI workloads demand 99.995% uptime guarantees that can only be delivered by the highest reliability standards, with fault-tolerant infrastructure supporting continuous operation during maintenance and equipment failures. GPU cluster training runs, which consume millions of dollars in compute resources, cannot tolerate interruptions, driving hyperscaler preference for Tier IV facilities with redundant power, cooling, and networking systems. Tier III facilities demonstrate faster growth at 32.09% CAGR through 2031, capturing cost-conscious enterprises seeking AI infrastructure with 99.982% availability while accepting slightly higher downtime risk for reduced operational expenses.

Tier IV construction costs exceed USD 15 million per megawatt, compared to USD 8-10 million for Tier III facilities, reflecting the comprehensive redundancy requirements that include dual utility feeds, backup generators, and N+1 cooling systems, which are essential for maintaining AI workload continuity. Liquid cooling retrofits in Tier IV facilities require specialized leak detection systems, emergency shutdown procedures, and maintenance protocols that exceed traditional air-cooled infrastructure complexity while enabling power densities necessary for next-generation AI processing.

By End-User Industry: IT Rules, Media Races Ahead

IT and ITES maintained 33.82% market share in 2025, reflecting software companies' aggressive AI adoption for product development, customer service automation, and business process optimization requiring specialized compute infrastructure. Enterprise software vendors, including Salesforce, ServiceNow, and Adobe, integrate AI capabilities across their product portfolios, driving demand for training and inference infrastructure that supports millions of daily transactions.

Internet and digital media emerge as the fastest-growing segment with 30.88% CAGR through 2031, as streaming platforms, social media companies, and content creators deploy AI for personalization, content moderation, and synthetic media generation, requiring massive parallel processing capabilities. Telecommunications operators invest heavily in AI infrastructure for network optimization, predictive maintenance, and 5G service deployment, with Verizon's USD 10 billion commitment including edge computing nodes supporting autonomous vehicle communication and industrial IoT applications.

Geography Analysis

Northern Virginia hosts the largest cluster of United States artificial intelligence data center capacity, channeling roughly 70% of global web traffic through its dense fiber nexus. Pending grid upgrades are prompting new builds to shift toward Richmond and Norfolk.

Texas registers the fastest growth pace, with Austin, Dallas, and Houston offering competitive power pricing and large renewable energy pipelines. However, ERCOT grid volatility introduces operational risk mitigation costs. Arizona draws steady investment into Phoenix due to its land availability and proximity to California demand, although interconnection and water-usage caps are lengthening project schedules.

Pacific Northwest sites in Oregon and Washington benefit from hydroelectric baseload and cooler climates that lower cooling overhead, appealing to operators with carbon-neutral mandates. Silicon Valley remains a premium micro-region despite high land costs because of its venture capital density and AI talent pool, yet municipal moratoria on large diesel gensets continue to complicate permitting.

Analysis of the artificial intelligence (ai) data center market by Mordor Intelligence spans multiple other regional evaluations across Asia, Middle East and Africa, and North America, supported by country-level insights for Chile, Mexico, Singapore, Saudi Arabia, Canada, and Germany, wherein local market conditions keep varying from one country to another.

Competitive Landscape

Microsoft, Amazon, and Google collectively control more than 60% of installed AI data-center GPU capacity. Each pursues vertical integration that spans proprietary silicon, software frameworks, and high-voltage infrastructure. They also enjoy scale economies in power-purchase agreements and component procurement.

Specialist providers such as Digital Realty, Equinix, CoreWeave, and Lambda Labs capture share in colocation and GPU-as-a-Service niches by offering rapid deployment and contract flexibility. Technology differentiation is visible in immersion-cooling start-ups like LiquidStack, which supports 200-kilowatt racks that satisfy next-generation accelerator thermal loads.

Policy drivers, including FERC Order 2222, incentivize operators to integrate battery storage and participate in demand-response markets, unlocking incremental revenue while mitigating grid stress in congestion-prone metropolitan areas.

United States Artificial Intelligence (AI) Data Center Industry Leaders

NVIDIA Corporation

Intel Corporation

Advanced Micro Devices, Inc.

Cisco Systems, Inc.

ARM Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: LightHouse Data Centers and Wharton Digital have teamed up to unveil a comprehensive platform. This initiative aims to develop, own, and operate hyperscale data centers throughout North America. With a target capacity exceeding 2 GW, the platform is set to cater to the surging demands of AI and cloud services.

- January 2026: NVIDIA and CoreWeave strengthen collaboration to accelerate AI factory buildout, NVIDIA Corporation and CoreWeave, Inc. announced an expanded strategic relationship with NVIDIA investing USD 2 billion in CoreWeave stock to accelerate deployment of AI infrastructure and support the buildout of more than 5 GW of AI compute capacity by 2030.

- October 2025: NVIDIA Corporation revealed a major initiative with U.S. Department of Energy labs (Argonne and Los Alamos) and industry partners to scale advanced AI systems, accelerating nationwide AI infrastructure, including plans for Vera Rubin and Blackwell GPU-based supercomputing and hyperscale deployments.

- April 2025: Schneider Electric secured USD 2.3 billion in AI power and cooling contracts with major U.S. data center operators (including Switch and Digital Realty) to underpin power and thermal systems essential for high-density AI workloads.

United States Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

The United States Artificial Intelligence Data Center Market Report is Segmented by Data Center Type (Cloud Service Providers, Colocation Data Centers, and More), Component (Hardware, Software Technology, and Services), Tier Standard (Tier III and Tier IV), and End-User Industry (IT and IT Services, Internet and Digital Media, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier III |

| Tier IV |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier III | |

| Tier IV | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

How large is the United States artificial intelligence data center market in 2026?

The market is valued at USD 11.52 billion in 2026.

What is the forecast CAGR for United States AI data centers from 2026 to 2031?

The market is projected to grow at 29.77% CAGR through 2030.

Which data center type is expected to grow fastest in AI workloads?

Colocation facilities are forecast to expand at 31.22% CAGR as enterprises seek turnkey GPU-ready space.

Why are Tier IV facilities preferred for AI training?

Tier IV delivers 99.995% uptime, which safeguards multi-million-dollar model-training runs from costly interruptions.

How do CHIPS Act incentives affect data-center supply chains?

Federal grants are accelerating domestic production of AI chips and advanced packaging, giving US builders priority access to leading-edge components.

Page last updated on: