Thailand Artificial Intelligence (AI) Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

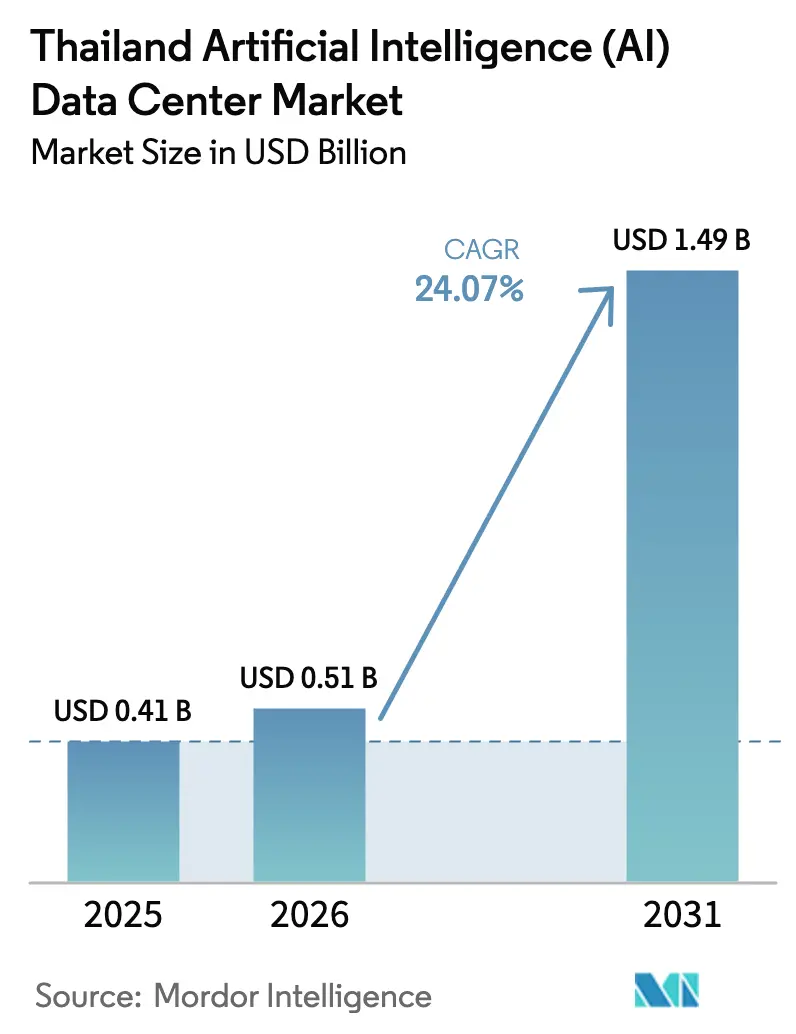

| Base Year Market Size (2025) | USD 0.41 Billion |

| Market Size (2026) | USD 0.51 Billion |

| Market Size (2031) | USD 1.49 Billion |

| Growth Rate (2026 - 2031) | 24.07% CAGR |

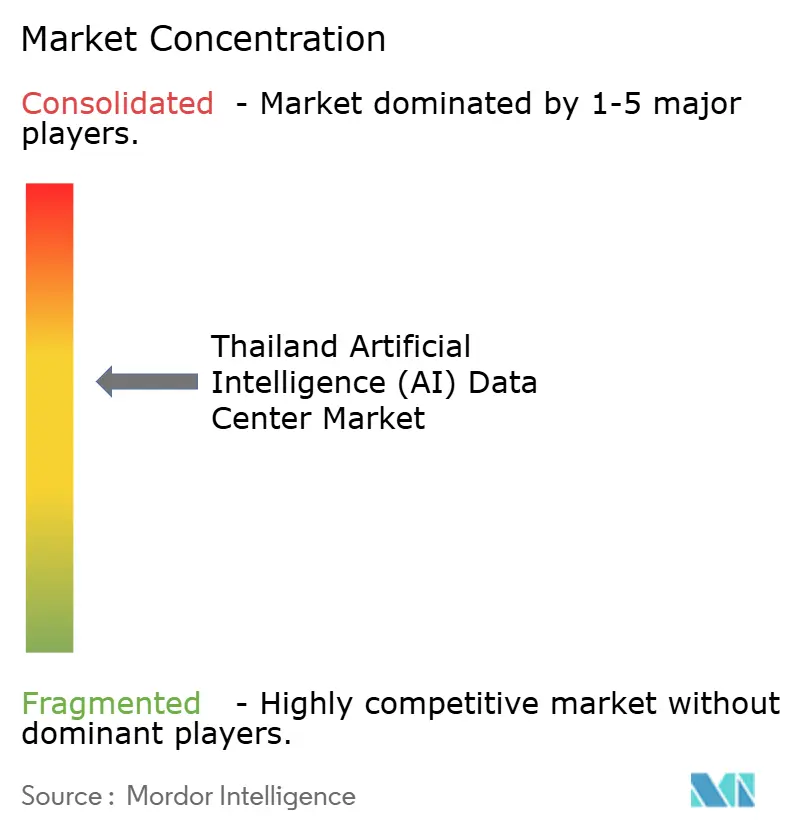

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Artificial Intelligence (AI) Data Center Market Analysis by Mordor Intelligence

The Thailand AI data center market size was valued at USD 0.41 billion in 2025 and estimated to grow from USD 0.51 billion in 2026 to reach USD 1.49 billion by 2031, at a CAGR of 24.07% during the forecast period (2026-2031). Robust policy commitment, geographic advantages, and rapidly growing enterprise AI adoption continue to propel the Thailand AI data center market on a steep growth curve. Government incentives under the Eastern Economic Corridor (EEC), foreign direct investment from hyperscalers, and nationwide 5G coverage are jointly lifting demand for low-latency infrastructure. Renewable power-purchase agreements enhance sustainability and price stability, while innovations in immersion and liquid cooling mitigate Thailand’s tropical heat. Competition remains intense as global hyperscalers and local champions race to deploy AI-ready capacity, particularly outside the grid-constrained Bangkok area.

Key Report Takeaways

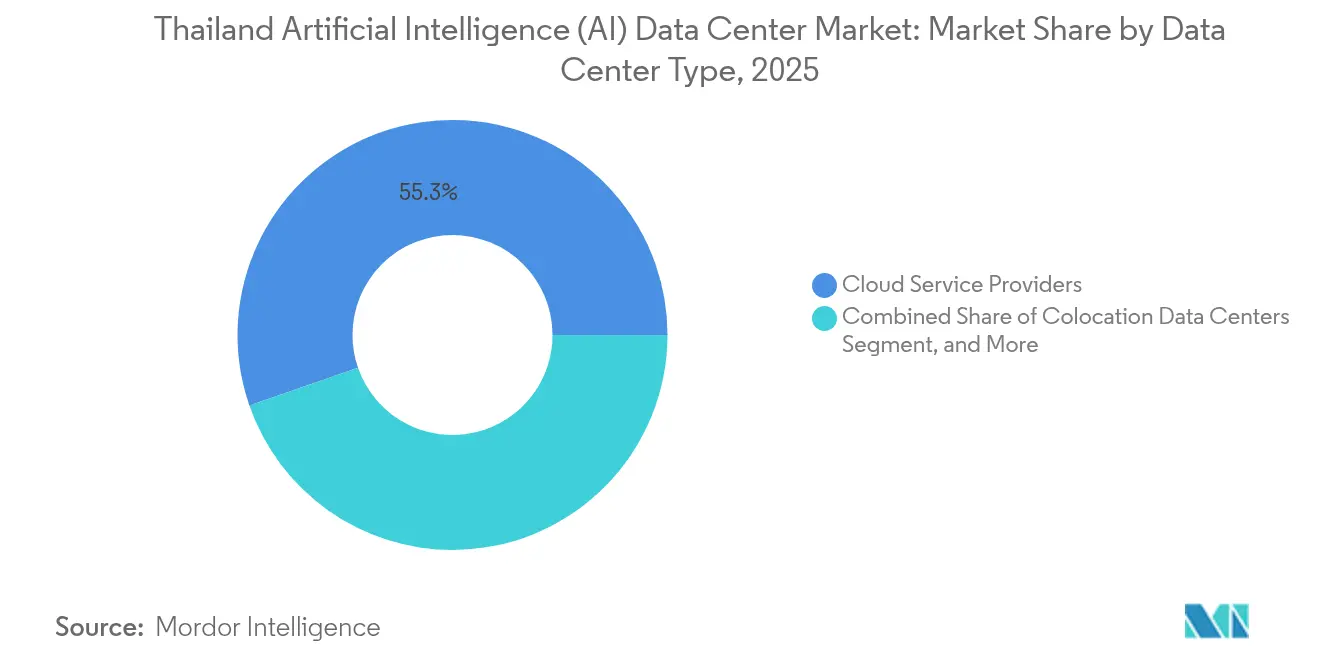

- By data center type, cloud service providers led the Thailand AI data center market with a 55.31% revenue share in 2025; colocation facilities are expected to advance at a 25.71% CAGR through 2031.

- By component, software captured 45.52% of the Thailand AI data center market share in 2025, while hardware is forecast to grow at a 25.49% CAGR to 2031.

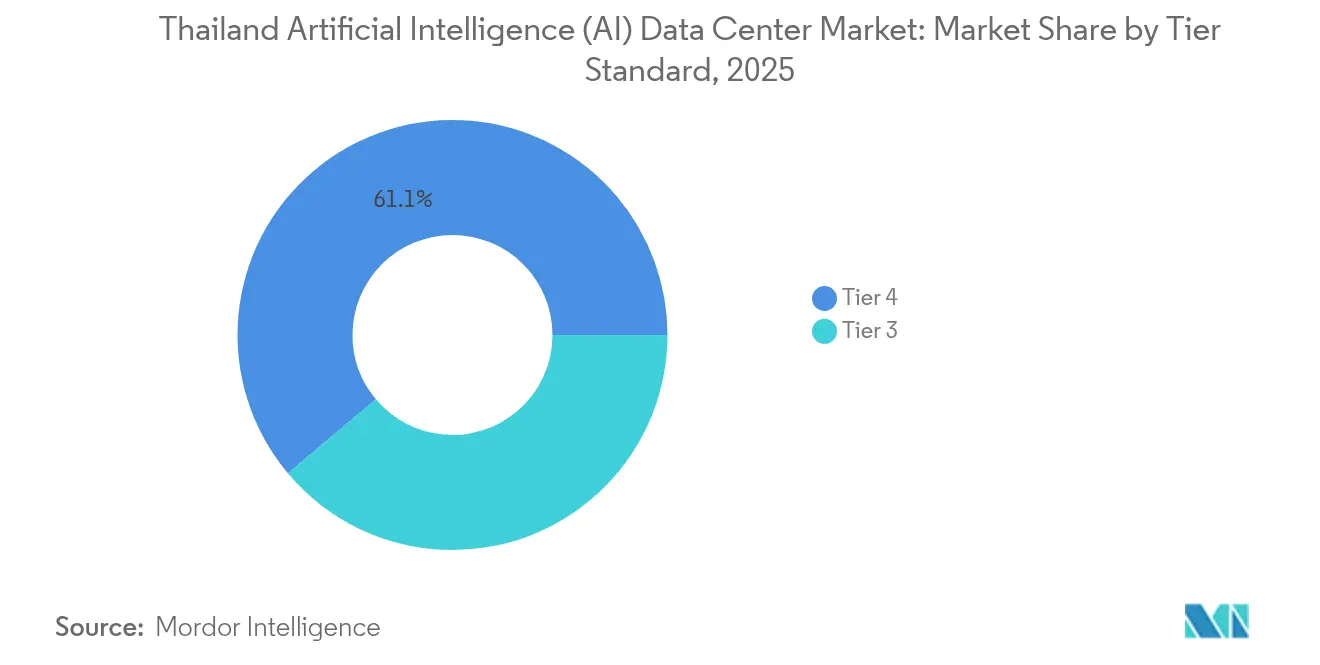

- By tier standard, Tier 4 sites accounted for 61.12% of deployments in the Thailand AI data center market in 2025; Tier 3 is the fastest-growing class, with a 26.18% CAGR through 2031.

- By end-user industry, IT and ITES accounted for 33.45% of the Thailand AI data center market size in 2025, whereas internet and digital media workloads are expected to surge at a 25.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand operates as part of an interconnected international environment rather than as a self-contained country level unit. The artificial intelligence (ai) data center market research by Mordor Intelligence places together all major developments across the globe within that wider frame.

Thailand Artificial Intelligence (AI) Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EEC incentives boosting hyperscale builds | +4.2% | Chonburi, Rayong, Chachoengsao | Medium term (2-4 years) |

| NBTC-backed 5G rollout enabling edge AI | +3.8% | Nationwide, early Bangkok, Chiang Mai, Phuket | Short term (≤ 2 years) |

| AI Thailand 2030 sovereign GPU budget | +3.1% | Nationwide | Long term (≥ 4 years) |

| Renewable PPA scheme for low-carbon AI | +2.7% | Solar-rich regions | Medium term (2-4 years) |

| Thai-language LLM momentum | +2.9% | Bangkok, tourist hubs | Short term (≤ 2 years) |

| Fintech KYC/AML mandates | +2.5% | Banking centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Eastern Economic Corridor incentives accelerating hyperscale builds

The Board of Investment has approved 37 digital-infrastructure projects worth THB 98.5 billion since 2024, granting eight-year corporate tax holidays for AI-optimized data centers exceeding 10 MW.[1]Board of Investment, “EEC Digital Infrastructure Investment Approvals,” boi.go.th These perks shift hyperscale interest from Bangkok to coastal provinces, where land banks and access to submarine cables are plentiful. Gulf Edge’s 100 MW Chonburi campus demonstrates cost savings, achieving parity with Singapore pricing while securing superior grid headroom. Amazon Web Services and Microsoft have also earmarked EEC parcels that offer renewable PPA eligibility. Investors value the corridor’s single-window permitting, which shortens building schedules from 24 months to approximately 14 months. This momentum anchors the Thailand AI data center market as a credible alternative to Singapore for regional workloads.

NBTC 5G rollout fuelling edge AI inference demand

The National Broadcasting and Telecommunications Commission aims to achieve 5G coverage in all 77 provinces by 2024, with a target of cutting wireless latency to below 20 milliseconds.[2]National Broadcasting and Telecommunications Commission, “5G Rollout Progress Report,” nbtc.go.th Autonomous mobility pilots, industrial IoT, and AR/VR services now require inference nodes within a 50 km radius of users. True Corporation’s tower-based micro-data centers pack 1–5 MW pods, supporting GPU clusters for real-time processing. Regulatory data-sovereignty clauses block off-shoring of mission-critical traffic, effectively localizing demand. The Thailand AI data center market consequently sees brisk deployment of Tier 3 edge sites that co-exist with Bangkok hyperscale cores. Over the next two years, edge capacity is forecast to outpace hyperscale builds on a percentage basis, although absolute megawatts still favor large campuses.

AI Thailand 2030 strategy driving sovereign GPU clusters

The government has set aside THB 25 billion for national GPU clouds, which will serve sensitive workloads such as citizen registries and Thai-language LLM training. Ministries must, by directive, favor domestic infrastructure for datasets categorized as restricted. The National AI Training Center already secured anchor tenancy agreements that de-risk private-sector buildouts. Instruction-financed clusters require rack densities of 50–100 kW, steering investment into liquid-cool designs. Talent-transfer stipulations tie foreign vendors to local universities, thereby enlarging the skilled labor pool. Over the long term, sovereign AI clusters are expected to secure a base load for the Thailand AI data center market, thereby cushioning operators against cyclical enterprise spending.

Renewable-PPA scheme enabling low-carbon AI workloads

In 2024, the Energy Regulatory Commission cleared 500 MW of direct renewable PPAs, with data centers securing the largest allocation. Operators now bypass state utilities, contracting for 15-year solar or wind deals that are bundled with battery storage. Amazon’s Rayong facility sources 100% of its energy from solar, meeting both customer ESG targets and internal carbon commitments. Levelized electricity costs fall by up to 15%, partially offsetting high cooling bills in tropical regions. The framework also accelerates the integration of green energy in rural provinces, indirectly expanding the viable site inventory for the Thailand AI data center market. Over the medium term, PPA-backed sites are expected to win hyperscaler workloads bound by science-based target mandates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bangkok grid-constraint (MEA) limits new above 30 MW connections | -2.8% | Bangkok metropolitan area | Short term (≤ 2 years) |

| Year-round humidity and 40°C peaks raise OPEX for cooling | -1.9% | National, particularly severe in central plains | Long term (≥ 4 years) |

| Multi-agency permitting lengthens construction timelines | -1.5% | National, with variations by province | Medium term (2-4 years) |

| Shortage of high-skill thermal engineers for above 30 kW/rack designs | -1.3% | National, concentrated in technical hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Bangkok grid constraint limiting hyperscale expansion

The Metropolitan Electricity Authority caps new connections above 30 MW unless operators finance the costly grid upgrades, which require a lead time of 18–24 months.[3]Metropolitan Electricity Authority, “Grid Capacity and Connection Limitations,” mea.or.th Data center investors, therefore, re-route projects to Rayong, Chachoengsao, or on-site microgrid setups. Hyperscalers test split-campus architectures, distributing 10–15 MW blocks across multiple substations. Some are located in industrial parks that already have heavy-industry allocations. Unless MEA accelerates transmission upgrades, Bangkok may cede its share of the Thailand AI data center market to EEC coastal zones during the next two years.

Tropical climate elevating cooling operational costs

An average humidity of 75% and summer peaks of 40 °C push the air-cool PUE to nearly 2.0, well above global best practices. AI racks that exceed 30 kW demand immersion or direct-to-chip liquid cooling. Early adopters such as Gulf Edge report sub-1.3 PUE but at higher capex for fluid tanks and heat exchangers. Operators also explore district-cooling tie-ins and seawater loops along the eastern seaboard. The climate factor acts as a permanent cost premium embedded in the Thailand AI data center market, influencing pricing strategy and site-selection calculus.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Cloud dominance meets colocation growth

Cloud providers accounted for USD 0.23 billion, equal to 55.31% of the Thailand AI data center market size in 2025. Their leadership stems from massive capex commitments and broad service catalogs that absorb complex AI workloads. Enterprises gravitate toward managed GPU clusters that eliminate infrastructure risk and speed model deployment. However, data-sovereignty rules and specialized latency requirements keep colocation relevant. The colocation slice is forecasted to grow at a 25.71% CAGR, faster than any other type, as firms adopt hybrid strategies that balance cloud agility with controlled environments for sensitive data.

Regional banking and telecom players deploy bare-metal GPU nodes within colocation rooms adjacent to cloud on-ramps, achieving near-cloud latency without relinquishing physical custody. Edge nodes, often built in modular increments of 1 MW, are positioned near 5G towers to support AR/VR and autonomous-vehicle inference. The resulting architectural diversity cements the Thailand AI data center market as a multi-modal ecosystem where hyperscale and micro-edge facilities coexist, each optimized for distinct workload classes.

By Component: Software leadership amid hardware acceleration

Software captured 45.52% of revenue in 2025 thanks to machine-learning platforms, model-training stacks, and subscription-based AI toolkits tailored for Thai-language use cases. Hardware, nonetheless, is racing ahead at a 25.49% CAGR as GPU clusters, high-speed switches, and liquid-cooling gear become mandatory for modern AI. Capital intensity rises because AI racks draw 10–20× the power of legacy IT.

Within software, machine-learning frameworks dominate, serving as the backbone for banking fraud detection and ecommerce recommendation engines. Computer vision is integral to electronics manufacturing QA lines, while NLP workloads gain traction in tourism chatbots. Services both managed and professional add steady revenue as enterprises seek integration expertise and compliance assurance. Hardware vendors partner with local system integrators to pre-configure Thai-language inferencing bundles, thereby deepening supply chain localization within the Thailand AI data center industry.

By Tier Standard: Tier 4 dominance with Tier 3 momentum

Tier 4 footprints represented 61.12% of deployments in 2025, reflecting enterprise appetite for maximum uptime when processing financial transactions or medical images. The configuration often includes 2 N+1 redundancy and 72-hour fuel reserves in line with Energy Regulatory Commission mandates. Meanwhile, Tier 3 sites grow at 26.18% CAGR, serving edge and cost-sensitive workloads that accept limited downtime in favor of rapid deployment and lower capex.

Operators now blend modular Tier 3 blocks into large campuses, achieving “Tier 3+” resilience via automated switchgear and lithium-ion UPS systems. This strategy aligns with AI inference workloads that can tolerate micro-outages through model replication. As a result, the Thailand AI data center market share may subtly rebalance toward Tier 3 over the forecast horizon, though Tier 4 remains essential for regulated industries.

By End-User Industry: IT sector leadership amid digital-media surge

IT and ITES firms accounted for 33.45% of the Thailand AI data center market size in 2025, leveraging AI for DevOps, analytics, and customer support bots. Banks follow close behind, compelled by KYC/AML rules. Internet and digital-media platforms, however, are the fastest risers with 25.22% CAGR, driven by surging ecommerce GMV and video-streaming personalization.

Healthcare is growing steadily as tele-radiology and medical tourism diagnostics migrate to AI-enhanced workflows. Manufacturing utilizes computer vision for defect detection and predictive maintenance analytics on factory equipment. Government, spurred by AI Thailand 2030, rolls out sovereign clusters for language translation and citizen-service chatbots. Collectively, diversified demand keeps utilization high across urban hyperscale hubs and provincial edge sites, broadening revenue resiliency for the Thailand AI data center market.

Geography Analysis

Bangkok remains the largest node in the Thai AI data center market, hosting the majority of Tier 4 capacity due to its dense enterprise clusters and proximity to submarine cables. However, grid caps and land scarcity curb future megawatt additions. Operators mitigate by adopting split-campus designs and virtual metro fabrics that link scattered pods into a logical availability zone.

The Eastern Economic Corridor leads expansion, buoyed by eight-year tax holidays and ready access to renewable energy. Large campuses in Rayong and Chonburi already secured more than 250 MW of announced capacity, underpinned by hyperscaler anchor tenants. Coastal siting lowers inlet water temperature, improving cooling efficiency by approximately 7% compared to inland Bangkok. Consequently, the Thailand AI data center market is geographically tilting toward these EEC provinces.

Northern and northeastern provinces play niche roles. Chiang Mai’s digital nomad scene drives edge nodes supporting tourism platforms, while Khon Kaen’s solar belt supplies renewable PPAs to distant campuses via new 500 kV lines. Nationwide 5G drives micro-data center cabins that localize inference traffic for autonomous vehicle test corridors. Over the forecast horizon, provincial capacity is expected to shift from under 10% today to roughly 18%, signaling a more distributed Thailand AI data center industry landscape.

The artificial intelligence (ai) data center market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Middle East and Africa, North America, and South America, along with detailed country-level analysis for India, China, Saudi Arabia, United States, Brazil, and South Africa.

Competitive Landscape

The Thailand AI data center market shows moderate concentration. Domestic incumbents, True Internet Data Center and STT GDC, retain sticky enterprise accounts and possess deep local permitting expertise. Yet hyperscalers Amazon Web Services, Google Cloud, and Microsoft Azure pledge more than USD 8 billion combined through 2030, dwarfing local capex.[4]Amazon Web Services, “Multi-Billion Dollar Investment Announcement,” aws.amazon.com The influx intensifies land-bank competition, particularly in EEC districts, where plots wider than 40 acres are scarce.

Operators differentiate via cooling innovation. Gulf Edge’s immersion-cool campus targets sub-1.3 PUE, while STT GDC pilots waste-heat reuse for district-cooling loops. Renewable PPAs have become table stakes; firms lacking green energy risk missing hyperscaler RFPs. Edge computing is the newest battleground. True Corporation’s 20-site edge mesh offers sub-20 ms latency, challenging AWS Local Zones, which are planned for 2026. Start-ups focusing on modular prefabs and AI-optimized networking may carve out a share, but must overcome financing obstacles in a capital-intensive arena.

Strategic alliances proliferate. Microsoft partners with the Provincial Electricity Authority on wind-powered microgrids, whereas Google teams with leading universities to train data center engineers. Foreign vendors often sign technology-transfer clauses, gradually narrowing capability gaps. Overall, competitive intensity elevates service quality and pushes the Thailand AI data center market toward global best-practice standards.

Thailand Artificial Intelligence (AI) Data Center Industry Leaders

True Internet Data Center Co., Ltd.

STT GDC (Thailand) Company Limited

NTT Global Data Centers (Thailand) Limited

SUPERNAP (Thailand) Co., Ltd.

Advanced Info Service Public Company Limited (AIS) – CBN Data Center

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Amazon Web Services committed an additional USD 2 billion through 2027 for new EEC availability zones and GPU clusters.

- January 2025: NTT Global received ISO 27001 certification for its Bangkok facility.

- December 2024: Google Cloud has opened a 30 MW Chonburi data center featuring liquid cooling and a direct renewable power purchase agreement (PPA) supply.

- December 2024: WHA Digital partnered with Schneider Electric on AI-grade power-management upgrades.

Thailand Artificial Intelligence (AI) Data Center Market Report Scope

The research encompasses the full spectrum of AI applications in data centers, covering hyperscale, colocation, enterprise, and edge facilities. The analysis is segmented by component, distinguishing between hardware and software. Hardware considerations include power, cooling, networking, IT equipment, and more. Software technologies under scrutiny encompass machine learning, deep learning, natural language processing, and computer vision. The study also evaluates the geographical distribution of these applications.

Additionally, it assesses AI's influence on sustainability and carbon neutrality objectives. A comprehensive competitive landscape is presented, detailing market players engaged in AI-supportive infrastructure, encompassing both hardware and software utilized across various AI data center types. Market size is calculated in terms of revenue generated by products and solutions providers in the market, and forecasts are presented in USD Billion for each segment.

| Cloud Service Providers |

| Colocation Data Centers |

| Enterprise / On-Premises / Edge |

| Hardware | Power Infrastructure |

| Cooling Infrastructure | |

| IT Equipment | |

| Racks and Other Hardware | |

| Software Technology | Machine Learning |

| Deep Learning | |

| Natural Language Processing | |

| Computer Vision | |

| Services | Managed Services |

| Professional Services |

| Tier 3 |

| Tier 4 |

| IT and ITES |

| Internet and Digital Media |

| Telecom Operators |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial IoT |

| Government and Defense |

| By Data Center Type | Cloud Service Providers | |

| Colocation Data Centers | ||

| Enterprise / On-Premises / Edge | ||

| By Component | Hardware | Power Infrastructure |

| Cooling Infrastructure | ||

| IT Equipment | ||

| Racks and Other Hardware | ||

| Software Technology | Machine Learning | |

| Deep Learning | ||

| Natural Language Processing | ||

| Computer Vision | ||

| Services | Managed Services | |

| Professional Services | ||

| By Tier Standard | Tier 3 | |

| Tier 4 | ||

| By End-user Industry | IT and ITES | |

| Internet and Digital Media | ||

| Telecom Operators | ||

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial IoT | ||

| Government and Defense | ||

Key Questions Answered in the Report

What is the 2026 value of the Thailand AI data center market?

The market is valued at USD 0.51 billion in 2026.

How fast is the Thailand AI data center market expected to grow?

It is forecast to expand at a 24.07% CAGR between 2026 and 2031.

Which data center type currently holds the largest share?

Cloud service providers lead with 55.31% share in 2025.

Which segment is projected to grow the quickest?

Colocation facilities are expected to post a 25.71% CAGR through 2031.

What geographic area is drawing the most new hyperscale investment?

The Eastern Economic Corridor provinces of Chonburi, Rayong, and Chachoengsao attract the bulk of emerging capacity.

How are operators addressing Thailand’s high-temperature environment?

They are deploying immersion and liquid cooling, which has pushed some facilities’ PUE below 1.3.

Page last updated on: