South America Pharmaceutical Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

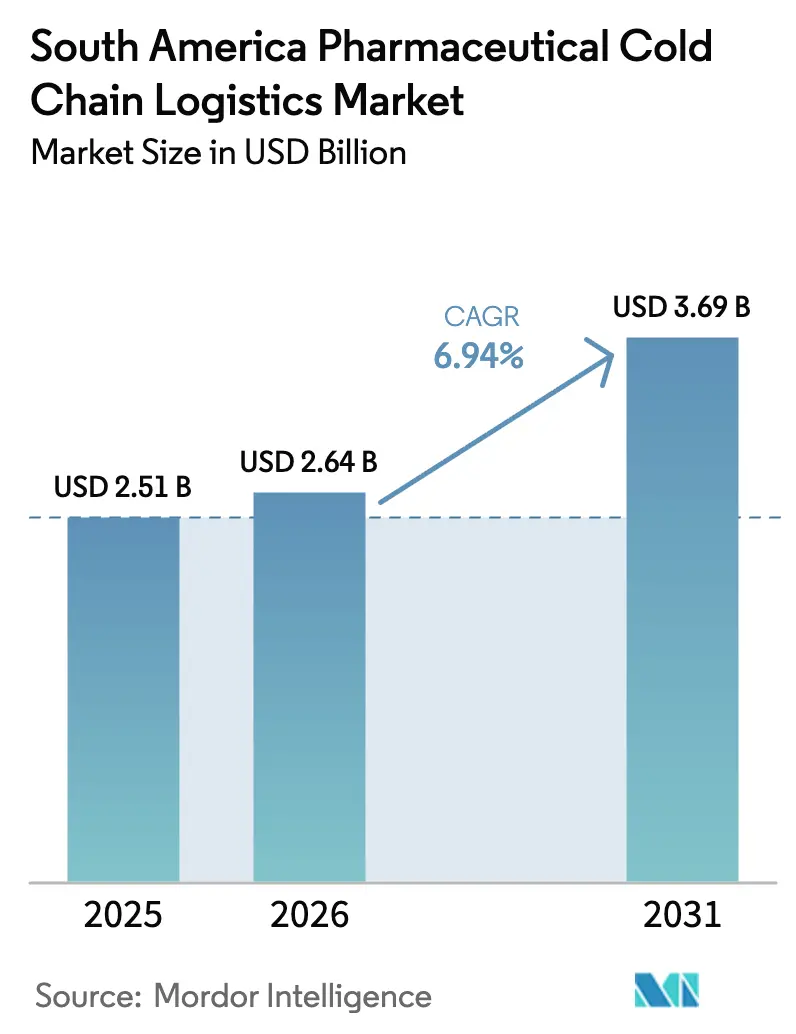

| Base Year Market Size (2025) | USD 2.51 Billion |

| Market Size (2026) | USD 2.64 Billion |

| Market Size (2031) | USD 3.69 Billion |

| Growth Rate (2026 - 2031) | 6.94% CAGR |

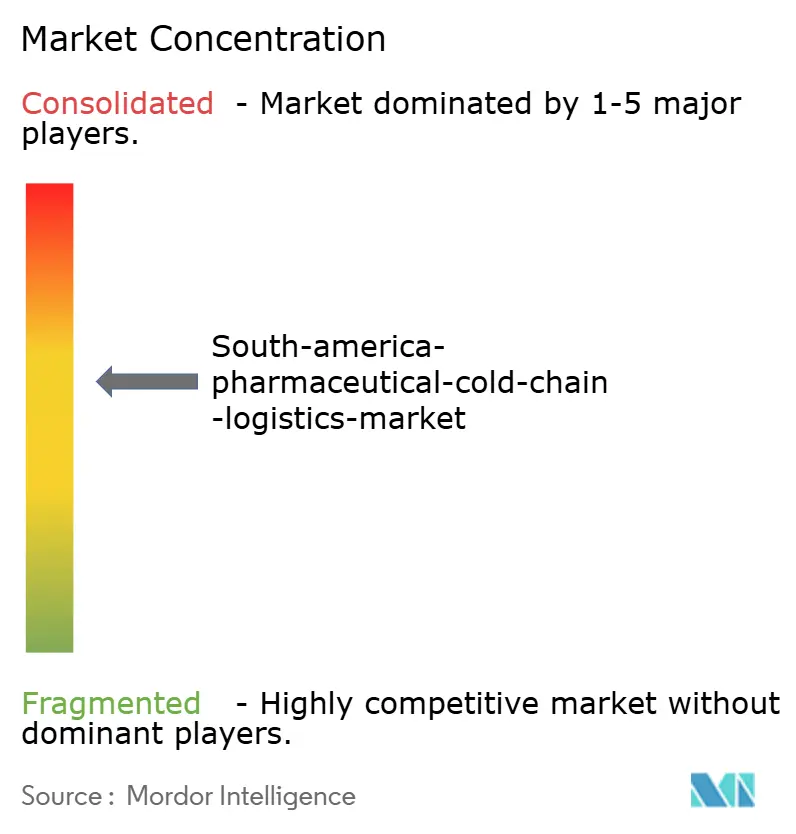

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Pharmaceutical Cold Chain Logistics Market Analysis by Mordor Intelligence

The Market size is expected to grow from USD 2.51 billion in 2025 to USD 2.64 billion in 2026 and is forecast to reach USD 3.69 billion by 2031 at 6.94% CAGR over 2026-2031.

Accelerating biologics approvals, government immunization drives, and wider IoT adoption are reshaping service-mix economics across South America. Brazil’s newly commissioned biologics plants are anchoring corridors that now stretch from Minas Gerais to Andean export gateways, while Colombia’s airport-centric expansion underwrites the region’s fastest growth. Multinational 3PLs dominate cross-border lanes thanks to dense certified-capacity networks, yet regional specialists retain rural and last-mile strongholds where municipal cold rooms and local licensing define access. Ultra-low storage remains scarce; only nine certified facilities span Brazil, Argentina, and Chile, creating a bottleneck that is fueling brownfield retrofits and M&A interest. Persistently high electricity and diesel prices, however, threaten margin integrity and accelerate solar and ammonia-refrigeration retrofits throughout the pharmaceutical cold chain logistics market.

Key Report Takeaways

- By service type, transportation accounted for 60.92% of the South America pharmaceutical cold chain logistics market share in 2025, while air freight is forecast to expand at an 8.74% CAGR through 2031.

- By temperature type, chilled storage accounted for 41.75% of the South America pharmaceutical cold chain logistics market size in 2025; the deep-frozen and ultra-low segments are advancing at a 7.48% CAGR through 2031.

- By product, branded drugs led with 51.84% revenue share in 2025, while specialty and orphan formulations will rise at a 7.36% CAGR through 2031.

- By end user, pharmaceutical manufacturers represented 46.18% of 2025 spending, whereas biotech and biosimilar producers are projected to post the fastest 7.61% CAGR through 2031.

- By Country, Brazil commanded 58.73% of the 2025 value, but Colombia is expected to log the quickest 8.98% country-level CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Pharmaceutical Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of biologics & vaccine pipelines | +1.8% | Brazil, Argentina, with spillover to Colombia and Chile | Medium term (2-4 years) |

| Expansion of pharma manufacturing hubs in Brazil & Argentina | +1.5% | Brazil (Sao Paulo, Minas Gerais), Argentina (Buenos Aires, Cordoba) | Long term (≥ 4 years) |

| Government-led immunization campaigns | +1.3% | Global South America, early gains in Brazil, Colombia, Peru | Short term (≤ 2 years) |

| Scaling 3PL partnerships for IoT-enabled last-mile delivery | +1.0% | Urban corridors in Brazil, Chile, and Colombia; gradual rural penetration | Medium term (2-4 years) |

| Mercosur GDP guideline harmonization | +0.6% | Argentina, Brazil, Paraguay, Uruguay | Long term (≥ 4 years) |

| Climate-change-driven demand for ultra-cold storage | +0.7% | Amazon basin (Brazil), coastal Argentina, Andean regions (Colombia, Peru) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Biologics & Vaccine Pipelines

Fiocruz executed seven technology-transfer contracts in 2024 covering adalimumab, rituximab, and trastuzumab, and each shipment now traverses 3,200 km corridors from Rio de Janeiro to Manaus. INVIMA cleared six biologic filings in 2025, triggering a USD 28 million cold-room retrofit program covering 140 Colombian municipalities. Chile’s CENABAST now excludes bidders lacking ISO 9001 and GDP proof, consolidating vaccine flows with DHL and Ransa.

A broader pipeline shift toward mRNA and cell therapies requires unprecedented temperature integrity. Only nine ultra-low sites are certified in Brazil, Argentina, and Chile, forcing Brazil’s Fiocruz to lease contingency space in Sao Paulo at premium tariffs while it adds six new -80 °C units by 2027[1].Fiocruz, “Ultra-Cold Expansion Plans,” portal.fiocruz.br Argentinian distributors have begun rationing vapor-phase nitrogen containers, and freight rates for -150 °C payloads have increased 18% since 2024, accelerating capital flows into dry-ice manufacturing and nitrogen-plant upgrades throughout the pharmaceutical cold chain logistics market.

Expansion of Pharma Manufacturing Hubs in Brazil & Argentina

Brazil is leveraging its position as the region’s largest pharmaceutical market and supportive initiatives such as the Economic-Industrial Health Complex and Nova Industria Brasil to attract major greenfield and brownfield investments in biologics, injectables, and formulation plants. Over 2025 - 2031, this will deepen Brazil’s role as both a domestic supply base and an export-oriented platform, particularly for high-value chronic disease and specialty products.

Argentina’s Plan de Desarrollo Productivo Farmaceutico grants 25% tax credits on plant CAPEX and prompted Laboratorios Richmond and Bago to unveil USD 40 million expansions in 2025. These brown- and green-field projects will lift outbound biologic tonnage 14% above 2024 baselines by 2026, pressuring warehouse vacancy below 4% in Buenos Aires and spurring 22,000 additional pallet leases across Sao Paulo, Cordoba, and Santiago. The investment wave is also re-routing intra-Mercosur lanes, with 3PLs adding temperature-controlled rail trials on the Santos Rondonopolis axis to balance northbound grain backhauls with pharma southbound loads.

Government-Led Immunization Campaigns

Brazil moved 18.3 million dengue doses to 521 high-risk municipalities via SIPNI, mandating continuous 2-8 °C telemetry. Peru’s 2025 HPV drive relied on GPS-tagged vans that sliced last-mile transit by 38 hours on average and lowered spoilage to 3.1%.

Chile sustained 94% pediatric vaccination by partnering with DHL’s LifeConEx for temperature-controlled routes into the Atacama and Aysen regions. Collectively, these campaigns embed high-frequency transit rhythms into the pharmaceutical cold chain logistics market, raising baseline throughput and shortening replenishment cycles.

Scaling 3PL Partnerships for IoT Last-Mile Delivery

UPS-Bomi fitted 320 vans with 15-minute interval loggers that auto-alert on excursions beyond 8 °C and allow pharmacies to reject compromised loads. Maersk’s blockchain pilot across Santos, Valparaíso, and Callao cut documentation errors by 41% and became a key selling point in its 2025 vaccine-distribution win.

CEVA introduced unattended 2-8 °C lockers in Sao Paulo that enable after-hours pharmacy pickup, potentially scaling to 140 Brazilian cities by 2027, subject to ANVISA green lights. Kuehne + Nagel’s PharmaChain processed 2.3 million shipments in 2025 with 89% GDP compliance, up from 76% in 2023, after adding predictive delays-avoidance algorithms. Colombia’s ICT ministry subsidizes 40% of IoT hardware for rural-serving 3PLs, lowering entry barriers for mid-tier providers and diffusing visibility standards across the pharmaceutical cold chain logistics industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited rural cold-chain infrastructure | -0.9% | Amazon basin (Brazil), Pampas (Argentina), Andean highlands (Peru, Colombia) | Medium term (2-4 years) |

| High energy & fuel-linked operating costs | -1.2% | Argentina, Brazil, Chile; acute in diesel-dependent road corridors | Short term (≤ 2 years) |

| Scarcity of accredited calibration labs for data logger validation | -0.4% | Brazil (outside São Paulo, Rio), Argentina (outside Buenos Aires), Peru, Colombia | Medium term (2-4 years) |

| Flood-related route disruptions across the Amazon & Pampas corridors | -0.6% | Amazon basin (Brazil, Peru), Parana-Paraguay river system (Argentina, Paraguay) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Rural Cold-Chain Infrastructure

Brazil’s Amazon region frequently airlifts vaccines at USD 450 per mission, five times standard refrigerated‑truck costs, because extreme distances, seasonal flooding, and limited roads make ground distribution unreliable. These flights typically depart from hubs like Manaus to small airstrips or river ports, adding handling steps and cold‑chain risk versus standard truck routes. Colombia lifted rural coverage to 38% with solar fridges but still relies on ice‑box transport for 62% of remote deliveries, effectively excluding mRNA products that need stable ultra‑cold conditions. Both countries are therefore expanding solar‑powered cold rooms and piloting new last‑mile technologies to narrow access gaps without letting logistics costs spiral.

High Energy & Fuel-Linked Operating Costs

Sao Paulo peak charges hit BRL 0.92/kWh, motivating SuperFrio to install 2.8 MW of rooftop solar across six sites, trimming bills 16% and enabling 8% tariff savings for customers. Argentina’s diesel surged to ARS 1491 (USD 1.03) per liter in late 2025, and refrigerated-haul rates jumped 5.58%, pressuring pharmaceutical manufacturers to absorb freight mark-ups to prevent stocking gaps. LNG shortages raised Chilean power prices by 16%. Friozem is spending USD 8 million on ammonia systems expected to cut kWh consumption 22% by 2026

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Air Freight Gains Altitude

The South America pharmaceutical cold chain logistics market share is dominated by the transportation segment, which accounted for 60.92% of total revenue in 2025. Air transportation is projected to surge at a CAGR of 8.74% between 2026 and 2031, the fastest among all service lines, as pharma distributors prioritize speed and temperature integrity. LATAM Cargo committed USD 22 million in mid-2025 to retrofit 18 Airbus A320 and Boeing 767 freighters with active containers and to install 12 cool dollies across its São Paulo (Viracopos) and Santiago hubs, targeting a 35% tonnage jump by 2027.[2]LATAM Airlines Group, “Pharma Retrofit Investment,” latamairlinesgroup.net

Aerolineas Argentinas has also advanced its competitiveness by completing GDP certification at Ezeiza and equipping four Boeing 737‑700 freighters with real-time temperature loggers, enabling it to challenge DHL and UPS on cross-border lanes to Uruguay and Paraguay. While transportation remains the market leader, the sector faces fuel-inflation pressures and flood-related detours along the Amazon and Parana River corridors, prompting shippers to adopt air-road intermodal strategies. In warehousing, Lineage and Americold control about 48% of certified pallet slots in Brazil and added 18,000 positions between 2024 and 2025, while at sea, Maersk and Hamburg Süd maintain the only pharma-grade reefer services, mainly handling bulk API flows to Caribbean destinations.

By Temperature Type: Deep-Frozen Segment Accelerates

In the South America pharmaceutical cold chain logistics market share, the chilled segment accounted for 41.75% of revenue in 2025, driven by the storage needs of insulin and conventional monoclonal antibodies. However, the deep-frozen and ultra-low (-20 °C and below) category is set to expand at a 7.48% CAGR, outpacing the chilled and ambient segments, as rising mRNA and CAR‑T therapies require -80 °C custody. Fiocruz installed two ‑80 °C freezer units in 2024 and plans to install six more by 2027, each adding 12,000‑vial capacity and requiring weekly dry‑ice replenishment contracts.

Argentina’s mAbxience will invest USD 18 million to double its ultra-cold storage by 2027 after securing three mRNA pipeline candidates. The frozen storage segment (-18 °C to 0 °C) ranks second by earnings, supporting plasma-derived and hormone injectable products. Meanwhile, Chile’s ISP mandated ‑150 °C vapor-phase nitrogen conditions for all CAR‑T imports in 2025, effectively limiting last‑mile deliveries to DHL’s LifeConEx and Kuehne + Nagel’s PharmaChain networks.

By Product: Specialty & Orphan Drugs Reshape Demand

In the South America pharmaceutical cold chain logistics market share, branded drugs remained the largest product segment in 2025, accounting for 51.84% of total revenue, though their dominance is projected to ease by four percentage points by 2031 as biosimilars gain ground. Specialty and orphan formulations are expected to expand at the fastest pace, with a 7.36% CAGR, reflecting accelerating investment in advanced and rare-disease therapies. INVIMA issued eight orphan designations in 2025 and allocated USD 14 million to subsidize logistics for therapies serving fewer than 500 patients that require 2-8 °C chain continuity.

In Argentina, ANMAT fast-tracked five CAR‑T cell therapies, each valued at over USD 300,000 and requiring dual-logger, ‑150 °C vapor-phase shipping. Meanwhile, Peru’s national rare-disease registry identified 1,800 enzyme therapy candidates, spurring Ransa to establish a dedicated cold corridor that reduced transit times from 96 hours to 36 hours and cut product wastage by seven percentage points.

By End User: Biotech Manufacturers Drive Growth

In the South America pharmaceutical cold chain logistics market share, manufacturers accounted for the largest share at 46.18% of revenue in 2025, though their expansion is expected to moderate as direct-to-hospital channels rise. Biotech and biosimilar companies are projected to post the fastest growth at a 7.61% CAGR, driven by the escalating production of cell and gene therapies that demand stringent temperature assurance. Eurofarma’s 2025 service-level agreement with PharmaChain highlights this shift, enforcing zero temperature excursions and a 99.5% on‑time performance threshold as the new industry standard.

Hospitals and retail pharmacies followed closely, benefitting from in‑store vaccination and increased biologic dispensing. Wholesalers, however, are likely to lose two percentage points of share by 2031 amid expanding direct‑distribution networks and the adoption of data‑driven control towers. In Brazil, Raia Drogasil reinforced its cold‑chain readiness by equipping 1,200 outlets with medical refrigerators in 2025 and partnering with UPS‑Bomi for nightly restocks, ensuring consistent 2-8 °C compliance.

Geography Analysis

Brazil anchored 58.73% of the 2025 pharmaceutical cold chain logistics market share, buoyed by Viracopos and Guarulhos airports moving 1.8 million kg of pharma air freight in the year, a 14% rise over 2024. SuperFrio operates 120,000 pallet positions across 18 GDP-certified sites and leveraged 2.8 MW of rooftop solar to cut storage tariffs by 8% in Sao Paulo’s Zona Leste corridor[3]SuperFrio Logística Frigorificada, “Solar Implementation Report,” superfrio.com.br . JSL’s Fadel Logistica Fria manages 340 telemetry-enabled trucks that lifted 2-8 °C compliance to 94% in 2025. Friozem’s USD 8 million ammonia retrofit will shave electricity by 22% at Santos and Rio warehouses by 2026. Floods on BR-319 forced a ten-day helicopter relief in Q1-2025, elevating per-dose logistics from USD 2.40 to USD 18.60.

Colombia is projected to register the fastest 8.98% CAGR through 2031. El Dorado airport’s 8,500 m² GDP extension raised monthly pharma throughput 41% to 320,000 kg. The Ministry of Health budgeted USD 28 million for 140 cold-room retrofits, slicing vaccine wastage to 2.8% in 2025. DHL opened a 12,000 m² -80 °C-ready warehouse in Bogota’s Fontibon district in December 2024. Ransa’s Coordinadora JV targets a 15% Colombian share by 2027, aided by a 1,100-municipality delivery grid.

Argentina, Chile, and Peru together account for more than 25% of the value, yet navigate divergent challenges. Diesel at ARS 850/liter inflated refrigerated-haul tariffs 28% in Argentina; Andreani’s route-optimization trimmed empty miles 11% to blunt the blow. Peru’s Ransa-run vaccine network cut wastage from 8.4% in 2024 to 3.1% in 2025 via GPS-tracked vans. Remaining South American markets-Ecuador, Bolivia, Paraguay, Uruguay, Venezuela hold 8% share and will grow at a 7.2% CAGR as Quito and Asuncion modernize GDP protocols

Competitive Landscape

Five multinationals-DHL Supply Chain, UPS Healthcare, Kuehne + Nagel, DSV, and CEVA Logistics control about 50% of certified GDP capacity, wielding scale economies and integrated sea-air-road service portfolios that attract high-value biologic flows. Each has extended IATA CEIV Pharma accreditations beyond primary hubs to secondary cities such as Medellín, Curitiba, and Guayaquil, reinforcing quality leadership while capturing incremental pharmaceutical cold chain logistics market share.

Regional contenders remain formidable in rural and intra-country lanes. Peru’s Ransa, Argentina’s Andreani, and Brazil’s SuperFrio and JSL’s Fadel Logistica Fria combine dense municipal cold-room networks with local regulatory expertise, allowing on-time ratios above 94% for last-mile vaccine deliveries. Energy self-generation, seen in SuperFrio’s solar rollout and Friozem’s ammonia shift, is becoming a differentiator as power costs escalate.

Technology-centric entrants such as Maersk’s blockchain platform and CEVA’s autonomous 2-8 °C lockers represent emerging competitive vectors. Maersk trimmed documentation errors by 41% and won a three-year vaccine contract, while CEVA’s locker network could reach 140 Brazilian cities by 2027, pending ANVISA approval[4]Maersk, “Annual Report 2025,” maersk.com. Lineage and Americold accelerate bolt-on acquisitions to tie up ultra-low warehouse real estate, anticipating mRNA therapy scale-up and aiming to lift their combined pharmaceutical cold chain logistics industry footprint beyond food heritage.

South America Pharmaceutical Cold Chain Logistics Industry Leaders

DHL Supply Chain & Global Forwarding

UPS Healthcare / Bomi Group

DSV

FedEx Temperature Controlled Solutions

Kuehne + Nagel PharmaChain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Eurofarma began commercial filgrastim production at its USD 120 million Montes Claros plant, shipping 800,000 syringes monthly via PharmaChain

- January 2026: Friozem announced a USD 8 million ammonia retrofit for Santos and Rio warehouses, targeting 22% energy savings

- December 2025: Biomm’s USD 90 million insulin complex in Nova Lima entered phase-1 output, projecting 18 million vials by 2027

- December 2025: CEVA piloted unattended 2–8 °C lockers in São Paulo’s Zona Sul district

South America Pharmaceutical Cold Chain Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Warehousing and Distribution | |

| Value-Added Services and Others |

| Chilled ((0–5 °C)) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

| Generic Drugs |

| Branded Drugs |

| Specialty / Orphan Drugs |

| Pharmaceutical Manufacturers |

| Biotech & Biosimilar Manufacturers |

| Hospitals & Retail Pharmacies |

| Healthcare Distributors & Wholesalers |

| Others |

| Argentina |

| Brazil |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Service Type | Transportation | Road |

| Rail | ||

| Sea | ||

| Air | ||

| Warehousing and Distribution | ||

| Value-Added Services and Others | ||

| By Temperature Type | Chilled ((0–5 °C)) | |

| Frozen (-18–0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Product | Generic Drugs | |

| Branded Drugs | ||

| Specialty / Orphan Drugs | ||

| By End User | Pharmaceutical Manufacturers | |

| Biotech & Biosimilar Manufacturers | ||

| Hospitals & Retail Pharmacies | ||

| Healthcare Distributors & Wholesalers | ||

| Others | ||

| By Country | Argentina | |

| Brazil | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America |

Key Questions Answered in the Report

How large will the pharmaceutical cold chain logistics market be by 2031?

Forecasts place the market at USD 3.69 billion by 2031 on a 6.94% CAGR trajectory.

Which sub-segment is expanding fastest by service type?

Air freight is projected to grow at an 8.74% CAGR through 2031, outpacing road, sea, and warehousing.

Why is ultra-low storage capacity considered a bottleneck?

Only nine certified facilities support –80 °C or colder custody across Brazil, Argentina, and Chile, limiting scale-up for mRNA and CAR-T therapies.

What is the main cost pressure facing 3PLs?

An 18% regional rise in industrial electricity and sharp diesel inflation are compressing cold-storage and haulage margins.

Which country offers the highest growth opportunity?

Colombia, driven by El Dorado airport’s GDP expansion and government cold-room grants, is set to post an 8.98% CAGR to 2031.

How are operators mitigating excursion risk on last-mile routes?

Widespread deployment of IoT sensors, predictive analytics, and blockchain tracking now allows shippers to detect temperature breaches in real time and reroute inventory proactively.

Page last updated on: