India Chemical Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

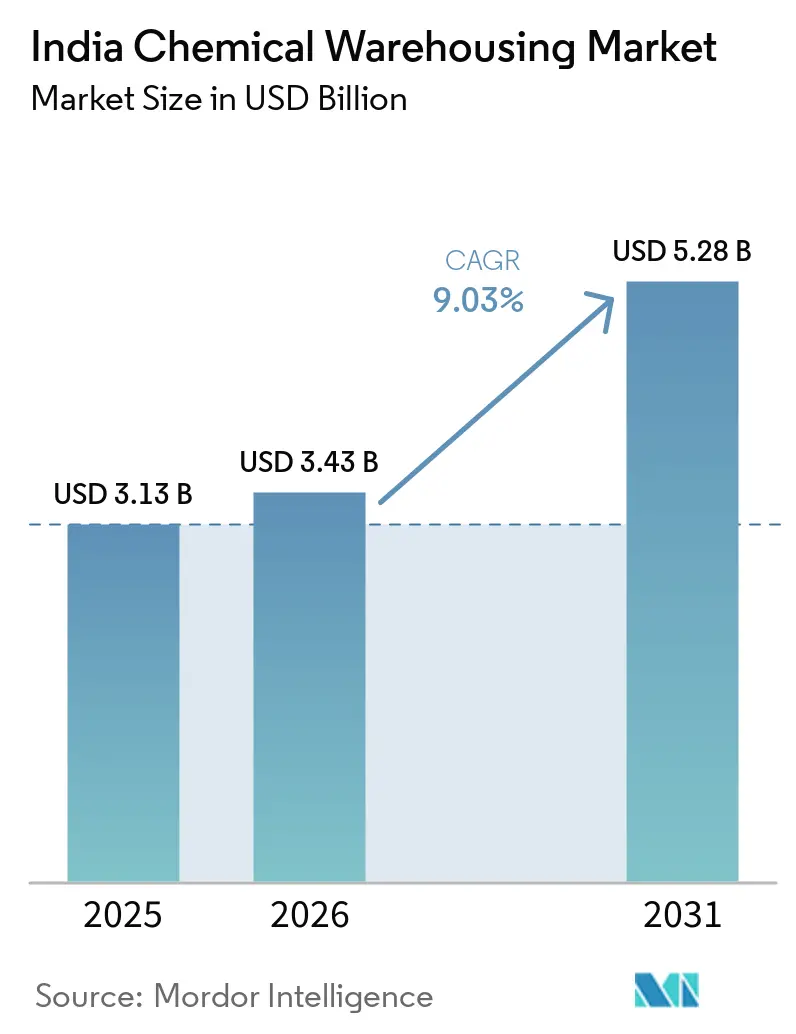

| Base Year Market Size (2025) | USD 3.13 Billion |

| Market Size (2026) | USD 3.43 Billion |

| Market Size (2031) | USD 5.28 Billion |

| Growth Rate (2026 - 2031) | 9.03% CAGR |

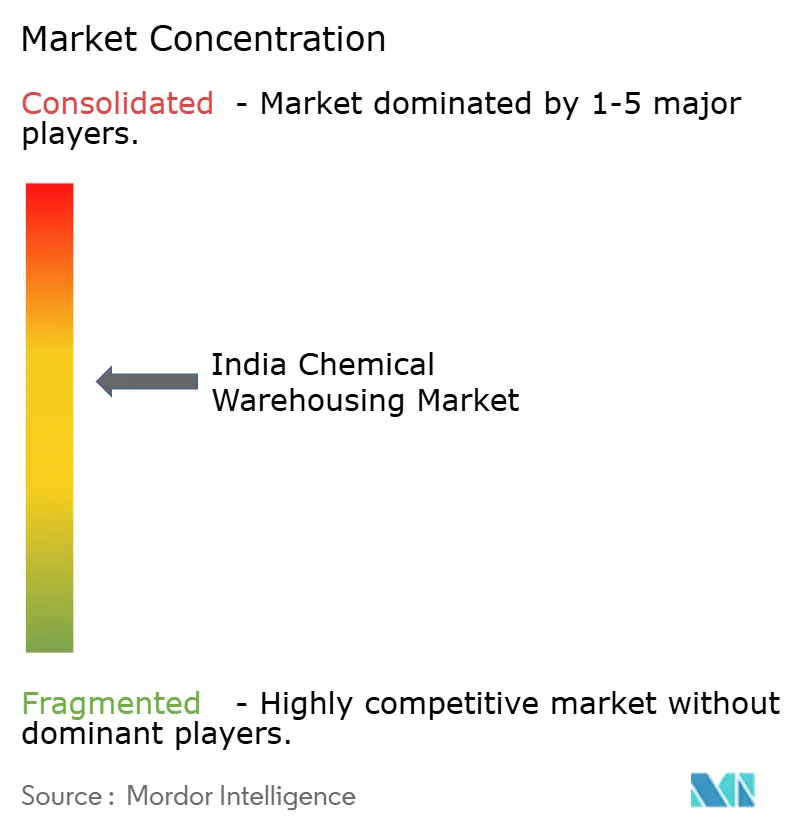

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Chemical Warehousing Market Analysis by Mordor Intelligence

The India chemical warehousing market size is expected to increase from USD 3.13 billion in 2025 to USD 3.43 billion in 2026 and reach USD 5.28 billion by 2031, growing at a CAGR of 9.03% over 2026-2031.

Inventory expansion is being fueled by a USD 20 billion specialty-chemical capital-expenditure wave, the National Logistics Policy’s cost-reduction targets, and Dedicated Freight Corridors that shorten port-to-hinterland transit. Federal funding for three new Chemical Parks and a five-year, USD 2.38 billion Carbon Capture, Utilization and Storage program is trimming compliance costs for operators that invest in low-carbon, shared infrastructure. Pharmaceutical demand for temperature-controlled hazardous-material (HAZMAT) space, lithium-ion battery raw-material imports, and tighter Petroleum and Explosives Safety Organisation (PESO) rules are reshaping site-selection decisions. Established logistics groups such as Aegis, Allcargo, and DHL are consolidating port-proximate capacity, yet fragmentation among regional third-party logistics (3PL) firms remains pronounced as small and medium enterprises seek flexible lease terms. Near-term risks center on a 15-30% jump in marine-cargo war-risk premiums and draft limitations on inland waterways, both of which squeeze operator margins.

Key Report Takeaways

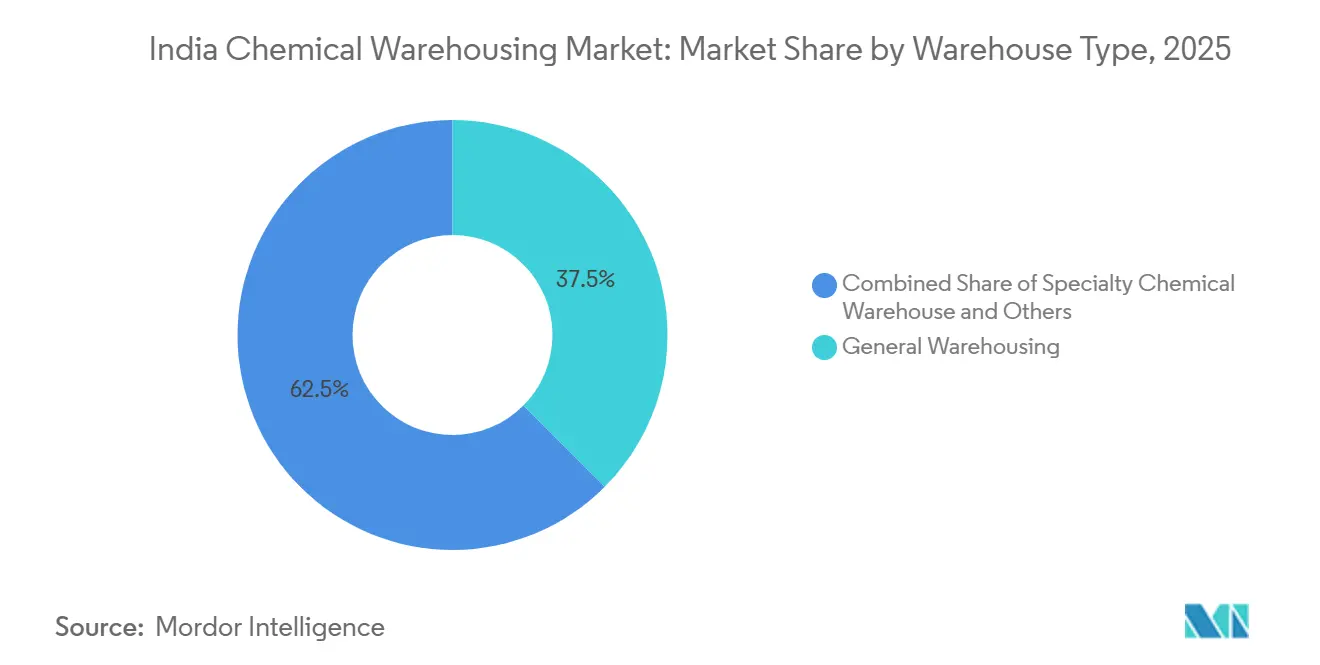

- By warehouse type, general warehousing led with 37.47% of India chemical warehousing market share in 2025, temperature-controlled chemical warehouses are projected to post the fastest growth at a 12.11% CAGR through 2031.

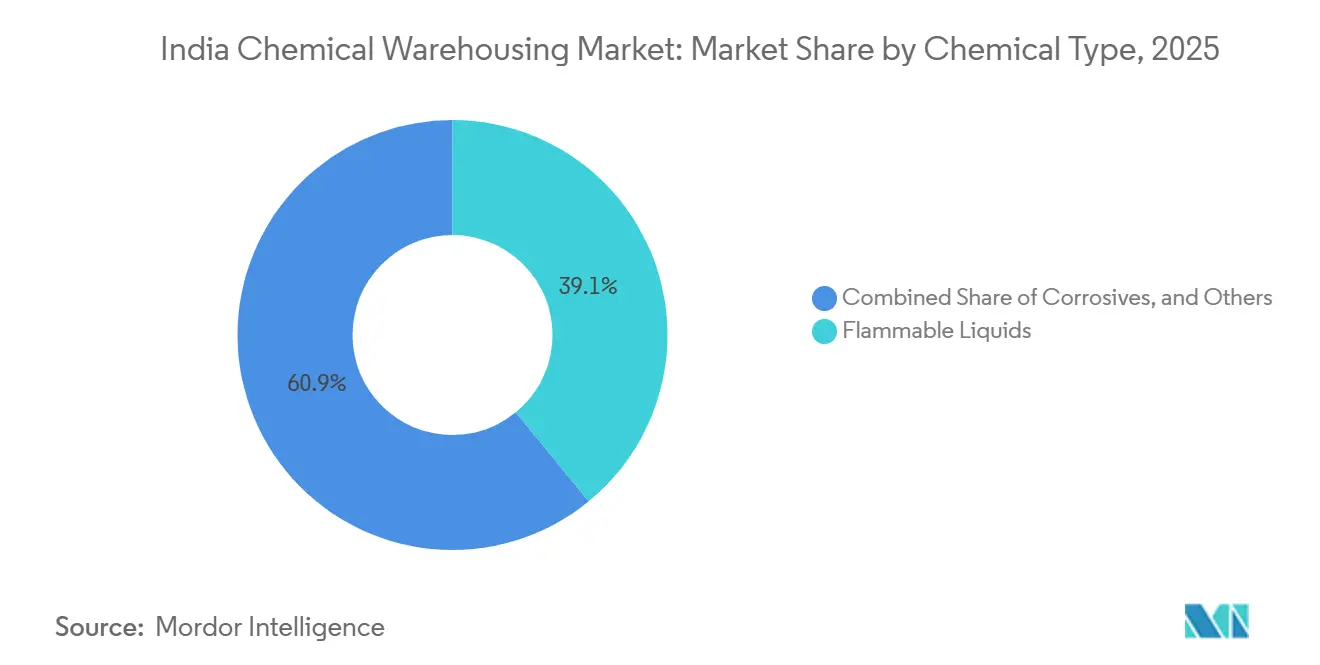

- By chemical type, flammable liquids held 39.08% share of the India chemical warehousing market size in 2025, toxic substances storage is forecast to expand at a 12.02% CAGR over 2026-2031.

- By end-user, basic chemicals manufacturing accounted for 35.87% share in 2025, while pharmaceuticals and life sciences will register the fastest 14.91% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Understanding the full system requires moving beyond India boundaries into a wider international view. Mordor Intelligence captures the global chemical warehousing market scope in its worldwide coverage.

India Chemical Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| USD 20 Billion Specialty-Chemical CAPEX Wave (2024-28) | +2.1% | National, especially Gujarat and Maharashtra | Medium term (2-4 years) |

| National Logistics Policy Tax Holidays for Grade A HAZMAT Facilities | +1.5% | National, early gains in port clusters | Long term (≥ 4 years) |

| Bharatmala Freight-Corridor Rail Sidings Unlocking Bulk-Chemical Reach | +1.8% | National, spillover to interior states | Medium term (2-4 years) |

| Lithium-Ion Battery Raw-Material Imports Boost Class 3 & 8 Storage | +1.3% | Gujarat, Maharashtra, West Bengal ports | Short term (≤ 2 years) |

| Agro-Pesticide PLI Scheme Raising Regional Warehouse Demand | +0.9% | Gujarat, Andhra Pradesh, Karnataka | Long term (≥ 4 years) |

| QR-Based Hazardous-Waste E-Tracking (NHWIS-2025) Speeds WMS Adoption | +0.7% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

USD 20 Billion Specialty-Chemical CAPEX Wave (2024-28)

A multi-year investment surge is reshaping regional warehouse demand as producers back-integrate and chase export growth Godrej Industries, for example, is injecting USD 59.5 million into its Valia plant to lift capacity to 275,000 tons per year and add specialty alcohol lines. Similar outlays by Tanfac in Tamil Nadu and Tata Chemicals in Ramanathapuram are aligning new plants with port-centric logistics corridors. These expansions draw the India chemical warehousing market toward Hazira, Dahej, and Cuddalore, where rail sidings and coastal shipping compress dwell times. Operators are simultaneously exposed to raw-material volatility and possible tariff shifts, prompting cautious phase-wise spending. Industry forecasts that India’s chemicals sector could touch USD 300 billion by 2028 bolster the long-term case for additional HAZMAT capacity.

National Logistics Policy Tax Holidays for Grade A HAZMAT Facilities

State-level industrial policies are offering tax incentives that cut the effective cost of capital for Grade A warehouses that comply with the National Building Code fire-safety schedule and PESO licensing. At the federal level, the Unified Logistics Interface Platform now links 36 government systems to significantly shrink port document cycles and reduce dwell times.[1]Press Information Bureau, “Unified Logistics Interface Platform Progress Update,” Pib.gov.inA new e-Handbook from the Warehousing Association of India has consolidated codes and standards, lowering search costs for developers. Operators such as Allcargo have responded by rolling out multi-hazard complexes with in-rack sprinklers and foam suppression, while three federally funded Bulk Drug Parks socialize part of the compliance burden.[2]Warehousing Association of India (WAI). "Warehousing Handbook 2025." DPIIT and WAI, 2025. Conversely, the late-2025 rollback of 20 Chemical Quality-Control Orders has lightened certification overhead, temporarily widening operating margins for smaller 3PL providers.

Bharatmala Freight-Corridor Rail Sidings Unlocking Bulk-Chemical Reach

Completion of the Eastern and Western Dedicated Freight Corridors is shaving door-to-door lead times, letting warehouses in Rajasthan and Madhya Pradesh serve northern buyers that once relied on congested road routes. Shivtek Spechemi’s twin greenfield sites, one near Hazira, the other near Jaipur, explicitly cite rail connectivity as a cost lever that can cut per-ton freight charges by double digits. The corridors also integrate seamlessly with coastal ports, allowing liquid-bulk transshipment without multiple handling points. Infrastructure bottlenecks persist around berth congestion and hazardous-goods stacking, yet the modal shift to rail is anchoring long-term location strategies within the India chemical warehousing market.

Lithium-Ion Battery Raw-Material Imports Spurring Class 3 & 8 Storage Demand

India’s USD 2.15 billion Advanced Chemistry Cell incentive is scaling domestic battery factories, but cathode precursors and electrolyte salts remain import-dependent. PESO rules for flammable and corrosive liquids are pushing developers toward purpose-built Class 3 and Class 8 blocks at JNPT, Kandla, and Haldia. Aegis Logistics has already launched new cryogenic berths capable of handling battery-grade chemicals, and DHL plans two Battery Logistics Centers of Excellence by 2026. Stricter export controls on used battery black mass will add a recycling-logistics layer that requires segregated bays and advanced fire-suppression media.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Marine-Cargo Insurance Surcharges on Bulk Chemicals | –1.2% | All major ports | Short term (≤ 2 years) |

| Mandatory BIS Quality-Control Orders Raising Compliance Costs | –0.3% | National | Short term (≤ 2 years) |

| Short Supply of PFAS-Free Fire-Suppression Systems | –0.5% | New Grade A builds | Medium term (2-4 years) |

| Variable Inland-Waterway Draft Hindering Barge Logistics | –0.8% | Ganga-Bhagirathi-Hooghly stretch | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Marine-Cargo Insurance Surcharges on Bulk Chemicals

War-risk premiums on Red Sea and Persian Gulf routes climbed 15-30% in 2025, lifting the landed cost of imported solvents and raising collateral requirements for letters of credit.[3]Insurance Regulatory and Development Authority of India, “Marine Cargo Premium Trends 2025,” Irdai.gov.inA single USD 5.95 million cargo now pays nearly USD 7,800 in total cover, eroding throughput margins for India chemical warehousing market operators that rely on import-export flows. Aegis has hedged part of this exposure via long-term charter-party deals, but smaller 3PLs face working-capital squeezes that could delay expansion. Deep-draft projects such as Vadhavan Port promise partial relief post-2029, yet until then, premium volatility remains a drag on capital deployment.

Mandatory BIS Quality-Control Orders Raising Compliance Costs

New Bureau of Indian Standards (BIS) orders covering polymers and intermediates have forced warehouses to upgrade test labs and certification protocols, adding significant operational cost layers. November 2025 rollbacks for 20 chemicals have eased the burden slightly, but future reinstatements remain possible PIB.GOV.IN. Operators serving multiple product classes must therefore maintain flexible compliance budgets, dampening near-term earnings within the India chemical warehousing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Grade A Facilities Capture Premium Demand

General warehousing captured 37.47% of the India chemical warehousing market in 2025, serving bulk commodity flows that need only ambient storage. Despite this lead, temperature-controlled chemical warehouses will register a brisk 12.11% CAGR through 2031 due to biologics, active pharmaceutical ingredients, and temperature-sensitive catalysts. Operators are adding dedicated cold rooms, glycol chillers, and insulated dock doors to meet Good Distribution Practice requirements. Allcargo’s 160,000-square-foot Uran site illustrates the trend, blending sub-25 °C chambers with explosion-proof lighting as part of a broader national network that serves more than 70 companies.

Specialty chemical warehouses configured for inert-gas blanketing, HEPA filtration, and ISO 9001 workflows have emerged as the market’s value-migration zone. Land near Hazira and Dahej now commands significant price premiums as developers bid for rail-siding parcels that link directly to the Western Dedicated Freight Corridor. Celcius Logistics’ 2025 launch of a GDP-compliant cross-dock network for pharma exemplifies convergence between cold chain and HAZMAT, while insurer premium reductions of 15-30% for certified fire systems create an added incentive to shift from Grade B sheds to Grade A facilities. Collectively, these factors anchor the long-term expansion strategy of the India chemical warehousing market.

By Chemical Type: Flammable Liquids Dominate, Toxic Substances Accelerate

Flammable liquids held 39.08% of India chemical warehousing market share in 2025, reflecting sustained demand for solvents, petroleum distillates, and specialty intermediates that require Class 3 compliant bays. Storage specifications include vapor-recovery systems and explosion-proof switchgear, areas where Aegis leveraged its new LPG terminals at Pipavav and Mangalore. Yet, toxic substances are poised for 12.02% CAGR through 2031 as lithium-ion battery precursors such as cobalt sulfate and lithium hexafluorophosphate flow into ACC gigafactories. DHL’s planned Centers of Excellence in Chennai and Mumbai will dedicate segregated bays to handle corrosive and toxic chemistries, reinforcing the modal shift toward specialized storage.

The rollback of Quality-Control Orders for several petrochemicals has reduced mandatory testing cycles, shortening dwell time for polypropylene and vinyl chloride. However, oxidizers and corrosives still demand costly segregation to prevent runaway reactions, nudging operators toward vertical-integration plays that bundle tank farms and independent truck parking. Den Hartogh’s 2026 service pact with Bhatinda Industrial Gases adds ISO tank logistics muscle, underscoring multinational appetite for India chemical warehousing market growth.

By End-User Industry: Pharma Leads Growth, Basic Chemicals Anchor Volume

Basic chemicals manufacturing accounted for 35.87% of the India chemical warehousing market size in 2025, underpinned by high-volume acids, alkalis, and commodity solvents. Volumes flow mostly through ambient sheds near port terminals. Nevertheless, pharmaceuticals and life sciences will post a 14.91% CAGR to 2031, lifted by a Production-Linked Incentive that has already mobilized USD 4.86 billion in cumulative capital. Bulk Drug Parks in Andhra Pradesh, Gujarat, and Himachal Pradesh offer shared chillers, solvent recovery, and emergency response facilities that shift some compliance costs from private warehouses to public infrastructure.

Specialty-chemicals producers, led by Godrej Industries and Shivtek Spechemi, are adding surfactants and performance additives for personal-care export markets. Such high-margin lines require batch tracking, allergen separation, and inert-gas blanketing, strengthening demand for Grade A multi-user warehouses with advanced WMS. Agrochemicals, India’s third-largest export earnings segment, push similar needs as producers seek PESO-certified oxidizer bays. Over the forecast window, warehouse operators that can overlay temperature control, digital traceability, and multi-class segregation are positioned to capture a disproportionate share of incremental India chemical warehousing market revenue.

Geography Analysis

Gujarat and Maharashtra form the twin pillars of capacity, thanks to a port complex that handled the majority of India’s chemical cargoes in 2025. Hazira, Dahej, Kandla, and Mundra link seamlessly with the Western Dedicated Freight Corridor, trimming door-to-door times to Delhi and Rajasthan. Godrej’s USD 59.5 million upgrade in Valia and Shivtek Spechemi’s Hazira export warehouse highlight Gujarat’s gravitational pull. State tax holidays and cluster-based infrastructure promise to host one of three federally backed Chemical Parks, cementing its lead in the India chemical warehousing market.

Maharashtra’s JNPT-Uran-Ambernath belt ranks second by throughput, bolstered by Allcargo’s multi-user Grade A sheds and Aegis’s planned investment at Vadhavan Port. Although the state has recorded several high-profile fire incidents, tighter audits by the State Pollution Control Board and better insurer incentives for certified systems are beginning to close the compliance gap. Chennai-Cuddalore in Tamil Nadu is fast emerging as a southern counterpart, anchored by Tanfac’s fluorinated chemicals and Tata Chemicals’ planned 210 kiloton salt plant. DHL’s Battery Logistics Center in Chennai targets automotive and electronics supply chains that value proximity to both seaports and international airports.

Eastern and northern nodes are maturing as Dedicated Freight Corridors come online. Aegis’s 25,000 ton LPG berth at Haldia extends the firm’s national footprint to the Bay of Bengal, while Shivtek’s planned Rajasthan site leans on rail sidings to serve interior chemical clusters. Inland waterways along the Ganga have yet to draw meaningful liquid-bulk volumes, but government incentives for modal shift may unlock new warehouse niches once seasonal draft issues are resolved. Collectively, geographic concentration is expected to persist, with Gujarat and Maharashtra still capturing more than half of India chemical warehousing market revenue by 2031.

Mordor Intelligence examines the chemical warehousing market across diverse other regional markets as well, including Europe, Middle East, and Africa, while also offering granular country-level perspectives for Japan, China, United Kingdom, France, Italy, and South Korea and more.

Competitive Landscape

India’s chemical-warehousing ecosystem remains moderately concentrated. Aegis Logistics, bolstered by USD 174 million in FY 2025 capex and majority control of Hindustan Aegis LPG, commands the largest tank-terminal footprint and a growing portfolio of multi-hazard sheds. Its long-term target of USD 5 billion cumulative investment by 2030 underscores an arms race to secure anchor tenants on take-or-pay terms. DHL, DSV, and Rhenus are deepening vertical integration by pairing ISO tank fleets with Grade A storage, leveraging global procurement power to lock in scarce PFAS-free fire systems.

Mid-tier firms such as Allcargo Logistics, LP Logiscience, and BEST Roadways focus on flexible, multi-user models that cater to SMEs with low minimum-volume commitments. Allcargo’s Uran launch raised its chemical storage footprint to 1.5 million square feet, yet the company posted a net loss in the June 2025 quarter, highlighting margin pressure in an inflationary insurance environment. Technology disruptors, including Simpana and Sigzen, provide ERPNext-based modules for batch traceability and regulatory compliance, enabling smaller warehouses to meet audit requirements without large upfront software licenses.

Price competition has intensified after the late-2025 rollback of several polymer Quality-Control Orders, which removed a compliance moat that once favored large operators. Nonetheless, differentiation around temperature-controlled pharma storage, lithium-ion battery precursor handling, and inland rail-siding access continues to offer strategic white space. Multinationals respond by forming joint ventures: Den Hartogh’s 2026 pact with Bhatinda Industrial Gases extends its ISO tank reach, while Blue Dart’s low-carbon facility at Bijwasan demonstrates a pivot to sustainability credentials that resonate with export-oriented shippers. Overall, the India chemical warehousing market is likely to see selective consolidation as insurers, regulators, and customers converge on higher safety and traceability thresholds.[4]Press Release, “DHL Announces USD 1 Billion India Investment,” DHL.com

India Chemical Warehousing Industry Leaders

-

Aegis Logistics Ltd

-

Allcargo Logistics

-

DHL Group

-

Den Hartogh Logistics

-

Snowman Logistics Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Den Hartogh Logistics signed a service agreement with Bhatinda Industrial Gases Pvt Ltd to expand ISO tank services in India.

- February 2026: Rashtriya Chemicals and Fertilizers approved USD 103 million for a 300 MTPD phosphoric-acid plant in Alibag, Maharashtra.

- February 2026: Tata Chemicals earmarked USD 61.3 million for a 210 KTPA iodized-salt plant in Valinokkam, Tamil Nadu.

- January 2026: Aegis Logistics acquired 75% of Hindustan Aegis LPG, adding 25,000 tons of LPG storage at Haldia.

India Chemical Warehousing Market Report Scope

| General Warehousing |

| Speciality Chemical Warehouse |

| Hazardous Materials (HAZMAT) Warehouses |

| Temperature-Controlled Chemical Warehouses |

| Flammable Liquids |

| Corrosives |

| Toxic Substances |

| Oxidizers |

| Others |

| Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing |

| Pharmaceuticals and Life Sciences |

| Agrochemicals |

| Paints, Coatings and Adhesives |

| Food and Feed Additives |

| Oil and Gas / Petrochemicals |

| Others |

| By Warehouse Type | General Warehousing |

| Speciality Chemical Warehouse | |

| Hazardous Materials (HAZMAT) Warehouses | |

| Temperature-Controlled Chemical Warehouses | |

| By Chemical Type | Flammable Liquids |

| Corrosives | |

| Toxic Substances | |

| Oxidizers | |

| Others | |

| By End-user Industry | Basic Chemicals Manufacturing |

| Specialty Chemicals Manufacturing | |

| Pharmaceuticals and Life Sciences | |

| Agrochemicals | |

| Paints, Coatings and Adhesives | |

| Food and Feed Additives | |

| Oil and Gas / Petrochemicals | |

| Others |

Key Questions Answered in the Report

What is the projected size of India’s chemical warehousing space by 2031?

It is forecast to reach USD 5.28 billion, up from USD 3.43 billion in 2026.

Which warehouse format is expected to grow the fastest through 2031?

Temperature-controlled chemical warehouses are projected to expand at a 12.11% CAGR.

Which chemical class currently accounts for the largest share of stored volumes?

Flammable liquids hold 39.08% of 2025 storage demand.

What end-user group is set to record the quickest growth?

Pharmaceuticals and life sciences facilities are expected to post a 14.91% CAGR to 2031.

How are Dedicated Freight Corridors influencing site selection?

Rail sidings tied to the corridors cut inland transit times and lower freight costs, making interior sites more attractive.

What key risk is pressing margins for port-based operators?

A 15-30% rise in war-risk marine-cargo premiums is inflating the landed cost of imported chemicals.

Page last updated on: