India Mango Market Size and Share

India Mango Market Analysis by Mordor Intelligence

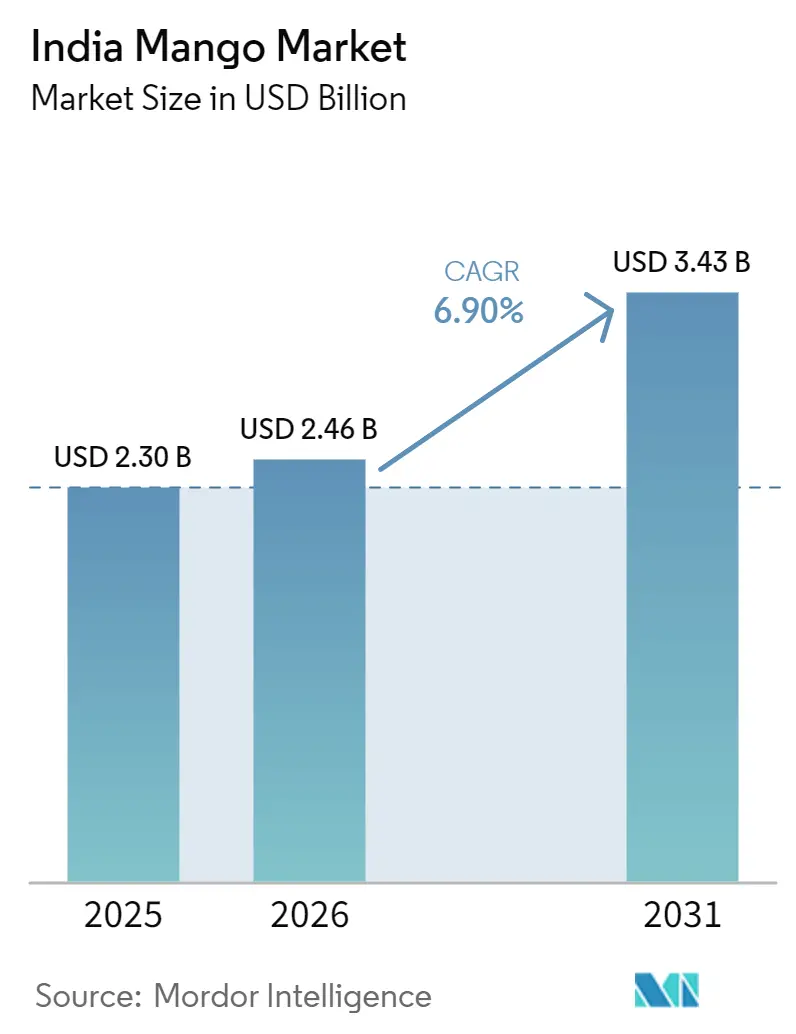

The India Mango Market size is projected to grow from USD 2.30 billion in 2025 to USD 2.46 billion in 2026, reaching USD 3.43 billion by 2031, with a CAGR of 6.9% during 2026-2031. Increasing disposable income supports the demand for premium geographical-indication (GI) mango varieties, although post-harvest losses continue to impact producer margins despite advancements in cold-chain infrastructure. Investments in processing facilities, such as Mother Dairy’s two new plants, indicate a shift from a fresh-only trade model to value-added products like pulp and concentrate, enabling the market to capture a greater share of downstream revenues. Challenges such as monsoon variability and phytosanitary compliance costs remain significant. However, staggered harvest periods across fifteen agro-climatic zones help stabilize national supply, mitigating the impact of localized crop failures.

Key Report Takeaways

- In India mango market, Uttar Pradesh, Andhra Pradesh, Karnataka, Gujarat, and Maharashtra collectively contributed more than 67% to the total mango production in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on mango market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India Mango Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Favorable agro-climatic diversity enabling year-round output | +0.8% | Nationwide, with March–August harvests staggered south-north | Medium term (2-4 years) |

| Rising disposable income driving premium demand | +1.2% | Major urban centers–Mumbai, New Delhi, Bengaluru, Hyderabad, and Ahmedabad | Short term (≤ 2 years) |

| Pradhan Mantri Kisan Sampada Yojana (PMKSY) subsidies accelerating processing capacity | +1.0% | Uttar Pradesh, Andhra Pradesh, Karnataka, and Gujarat | Medium term (2-4 years) |

| Growing demand for natural sweeteners boosting exports | +0.7% | Gulf Cooperation Council countries, and North America | Long term (≥ 4 years) |

| Japan-India cold-chain grants opening East Asian markets | +0.9% | Export corridors in Andhra Pradesh, Maharashtra, and Gujarat | Medium term (2-4 years) |

| Blockchain traceability easing EU compliance | +0.6% | Maharashtra, Gujarat, Andhra Pradesh, and Uttar Pradesh | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Favorable Agro-Climatic Diversity Enabling Year-Round Output

India's fifteen agro-climatic zones extend the commercial mango season from March to August, effectively doubling the marketing window compared to single-origin suppliers. For instance, when Maharashtra's Konkan belt experienced a 60-70% yield loss in 2026, concurrent harvests in Karnataka and Andhra Pradesh helped prevent nationwide shortages [1]Source: Commodity Board, “Alphonso Mango Season Squeezed,” commodity-board.com . Variety specialization, such as Alphonso in coastal Maharashtra, Kesar in Gujarat, Dasheri in Uttar Pradesh, and Totapuri in Karnataka, enables processors to cater to both premium and industrial demand streams within the Indian Mango Market. India’s mango harvesting season varies across regions, with production occurring from March to July, depending on the state, reflecting the country’s diverse agro-climatic conditions and enabling a staggered supply cycle [2]Source: National Horticulture Board, Mango Crop Report, nhb.gov.in.

Rising Disposable Income Driving Premium Demand

Affluent Indian consumers demonstrated consistent demand for GI-tagged Alphonso mangoes in March 2026. Kesar mango purchases increased in the second quarter of 2025, driven by younger consumers preferring naturally ripened fruit for use in desserts and milkshakes. While premium consumers absorbed price volatility, mid-income groups shifted toward non-GI varieties, reducing volume fluctuations but maintaining revenue for quality-focused growers. Direct-to-consumer platforms, such as MangoPoint, which raised funding in August 2025, addressed market dispersion by offering traceable, farm-fresh deliveries. This trend of premiumization has significantly increased retail margins within the Indian mango market.

Pradhan Mantri Kisan Sampada Yojana (PMKSY) Subsidies Accelerating Processing Capacity

Central and state incentives in India reimburse up to 35% of plant costs, reducing entry barriers for pulp and concentrate units in the mango industry [3]Source: Department of Horticulture and Food Processing Uttar Pradesh, “Food Processing Industry Policy 2022-2027,” invest.up.gov.in . Uttar Pradesh offers freight rebates and mandi-fee exemptions to processors sourcing directly from farmers, promoting backward integration [4]Source: Department of Horticulture and Food Processing Uttar Pradesh, “Food Processing Industry Policy 2022-2027,” invest.up.gov.in . India exported over 63,000 metric tons of mango pulp in FY 2024–25, driven by demand from the Middle East, Europe, and North America, demonstrating strong global demand and the country's prominent role in processed mango products [5]Source: Agricultural and Processed Food Products Export Development Authority (APEDA), Mango Pulp Export Data, apeda.gov.in. Converting lower-grade Totapuri into shelf-stable pulp trims waste and stabilizes grower income, aligning subsidies with waste-reduction goals.

Growing Demand for Natural Sweeteners Boosting Exports

Beverage, dairy, and bakery manufacturers in the Gulf Cooperation Council (GCC) and North America are increasingly replacing refined sugar with fruit bases, driving demand for Indian mango pulp, including freeze-dried Alphonso varieties. Buyers from the Gulf region now represent a significant portion of the processed-export earnings in the Indian mango market, particularly for Alphonso and Kesar blends used in premium juices. The United States has shown increased imports of mango derivatives, reflecting the growing trend of clean-label product positioning. Freeze-drying technology preserves nutrient content, extends shelf life, and generates margin premiums compared to fresh consignments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Erratic monsoons increasing yield volatility | -1.5% | Maharashtra, Karnataka, and Andhra Pradesh | Short term (≤ 2 years) |

| Fruit-fly infestations raising export rejections | -0.8% | Maharashtra, Gujarat, Andhra Pradesh, and Uttar Pradesh | Medium term (2-4 years) |

| Fragmented landholdings limiting mechanization and consistency | -0.7% | Uttar Pradesh, Bihar, West Bengal, and national smallholder belts | Long term (≥ 4 years) |

| Rising ocean freight rates reducing competitiveness | -0.5% | All export-oriented corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Erratic Monsoons Increasing Yield Volatility

The 2026 Konkan season experienced a significant decline, with output dropping to 10% of normal levels. This sharp reduction drove Alphonso wholesale prices to range between USD 29-34 per dozen, making them less accessible to mid-income buyers [6]Source: Commodity Board, “Alphonso Mango Season Squeezed,” commodity-board.com . Humid conditions led to an increase in thrips and hoppers, which negatively impacted flower retention and raised pesticide costs, further hindering growth in the Indian mango market. Additionally, alternate bearing cycles exacerbated the situation, as trees entering low-yield phases after bumper crop years struggled to maintain production even under normal weather conditions. To mitigate income fluctuations, growers are increasingly turning to pulp conversion and inter-cropping with cashew and kokum.

Fruit-Fly Infestations Raising Export Rejections

There are only a few United States Department of Agriculture-approved irradiation centers operating nationwide, leading to higher treatment fees and creating bottlenecks during peak-season shipments. A single irradiation process significantly impacts ex-farm prices. The vapor-heat treatment capacity for Japan remains limited, restricting the total volume of processed mangoes despite favorable retail prices. Inadequate field sanitation contributes to increased pest breeding, while strict residue-limit enforcement in the European Union causes shipment concerns. Exporters face additional costs for audits or risk shipment rejections, which reduces profit margins and slows the acquisition of new buyers in the Indian Mango Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

India's staggered south-to-north crop calendar plays a crucial role in stabilizing aggregate supply by ensuring a continuous flow of produce throughout the year. However, the effectiveness of this system is reduced due to infrastructure limitations, such as inadequate storage and transportation facilities. Uttar Pradesh leads in production volume, reflecting its strong agricultural base, but its processed export volume remains significantly lower than Maharashtra's, which benefits from better processing infrastructure and export networks. Andhra Pradesh is actively addressing this disparity by utilizing government subsidies and establishing new processing facilities to enhance its competitiveness.

Maharashtra continues to hold a prominent position in the premium segment of the mango market, with Alphonso mangoes commanding a significant price premium due to their unique flavor and quality. However, a production collapse in the Konkan region in 2026 led to a sharp decline in arrivals at the Pune Market Yard, causing wholesale prices to rise substantially. Despite this setback, the coastal terroir and GI certification of Alphonso mangoes continue to drive strong international demand. Nevertheless, the industry faces persistent challenges, including pest infestations and stringent compliance requirements for residue standards.

Gujarat benefits significantly from the GI certification of Kesar mangoes, which helps in establishing its unique identity and market value. This season experienced an increase in supply compared to the previous year. However, farm-gate prices rose due to a decline in national output and higher demand from juice processors, who rely on these mangoes for their quality and flavor. Smaller producing regions, including Bihar, West Bengal, and Tamil Nadu, play a crucial role in enhancing market diversity by supplying distinct varieties such as Mallika, known for its rich taste, Himsagar, valued for its sweetness, and pulp-grade Totapuri, widely used in processing industries.

Competitive Landscape

In 2025, the Indian mango market was characterized by the presence of several key players, including Jain FarmFresh Ltd., Kay Bee Exports Pvt. Ltd., Allana Sons Pvt. Ltd., INI Farms Pvt. Ltd., and Desai Fruits and Vegetables Pvt. Ltd. Mother Dairy’s investment in Gujarat and Andhra Pradesh plants integrates procurement, processing, and distribution, creating a model for dairy-fruit diversification. Additionally, venture-backed MangoPoint emphasizes direct-to-consumer delivery, improving traceability, and bypassing traditional mandis. This approach allows the company to secure higher retail margins and streamline operations.

Technology adoption is advancing as exporters implement blockchain to meet European Union compliance requirements. Malda’s organic QR code initiative demonstrated the effectiveness of this approach by improving product traceability and marketability. Trials with controlled-atmosphere and modified-atmosphere storage have shown extended shelf life, making sea freight to Europe more viable and cost-efficient, although market penetration remains limited. Third-party auditors, irradiation service providers, and packaging innovators are finding opportunities to generate profits by addressing export-related challenges and improving supply chain efficiency.

Farmer Producer Organizations (FPOs) provide scalability but face challenges related to governance and financing, which hinder their full potential. Policy measures such as freight rebates, capital subsidies, and cold-chain grants are fostering better integration between growers and processors, enabling smoother operations. Competitive advantage in the Indian mango market will favor players who combine extensive orchard networks, advanced processing capabilities, and compliance technologies. These factors are likely to strengthen their bargaining power and position them as key contributors to the market’s overall growth and development.

Recent Industry Developments

- January 2026: The National Innovation Foundation (NIF) introduced advanced HRMN-99 and Sadabahar saplings to Krishi Vigyan Kendras (KVKs) in Uttar Pradesh to promote the adoption of resilient, high-yield varieties among farmers.

- January 2025: Sahyadri Farms (Sahyadri Farmers Producer Company Ltd - SFPCL) has collaborated with the Centre of Excellence for Farmer-Producer Organizations (CoE-FPO) to enhance the FPO ecosystem in Karnataka. This will improve quality, streamline the supply chain, and expand market access for horticultural products, including organic mangoes.

- May 2024: Agricultural and Processed Food Products Export Development Authority (APEDA), in collaboration with ICAR-CISH Lucknow, has initiated the development of a sea protocol for exporting mangoes to distant markets. India aims to access markets in the UK, Japan, Russia, and other countries by exporting multiple mango varieties, including Banganapalli, Kesar, Dasheri, and Chausa, via sea routes.

India Mango Market Report Scope

Mango is a tropical fruit crop extensively cultivated for its sweet, fleshy pulp and significant nutritional value. It is consumed both fresh and processed into products such as juices, pulp, and dried forms, making it a key fruit in global agriculture and trade. The India mango market report includes production analysis (volume, area harvested and yield), consumption analysis (value and volume), trade analysis (value and volume), import market analysis (import value and volume, key supplying markets), export market analysis (export value and volume, key destination markets), wholesale price trend analysis and forecast, regulatory framework, logistics and infrastructure, and seasonality analysis. The market forecasts are provided in terms of value (USD) and volume (metric tons).

| Production Volume |

| Area Harvested and Yield |

| Import Market Analysis | Import Value and Volume |

| Key Supplying Markets | |

| Export Market Analysis | Export Value and Volume |

| Key Destinations Markets |

| Production Analysis | Production Volume | |

| Area Harvested and Yield | ||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume |

| Key Supplying Markets | ||

| Export Market Analysis | Export Value and Volume | |

| Key Destinations Markets | ||

Key Questions Answered in the Report

How large will the India Mango market size be by 2031?

Forecasts place the India Mango market size at USD 3.43 billion by 2031, assuming a 6.9% CAGR from 2026-2031.

What factors most restrict fresh mango exports from India?

Irradiation and vapour-heat treatment capacity limits, alongside rising ocean freight costs and strict residue compliance, cap export volumes.

How are subsidies influencing the India Mango industry?

PMKSY and state incentives reimburse up to 35% of processing equipment cost, catalyzing new pulp and concentrate capacity that absorbs surplus fruit.

Which technological shift is easing European Union market access?

Blockchain-based traceability platforms such as TraceX and HortNet automate pesticide and cold-chain records, reducing rejection risk for exporters.

Page last updated on: