India Biostimulants Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

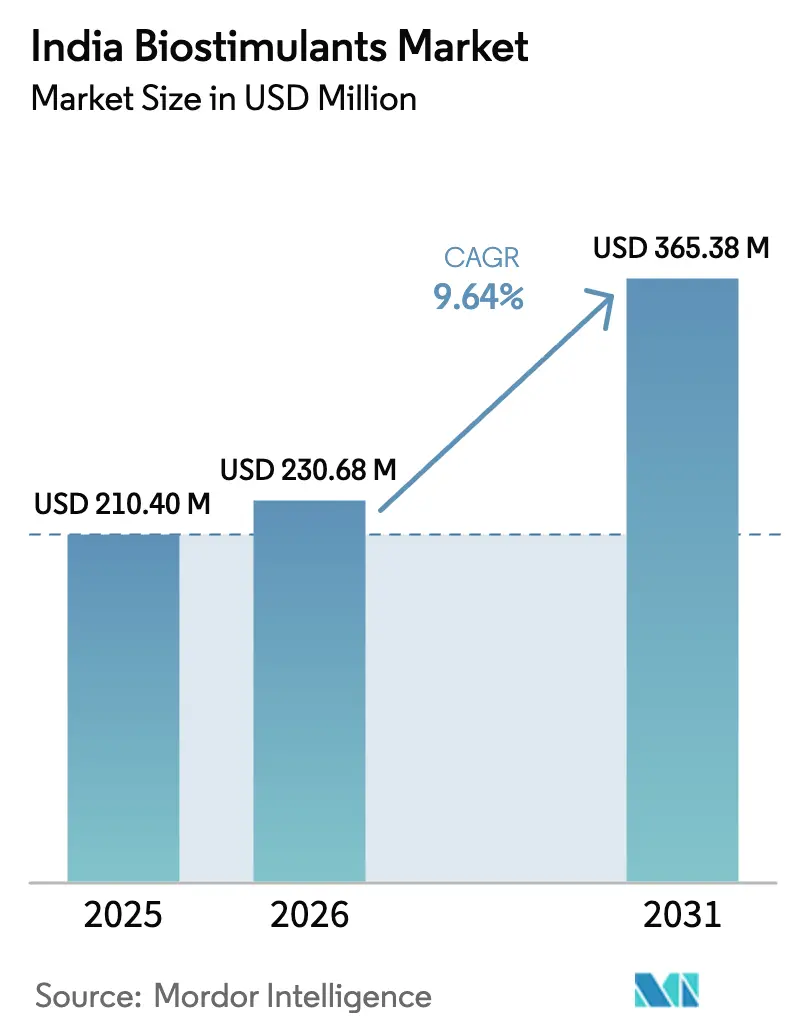

| Base Year Market Size (2025) | USD 210.4 Million |

| Market Size (2026) | USD 230.68 Million |

| Market Size (2031) | USD 365.38 Million |

| Growth Rate (2026 - 2031) | 9.64% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Biostimulants Market Analysis by Mordor Intelligence

The India biostimulants market size is expected to grow from USD 210.4 million in 2025 to USD 230.68 million in 2026 and is forecast to reach USD 365.38 million by 2031 at 9.64% CAGR over 2026-2031. Favorable policy incentives, rapid regulatory consolidation, and technology advances in marine and humic formulations align to accelerate adoption, while export-oriented horticulture and ethanol-driven sugarcane cultivation deepen commercial demand. Rising consumer preference for residue-free food, expansion of drip fertigation networks, and state-level bioeconomy roadmaps further reinforce growth momentum. Nonetheless, uneven farmer awareness and the absence of uniform national standards temper the near-term pace of penetration, especially in Eastern and Northeastern states. Market concentration remains extremely fragmented, indicating significant opportunities for consolidation ahead. This fragmentation creates space for both domestic manufacturers and international players to establish market presence through strategic partnerships, technology transfers, and localized production capabilities. The regulatory cleanup eliminates substandard products while creating barriers to entry that favor established players with robust quality systems and regulatory compliance capabilities.

Key Report Takeaways

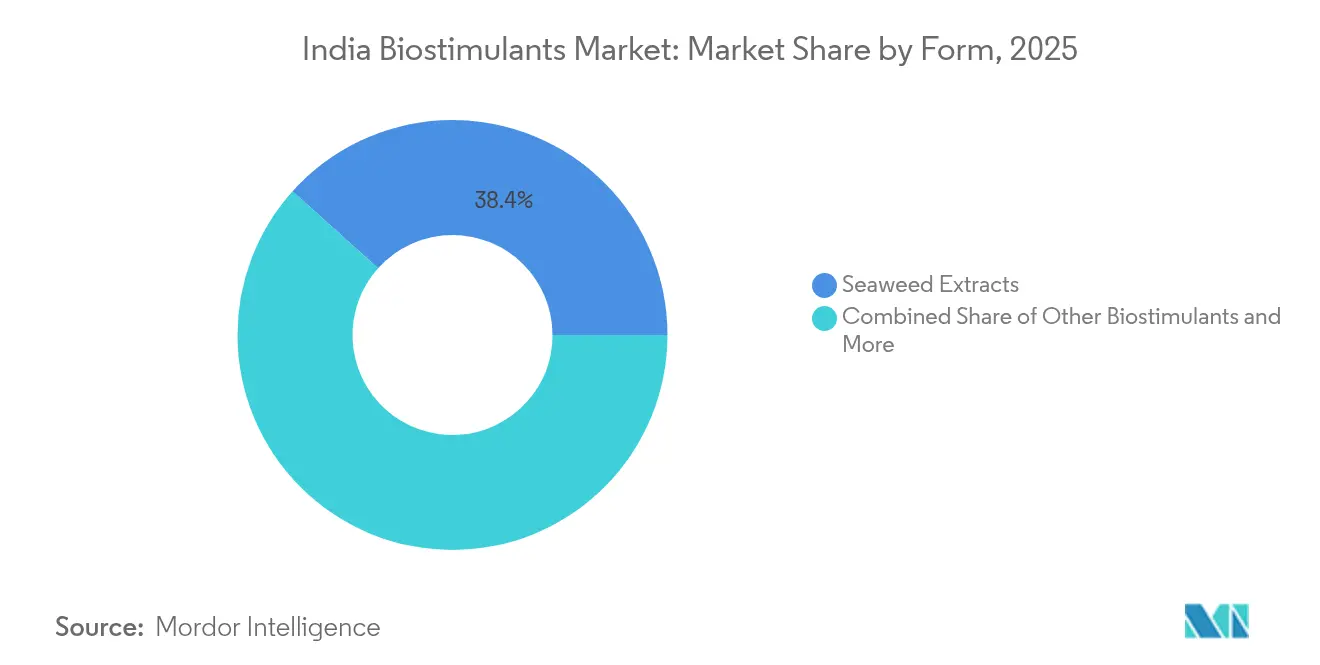

- By form, seaweed extracts led with 38.35% of the India biostimulants market share in 2025, while humic acid is forecast to expand at 11.56% CAGR through 2031.

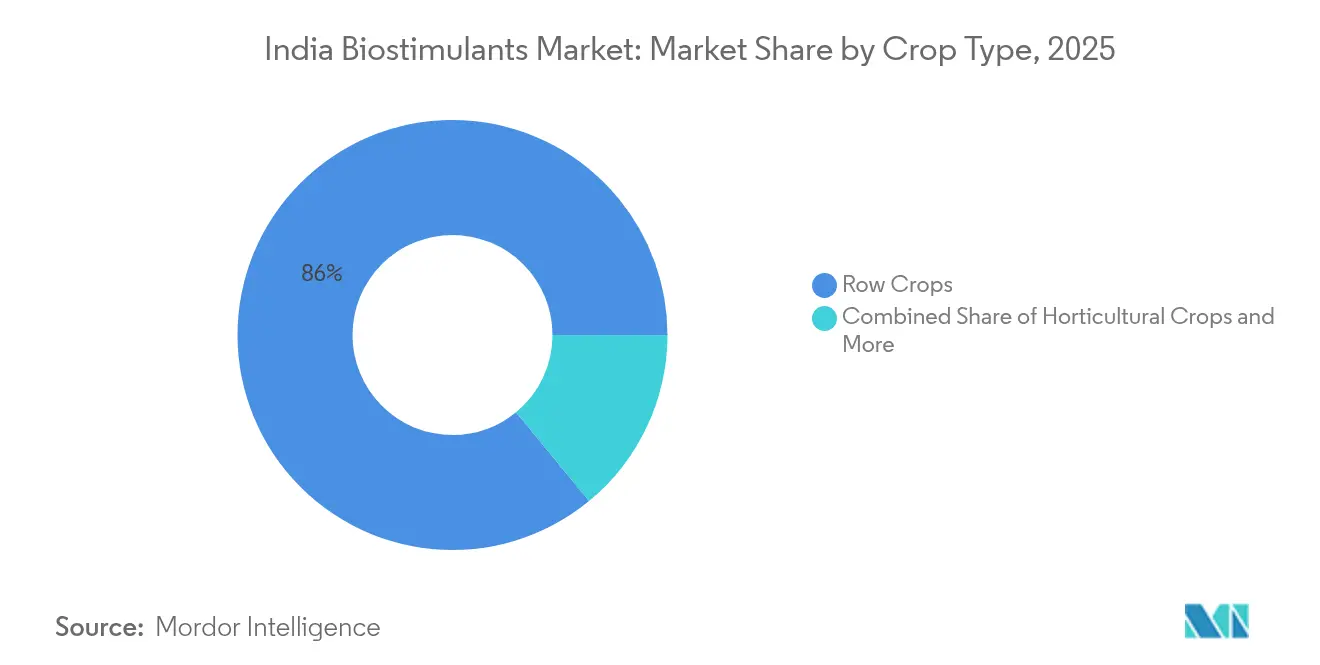

- By crop type, row crops accounted for 85.95% share of the India biostimulants market size in 2025 and are advancing at 10.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Biostimulants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies for organic and natural inputs | +2.1% | National, with early gains in Maharashtra, Gujarat, Karnataka | Medium term (2-4 years) |

| Rising consumer demand for pesticide-free produce | +1.8% | National, concentrated in urban centers and export corridors | Long term (≥ 4 years) |

| Export-oriented horticulture expansion | +1.5% | Maharashtra, Karnataka, Andhra Pradesh, Tamil Nadu | Medium term (2-4 years) |

| Growing penetration of seaweed extract-based products | +1.3% | Coastal states with manufacturing advantages | Short term (≤ 2 years) |

| Ethanol-blended fuel policy accelerating sugarcane yields | +1.2% | Uttar Pradesh, Maharashtra, Karnataka | Medium term (2-4 years) |

| Integration with precision drip-fertigation systems | +0.9% | Gujarat, Maharashtra, Rajasthan, Haryana | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies for Organic and Natural Inputs

The PM-PRANAM (Promotion of Alternate Nutrients for Agriculture Management) scheme rewards states that reduce chemical fertilizer consumption by 15% or more, channeling 70% of subsidy savings into bio-input infrastructure, which directly stimulates India biostimulants market demand.[1]Source: Ministry of Agriculture and Farmers Welfare, “Spurious Seeds, Pesticides and Fertilizers Supplied to the Farmers,” Press Information Bureau, pib.gov.in Karnataka’s Biotechnology Policy 2024-2029 targets a USD 100 billion bioeconomy and offers production incentives that favour compliant manufacturers. Gujarat’s micro-irrigation subsidies cover up to 90% of drip system costs, facilitating liquid biostimulant dosing through fertigation networks.[2]Source: Gujarat Green Revolution Company Limited, “Welcome to GGRC,” ggrc.co.in Combined, these programs reduce farmer risk, underpin steady offtake, and broaden the India biostimulants market footprint.

Rising Consumer Demand for Pesticide-Free Produce

India’s organic exports climbed to USD 666 million in FY 2025 and target USD 2 billion by 2030 as European Union residue limits tighten.[3]Source: Indian Brand Equity Foundation, “Indian Fertilizer Industry on Track to Reach US$ 16.58 Billion by 2032,” ibef.org Domestic retail chains mirror this shift with premium procurement programs that pay 15-25% more for pesticide-free fruits and vegetables, which accelerates India biostimulants market acceptance among commercial farmers. Long-term offtake agreements from food-processing majors lock in demand and de-risk investment in bio-input protocols.

Export-Oriented Horticulture Expansion

Horticultural export demand has been flourishing in recent years, and seaweed extract foliar sprays have cut storage losses in grapes and mangoes by 12-18% while extending shelf life for shipments. APEDA (Agricultural and Processed Food Products Export Development Authority) offers quality-upgradation support that includes biostimulant training, anchoring the India biostimulants market among grape, pomegranate, and cut-flower growers.

Growing Penetration of Seaweed Extract-Based Products

The national seaweed mission promotes Kappaphycus alvarezii farming across production land, ensuring cost-competitive raw material for domestic extraction. Sea6 Energy has scaled AgroGain seaweed extract capacity annually, supplying 12 states and validating commercial viability. Consistent efficacy data from state agricultural universities underpins extension recommendations and cements trust, lifting the India biostimulants market adoption curve.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Absence of uniform national biostimulant standards | -1.4% | National, affecting interstate commerce | Short term (≤ 2 years) |

| Limited farmer awareness outside progressive states | -1.2% | Eastern and northeastern states primarily | Medium term (2-4 years) |

| Price premium versus conventional fertilizers | -0.8% | Cost-sensitive regions and smallholder areas | Long term (≥ 4 years) |

| Product adulteration eroding trust in the category | -0.6% | National, concentrated in unregulated channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Absence of Uniform National Biostimulant Standards

The Fertilizer Control Order cancelled 9,352 provisional registrations, leaving only 146 approved products in 2025 and exposing significant gaps in testing protocols across states. These gaps highlight inconsistencies in regulatory enforcement, leading to interstate discrepancies that raise compliance costs and create barriers for new entrants. This situation has temporarily restrained volume growth in the India biostimulants market, while also emphasizing the need for a more uniform and streamlined regulatory approach to foster long-term development.

Limited Farmer Awareness Outside Progressive States

Maharashtra, Gujarat, and Karnataka consume over 60% of biostimulants although they represent only one-quarter of India’s cultivated land. Extension gaps in Bihar, Odisha, and Assam slow diffusion, keeping the India biostimulants market penetration uneven. Targeted vernacular training modules and digital advisory apps are closing this gap but will take time to scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Performance Advantage Drives Seaweed Dominance

Seaweed extracts commanded 38.35% share of the India biostimulants market in 2025, capitalizing on proven abiotic-stress mitigation and wide crop compatibility. Domestic seaweed farming reduces input costs and shortens supply chains, amplifying price competitiveness and supporting rapid expansion. Humic acid, though currently smaller, is the fastest-growing sub-segment at 11.56% CAGR to 2031, buoyed by government soil-health campaigns that position carbon-rich inputs as foundational to regenerative agriculture. Amino acids and fulvic acid maintain steady demand among horticultural exporters who prize quality and shelf life, while protein hydrolysates address emerging climate-resilient farming niches. Regulatory cleanup favoured seaweed and humic products with validated dossiers, reinforcing their availability across the India biostimulants market.

Ecosystem investments deepen competitive moats. Sea6 Energy’s 5,000 metric tons capacity plant leverages proprietary extraction technology, ensuring consistency and scale. Coromandel International allocated funds toward specialty and nano-fertilizer facilities that integrate biostimulant modules, securing raw material collaboration and margin upside. Academic partnerships, including CSIR-CSMCRI trials, underpin scientific claims, enhancing farmer confidence and distributor pull-through. Collectively, these dynamics fortify the India biostimulants market size trajectory across form factors.

By Crop Type: Row Crops Underpin Volume, Horticulture Captures Value

Row crops held 85.95% of the India biostimulants market share in 2025 and exhibit a robust 10.05% CAGR through 2031, mirroring broad-acre adoption of foliar and fertigation practices. Sugarcane, rice, and wheat leverage existing mechanization and irrigation infrastructure, allowing seamless integration of low-volume, high-efficacy formulations. Government ethanol mandates and food-grain self-sufficiency goals sustain investment, ensuring stable growth in core acreage and application frequency.

Horticultural crops, while smaller in acreage, deliver outsized revenue through export premiums and stringent residue requirements. Grapes and mangoes benefit from seaweed-induced shelf-life extension, and floriculture adopts amino acids to improve vase life. Cash crops, particularly cotton and spices, present a mid-term opportunity as pest resistance management shifts toward integrated biological solutions. The India biostimulants market size for high-value crops is set to widen as domestic retail chains promote certified residue-free produce, reinforcing farmer economics beyond subsidies.

Geography Analysis

Western India anchors demand. Maharashtra leverages strong cooperatives and export-oriented grape and pomegranate clusters to champion innovative inputs, translating into the highest per-acre biostimulant spend in the country. Gujarat’s chemical manufacturing ecosystem and GGRC’s subsidy framework embed liquid formulations into drip networks, securing steady offtake and cultivating brand loyalty among progressive growers. Karnataka’s bioeconomy blueprint and proximity to seaweed cultivation sites accelerate early adoption rates, carving a leadership position in the India biostimulants market.

Northern grain belts are entering a transition phase. Punjab and Haryana, historically reliant on high fertilizer intensity, respond to PM-PRANAM incentives by piloting humic acid blends that cut synthetic nitrogen use without yield loss. Uttar Pradesh’s sugarcane acreage amplifies demand, aided by mill-backed field demonstrations that validate economic gains. Extension penetration remains a challenge, yet rising input-use efficiency mandates a shift in farmer attitudes in favour of biological enhancers.

Eastern and northeastern states lag but hold latent potential. Smaller farm holdings and limited mechanization slow uptake and organic certification programs under Paramparagat Krishi Vikas Yojana unlock subsidies that mitigate price barriers. Digital advisory platforms and localized language content close knowledge gaps, laying the groundwork for inclusive expansion of the India biostimulants market over the forecast window. Coastal Andhra Pradesh and Tamil Nadu additionally benefit from proximity to marine raw materials, positioning them as emerging processing hubs that could shorten supply chains and stimulate regional adoption.

Competitive Landscape

The India biostimulants market is highly fragmented, with the top five companies controlling a minor share of the overall revenue. Regulatory tightening is triggering an attrition cycle that favors well-capitalized firms able to compile comprehensive efficacy dossiers and invest in ISO-certified facilities. Coromandel International is reinforcing vertical integration by directing funds into specialty and nano-fertilizer capacity that dovetails with its bio-input portfolio. Sea6 Energy pushes technology frontiers through proprietary large-scale seaweed extract platforms that secure consistent quality and cost optimization.

Indian Farmers Fertiliser Cooperative (IFFCO) is commercializing nano-urea and nano-zinc liquids, leveraging its 36,000-member distribution network to fast-track farmer trials and build category credibility. KRIBHCO’s alliance with Novonesis enhances microbial R&D depth and broadens pilot pipelines into biofertilizers that run adjacent to biostimulant offerings. Start-ups such as BharatAgri and AgroStar integrate e-commerce logistics with agronomic advisory, extending last-mile reach into underserved rural pockets and lowering distribution costs.

Global incumbents, attracted by scale and growth prospects, pursue minority stakes and technology-licensing deals to gain regulatory footholds while mitigating execution risk. Dhanuka Agritech and Godrej Agrovet, with strong domestic brand equity, are prime partners for such collaborations, offering established sales teams and registered product lines. The race to secure compliant portfolios before the next regulatory deadline is anticipated to catalyse mergers, raising the bar for manufacturing quality and consolidating the India biostimulants market leadership structure.

India Biostimulants Industry Leaders

Biostadt India Limited (Bilag Industries Pvt Ltd)

Valagro (Syngenta Group)

Coromandel International Limited (Murugappa Group)

T. Stanes and Company Limited (Amalgamations Group)

Southern Petrochemical Industries Corporation [SPIC] (AM International Holdings)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Koppert has transferred its biostimulant and fertilizer portfolio to REKA Group to prioritize biological crop protection. Products such as Veni, Vidi, Vici will now be managed and distributed by REKA, including in India. This decision enables Koppert to focus on developing pest and disease control solutions.

- July 2024: Coromandel International committed INR 1,000 crore (approximately USD 120.5 million) toward specialty and nano-fertilizer lines, including biostimulants, supplementing its earlier investment to deepen portfolio integration.

India Biostimulants Market Report Scope

Amino Acids, Fulvic Acid, Humic Acid, Protein Hydrolysates, Seaweed Extracts are covered as segments by Form. Cash Crops, Horticultural Crops, Row Crops are covered as segments by Crop Type.| Amino Acids |

| Fulvic Acid |

| Humic Acid |

| Protein Hydrolysates |

| Seaweed Extracts |

| Other Biostimulants |

| Cash Crops |

| Horticultural Crops |

| Row Crops |

| Form | Amino Acids |

| Fulvic Acid | |

| Humic Acid | |

| Protein Hydrolysates | |

| Seaweed Extracts | |

| Other Biostimulants | |

| Crop Type | Cash Crops |

| Horticultural Crops | |

| Row Crops |

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of biostimulants applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - The Crop Protection function of agirucultural biological include products that prevent or control various biotic and abiotic stress.

- TYPE - Biostimulants boost crop growth and yield by preventing or controlling various abiotic stresses.

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.