Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

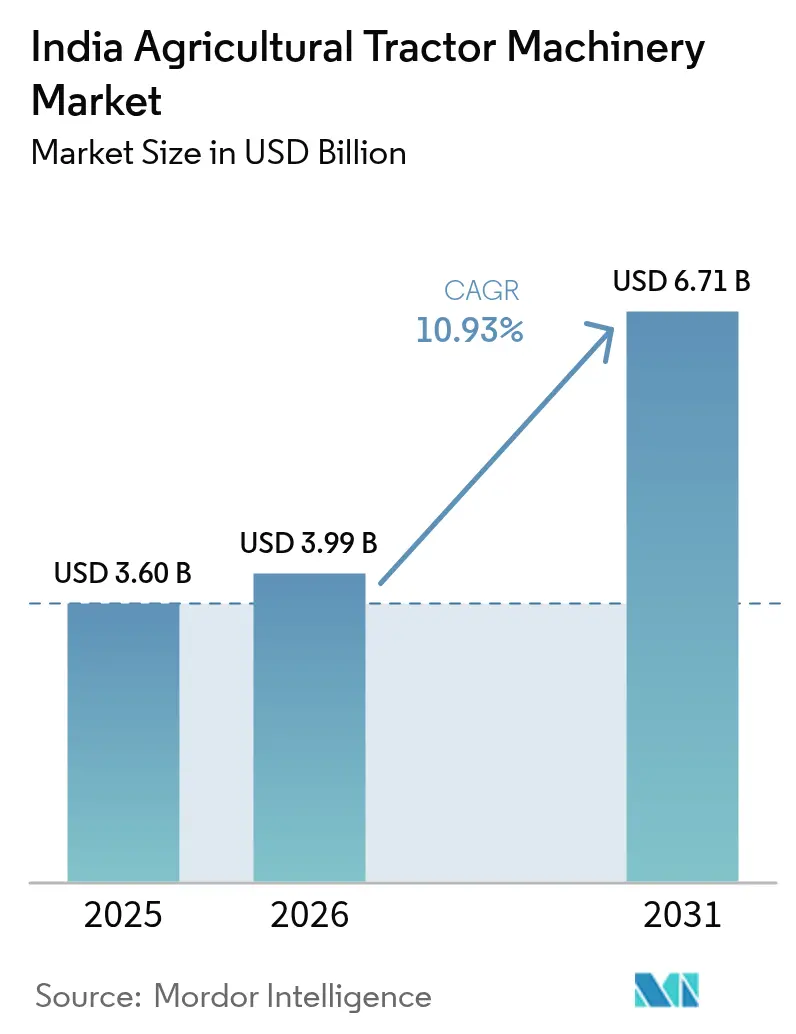

| Base Year Market Size (2025) | USD 3.60 Billion |

| Market Size (2026) | USD 3.99 Billion |

| Market Size (2031) | USD 6.71 Billion |

| Growth Rate (2026 - 2031) | 10.93% CAGR |

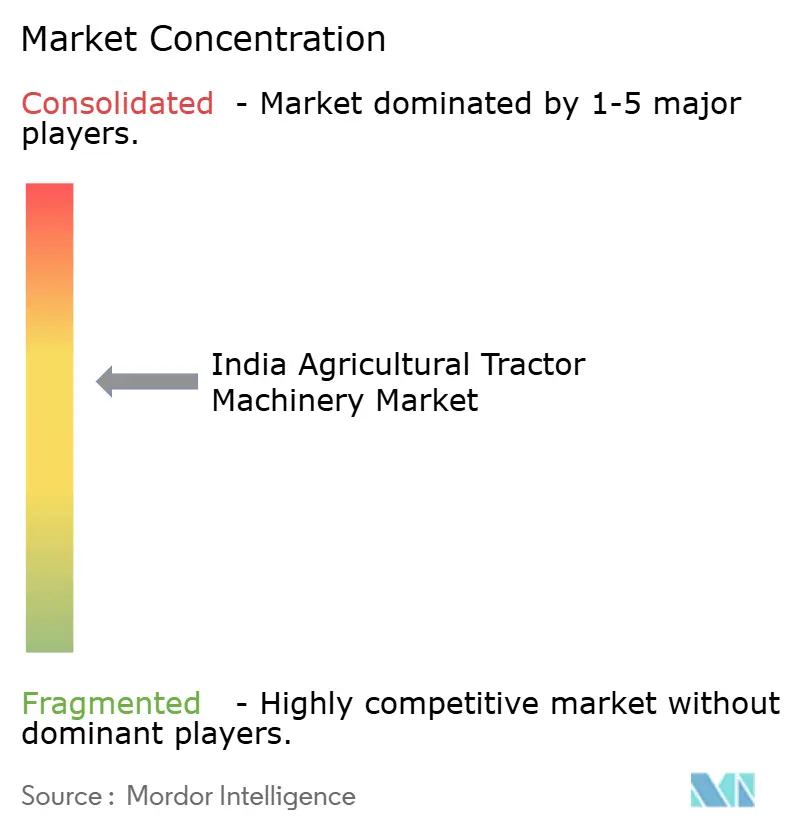

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Agricultural Tractor Machinery Market Analysis by Mordor Intelligence

The India agricultural tractor machinery market size in 2026 is estimated at USD 3.99 billion, growing from 2025 value of USD 3.60 billion with 2031 projections showing USD 6.71 billion, growing at 10.93% CAGR over 2026-2031. Rising subsidy coverage for implements, an acute farm labor crunch, and upcoming precision agriculture mandates are widening equipment replacement cycles and lifting average selling prices. Government support through the Sub-Mission on Agricultural Mechanization and the Custom Hiring Center programs is lowering ownership barriers and expanding rental fleets, while digital public infrastructure is improving subsidy targeting. Original equipment manufacturer (OEM) are bundling telematics-ready implements with tractors, encouraging data-driven farming practices. Start-ups that match idle tractors with neighboring growers are expanding addressable demand beyond traditional dealer territories. The looming Tractor and Related Equipment Mechanization Stage V emission rule, along with a shortage of trained mechanics in smaller towns, restrain near-term growth.

Key Report Takeaways

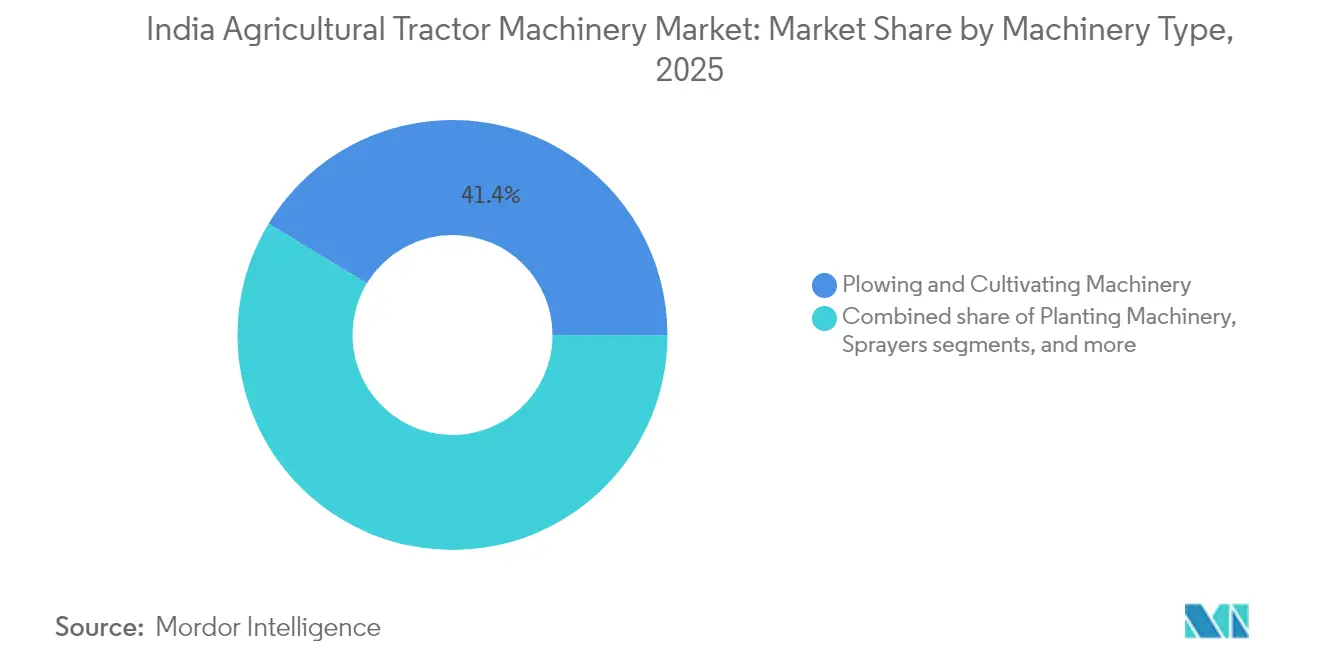

- By machinery type, plowing and cultivating machinery led with 41.35% of the India agricultural tractor machinery market size in 2025, and sprayers are forecast to record the fastest 14.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Agricultural Tractor Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidized purchase of tractor-mounted implements under SMAM/CHC schemes | +2.8% | National, strongest in Punjab, Haryana, Uttar Pradesh, and Madhya Pradesh | Medium term (2-4 years) |

| Precision-ready rotavators now bundled by leading OEMs | +1.5% | National, concentrated in Punjab, Haryana, Gujarat, and Maharashtra | Medium term (2-4 years) |

| Demand spike from labor-scarcity during kharif sowing season | +2.2% | National, acute in Punjab, Haryana, Uttar Pradesh, and Bihar | Short term (≤ 2 years) |

| Government push for crop-residue management attachments | +1.3% | Punjab, Haryana, spillover into Uttar Pradesh, and Rajasthan | Short term (≤ 2 years) |

| Surge in start-up led “implements-as-a-service” mobile apps | +0.9% | National, early uptake in Karnataka, Tamil Nadu, Madhya Pradesh, and Rajasthan | Long term (≥ 4 years) |

| Rising vineyard/orchard acreage driving niche PTO sprayers | +1.2% | Maharashtra, Karnataka, Andhra Pradesh, Tamil Nadu, and Punjab | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Subsidized purchase of tractor-mounted implements under SMAM/CHC schemes

Direct benefit transfers covering 40-50% of equipment cost for individual buyers and up to 80% for community Custom Hiring Centers (CHCs) have become the market’s primary accelerator[1]Source: Press Information Bureau staff, “Sub-Mission on Agricultural Mechanization Spurs Equipment Adoption,” Press Information Bureau, pib.gov.in. The 26,662 CHCs established by December 2024 are providing rental access to implements that were once unaffordable to marginal growers. A National Bank for Agriculture and Rural Development (NABARD) priority lending target for farm machinery during FY 2024-25 indicates continued liquidity for new fleets. Higher subsidy slabs for crop-residue management equipment have already cut stubble-burning incidents in Punjab in 2024.

Precision-ready rotavators now bundled by leading OEMs

Mahindra and Mahindra Limited’s Krish-e Smart Kit, priced at INR 4,995 (USD 60), converts rotavators into connected assets that track acres covered and fuel use; daily active usage exceeds 85%, proving operator stickiness[2]Source: Editors, “Krish-e Smart Kit Brings Telematics to Implements,” Mahindra and Mahindra Limited, mahindra.com. Tractors and Farm Equipment Limited mirrors the model with JFarm Services, which processed more than 100,000 rental orders by January 2025. The integration of telemetry and digital marketplaces shortens the payback periods for Custom Hiring Center (CHC) investors and provides real-time maintenance data to service networks.

Demand spike from labor-scarcity during kharif sowing season

The National Institution for Transforming India (NITI) Aayog's 2025 agriculture roadmap noted that 70 to 80 percent of marginal and small farmers lack tractors or power tillers, relying on manual labor for soil preparation. This labor constraint is most acute in states with high out-migration of rural youth to urban centers, where the extension-officer-to-farm ratio stands at approximately 1:1,100, compared to a recommended ratio of 1:750. Mechanization via Custom Hiring Center (CHC) rentals offers a hedge against wage inflation, as a rotavator can prepare one hectare in two to three hours at a rental cost of INR 800 to INR 1,200 (USD 9.6 to USD 14.4), compared to INR 3,000 to INR 4,000 (USD 36 to USD 48) for manual labor over two days. The government's FARMS (Farm Machinery Solutions) mobile app, launched in May 2024, digitizes CHC booking and connects farmers to over 26,000 service providers, reducing search costs and idle time.

Rising vineyard/orchard acreage driving niche PTO sprayers

India's horticulture sector covered 28.98 million hectares in 2023-24, producing 353.19 million metric tons, with vineyards and orchards concentrated in Maharashtra, Karnataka, Andhra Pradesh, Tamil Nadu, and Punjab Press Information Bureau. The shift from field crops to high-value horticulture, which commands better price realization and export potential, has created demand for low-profile PTO sprayers that navigate narrow row spacing and deliver precise canopy coverage. CNH Industrial's AI-enabled sprayers, introduced in June 2025 under the Case IH, New Holland, and Miller brands, use camera sensing to detect green-on-brown (weeds on soil) and apply herbicides selectively, reducing chemical usage and water consumption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of powered implements | -1.8% | National, strongest in the east and northeast | Short term (≤ 2 years) |

| Fragmented small holdings limit pay-back period | -1.3% | National, acute in Bihar, West Bengal, Uttar Pradesh, Kerala | Medium term (2-4 years) |

| Looming 2026 TREM-V emission rule requiring PTO-power-matching retrofits | -1.1% | National, costlier for high-horsepower equipment | Short term (≤ 2 years) |

| Shortage of skilled mechanics for gear-box repair in Tier-3 towns | -0.7% | National, most evident in rural and semi-urban districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented small holdings limit pay-back period

The average farm size of 0.74 hectares restricts the economic viability of large attachments such as balers and combine harvesters, which require minimum plot sizes of 5 to 10 hectares to achieve breakeven utilization. Bihar, West Bengal, Uttar Pradesh, and Kerala exhibit the highest fragmentation, with marginal holdings (below 1 hectare) comprising over 70 percent of operational farms in these states. For INR 1.5 lakh (USD 1,800) rotavator, a farmer cultivating 0.5 hectares would need to rent out the implement for 100 to 150 hours annually to recover costs, but localized demand and seasonal clustering make such utilization difficult without digital aggregation platforms[3]Source: Research Department, “National Sectoral Paper on Farm Mechanisation,” National Bank for Agriculture and Rural Development, nabard.org.

Looming 2026 TREM-V emission rule requiring PTO-power-matching retrofits

The TREM Stage V emission standards, scheduled for full enforcement by April 2026, mandate recalibration of PTO horsepower to comply with cleaner engine outputs, which is anticipated to raise implement prices by an estimated 10 to 20 percent. Implementations such as rotavators, balers, and combine attachments rely on PTO shafts to draw power from tractor engines; TREM-V's stricter particulate-matter and nitrogen-oxide limits reduce available PTO power, requiring redesigns of gearboxes and torque converters. Escorts Kubota Limited, which announced an INR 4,500 crore (USD 540 million) investment to double tractor capacity to 340,000 units per year, has indicated that TREM-V compliance will necessitate supply-chain adjustments and component re-sourcing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Plowing and Cultivating Machinery Sustain Tillage Leadership While Sprayers Accelerate

Plowing and cultivating machinery accounted for 41.35% market share, with rotary tillers as the dominant stock-keeping unit (SKU). Tirth Agro Technology (Shaktiman) accounts for the most domestic rotavator sales, underscoring the segment’s brand concentration. Rotavators cut seedbed preparation to a single pass, saving diesel and time. The Indian agricultural tractors machinery market size for Sprayers is set to expand at a CAGR of 14.2% through 2031, driven by orchard expansion and precision input mandates. CNH Industrial N.V.'s AI sprayer platform promises double-digit chemical savings, a strong selling point for high-value fruit growers.

Planting Machinery gains from 40-50% subsidies that encourage seed-drill ownership and from digital soil maps that call for precise seeding depth. Deere and Company offers bundled tractor-plus-planter packages to medium farms, helping it capture affluent buyers. Haying and Forage equipment remains predominantly rented due to high ticket prices, reinforcing the relevance of the Custom Hiring Center. Smaller niche categories, such as potato planters and sugarcane harvesters, are still supplied by regional specialists that tailor frame widths to local crops.

Geography Analysis

Punjab, Haryana, and western Uttar Pradesh lead the adoption, with mechanization penetration above 90%, and stringent residue-burning penalties driving the uptake of Happy Seeders. Uttar Pradesh, Madhya Pradesh, and Rajasthan hold the largest priority-lending allocations for farm machinery, indicating strong latent demand. Southern states dominate horticulture and are early adopters of AI sprayers. Tamil Nadu alone has an estimated lending potential of INR 11,282.54 crore (USD 1.4 billion) for agricultural implements.

Eastern and northeastern regions lag, posting mechanization rates below 30%. Higher 60% individual and 90% CHC subsidy slabs apply here, though the small plot sizes and limited banking reach slow down traction. The Digital Agriculture Mission aims to narrow gaps through the rollout of a national Farmer ID and crop survey, which will improve subsidy delivery.

Northeastern states receive higher SMAM subsidies to offset hilly terrain and limited dealer networks, but mechanization penetration remains below 20 percent due to small plot sizes (average below 0.5 hectares) and inadequate service infrastructure. The government's emphasis on Krishi Sakhis, women extension workers trained in machinery operation and basic maintenance aims to close the last-mile service gap, with 250,000 youth and Krishi Sakhis targeted for training under the Digital Agriculture Mission.

Competitive Landscape

The market is moderately fragmented, with key players such as Deere & Company, Mahindra & Mahindra Ltd., Tirth Agro Technology (Shaktiman), Beri Udyog Pvt. Ltd. (Fieldking), and Maschio Gaspardo S.p.A. accounting for a significant share. Mahindra & Mahindra Ltd. leads the market, supported by its integrated hardware-software Krish-e ecosystem. Tirth Agro Technology (Shaktiman) holds a significant share, primarily driven by its dominance in the rotavator segment. Beri Udyog Pvt. Ltd. (Fieldking) captures a notable portion of the market, leveraging a robust export network. Deere & Company, Maschio Gaspardo S.p.A., and CNH Industrial N.V. focus on premium planters and sprayers, strengthening their position in the high-tech segment. Additionally, VST Tillers Tractors Limited's entry into the 40-50 horsepower tractor category through its Zetor venture underscores the growing competition for medium-sized farm customers.

Strategic pivots emphasize digital ecosystems. Firms launch app-based service bookings, subscription maintenance, and parts e-stores. Mahindra’s Krish-e platform uses sensor data to recommend agronomic practices, creating cross-sell for implements and inputs. TAFE’s JFarm Services app aggregates custom hiring demand, accelerating fleet utilization. Emission-compliance deadlines drive alliances with component suppliers: CNH partners with BOSCH for after-treatment, while Escorts taps Kubota for stage-V-ready combustion systems. Electric tractor prototypes surface, but commercialization timelines depend on battery localization.

Traditional incumbents hedge by investing in ventures or launching in-house incubators. Used-tractor portals disrupt dealers’ residual pricing. As technology, regulation, and credit dynamics evolve, competitive advantage will hinge less on metal and more on data, finance, and service depth within the tractor industry in India.

India Agricultural Tractor Machinery Industry Leaders

Deere & Company

Mahindra & Mahindra Ltd.

Tirth Agro Technology (Shaktiman)

Beri Udyog Pvt. Ltd. (Fieldking)

Maschio Gaspardo S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mahindra & Mahindra Ltd.'s Farm Equipment Sector announced record-high annual domestic tractor sales of 407,094 units for fiscal year 2025, a 12% increase over the previous year. In March 2025, the company sold 32,582 tractors in the domestic market, totaling 34,934 units, including exports, marking a 34% year-over-year growth for the month.

- August 2024: Mahindra & Mahindra Ltd announced the ramp-up of production of rotavators from its dedicated manufacturing unit in Nabha, Punjab, expanding its range of tillage implements compatible with a variety of tractors (15–70 HP) for Indian soil conditions.

India Agricultural Tractor Machinery Market Report Scope

The India Agricultural Tractor Machinery Market Report is Segmented by Machinery Type (Plowing and Cultivating Machinery, Planting Machinery, Haying and Forage Machinery, Sprayers, and Other Types).The Market Forecasts are Provided in Terms of Value (USD).

By Machinery Type

| Plowing and Cultivating Machinery | Plows |

| Harrows | |

| Rotovators and Cultivators | |

| Other Plowing and Cultivating Machinery | |

| Planting Machinery | Seed Drills |

| Planters | |

| Spreaders | |

| Other Planting Machinery | |

| Haying and Forage Machinery | Mowers and Conditioners |

| Balers | |

| Other Haying and Forage Machinery | |

| Sprayers | |

| Other Types |

| By Machinery Type | Plowing and Cultivating Machinery | Plows |

| Harrows | ||

| Rotovators and Cultivators | ||

| Other Plowing and Cultivating Machinery | ||

| Planting Machinery | Seed Drills | |

| Planters | ||

| Spreaders | ||

| Other Planting Machinery | ||

| Haying and Forage Machinery | Mowers and Conditioners | |

| Balers | ||

| Other Haying and Forage Machinery | ||

| Sprayers | ||

| Other Types | ||

Key Questions Answered in the Report

What is the current value of the India agricultural tractors machinery market?

The market generated USD 3.99 billion in 2026.

How fast is demand for sprayers expected to grow?

Sprayers are projected to register a 14.2% CAGR through 2031, the fastest among all implement categories.

Which state clusters show the highest mechanization penetration?

Punjab, Haryana, and western Uttar Pradesh each exceed 90% mechanization levels.

How will Stage V emission norms affect implement prices?

Compliance is anticipated to raise equipment prices by 10-20% as manufacturers redesign power-take-off systems.

What role do Custom Hiring Centers play for smallholders?

CHCs provide pay-per-use access to machinery, reducing ownership costs and widening mechanization reach among farms under five hectares.

Page last updated on: