Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

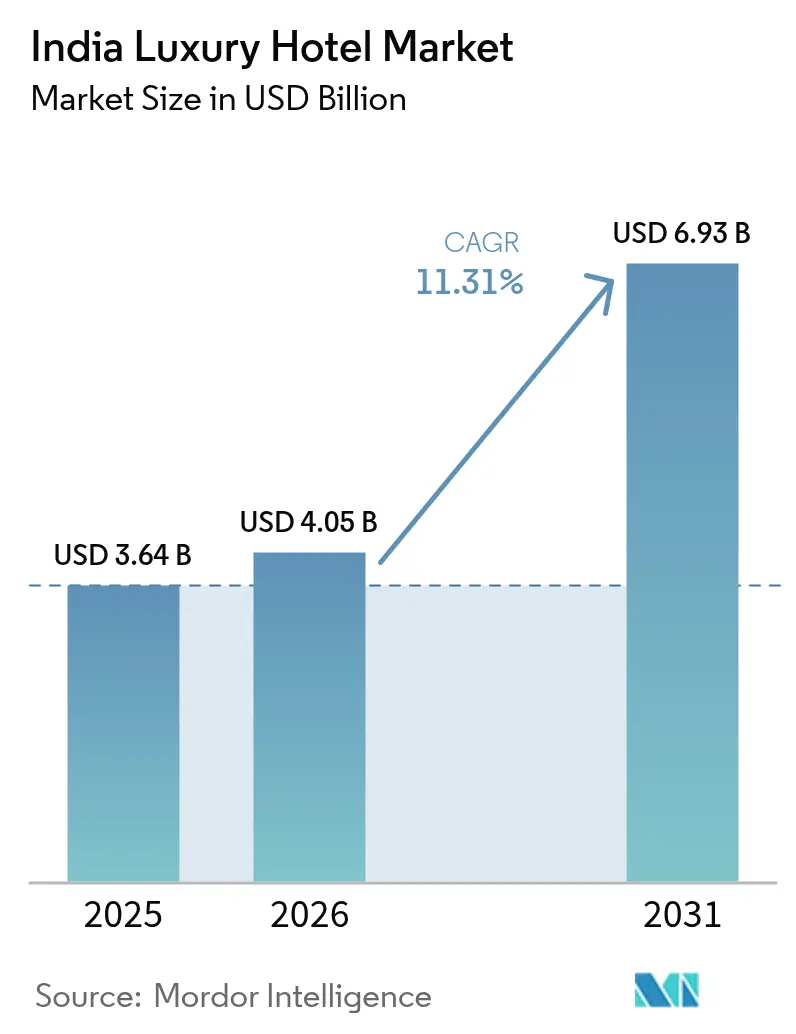

| Base Year Market Size (2025) | USD 3.64 Billion |

| Market Size (2026) | USD 4.05 Billion |

| Market Size (2031) | USD 6.93 Billion |

| Growth Rate (2026 - 2031) | 11.31% CAGR |

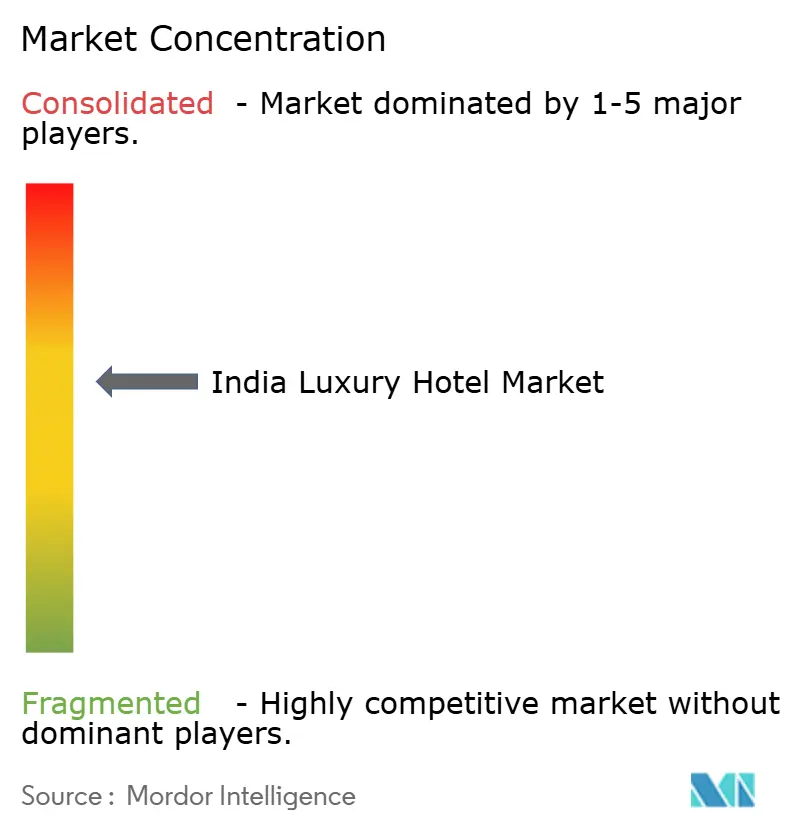

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Luxury Hotel Market Analysis by Mordor Intelligence

The India Luxury Hotel Market size was valued at USD 3.64 billion in 2025 and estimated to grow from USD 4.05 billion in 2026 to reach USD 6.93 billion by 2031, at a CAGR of 11.31% during the forecast period (2026-2031).

Strong domestic purchasing power, sustained infrastructure spending, and policy support, such as the Coastal Regulation Zone (CRZ-2019) liberalization, have firmly positioned the country as Asia’s fastest-growing premium hospitality destination[1]Source: Press Information Bureau, “Cabinet approves Coastal Regulation Zone (CRZ) Notification 2018,” pib.gov.in. A 50.1% rise in India’s ultra-high-net-worth (UHNW) population projected through 2028 is reshaping demand toward experiential and wellness-oriented stays, while digital adoption is compressing booking cycles and lifting direct-to-hotel margins. International brands announced six luxury signings within four days in April 2025, underscoring heightened investor confidence and sharpening competitive intensity. At the same time, the April 2025 GST restructuring lifted the dining tax on rooms above INR 7,500 to 18%, temporarily pressuring food-and-beverage spend even as hotels gained input-tax-credit eligibility.

Key Report Takeaways

- By geography, north India held a 42.60% of the India luxury hotel market share in 2025, while east & north-east India are advancing at a 14.6% CAGR through 2031.

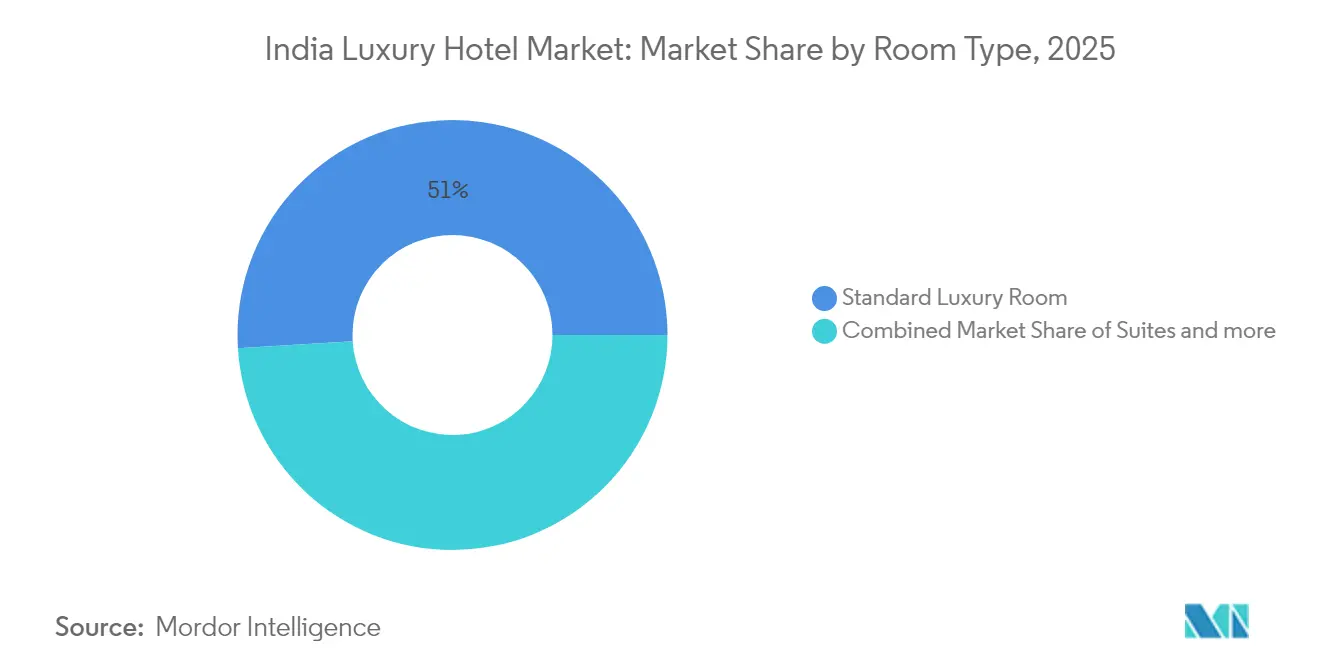

- By room type, standard luxury rooms commanded 50.98% of the India luxury hotel market share in 2025; villas/bungalows are expanding at a 12.1% CAGR to 2031.

- By booking channel, direct booking led with a 37.40% of the India luxury hotel market share in 2025 2025, whereas online travel agencies are forecast to rise at a 13.7% CAGR through 2031.

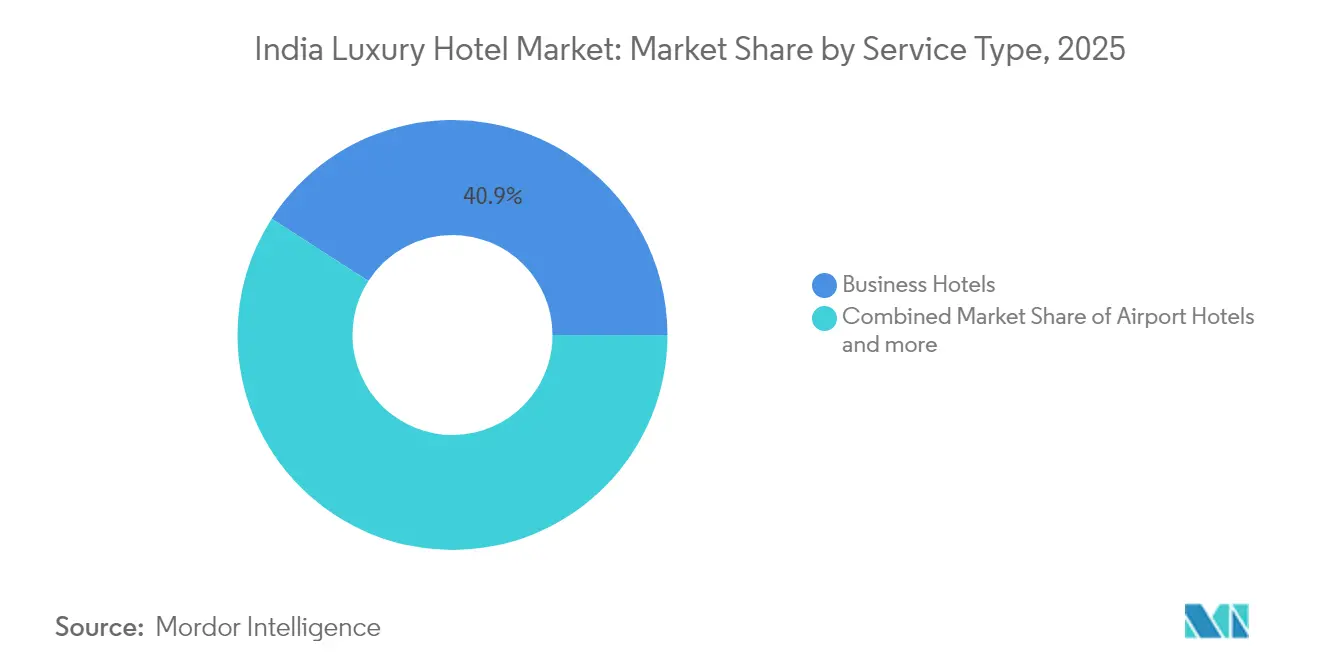

- By service type, business hotels accounted for 40.90% of the India luxury hotel market size in 2025, and resorts are set to grow at a 13.2% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Luxury Hotel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes & affluent base | +2.8% | Tier-I metros and fast-growing Tier-II cities | Long term (≥ 4 years) |

| Domestic luxury-staycation boom | +2.1% | Goa, Rajasthan, Kerala | Medium term (2-4 years) |

| International chains’ expansion inland | +1.9% | Tier-II cities such as Jaipur, Kochi, Indore | Long term (≥ 4 years) |

| CRZ-2019 beachfront unlock | +1.4% | Coastal states—Goa, Kerala, Tamil Nadu, Maharashtra | Medium term (2-4 years) |

| UHNW wedding demand surge | +1.8% | Rajasthan, Goa, Kerala, Uttarakhand | Medium term (2-4 years) |

| High-end medical-tourism recovery stays | +1.0% | Kerala, Karnataka, Tamil Nadu | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes and Affluent Domestic Traveller Base

The India luxury hotel market is underpinned by a swift rise in UHNW households, whose ranks are set to jump 50.1% by 2028. Nearly one-third of UHNW spending now flows into premium real estate and upscale experiences, prompting hotel chains to seed properties beyond metros into aspirational Tier-III towns. Credit-card outlays above INR 200,000 (USD 2,294.46) per year quadrupled in smaller cities, illustrating an untapped luxury appetite. Tata CLiQ Luxury reports that 55% of sales originate outside the eight largest metros, signaling a democratization of high-end consumption. Hyatt targets 100 domestic hotels by 2030, and Radisson plans 200 by 2027, each intentionally allocating pipelines to secondary and tertiary locations. The purchasing power that previously fueled outbound holidays—28.2 million departures in 2023, spending USD 17 billion—has begun to redirect toward local staycations. Together, these factors anchor a durable, long-range demand curve for premium hospitality products.

Domestic Luxury-Staycation Boom Post-COVID

Domestic leisure surged after pandemic-era travel restrictions, elevating nationwide occupancy to 67.5% in 2024—the highest in ten years. Average Daily Rates (ADR) for luxury hotels climbed to INR 8,055 (USD 92.38), confirming price resilience. High-net-worth households increasingly favor resort-style escapes within driving distance of major cities, a habit accelerated by health-security considerations and amplified by flexible work models. The branded rental villa sub-segment expanded from USD 329.6 million to an expected USD 1.377 billion by 2028, translating to a 33.2% CAGR, as guests opt for privacy-rich inventory such as pool villas and heritage bungalows. Jaipur, Goa, and Kochi now rank among the top leisure circuits, with over half of surveyed travelers planning another domestic vacation in the next 12 months. Contactless check-in, IoT housekeeping, and virtual concierge tools have become baseline expectations, reinforcing technology’s role in sustaining the staycation trend[2]Source: Hotelivate, “Sizing Up Indian Hospitality,” hotelivate.com.

Expansion of International Chains in Tier-I & Tier-II Cities

Branded key inventory is projected to jump from 180,000 rooms in FY 2024 to 300,000 by 2030, spearheaded by global operators scaling inland. Hilton’s Conrad Jaipur, Accor’s Sofitel Jaipur and Raffles Ranthambore, and Hyatt’s Grand Hyatt Indore typify an aggressive land-grab for first-mover advantage in high-growth provincial hubs. Tech centers such as Bengaluru catalyze this expansion, having expanded from 1,400 rooms in 2000 to 18,500 in 2023. Each new luxury key is estimated to create ten downstream jobs, magnifying socioeconomic impact. Better airlift is pivotal; India is on track to double operational airports within the decade, reducing travel times to previously inaccessible destinations. The compressed development cycle from announcement to opening averages five years for premium projects, reflecting both streamlined clearances and heightened capital efficiency. In aggregate, international participation elevates brand standards and encourages local operators to upgrade offerings.

Coastal Regulation Zone 2019 Unlock Enabling Beachfront Villas

CRZ-2019 amended setbacks and simplified environmental clearances, allowing resorts nearer to the shoreline and enabling a higher Floor Space Index in designated tourism nodes. Goa and Kerala have seen a pronounced uptick in applications for beachfront villas featuring private plunge pools and on-demand butler services. Luxury tented camps and beach clubs—once hampered by regulatory uncertainty—now benefit from a clearly defined approval pathway under CRZ-IIIA and IIIB rules. State governments deploy revenue-sharing land-lease models that lower upfront capital while ensuring public oversight. Concerns persist among fishing communities and conservation advocates, yet adaptive reuse of existing coastal structures has reduced ecological footprints. Early projects such as Accor’s Raffles Ranthambore signal the brand's appetite for combining natural assets with top-tier hospitality. Collectively, CRZ liberalization is expected to add 7,500 premium keys across coastal states by 2030[3]Source: Press Information Bureau, “Tourism Expansion in India,” pib.gov.in.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex & long pay-back | -1.8% | Nationwide, acute in greenfield projects | Long term (≥ 4 years) |

| GST 18% on luxury dining | -2.2% | Hotels with room tariffs above INR 7,500 (USD 85.99) | Short term (≤ 2 years) |

| Pronounced seasonality & monsoons | -1.5% | Goa, Kerala, Himachal Pradesh | Medium term (2-4 years) |

| Rising ESG compliance costs | -0.9% | Metros & new developments pursuing international certifications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex & Long Pay-Back Periods

Luxury construction averages INR 236.25 lakh (USD 270,896.66) per key—more than six-times budget-hotel ratios—and timelines frequently stretch beyond 40 months. Land acquisition, multi-agency clearances, and interest during construction elevate total project cost and extend the pay-back window. Roughly 30% of announced hotels stall mid-build from funding gaps or design revisions. Sector lobby groups seek infrastructure status for projects costing over INR 10 crore (USD 1.15 million) to unlock cheaper long-tenor credit. Notwithstanding these hurdles, the listed hospitality firms’ combined market capitalization leapt from INR 20,700 crore (USD 2,373.26 million) in 2015 to INR 250,000 crore (USD 28,675.86 million) in 2025, signaling investor faith in long-term returns. IHCL alone earmarked INR 5,000 crore (USD 573.52 million) for expansion under its “Accelerate 2030” plan, illustrating the scale necessary for portfolio depth. Developers are increasingly adopting asset-light management contracts to reduce balance-sheet leverage while preserving brand reach.

GST Slab (18%) Inflates Luxury Tariffs

Effective April 2025, dining at hotels with room rates above INR 7,500 (USD 85.99) now attracts an 18% GST, replacing the earlier 5% slab. Operators welcome the concomitant input-tax-credit benefit yet fear softer restaurant footfall as total bills rise sharply. The Federation of Hotel & Restaurant Associations of India continues to lobby for a uniform 12% structure, citing competitive disadvantages versus Thailand and Singapore, where tourism taxes are lower. Hotels may freeze room-rate hikes to keep tariff-inclusive value under the GST trigger, thereby squeezing RevPAR in the short term. Some operators are unbundling meal plans from packages to preserve headline rate optics. Technology-driven dynamic pricing is also being explored to optimize occupancy without breaching GST cut-offs during peak periods. While the rule is unlikely to derail demand fundamentally, it introduces revenue-management complexity for at least the next two fiscal cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Room Type: Villas Redefine Premium Personal Space

Standard Luxury Rooms led 2025 revenue with a 50.98% share, underscoring their universal appeal for corporate and leisure travelers seeking familiar luxury amenities. However, Villas/Bungalows are charting a 12.1% CAGR to 2031, signaling a pivot toward privacy, larger footprints, and bespoke services. The branded villa pipeline is expected to inject 27,000 keys into the India luxury hotel market, particularly across resort hubs in Goa and Kerala. Major chains now bundle villa stays with dedicated butlers, private plunge pools, and curated local excursions to justify nightly rates exceeding INR 50,000 (USD 573.61). Suites retained a 28.20% slice, buoyed by extended-stay executives and multi-generational families, while Penthouses & Presidential Suites, though only 5.10% of inventory, remain critical for brand positioning and high-margin ancillary spend. The India luxury hotel market size in Villas is projected to jump from USD 546.3 million to USD 857.9 million by 2029, reflecting escalating consumer willingness to pay for solitude and exclusivity.

Continued interest in home-style layouts, amplified by remote-work flexibility, underpins new product innovations such as modular villa clusters that hotels can rent as a single estate for destination weddings. Operators are also leveraging hybrid ownership models, pre-selling branded residences to finance development. Such initiatives shorten pay-back periods and create built-in demand through fractional-use owners. Sustainability certifications—using local materials and renewable power—are increasingly advertised as points of differentiation. Collectively, these factors ensure Villas/Bungalows will remain the fastest-expanding room category within the India luxury hotel market.

By Booking Channel: Digital Disruption Shifts Commission Economics

Direct Booking captured a 37.40% share in 2025 as brands reward loyalty-program members with room upgrades and flexible check-in. Yet Online Travel Agencies (OTAs) are surging at a 13.7% CAGR through 2031, propelled by comparison-site culture and personalized upsell algorithms that resonate with mobile-first consumers. OTAs already exceed 2019 transaction volumes by 52% across Asia, although commission structures of 15-25% dent hotel margins. To rebalance, groups deploy rate-parity clauses and guarantee best-price widgets on proprietary sites. Travel Agents/Tour Operators account for a 15.10% share, mostly channeling inbound groups and weddings requiring complex logistics. Corporate Contracts contribute another 14.80%, anchored in Fortune 500 headquarters across Delhi-NCR, Mumbai, and Bengaluru.

Customer-experience research shows 65% of guests prioritize seamless mobile check-in, prompting chains to integrate AI-driven chatbots that handle 70% of pre-arrival queries. Hotels also employ cloud-based revenue-management engines that recalibrate prices in real time to hedge high OTA cancellation rates. Ultimately, a balanced multichannel strategy appears optimal, ensuring brand control while tapping OTA reach. The evolution of distribution will decisively shape profitability in the India luxury hotel market over the next decade.

By Service Type: Resorts Capture Leisure Tailwinds

Business Hotels commanded 40.90% of 2025 revenue, supported by India’s expanding services economy and MICE demand centered on Delhi, Mumbai, and Bengaluru. Nevertheless, Resorts are slated to outpace all categories with a 13.2% CAGR to 2031, fueled by the wedding economy, wellness tourism, and a burgeoning bleisure culture. The India luxury hotel market size for Resorts is boosted by destination weddings valued at USD 603 million in annual hotel bookings, with palace conversions in Rajasthan and beachfront venues in Goa setting global benchmarks. Suite Hotels hold 12.10%, attracting expatriates and senior executives on long assignments. Airport Hotels, although just 8.20%, will scale as aviation capacity doubles foreign arrivals to a targeted 25 million by 2030.

Medical tourism acts as an ancillary growth engine; Kerala alone generates INR 100 crore (USD 11.47 million) monthly from high-end recovery stays that blend clinical care with spa-grade amenities. Other niche formats—eco-retreats, heritage havelis, and wellness ashrams—occupy the balance, yet punch above their weight in brand equity and occupancy yield. Over the forecast period, Resorts will remain the face of leisure-led diversification across the India luxury hotel market.

Geography Analysis

North India, accounting for 42.60% of 2025 revenue, benefits from Delhi-NCR’s diplomatic and corporate gravity, Rajasthan’s palace-driven wedding segment, and Uttarakhand’s luxury hill-station resorts. Indira Gandhi International Airport’s capacity expansion and expressway upgrades enable seamless multi-city itineraries that combine business and leisure. Luxury ADR in Delhi breached INR 11,000 (USD 126.14) during the 2023 G20 Summit, affirming pricing power in peak periods. The region’s mature infrastructure underpins an 7.7% CAGR to 2031, with growth pockets emerging in Agra, Lucknow, and Chandigarh.

South India secures a 24.10% share, anchored by Bengaluru’s IT corridor and Kerala’s wellness tourism. Bengaluru alone houses 18,500 branded rooms, the nation’s largest single city inventory. Kerala’s medical-value-travel ecosystem adds INR 100 crore (USD 11.47 million ) monthly to upscale hotel receipts, while Tamil Nadu’s temple circuits lure affluent cultural explorers. Projected growth stands at 9.6% CAGR through 2031, buoyed by coastal resort developments in the Andaman & Nicobar archipelago.

West India claims 22.70% share on the back of Mumbai’s financial-services concentration and Goa’s perennial beach appeal. Upcoming projects in Pune, Nashik, and Ahmedabad will diversify regional supply, sustaining a 8.7% CAGR. Meanwhile, East & North-East India though only 10.60% of 2025 revenue emerges as the fastest riser at a 14.6% CAGR, catalyzed by public-private flagship projects like Taj Vivanta Guwahati and DoubleTree Siliguri. Enhanced air links to Southeast Asia and government tourism incentives position the region as the next frontier in the India luxury hotel market.

Competitive Landscape

The Indian luxury hotel market is moderately concentrated, with the leading operators accounting for more than half of 2024 revenues, yet no single player holds more than a 25% share. Taj leads at 20%, supported by its 120-year legacy and a bold target of 700 hotels by 2030 under an INR 5,000 crore (USD 573.52 million) capex plan. Marriott follows closely at 18%, focusing on asset-light growth in Tier-II cities to limit capital exposure. ITC Hotels commands 12%, promoting its “Responsible Luxury” platform with over 60% renewable energy usage across premium properties. Oberoi and Radisson pursue divergent strategies—premium selectivity and Tier-III expansion, respectively.

Sustainability is becoming a major factor in corporate travel RFPs, with ITC setting benchmarks by recycling 100% of its wastewater and 99% of solid waste. Digital tools are also shaping competitive advantage, for instance, Taj’s advanced revenue-management systems enhance yield, while Hilton’s Connected Room allows personalized in-room experiences. Accor’s entry with its Fairmont, Raffles, and Sofitel brands in Rajasthan is intensifying brand competition. These developments are redefining guest expectations around sustainability and digital service delivery. Operators are increasingly investing to meet evolving standards and maintain relevance.

Opportunities for luxury expansion remain in East and North-East India, where branded supply is still limited. Hotel Polo Towers Group is investing INR 150 crore (USD 17.20 million) to build Nagaland’s first five-star hotels, signaling confidence in frontier markets. The competitive landscape now hinges on speed to market, ESG leadership, and technological innovation. Global and domestic brands are racing to secure first-mover advantages in emerging regions. This momentum is reshaping the structure and priorities of India’s luxury hospitality sector.

India Luxury Hotel Industry Leaders

The Indian Hotels Company Ltd (Taj)

Marriott International – India

ITC Hotels

EIH Ltd (Oberoi Group)

The Leela Palaces Hotels & Resorts

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ITC inaugurated ITC Royal Bengal in Kolkata after a INR 1,400 crore (USD 160.55 million) outlay, adding 456 keys and 61,000 sq ft of banqueting.

- April 2025: Fairmont Mumbai launched 446 Art Deco-inspired rooms, Accor’s second domestic Fairmont.

- April 2025: Hyatt announced six property signings totaling 1,350 keys across Ghaziabad, Kasauli, Kochi, Bhopal, Vithalapur, and Jaipur.

- April 2025: Accor inked Sofitel Jaipur Jawahar Circle (275 rooms) and Raffles Ranthambore (63 villas).

India Luxury Hotel Market Report Scope

A luxury hotel is a hotel that provides a luxurious accommodation experience to the guest. Luxury hotels typically accommodate high-paying guests, and the services and dining are expected to be high quality. A complete background analysis of the India Luxury Hotel Market, which includes an assessment of the emerging trends by segments and regional markets, significant changes in market dynamics, and a market overview, is covered in the report. The India Luxury Hotel Market is segmented by service type (Business Hotel, Airport Hotel, Suite Hotel, Resort & Spa, and others). The report offers market size and forecasts for the India Luxury Hotel Market in value (USD Million) for all the above segments.

By Room Type

| Standard Luxury Room |

| Suites |

| Villas / Bungalows |

| Penthouses & Presidential Suites |

By Booking Channel

| Direct Booking (Brand Website, Call Centre) |

| Online Travel Agencies (OTA) |

| Travel Agents / Tour Operators |

| Corporate Contracts |

By Service Type

| Business Hotels |

| Airport Hotels |

| Suite Hotels |

| Resorts |

| Other Service Types |

By Geography

| North India |

| South India |

| West India |

| East & North-East India |

| By Room Type | Standard Luxury Room |

| Suites | |

| Villas / Bungalows | |

| Penthouses & Presidential Suites | |

| By Booking Channel | Direct Booking (Brand Website, Call Centre) |

| Online Travel Agencies (OTA) | |

| Travel Agents / Tour Operators | |

| Corporate Contracts | |

| By Service Type | Business Hotels |

| Airport Hotels | |

| Suite Hotels | |

| Resorts | |

| Other Service Types | |

| By Geography | North India |

| South India | |

| West India | |

| East & North-East India |

Key Questions Answered in the Report

What is the current value of the India luxury hotel market?

It reached USD 4.05 billion in 2026 and is projected to hit USD 6.93 billion by 2031.

How fast is the segment for Villas and Bungalows growing?

Villas/Bungalows are expanding at a 12.1% CAGR, outpacing all other room categories.

Which region is forecast to grow fastest in premium hospitality?

East & North-East India is set to grow at a 14.6% CAGR through 2031 on new infrastructure and flagship projects.

How does the April 2025 GST change affect luxury hotels?

Dining bills at hotels charging above INR 7,500 (USD 85.99) per night now carry an 18% GST, which may dampen restaurant spend even as hotels gain input-tax credits.

Page last updated on: