Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 20.29 Billion |

| Market Size (2026) | USD 21.34 Billion |

| Market Size (2031) | USD 27.46 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Hospitality Market Analysis by Mordor Intelligence

The Canada Hospitality Market size was valued at USD 20.29 billion in 2025 and estimated to grow from USD 21.34 billion in 2026 to reach USD 27.46 billion by 2031, at a CAGR of 5.18% during the forecast period (2026-2031).

This growth reflects a sector that has moved beyond simple recovery to embrace a structural realignment driven by corporate sustainability mandates, mega-event preparations, and tighter short-term-rental regulations. Rising inbound tourism, particularly from the United States, is boosting average length of stay and pushing demand toward boutique hotels that provide authentic local experiences. Meanwhile, global chains leverage loyalty platforms and scale purchasing to defend share in major commercial corridors.

New hotel construction in Toronto, Vancouver, and Calgary indicates investor confidence despite elevated borrowing costs, while suburban and secondary markets attract projects that seek lower land prices and extended-stay demand. Corporate travel buyers, under net-zero commitments, have begun shifting room nights to properties with verified green credentials, an action that is accelerating capital upgrades across asset classes. Market dynamics reveal a sector transitioning from recovery to strategic repositioning, where traditional demand drivers intersect with sustainability imperatives and technology adoption. Corporate net-zero travel policies increasingly influence accommodation selection, while labor shortages force operational innovations that may permanently alter service delivery models [1]Tourism HR Canada, “Canadian Tourism Labour Market Snapshot: April 2025,” tourismhr.ca..

Key Report Takeaways

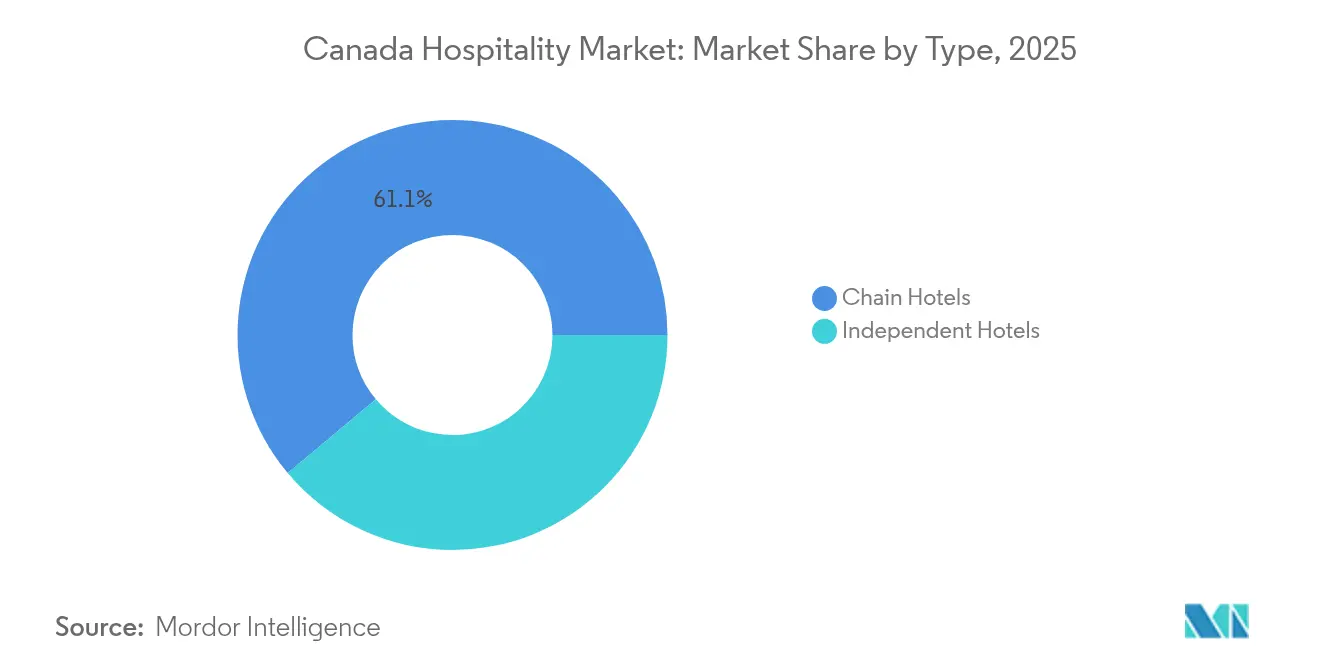

- By type, chain hotels held a 61.10% Canada hospitality market share in 2025, while independent hotels are expanding at a 5.25% CAGR through 2031.

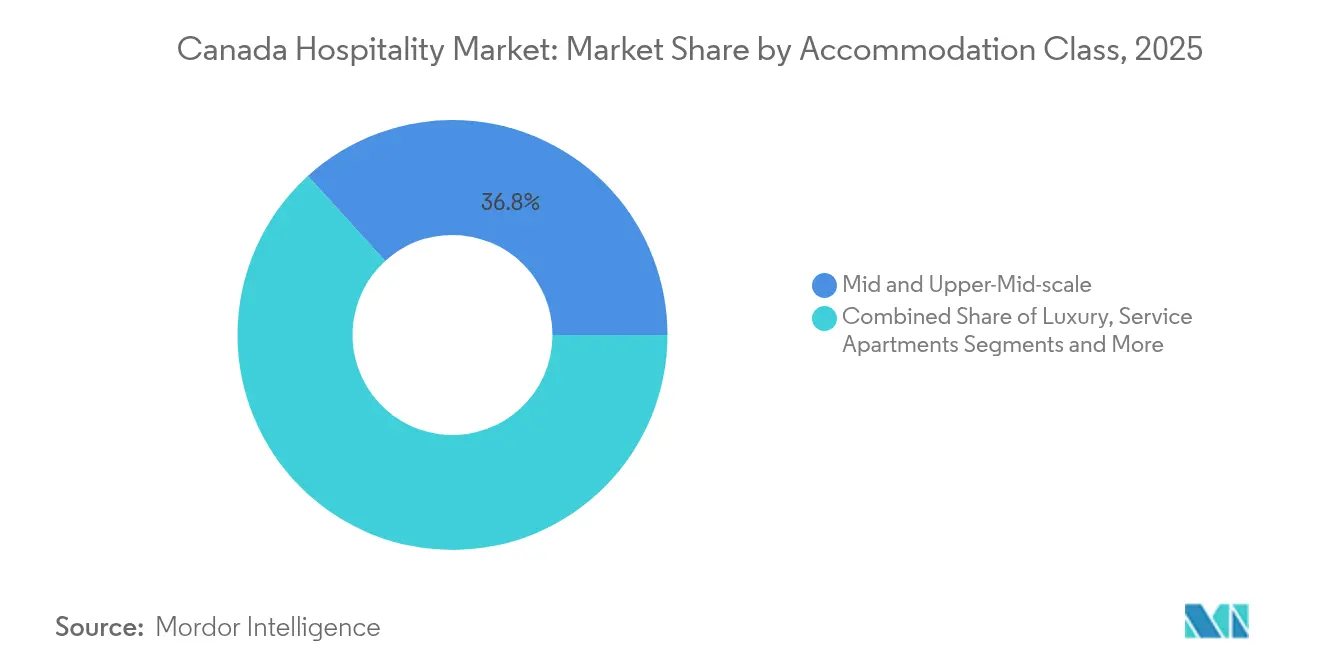

- By accommodation class, mid and upper-mid-scale properties commanded 36.75% of the Canada hospitality market size in 2025, and service apartments are projected to grow at a 6.05% CAGR to 2031.

- By booking channel, direct digital captured 42.80% of Canada hospitality industry share in 2025, yet online travel agencies are advancing at a 6.60% CAGR over the forecast horizon.

- By geography, Ontario led with 29.75% of Canada hospitality market share in 2025; British Columbia is forecast to record the fastest CAGR at 5.85% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Four-Season Tourism Economy Supporting Year-Round Resort Demand | 0.90% | Western Canada mountain resort corridors | Medium term (2–4 years) |

| Immigration-Led Population Growth Expanding Urban Accommodation Needs | 0.70% | Major Canadian metropolitan accommodation markets | Short term (≤ 2 years) |

| Outdoor Recreation Economy Driving Remote Destination Hospitality | 0.50% | Northern Canada adventure tourism regions | Long term (≥ 4 years) |

| Cross-Border Travel Advantage Supporting US Visitor Demand | 1.10% | Ontario, BC, Quebec gateway corridors | Short term (≤ 2 years) |

| Growth of Extended-Stay Accommodation Models | 0.60% | Major urban business travel hubs | Medium term (2–4 years) |

| Major International Events Enhancing Destination Visibility | 0.40% | Major event-hosting metropolitan cities | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Four-Season Tourism Economy Supporting Year-Round Resort Demand

Canada’s geography supports a diversified, four-season tourism economy that sustains hotel and resort demand year-round and reduces reliance on a single weather window. Statistics Canada recorded 29.8 million international visitor trips in 2024, with tourism expenditure reaching CAD 129.7 billion (USD 94.72 billion). Domestic tourism accounted for 76% of total tourism, or CAD 98.6 billion (USD 72.0 billion), supporting demand during shoulder and off-peak periods[2]Statistics Canada, “The Daily - Travel Between Canada and Other Countries, June 2025. The ski sector anchors winter resort demand. The Canada West Ski Areas Association reported 9.8 million skier visits across Western Canada in the 2024/25 season, up from 8.75 million in 2023/24 and the second-highest level on record. British Columbia’s ski sector generated CAD 562.1 million (USD 410.5 million) in operating revenue in 2023–24, followed by Quebec, Alberta, and Ontario. Resorts are also investing in summer programming, bike parks, culinary offerings, and wellness infrastructure. Big White Ski Resort recorded an 83% increase in website interest between 2015 and 2024.

Immigration-Led Population Growth Expanding Urban Accommodation Needs

Canada's immigration-led population growth continues to support urban hospitality demand, particularly in accommodation and extended-stay segments serving newcomers, corporate travelers, and business visitors linked to migrant workers and related industries. Statistics Canada reported that international migration accounted for 98.5% of the total population growth of 62,401 people in Q4 2024 and 97.3% of the full-year growth of 724,586 people in 2024. Canada welcomed 483,591 permanent immigrants in 2024, the highest annual total since 1972. Immigrant concentration in Toronto, Vancouver, Montreal, Calgary, and Ottawa supports demand for extended-stay accommodation, serviced apartments, and budget hotels during settlement, when new residents often need temporary housing. The accommodation services subsector recorded CAD 35.9 billion (USD 26.22 billion) in revenue in 2024, up 2.9% from 2023, while hotels, motor hotels, and motels generated CAD 30.0 billion (USD 21.91 billion). The 2025–2027 Immigration Levels Plan targets 395,000 permanent residents in 2025, 380,000 in 2026, and 365,000 in 2027, sustaining demand for transitional and short-term accommodation.

Outdoor Recreation Economy Driving Remote Destination Hospitality

Canada's outdoor recreation and ecotourism economy supports remote and wilderness hospitality by driving demand for lodges, camps, and boutique accommodations in regions with limited commercial investment. In summer 2024, the Government of Canada, through the Canadian Northern Economic Development Agency (CanNor), invested nearly CAD 800,000 (USD 584,288) in seven Yukon tourism projects covering accommodation upgrades, green energy transitions, and ecotourism programming[3]Travel And Tour World, “Yukon’s Tourism Sector Receives CAD 800K Investment for Growth and Accessibility. CanNor later announced another CAD 800,000 (USD 584,288) for seven tourism projects across the North, targeting infrastructure upgrades, eco-tourism and Indigenous cultural tourism experiences, additional accommodation options, and year-round operations. Indigenous-led tourism remains a growth segment, supported by the CAD 10 million (USD 7.30 million) Signature Indigenous Tourism Experiences Stream (SITES), administered by NACCA and representing over 50 Indigenous financial institutions. The Alberta Rockies recorded 793,000 visits in August 2024, up 6.0% year-over-year, while visits in March 2024 reached 516,000, up 98.5% from March 2019, showing strong seasonal demand. Yellowknife's hotel occupancy is projected to reach 77% in 2025, with an average room rate of CAD 208 (USD 151.91), while Airbnb searches grew 85% between 2023 and 2025.

Cross-Border Travel Advantage Supporting US Visitor Demand

The United States remains Canada’s largest international tourism source market. Geography, a shared language, cultural affinity, and CUSMA trade integration support large cross-border travel flows for the Canadian hospitality market, despite headwinds in 2025. Statistics Canada recorded 23.5 million trips to Canada by United States residents in 2024, up 10.7% from 2023, representing 78.7% of non-resident trips and CAD 15.6 billion (USD 11.39 billion) in spending. Accommodation accounted for 35.8% of non-resident visitor spending, the highest tourism expenditure category, supporting hotel and lodging revenues across Canada’s provinces. TIAC identified the United States and Mexico as Canada’s most critical source markets and proposed a Travel and Tourism Trade Working Group under the CUSMA joint review. OECD reported that travel accounted for 29.9% of Canada’s service exports in 2025 and supported 702,650 jobs. Although United States automobile arrivals fell 7.4% in July 2025, air arrivals rose 0.7%, indicating continued structural resilience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geographic Dispersion Creates Operational Challenges Across Remote Hospitality Markets | −0.5% | Northern and rural tourism regions | Long term (≥ 4 years) |

| Severe Seasonality Drives Revenue Volatility in Leisure-Focused Destinations | −0.6% | Major resort market seasonality | Medium term (2–4 years) |

| High Construction Costs Limit the Feasibility of New Hotel Developments | −0.7% | Major urban operating cost pressures | Medium term (2–4 years) |

| Persistent Labor Shortages Affect Hospitality Service Delivery | −0.6% | Western and northern labor shortages | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Geographic Dispersion Creates Operational Challenges Across Remote Hospitality Markets

Canada's geographic scale creates operational challenges for hospitality businesses in remote and dispersed markets, especially in the territories and northern regions, where infrastructure gaps raise costs and limit profitability and scalability. The OECD Tourism Trends and Policies 2026 report notes that tourism remains concentrated along a narrow southern corridor, leaving large wilderness and cultural tourism areas underserved because remote infrastructure is costly and complex to build and maintain. Destination Canada's Northern Indigenous Lodge Network Strategy identifies accessibility as a key constraint, noting that airports and alternative modes of transportation are essential to improving connectivity for visitors and residents. In Yukon, remoteness continued to restrict tourism growth, with air capacity remaining below pre-pandemic levels and labor challenges requiring targeted recruitment and retention plans. Remote wilderness lodges rely heavily on the short peak season, creating cash flow pressure and limiting investment in upgrades, staffing, and marketing. Destination Canada's outlook also prioritizes demand growth in seasons and places with available capacity, reflecting uneven supply and demand across the country.

Severe Seasonality Drives Revenue Volatility in Leisure-Focused Destinations

Seasonal demand concentration remains a key structural restraint on the Canadian hospitality industry, creating intra-year revenue swings that affect the financial viability and investment appeal of leisure-focused accommodation assets. Sun Peaks Resort’s five-year MRDT Strategic Business Plan states that April-to-November occupancy averages about 28%, compared with peak winter occupancy above 75%, and targets 32–35% off-peak occupancy by 2030. Statistics Canada reported that Canadian residents took 117.7 million trips in Q3 2025, the annual peak, while domestic visits fell to 74.9 million in Q4 2025, down 6.2% year over year. Downhill ski facilities recorded a 4.4% decline in operating revenue in winter 2024 compared with 2023 highs, highlighting exposure to weather and sentiment shifts[4]Statistics Canada, “Downhill Skiing Hit a Rough Patch in the Winter of 2024. Leisure operators must use peak-season revenue to cover fixed costs during low-revenue months. Alberta’s 28.8% share of “other accommodation industries” revenue in 2024 further shows dependence on seasonal or project-driven demand

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Independent Properties Gain Momentum

Independent hotels are projected to achieve a 5.25% CAGR through 2031, surpassing the overall Canada hospitality market growth and eroding the dominance of global chains. The segment’s agility allows operators to pivot quickly toward thematic décor, hyper-local food sourcing, and neighborhood storytelling, which resonate with millennial and Gen Z travelers who perceive authenticity as a primary value driver. Chain brands, however, still benefit from centralized procurement and loyalty-program capture, enabling them to defend a 61.10% revenue lead in 2025. Many independents now affiliate with soft-brand collections or third-party managers to tap into global distribution while retaining unique identities, balancing independence with reach. Sustainability certifications, from LEED to Green Key, act as competitive equalizers because smaller properties can often retrofit more quickly than legacy high-rise assets. Analysts expect the coexistence of both models: large chains will supply standardized reliability for corporate road warriors, while boutique independents will fill experiential niches, together sustaining a diverse Canada hospitality market ecosystem.

The scale-versus-character divide opens acquisition prospects for investors specialized in repositioning under-performing independents into curated lifestyle assets. Provincial governments provide renovation tax credits that reduce capital outlays for heritage building conversions, encouraging adaptive reuse strategies. Technology vendors cater to independents with cloud-based PMS platforms that lower upfront capex and integrate seamlessly with OTA channels. As wage costs climb, chain operators may experiment with lean-staff prototypes that emulate independent hotel intimacy but maintain brand standards. The competitive outcome hinges on guest loyalty economics: if personalized service and local immersion carry higher repeat-visit propensity, independents could command premium ADR and maintain share gains despite scale disadvantages.

By Accommodation Class: Service Apartments Lead Growth

Service apartments are forecast to expand at a 6.05% CAGR, reflecting the mainstreaming of hybrid work and extended business assignments that blur leisure and corporate segments. Average stays of 54 nights translate into stable occupancy and reduce marketing churn, enhancing margin resilience relative to transient-led luxury hotels. Mid and upper-mid-scale properties retained 36.75% of the Canada hospitality market share in 2025, capturing guests who demand full-service convenience without luxury price points. Luxury flags confront margin erosion as corporate travel policies emphasize duty-of-care compliance over prestige, channeling executive room nights to brands that deliver wellness amenities and environmental transparency. Budget and economy hotels stand to benefit from the short-term-rental crackdown, yet labor scarcity constrains their ability to open all available room inventory. Owners of extended-stay brands such as Candlewood Suites and Staybridge Suites plan 16 new Canadian locations, suggesting that capital flows will continue favoring residential-style layouts.

Guest feedback indicates rising preference for in-room kitchens, laundry facilities, and flexible workspace, all of which increase average revenue per stay through ancillary sales. Operators of service apartments negotiate corporate housing agreements that lock in minimum occupancy thresholds, insulating them from seasonality shocks. Real estate investment trusts view this asset class as a hedge against economic cycles because guests with relocation or project assignments exhibit inelastic demand. Sustainability retrofits pay off quickly given longer dwell times and lower energy variability per guest night. Developers also cite zoning advantages: municipalities eager to add housing supply often approve extended-stay projects faster than conventional hotels, accelerating market entry. In net effect, the accommodation mix is tilting toward formats optimized for longer stays, a trend likely to remain entrenched well beyond 2030.

By Booking Channel: OTA Acceleration Challenges Direct Bookings

Online travel agencies are expected to grow at a 6.60% CAGR to 2031, even though direct digital channels accounted for a 42.80% revenue lead in 2025. Intensified meta-search advertising has raised cost-per-click by 62.5%, prompting hotels to reevaluate marketing spend efficiency relative to OTA commissions. Loyalty programs remain a bulwark for chains, but independents find it economical to lean on OTA reach, despite margin dilution. Corporate buyers increasingly adopt integrated online booking tools that automatically compare brand sites with OTA-negotiated rates, reducing leakage from preferred channels. Regulatory scrutiny concerning data privacy may force platforms to adopt transparent pricing displays, slightly leveling the playing field. Hotels experiment with member-only rates, gift-card incentives, and digital concierge experiences that enhance the perceived value of direct booking without eroding public ADR.

Artificial-intelligence chatbots and dynamic packaging engines promise to streamline conversion funnels, yet require investment that smaller properties cannot always justify. Some owners enter white-label partnerships where technology providers manage the full direct-booking stack in exchange for variable fees aligned with performance. Meanwhile, wholesale and traditional agency segments continue to slide as digitally native travelers bypass intermediaries. OTA loyalty tiers, such as Genius and Expedia OneKey, expand benefits scopes, further complicating hotel attempts to lure repeat guests to proprietary apps. The ultimate channel equilibrium will hinge on whether hotels can sustain differentiated service propositions that offset commission savings against rising customer-acquisition costs. For now, dual-channel strategies remain essential within the Canada hospitality market playbook.

Geography Analysis

Ontario maintained 29.75% of national revenue in 2025, anchored by Toronto’s status as the primary corporate gateway and Ottawa’s steady government-driven demand. The province leverages proximity to U.S. border crossings, a diversified economy, and established transportation infrastructure to capture year-round occupancy. Office-to-hotel conversions in downtown Toronto relieve inventory shortages while revitalizing under-utilized buildings, aligning real estate supply with evolving work-from-anywhere patterns. Growth, however, moderates as the market approaches maturity and faces competition from regions promising higher yields. Provincial tourism initiatives continue to target high-value international visitors rather than pure volume, reinforcing ADR strength. Investors remain confident, but acquisition yields have compressed, leading some funds to pivot toward suburban assets with value-add potential.

British Columbia records the fastest provincial trajectory with a 5.85% CAGR forecast through 2031, fueled by Vancouver’s FIFA 2026 preparations and chronic hotel undersupply that underpins pricing power. Victoria benefits from Indigenous tourism alliances and green-travel branding, drawing visitors who prioritize low-carbon itineraries. Whistler’s transition into a four-season destination showcases diversification away from snow-reliant revenue streams. The province’s restriction on entire-home short-term rentals redirects budget travelers toward regulated hotels, buffering occupancy outside peak summer months. Infrastructure upgrades, including Vancouver International Airport’s terminal expansion, further enhance capacity to absorb future demand. Development costs remain high, yet investor appetite persists due to above-national ADR and RevPAR metrics.

Alberta and Atlantic Canada emerge as growth corridors driven by energy-sector rebound and authentic cultural offerings, respectively. Calgary’s Stampede Park redevelopment positions the city as a meeting-conventions-incentives hub, while Edmonton capitalizes on industrial diversification into technology and film production. Halifax, benefitting from expanded cruise schedules and military procurement activity, demonstrates outsized weekday occupancy relative to population size. Saskatchewan and Manitoba nurture niche opportunities in agro-tourism and Indigenous heritage trains, providing counter-seasonal revenue streams that even out cash flow volatility. The Territories, though currently small in absolute terms, lure high-spend adventure travelers to luxury eco-lodges linked by charter flights, underpinning long-run potential for upscale expansion. Geographic diversification remains a core strategy for national operators seeking to hedge against localized economic shocks.

Competitive Landscape

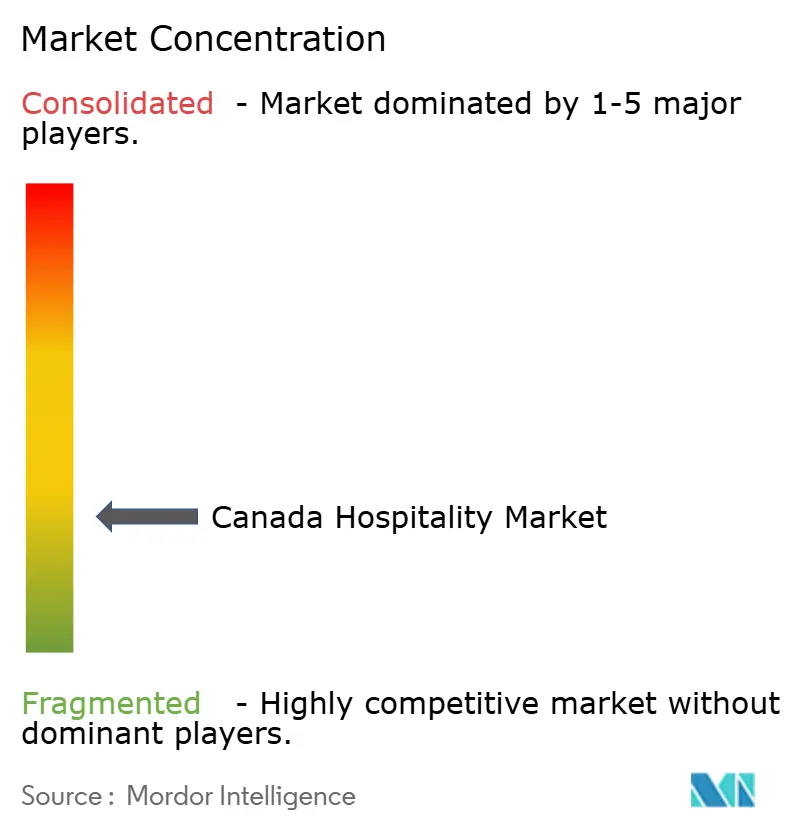

The Canada hospitality market displays moderate fragmentation, with the leading companies have significant share in the market. Marriott International and Hilton have domoianting share reflect the power of global distribution systems and robust loyalty ecosystems, which secure preferred corporate agreements and group contracts. Accor continues to roll out lifestyle-oriented collections, such as the Emblems brand debuting in Banff, to capture upscale leisure demand. Regional players like Sandman and Germain Hotels exploit local market knowledge and development agility to convert office towers and heritage buildings into differentiated assets. Investment funds enter management partnerships when they see upside in repositioning or scaling independent portfolios.

Strategic differentiation revolves around three archetypes: international giants expanding via franchise and management models; domestically anchored brands emphasizing regional authenticity; and asset-light investors assembling diversified portfolios for operational optimization. Technology adoption has become a competitive fulcrum as properties deploy mobile keys, AI-enabled revenue-management systems, and frictionless payment solutions to enhance guest satisfaction while controlling labor expenses. Sustainability credentials serve as tiebreakers in corporate bidding, pushing operators to commit to science-based emission targets and transparent reporting. The ongoing consolidation trend is selective: well-capitalized buyers pursue distressed or under-managed assets, but valuation gaps persist between sellers’ expectations and higher-interest-rate realities.

White-space opportunities remain plentiful in secondary markets lacking branded inventory, in extended-stay concepts that cater to hybrid workforces, and in Indigenous-led developments where cultural storytelling is a unique selling proposition. Disruptors include corporate housing specialists negotiating master leases, and co-living platforms that blur the boundary between residential and transient lodging. Global chains experiment with subscription-style memberships that guarantee nightly credits worldwide, a model geared toward digital nomads. Competitive dynamics also hinge on evolving distribution tactics; players who master direct-to-consumer engagement without elevating acquisition costs will secure superior margins. Sustained market share advances will likely stem from nimble capital deployment, guest-centric innovation, and disciplined cost structures rather than sheer scale alone.

Canada Hospitality Industry Leaders

Accor S.A.

Hilton Worldwide

IHG Hotels & Resorts

Marriott International

Best Western Hotels & Resorts

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The Rimrock Banff joined Accor’s Emblems Collection following a USD 100 million renovation introducing new wellness amenities.

- May 2025: Hilton confirmed Canada’s first Tempo by Hilton near Toronto Pearson Airport, a 193-room wellness-focused hotel set to open in 2028.

- April 2025: AC Hotel by Marriott Ottawa Downtown opened with 159 rooms and EV-charging infrastructure, marking RIMAP Hospitality’s entry into the capital.

- March 2025: Germain Hotels and Reliance Properties announced a 180-room Le Germain Hotel Vancouver conversion targeting a 2029 opening.

Canada Hospitality Market Report Scope

The hospitality industry comprises services such as lodging, food and drinks service, event planning, theme parks, travel, and tourism. It also covers hotels, tourism agencies, restaurants, and bars. The hospitality industry in Canada is segmented by type and segment. By type, the market is segmented into chain hotels and independent hotels. By segment, the market is segmented into service apartments, budget and economy hotels, mid and upper-mid-scale hotels, and luxury hotels. The report offers a forecast and market size for the Canadian hospitality industry in value (USD billion) for all the above segments.

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| Ontario |

| Québec |

| British Columbia |

| Alberta |

| Saskatchewan |

| Manitoba |

| Atlantic Canada |

| Territories |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | Ontario |

| Québec | |

| British Columbia | |

| Alberta | |

| Saskatchewan | |

| Manitoba | |

| Atlantic Canada | |

| Territories |

Key Questions Answered in the Report

How large is the Canada hospitality market in 2026?

The market generated USD 21.34 billion in 2026 and is on track to reach USD 27.46 billion by 2031.

What is the projected growth rate for Canadian hotels through 2031?

The sector is forecast to expand at a 5.18% CAGR over the 2026-2031 period.

Which province is growing fastest in hotel revenue?

British Columbia is expected to post a 5.85% CAGR through 2031, driven by FIFA 2026-linked demand and a persistent room shortage.

Which hotel segment is seeing the quickest expansion?

Service apartments are leading, with a projected 6.05% CAGR thanks to longer stays by remote workers and project-based travelers.

How are corporate sustainability goals affecting hotel choices?

Companies are directing bookings toward properties with verified green credentials, boosting demand for hotels that invest in energy efficiency and carbon reporting.

What share of rooms do the top five hotel operators hold in Canada?

The leading five brands control 36.6% of available rooms, reflecting a moderately fragmented competitive landscape.

Page last updated on: