Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

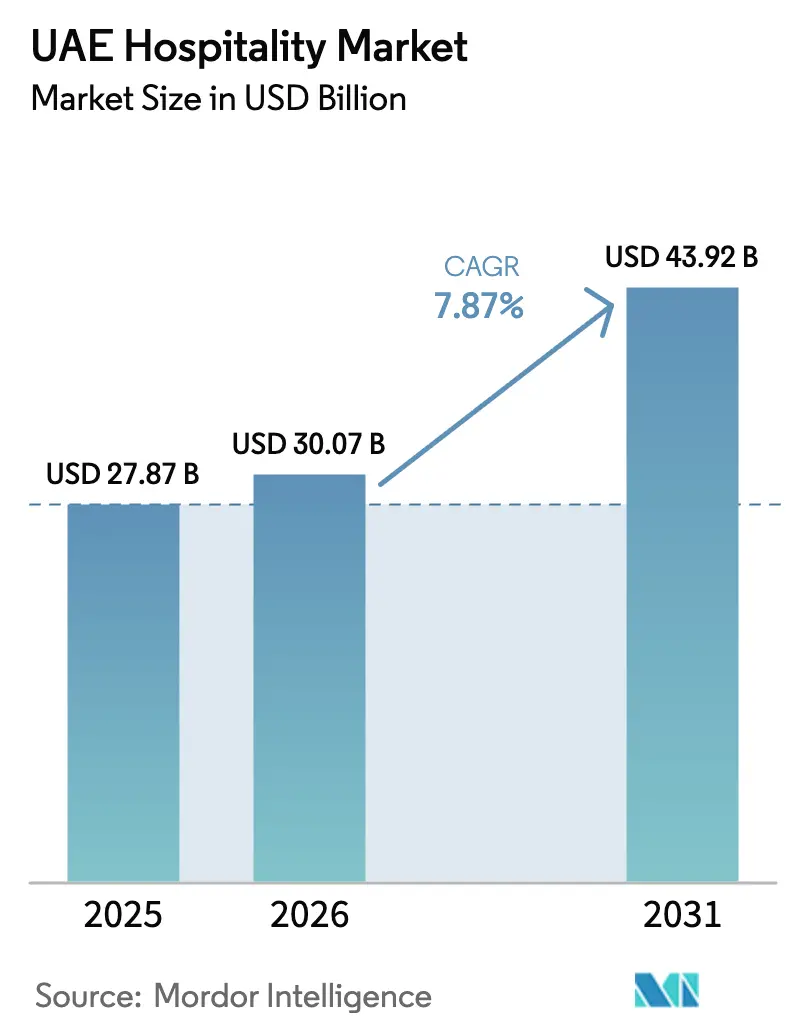

| Base Year Market Size (2025) | USD 27.87 Billion |

| Market Size (2026) | USD 30.07 Billion |

| Market Size (2031) | USD 43.92 Billion |

| Growth Rate (2026 - 2031) | 7.87% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

UAE Hospitality Market Analysis by Mordor Intelligence

The UAE Hospitality Market size is projected to expand from USD 27.87 billion in 2025 and USD 30.07 billion in 2026 to USD 43.92 billion by 2031, registering a CAGR of 7.87% between 2026 to 2031.

Growth is driven by policy initiatives, demand diversification, and rapid development cycles, enhancing operational efficiency across asset classes. The Tourism Strategy 2031 aims to attract 40 million hotel guests and increase tourism’s contribution to non-oil GDP, emphasizing the market's strategic importance for sustainable growth. Expo City Dubai’s legacy infrastructure supports year-round demand through MICE and mixed-use developments, boosting premium ADR in key locations. Distribution channels are evolving, with OTAs remaining significant while direct digital platforms grow, aided by loyalty programs and government-led digitization, improving operator margins. New entertainment and integrated-resort projects in Ras Al Khaimah are driving longer stays and higher visitor spending, strengthening medium-term growth prospects for the UAE hospitality market.

Key Report Takeaways

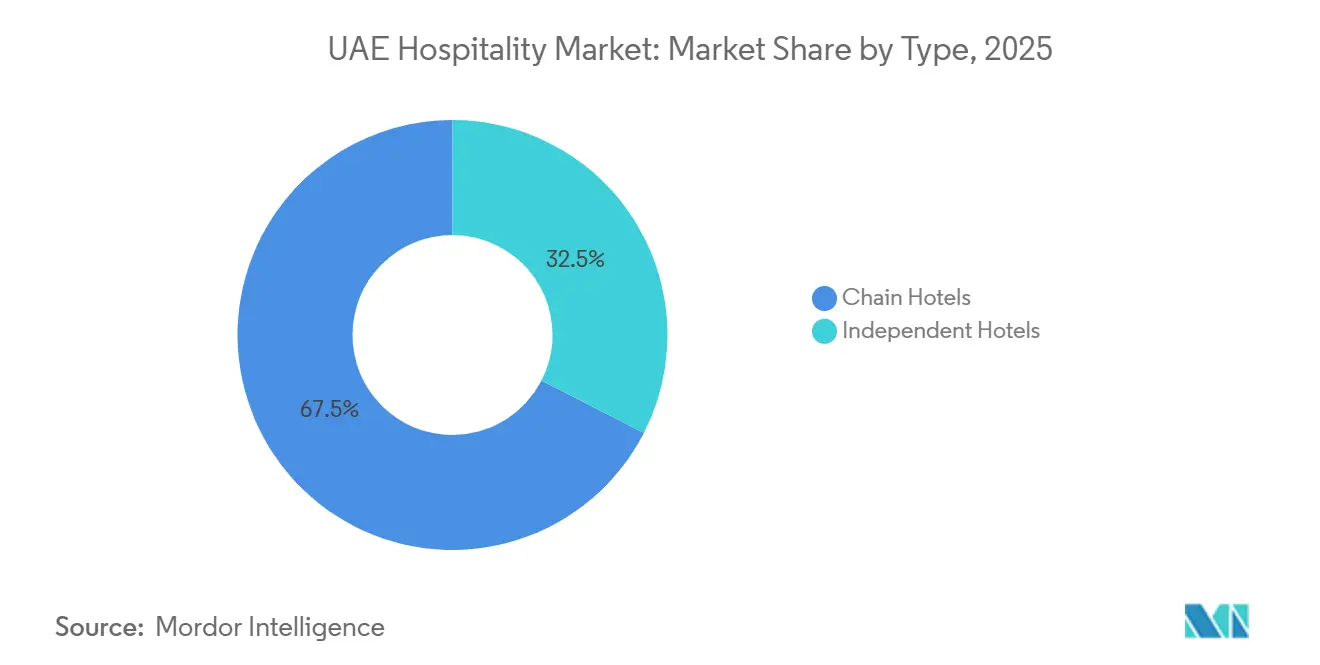

- By type, chain hotels held 67.47% of the UAE hospitality market share in 2025. Independent hotels recorded the highest projected CAGR at 10.35% through 2031.

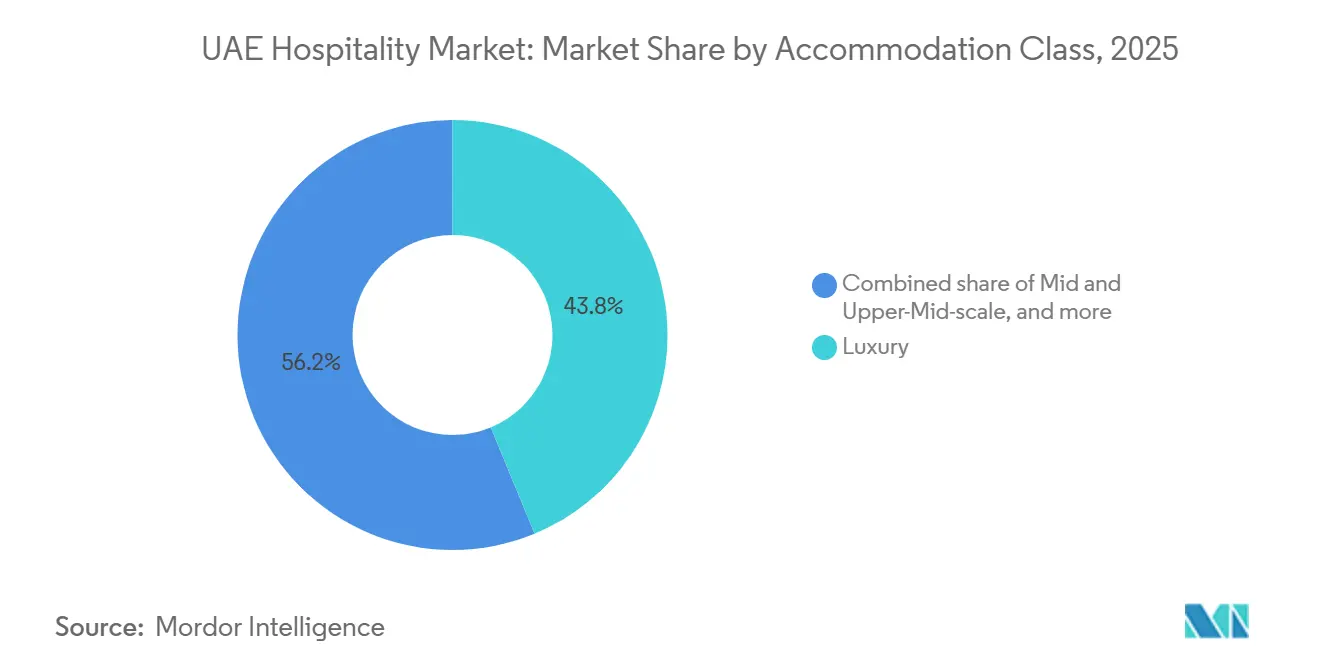

- By accommodation class, luxury properties accounted for 43.76% share of the UAE hospitality market size in 2025. Service apartments are forecast to expand at an 11.76% CAGR through 2031.

- By booking channel, OTAs held 51.76% of the UAE hospitality industry share in 2025. Direct digital channels recorded the fastest projected growth at a 14.48% CAGR through 2031.

- By geography, Dubai captured 63.49% of keys in 2025. Ras Al Khaimah is projected to be the fastest-growing emirate at a 10.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Timeline |

|---|---|---|---|

| Transformation Into a Global Lifestyle and Entertainment Destination | 1.20% | Lifestyle and leisure districts | Short term (≤ 2 years) |

| High-Net-Worth Visitor Economy Supporting Premium Spending | 0.90% | Ultra-luxury hospitality clusters | Short term (≤ 2 years) |

| Free Zone Economy Creating International Business Visitor Demand | 0.80% | Business and free zone corridors | Medium term (2–4 years) |

| Mixed-Use Real Estate Models Integrating Hospitality Assets | 0.70% | Mixed-use hospitality developments | Long term (≥ 4 years) |

| Mega-Attraction Ecosystem Expanding Leisure Tourism Segments | 0.80% | Theme park entertainment hubs | Medium term (2–4 years) |

| Family Entertainment and Indoor Tourism Supporting Year-Round Visits | 0.60% | Indoor leisure destinations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Transformation Into a Global Lifestyle and Entertainment Destination

The UAE has evolved into a global lifestyle and entertainment destination, creating a strong foundation for hospitality growth. The National Tourism Strategy 2031 targets 40 million hotel guests and a tourism GDP contribution of AED 450 billion (USD 122.53 billion). Dubai welcomed 18.72 million international visitors in 2024, while national hotels achieved 78% occupancy and AED 45 billion (USD 12.25 billion) in revenue. Strong aviation connectivity and the D33 Economic Agenda continue supporting long-term tourism expansion. These structural initiatives are expected to sustain hospitality demand over the forecast period.

High-Net-Worth Visitor Economy Supporting Premium Spending

The UAE's growing high-net-worth population is strengthening demand for luxury hospitality and premium experiences. In 2024, the country attracted 7,200 new millionaires, increasing the HNWI population to 130,500. Luxury travelers contribute significantly to hotel, wellness, and branded residence revenues throughout the year. Around 43% of the hotel pipeline targets luxury properties, while Abu Dhabi recorded 24% RevPAR growth in luxury hotels during 2025. Continued visa reforms and luxury investments are expected to sustain premium hospitality growth[2]UAE Ministry of Economy, "National Tourism Strategy 2031," UAE Ministry of Economy, moec.gov.ae.

Free Zone Economy Creating International Business Visitor Demand

The UAE's network of over 40 free zones generates consistent business travel and year-round MICE demand. Corporate travel, exhibitions, and conferences support high hotel occupancy and premium accommodation demand. DWTC generated AED 25 billion (USD 6.80 billion) in economic output during 2025, while Abu Dhabi welcomed 2.2 million MICE delegates. Exhibition calendars remain strong through 2028, supporting continued hospitality growth. Expanding economic partnerships further strengthen the UAE's position as a global business hub[3]Department of Culture and Tourism – Abu Dhabi, "Business Events and MICE Performance Report 2025," DCT Abu Dhabi, dct.gov.ae.

Mixed-Use Real Estate Models Integrating Hospitality Assets

Large mixed-use developments are integrating hotels, residences, retail, and entertainment into self-sustaining hospitality ecosystems. Major projects, including Fahid Island, The Alba, and Mina masterplan, combine luxury hotels with residential communities. Branded residences help finance hotel development while generating year-round demand. Around 60% of Dubai's future hotel supply is expected to be delivered within mixed-use projects. This model enhances long-term revenue stability beyond traditional tourism demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Restraint | (~) % | Geographic Relevance | Timeline |

|---|---|---|---|---|---|

| High Competition Among Luxury Hospitality Destinations Pressuring Differentiation | −0.7% | High Competition Among Luxury Hospitality Destinations Pressuring Differentiation | −0.7% | Dubai prime districts and luxury corridors | Medium term (2–4 years) |

| Dependence on International Visitors Creates Exposure to Global Travel Disruptions | −0.8% | Dependence on International Visitors Creates Exposure to Global Travel Disruptions | −0.8% | Dubai Airport, Abu Dhabi, northern emirates | Short term (≤ 2 years) |

| Oversupply Risk in Premium Hotel Segments Due to Rapid Accommodation Expansion | −0.7% | Oversupply Risk in Premium Hotel Segments Due to Rapid Accommodation Expansion | −0.7% | Dubai and Abu Dhabi luxury clusters | Medium term (2–4 years) |

| Climate Conditions and Seasonality Challenges Affect Outdoor and Resort Operations | −0.5% | Climate Conditions and Seasonality Challenges Affect Outdoor and Resort Operations | −0.5% | Ras Al Khaimah, Fujairah, UAE coast | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||||

High Competition Among Luxury Hospitality Destinations Pressuring Differentiation

Intensifying competition from regional destinations and the expansion of luxury hotel supply are increasing pressure on the UAE hospitality market. Countries including Saudi Arabia, Qatar, and the Maldives are targeting similar high-value travelers. Nearly 43% of the UAE's hotel pipeline focuses on luxury properties, increasing competitive intensity. Greater supply makes pricing and service differentiation more challenging. Rising guest expectations further pressure premium hotel profitability[4]Department of Economy and Tourism – Dubai, "Dubai Tourism Performance Report 2025," Dubai Department of Economy and Tourism, dubaidet.gov.ae.

Dependence on International Visitors Creates Exposure to Global Travel Disruptions

The UAE hospitality market remains highly dependent on international tourism, making it vulnerable to global travel disruptions. Regional conflicts and aviation restrictions in early 2026 significantly reduced hotel occupancy and revenues. Dubai hotel occupancy temporarily fell to 15–20% from normal seasonal levels. Recovery is expected to depend on restoring international traveler confidence. Market diversification efforts continue, but global connectivity remains critical.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Chain Dominance Meets Boutique Insurgency

Chain hotels dominated 67.47% of the market in 2025, supported by global distribution systems, loyalty programs, and standardized operations that scale efficiently across urban and resort locations. Major operators are expanding inventory and diversifying brand portfolios with new lifestyle and upper-upscale properties to meet segmented demand in key micro-markets. Brand launches and conversions in high-traffic areas enhance network coverage, strengthening corporate engagement and event-driven business opportunities. Pipeline projects focus on landmark developments serving as hubs for leisure and MICE (Meetings, Incentives, Conferences, and Exhibitions), ensuring chain hotels remain central to city narratives. Owner-operators use brand standards and centralized procurement to maintain margins while tailoring experiences to local preferences.

Independent and emerging hospitality concepts are expected to grow at a 10.35% CAGR through 2031, driven by experience-focused positioning, flexible space utilization, and local partnerships that enhance guest experiences across neighborhoods and resort areas. Boutique and lifestyle properties emphasize unique identities through design, F&B offerings, wellness initiatives, and art collaborations, appealing to younger and repeat travelers. Regional developers and owner-operators contribute by launching curated luxury and premium-lifestyle properties, strengthening destination narratives and value creation. Licensing and classification frameworks establish transparent standards while fostering innovation in service delivery, promoting sustainable growth for both branded and independent operators. This dual-paced structure sustains competitive dynamics, benefiting guests and enhancing operational discipline across the UAE hospitality industry.

By Accommodation Class: Luxury Leadership Amid Service-Apartment Surge

Luxury properties held a 43.76% share of the UAE hospitality market size in 2025, supported by investments in flagship hotels and branded residences. These projects enhance high-end options and global recognition. Developments in coastal and urban areas boost destination appeal, allowing operators to focus on culture, gastronomy, and wellness. Premium additions in Abu Dhabi and Ras Al Khaimah diversify the luxury market beyond Dubai's main zones. Emphasis on design, sustainability, and unique experiences strengthens pricing power and encourages repeat visits, ensuring the long-term value of top-tier inventory. The luxury pipeline also supports event-driven calendars and curated travel experiences, keeping the segment central to the UAE hospitality market.

Service apartments are expected to grow at a CAGR of 11.76% through 2031, driven by demand from leisure travelers, families, and long-stay professionals seeking spacious accommodations with kitchens and flexible services. Operators use this format to attract cost-conscious, long-stay guests and support corporate relocations, reducing seasonality and improving occupancy rates. Digital platforms enhance the category’s appeal by offering bundled value, such as co-working access and extended-stay packages aligned with corporate travel policies. Mid and upper-mid brands are expanding social spaces and fitness amenities to attract younger travelers planning extended leisure stays. This balance between luxury properties and serviced apartments provides a comprehensive accommodation portfolio that meets diverse traveler needs in the UAE hospitality market.

By Booking Channel: OTA Supremacy Challenged by Direct-Digital Velocity

OTAs play a significant role in the UAE hospitality market, accounting for 51.76% of bookings in 2025. They are key for discovery and price comparison, while loyalty-backed direct channels are gaining traction as operators enhance rate integrity and app-based convenience. Direct channels are projected to grow at a 14.48% CAGR through 2031, driven by loyalty perks and sustainability-focused communications that appeal to corporate and leisure buyers. Dubai’s digital licensing and guest identity frameworks streamline online workflows, increasing confidence in direct transactions and expediting check-in and reporting. Metasearch platforms and brand campaigns complement OTA distribution by expanding reach and encouraging conversions to owned channels through best rate guarantees. A balanced channel mix is expected to stabilize acquisition costs and improve loyalty economics over time.

Wholesale, corporate, and MICE agreements are vital for maintaining mid-week occupancy and group demand. Event-driven destinations utilize master agreements and integrated-resort features to secure larger booking blocks. Hotels with transparent sustainability credentials and flexible terms see higher conversion rates as travel managers prioritize value and sustainability. Loyalty-linked direct offers and OTA visibility remain essential, with operators timing promotions by season and submarket to optimize channel mix. Improved data access enhances the role of analytics, enabling operators to maintain pricing discipline and respond to changes in feeder-market conditions. These strategies support healthier channel economics across the UAE hospitality industry.

Geography Analysis

Dubai held 63.49% of national keys in 2025, supported by investments in destination assets and diverse offerings across price points in the UAE hospitality market. Enhanced digital services and tourism analytics optimize pricing and market mix, enabling faster responses to market signals. Expo City Dubai’s year-round MICE and community programming boosts mid-week demand and premium rate capture for nearby hotels. Clear licensing frameworks ensure confidence in new openings and asset repositioning, maintaining a fresh and diversified appeal for global travelers. Dubai’s data-driven approach emphasizes quality and sustainability improvements.

Abu Dhabi diversifies its hospitality portfolio with cultural institutions, entertainment districts, and integrated resort transformations, catering to both leisure and corporate demand. Hosting global events and expanding premium inventory complements Dubai’s scale and services. The Etihad Rail passenger service enhances intra-UAE travel, connecting cultural and leisure hubs and improving hotel access during peak periods. These developments stabilize occupancy and attract visitors to multi-emirate itineraries.

Ras Al Khaimah leads growth with a projected 10.85% CAGR through 2031, driven by the Wynn Al Marjan Island development and luxury offerings that enhance entertainment and wellness options. Pipeline projects from global brands boost investor confidence and visibility among travelers. Ajman expands its coastal premium offerings with a Four Seasons resort, complementing Dubai’s leisure flows. Sharjah and Fujairah focus on cultural and nature-led identities, encouraging repeat visits and longer stays. These diversified profiles reduce competition and enable targeted approaches to source markets.

Competitive Landscape

Competition in the UAE hospitality market involves global chains, regional groups, and experience-driven concepts focusing on design, programming, and location to cater to diverse traveler segments. Global operators invest in flagship properties and conversions to refresh portfolios and enhance cross-selling opportunities. Regional developers leverage mixed-use ecosystems integrating retail and attractions to boost guest engagement. Entertainment-focused formats in Ras Al Khaimah (RAK) introduce unique revenue streams, expanding tourism offerings, and fostering brand collaborations. Authorities emphasize quality, sustainability, and data-driven performance to ensure a competitive environment centered on guest experience and long-term value.

Strategic initiatives reflect brand expansion, integrated resort developments, and landmark openings, highlighting confidence in market growth. IHG’s partnership with Aldar integrates six hotels on Yas Island, enhancing Abu Dhabi’s resort offerings and MICE capabilities. Marriott’s Luxury Collection conversion in RAK strengthens its high-end presence in a growing emirate. Hilton’s new brand introductions in Dubai diversify lifestyle offerings and expand coverage in business districts.

Large-scale developments like Ciel Dubai Marina demonstrate demand for iconic properties that set benchmarks in engineering and guest experience. Four Seasons’ new properties in Ajman and RAK expand the luxury footprint beyond Dubai. Minor Hotels’ Sharjah resort enhances cultural and wellness-focused offerings, complementing the region’s diverse product mix. Emaar’s integrated asset strategies align hospitality with retail and attractions, reinforcing ecosystem advantages in key UAE locations.

UAE Hospitality Industry Leaders

-

Marriott International

-

Accor

-

Hilton Worldwide

-

IHG Hotels & Resorts

-

Rotana Hotels

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: The world's tallest hotel, Ciel Dubai Marina (377 meters), opened in November 2025 as part of IHG's Vignette Collection. Developed by The First Group, it offers 1,004 rooms, a unique architectural design, and a high infinity pool, completing its final stages as planned.

- April 2025: Four Seasons plans to manage a beachfront resort in Al Zorah, rebranding it as Four Seasons Resort Ajman at Al Zorah. Scheduled to open in 2026, the resort will undergo enhancements to its spa, fitness facilities, and dining options before the relaunch.

- March 2025: Marriott International and Abu Dhabi National Hotels have partnered to bring The Luxury Collection brand to Ras Al Khaimah. The project involves converting a property on Al Marjan Island, with completion expected by late 2026.

UAE Hospitality Market Report Scope

The UAE hospitality market refers to the organized accommodation and tourism services industry across the seven emirates, encompassing hotels, resorts, service apartments, and related facilities that cater to both international and domestic travelers. The market is driven by Dubai’s scale and diversified offerings, Abu Dhabi’s cultural and corporate positioning, and Ras Al Khaimah’s fast-growing luxury pipeline, supported by government initiatives such as Tourism Vision 2031, visa reforms, and infrastructure upgrades. Enhanced digital-first booking behavior, expansion of low-cost carriers, and sustainability mandates further shape demand and investment strategies.

The market is segmented by type, accommodation class, booking channel, and geographic region. By type, it includes chain hotels and independent hotels, reflecting differences in brand distribution, loyalty-driven expansion, and asset-light strategies. By accommodation class, the market is divided into luxury, mid and upper-mid-scale, budget and economy, and service apartments, each catering to distinct traveler segments and pricing tiers. By booking channel, the market covers direct digital platforms, online travel agencies (OTAs), corporate/MICE bookings, and wholesale or traditional agents, highlighting the evolving distribution landscape and cost of acquisition. By geographic region, the market is segmented into Dubai, Abu Dhabi, Sharjah, Ras Al Khaimah, Ajman, Fujairah, and Umm Al Quwain. The report offers market size and forecasts for the upholstered furniture market in value (USD) for all the above segments.

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| Dubai |

| Abu Dhabi |

| Sharjah |

| Ras Al Khaimah |

| Ajman |

| Fujairah |

| Umm Al Quwain |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | Dubai |

| Abu Dhabi | |

| Sharjah | |

| Ras Al Khaimah | |

| Ajman | |

| Fujairah | |

| Umm Al Quwain |

Key Questions Answered in the Report

What is the UAE hospitality market size today, and how fast is it growing?

The UAE hospitality market size is USD 30.07 billion in 2026 and is projected to reach USD 43.92 billion by 2031 at a 7.87% CAGR, supported by national tourism strategy execution and destination investments.

Which segments lead growth within the UAE hospitality market through 2031?

Service apartments are the fastest-growing accommodation class at an 11.76% projected CAGR, while direct digital channels lead distribution growth at a 14.48% projected CAGR through 2031.

Which emirate contributes the most keys to the UAE hospitality market?

Dubai accounts for 63.49% of national keys in 2025, reflecting its global hub status, diversified product stack, and sustained pipeline momentum.

How are policy changes influencing the UAE hospitality market outlook?

Tourism Strategy 2031 targets 40 million hotel guests by 2031, and visa reforms improve travel flexibility, which together expand the addressable base and stabilize demand across seasons.

What new developments could reshape demand in the UAE hospitality market?

The integrated resort under development at Wynn Al Marjan Island in Ras Al Khaimah and multiple luxury openings in Ajman and RAK are set to diversify entertainment and premium offerings.

How are sustainability requirements affecting hotel investment in the UAE?

Green building regulations and certification programs increase upfront capex but improve lifecycle costs and appeal to corporate buyers, supporting long-run asset performance.

Page last updated on: