Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.87 Billion |

| Market Size (2026) | USD 3.13 Billion |

| Market Size (2031) | USD 4.78 Billion |

| Growth Rate (2026 - 2031) | 8.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Maldives Hospitality Market Analysis by Mordor Intelligence

The Maldives Hospitality Market size was valued at USD 2.87 billion in 2025 and is estimated to grow from USD 3.13 billion in 2026 to reach USD 4.78 billion by 2031, at a CAGR of 8.87% during the forecast period (2026-2031).

Growth is fueled by rising demand from affluent international travelers and improved connectivity, enhancing accessibility to the islands. Investments in luxury resorts are supported by government initiatives, including tenders, streamlined approvals, and fiscal incentives, particularly in underdeveloped atolls where tourism demand absorbs new accommodations quickly.

Enhanced airport infrastructure and expanded flight routes have reduced travel times, increasing access to remote islands and attracting repeat visitors. Sustainability is a growing focus, with renewable energy investments like solar-plus-battery systems reducing fuel dependency, controlling costs, and strengthening resorts' environmental credentials. Digital transformation is also reshaping the market, with direct booking engines, personalized guest experiences, and integrated service platforms improving conversion rates, reducing reliance on online travel agencies, and boosting profitability.

Key Report Takeaways

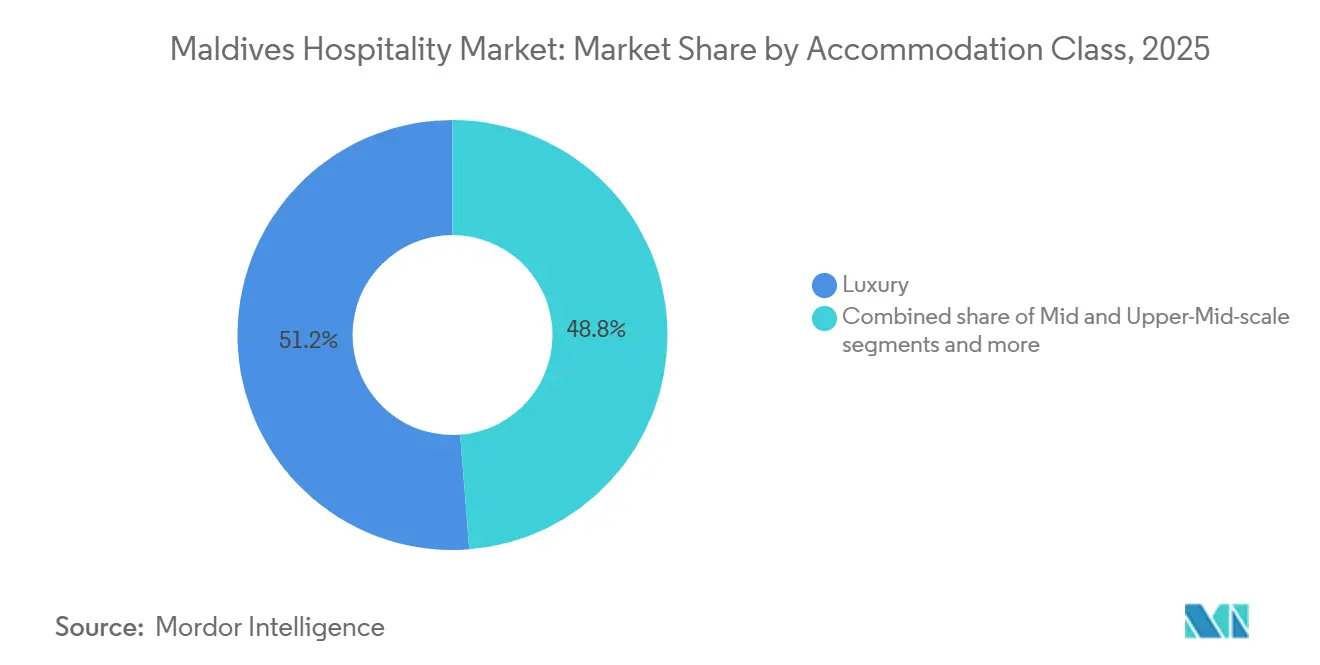

- By accommodation class, luxury properties led with 51.24% of the Maldives hospitality market share in 2025, and luxury is projected to expand at an 11.37% CAGR through 2031.

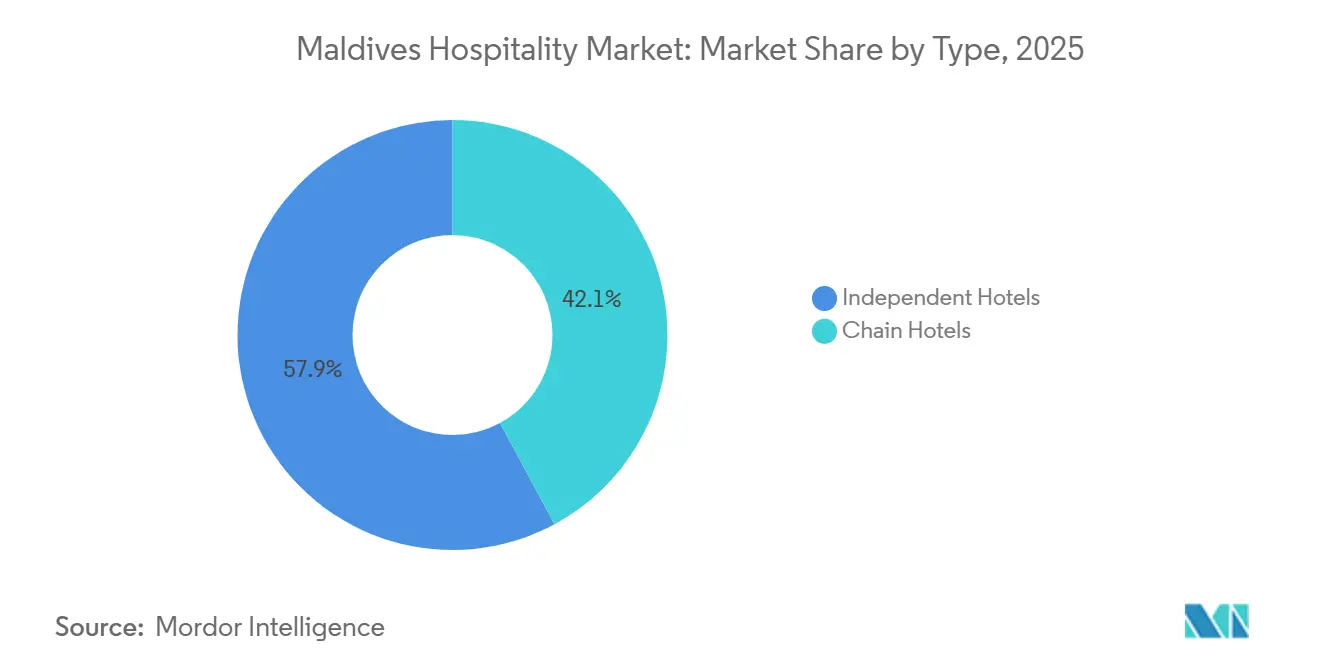

- By type, independent hotels held 57.87% of the Maldives hospitality market share in 2025, while chain hotels are growing at a 9.29% CAGR through 2031.

- By booking channel, OTAs accounted for 61.37% of the Maldives hospitality market share in 2025, and direct-digital is forecast to grow at a 12.73% CAGR through 2031.

- By region, the Greater Malé Region held 37.37% of the Maldives hospitality market share in 2025, and the Southern Atolls are the fastest-growing at a 13.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Maldives Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-driven luxury resort expansion | +2.1% | National, with concentrations in Northern Atolls (Haa Alifu, Haa Dhaalu, Shaviyani) | Medium term (2-4 years) |

| Expansion of direct air connectivity to new source markets | +1.8% | Global, with early gains in the Greater Malé Region, spillover to the Central and Northern Atolls | Short term (≤ 2 years) |

| Uptick in affluent tourists from Asia-Pacific | +1.6% | National, with pronounced uptake in luxury segments across all atolls | Medium term (2-4 years) |

| Seaplane-scheduling technology enhancing occupancy | +0.9% | National, benefiting the remote Northern and Southern Atolls most | Short term (≤ 2 years) |

| Green-finance incentives for solar-powered over-water villas | +0.7% | National, with pilot installations concentrated in Greater Malé and Central Atolls | Long term (≥ 4 years) |

| Experiential wellness offerings at lagoon-based retreats | +1.2% | National, with flagship properties in Baa Atoll (UNESCO Biosphere Reserve) and South Ari Atoll | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-Led Luxury-Resort Expansion Pipeline

The hospitality industry in Maldives is being strongly supported by government-led initiatives that encourage luxury resort development across the archipelago. The Maldives has sustained a record surge in international arrivals, with the government reporting over 2.24 million tourists in 2025, nearly 10% higher than the previous year, and resorts consistently hosting a significant majority of visitors. This performance reflects strong demand for island‑based luxury stays, with resorts accounting for around 70% of total arrivals and expanding bed capacity to over 64,000 operational beds across more than 1,200 tourist facilities[1]Source: Maldives Ministry of Tourism, “Statistics Dashboard,” Government of Maldives, tourism.gov.mv. Continued additions of tourism infrastructure, including thousands of new beds in luxury resort categories, have broadened accommodation options and reinforced the absorption of new supply. High resort demand and government incentives are encouraging investment into underdeveloped atolls, aligning economic policy with tourism infrastructure expansion. The robust tourist performance and growing resort capacity underscore the strategic importance of government support in driving luxury resort development and strengthening the hospitality sector’s growth trajectory.

Growth in direct air links to emerging source markets

The Maldives’ direct air connectivity has expanded significantly, supporting luxury tourism growth and higher resort occupancy. The July 2025 completion of Velana International Airport’s USD 1 billion terminal expansion increased throughput capacity to 7 million passengers per year, unlocking additional wide-body slots and enabling schedule upgrades from Middle Eastern and European carriers during peak seasons. Maldivian Airlines added long-haul flights to major Chinese cities in early 2025, reinforcing the rebound of Chinese arrivals and improving route economics for resorts relying on seaplane transfers to remote atolls. Official tourism statistics show that international travel receipts exceeded USD 5.4 billion in 2025, driven by nearly 10% growth in arrivals and strong performance from key markets such as China and Russia. Additional point-to-point services to Australia and regional airport upgrades are expected to ease distribution bottlenecks, support longer-stay bookings, stabilize day-of-arrival operations for far-flung resorts, and enhance high-value itinerary planning, reducing dependence on a single gateway and maximizing occupancy yields across peak and shoulder seasons[2]Visit Maldives, “Maldives Records Historic Tourism Performance in 2025,” MMPRC, corporate.visitmaldives.com.

Uptick in affluent tourists from APAC

High-spending tourists from the Asia-Pacific region are driving growth in the Maldives hospitality sector. China contributed over 329,000 arrivals in 2025, nearly 15% of total visitors, while India added more than 130,000 arrivals. Resorts are adapting to Asia-Pacific preferences by enhancing Mandarin and Hindi guest services, offering Ayurvedic and East Asian wellness options, and adding live kitchen features like wok stations and tandoor ovens. Higher ADRs and longer stays by Asia-Pacific luxury travelers are boosting RevPAR and revenue. Operators are tailoring villa configurations, private dining, and excursions for couples, families, and corporate groups. Marketing efforts, including a 2025 partnership with the Mumbai Indians, have strengthened Indian bookings for 2026. Rising corporate and MICE demand from Singapore, Hong Kong, and Tokyo is supported by flexible meeting spaces and on-island activities. These trends are increasing occupancy and driving service enhancements year-round.

Seaplane-scheduling technology enhancing occupancy

The Maldives’ premium resorts benefit from optimized seaplane operations, with Trans Maldivian Airways leveraging real-time scheduling data to improve load factors and on-time performance during peak travel periods. Operational enhancements, alongside the dedicated Noovilu Seaplane Terminal, enable resorts to accurately forecast guest arrivals and efficiently coordinate housekeeping and welcome services. Predictable transfers reduce no-show risks, lower reliance on costly backup charters, and safeguard guest satisfaction, especially in weather-sensitive seasons affecting remote atolls. Certified maintenance for DHC Twin Otter aircraft shortens parts lead times and minimizes downtime, ensuring reliable inter-island connectivity during high-demand periods. These advancements allow resorts to capture late-booking demand, maximize occupancy yields, and maintain premium ADRs while sustaining high service standards for luxury travelers.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-related disruptions and sea-level risk | -1.9% | National, with acute exposure in low-lying atolls (Addu, Fuvahmulah, Gaafu Dhaalu) | Long term (≥ 4 years) |

| High operating costs due to import dependence | -1.4% | National, with the highest transport premiums in remote Northern and Southern Atolls | Medium term (2-4 years) |

| Tightening of skilled-labor quotas | -1.1% | National, with early workforce gaps in the Greater Malé Region and the Central Atolls | Short term (≤ 2 years) |

| Currency-exchange volatility impacting long-term resort leases | -0.8% | National, with liquidity strain concentrated in Category A resorts (ADR > USD 800) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Climate-Related Disruption & Sea-Level Vulnerability

The Maldives is highly exposed to sea-level rise, as most land lies below one meter, making resorts vulnerable to flooding and coastal damage. Projections indicate that even moderate sea-level increases could threaten a significant portion of assets by mid-century without adaptation measures. Resort operators face increased capital expenditures for seawalls, land reclamation, and ecosystem restoration to protect infrastructure. Coral reef degradation from rising temperatures poses a direct risk to dive and snorkeling activities, impacting revenue and limiting product offerings in marine-focused atolls. Environmental approvals and impact assessments now involve longer timelines and higher costs, presenting barriers for smaller developers compared to established chains. To mitigate risks, operators are introducing preemptive conservation and adaptation programs, though these initiatives add complexity and costs to new developments and renovations.

High operating costs due to import dependence

Reliance on imports for goods and fuel raises operating costs for Maldives resort operators compared to regional competitors. Import duties on most items form a significant share of tax revenue, while tourism-related taxes, such as the Tourism Goods and Services Tax and Green Tax, contribute heavily to government income. These levies are passed on to guests and operators. Fuel imports, a major expense, drive resorts to adopt renewable energy systems to reduce reliance on volatile global markets and manage costs. Electricity subsidies partially offset high tariffs, but remote atoll properties face added transport costs for perishables and maintenance, further squeezing margins. Recent increases in tourism taxes, including the Green Tax, add to operators' cost burdens[3]Maldives Ministry of Finance and Planning, “Revenue Policy,” Government of Maldives, finance.gov.mv/public-finance/revenue-policy. To address these challenges, resorts are investing in solar energy, on-island production, and bulk procurement, which require upfront capital but offer long-term savings and resilience against import cost fluctuations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Chain-Hotel Surge Reshapes Atoll Footprint

Independent hotels held 57.87% of bed inventory in 2025. Chain brands are expected to grow at a 9.29% CAGR from 2026 to 2031, supported by loyalty ecosystems, centralized revenue management, and procurement efficiencies. Chain-led expansions target northern and southern atolls, where limited supply and larger plots favor flagship resorts. New global brand openings in 2025 and 2026 diversify pricing and focus on wellness, design, and family amenities, reducing seasonality and boosting repeat visits. Chains adopt asset-light models for franchise and management-fee revenue, while independents rely on niche positioning and local partnerships to differentiate. This dual strategy enhances service levels and marketing reach while preserving the unique character of island retreats.

New luxury and lifestyle brands expand chain presence and attract investments in airlift and marina infrastructure. Independents maintain strong eco-luxury and wellness niches, adopting solar, water, and waste innovations to improve margins. Chains address skilled labor gaps with standardized training, while independents enrich offerings through local partnerships.

Chain-led growth is balanced by independent conversions into soft brands, retaining identity while leveraging global demand. Portfolio strategies combining flagship chain properties with sister resorts across islands enable cross-selling and operational support, supporting occupancy during shoulder seasons.

By Accommodation Class: Luxury Dominance Widens as Ultra-High-Net-Worth Demand Lifts ADRs

Luxury properties dominate the hospitality industry in Maldives, contributing 51.24% of 2025 revenue and are anticipated to grow at an 11.37% CAGR through 2031. This segment outpaces mid-scale and economy categories, which are more affected by cost inflation and adaptation expenses. Higher average daily rates (ADRs) and longer stays by affluent travelers from Asia-Pacific and the Middle East drive premium segment performance. Development plans include ultra-luxury concepts with larger villas, private marinas, and signature dining. Immersive experiences, such as marine conservation and wellness programs, sustain high gross operating profit (GOP) levels despite lower occupancy compared to other regional destinations. Mid-scale operators are introducing all-inclusive packages and family-friendly amenities to remain competitive, while economy and guesthouse segments focus on direct booking strategies and partnerships to reduce costs and improve cash flow during off-peak periods.

Ultra-luxury properties are expanding in southern and northern atolls, leveraging lagoon plots for multi-island masterplans that balance regional development. Branded-residence components and strata-enabled ownership structures attract investors and create repeat-guest pipelines. Wellness resorts achieve higher ADRs through comprehensive programs and skilled practitioners, with international recognition enhancing credibility. Growth in the luxury segment is supported by exclusive island offerings, diversified source markets, and new air routes simplifying long-haul travel. The market is shifting toward premium and ultra-luxury offerings, while service-apartment developments near Greater Malé address long-stay and corporate demand.

By Booking Channel: Direct-Digital Acceleration as Resorts Deploy AI-Personalization Tools

OTAs held 61.37% of bookings in 2025, supported by strong SEO, instant confirmations, and global brand recognition, enabling large-scale discovery and conversion. Direct-digital bookings are expected to grow at a 12.73% CAGR through 2031, as resorts leverage machine-learning tools to personalize recommendations for villas, spas, and excursions, improving conversion rates. Direct booking engines with CRM integration, on-site chat, dynamic pricing, and loyalty programs are boosting repeat bookings and reducing commission costs in a high-value market. Corporate and MICE channels accounted for a 9.0% share in 2025, with resorts offering modular event spaces and curated group activities seeing growth. Wholesale and traditional agents are losing share as mobile-first travelers favor direct engines and social commerce for faster content discovery and response times.

Direct-digital channels benefit from digital storytelling and community marketing focused on conservation, wellness, and culinary programs, differentiating the Maldives market. Resorts enhance pre-arrival experiences with upsell modules for transfers, dining, and activities, increasing per-stay spending and guest satisfaction. Data-driven audience segmentation ensures marketing budgets target priority markets, while OTA partnerships remain vital for new geographies and short-notice travel. Market share dynamics will depend on CRM adoption and diverse payment options, including installment plans for higher ADRs. Properties integrating booking, itinerary planning, and on-island experiences into a single app are positioned to capture higher-margin direct bookings.

Geography Analysis

The Greater Malé Region held 37.37% of beds in the Maldives hospitality market in 2025, benefiting from its proximity to Velana International Airport and robust infrastructure that minimizes supply chain risks. The airport's capacity expansion has improved flight clearance and facilitated same-day transfers to nearby speedboat-accessible islands. This region features a mix of upscale and luxury resorts with strong brand recognition, supported by shorter transfer times that suit short-stay city-plus-island itineraries. Its connectivity and retail ecosystem help balance demand during shoulder seasons when weather impacts seaplane schedules. While its market share is expected to remain stable, other regions are poised for growth due to greenfield developments.

The Central Atolls attract visitors with marine biodiversity, including whale shark habitats that drive year-round demand for diving and snorkeling. New wellness, culinary, and conservation-focused concepts are emerging, with brand entries and renovations refreshing inventory without overbuilding. This sustainable approach enhances the region's appeal to diverse traveler segments.

The Northern Atolls benefit from regional airport upgrades that improve accessibility for long-haul visitors. Developments in Baa and Noonu leverage UNESCO recognition and reef access, offering premium experiences. Market share in this region is expected to grow as lagoon plot tenders are finalized and air access improves.

The Southern Atolls are forecast to grow at a 13.48% CAGR through 2031, driven by greenfield projects featuring lagoon plots, superyacht-ready marinas, and low-density villas targeting ultra-high-net-worth guests. These developments focus on privacy, wellness, and marine adventures, diversifying the Maldives' appeal. Challenges like logistics complexity are mitigated through solar energy, on-island water systems, and local sourcing. This expansion moderates seasonality and broadens the product portfolio for longer stays tied to jet, yacht, and charter travel.

Competitive Landscape

The Maldives hospitality market is moderately concentrated, with leading operators holding a significant share while independent resorts and regional groups serve the rest. Competition is shifting from occupancy-focused strategies to yield management, guest loyalty, and sustainability differentiation, which support premium pricing and higher booking conversions. Independent properties increasingly adopt soft-brand conversions, maintaining their identity while leveraging global distribution networks and loyalty programs to boost direct bookings and reduce commission costs. Technology adoption, including dynamic pricing, predictive maintenance, biometric check-ins, and integrated seaplane scheduling, enhances guest experiences and operational efficiency. This combination of chain standardization and independent innovation ensures destination diversity and pricing stability across seasons.

Green-certified operators gain visibility in eco-conscious searches and command higher rates. Energy and water efficiency initiatives are linked to cost control in a resource-import-dependent environment. Multi-property groups reduce per-key operating costs through centralized procurement, training, and yield management, while single-asset operators focus on curated experiences to retain repeat guests. Loyalty programs are increasingly important for high-frequency visitors exploring regional island circuits. Brand portfolios emphasize wellness, culinary experiences, and family-focused offerings to compete with nearby islands with better flight connectivity. Risk management strategies addressing foreign exchange policies, labor localization, and energy regulations favor financially strong operators with access to financing.

Resorts are integrating renewable energy projects, such as solar installations, to lower costs and enhance guest experiences. Soft-brand conversions are expanding lifestyle and luxury offerings in key atolls, strengthening chain presence. Luxury and lifestyle portfolios target high-value guests, focusing on speedboat-accessible and remote locations. ESG investments, loyalty-driven cross-selling, and curated experiences remain critical as competition grows for premium travelers seeking longer stays and higher spending. The market reflects a dynamic interplay of sustainability, technology, and brand strategy, shaping the Maldives hospitality sector's evolution.

Maldives Hospitality Industry Leaders

Universal Resorts

Crown & Champa Resorts

Marriott International

Hilton Worldwide

Accor S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: NH Collection Maldives Reethi Resort, located in Baa Atoll, has reopened after renovations. The resort offers 105 villas, seven dining venues, and the REVIVE spa. It is the brand’s first property in a UNESCO Biosphere Reserve in the Maldives, combining luxury with environmental significance.

- March 2025: Ennismore plans a Mondrian-branded resort on Kuredhivaru Island, Noonu Atoll. Opening in 2026, it will feature distinctive villas, wellness and dining venues, and experiential amenities, highlighting the brand's growth and luxury focus in the Maldives hospitality market.

- March 2025: Visit Maldives and MMPRC partnered with the Mumbai Indians to boost Indian tourist traffic and promote destination awareness through IPL 2025, aiming for stronger engagement and visibility by 2026.

Maldives Hospitality Market Report Scope

The Maldives hospitality market refers to the organized accommodation and tourism services industry across the island nation, encompassing luxury resorts, hotels, service apartments, and related facilities that cater to international and domestic travelers. The Maldives’ positioning drives the market as a premier global destination for luxury tourism, supported by strong air connectivity, exclusive resort offerings, and rising demand for personalized guest experiences.

The market is segmented by type, accommodation class, booking channel, and geographic region. By type, it includes chain hotels and independent hotels, reflecting differences in brand distribution, loyalty programs, and asset-light expansion strategies. By accommodation class, the market is divided into luxury, mid and upper-mid-scale, budget, and economy, and service apartments, each catering to distinct traveler segments and pricing tiers. By booking channel, the market covers direct digital platforms, online travel agencies (OTAs), corporate/MICE bookings, and wholesale or traditional agents, highlighting the evolving distribution landscape. By geographic region, the market is segmented into the Greater Malé Region, Central Atolls, Northern Atolls, and Southern Atolls, each with unique demand drivers such as proximity to airports, dive sites, lagoons, and large-scale luxury projects.

The report offers market size and forecasts for the upholstered furniture market in value (USD) for all the above segments.

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| Greater Malé Region |

| Central Atolls |

| Northern Atolls |

| Southern Atolls |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | Greater Malé Region |

| Central Atolls | |

| Northern Atolls | |

| Southern Atolls |

Key Questions Answered in the Report

What is the current size and growth outlook of the Maldives hospitality market?

The Maldives hospitality market reached USD 3.13 billion in 2026 and is projected to reach USD 4.78 billion by 2031 at an 8.87% CAGR, supported by luxury resort development and improved air access.

Which segments are leading and growing the fastest in the Maldives hospitality market?

Luxury led with 51.24% revenue share in 2025 and is the fastest-growing at an 11.37% CAGR through 2031, as ultra-luxury demand and wellness-led positioning advance.

How is booking behavior changing for the Maldives hospitality market?

OTAs captured 61.37% of bookings in 2025, while direct-digital is growing at a 12.73% CAGR as resorts deploy personalized booking platforms to improve conversion and margins.

Which regions show the strongest growth within the Maldives hospitality market?

The Southern Atolls are forecast to grow at a 13.48% CAGR to 2031, while the Greater Malé Region remains the largest inventory base at 37.37% in 2025, supported by airport proximity.

What risks could impact the Maldives' hospitality market over the next few years?

Key risks include climate-related disruptions, import-driven operating costs, skilled-labor localization pressures, and FX conversion mandates that can reduce USD liquidity for operators.

Are chain hotels or independents growing faster?

Chain hotels are expanding at 9.29% CAGR, leveraging brand strength, yet independents still control the majority of keys.

Page last updated on: