Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

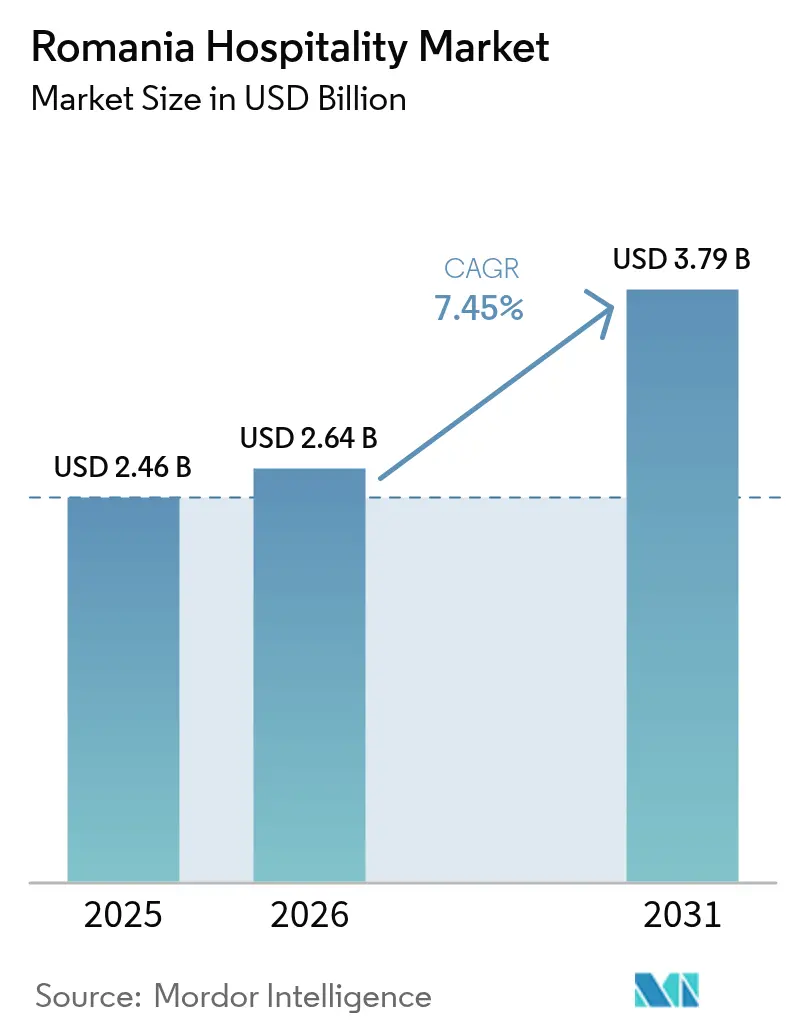

| Base Year Market Size (2025) | USD 2.46 Billion |

| Market Size (2026) | USD 2.64 Billion |

| Market Size (2031) | USD 3.79 Billion |

| Growth Rate (2026 - 2031) | 7.45% CAGR |

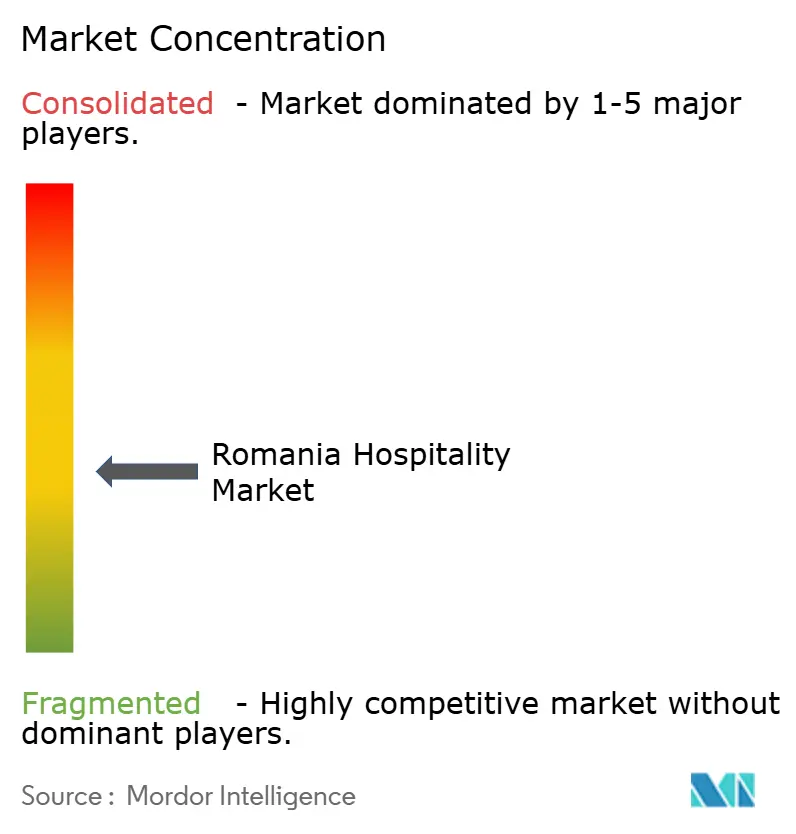

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Romania Hospitality Market Analysis by Mordor Intelligence

The Romania hospitality market size is expected to grow from USD 2.46 billion in 2025 to USD 2.64 billion in 2026 and is forecast to reach USD 3.79 billion by 2031 at 7.45% CAGR over 2026-2031. Schengen-driven connectivity gains power the expansion, sustained domestic leisure demand, rural tourism funding, and rapid digital adoption. International chains are deploying aggressive pipelines, while independent operators keep leveraging local touchpoints to preserve market breadth. Consumer interest in premium ski and wellness experiences, coupled with EU-financed infrastructure, widens seasonality windows and lifts average daily rates. Persistent labor shortages and legacy licensing hurdles temper growth but also accelerate automation and foreign-talent recruitment strategies, reshaping operating models across the Romania hospitality market.

Key Report Takeaways

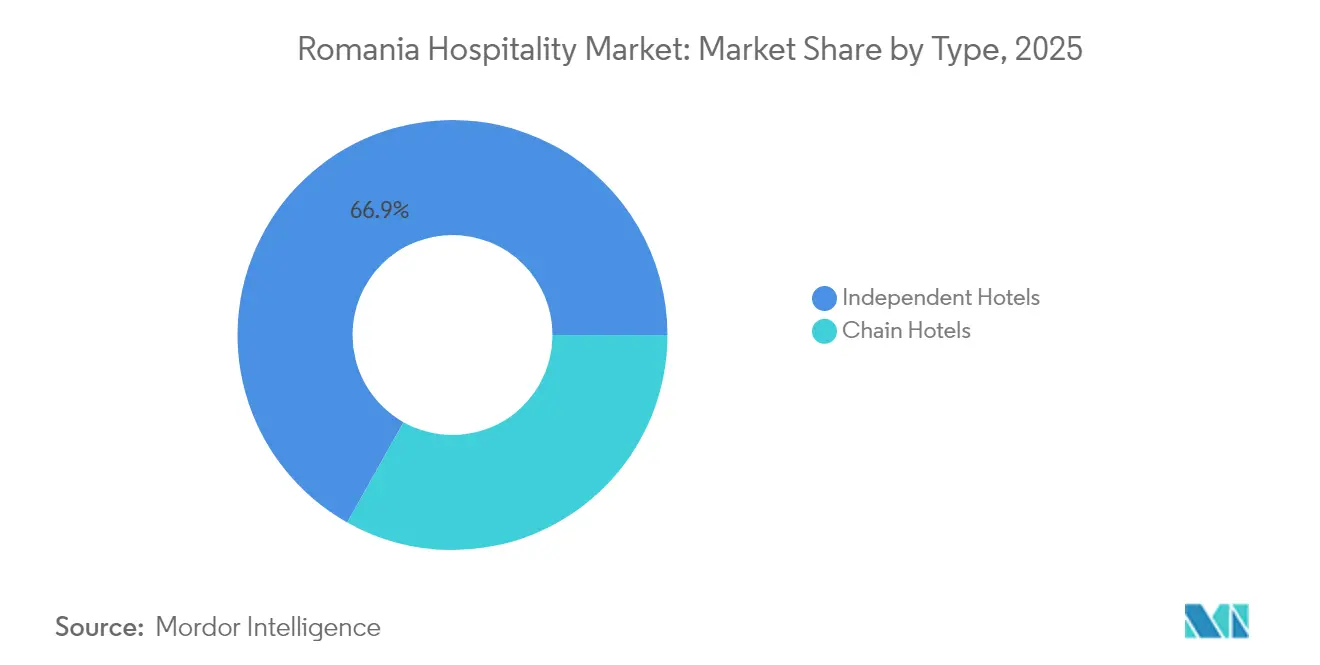

- By type, Independent Hotels led with 66.85% Romania hospitality market share in 2025, whereas Chain Hotels are projected to expand at an 10.78% CAGR through 2031.

- By hotel category, Mid-Scale Hotels commanded 41.92% share of the Romania hospitality market size in 2025, while the Upscale & Luxury segment is set to grow at a 10.28% CAGR to 2031.

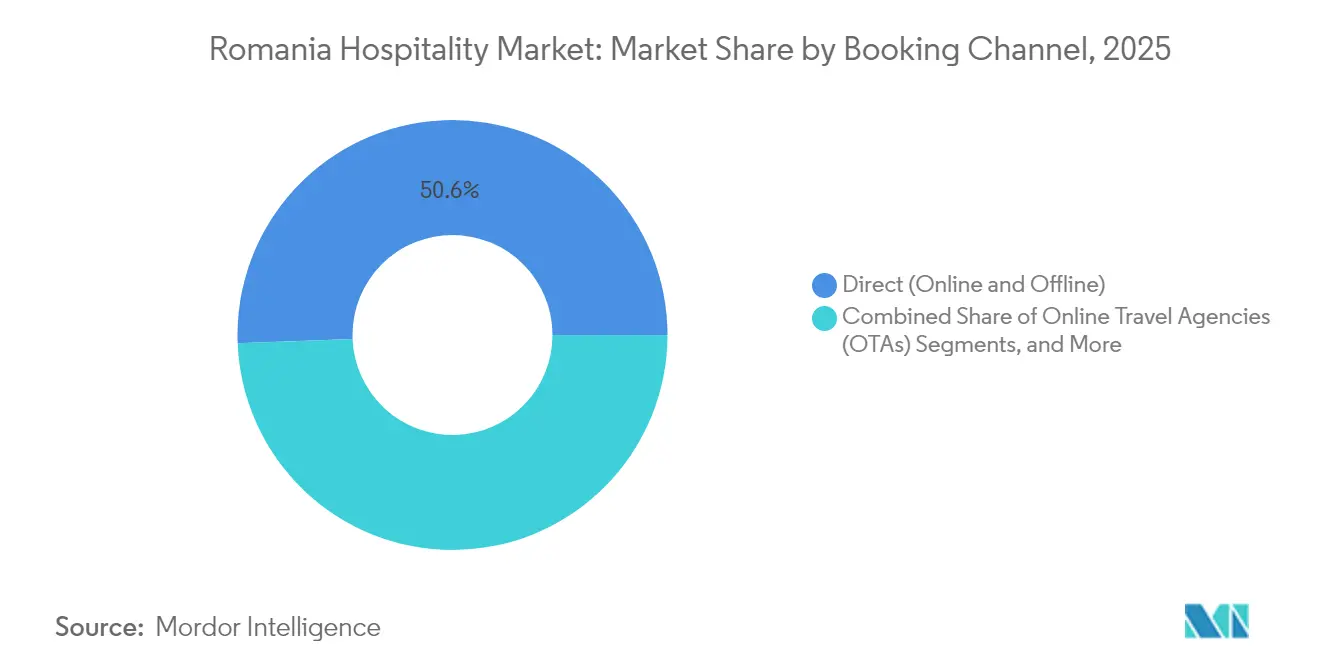

- By booking channel, Direct bookings held 50.62% of the Romania hospitality market in 2025; Online Travel Agencies record the fastest momentum at 11.62% CAGR through 2031.

- By guest origin, Domestic travelers accounted for 81.74% share of the Romania hospitality market in 2025; International arrivals are accelerating at an 11.28% CAGR.

- By region, Bucharest-Ilfov captured 36.95% Romania hospitality market share in 2025, while the North-East region is advancing at a 10.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Romania Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing tourist arrivals rebound | +1.8% | National, with concentration in Bucharest, Constanța, Brașov | Short term (≤ 2 years) |

| Surge in domestic leisure travel post-COVID | +1.5% | National, particularly rural and secondary cities | Medium term (2-4 years) |

| Rapid OTA and digital-payments penetration | +1.2% | Urban centers, expanding to rural areas | Medium term (2-4 years) |

| EU-funded rural and agro-tourism programs | +0.9% | Rural regions, North-East, Centre, Maramureș | Long term (≥ 4 years) |

| Partial Schengen accession boosting connectivity | +1.4% | National, with immediate impact on border regions | Short term (≤ 2 years) |

| Premium ski-resort pipeline in Carpathians | +0.8% | Carpathian regions, Brașov, Maramureș | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Tourist Arrivals Rebound

Visitor volumes surpassed pre-COVID benchmarks, with 14.26 million arrivals in 2024, 4.5% higher year on year, as Germany, Italy, and Israel surfaced as top source markets while domestic travellers represented 83.3% of total traffic. Overnight stays reached 30.2 million, signalling longer dwell times that underpin revenue consistency across the Romania hospitality market. The rebound allows properties to diversify their international mix and hedge against demand shocks emanating from rival destinations facing geopolitical or capacity constraints.

Surge in Domestic Leisure Travel Post-COVID

Romanian residents generated 83.7% of overnight stays in 2024, fuelling regionally dispersed room demand and prompting a 200% increase in rural accommodation supply in Bucovina alone. National campaigns celebrating local gastronomy and heritage deepen loyalty and support, yield-management flexibility, anchoring baseline occupancy throughout the Romania hospitality market.

Rapid OTA and Digital-Payments Penetration

Government allocation of USD 4.1 billion under the National Recovery and Resilience Plan catalysed fibre rollout and cashless infrastructure, enabling OTAs to grow bookings 12.03% CAGR while direct digital channels employ AI concierges to lift conversion rates [1]Source: Staff Report, “Digitalisation funds under NRRP,” U.S. Department of Commerce, commerce.gov. . Indigenous platforms such as Szallas capture regional wallet preferences, highlighting the competitive imperative of payment localisation in the Romania hospitality market.

EU-Funded Rural and Agro-Tourism Programs

Common Agricultural Policy grants converted thousands of farms into guesthouses, diversifying rural income and preserving vernacular architecture; current allocations include EUR 50 million for Borșa ski infrastructure. Such projects lengthen seasonal appeal and channel traffic from overcrowded urban nodes into high-spend countryside niches of the Romania hospitality market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skill shortages and wage inflation | -1.6% | National, acute in urban tourist areas | Short term (≤ 2 years) |

| Complex licensing / zoning regulations | -0.8% | Urban centers, particularly Bucharest | Medium term (2-4 years) |

| Ageing transport infrastructure outside major hubs | -0.7% | Rural and secondary regions, excluding Bucharest-Ilfov | Long term (≥ 4 years) |

| Exposure to volatile energy costs | -0.6% | National, with higher impact on energy-intensive facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skill Shortages and Wage Inflation

Labor gaps of 20-25% nationally, peaking at 50% in prime destinations, force operators to hire South Asian workers at monthly wages of 4,500-5,000 lei (USD 950-1,050), squeezing GOP margins across the Romania hospitality market. Rising personnel expenses accelerate interest in automation and multilingual self-service solutions, but onboarding and cultural-fit costs remain pronounced.

Complex Licensing and Zoning Regulations

Although Emergency Ordinance 31/2025 sets 30-day limits for urban planning permits, overlapping sanitary, energy, and heritage requirements still create unpredictable timelines and capex overruns that deter greenfield projects in the Romania hospitality market [2]Source: Government of Romania, “Emergency Ordinance No. 31/2025 on Urban Planning and Building Permits,” legislatie.just.ro. . Frequent rule changes without stakeholder input heighten perceived regulatory risk among foreign investors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Independent Hotels Hold Scale While Chains Add Pace

Independent Hotels commanded 66.85% of the Romania hospitality market share in 2025, reflecting the sector’s fragmented roots and guests’ appetite for local character. These operators keep costs lean and tailor experiences to regional tastes, which helps them protect margins even as wages rise. Chain Hotels, though smaller in footprint today, are adding keys at an 10.78% CAGR to 2031 on the back of loyalty-program pull and easier access to investment capital. Their expansion is most visible in Bucharest, Brașov, and along the Black Sea coast, where global brands want to lock in prime plots ahead of demand spikes from Schengen-driven tourism.

The two groups increasingly overlap in guest expectations. Independents are upgrading tech, adopting cloud PMS tools, and pursuing soft-brand affiliations to stay visible on global distribution systems. Chains, meanwhile, are integrating Romanian design cues and farm-to-table menus to sidestep a “cookie-cutter” perception. M&A chatter is growing; high-performing family hotels are becoming targets for groups that need local know-how. Long term, the market is likely to see gradual consolidation, yet a diverse ownership mix should persist and keep price points varied within the Romania hospitality market.

By Hotel Category: Mid-Scale Dominance Faces Luxury Catch-Up

Mid-Scale Hotels represented 41.92% of the Romania hospitality market in 2025, anchored by domestic corporate trips and mid-income leisure stays that favour dependable service over amenities they may not use. Steady conference demand in Bucharest and second-tier cities also underpins weekday occupancy for this band. Upscale and Luxury properties record the fastest lift at 10.28% CAGR, accelerated by projects like the EUR 70 million Kempinski Poiana Brașov and the upgraded InterContinental Athénée Palace Bucharest. Rising disposable income and a stronger outbound elite that now prefers to spend locally drive this pivot to premium.

Luxury developers emphasise larger wellness zones, rooftop dining, and branded residences that create year-round revenue. Operators also bundle cultural tours and vineyard visits to lengthen stays beyond weekend ski runs or city breaks. The shift pressures mid-scale owners to refresh rooms, add co-working lounges, and refine F&B concepts to hold share. Budget and Economy hotels stay resilient by courting price-sensitive groups and sports teams, yet they feel cost heat from higher utilities and staffing. All categories benefit when Schengen entry widens the demand funnel, but each must fine-tune value propositions to capture its slice of the Romania hospitality market.

By Booking Channel: Direct Sales Lead While OTA Momentum Builds

Direct channels—hotel websites, walk-ins, and call centres—retained 50.62% of bookings in 2025, as operators doubled down on member-only rates and digital concierge chat that ease pre-arrival questions. Romanian guests often favour direct contact to secure personalised extras such as late checkout or event tickets Hotels now walk a tightrope: they need OTA visibility for reach yet aim to cap commission costs. Successful properties use rate-parity software, capture email addresses at check-in, and nudge repeat guests toward proprietary apps. Local OTAs such as Szallas Group gain an edge by offering instalment payments and meal vouchers that align with Romanian payroll schemes. Global distribution systems hold steady in corporate travel, though clients increasingly request green-certified properties and dynamic packaging. As digital literacy rises across age groups, channel diversification becomes central to sustaining RevPAR in the Romania hospitality market.

By Guest Origin: Domestic Base Anchors Stability as Foreign Share Rises

Domestic travelers produced 81.74% of total stays in 2025, giving operators a dependable weekday base and softening exposure to currency shifts. Government road upgrades and “Discover Romania” media campaigns nudged city dwellers toward rural guesthouses and spa towns, spreading revenue beyond the capital. International arrivals expand at an 11.28% CAGR thanks to Schengen integration, airline route launches, and glowing coverage in TIME and CNN. Germany, Italy, and Israel supply the largest visitor pools, with North American traffic gaining traction through heritage tourism.

Hotels segment pricing calendars to reflect this mix: value bundles and flexible check-in appeal to locals, while curated wine tastings and castle tours fetch premium rates from foreign guests. Loyalty schemes roll out bilingual apps and QR-based tipping to bridge service expectations. Rural operators add card terminals and multilingual signage to court cross-border self-drive tourists. The combined surge supports year-round occupancy but raises service-quality demands, pressing brands to refine staff training and cultural-awareness modules across the Romania hospitality market.

Geography Analysis

Bucharest-Ilfov remains the country’s demand anchor, marrying corporate, MICE, and cultural itineraries. Swissôtel Bucharest and Hyatt Regency Aro Palace next lift the skyline, while labour scarcity pushes hoteliers toward migrant-worker partnerships and service automation. The North-East region surges on EU rural funds, doubling guesthouse stock and unveiling Borșa’s 25 km ski grid. Authentic heritage draws higher-spend visitors seeking vernacular immersion, yet last-mile transport still limits full potential of the Romania hospitality market. Black Sea coast assets in the South-East tap NATO air-base expansion for year-round bed-night spikes, while Carpathian enclaves in the Centre region upscale with Kempinski and Swissôtel Poiana Brașov. Western border cities benefit from cross-border tourism but need cohesive branding to increase dwell time within the Romania hospitality market.

Competitive Landscape

Romania hospitality market displays moderate concentration that balances the brand strength of global chains with the numerical dominance of local independents. Ana Hotels, Continental Hotels, Accor, Hilton Worldwide, and Radisson Hotel Group hold leading positions, yet no single operator controls an overwhelming share, preserving space for vigorous price and service competition. Independent properties remain the majority, giving guests varied style and price options while pressuring chains to differentiate through loyalty programmes and consistent standards. Full Schengen accession has lowered access barriers, prompting both incumbents and newcomers to speed up renovation cycles and upgrade brand portfolios.

Radisson Hotel Group has committed to three high-profile openings—Radisson RED Bucharest Old Town, Radisson Blu Grand Mountain Resort Brașov, and Radisson Blu Resort & Residences Mamaia—to seize growing urban and leisure demand. Accor is advancing via management agreements with Construcții Erbașu on Swissôtel Bucharest, Novotel Living Bucharest Baneasa, and ibis Styles Oradea, sharing development risk while scaling brand presence. Ana Hotels is investing EUR 25 million to refurbish the InterContinental Athénée Palace Bucharest, reinforcing premium positioning in the capital. Technology is another differentiator: Le Boutique Hotel Moxa deployed an AI guest-communication platform that lifted direct bookings and guest-satisfaction metrics. Cross-border capital is entering as well, illustrated by Rainbow Tours’ strategic investment in tour operator Paralela 45, which expands distribution reach for domestic hotels [3]Source: Banca Transilvania – BT Capital Partners, “Rainbow Tours Invests in Paralela 45 to Strengthen Romanian Footprint,” bancatransilvania.ro.

Romania Hospitality Industry Leaders

Ana Hotels

Continental Hotels

Accor / Orbis

Hilton Worldwide

Radisson Hotel Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Radisson Hotel Group unveiled a multi-property pipeline, including Radisson RED Bucharest Old Town and Radisson Blu Grand Mountain Resort Brasov.

- May 2025: BT Capital Partners advised Paralela 45 on investment from Poland’s Rainbow Tours, boosting outbound package capability.

- April 2025: Government Emergency Ordinance 31/2025 shortened permitting deadlines, embedding tacit approval clauses.

- April 2025: Borșa obtained EUR 50 million in EU funds for 25 km ski slopes and wellness assets.

Romania Hospitality Market Report Scope

Hospitality means welcoming a guest and making them comfortable at your place by looking after their needs during their temporary stay. The hospitality industry in Romania refers to the total transactions recorded by various accommodation establishments in Romania. The study captures the market value of the hospitality industry in Romania. The Romania Hospitality Industry is segmented By Type (Chain Hotels and Independent Hotels) and By Category (Upscale and Luxury Hotels, Mid-Scale Hotels, and Budget and Economy Hotels). The report offers market size and forecasts for the Romania Hospitality Industry in value (USD) for all the above segments.

By Type

| Chain Hotels |

| Independent Hotels |

By Hotel Category

| Upscale and Luxury Hotels |

| Mid-Scale Hotels |

| Budget and Economy Hotels |

By Booking Channel

| Direct (Online and Offline) |

| Online Travel Agencies (OTAs) |

| GDS and Wholesalers |

By Guest Origin

| Domestic Travelers |

| International Travelers |

By Region

| North East |

| South East |

| South Muntenia |

| South West Oltenia |

| West |

| North West |

| Centre |

| Bucharest Ilfov |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Hotel Category | Upscale and Luxury Hotels |

| Mid-Scale Hotels | |

| Budget and Economy Hotels | |

| By Booking Channel | Direct (Online and Offline) |

| Online Travel Agencies (OTAs) | |

| GDS and Wholesalers | |

| By Guest Origin | Domestic Travelers |

| International Travelers | |

| By Region | North East |

| South East | |

| South Muntenia | |

| South West Oltenia | |

| West | |

| North West | |

| Centre | |

| Bucharest Ilfov |

Key Questions Answered in the Report

How large is the Romania hospitality market in 2026?

The Romania hospitality market is valued at USD 2.64 billion in 2026 and is projected to grow to USD 3.79 billion by 2031 at a 7.45% CAGR.

Which hotel segment is expanding fastest?

Upscale and Luxury hotels show the highest growth, advancing at a 10.28% CAGR on the back of premium ski resorts and wellness investments.

What impact does Schengen accession have on tourism?

Full Schengen membership from January 2025 lifted Q1 2025 international arrivals by 11.7%, improving accessibility and boosting investor interest.

How severe is the labour shortage in Romanian hospitality?

The sector faces a 20-25% worker deficit nationally, rising to 50% during peak seasons in tourist hotspots, driving wage inflation and recruitment of foreign staff.

Which Romanian region offers the highest growth potential?

The North-East region leads with a 10.34% CAGR through 2031, supported by EU-financed rural tourism projects and ski infrastructure upgrades.

Are Online Travel Agencies gaining share?

Yes, OTA bookings are forecast to grow at a 11.62% CAGR as improved digital infrastructure and mobile payment adoption make third-party platforms more convenient for domestic and international consumers.

Page last updated on: