Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 120.46 Billion |

| Market Size (2026) | USD 125.34 Billion |

| Market Size (2031) | USD 152.84 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

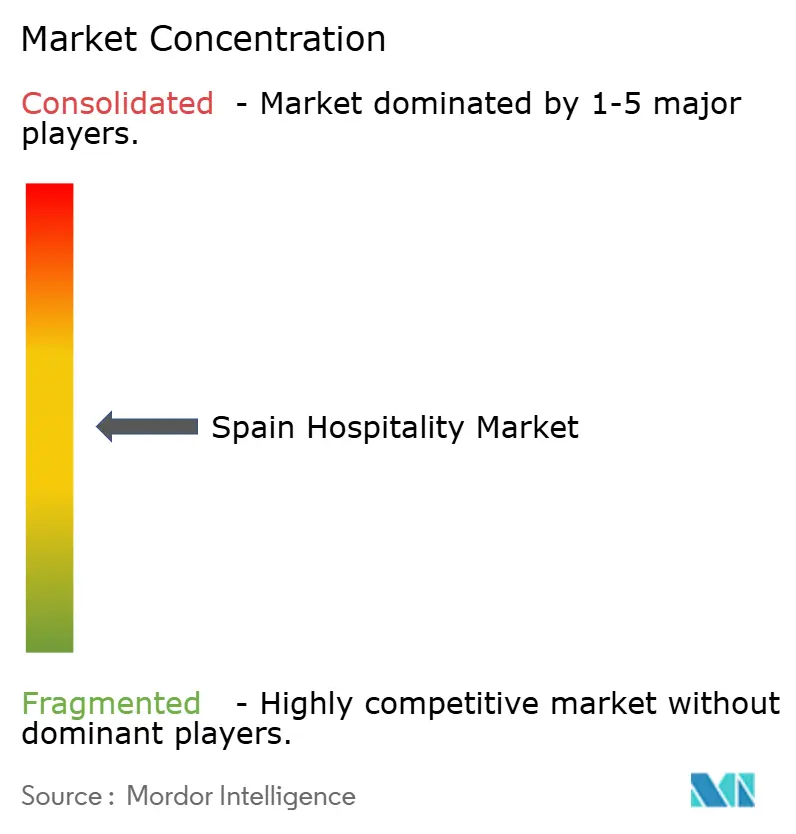

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Hospitality Market Analysis by Mordor Intelligence

Spain Hospitality market size in 2026 is estimated at USD 125.34 billion, growing from 2025 value of USD 120.46 billion with 2031 projections showing USD 152.84 billion, growing at 4.05% CAGR over 2026-2031.

This growth momentum underscores the sector’s post-pandemic resilience and its status as the world’s second-largest tourism destination. Spain hospitality market growth is reinforced by a 16.1% jump in 2024 tourist spending, steady gains in disposable income in the United Kingdom, Germany, and France, and sustained geopolitical stability that redirects leisure flows from competing Mediterranean destinations. A government pivot from volume to value under Tourism Strategy 2030 channels Recovery and Resilience funds toward digitalization, sustainability, and inland diversification, thereby easing seasonality and stimulating higher-spending arrival[1]Ministry of Industry and Tourism, “Sustainable Tourism Strategy 2030,” turismo.gob.es. Robust urban demand, notably in Madrid and Barcelona, pushes average daily rates upward, while Canary Islands’ year-round climate elevates off-peak occupancy, mitigating traditional winter troughs. Technology-enabled direct booking initiatives and SOCIMI-led asset reinvestment complement these macro drivers, positioning the Spain hospitality market for durable gains across the forecast horizon.

Key Report Takeaways

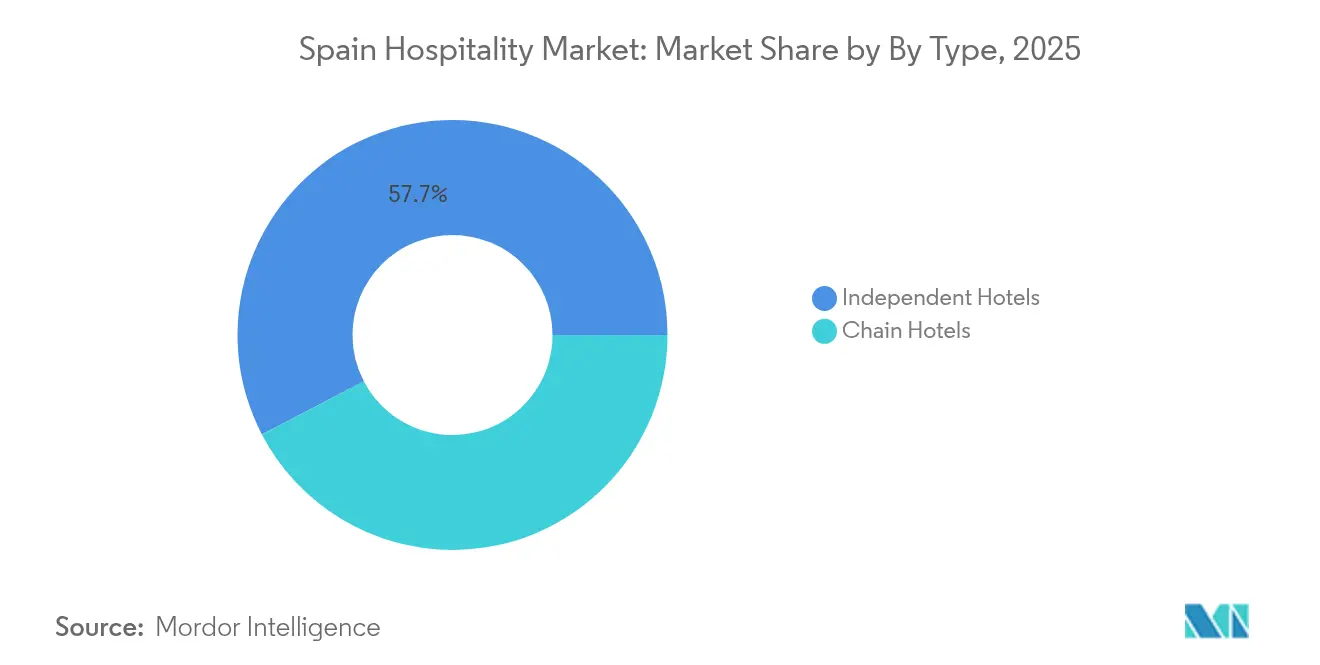

- By type, Independent Hotels held 57.65% of Spain hospitality market share in 2025, whereas Chain Hotels are forecast to record the fastest 5.78% CAGR between 2026-2031.

- By accommodation class, Mid & Upper-Mid-scale properties commanded 44.20% of Spain hospitality market size in 2025, while Luxury accommodations are projected to advance at a 6.42% CAGR between 2026-2031.

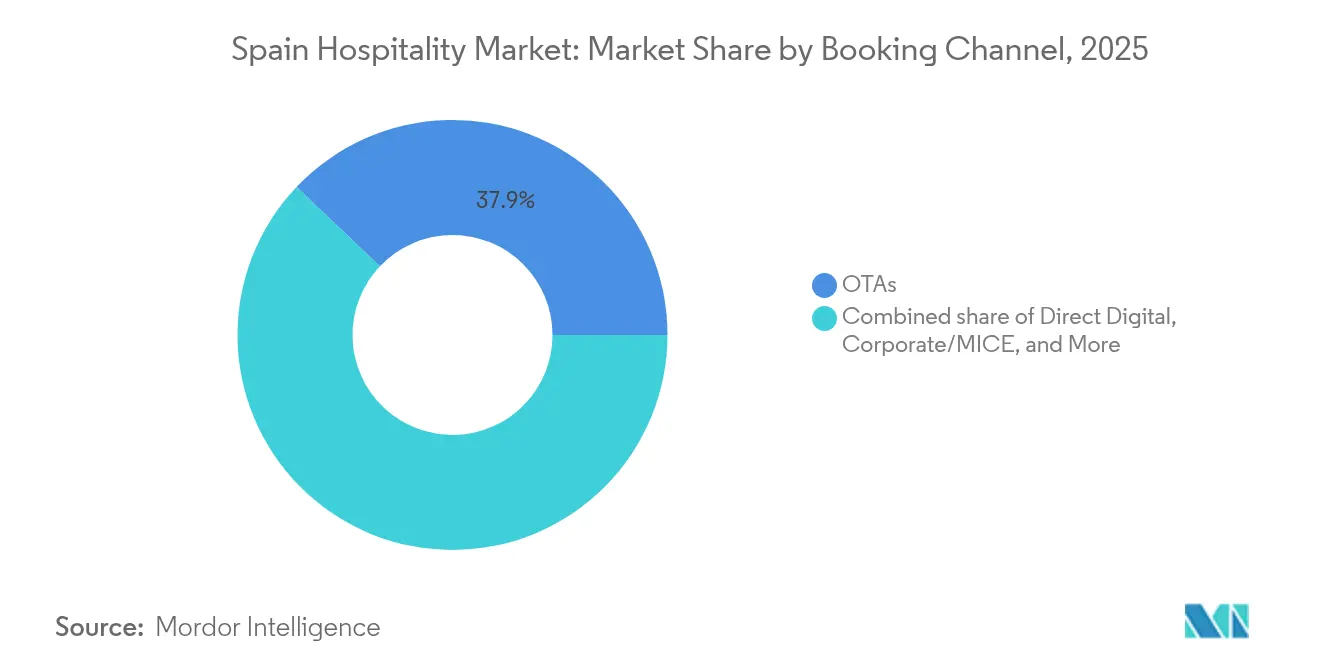

- By booking channel, OTAs controlled 37.92% share of Spain hospitality market size in 2025, yet Direct Digital bookings are rising at a 9.35% CAGR between 2026-2031.

- By region, Andalusia led with 17.10% of Spain hospitality market size in 2025, whereas the Canary Islands exhibit the highest 4.72% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising inbound leisure tourism post-pandemic | +1.2% | Global, with concentration in Andalusia, Catalonia, Canary Islands | Medium term (2-4 years) |

| Surge in boutique & lifestyle concepts driving ADR | +0.8% | Urban centers: Madrid, Barcelona, Seville | Short term (≤ 2 years) |

| Government push for high-spending visitors (Tourism Strategy 2030) | +0.7% | National, with emphasis on cultural destinations | Long term (≥ 4 years) |

| Expansion of hotel REIT structures boosting capex | +0.6% | Madrid, Barcelona, Balearic Islands | Medium term (2-4 years) |

| Emergence of digital nomad visas expanding long-stay demand | +0.4% | Urban centers and coastal regions | Medium term (2-4 years) |

| Climate-driven shoulder-season travel shift | +0.5% | Coastal regions, particularly Mediterranean and Atlantic coasts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Inbound Leisure Tourism Post-Pandemic

Visitor arrivals rebounded to 94 million in 2024, surpassing pre-crisis peaks and generating EUR 126 billion (USD 137.34 billion) in spending, a performance that lifted tourism GDP by 6% twice the national economic growth rate. The United Kingdom delivered 18.4 million visitors, while the United States posted 40% growth as long-haul connectivity improved. Hotel occupancy climbed to 74.6% in 2024, and average daily rates reached EUR 158.40 (USD 172.66) as supply discipline preserved pricing power[2]Cushman & Wakefield, “Spanish hotel RevPAR sets record,” cushmanwakefield.com. . Off-peak travel accelerated faster than high-season bookings, confirming seasonality dilution that sustains year-round employment. This demand uptick is projected to keep Spain's hospitality market ADR above inflation across the medium term. Employment expanded 3.8% by December 2024, highlighting labor absorption capacity that underpins wider economic contributions.

Surge in Boutique & Lifestyle Concepts Driving ADR

Design-led hotels command rate premiums as travelers favor authentic urban experiences; Room Mate Hotels reported 37% sales growth in 2023 after launching its upscale Room Mate Collection and integrating contactless tech to reinforce guest personalization. Luxury ADR now ranges EUR 479–761 (USD 522.11–830.49), well above mid-scale averages, and RevPAR for top-tier assets rose beyond USD 128.62 per room in 2024. Environmental certification also plays a pricing role, with 52.4% of surveyed travelers willing to pay premiums for eco-certified stays[3]MDPI, “Willingness to Pay More for Eco-Certified Hotels,” mdpi.com. Food and beverage contribute up to 40% of total revenue in luxury properties, confirming experiential dining as a profit lever. Dynamic pricing tools adopted by independents generated 15% revenue gains, narrowing the distribution gap with branded chains. Consumers increasingly book boutique properties directly, amplifying margin benefits. Continued urbanization of lifestyle brands is expected to widen rate differentials and elevate Spain hospitality market earnings.

Government Push for High-Spending Visitors

Tourism Strategy 2030 redirects national promotion toward travelers spending EUR 2,000-3,000 (USD 2,180–3,270) per trip, prioritizing cultural and gastronomic segments that accounted for 32% and 28% of visits in 2024 respectively[4]Tourism Review, “Spain expects record numbers of international travelers,” tourism-review.com. . The strategy allocates USD 4.29 billion in Recovery and Resilience Mechanism funding toward digitalization, sustainability, and competitiveness enhancements, with specific emphasis on cultural and gastronomic tourism that drove 32% and 28% of visits respectively in 2024. The Startup Law introduced a digital-nomad visa that lengthens average stays and diversifies seasonality, reinforcing inland and secondary-city tourism flows. Marketing in North America lifted U.S. spending 74.1% above 2019-figures, showcasing the potency of high-yield source diversification. Heritage-rehabilitation grants spur investment in historic assets, enriching product depth. These interventions collectively add approximately 0.7 percentage points to Spain hospitality market CAGR.

Expansion of Hotel REIT Structures Boosting Capex

SOCIMI vehicles enjoy 0% corporate tax on qualifying rents, funneling capital toward refurbishments and consolidations that heighten asset quality. Hotel investment reached USD 3.27 billion across 147 deals in 2024, with domestic investors accounting for 57% of volume as local players capitalized on recovery visibility. The USD 228.9 million sale of Madrid’s Hotel Miguel Ángel exemplifies renewed appetite for trophy assets. Urban properties took 53% of 2024 capital flows, overtaking resort assets for the first time, signaling investor faith in business-travel normalization. Prospective tax reforms, however, threaten USD 16.35 billion in pipeline investments and could temper future deal counts. Even with policy uncertainty, SOCIMIs are expected to continue upgrading room stock, boosting the hospitality industry in Spain positioning through higher RevPAR potential.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Over-tourism regulations in key coastal cities | -0.9% | Barcelona, Balearic Islands, Malaga | Short term (≤ 2 years) |

| Escalating labour shortages & wage inflation | -1.1% | Madrid, Barcelona, nationwide | Medium term (2-4 years) |

| Regulatory delays in hotel project approvals | -0.6% | Andalusia, Canary Islands, Valencia | Medium term (2–4 years) |

| Rising insurance and utility costs | -0.7% | Nationwide | Short to medium term (1–3 years) |

| Source: Mordor Intelligence | |||

Over-Tourism Regulations in Key Coastal Cities

Barcelona will phase out 10,000 short-term rental licenses by 2028, reducing alternative supply and nudging demand toward hotels, where 75% of visitors already stay. Malaga froze new holiday-rental permits across 43 districts, while Mallorca tightened cruise berthing rules to alleviate congestion. New guest-registration mandates effective December 2024 require 40-plus data fields per traveler, raising compliance costs for small operators. Valencia now issues five-year accommodation permits and bans room-only lets, adding administrative hurdles. Expanded tourist taxes and insurance requisites also temper price competitiveness. Although hotels may benefit from reduced peer-to-peer competition, cap-ex for regulatory adaptation can dilute immediate gains. These measures collectively shave 0.9 percentage points off Spain hospitality market CAGR in the near term.

Escalating Labour Shortages & Wage Inflation

Hotel wages advanced merely 10% from 2021-2024 while room rates climbed 61.5%, fueling worker unrest and elevating turnover. Unions in Madrid are demanding 10% salary hikes, a move likely to ripple across other tourist hubs. Labor costs account for 35-38% of revenue in upscale hotels, so wage inflation exerts direct pressure on gross operating profit margins. The sector added nearly 25,000 jobs in March 2025 yet still struggles to fill skills gaps in revenue management and guest engagement. Automation and contactless service investments offer partial relief but require capital and process redesign. Escalating energy prices from 2.9% to 3.3% of revenue—compound cost burdens. Together, these dynamics subtract 1.1 percentage points from Spain hospitality market CAGR during the forecast window.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Independent Properties Sustain Dominance Amid Chain Acceleration

Independent Hotels captured 57.65% Spain hospitality market share in 2025, reflecting a legacy of family-owned establishments embedded in local communities. Many independents leverage cultural authenticity and flexible service models to match dynamic traveler expectations, yet they often lag in technology adoption and international distribution reach. Chain Hotels, supported by loyalty programs and standardized service, are expanding via franchise and management contracts, with IHG signing four new Spanish properties in 2024 and targeting 50 openings by 2026. The segment’s projected 5.78% CAGR indicates sustained investor appetite for brand penetration, particularly in secondary cities seeking uplift in average daily rate and RevPAR. Management-light “manchise” models help owners pivot from lease agreements to variable-fee structures that share demand risk, thereby elevating Spain hospitality market efficiency. Synergies between local knowledge and global standards continue to blur the distinction between pure independent and branded operations through soft-brand programs.

Independent operators increasingly collaborate with distribution technology providers, narrowing rate-shopping disadvantages and boosting direct digital traffic. Meanwhile, multinational platforms such as Wyndham’s Super 8 expansion and Hyatt’s joint venture with Grupo Piñero introduce budget and all-inclusive scale economies that independents struggle to replicate. Consolidation among domestic chains is expected, given the under-30% combined share held by the top five groups. Overall, competitive dynamics signify that Spain hospitality market size for chain operators will rise faster than independents’, albeit from a lower base, as branding, standardized safety protocols, and loyalty perks resonate with price-insensitive travelers.

By Accommodation Class: Mid-Scale Commands Volume While Luxury Outpaces Growth

Mid & Upper-Mid-scale hotels accounted for 44.20% of Spain hospitality market size in 2025, buoyed by broad appeal among middle-income European tourists and domestic weekend travelers. Properties in this category balance amenity breadth and rate positioning, making them a stable backbone for both chains and independents. Conversely, Luxury accommodations register a leading 6.42% CAGR as affluent guests seek privacy, wellness, and curated cultural experiences, trends reinforced by strong U.S. and Middle-Eastern arrivals. Meliá’s premium re-positioning of 40 hotels confirms strategic capital allocation toward top-tier segments that deliver superior margins.

Sustainability credentials increasingly drive booking decisions in luxury, with Five-star resorts adopting renewable energy and zero-single-use plastic initiatives that justify ADR premiums. Extended stays by digital nomads and relocation travelers also fuel Service Apartment demand, providing an alternative to peer-to-peer rentals constrained by regulatory tightening. Budget & Economy hotels benefit from airline capacity recovery and inland tourism promotion, yet must contend with higher energy cost exposure due to thin margins. Segment interplay therefore suggests Spain hospitality market size will tilt modestly toward upscale offerings, even as mid-scale retains the greatest absolute revenue base.

By Booking Channel: Direct Digital Gains Traction Against OTA Dominance

OTAs retained a 37.92% share of the Spain hospitality market size in 2025, underscoring online intermediaries’ entrenched role in leisure trip planning. However, hotels’ investment in proprietary engines, membership rates, and targeted CRM has pushed Direct Digital bookings to a 9.35% CAGR, eroding commission drag and improving data ownership. Corporate/MICE reservations revived in tandem with conference calendar normalization, particularly in Madrid and Barcelona, where convention center upgrades attract high-yield events.

Mobile-first approaches boost direct consumer engagement through chat-based upselling, AI-powered rate alerts, and seamless payment solutions that foster repeat bookings. OTA power continues, but metasearch fee inflation and changes in Google travel rankings amplify hotels’ resolve to diversify. Wholesale and traditional agents pivot to bespoke group products, plugging gaps in service complexity and insurance that pure digital pathways cannot match. Consequently, the channel mix evolution supports higher net RevPAR and margin accretion within the hospitality industry in Spain.

Geography Analysis

Spain hospitality market exhibits nuanced regional dynamics: Andalusia’s 17.10% revenue share reflects synergistic coastal and cultural assets, supported by infrastructure upgrades that maintain high occupancy even in traditional low seasons. The region’s initiative to diversify into inland eco-tourism further shields revenue from beach-centric volatility and positions it for gradual ADR enhancement. Catalonia continues to capitalize on Barcelona’s global appeal; however, stricter lodging and cruise controls aim to alleviate crowding, potentially redistributing demand toward Girona and Tarragona. Madrid’s hotel pipeline of roughly 2,300 rooms tilts toward boutique independents, while conference-driven weekday demand accelerates recovery of corporate average rates beyond 2019 benchmarks.

The Canary Islands lead growth velocity at 4.72% CAGR, aided by the rollout of direct transatlantic routes and investments in solar energy that cut operating costs for large resort complexes. The archipelago’s visitor cap on protected natural parks balances conservation with experiential quality, reinforcing its long-term competitiveness. Valencia blends Mediterranean sun-and-beach with UNESCO gastronomy credentials; its emergent film-tourism segment, spurred by regional production incentives, widens off-season footfall.

Rest-of-Spain clusters like Galicia, Basque Country, and Castilla-La Mancha increasingly benefit from Tourism Strategy 2030 funding streams that promote inland heritage circuits and agritourism. High-speed rail expansion shortens travel times from Madrid to northern provinces, facilitating multiregional itineraries and lifting average length of stay. Climate change’s asymmetric effects, reflected in 10% differential spending tied to temperature variance, fortify these cooler destinations as summer alternatives.

Competitive Landscape

Spain's hospitality market is highly fragmented, with major players holding a limited share of the total room inventory. This fragmentation presents considerable headroom for growth, creating opportunities for both scale-driven expansion and niche brand differentiation. Meliá Hotels International is leading the charge in upscale repositioning, reporting an EBITDA of over EUR 525 million (USD 572.25 million) in 2024 and allocating EUR 400 million (USD 436 million) toward 2025 upgrades to enhance ADR and loyalty capture. NH Hotel Group is countering rising operational costs by investing in energy-efficiency retrofits, boosting asset competitiveness without sacrificing guest experience. Barceló, meanwhile, is pursuing regional densification, exemplified by its acquisition of two León properties to unlock feeder-market synergies.

Global brands are deepening their footprint in Spain through strategic acquisitions and asset-light growth models. Hyatt expanded its all-inclusive offering with the acquisition of three resorts in Tenerife, targeting U.S. corporate travel demand. Wyndham is filling a gap in the economy segment by rolling out 40 Super 8 hotels across secondary Spanish cities, appealing to independent owners through cost-effective franchising. IHG continues its soft-brand expansion via the Vignette Collection in Mallorca, offering independent luxury hotels access to global distribution without sacrificing brand identity. These international moves reflect rising confidence in Spain’s long-term demand fundamentals, especially in leisure and midscale segments.

Technology and sustainability have emerged as core competitive battlegrounds across the Spanish hospitality landscape. Operators are differentiating through proprietary mobile apps, AI-enabled guest services, and zero-waste programs aimed at eco-conscious travelers. Regulatory developments — including stricter guest-registration protocols and caps on short-term rentals — are raising the bar for compliance and digital capability. This is inadvertently accelerating consolidation, favoring brands equipped with robust back-end systems and data governance. However, independent hotels continue to demonstrate resilience, capitalizing on authenticity, local roots, and operational agility to retain loyal domestic guests. With investor capital returning and global brands scaling via franchise and management deals, competitive intensity is set to rise sharply in the coming years.

Spain Hospitality Industry Leaders

Meliá Hotels International

NH Hotel Group (Minor)

Barceló Hotels & Resorts

Eurostars Hotel Company

Iberostar Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Barceló Hotel Group acquired two hotels in León, Spain the 134-room Barceló León Conde Luna and the 62-room Occidental León Alfonso V from By Vamuca, with renovation plans aimed at premium repositioning.

- June 2025: Barceló Group forecast net profit of EUR 310 million (USD 337.9 million) for 2025 and announced a EUR 500 million (USD 545 million ) cap-ex program focused on upgrades and openings across its 299-property network.

- April 2025: Wyndham signed an exclusive agreement with Soliteight to develop 40 Super 8 economy hotels across Spain and Portugal over the next decade.

- July 2024: Room Mate Hotels purchased Staying Valencia’s portfolio of 10 boutique assets, targeting EUR 40 million (USD 43.6 million) EBITDA for 2025 after integration.

Spain Hospitality Market Report Scope

Hospitality is a broad term that encompasses all aspects of the service industry, namely lodging, food and beverage, event planning, theme parks, travel agencies, tourism, hotels, restaurants, and bars. The hospitality industry in Spain is segmented by type and by segment. By type, the market is segmented into chain hotels and independent hotels. By segment, the market is bifurcated into service apartments, budget and economy hotels, mid- and upper-mid-scale hotels, and luxury hotels. The report offers market size and forecasts for the hospitality industry in Spain in terms of value (USD) for all the above segments.

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geography

| Andalusia |

| Catalonia |

| Madrid |

| Valencia |

| Canary Islands |

| Rest of Spain |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geography | Andalusia |

| Catalonia | |

| Madrid | |

| Valencia | |

| Canary Islands | |

| Rest of Spain |

Key Questions Answered in the Report

How large is the Spain hospitality market in 2026?

The sector generated USD 125.34 billion in 2026 and is forecast to reach USD 152.84 billion by 2031.

What is the expected growth rate for Spanish hospitality between 2026 and 2031?

Spain hospitality market is projected to grow at a 4.05% CAGR over the five-year period.

Which accommodation class is expanding fastest in Spain?

Luxury hotels lead growth with a 6.42% CAGR, fueled by high-spending international guests and upgrade investments.

Which booking channel is gaining share most rapidly?

Direct Digital reservations are expanding at a 9.35% CAGR as hotels emphasize loyalty programs and lower commission costs.

Which Spanish region shows the highest hospitality growth potential?

The Canary Islands top the forecast with a 4.72% CAGR thanks to all-season demand and sustainable tourism policies.

Page last updated on: