India Architectural Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

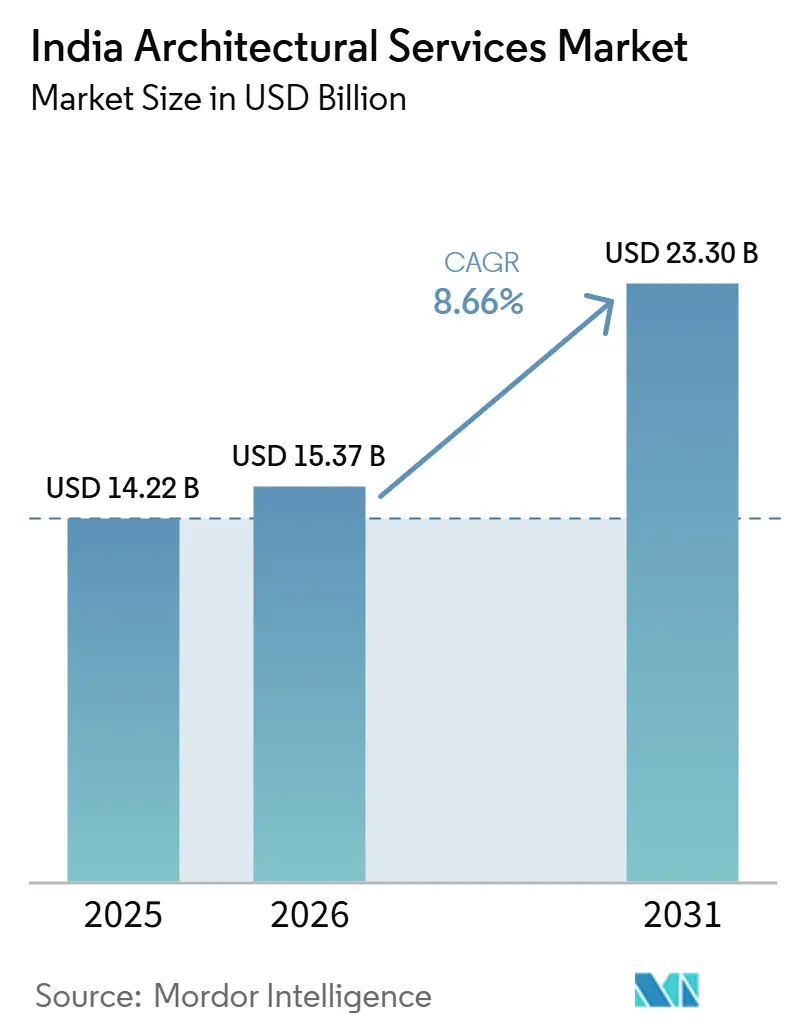

| Base Year Market Size (2025) | USD 14.22 Billion |

| Market Size (2026) | USD 15.37 Billion |

| Market Size (2031) | USD 23.30 Billion |

| Growth Rate (2026 - 2031) | 8.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Architectural Services Market Analysis by Mordor Intelligence

The India Architectural Services Market size is projected to be USD 14.22 billion in 2025, USD 15.37 billion in 2026, and reach USD 23.30 billion by 2031, growing at a CAGR of 8.66% from 2026 to 2031. Demand is being supported by public capital expenditure, healthier commercial project activity, and a rising flow of data infrastructure work that needs more specialized design input. The market also benefits from a structural urban buildout cycle, because India’s urban population is projected to reach 951 million by 2050 and more than half of the urban infrastructure needed by that point is still to be built[1]World Bank, “India Has a Critical Opportunity to Drive Resilient Urban Development,” World Bank, worldbank.org. This keeps the India architectural services market tied to long-term city-building, housing, transport, and civic asset creation rather than only to short property cycles. Competition remains moderately concentrated in the premium project layer, where global firms and established Indian practices compete for complex mandates, while a wide field of local firms still handles a large share of routine volume. Firms that can manage BIM workflows, sustainability compliance, and retrofit complexity are in a stronger position to protect pricing and expand their role in the India architectural services market.

Key Report Takeaways

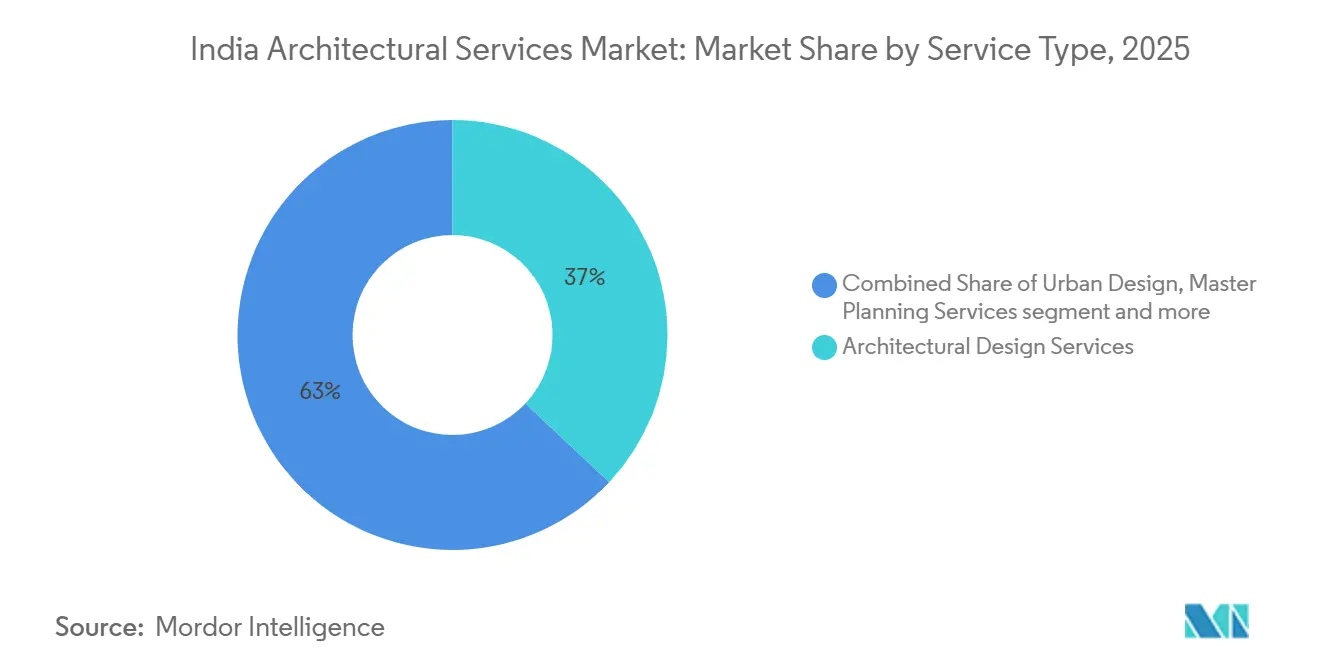

- By service type, architectural design Services held 37% of the India architectural services market share in 2025, while interior Architecture and splace planning services are forecast to expand at a 10.1% CAGR through 2031.

- By project type, new construction accounted for 76% of the India architectural services marke sizet in 2025, while renovation is projected to grow at a 9.6% CAGR through 2031.

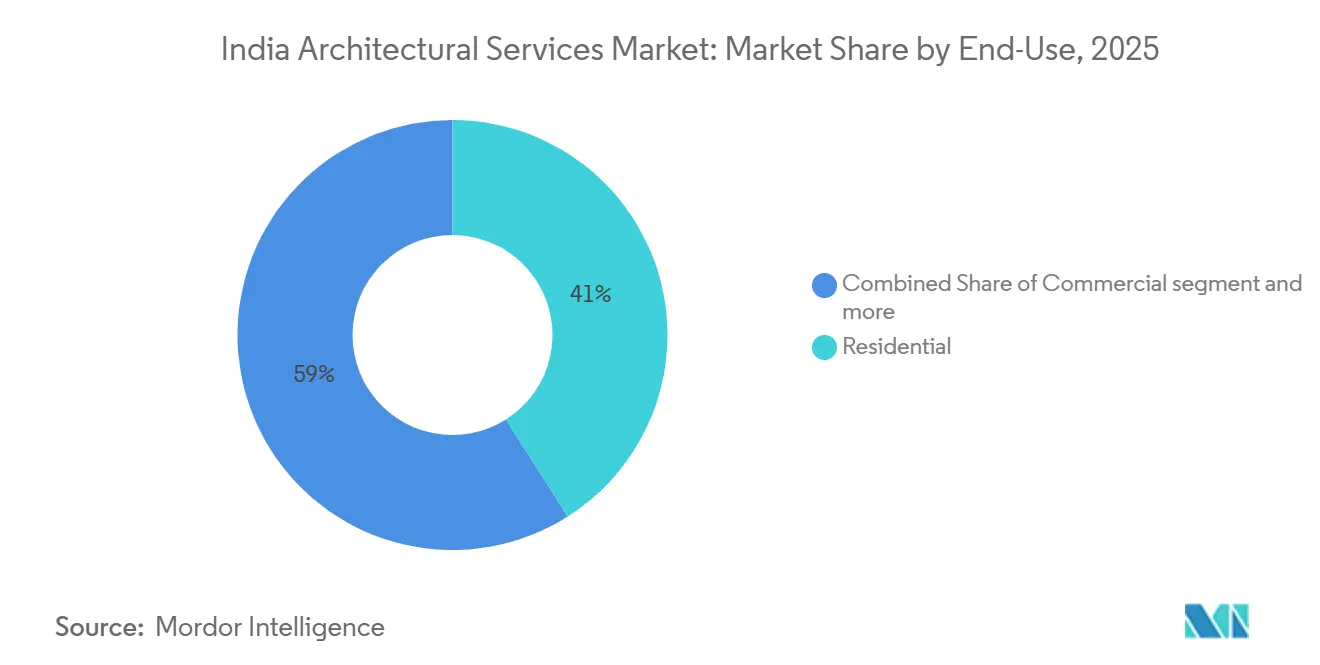

- By end-use, residential held 41% of the India architectural services market share in 2025, while Infrastructure-linked Buildings are advancing at 10.8% CAGR through 2031.

- By investment source, Private accounted for 58% of the India architectural services market in 2025, while Public is expected to record the highest CAGR of 9.9% through 2031.

- By geography, West India led with a 29% share of the India architectural services market in 2025, while North India is projected to grow at a 9.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Architectural Services Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-Led Urban Expansion | +2.3% | National, with strongest traction in Delhi NCR, Mumbai MMR, Bengaluru, and Pune | Medium term (2-4 years) |

| Commercial Real Estate Recovery | +1.7% | National, concentrated in Bengaluru, Mumbai, Hyderabad, and Delhi NCR | Short term (≤ 2 years) |

| Industrial Park and Logistics Hub Development | +1.1% | North India, West India, and Central India | Medium term (2-4 years) |

| Metro Rail, Airport, and Transit-Oriented Development | +1.0% | National, led by Thane, Chennai, Jaipur, Ahmedabad, and Bhubaneswar | Medium term (2-4 years) |

| Data Center and GCC Campus Expansion | +0.9% | South India, West India, and North India | Long term (≥ 4 years) |

| Green Building and Sustainability Demand | +0.7% | National, with stronger traction in North and South India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure-Led Urban Expansion Anchors Greenfield Demand

Public capital expenditure remains the strongest structural support for the India architectural services market. Budget 2026-27 kept central capital expenditure at 3.1% of GDP, which sustained a broad pipeline across transport, housing, and civic infrastructure. PMAY-U dashboards showed that 9.9 million homes had been grounded by June 2026, which kept housing drawings, approvals, and site-level design supervision active across states. The World Bank also said that India still has more than half of its future urban infrastructure left to build, which gives firms a longer project runway than a normal real estate cycle would provide. This mix keeps greenfield design demand spread across affordable housing, civic facilities, and mixed-use urban districts. It also favors firms that can meet technical qualification filters and government compliance requirements before price becomes the deciding factor.

Commercial Real Estate Recovery Recalibrates Program Complexity

Commercial activity is supporting the India architectural services market through a more specialized type of project demand. India now hosts more than 2,117 GCCs, employs over 2.3 million professionals in that base, and generates nearly USD 100 billion in related revenue, underscoring the need for custom workplace planning and interior delivery. That matters because newer mandates are no longer simple office fit-outs and now require stricter standards for collaboration spaces, sustainability, employee experience, and branded workplace identity. Interio by Godrej’s projects business has already executed more than 1,000 projects across 100 million sq ft and is targeting 500 GCC sites by 2027, which shows the scale of the design and fit-out pipeline. As a result, the faster growth in interior architecture and space planning reflects program complexity as much as it reflects pure project volume. The India architectural services market is therefore benefiting from a commercial cycle in which design depth matters more than standard floorplate delivery.

Industrial Park and Logistics Hub Development Opens Mid-Tier Project Pipeline

Industrial and logistics development is opening a wider layer of mid-scale work within the Indian architectural services market. Jacobs was appointed as a knowledge partner by NICDC under a 3-year contract to support program delivery for 12 industrial corridors across 10 states, with an expected investment of USD 18 billion and 1 million direct jobs, indicating a long pipeline for planning and industrial campus design. CIDCO is also developing a 924-acre integrated logistics park in Navi Mumbai, which adds another large mandate tied to airport and port-linked infrastructure. These projects require more than building design; they also require master planning, circulation design, utility integration, and phased delivery coordination. That creates room for Indian firms with local approval experience and for global firms that can manage multi-site industrial programs. It also broadens the revenue pool beyond residential and office-led assignments.

Metro Rail, Airport, and Transit-Oriented Development Multiplies Design Scopes

Transit and airport projects are expanding the design scope of the India architectural services market beyond stand-alone buildings. The revised transit-oriented development framework that requires 65% affordable housing along metro corridors is raising the amount of redesign and mixed-use planning needed around new lines. Adani Airports also announced more than INR 20,000 crore (USD 2.3 billion) in first-phase airport city investment across 6 airports, covering more than 655 acres and nearly 22 million sq ft, with LEED Gold pre-certification already in place. That pipeline extends architecture work into terminals, hospitality, offices, retail, and surrounding urban districts. It also increases the value of firms that can combine transport interface planning with sustainability documentation and mixed-use district design. In practical terms, one transit program can now generate several linked assignments over multiple years.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Approval and Land-Acquisition Delays | -1.1% | National, with acute pressure in Maharashtra, Karnataka, and corridor-heavy North India | Medium term (2-4 years) |

| Price Pressure in a Fragmented Design Market Suppresses Mid-Market Margins | -0.8% | National, with stronger pressure in Tier-2 and Tier-3 cities and affordable housing | Short term (≤ 2 years) |

| Skilled Talent Shortage in BIM and Sustainable Design | -0.6% | National, with stronger impact in major metros and large public project clusters | Medium term (2-4 years) |

| Fee Compression from Design-Build and EPC-Led Procurement | -0.4% | National, especially in commercial, affordable housing, and mid-market institutional projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Approval and Land-Acquisition Delays Compress Fee Realization

Approval bottlenecks continue to slow billing cycles in the India architectural services market. Cabinet Secretary Somanathan said that land acquisition accounted for 35% of issues raised across major infrastructure projects under the PRAGATI framework, underscoring how early-stage delays carry over into project execution. Business Standard also reported disruptions to approvals affecting project schedules and profitability in MMR and Bengaluru during 2025. For architecture firms, the main issue is not only a slower project launch, but also a slower pace of work. The deeper problem is that teams remain engaged during design freeze periods even as the freeze is pushed back. This weakens cash flow visibility and makes it harder for firms to scale specialist staff at the same pace as opportunities.

Price Pressure in a Fragmented Design Market Suppresses Mid-Market Margins

Price pressure remains a basic restraint across the India architectural services market because the competitive base is very broad and much of it is local. The draft points to an estimated licensure base of more than 100,000 registered architects, with many operating in private practice and competing for residential and mid-market commercial work. That structure keeps fee recovery under pressure in many routine assignments, especially outside the premium project layer. The problem becomes sharper when design-build and EPC structures absorb architecture fees inside a wider project budget rather than pricing design as a stand-alone value stream. Firms that cannot show strength in BIM, sustainability certification, or a specialized building type face weaker pricing power and a slower path to margin improvement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Interior Architecture Outpaces Legacy Design Revenue

Architectural Design Services held 37% of the India architectural services market in 2025, while Interior Architecture and Space Planning Services are set to grow at 10.1% CAGR through 2031. This keeps design services in the lead because every new build and most retrofit projects still begin with core architectural planning, client briefing, and statutory documentation. At the same time, faster growth in interior architecture reflects the rising role of GCC campuses, branded workplaces, premium housing, and specialized fit-outs. India’s GCC base has crossed 2,117 entities, with more than 2.3 million professionals, keeping demand strong for customized interiors and space optimization. Interio by Godrej has already executed more than 1,000 projects across 100 million sq ft and is targeting 500 GCC sites by 2027, which shows the commercial depth of this service line[2]Deccan Herald, “Interio by Godrej Bets Big on India’s GCC Surge,” Deccan Herald, deccanherald.com.

The second layer of change is happening in documentation and delivery capability, where digital coordination is becoming a competitive filter rather than a back-office function. The National BIM Policy, published in March 2025, signals that public-sector eligibility will increasingly depend on documentation quality, model coordination, and workflow discipline. That benefits firms that can move beyond concept design and deliver structured technical packages for large institutional or infrastructure jobs. Urban Design and Master Planning Services are also gaining ground as more projects shift toward long-horizon district development rather than stand-alone buildings. The Bhubaneswar Development Authority’s agreement with Surbana Jurong for a new city master plan with an INR 8,179 crore (USD 951 million) outlay shows how master planning work can convert into multi-year delivery engagement rather than a one-time advisory role.

By Project Type: Renovation Emerges as the Durable Margin Opportunity

New Construction accounted for 76% of the India architectural services market size in 2025, which reflects the scale of greenfield housing, infrastructure, and commercial development underway. Renovation, however, is projected to grow faster at 9.6% CAGR through 2031, which points to a more durable opportunity than a simple cyclical rebound. A large share of India’s older office and commercial stock now needs energy upgrades, space reconfiguration, and compliance-driven modernization. That work is often more design-intensive because it requires phasing, occupied-site coordination, and detailed systems integration inside existing structures. The fee outcome is usually stronger than in standard new-build assignments because problem-solving intensity is higher and drawing revisions are more frequent.

This part of the India architectural services industry is also being supported by heritage reuse and by stalled projects returning to execution. The completion of the restoration of a 113-year-old Nizam-era landmark in Hyderabad during 2026 reflects a category of technically demanding adaptive reuse work that requires careful planning, specialist detailing, and institutional coordination. The 2025 Supreme Court ruling that cleared environmental approvals for 493 stalled residential projects in MMR and Pune also released a practical pipeline of redrawings, compliance resubmissions, and revised construction document packages. That kind of work rarely draws the same visibility as new launches, yet it creates steady demand for firms with regulatory knowledge and retrofit skill. Renovation therefore adds balance to the India architectural services market because it is tied to code upgrades and asset repositioning as much as to new capital cycles.

By End-Use: Infrastructure-Linked Buildings Drive Project Complexity Premium

Residential projects accounted for 41% of the India architectural services market in 2025, which kept housing as the largest end-use segment by revenue. Demand remained firm at both the affordable and premium ends, supported by public housing volumes and stronger upper-end buyer activity. Business Standard reported that Delhi-NCR premium housing sales rose 30% year over year in the first quarter of 2026, underscoring how design quality is carrying greater weight in high-value residential projects. Infrastructure-linked Buildings are growing faster at a 10.8% CAGR through 2031 because they draw on hospitals, educational assets, airports, metro stations, and civic facilities rather than a single construction cycle. This end-use group tends to support higher complexity because compliance requirements, circulation planning, safety standards, and public interface requirements are stricter.

Healthcare and institutional development add another layer of support to the India architectural services market. Budget 2026-27 took healthcare spending above INR 1 lakh crore (USD 11.6 billion) for the first time and proposed 5 regional medical hubs, which should sustain a wider flow of hospital and medical campus design mandates. Public schools, AIIMS-linked projects, and civic facilities under fast-tracked programs extend that pipeline into state-backed institutional work. Commercial demand remains important through GCC and flex workspace expansion, but infrastructure-linked buildings benefit from several public initiatives moving at the same time. That makes this segment a useful indicator of where complex, compliance-heavy design work is building fastest.

By Investment Source: Public Capex Closes the Gap on Private-Sector Dominance

Private investment sources accounted for 58% of the India architectural services market in 2025, reflecting the volume advantage of developer-led residential and commercial projects. Public investment, however, is projected to grow at a 9.9% CAGR through 2031, bringing it closer to the center of expansion. Budget 2026-27 sustained capital expenditure at 3.1% of GDP and maintained infrastructure creation as a policy priority, supporting a wider public design pipeline. The PMAY-U and PMAY-U 2.0 dashboards showed 9.9 million homes grounded by June 2026 and total central assistance sanctioned at INR 2.09 lakh crore (USD 24.3 billion), confirming the scale of publicly linked housing demand. These projects generate recurring work in drawings, site adaptations, supervision support, and compliance certification before construction advances.

Public mandates also behave differently from private ones inside the India architectural services market. They usually require empanelment, technical qualification checks, and multi-agency coordination, which narrows the field to firms with stronger track records and deeper staffing. That tends to favor mid-sized and large practices over smaller studios that cannot hold long bidding cycles or compliance overhead. AGICL’s July 2026 invitation to empanel architectural firms for nearly 100 Amaravati capital projects is a clear example of how public demand can concentrate around firms ready for scale. Over the forecast period, that shift should make public capex one of the strongest reallocators of competitive opportunity in the India architectural services market.

Geography Analysis

West India accounted for 29% of the India architectural services market size in 2025, which kept it as the largest regional segment. Maharashtra remains the main anchor because it combines urban redevelopment, data center activity, logistics infrastructure, and large mixed-use urban expansion. The Third Mumbai development, with its 324 sq km scale and planned clusters for education, healthcare, GCCs, and green data centers, adds depth to the regional design pipeline. Gujarat strengthens the region through GIFT City, DREAM City, and Dholera Smart City, where urban design, campus planning, and mixed-use architecture continue to overlap. CIDCO’s 924-acre integrated logistics park in Navi Mumbai adds another complex assignment tied to airport and port connectivity[3]CIDCO, “CIDCO Plans Integrated Logistics Park in Navi Mumbai, Earmarks 924 Acres Land,” The Economic Times, economictimes.indiatimes.com.

North India is the fastest-growing geography in the India architectural services market, with forecast growth of 9.7% CAGR through 2031. The growth base is being supported by Noida-Greater Noida infrastructure corridors, the Jewar Airport ecosystem, and stronger transit-led expansion across NCR. Uttar Pradesh has secured 1,673 IGBC-registered projects covering 1.78 billion sq ft, indicating that green design compliance is becoming a commercial opportunity for architecture firms. This regional mix is expanding design demand into suburban and peri-urban locations that previously had a smaller project base. It also supports firms that can combine mobility-linked planning, green certification, and large township documentation.

South India and East India bring a different set of demand signals to the India architectural services market. In South India, the emerging data center buildout in Visakhapatnam has raised the need for specialized industrial building design after Google broke ground on a USD 15 billion AI hub in partnership with AdaniConneX and Airtel. Chennai continues to benefit from GCC and transit-linked demand, while East India is building presence through sustainability-led mixed-use and master planning work. Central India remains the smallest regional opportunity today, but logistics and new city development in Nagpur suggest that a broader architecture pipeline can form from 2027 onward.

Competitive Landscape

The India architectural services market is moderately concentrated at the premium project tier and fragmented across the wider volume base. Global firms such as AECOM, Jacobs, Gensler, HOK, and Skidmore, Owings and Merrill compete for complex infrastructure, airport, campus, and large institutional work. Indian firms such as Morphogenesis, CP Kukreja Architects, and Hafeez Contractor remain important because they combine local code familiarity, cost discipline, and client relationships across residential and mixed-use work. This structure means that concentration is visible at the top end of project complexity but not across total project count. The result is a market where brand strength matters, yet local execution depth still decides a large share of awards.

Recent company moves show how leaders are positioning themselves inside the India architectural services market. AECOM emerged as the lowest bidder for the INR 148 crore (USD 17.2 million) Thane Integral Ring Metro general consultancy contract, which reinforces how infrastructure-led consulting wins can anchor long project cycles. Jacobs strengthened its industrial and public-sector position through the NICDC program management mandate, which spans 12 corridors across 10 states. Adani Airport City Limited also awarded architecture mandates to KPF, Benoy, and Znera Space for its airport city platform, which shows how large developers are packaging multiple design opportunities under one capital program. These moves suggest that scale, institutional access, and multidisciplinary coordination remain the most reliable ways to build share at the upper tier.

Indian practices still hold an advantage in the mid-market and in city-specific execution, especially where approval handling and local consultant networks are critical. Morphogenesis and CP Kukreja Architects stand out in sustainability-led work and culturally grounded planning, which is becoming more valuable as clients look for design quality that also supports certification outcomes. The white space remains strongest in Tier-2 master planning, healthcare architecture, and retrofit-heavy urban projects where demand is rising but specialist capacity is still limited. Smaller firms can compete effectively when they focus on a building type, a compliance niche, or a local market they know deeply. The broader competitive picture in the India architectural services market therefore remains mixed, with leadership more visible in complex mandates than in the overall project base.

India Architectural Services Industry Leaders

AECOM

Jacobs Solutions Inc.

Gensler

Perkins and Will

HOK

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: AirTrunk (Blackstone-backed) committed USD 30 billion to build 5GW of AI data-center capacity in India by 2030; Maharashtra's Chief Minister signed a letter of intent for a 3GW facility at Raigad Pen Growth Center, representing an investment of approximately USD 23.5 billion (converted from ~₹2 trillion), generating substantial demand for specialized data-center architectural and engineering design.

- June 2026: Amazon announced an additional USD 13 billion investment in AI and cloud infrastructure in India by 2030, raising its total committed investment to more than USD 21 billion between 2026 and 2030, adding to a hyperscale construction pipeline that directly drives demand for data-center campus architectural services.

- May 2026: Google broke ground on its USD 15 billion AI Hub in Visakhapatnam, Andhra Pradesh, in partnership with AdaniConneX and Airtel; the three-campus gigawatt-scale data-center development, supported by Union IT Minister Ashwini Vaishnaw, positions Andhra Pradesh as a major market for specialised industrial architecture.

- April 2026: Bhubaneswar Development Authority (BDA) signed an agreement with Singapore-based Surbana Jurong for the preparation of a comprehensive new-city master plan covering the proposed New City, with an estimated project outlay of approximately USD 960 million (converted from ₹8,179 crore), marking a significant eastern-India public-sector mandate for international urban-design services.

India Architectural Services Market Report Scope

| Architectural Design Services |

| Architectural Documentation and Delivery Services |

| Interior Architecture and Space Planning Services |

| Urban Design and Master Planning Services |

| Others |

| New Construction |

| Renovation |

| Residential | |

| Commercial | Office |

| Retail | |

| Institutional | |

| Industrial and Logistics | |

| Others | |

| Infrastructure-linked Buildings |

| Public |

| Private |

| North India |

| South India |

| West India |

| East India |

| Central India |

| By Service Type | Architectural Design Services | |

| Architectural Documentation and Delivery Services | ||

| Interior Architecture and Space Planning Services | ||

| Urban Design and Master Planning Services | ||

| Others | ||

| By Project Type | New Construction | |

| Renovation | ||

| By End-Use | Residential | |

| Commercial | Office | |

| Retail | ||

| Institutional | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure-linked Buildings | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | North India | |

| South India | ||

| West India | ||

| East India | ||

| Central India | ||

Key Questions Answered in the Report

What is the expected value of India architectural services by 2031?

The India architectural services market is projected to reach USD 23.3 billion by 2031, up from USD 15.4 billion in 2026, at an 8.66% CAGR over 2026-2031.

Which service segment is growing fastest in India?

Interior Architecture and Space Planning Services are expected to post the fastest growth, with a 10.1% CAGR through 2031, supported by GCC, workplace, and fit-out demand.

Which project type still leads revenue generation?

New Construction remained the largest project type in 2025 with 76% share, although Renovation is growing faster at 9.6% CAGR because of retrofits, compliance upgrades, and adaptive reuse work.

Which end-use creates the most complex assignments?

Infrastructure-linked Buildings are growing fastest at 10.8% CAGR because hospitals, airports, metro stations, education assets, and civic buildings require more compliance-heavy and multi-stakeholder design work.

Page last updated on: