Large Molecule Bioanalytical Testing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

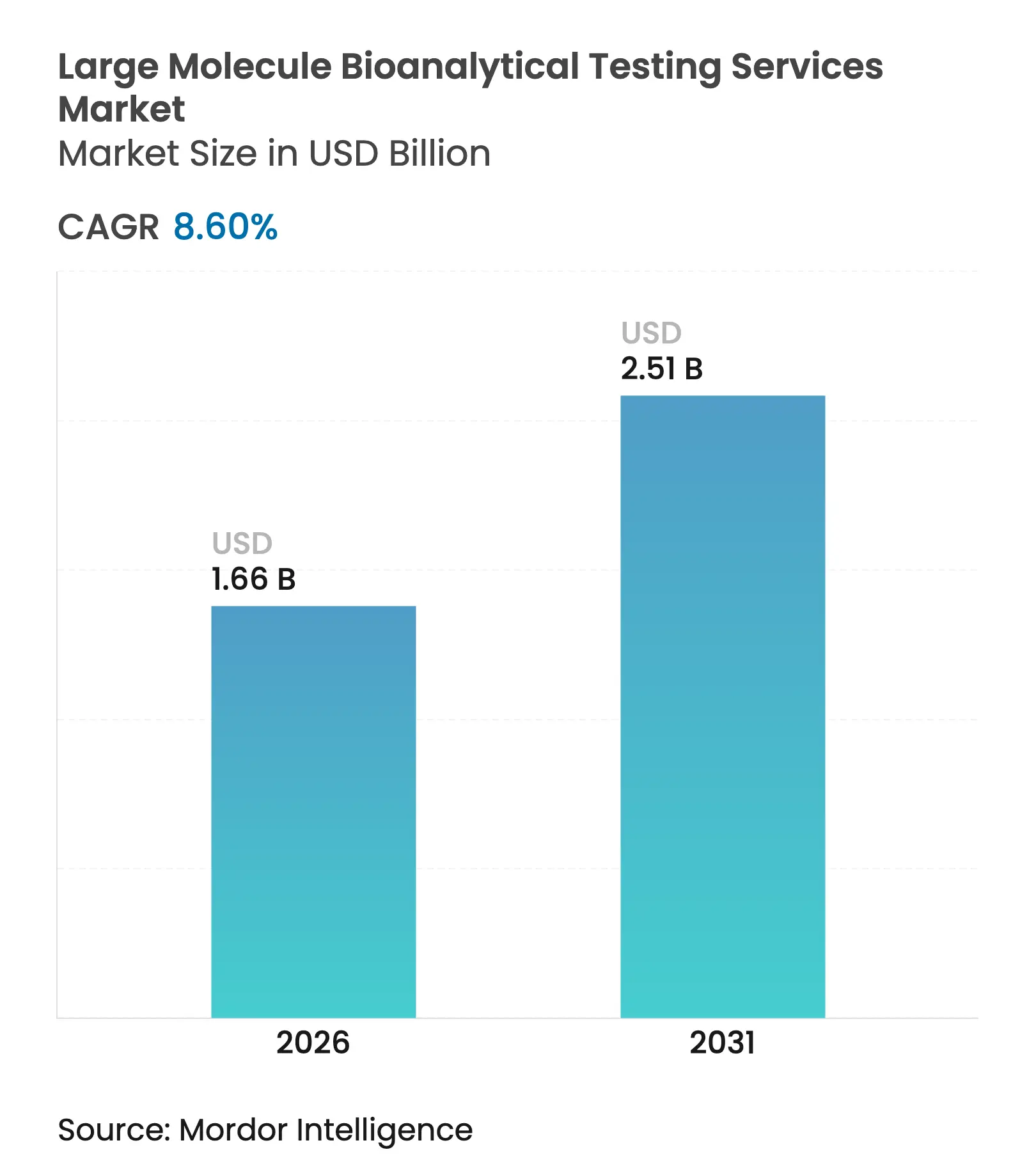

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 2.51 Billion |

| Growth Rate (2026 - 2031) | 8.60 % CAGR |

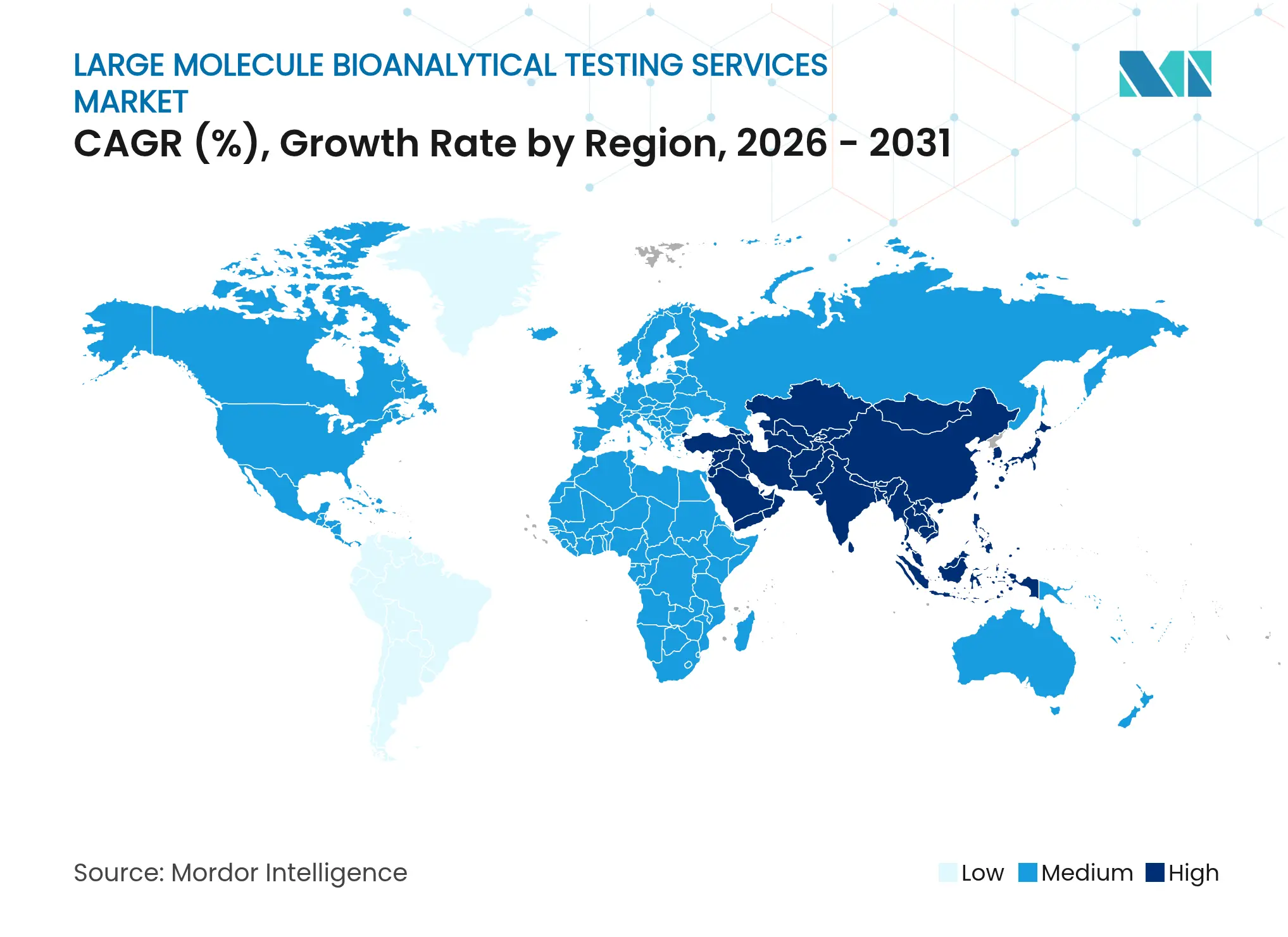

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

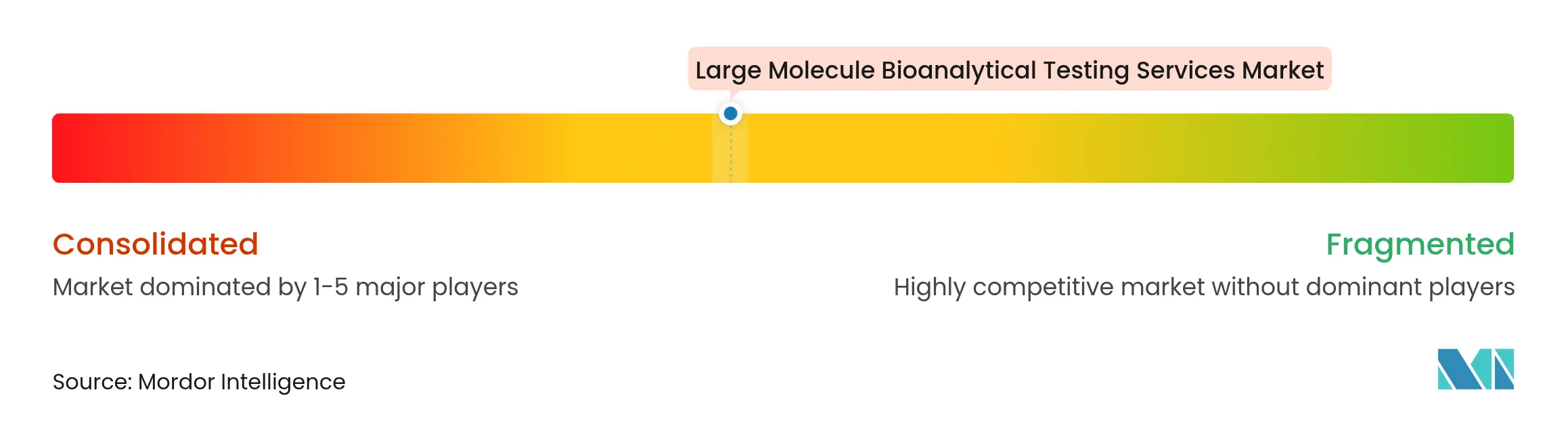

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Large Molecule Bioanalytical Testing Services Market Analysis by Mordor Intelligence

Strong clinical-phase demand, an expanding biologics pipeline, and more stringent regulatory expectations for immunogenicity testing together underpin the current momentum of the large molecule bioanalytical services market. Hybrid ligand-binding assay/liquid-chromatography platforms are widening analytical scope for complex modalities, while cloud-enabled laboratory automation is accelerating sample throughput and reducing turnaround times. Rapid technology adoption is intensifying competition as mid-tier providers challenge the scale advantages of global contract research organizations. Growing outsourcing to Asia Pacific laboratories, coupled with capacity expansions by U.S. facilities, is broadening geographic access to specialized expertise. Strategic acquisitions aimed at end-to-end capabilities and data-integrity enhancements continue to reshape the large molecule bioanalytical services market landscape.

Key Report Takeaways

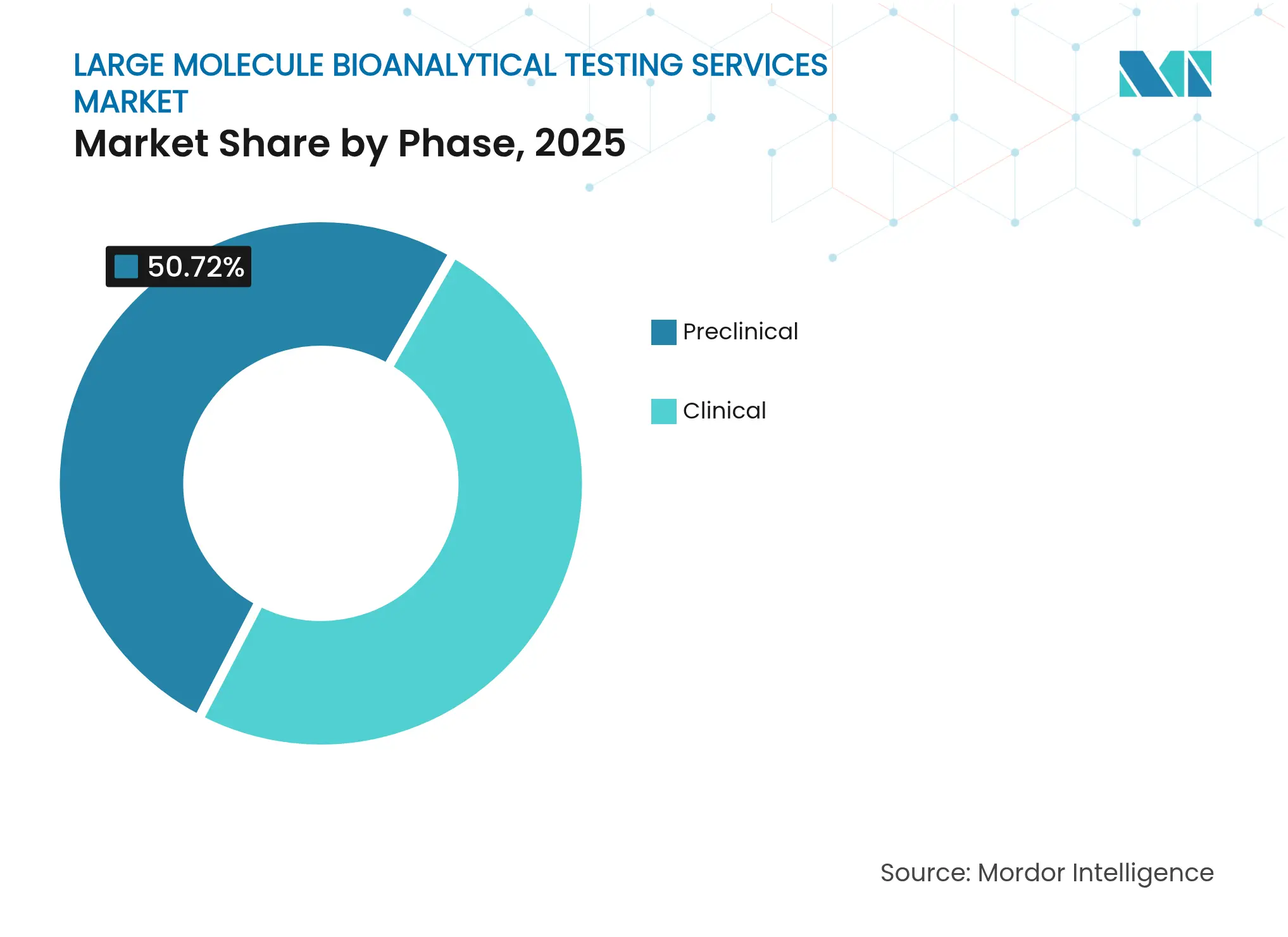

- By phase, clinical-stage testing held 49.28% of the large molecule bioanalytical services market share in 2025 and preclinical bioanalytical work is projected to grow at an 10.86% CAGR through 2031, the fastest rate among development phases.

- By molecule type, monoclonal antibodies accounted for 43.35% revenue share of the large molecule bioanalytical services market size in 2025 and cell therapy analytics are expanding at an 11.6% CAGR to 2031, the quickest pace within molecule categories.

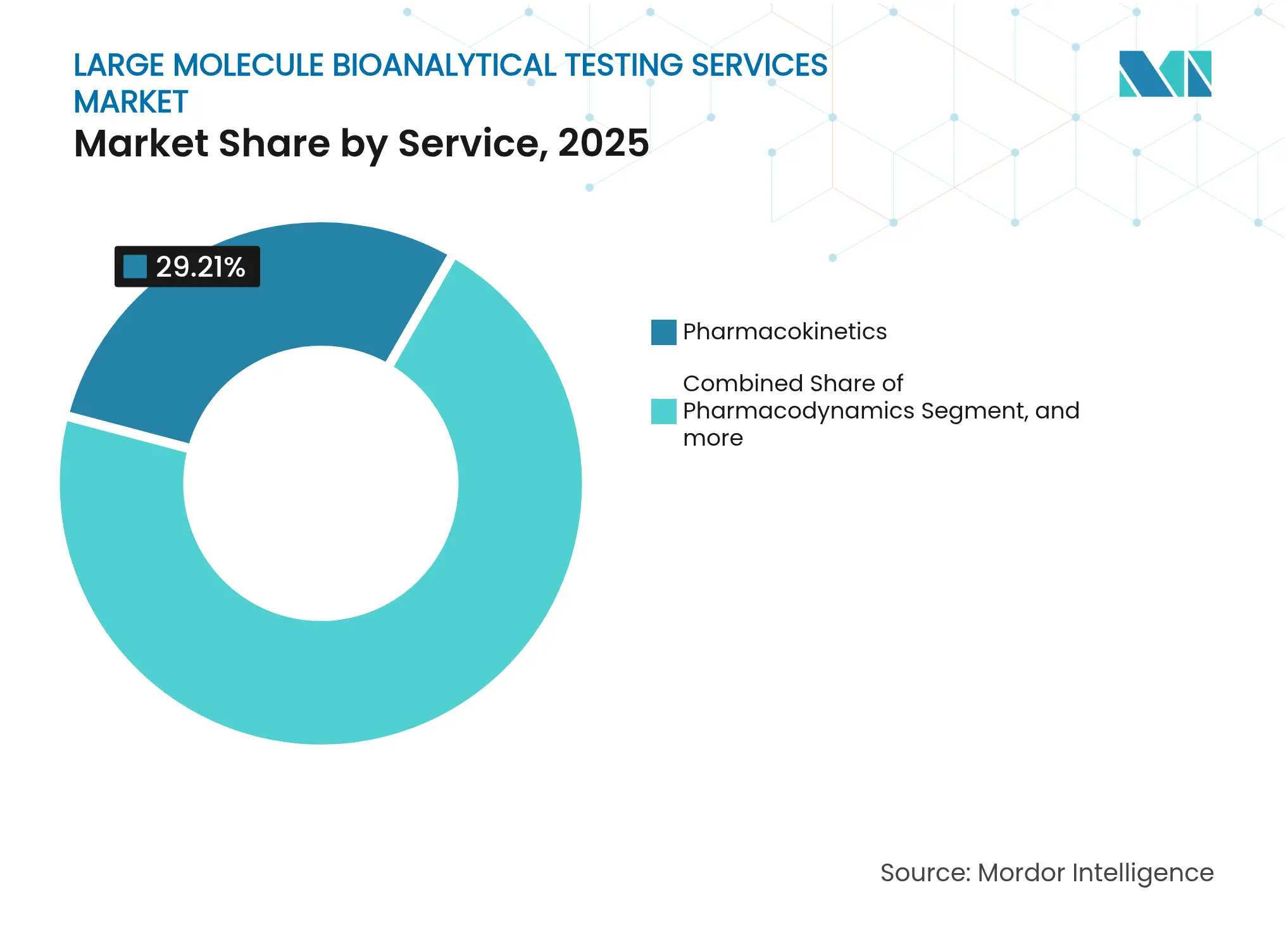

- By service, pharmacokinetics led with 29.21% of 2025 revenue, whereas bioequivalence testing is expected to post the 12.35% CAGR through 2031 on the back of biosimilar pipelines.

- By therapeutic area, oncology represented 34.45% of 2025 spending; rare-disease programs are set to rise at a 13.1% CAGR, the most rapid among therapeutic fields.

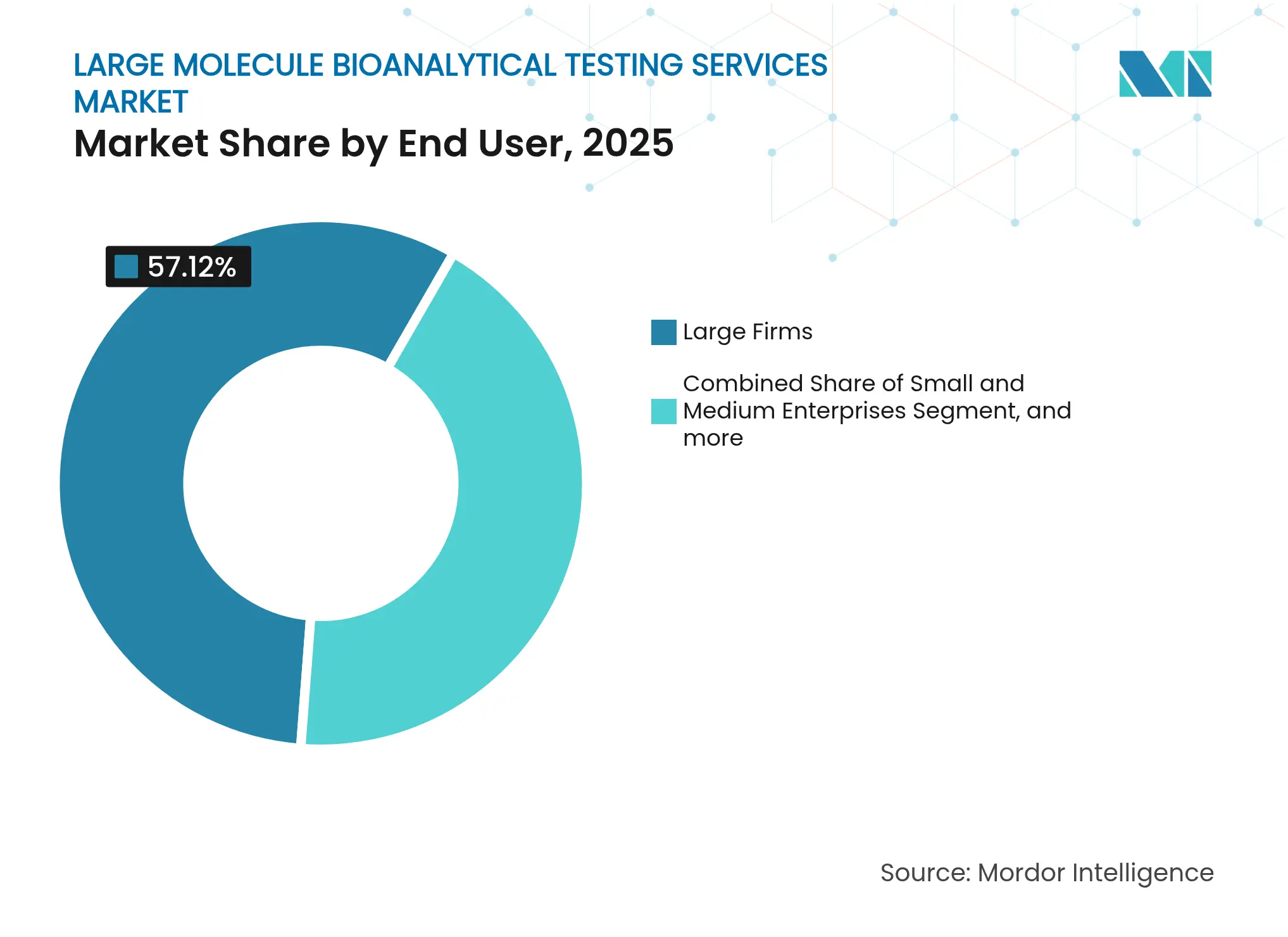

- By end user, large pharmaceutical companies contributed 57.12% of demand in 2025, while small and mid-size enterprises are forecast to increase outlays at a 9.95% CAGR to 2031.

- By geography, North America retained 35.40% regional share in 2025, whereas Asia-Pacific is forecast to post a 12.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Large Molecule Bioanalytical Testing Services Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing

clinical-trial applications of biologics & biomarkers

Increasing

clinical-trial applications of biologics & biomarkers

| +2.8% | Global, early gains in North America and Europe | Medium term (2-4 years) |

(~) %

Impact on CAGR Forecast

:

+2.8%

|

Geographic

Relevance

:

Global, early

gains in North America and Europe

|

Impact

Timeline

:

Medium term

(2-4 years)

|

Rising

R&D expenditure by biopharma companies

Rising

R&D expenditure by biopharma companies

| +2.1% | Global, concentrated in US, China, EU core markets | Long term (≥ 4 years) | |||

Heightened

regulatory expectations for immunogenicity testing

Heightened

regulatory expectations for immunogenicity testing

| +1.9% | Global, spill-over from FDA/EMA to Asia Pacific | Short term (≤ 2 years) | |||

Growing

outsourcing trend to specialized CROs & CDMOs

Growing

outsourcing trend to specialized CROs & CDMOs

| +1.7% | Global, accelerated adoption in Asia Pacific | Medium term (2-4 years) | |||

Adoption of

hybrid LBA/LC-MS platforms for multiplex assays

Adoption of

hybrid LBA/LC-MS platforms for multiplex assays

| +1.4% | North America & EU, expanding to Asia Pacific | Medium term (2-4 years) | |||

Expansion of

cell & gene-therapy pipelines needing novel viral-vector assays

Expansion of

cell & gene-therapy pipelines needing novel viral-vector assays

| +1.2% | North America core, early expansion to Singapore & UK | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing Clinical-Trial Applications of Biologics & Biomarkers

More than 700 active adeno-associated virus programs and a steady flow of bispecific antibody candidates have moved complex assays from niche to mainstream, reinforcing the centrality of the large molecule bioanalytical services market in global drug development.[1]Cell & Gene Therapy Insights, “Gene Therapy Clinical Landscape,” cellandgene.com Regulatory guidance now demands anti-drug-antibody and neutralizing-antibody data in labeling, obliging sponsors to integrate immunogenicity testing early. Service providers that support most FDA approvals, such as Labcorp, highlight how bioanalytics have become pivotal for submission success.[2]Labcorp, “2024 Regulatory Approvals Supported,” labcorp.com Wider use of disease-related biomarkers in oncology and metabolic studies is also elevating method-validation requirements. Collectively these forces expand both volume and sophistication of contracted analytical work within the large molecule bioanalytical services market.

Rising R&D Expenditure by Biopharma Companies

Capital inflows have lifted global biotechnology valuations and stretched internal laboratory capacity, prompting sponsors to externalize specialized assays. One-third of U.S. pharmaceutical R&D budgets already flow to external partners, and spend is skewing toward large molecule programs that rely on complex potency and PK analyses. The multitrillion-dollar expansion of the wider biotechnology sector underscores a long runway for outsourced analytics. Cell and gene therapy manufacturing qualification, in particular, demands extensive viral safety and impurity profiling that few drug makers maintain in-house. Robust spending therefore compounds long-term demand in the large molecule bioanalytical services market.

Heightened Regulatory Expectations for Immunogenicity Testing

Adoption of ICH M10 has harmonized method-validation norms, but operational burdens have risen. Agencies increasingly request neutralizing-antibody and cross-reactivity data for bispecifics and recombinant peptides, extending test panels beyond legacy ELISAs.[3]FDA, “Immunogenicity Guidance for Therapeutic Protein Products,” fda.gov Public dockets assessing immunogenicity risks underscore that standards will evolve further. Providers able to automate ligand-binding workflows and integrate LC-MS confirmation are positioned to capture a larger slice of the large molecule bioanalytical services market as sponsors seek turnkey compliance solutions.

Growing Outsourcing Trend to Specialized CROs & CDMOs

The outsourcing model has shifted from transactional cost savings to strategic capability acquisition. Roughly 60-65% of early-stage U.S. biotechs report difficulty locating adequately sized partners, opening space for mid-tier laboratories with flexible engagement terms. Asia Pacific capacity has grown quickly due to regulatory harmonization, illustrated by new CGMP cell-therapy analytics in Singapore. Broader adoption of distributed development strategies continues to enlarge the global footprint of the large molecule bioanalytical services market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Complex &

evolving GLP regulatory framework

Complex &

evolving GLP regulatory framework

| -1.8% | Global, highest impact in US and EU | Short term (≤ 2 years) |

(~) %

Impact on CAGR Forecast

:

-1.8%

|

Geographic

Relevance

:

Global,

highest impact in US and EU

|

Impact

Timeline

:

Short term (≤

2 years)

|

High capital

cost of advanced bioanalytical instruments

High capital

cost of advanced bioanalytical instruments

| -1.5% | Global, particularly burdensome for smaller CROs | Medium term (2-4 years) | |||

Shortage of

skilled large-molecule bioanalytical scientists

Shortage of

skilled large-molecule bioanalytical scientists

| -1.2% | North America & EU, emerging in Asia Pacific | Long term (≥ 4 years) | |||

Cyber-security

vulnerabilities in cloud-connected lab analyzers

Cyber-security

vulnerabilities in cloud-connected lab analyzers

| -0.9% | Global, with concentrated risk in digitally advanced labs | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Complex & Evolving GLP Regulatory Framework

New FDA guidance on data integrity for bioequivalence studies forces laboratories to upgrade electronic systems and audit trails, raising near-term compliance cost. Divergent regional interpretations of ICH M10 further compel providers to maintain variant SOPs, reducing operational efficiency. Smaller firms face disproportionate burdens that can delay capacity expansions in the large molecule bioanalytical services market.

Cyber-Security Vulnerabilities in Cloud-Connected Lab Analyzers

Default credentials in automated blood culture and chromatograph systems have scored critical CVSS ratings of 9.8, revealing how networked instruments can be exploited. Breaches risk raw data manipulation and threaten regulatory submissions. Consequently, sponsors scrutinize cyber-resilience when selecting partners, and providers must invest in zero-trust architectures, modestly tempering near-term profitability across the large molecule bioanalytical services market.

Segment Analysis

By Phase: Early-Stage Momentum Accelerates Growth

Clinical-phase projects retained 49.28% of the large molecule bioanalytical services market share in 2025 as late-stage trials require repeated PK, immunogenicity, and biomarker sampling over multi-year timelines. This high volume anchors service provider revenue. Preclinical demand nonetheless expands at an 10.86% CAGR driven by IND-enabling packages for novel antibodies and gene therapies. The large molecule bioanalytical services market benefits as sponsors front-load detailed characterization to de-risk clinical phases. Advanced modeling tools that integrate non-clinical PK data with humanized mouse models are shortening transition times, stimulating further uptake. Real-time data review portals help align preclinical and clinical teams, enhancing study continuity and reinforcing outsourcing dependence.

Automation and AI-driven peak detection now deliver same-day results for toxicokinetic assays, a key differentiator for smaller biotech clients seeking rapid go/no-go decisions. Providers able to combine early-stage assay design with scalable clinical bioanalysis win multi-phase contracts, improving lifetime client value inside the large molecule bioanalytical services market.

Note: Segment shares of all individual segments available upon report purchase

By Molecule Type: Complexity Drives Diversification

Monoclonal antibodies delivered 43.35% of the large molecule bioanalytical services market size in 2025. Robust patent cliffs in oncology and immunology sustain heavy analytical workloads for both originators and biosimilar entrants. Meanwhile, cell therapy analytics post the highest 11.6% CAGR as allogeneic CAR-T programs and induced pluripotent stem-cell therapies enter multicenter trials, demanding flow cytometry-based cellular kinetics and vector potency quantification. Hybrid immunoaffinity LC-MS/MS workflows quantify intact antibody-drug conjugate species alongside free drug payload, illustrating how platform innovation answers the structural diversity of next-generation biologics.

Bispecific antibodies require epitope-specific bridging ELISAs and orthogonal mass-spectrometry confirmation, extending assay development cycles yet generating premium revenue per study. Fusion proteins, peptide hormones, and vaccines maintain stable contributions. Rare-enzyme replacement therapies necessitate sub-nanogram sensitivity, spurring investments in ultra-high-resolution MS that further segment the large molecule bioanalytical services market.

By Service: Pharmacokinetics Anchors Revenue Streams

Pharmacokinetics remained the dominant service line with 29.21% of 2025 billings across the large molecule bioanalytical services market. Complex biologics now demand tissue distribution, neonate exposure, and receptor occupancy analyses, widening scope beyond classic serum concentration curves. Bioequivalence testing is projected to grow at the fastest double-digit pace on account of a surging biosimilar pipeline and the global shift toward interchangeability. Multiparametric ADME studies integrating permeability, catabolism, and excretion endpoints re-enter focus as regulatory agencies question accumulation risks of high-molecular-weight constructs. Immunogenicity testing differentiates providers because anti-drug-antibody assays need context-specific sensitivity and drug-tolerance thresholds. Biomarker programs linked to companion diagnostics multiply sample numbers per subject and solidify recurring revenue within the large molecule bioanalytical services industry.

Stability testing adapts to advanced modalities. Cryogenic chain-of-custody verification for cell therapy drug products and accelerated vector aggregation assays call for specialized chambers and orthogonal release testing. Providers that align these offerings within unified quality systems secure cross-functional contracts and elevate switching barriers.

Note: Segment shares of all individual segments available upon report purchase

By Therapeutic Area: Oncology Still Leads, Rare Diseases Surge

Oncology captured 34.45% of 2025 turnover in the large molecule bioanalytical services market owing to immuno-oncology trial intensity and the biomarker-heavy nature of checkpoint inhibitor studies. Every treatment cycle generates multiplex cytokine, T-cell activation, and soluble receptor assays that underpin dosing decisions. Gene-editing approaches for hemato-oncologic indications add viral-vector characterization layers, extending analytical packages. Rare diseases, however, post the fastest 13.1% CAGR as accelerated approval incentives and premium pricing justify investments in ultralow-volume, high-sensitivity assays. Genetically inherited metabolic disorders moving into gene therapy trials contribute sustained sample volumes despite small patient populations.

Infectious-disease programs pivot from prophylactic vaccines toward antibody therapeutics requiring neutralization titers and Fc-effector-function assays. Cardiovascular gene-delivery platforms targeting inherited cardiomyopathies demand cardiac-specific troponin and vector biodistribution profiling. Neurology projects ascribe growing budgets to blood–brain barrier penetration analytics, necessitating microdialysis and intracerebral sampling competence, broadening the remit of the large molecule bioanalytical services market.

By End User: SMEs Propel Incremental Demand

Large pharmaceutical companies commanded 57.12% of 2025 spend as portfolio breadth obliges constant assay execution and global regulatory support. Yet small and mid-size enterprises drive incremental growth at a 9.95% CAGR through 2031. Virtual biotechs often outsource 100% of laboratory functions, preferring full-service partners that couple method development with regulatory dossier preparation.

Academic translational centers and government agencies also expand contracting activity under pandemic-preparedness and rare-disease funding streams. Venture-capital backing levels fluctuate, creating cyclical demand; service providers that offer milestone-based pricing and risk-share terms mitigate sponsor budget uncertainty, maintaining utilization across the large molecule bioanalytical services market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America accounted for 35.40% of 2025 revenue aided by a mature regulatory environment, established GLP laboratories, and sustained venture funding. The United States hosts most IND and BLA submissions, producing consistent sample flows. Ongoing capacity expansion, including new large-animal testing suites and vector analytics labs, ensures regional ability to manage complex modality growth. The large molecule bioanalytical services market size for North America is projected to keep pace with global averages as domestic biosimilar activity amplifies comparative testing needs.

Asia Pacific is the fastest-growing geography, advancing at a 12.05% CAGR to 2031. Chinese biomanufacturing parks, Japanese regenerative-medicine hubs, and Singapore’s CGMP cell-therapy banks jointly attract multinational trials. Regional regulatory convergence, exemplified by TGA and HSA alignment with ICH M10, reduces duplicative validation work and enables global data acceptance. Local CROs benefit from cost competitiveness and government incentives but must elevate data-integrity and cyber-security standards to win late-phase studies within the large molecule bioanalytical services market.

Europe offers steady growth anchored in biosimilar expertise and strong pharmacovigilance frameworks. The European Medicines Agency’s emphasis on comparability drives sustained bioequivalence testing demand. Investments in next-generation sequencing for viral safety and in silico immunogenicity risk evaluation are positioning EU labs to capture advanced modality work. CEE countries provide cost-effective sample-analysis centers, expanding the continent’s internal supply chain.

Other regions reveal nascent opportunities. India pursues regulatory-system upgrades to attract Western sponsors. The Middle East leverages health-care infrastructure spending to seed specialty labs. Africa’s engagement remains limited to sporadic vaccine and infectious-disease programs but signals long-term potential as clinical-trial diversity initiatives spread across the large molecule bioanalytical services market.

Competitive Landscape

Market Concentration

Market concentration is moderate. Integrated providers such as Labcorp Drug Development, Charles River Laboratories, and IQVIA combine global footprints with deep regulatory insight, providing cradle-to-commercial services that appeal to large biopharma clients. Mid-tier specialists like BioAgilytix and Eurofins carve out niches in ultra-sensitive immunogenicity and cell-based potency assays, leveraging scientific depth to offset smaller scale. Technology-forward entrants promote cloud-native laboratory-information systems and AI-driven peak detection to differentiate on turnaround time and analytical granularity. Investments in hybrid LBA/LC-MS workflows anchor many recent capital projects as providers target high-margin complex biologics.

Consolidation accelerates as firms seek broader modality coverage and geographic reach. Thermo Fisher Scientific has publicly signaled USD 40-50 billion for strategic acquisitions, illustrating the high premium placed on analytical capacity. Agilent’s USD 925 million purchase of BIOVECTRA expands bioprocessing analytics while Labcorp’s oncology and pathology acquisitions widen its precision-medicine network. Integration success hinges on harmonizing quality systems and cybersecurity protocols, fields where larger players hold an advantage.

Technological arms races focus on automation, digital continuity, and cyber-resilience. Providers now deploy machine-learning-based drift detection to flag assay deviations in real time, minimizing reruns and audit findings. However, wider connectivity exposes critical instruments to cyber threats; companies with zero-trust architectures and dedicated security operations centers are increasingly favored by sponsors concerned with data integrity. Geopolitical considerations also influence outsourcing strategies as potential biosecurity legislation encourages U.S. federal projects to favor domestic laboratories, shaping demand distribution across the large molecule bioanalytical services market.

Large Molecule Bioanalytical Testing Services Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Charles River Laboratories announced an agreement with Singapore General Hospital to provide CGMP-compliant master cell banking and next-generation sequencing services for cord blood-derived allogeneic CAR-T cells aimed at cancer therapy

- March 2025: Labcorp revealed acquisitions of BioReference Health’s oncology and clinical testing assets along with Incyte Diagnostics’ pathology operations, expanding precision-medicine capabilities and U.S. regional presence.

- May 2024: Precision for Medicine, a global biomarker-driven clinical research and development supporting life sciences company, reported the expansion of its laboratory campus in Frederick, Maryland. This state-of-the-art facility serves as a center of excellence for Precision for Medicine’s gene therapy companion diagnostic manufacturing, advanced immunological monitoring research, and large molecule bioanalytical testing services.

- April 2024: Smithers, a leading provider of bioanalytical testing, reported the launch of its Generic Pharmacokinetic (PK) Assay. The assay measures the drug concentration of human or humanized mAb kappa IgG molecules with ECL detection.

Table of Contents for Large Molecule Bioanalytical Testing Services Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increasing Clinical-Trial Applications of Biologics & Biomarkers

- 4.2.2Rising R&D Expenditure by Biopharma Companies

- 4.2.3Heightened Regulatory Expectations for Immunogenicity Testing

- 4.2.4Growing Outsourcing Trend to Specialized CROs & CDMOs

- 4.2.5Adoption of Hybrid LBA/LC-MS Platforms for Multiplex Assays

- 4.2.6Expansion of Cell & Gene-Therapy Pipelines Needing Novel Viral-Vector Assays

- 4.3Market Restraints

- 4.3.1Complex & Evolving GLP Regulatory Framework

- 4.3.2High Capital Cost of Advanced Bioanalytical Instruments

- 4.3.3Shortage of Skilled Large-Molecule Bioanalytical Scientists

- 4.3.4Cyber-Security Vulnerabilities in Cloud-Connected Lab Analyzers

- 4.4Porter’s Five Forces Analysis

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers/Consumers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitute Products

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value in USD)

- 5.1By Phase

- 5.1.1Preclinical

- 5.1.1.1With Antibody

- 5.1.1.2Without Antibody

- 5.1.2Clinical

- 5.1.2.1Phase I

- 5.1.2.2Phase II

- 5.1.2.3Phase III

- 5.1.2.4Phase IV (Post-marketing)

- 5.2By Molecule Type

- 5.2.1Monoclonal Antibodies

- 5.2.2Bispecific Antibodies

- 5.2.3Antibody-Drug Conjugates

- 5.2.4Fusion Proteins

- 5.2.5Peptides & Hormones

- 5.2.6Vaccines (Protein / Polysaccharide)

- 5.2.7Recombinant Proteins & Enzymes

- 5.2.8Cell Therapy Products

- 5.3By Service

- 5.3.1Absorption, Distribution, Metabolism & Excretion (ADME)

- 5.3.2Pharmacokinetics

- 5.3.3Pharmacodynamics

- 5.3.4Bioavailability

- 5.3.5Bioequivalence

- 5.3.6Immunogenicity (ADA)

- 5.3.7Biomarker Testing

- 5.3.8Stability Testing

- 5.3.9Other Tests

- 5.4By Therapeutic Area

- 5.4.1Oncology

- 5.4.2Infectious Diseases

- 5.4.3Cardiology

- 5.4.4Neurology

- 5.4.5Immunology

- 5.4.6Endocrinology & Metabolic Disorders

- 5.4.7Hematology

- 5.4.8Rare Diseases

- 5.4.9Other Therapeutic Areas

- 5.5By End User

- 5.5.1Small & Medium Enterprises (SMEs)

- 5.5.2Large Firms

- 5.5.3Academic & Research Institutes

- 5.5.4Government / Non-profit Organizations

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4Australia

- 5.6.3.5South Korea

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East & Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East & Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Labcorp Drug Development

- 6.3.2Pacific BioLabs Inc.

- 6.3.3NorthEast BioAnalytical Laboratories LLC

- 6.3.4BioAgilytix Labs

- 6.3.5SGS SA

- 6.3.6ICON plc

- 6.3.7Smithers

- 6.3.8Syneos Health

- 6.3.9PPD Inc.

- 6.3.10IQVIA Inc.

- 6.3.11Thermo Fisher Scientific Inc.

- 6.3.12Charles River Laboratories International Inc.

- 6.3.13Eurofins BioPharma Product Testing

- 6.3.14WuXi AppTec

- 6.3.15Frontage Laboratories

- 6.3.16KBI Biopharma

- 6.3.17AGC Biologics

- 6.3.18Parexel International

- 6.3.19Medpace Holdings

- 6.3.20LGC Group (Biosearch Technologies)

- 6.3.21Selvita

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Large Molecule Bioanalytical Testing Services Market Report Scope

As per the scope of the report, bioanalysis of large molecules such as proteins or specific biotherapeutics refers to a set of methods and procedures that allow scientists to analyze particular proteins found in living organisms and the biochemical reactions underlying life processes. The large molecule bioanalytical testing services market is segmented by phase, services, therapeutic area, end user, and geography. By phase, the market is segmented into preclinical (with antibody, without antibody) and clinical. By services, the market is segmented into absorption, distribution, metabolism, and excretion (ADME), pharmacokinetics, pharmacodynamics, bioavailability, bioequivalence, and other tests. By therapeutic area, the market is segmented into oncology, infectious diseases, cardiology, neurology, and other therapeutic areas. By end user, the market is segmented into small and medium enterprises (SMEs) and large firms. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (USD) for the above segments.