Biological Safety Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

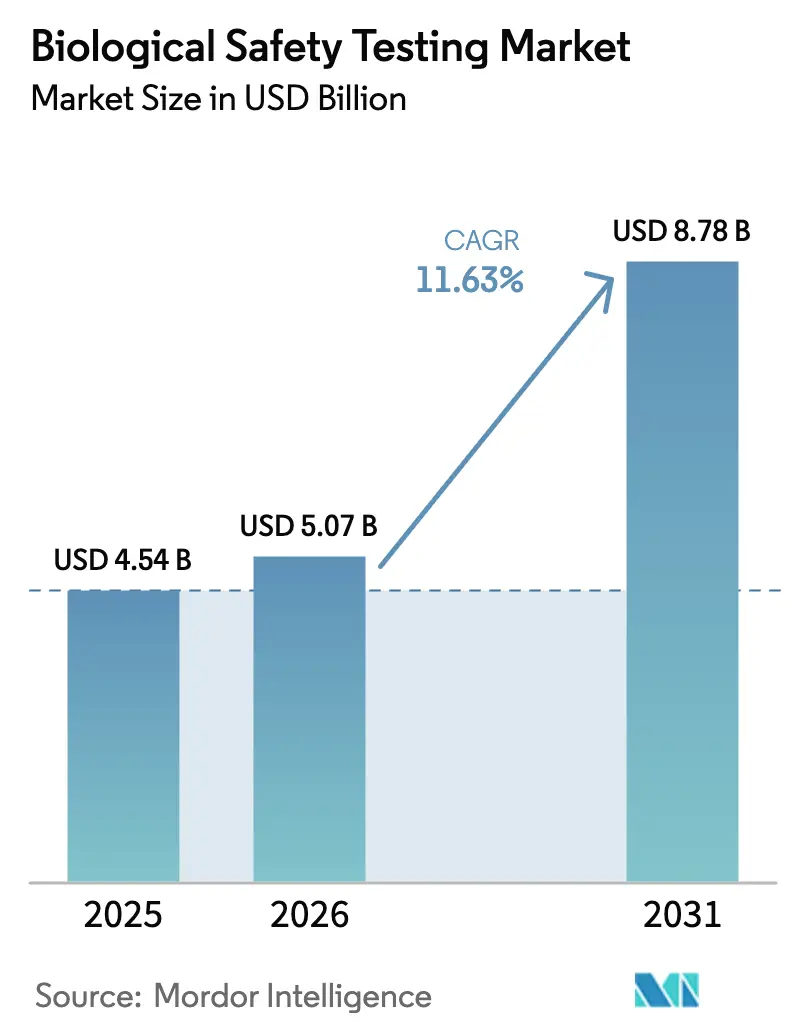

| Market Size (2026) | USD 5.07 Billion |

| Market Size (2031) | USD 8.78 Billion |

| Growth Rate (2026 - 2031) | 11.63% CAGR |

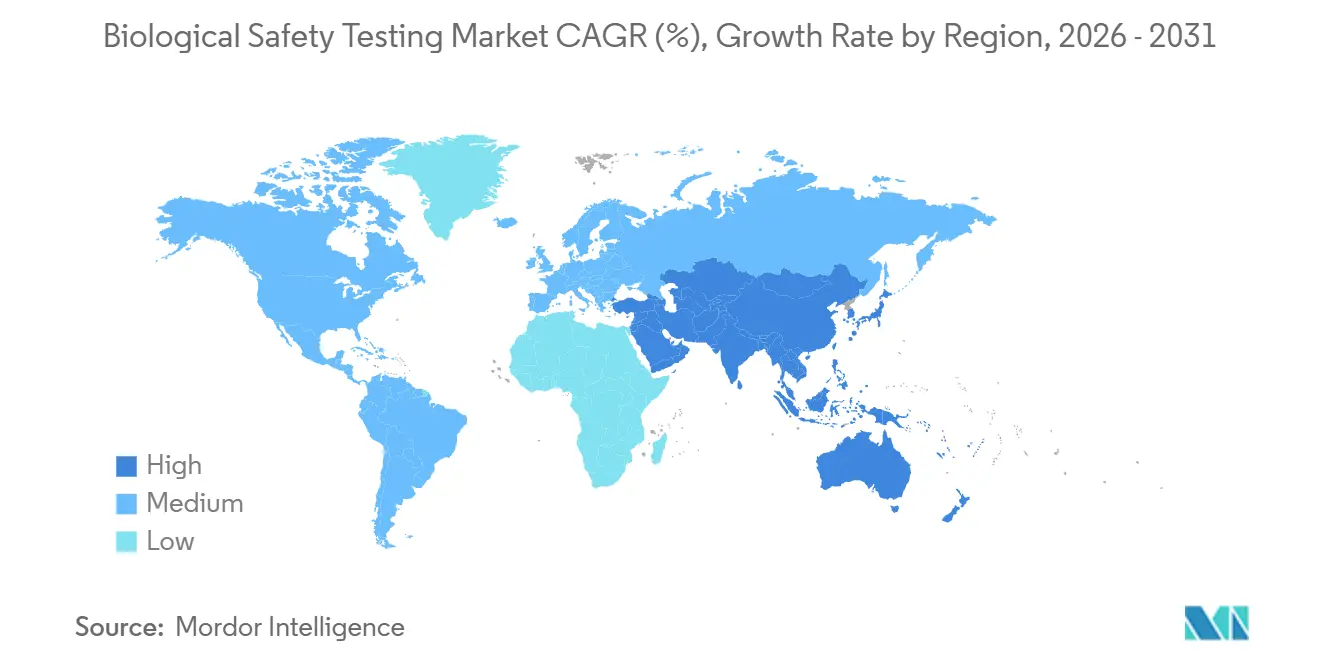

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biological Safety Testing Market Analysis by Mordor Intelligence

The biological safety testing market size is expected to grow from USD 4.54 billion in 2025 to USD 5.07 billion in 2026 and is forecast to reach USD 8.78 billion by 2031 at 11.63% CAGR over 2026-2031. This growth is driven by increased venture funding in cell and gene therapy pipelines, stricter global contamination-control regulations, and the rising trend of outsourcing to contract development and manufacturing organizations (CDMOs). CDMOs now account for a significant share of spending as sponsors reallocate resources toward clinical trials. Additionally, the adoption of rapid-method validation is becoming a key differentiator, enabling faster time-to-market upon regulatory approval. Sterility tests remain the highest revenue-generating segment due to their universal application to injectables. However, adventitious virus detection is gaining traction, particularly as gene-therapy developers address the risks associated with replication-competent lentivirus. The competitive landscape is intensifying, with major laboratories acquiring regional players to streamline quality agreements across release sites in North America, Europe, and the Asia-Pacific. Despite these advancements, the market faces two critical challenges: the volatile supply of Limulus Amebocyte Lysate and the slow regulatory acceptance of rapid sterility methods. These factors are expected to influence cost structures and vendor strategies over the next four years.

Key Report Takeaways

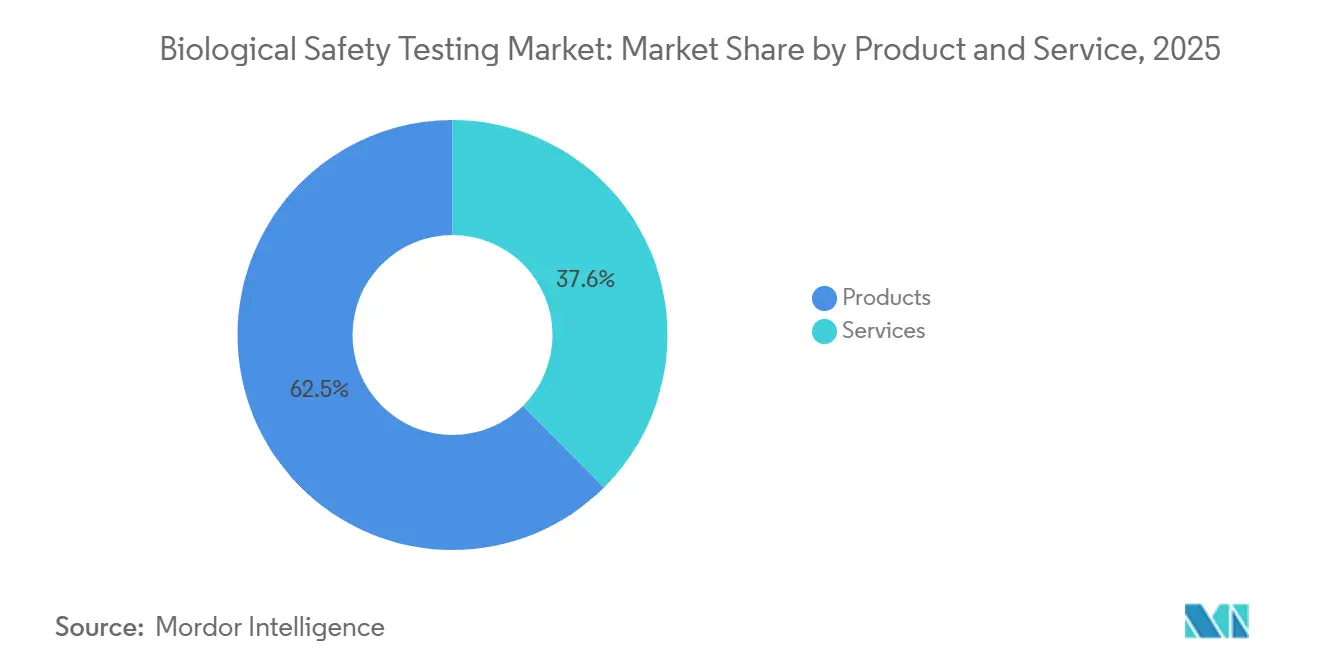

- By product & service, reagent kits, culture media, and detection instruments held a 62.45% revenue share of the biological safety testing market in 2025, whereas services are expected to expand at a 13.54% CAGR through 2031.

- By test type, sterility tests led with a 28.54% share of the biological safety testing market in 2025; adventitious virus detection is projected to advance at a 13.76% CAGR through 2031.

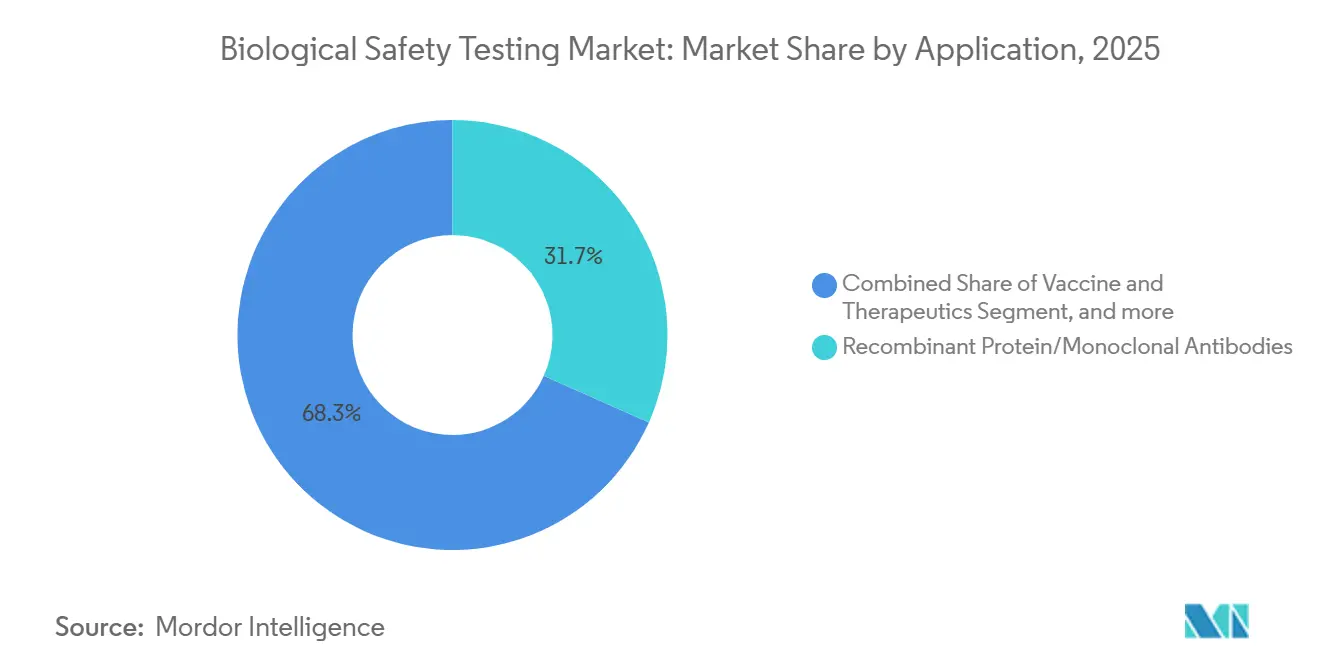

- By application, recombinant protein and monoclonal antibodies accounted for 31.67% share of the biological safety testing market size in 2025, while cellular and gene therapy is growing at a 14.88% CAGR through 2031.

- By end user, biopharma and biotech companies accounted for 47.54% of spending in 2025, whereas CDMOs are projected to record the highest CAGR of 14.67% from 2026 to 2031.

- By geography, North America led with a 41.67% revenue share in 2025, whereas the Asia-Pacific region is estimated to grow at a 12.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biological Safety Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Global Biopharma R&D and Venture Financing | +2.8% | North America and Europe core | Medium term (2-4 years) |

| Accelerated Commercialization of Cell & Gene Therapies | +3.2% | North America and Europe core, Asia-Pacific emerging | Long term (≥4 years) |

| Stringent Global Regulatory Standards for Contamination Control | +2.1% | Global | Short term (≤2 years) |

| Growing Outsourcing of Quality Control to Cost-Efficient CDMOs | +2.5% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Adoption of Digital Twins and Predictive Analytics for Batch Release | +1.3% | Early adopters in North America and Europe | Medium term (2-4 years) |

| Government Biodefense Stockpile Initiatives Boosting Validation Demand | +0.9% | United States and selected EU member states | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Expansion of Global Biopharma R&D and Venture Financing

Venture investors deployed USD 23 billion into biopharma in 2024, channeling 42% of capital toward immunology and gene-editing platforms that require extensive safety testing before investigational new drug filings[1]U.S. Securities and Exchange Commission, “Biopharma Venture Funding Data 2024,” sec.gov. European Medicines Agency data show a 19% increase in biologics submissions during the first half of 2025, with each submission requiring sterility, endotoxin, and mycoplasma panels. Series B-stage sponsors are locking in three-year master service agreements that hedge reagent inflation of 8-12% seen in 2024–2025, concentrating spend among the five largest global laboratories. Pfizer reported a 14% increase in outsourced quality-control spending in 2025, as its mRNA vaccine portfolio expanded, underscoring the trend's durability. These trends collectively raise baseline testing volumes and translate venture funding into predictable service revenues.

Accelerated Commercialization of Cell & Gene Therapies

The U.S. FDA approved eight cell and gene therapy products in 2024, bringing the cumulative number of authorizations to 37 since 2017. Each autologous launch multiplies safety-testing demand, as batches cannot be pooled. Novartis processed more than 12,000 sterility tests in 2024 for its CAR-T network, illustrating the one-patient-one-batch paradigm. The EMA guidance issued in 2025 doubled viral testing for lentiviral vectors by mandating both in vitro and in vivo assays, while Japan shortened sterility holds from 28 days to seven, spurring the uptake of rapid methods across the Asia-Pacific region. Bluebird Bio reduced its release cycle time by 30% after installing automated mycoplasma detection at its Seattle site, confirming that in-house rapid platforms can quickly pay back when throughput is high. Geographic clusters are now co-locating manufacturing and testing to keep autologous products within a 48-hour cold-chain window.

Stringent Global Regulatory Standards for Contamination Control

The U.S. FDA issued 14 warning letters for sterility assurance lapses in 2024, a 27% year-over-year increase that triggered remediation testing across affected sites. Revised guidance now links environmental monitoring results to batch-release data, expanding routine bioburden panels. China aligned its endotoxin limits with those of USP <85> in mid-2025, thereby increasing the retest frequency for injectables. Meanwhile, ISO 13485:2024 introduced traceability rules that widened the demand for extractables and leachables analysis. Europe introduced a rapid-method chapter in 2025, yet withheld full equivalence, prolonging dual-method validation requirements. Collectively, these mandates encourage sponsors to partner with laboratories that maintain current Good Manufacturing Practice (cGMP) accreditation and offer diversified assay menus.

Growing Outsourcing of Quality Control to Cost-Efficient CDMOs

CDMOs absorbed a significant share of end-user spend in 2025 as sponsors redirected internal budgets toward clinical pipelines. WuXi Biologics logged 22% revenue growth in integrated testing services during 2024, while Biocon Biologics secured EMA approval for its Bengaluru laboratory to act as a qualified-person site, allowing sterility results to travel with the product across borders. NMPA policies now let foreign sponsors use Chinese contract labs in investigational filings, diverting work from Singapore to Suzhou. Samsung Biologics operates three segregated QC suites to accommodate multiple clients, an investment that smaller CDMOs struggle to match. As labor costs climb in U.S. biotech hubs, outsourcing provides variable cost structures and bundled service efficiencies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged Validation Timelines for Novel Rapid Microbiology Methods | −1.4% | North America and Europe | Medium term (2-4 years) |

| Volatile Supply of Horseshoe Crab Lysate and Alternate Reagent Uncertainty | −1.1% | North America and Asia-Pacific | Short term (≤2 years) |

| Limited Skilled Workforce and Rising Training Expenditure | −0.8% | Global, acute in high-cost biotech hubs | Medium term (2-4 years) |

| Margin Compression From Vendor Consolidation in Testing Supply Chain | −0.6% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Prolonged Validation Timelines for Novel Rapid Microbiology Methods

Rapid sterility platforms promise three-day results versus the 14-day compendial benchmark; however, U.S. FDA guidance issued in 2024 requires side-by-side equivalence studies over at least 30 production batches, which pushes validation timelines to 18–24 months for low-volume biologics. Charles River Laboratories noted a sub-forecast adoption of its Celsis system due to this burden, and the European Pharmacopoeia’s 2025 framework grants full equivalence only to technologies detecting under 10 colony-forming units, a threshold that many ATP and cytometry platforms miss. Contract labs cannot amortize single-product validations across clients, choking mid-tier investment appetite. Consequently, fewer than 12% of Lonza’s biologics customers had migrated to rapid sterility testing by mid-2025. Widespread adoption is therefore unlikely before 2028, which will limit the benefits of cycle-time compression in the intermediate term.

Volatile Supply of Horseshoe Crab Lysate and Alternate Reagent Uncertainty

Atlantic horseshoe crab landings fell 31% between 2019 and 2024, driving Limulus Amebocyte Lysate (LAL) reagent prices up 18% in 2024 and delaying batch release by up to 10 days when stockouts occurred[2]Atlantic States Marine Fisheries Commission, “Horseshoe Crab Stock Assessment 2024,” asmfc.org. Recombinant Factor C (rFC) received provisional European approval in 2024; however, USP equivalence is pending, leaving North American sponsors in limbo. Eli Lilly qualified rFC for European facilities but still uses LAL in the United States, doubling QC complexity. Japan now permits rFC yet demands validation across 50 production lots, a hurdle similar to rapid-method challenges. Larger CDMOs, such as Fujifilm Diosynth, hedged their risk by signing multi-year LAL contracts. Still, virtual biotech firms remain exposed to spot-market volatility, creating cost unpredictability over the next two years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Outsourced Testing Gains Momentum

Services are rising at a 13.54% CAGR through 2031, even though products commanded 62.45% of the biological safety testing market in 2025. The high upfront price of automated microbiology platforms-often above USD 500,000 per unit-pushes early-stage sponsors toward variable-cost outsourcing. Suppliers of reagents are bundling LAL kits with rFC alternatives to mitigate lysate shortages, while single-use containers now require extractables- and leachables assays under ISO 13485:2024. Eurofins grew biopharma services revenue 16% year-over-year in 2024 as clients avoided 12- to 18-month in-house validation lead times.

Structural shifts favor services because CDMOs can amortize capital across multiple clients and offer faster turnaround times. Laboratories, such as Pacific BioLabs, have trimmed sterility cycles to 10 days by implementing staggered incubation, whereas product vendors face margin pressure due to competitive pricing per test. The services segment also captures value from new viral-safety requirements that many sponsors cannot support internally without BSL-2 or BSL-3 facilities. Consequently, outsourcing continues to gain momentum as complexity and regulatory expectations escalate.

By Test Type: Virus Detection Outpaces Legacy Panels

Sterility tests held 28.54% of revenue in 2025, but face commoditization as automated liquid handlers cut labor input. Adventitious virus detection is the fastest-growing segment, with a 13.76% CAGR, driven by concerns about replication-competent lentivirus in gene therapy. Endotoxin assays remain high-margin because reagent scarcity inflates prices, yet widespread rFC approval could trim costs by 20% within three years. Mycoplasma detection is pivoting to PCR-based kits that provide four-hour results and comply with European Pharmacopoeia chapter 2.6.7.

Segment dynamism hinges on regulatory incentives. Charles River saw viral-safety revenue increase by 21% in 2024, as more clients required both pre-clinical and commercial testing. Rapid technology adoption is uneven; BioMérieux launched a multiplex assay that detects eight Mycoplasma species in a single run, while USP <71> revisions forced sponsors to revalidate sterility filters, temporarily boosting demand for contract labs. The biological safety testing market size for adventitious virus panels is set to expand as allogeneic therapies push master-cell-bank testing upstream.

By Application: CGT Complexity Drives Premium Pricing

Cellular and gene therapy testing is projected to grow at a 14.88% CAGR through 2031, the fastest among applications, as each patient-specific batch requires a unique safety panel. Recombinant proteins and monoclonal antibodies still accounted for 31.67% of application revenue in 2025; however, biosimilar pathways allow for abbreviated testing, which could dampen growth. Vaccine programs remain volume drivers; Moderna executed more than 8,000 sterility and endotoxin tests in 2024 alone.

Price elasticity favors complex modalities. Lonza estimated that traceability and documentation add 22% to per-batch costs for autologous products. The vaccine segment is regionalizing, with India’s Serum Institute qualifying for WHO pre-approval after conducting 1,200 tests over 18 months. Blood products may face disruption from pathogen-reduction technology, which could reduce the frequency of future testing for adventitious agents. Overall, higher test intensity in gene and cell therapies will keep the biological safety testing market expanding at a rate above double digits, even as mature biologics plateau.

By End User: CDMOs Capture Outsourcing Wave

CDMOs are forecast to grow at a 14.67% CAGR through 2031, overtaking the 47.54% market share held by biopharma and biotech companies in 2025. Wage inflation of 12–14% for microbiologists in Boston and San Francisco clusters has made external testing more attractive to virtual biotech. Samsung Biologics reported that 68% of manufacturing clients bundled testing in 2025, up from 54% in 2023, highlighting the stickiness of integrated contracts.

Academic institutes continue to outsource because maintaining viral-safety suites exceeds grant budgets. NIH allocated USD 47 million to contract testing in 2024, while device makers require hybrid pharmaceutical and biocompatibility panels for combination products. CDMOs are bifurcating into full-service providers and specialized labs, but integrated service bundles command higher margins and reinforce customer lock-in across multi-year programs.

Geography Analysis

North America contributed a 41.67% revenue share in 2025, anchored by venture-backed biotech clusters and the FDA's enforcement of revised sterility rules that link environmental monitoring with batch release. Thermo Fisher completed a USD 150 million expansion in Rockville to add capacity for 2,000 in vivo viral assays, while Canada harmonized mycoplasma PCR requirements with USP <63>. Mexico’s Grupo PiSA gained FDA recognition as a foreign testing site, shortening batch-release timelines for U.S. sponsors.

Europe benefits from a centralized EMA pathway, concentrating the biological safety testing market share in Germany, Switzerland, and Ireland. Lonza’s EU labs operated at 87% utilization during the second half of 2024. Rapid-method interest is rising following the European Pharmacopoeia’s alternative methods chapter; however, the U.K.’s divergent viral-safety rules require dual testing for pan-European launches. France and Italy are scaling CAR-T testing through public-private partnerships, boosting regional capacity.

The Asia-Pacific region is expected to post the fastest growth at a 12.54% CAGR from 2026 to 2031, following the NMPA's alignment with ICH standards and rising CDMO investment. WuXi’s Shanghai lab secured EMA release-site status, and Japan reduced sterility holds to seven days, facilitating rapid method adoption. Samsung Biologics’ three QC suites in Incheon illustrate capital intensity that smaller regional CDMOs cannot match. India’s Biocon won EMA approval for its Bengaluru lab, while Australia reduced the review time for investigational testing to 30 days, attracting early-phase sponsors.

Emerging regions, such as South America and the Middle East, are adding capacity to meet WHO prequalification standards. Brazil now mandates Mycoplasma PCR for cell-culture products, and the UAE is building a USD 25 million testing center in Dubai Science Park. South Africa partnered with SGS to reduce sample shipping delays, signaling a greater level of regional self-sufficiency.

Competitive Landscape

The top five providers—Charles River Laboratories, Eurofins Scientific, SGS, Thermo Fisher Scientific, and Lonza—held an estimated 38–42% share of the biological safety testing market revenue in 2025. Consolidation is intensifying as networks acquire regional labs to streamline multi-region quality agreements, while investment focuses on automated microbiology to defend margins against rising wages. Sartorius aims to capture on-site testing demand from gene-therapy developers through portable rapid-detection systems, and technology leadership in rapid sterility validation is a key differentiator.

Lonza’s patent filing for a closed-system rapid-sterility cartridge encapsulates the race to compress cycle time. Danaher’s acquisition of Abcam created a vertically integrated reagent and instrument supplier able to bundle pricing for large CDMOs, pressuring independent labs. Smaller players compete through niche capabilities, such as Pacific BioLabs’ dedicated viral-safety suites, which reduce the risk of cross-contamination. Regulatory frameworks are enabling hybrid strategies as FDA guidance now allows risk-based rapid methods for low-risk products without full validation, benefiting labs with diversified portfolios.

On balance, market concentration remains moderate but is trending upward as global players leverage scale for price negotiations and technology investment. Laboratories that validate rapid methods first are well-positioned to win high-throughput gene-therapy accounts, capturing a disproportionate share of growth as the biological safety testing market matures.

Biological Safety Testing Industry Leaders

Eurofins Scientific

Merck KGaA

Promega Corporation

Thermo Fisher Scientific

Lonza Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Nelson Laboratories, LLC, a unit of Sotera Health launched RapidCert, a rapid biological indicator sterility testing service. This innovative method combines traditional BIs with rapid microbiological techniques. It can confirm sterility for medical and pharmaceutical products in just three days.

- May 2025: Thermo Fisher Scientific announced the launch of the Thermo Scientific 1500 Series Class II, Type A2 Biological Safety Cabinet (BSC). This new cabinet is engineered to enhance protection, ergonomics, and operational ease for laboratory users. It aims to support various labs across academic, pharmaceutical, and biotech sectors.

- April 2024: Merck announced the launch of the Aptegra CHO genetic stability assay, the first of its kind to be fully validated as an all-in-one solution. This innovative assay uses whole-genome sequencing and bioinformatics to enhance biosafety testing. It aims to accelerate clients' progress into commercial bioproduction.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the biological safety testing market as the value generated by reagents, kits, instruments, and outsourced laboratory services applied to sterility, mycoplasma, bioburden, endotoxin, adventitious-agent, and residual host contaminant assays that certify biopharmaceuticals, vaccines, and advanced therapies as contamination-free before batch release. Scope touches every regulated stage from cell-bank establishment to commercial fill-finish while tracking revenues earned by in-house quality groups and external contract testing organizations.

Scope Exclusion: Routine environmental monitoring devices and biosafety cabinets fall outside this study.

Segmentation Overview

- By Product & Service

- Products

- Reagents & Kits

- Instruments

- Single-Use Consumables

- Services

- Sterility Testing Services

- Endotoxin & Pyrogen Testing Services

- Cell Line Authentication & Characterisation

- Products

- By Test Type

- Sterility Tests

- Bioburden Tests

- Endotoxin/LAL Tests

- Mycoplasma Detection

- Adventitious Virus Detection

- By Application

- Recombinant Protein / Monoclonal Antibodies

- Vaccine And Therapeutics

- Cellular And Gene Therapy

- Blood And Blood-Based Therapy

- Other Application

- By End User

- Biopharma & Biotech Companies

- Contract Development & Manufacturing Organisations

- Academic & Research Institutes

- Medical Device Manufacturers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest Of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest Of Asia-Pacific

- Middle East And Africa

- GCC

- South Africa

- Rest Of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest Of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with quality-assurance managers at large pharmas, CDMO commercial directors, and regulatory assessors across North America, Europe, and Asia helped us validate typical test volumes, outsourcing ratios, pricing corridors, and adoption of rapid-microbiological methods, filling gaps left by desk work.

Desk Research

Our analysts began with publicly available regulatory dossiers such as FDA's BLA approvals database, EMA's EudraGMDP listings, and WHO TRS annexes, which detail mandatory assay panels, thereby anchoring the universe of tests. We next sampled import-export codes for sterility test kits from UN Comtrade, cross-checked the bill-of-materials pricing trends on US ITC DataWeb, and reviewed industry association white papers from BioProcess International and PDA that quantify average quality-control spend per liter of biologic bulk. Paid repositories, D&B Hoovers for company financial splits, Questel for biosafety-related patent activity, and Dow Jones Factiva for contract award news, supplemented share and growth signals. These sources are illustrative; many other dependable publications and datasets were consulted for triangulation.

Market-Sizing & Forecasting

We first applied a top-down "biologic production volume × mandatory test intensity × average selling price" construct, rebuilt for five regions using batch filings and IND pipeline counts, then calibrated results with selective bottom-up vendor revenue roll-ups and channel checks. Key variables tracked included: 1) marketed biologic stock-keeping units, 2) new cell and gene therapy trials, 3) median assays per batch, 4) outsourcing penetration, and 5) assay ASP drift linked to rapid-method uptake. Multivariate regression, informed by expert consensus, projected each driver through 2030 and produced a defensible CAGR, while scenario analysis flagged upside demand from pandemic-preparedness funding. Data gaps in vendor splits were bridged by applying validated ASP benchmarks to disclosed sample volumes.

Data Validation & Update Cycle

Outputs pass a two-layer analyst review, variance tests against historical quality-control ratios, and anomaly checks versus quarterly earnings calls. Reports refresh yearly, with interim revisions triggered by material facility expansions, regulatory rewrites, or novel therapy approvals.

Why Mordor's Biological Safety Testing Baseline Commands Reliability

Published estimates often diverge because firms mix services with adjacent lab supplies, choose different base years, or refresh at uneven intervals.

Key gap drivers include narrower geographic cut-offs, omission of in-house testing revenue, one-time COVID windfalls embedded in some models, and currency conversion held constant by others despite recent dollar swings. Mordor's disciplined scope, annual refresh, and dual-approach modeling limit such distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.54 B (2025) | Mordor Intelligence | |

| USD 5.51 B (2025) | Global Consultancy A | Includes PPE consumables and viral clearance services beyond mandated assays |

| USD 5.38 B (2025) | Regional Consultancy B | Uses supplier revenue booked in 2024 converted at constant 2022 FX rates |

| USD 4.20 B (2024) | Trade Journal C | Excludes captive in-house testing and applies conservative ASP decline assumption |

In sum, our balanced, transparently sourced baseline gives decision-makers a dependable starting point, one that is repeatedly stress-tested against real production data and expert judgment so surprises stay minimal while confidence stays high.

Key Questions Answered in the Report

How large is the biological safety testing market in 2026?

The biological safety testing market size stands at USD 5.07 billion in 2026.

What CAGR is expected for biological safety testing through 2031?

The market is forecast to expand at an 11.63% CAGR between 2026 and 2031.

Which test type is growing the fastest?

Adventitious virus detection is the fastest-growing test type, projected at a 13.76% CAGR to 2031.

Why are CDMOs gaining market share in testing services?

Sponsors outsource quality control to reduce capital outlay and leverage bundled manufacturing-testing contracts offered by CDMOs, which are growing at a 14.67% CAGR.

Which region will experience the quickest growth?

Asia-Pacific is projected to rise at a 12.54% CAGR as China, Japan, and India harmonize regulations and expand testing infrastructure.

What supply risk could disrupt endotoxin testing?

Potential shortages of horseshoe crab lysate may elevate costs and delay batch release until recombinant Factor C gains full regulatory equivalence.

Page last updated on: