Bioengineered Protein Drugs Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

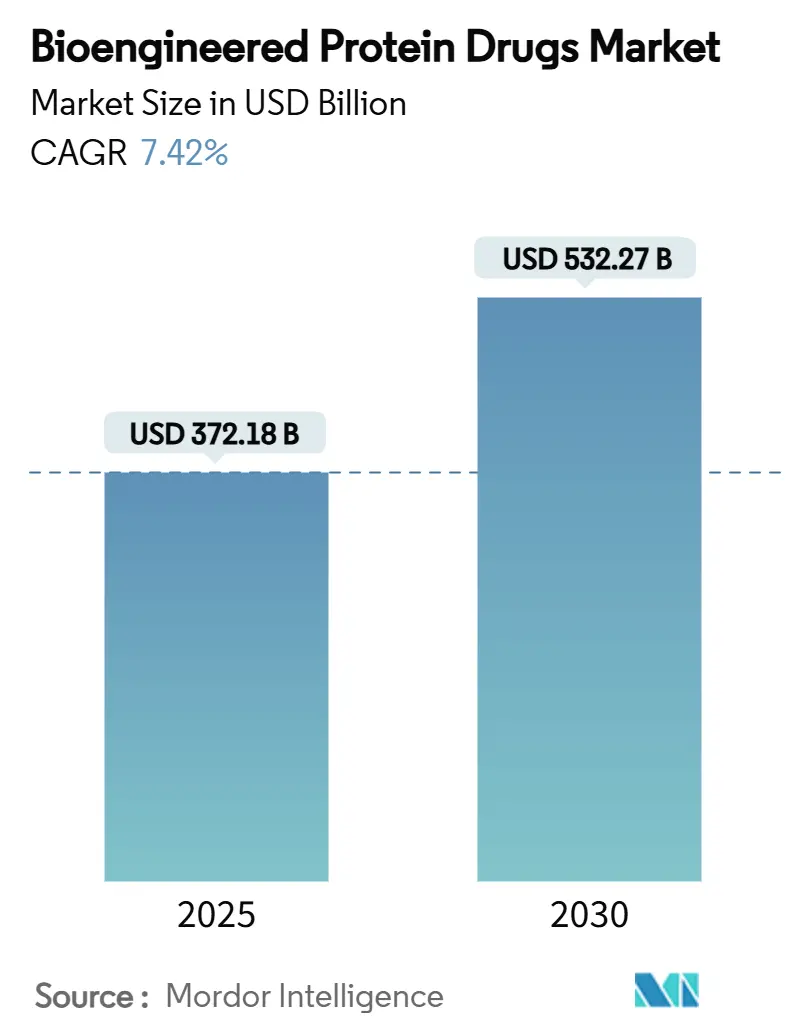

| Market Size (2025) | USD 372.18 Billion |

| Market Size (2030) | USD 532.27 Billion |

| Growth Rate (2025 - 2030) | 7.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioengineered Protein Drugs Market Analysis by Mordor Intelligence

The bioengineered protein drugs market size stood at USD 372.18 billion in 2025 and is forecast to reach USD 532.27 billion by 2030, advancing at a 7.42% CAGR. Expansion reflects the sector’s transition from first-generation recombinant therapies to AI-designed biologics that lower development costs and streamline scale-up. Demand rises as chronic diseases, notably cancer and diabetes, reshape care pathways and as patent expiries unlock biosimilar entry, intensifying competition. Investment in plant and cell-free expression systems, alongside distributed biomanufacturing, further improves economics. Regulators in the United States, Europe, and Asia continue to speed biosimilar approvals, reinforcing price competition while encouraging differentiated formulations. Manufacturers now prioritize ultra-long-acting drugs and home-based delivery models that align with patient convenience and payer cost-control mandates. These forces collectively bolster the bioengineered protein drugs market, even as cost and talent pressures persist.

Key Report Takeaways

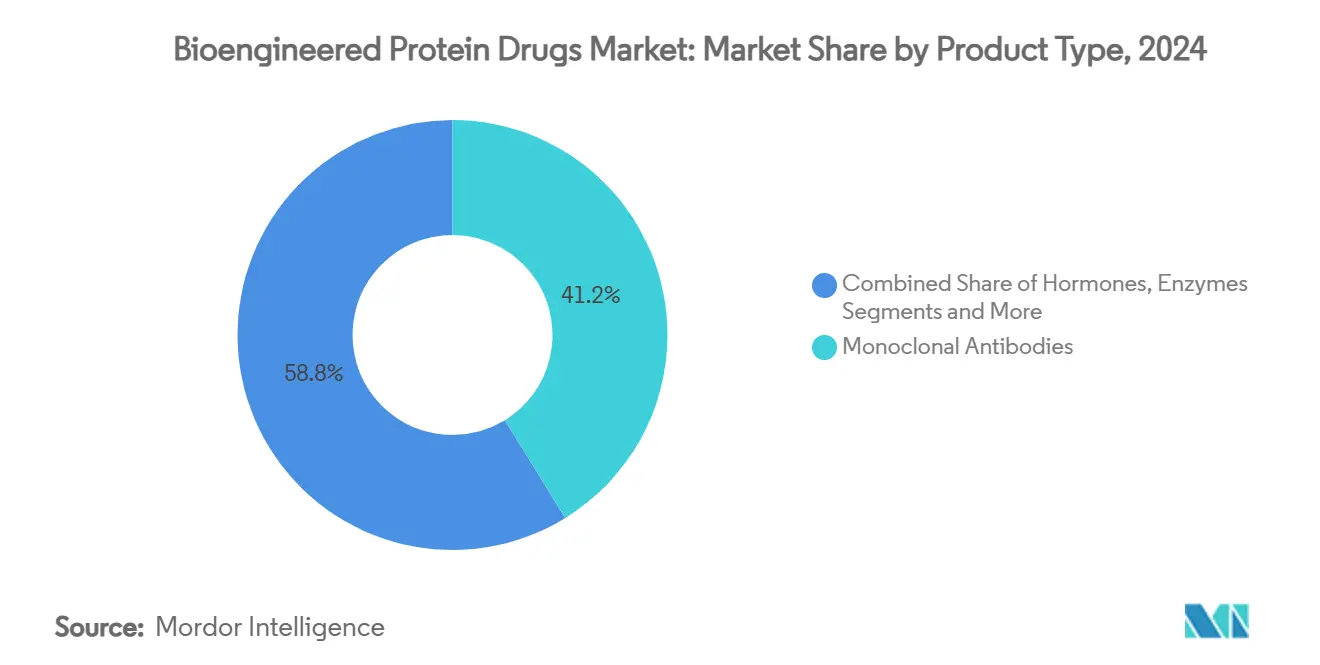

- By product type, monoclonal antibodies held 41.22% of the bioengineered protein drugs market share in 2024. Hormones, including insulin and GLP-1 agonists, are projected to expand at a 10.59% CAGR through 2030.

- By expression system, mammalian cell culture commanded 72.37% share of the bioengineered protein drugs market size in 2024. Plant-based systems are forecast to grow at an 11.34% CAGR to 2030.

- By disease indication, oncology applications captured 34.63% share of the bioengineered protein drugs market in 2024. Diabetes and metabolic disorders are advancing at a 9.47% CAGR through 2030.

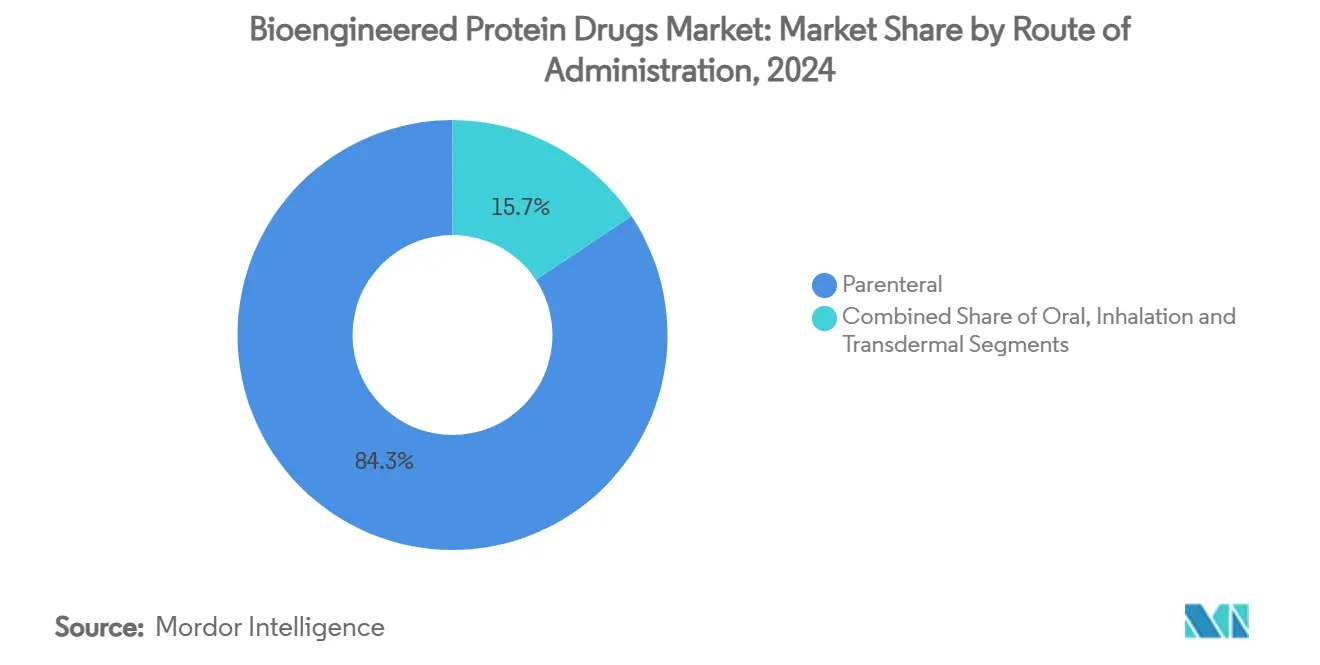

- By route of administration, parenteral formulations held 84.33% market share in 2024. Oral delivery innovations are rising at a 10.06% CAGR to 2030.

- By end user, hospitals accounted for 56.31% share of the bioengineered protein drugs market size in 2024. Homecare settings are growing at an 11.53% CAGR through 2030.

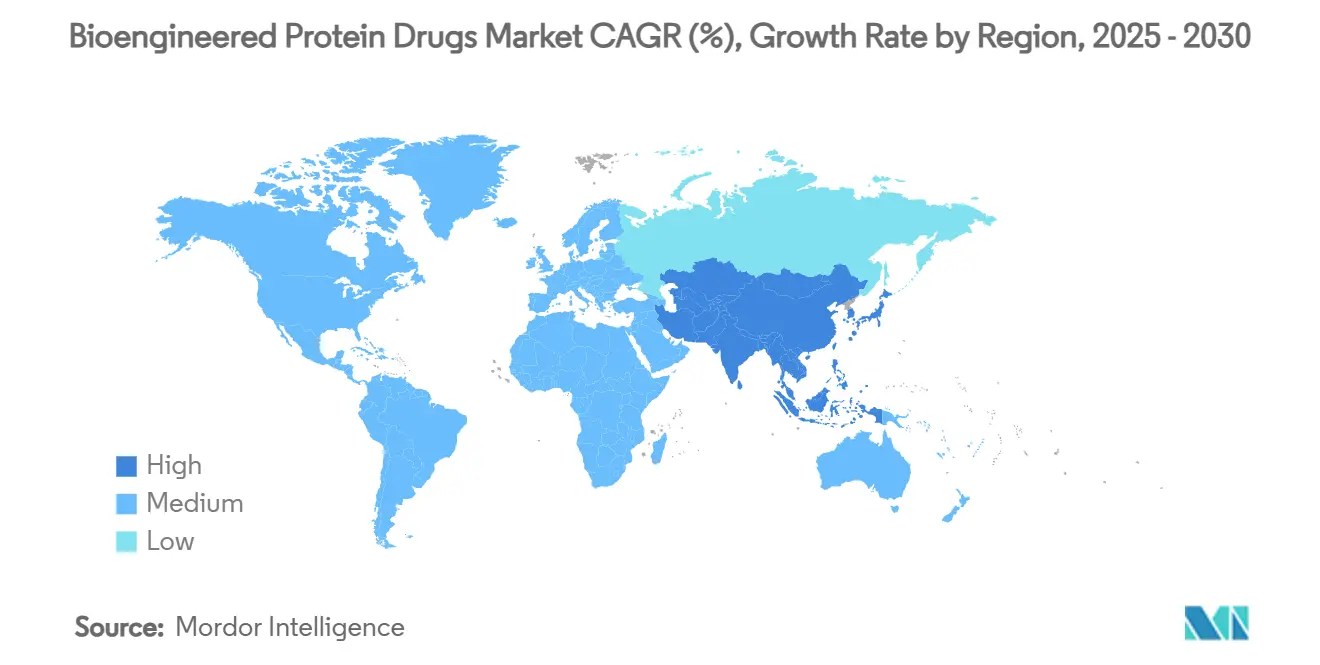

- North America held 44.29% regional share of the bioengineered protein drugs market in 2024. Asia-Pacific is expanding at a 9.88% CAGR, the fastest among all regions.

Global Bioengineered Protein Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases | +1.8% | Global, with concentration in aging populations of North America & Europe | Long term (≥ 4 years) |

| Advancements in protein-engineering & AI | +1.2% | North America & Europe leading, APAC adoption accelerating | Medium term (2-4 years) |

| Patent cliff of blockbuster biologics | +1.1% | Global, with regulatory advantages in US & EU | Short term (≤ 2 years) |

| Surge in global biomanufacturing capacity | +0.9% | APAC core manufacturing, spill-over to MEA | Medium term (2-4 years) |

| Shift to ultra-long-acting formulations | +0.7% | North America & EU early adoption, global expansion | Medium term (2-4 years) |

| Cost-efficient plant & cell-free platforms | +0.6% | Global, innovation centers in North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases

Cancer incidence is projected to rise 47% by 2040 while diabetes is poised to affect more than 700 million adults by 2030. These trends underpin sustained demand for precision biologics that can delay disease progression and reduce hospital stays, favoring protein drugs over small molecules. The 2025 FDA nod for penpulimab-kcqx in rare nasopharyngeal carcinoma exemplifies how oncology indications generate premium-priced opportunities. Premium reimbursement, accelerated approvals, and the crossover between oncology and metabolic disorders, such as immuno-oncology links to obesity, jointly fuel the bioengineered protein drugs market.

Advancements in Protein-Engineering & AI-Guided Design

Artificial intelligence now predicts folding, stability, and immunogenicity, cutting development time by up to half. Durham University’s advance in metalation prediction, crucial for enzyme function, highlights AI’s early-stage impact. UCSF’s creation of an artificial protein that mimics natural movement demonstrates potential for next-generation biosensors.[1]Elaine Watson, “Biotech Uses Fermentation to Produce Milk Proteins Without Cows,” Phys.org, phys.orgThese breakthroughs level the playing field, enabling start-ups to compete with incumbents, thereby broadening the competitive field of the bioengineered protein drugs market.

Patent Cliff of Blockbuster Biologics Driving Biosimilars

More than USD 200 billion in reference biologic revenue is at risk through 2030. FDA clearance of Kirsty, the first interchangeable insulin aspart biosimilar, signals pharmacy-level substitution that could seize up to 80% of reference sales within three years. The 15-year milestone of the Biologics Price Competition and Innovation Act marks streamlined reviews and lower development costs for biosimilar makers.[2]Center for Drug Evaluation and Research, “Commemorating the 15th Anniversary of the Biologics Price Competition and Innovation Act,” FDA, fda.gov

Surge in Global Biomanufacturing Capacity & CDMO Uptake

Pharma companies increasingly outsource to contract development and manufacturing organizations to reduce capital outlay. Genentech’s USD 700 million North Carolina site underscores repatriation of capacity amid supply-chain shocks. Biogen’s USD 2 billion expansion illustrates demand for specialized antisense oligonucleotide lines. Asian hubs leverage lower costs and harmonizing regulations to win manufacturing mandates, accelerating growth in the bioengineered protein drugs market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production & purification costs | -1.4% | Global, higher impact in cost-sensitive emerging markets | Long term (≥ 4 years) |

| Intensifying pricing & reimbursement pressure | -1.1% | North America & Europe primary impact, spreading globally | Short term (≤ 2 years) |

| Filtration-material supply bottlenecks | -0.8% | Global manufacturing hubs, concentrated in APAC | Medium term (2-4 years) |

| Talent gap in bioprocess automation | -0.6% | North America & Europe shortages, APAC capacity building | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production & Purification Costs

Chromatography and viral clearance drive 60-80% of manufacturing outlays. Single-use setups reduce contamination risk yet raise per-unit expense by up to 20%, a burden for smaller batches. Mammalian culture requires costly media and expert oversight. While plant and cell-free platforms promise savings, they demand upfront investment and fresh regulatory validation, moderating near-term impact on the bioengineered protein drugs market.

Intensifying Pricing / Reimbursement Pressure

Medicare price negotiations set a precedent for reference-based pricing in other markets, tightening margins. European health-technology assessments request real-world evidence, lengthening access timelines. Consolidated payers impose formulary restrictions and value-based contracts that place revenue at risk, challenging both innovators and biosimilar entrants in the bioengineered protein drugs market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hormones Propel Next-Generation Growth

Monoclonal antibodies retained 41.22% of the bioengineered protein drugs market share in 2024, leveraging broad indications and mature production systems. Yet hormones, especially insulin and GLP-1 agonists, accelerate at a 10.59% CAGR as diabetes and obesity rates climb, and as extended-delivery devices such as Susvimo reduce injection frequency.[3]Genentech, “FDA Approves Genentech’s Susvimo as Continuous Delivery Treatment,” gene.comComplementary segments like cytokines, coagulation factors, and protein-subunit vaccines serve niche indications with premium pricing. In 2025 the FDA cleared fitusiran, which cuts bleeding episodes by more than 70%, reinforcing market potential in rare diseases.

Diversification widens revenue streams and mitigates biosimilar erosion. Enzymes and fusion proteins command limited but high-margin patient pools, while protein-drug conjugates advance precision oncology. Manufacturing complexity varies, with monoclonal antibodies benefiting from standard CHO platforms whereas emerging modalities need tailored expression and purification, influencing capital allocation within the bioengineered protein drugs market.

By Expression System: Plant Platforms Challenge Mammalian Dominance

Mammalian culture accounted for 72.37% of the bioengineered protein drugs market size in 2024 due to its track record with glycosylated antibodies and regulatory familiarity. Plant-based systems, though smaller, are rising at an 11.34% CAGR. Facilities using precision fermentation produce dairy proteins, hinting at therapeutic possibilities and green credentials. Microbial platforms facilitate rapid production for non-glycosylated proteins, while insect cells straddle complexity and speed for vaccine antigens.

Regulators show growing openness to alternative hosts as analytics confirm comparability. Cell-free systems remove cellular maintenance overhead, supporting quick-turnaround small batches for personalized medicine. These trends point toward multi-platform portfolios that balance scalability, cost, and product complexity in the bioengineered protein drugs market.

By Disease Indication: Diabetes Acceleration Challenges Oncology Leadership

Oncology treatments held 34.63% share of the bioengineered protein drugs market in 2024, aided by expedited approvals and high willingness to pay. Yet diabetes and metabolic disorders are on track for 9.47% CAGR, powered by GLP-1 advancements that address both glycemic control and weight loss. Approval of Emrelis, a c-Met antibody-drug conjugate, underscores continuous oncology innovation, but payers increasingly scrutinize oncology pricing.

Cardiovascular, infectious, and genetic diseases add diversification. Gene therapy Zevaskyn highlights synergy between gene and protein approaches in rare disorders. Cross-indication use of antibodies optimizes ROI while intensifying competition across therapeutic franchises in the bioengineered protein drugs market.

By Route of Administration: Oral Innovation Disrupts Parenteral Dominance

Parenteral delivery accounted for 84.33% of the bioengineered protein drugs market share in 2024 due to protein instability in the gut. Breakthrough formulation science led to Journavx, the first oral pain-relief protein drug, signalling 10.06% CAGR for oral routes. Inhalation delivery serves respiratory and systemic applications, while transdermal methods progress via microneedles.

Nano-encapsulation, permeability enhancers, and receptor-mediated transport improve bioavailability, potentially shifting care to outpatient or home settings. Reduced administration burden is expected to improve adherence and broaden acceptance of therapies, extending reach of the bioengineered protein drugs market.

By End User: Homecare Transformation Reshapes Delivery

Hospitals captured 56.31% of the bioengineered protein drugs market size in 2024 owing to the need for controlled infusion and adverse-event management. Homecare grows fastest at 11.53% CAGR, driven by self-injectors and connected devices that link to telemedicine portals. Specialty clinics retain relevance in oncology and autoimmune fields, while research institutes ride clinical-trial activity.

Payers favor site-of-care shifts that trim facility fees. Manufacturers design packaging and dosing schedules to fit courier delivery and patient handling limits. Together, these trends anchor patient-centric strategies central to the bioengineered protein drugs market.

Geography Analysis

North America commanded 44.29% of the bioengineered protein drugs market in 2024, fueled by rapid FDA reviews and strong venture funding. Domestic production is reinforced by Genentech’s and Biogen’s multibillion-dollar plant investments, safeguarding supply amidst geopolitical shock. Medicare price negotiations temper growth but encourage differentiated products.

Europe remains steady, leveraging biosimilar expertise and cross-border regulatory alignment. Companies capitalize on established cold-chain logistics and hospital networks to roll out long-acting formulations. The region also pilots outcome-based reimbursement models that could ripple globally, influencing strategies across the bioengineered protein drugs market.

Asia-Pacific is the fastest-growing at 9.88% CAGR, gaining from cost advantages and government incentives. China scales domestic output for export, while India’s CDMOs win contracts by offering integrated services. Projects like Liberation Labs’ Saudi facility suggest growth corridors in the Middle East and Africa that complement APAC supply chains.

Competitive Landscape

Market consolidation is moderate. Amgen, Pfizer, and Roche anchor the bioengineered protein drugs market through scale, vertical integration, and patent estates. Still, biosimilar waves and AI-enabled design spur fresh entrants. Merck KGaA’s USD 3.9 billion purchase of SpringWorks signals appetite for rare-tumor pipelines that diversify beyond maturing blockbusters. Sanofi’s USD 9.1 billion Blueprint deal deepens its rare immunology foothold.

Competitive advantage now hinges on platform capabilities in AI design, continuous manufacturing, and novel expression systems. Companies able to pair data analytics with modular plants achieve faster turnaround and cost benefits. Meanwhile, pricing scrutiny motivates life-cycle management, such as fixed-dose combinations and self-injection variants, to sustain differentiation in the evolving bioengineered protein drugs market.

Bioengineered Protein Drugs Industry Leaders

F. Hoffmann-La Roche Ltd

AbbVie

Merck & Co.

Novo Nordisk

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Biogen announced a USD 2 billion investment in its North Carolina plant to scale antisense oligonucleotide production.

- July 2025: Merck & Co. completed the USD 10 billion acquisition of Verona Pharma to secure ensifentrine, a novel COPD maintenance therapy.

- June 2025: Gilead Sciences obtained FDA approval for twice-yearly lenacapavir for HIV prevention, offering 99.9% efficacy.

- June 2025: Sanofi agreed to buy Blueprint Medicines for USD 9.1 billion, adding Ayvakit for systemic mastocytosis and early immunology assets.

Global Bioengineered Protein Drugs Market Report Scope

| Monoclonal Antibodies |

| Hormones (e.g., Insulin, GLP-1) |

| Cytokines & Interleukins |

| Coagulation Factors |

| Enzymes |

| Fusion Proteins |

| Protein-subunit Vaccines |

| Others |

| Mammalian Cell Culture (CHO, HEK293, NS0, BHK) |

| Microbial Fermentation (E. coli, Yeast) |

| Plant-based Systems |

| Insect Cell Systems |

| Oncology |

| Diabetes & Metabolic Disorders |

| Autoimmune & Inflammatory Diseases |

| Cardiovascular Diseases |

| Infectious Diseases |

| Genetic Disorders |

| Others |

| Parenteral |

| Oral |

| Inhalation |

| Transdermal |

| Hospitals |

| Specialty Clinics |

| Homecare Settings |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Monoclonal Antibodies | |

| Hormones (e.g., Insulin, GLP-1) | ||

| Cytokines & Interleukins | ||

| Coagulation Factors | ||

| Enzymes | ||

| Fusion Proteins | ||

| Protein-subunit Vaccines | ||

| Others | ||

| By Expression System | Mammalian Cell Culture (CHO, HEK293, NS0, BHK) | |

| Microbial Fermentation (E. coli, Yeast) | ||

| Plant-based Systems | ||

| Insect Cell Systems | ||

| By Disease Indication | Oncology | |

| Diabetes & Metabolic Disorders | ||

| Autoimmune & Inflammatory Diseases | ||

| Cardiovascular Diseases | ||

| Infectious Diseases | ||

| Genetic Disorders | ||

| Others | ||

| By Route of Administration | Parenteral | |

| Oral | ||

| Inhalation | ||

| Transdermal | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Homecare Settings | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the bioengineered protein drugs market?

The bioengineered protein drugs market size reached USD 372.18 billion in 2025.

How fast is the market expected to grow?

It is projected to climb to USD 532.27 billion by 2030, reflecting a 7.42% CAGR.

Which product segment is expanding the quickest?

Hormones, led by insulin and GLP-1 agonists, are forecast to grow at a 10.59% CAGR.

Why are plant-based expression systems gaining traction?

They promise lower production costs and sustainability advantages, growing at an 11.34% CAGR.

Which region shows the highest growth rate?

Asia-Pacific leads with a 9.88% CAGR, buoyed by manufacturing expansion and regulatory harmonization.

How are biosimilars affecting market dynamics?

Patent expiries allow interchangeable biosimilars to quickly capture up to 80% of reference product sales, increasing competition and reducing prices.

Page last updated on: