Immunocytokines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

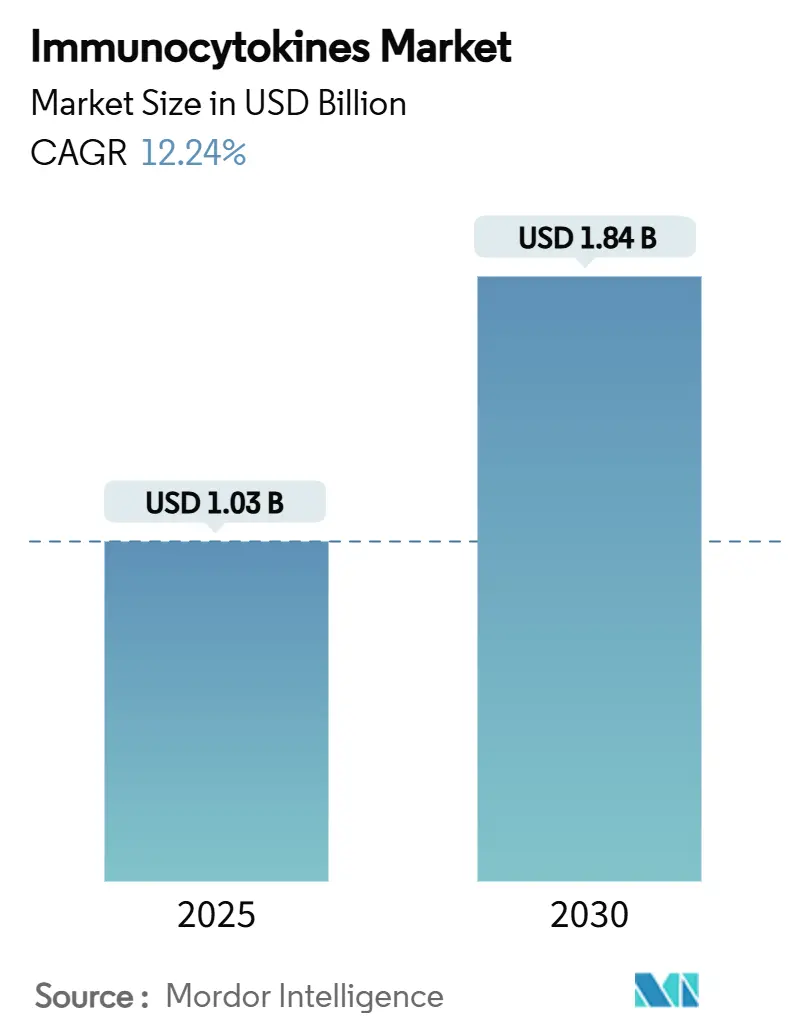

| Market Size (2025) | USD 1.03 Billion |

| Market Size (2030) | USD 1.84 Billion |

| Growth Rate (2025 - 2030) | 12.24% CAGR |

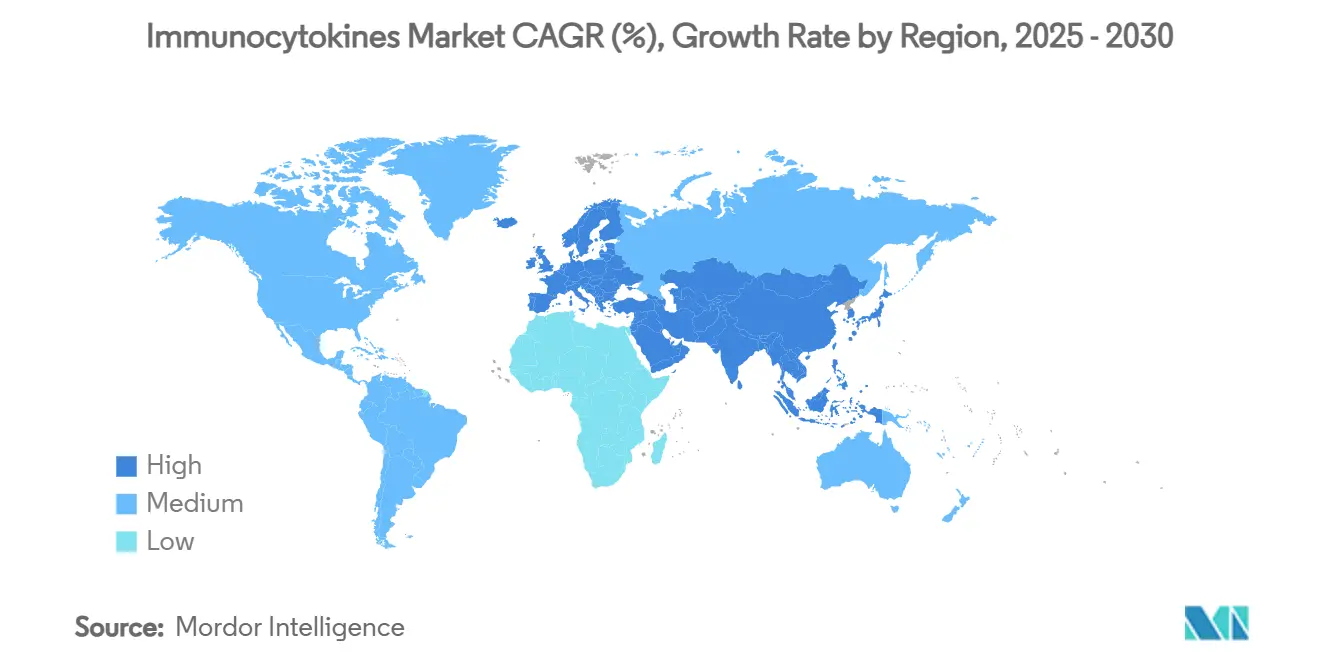

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Immunocytokines Market Analysis by Mordor Intelligence

The immunocytokines market size stood at USD 1.03 billion in 2025 and is forecast to expand at a 12.24% CAGR, lifting the value to USD 1.84 billion by 2030. Robust clinical evidence behind IL-2- and IL-15-based fusion therapies, sustained regulatory incentives such as FDA breakthrough and orphan designations, and capital inflows from large-cap pharmaceutical partners continue to propel the immunocytokines market. Manufacturing platform upgrades that pair continuous bioprocessing with AI-driven controls have lowered cost-of-goods-sold by up to 30%, encouraging smaller entrants to scale quickly. Synergistic regimens that combine immunocytokines with checkpoint inhibitors are improving survival in refractory tumors and broadening the eligible patient base, while next-generation gene and vector-encoded modalities promise durable in-situ cytokine expression. Regionally, North America retains first-mover advantage through deep clinical trial infrastructure and generous orphan-drug tax credits, yet Asia-Pacific now delivers the fastest incremental growth as regulators in Australia, Japan, and China accelerate approvals. Competitive intensity is rising as academic spin-outs translate bench discoveries into clinical programs, challenging established developers on innovation speed and niche indication focus.

Key Report Takeaways

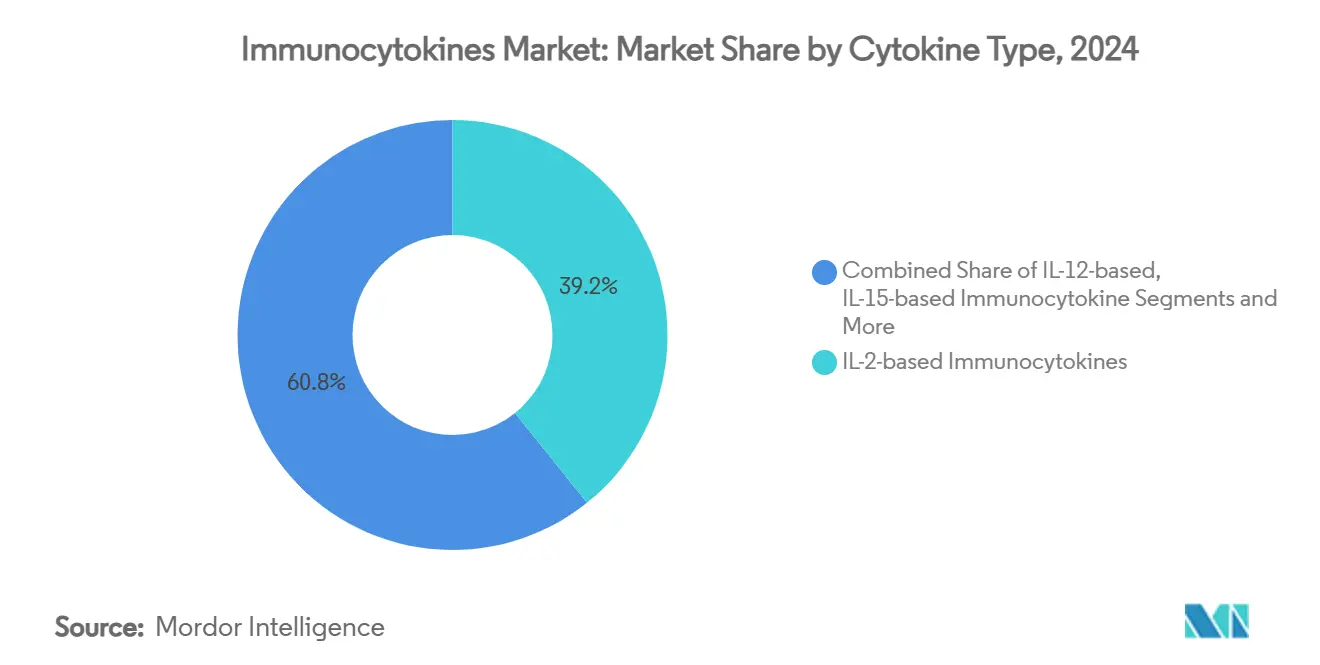

- By cytokine type, IL-2 fusion constructs commanded 39.24% immunocytokines market share in 2024, whereas IL-12 platforms are projected to advance at a 16.32% CAGR through 2030.

- By therapeutic area, oncology accounted for 48.24% of the immunocytokines market size in 2024, while autoimmune and inflammatory diseases are tracking a 14.57% CAGR to 2030.

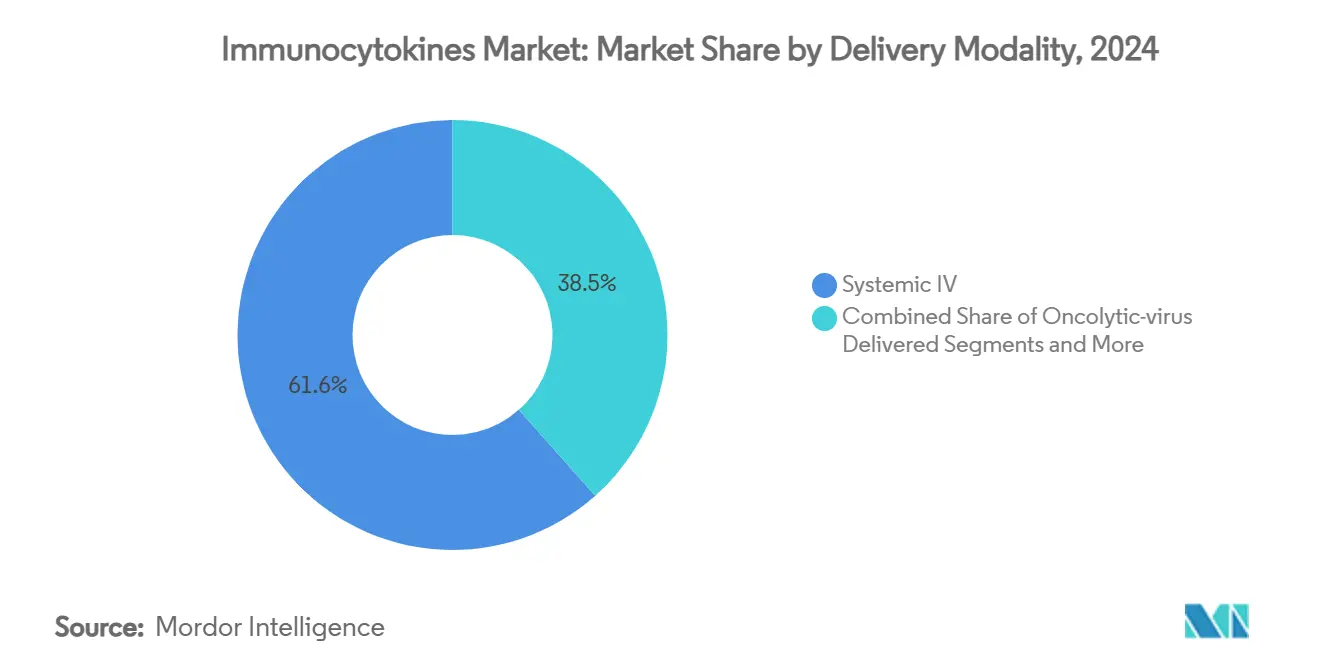

- By delivery modality, systemic IV infusions delivered 61.55% revenue share in 2024, yet gene and vector-encoded approaches are accelerating at a 16.89% CAGR.

- By end-user, pharmaceutical and biotech firms held 53.41% of demand in 2024, whereas academic and research institutes are rising fastest at 15.23% CAGR.

- By geography, North America led with 38.35% market share in 2024, while Asia-Pacific is expanding at 14.26% CAGR through 2030.

Global Immunocytokines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinical success of IL-2 fusion therapies | +2.1% | North America & EU | Medium term (2-4 years) |

| Adoption of immunocytokine + checkpoint regimens | +1.8% | Global, strongest in North America & Asia-Pacific | Short term (≤ 2 years) |

| Manufacturing platform advances reduce COGS | +1.6% | Global | Long term (≥ 4 years) |

| Pipeline expansion into autoimmune diseases | +1.4% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Orphan-drug incentives for rare tumors | +1.2% | US & EU | Short term (≤ 2 years) |

| On-demand, small-molecule-switchable constructs | +0.9% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Clinical success of IL-2 fusion therapies

Five years of durable responses from ANKTIVA in BCG-unresponsive bladder cancer have validated IL-2 design principles and unlocked sizeable venture rounds for next-wave entrants. The agent records a 71% complete response and 84% cystectomy-avoidance at 36 months, resetting expectations for non-surgical bladder preservation.[1]Paul Song, “Unmatched Long-Term Bladder Preservation,” ImmunityBio, immunitybio.com Follow-up studies pairing ANKTIVA with PD-1 inhibitors in non-small-cell lung cancer have delivered median overall survival of 14.1 months in refractory settings, prompting global confirmatory trials. Mechanistically, selective proliferation of NK and CD8 T cells without Treg expansion underpins a favorable safety profile that regulators now regard as manageable. FDA RMAT designation for pancreatic cancer further accelerates timelines and lowers capital risk. Multi-year data stability has convinced investors that IL-2 fusion therapeutics form a commercially bankable pillar of the immunocytokines market.

Rising adoption of immunocytokine + checkpoint-inhibitor regimens

Combination protocols address tumor escape by re-energizing exhausted lymphocytes while broadening antigen exposure. QUILT 3.055 reported a clinically meaningful survival lift in second-line lung cancer, corroborating pre-clinical synergy models. Cross-tumor applicability is evidenced by durable activity irrespective of PD-L1 status, encouraging developers to shift pipeline priorities from monotherapy to combination-centric strategies. Regulators have reciprocated with fast-track designations to streamline study start-up and review. Pharma sponsors now routinely embed immunocytokine arms into checkpoint backbones, setting a new investigational standard that enlarges the immunocytokines market.

Manufacturing platform advances reduce COGS

Automated perfusion bioreactors paired with inline analytics have cut batch failure by 40% and trimmed cost-of-goods by near 30% versus legacy fed-batch systems. AI-based predictive controls optimize feed rates, maximizing yield reproducibility even for complex multi-domain fusion proteins. Single-use assemblies permit rapid suite turnover, widening access for mid-cap contract manufacturers. Decentralized regional plants located near Asia-Pacific trial clusters shorten lead times and mitigate cold-chain risk. Collectively these gains ease capital thresholds, fueling a diverse company mix that broadens the immunocytokines industry footprint.

Pipeline expansion into autoimmune diseases

Sanofi’s USD 40 million alliance with Synthekine to engineer IL-10 immunocytokines for systemic lupus erythematosus signals big-pharma conviction that precision cytokine tuning can displace broad immunosuppressants. Early-phase data demonstrate site-restricted immune recalibration without systemic flare, converting hard-to-treat patients into potential long-term responders. Oncology safety databases enable accelerated autoimmune filings, compressing the clinical timeline. Rising prevalence of refractory autoimmune conditions multiplies the total addressable population, positioning non-oncology indications as the next growth frontier for the immunocytokines market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cytokine-release syndrome & safety issues | -1.5% | Global | Short term (≤ 2 years) |

| High GMP scale-up and QA/QC costs | -1.2% | Global | Medium term (2-4 years) |

| Inadequate biomarker-driven patient stratification | -0.8% | Global | Long term (≥ 4 years) |

| Competitive pull from bispecific and cell-therapy modalities | -0.6% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cytokine-release syndrome & related safety issues

Heightened immune activation carries risk of grade ≥3 reactions, demanding vigilant monitoring. ANKTIVA dose-escalation cohorts revealed manageable urinary irritation and transient creatinine rises, yet higher doses approached toxicity thresholds.[2]FDA, “Drug Trials Snapshot: ANKTIVA,” U.S. Food and Drug Administration, fda.gov Predictive biomarker panels that track interleukin surges now guide prophylactic steroid regimens. Activity-on-demand constructs hold promise for controllable exposure, though clinical validation is pending. Regulators insist on comprehensive mitigation plans before approving higher-potency candidates, tempering near-term adoption among cautious prescribers.

High GMP scale-up and QA/QC costs

Commercial manufacture of multi-domain fusion cytokines requires dedicated suites, viral clearance validation, and advanced analytics. Total facility investment can top USD 50 million, a figure that challenges small developers. Contract manufacturing organizations are adding specialized capacity, yet slot scarcity inflates per-batch pricing and stretches lead times. Continuous production and digital QC tools offer relief but demand upfront capital and process expertise, slowing time-to-market for resource-constrained entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cytokine Type: IL-12 Drives Next-Generation Innovation

The IL-2 class retained 39.24% immunocytokines market share in 2024 owing to ANKTIVA’s commercial lead and a mature clinical safety dossier. Nevertheless, IL-12 constructs are slated for a 16.32% CAGR to 2030, positioning them as the most dynamic contributor to the immunocytokines market. In tumor-activated formats such as XTX301, IL-12 payloads remain inert until enzymatically unmasked within the tumor microenvironment, driving potent innate and adaptive immunity while sparing healthy tissue.[3]Xilio Therapeutics Pipeline Team, “Xilio Therapeutics Pipeline,” Xilio Therapeutics, xiliotx.com IL-15 fusion designs extend durability by recruiting NK memory subsets, and IFN-α programs advance through mid-phase studies in hematologic malignancies. TNF-α candidates progress cautiously under heightened safety surveillance due to historical systemic toxicity, yet new masking technologies are rekindling interest. An expanding “Others” cohort, covering IL-21 and GM-CSF hybrids, underscores a trend toward combinatory payloads that fine-tune immune orchestration. Collectively, diversified cytokine engineering elevates the immunocytokines market by addressing tumor heterogeneity and broadening autoimmune applicability.

Platform developers emphasize modular designs that swap cytokine payloads without overhauling the scaffold, reducing cycle time between iterations. Novel linker chemistries compatible with high-concentration formulations improve subcutaneous options, expanding outpatient feasibility. Patents focus on protease-cleavable motifs and dual-checkpoint binding domains, creating intellectual property moats. As IL-12 data mature, analysts anticipate peer-validated endpoints sufficient for breakthrough submissions by 2027, potentially resetting the competitive hierarchy within cytokine classes.

By Therapeutic Area: Autoimmune Applications Accelerate

Oncology owned 48.24% of the immunocytokines market size in 2024, fueled by bladder, lung, and melanoma approvals that validated the modality’s anticancer efficacy. Yet, autoimmune and inflammatory indications will expand fastest at 14.57% CAGR through 2030 as IL-10 and IL-2 mute variants aim to achieve antigen-specific tolerance without broad suppression. Early systemic lupus trials report declines in double-stranded DNA titers and steroid requirements, signalling disease-modifying capacity. Infectious disease programs, including ImmunityBio’s HIV cure study combining N-803 with NK cells, open new pathogen-eradication horizons by amplifying cytolytic immunity. Fibrosis and ophthalmic candidates sit in exploratory phases, leveraging localized cytokine delivery to minimize systemic load. Across indications, payers scrutinize comparative effectiveness; thus, head-to-head data versus biologic standards will be pivotal for broad formulary inclusion.

Autoimmune diversification mitigates oncology-centric revenue cyclicality, creating steadier cash flows once chronic dosing regimens gain traction. Pharma partners view the segment as a chance to recycle oncology-derived safety datasets, accelerating proof-of-concept at reduced cost. Patient advocacy groups and regulatory agencies support expedited autoimmune studies given persistent unmet need. Consequently, therapeutic-area pluralism is becoming a hallmark of resilient pipeline strategy in the immunocytokines industry.

By Delivery Modality: Gene Vectors Transform Administration

Systemic IV remains dominant with 61.55% share due to clinician familiarity, predictable pharmacokinetics, and infrastructure compatibility with existing infusion centers. However, gene and vector-encoded platforms are tracking a 16.89% CAGR as mRNA and viral systems deliver sustained in-situ cytokine expression, shrinking dosing frequency and hospital chair time. Intratumoral injection gains momentum for solid tumors with accessible lesions, demonstrating local immunogenic cell death and antigen spread. Oncolytic-virus delivered constructs combine direct lysis with cytokine amplification, producing dual-mechanism potency attractive to combination regimens. Precision promoters and miRNA-responsive elements refine expression control, alleviating toxicity fears that historically hampered gene therapies.

Manufacturing pipelines now co-locate plasmid, mRNA, and lipid nanoparticle production lines, enabling rapid pivot between modalities based on indication need. Regulators have issued draft guidance on analytical comparability for vectorized cytokines, clarifying approval paths and encouraging investment. Collectively, delivery innovation broadens patient reach, strengthens differentiation, and sets the next growth wave for the immunocytokines market.

By End-user: Academic Partnerships Reshape Commercial Pathways

Pharmaceutical and biotech companies commanded 53.41% of the immunocytokines market share in 2024, leveraging capital resources, regulatory expertise, and established sales networks to accelerate product launches. Academic and research institutions are projected to expand at a 15.23% CAGR through 2030, steadily enlarging their slice of the immunocytokines market size by translating breakthrough cytokine-engineering concepts from bench to bedside and then licensing them to industrial partners. These university-based centers run early-phase trials that de-risk novel constructs before hand-off, shortening cycle times for commercial entrants. Cross-border consortia—such as Cardiff University’s LAG-3 collaboration with Immutep—illustrate how academia de-bottlenecks innovation for indications deemed too narrow by large pharma budgets. As clinical data mature, institutional technology-transfer offices negotiate milestone-rich deals that inject non-dilutive funding back into discovery programs, reinforcing a virtuous innovation loop.

Contract manufacturing organizations post mid-single-digit growth as smaller developers outsource complex GMP scale-up, though capacity constraints and premium pricing still influence timeline risk for late-stage programs. Hospitals and specialty clinics, the ultimate point of care, increasingly participate in investigator-initiated studies to gain early access for patients and to refine dosing protocols that improve real-world outcomes. Reimbursement dynamics steer adoption in community oncology settings, where payers weigh cytokine-therapy premiums against incremental survival benefits. Integrated delivery networks negotiate volume-based contracts that bundle infusion services with drug costs, driving gradual standardization of treatment pathways. Altogether, growing academic influence, specialized manufacturing alliances, and pragmatic hospital purchasing decisions are collectively redefining how value is created and captured across the immunocytokines market.

Geography Analysis

North America’s 38.35% share in 2024 reflects an integrated ecosystem linking venture capital, academia, and regulatory speed. The United States grants priority review vouchers and orphan incentives that de-risk capital, while National Cancer Institute networks supply trial sites experienced in advanced immunotherapies. Canada’s Strategic Innovation Fund co-finances biomanufacturing expansions, reinforcing regional supply resilience. Cross-border collaborations such as ImmunityBio’s agreement with India’s Serum Institute secure BCG supply chains vital for bladder cancer combinations, highlighting North America’s role as hub for global manufacturing orchestration.

Asia-Pacific is projected to climb at 14.26% CAGR through 2030 as regulatory agencies harmonize standards and expand accelerated pathways. Australia’s Therapeutic Goods Administration approved the first PD-1 checkpoint inhibitor-linked immunocytokine, demonstrating regional willingness to leverage international data packages. Japan’s Pharmaceuticals and Medical Devices Agency runs Sakigake fast-track designations that shorten review cycles by six months, enticing sponsors to locate bridging studies locally. China’s multibillion-dollar Bio-Made zones in Shanghai and Guangzhou offer tax holidays and GMP subsidies, supporting domestic contenders that address large unmet oncology demand. India’s clinical site expansion and robust generics infrastructure position it as a cost-efficient hub for phase II/III programs, further fueling regional momentum.

Europe maintains steady uptake supported by the European Medicines Agency’s centralized approval process and strong academic-industry consortia. Germany’s BioNTech-led ecosystems supply mRNA know-how transferable to vector-encoded cytokines, while the United Kingdom’s MHRA pilots rolling reviews that benefit advanced therapeutics. Horizon Europe grants fund translational cytokine biology, reinforcing pipeline depth. Smaller regions such as the Gulf Cooperation Council, Brazil, and South Africa show nascent interest, constrained by reimbursement hurdles yet buoyed by rising oncology incidence and partnerships aimed at technology transfer. Overall, geographic diversification smooths revenue exposure and injects competitive pressure that speeds technical diffusion across the immunocytokines market.

Competitive Landscape

The immunocytokines market demonstrates moderate concentration, with the top five developers holding close to 45% combined revenue, leaving material headroom for challengers. ImmunityBio leverages first-to-market status and robust manufacturing scale to defend share, while Nektar Therapeutics pivots toward tumor-conditioned activation technology. Xilio Therapeutics’ protease-unlocked cytokines and GT Biopharma’s TriKE platform showcase specialized engineering targeting tumor microenvironment barriers. Large pharma players such as Bristol Myers Squibb, AbbVie, and Sanofi hedge pipelines via licensing pacts; AbbVie’s USD 48 million upfront with OSE Immunotherapeutics and USD undisclosed milestones with Ichnos Glenmark exemplify deal-making intensity.

Strategic focus centers on differentiation through controllability, localized delivery, and combination coherence with checkpoint backbones. Companies emphasize intellectual property breadth, filing overlapping claims on fusion formats, masking linkers, and vector payload architecture. Manufacturing alliances between small innovators and seasoned biologics plants mitigate scale-up risk; for example, ImmunityBio’s use of Thermo Fisher facilities accelerates global rollout. Academic spin-outs foster disruptive ideas, and VC syndicates prioritize platform versatility that can address oncology, autoimmune, and infectious diseases under a single scaffold. Overall, sustained flow of capital and scientific ingenuity ensure vibrant competition that advances patient-centric innovation across the immunocytokines market.

Immunocytokines Industry Leaders

Philogen S.p.A.

Nektar Therapeutics

ImmunityBio Inc.

F. Hoffmann-La Roche AG

Xilio Therapeutics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: AbbVie entered an exclusive worldwide license with Ichnos Glenmark Innovation for ISB 2001, a CD38×BCMA×CD3 trispecific antibody in Phase 1 showing a 79% overall response rate in relapsed/refractory multiple myeloma.

- June 2025: ImmunityBio received FDA RMAT designation for ANKTIVA combined with CAR-NK to reverse lymphopenia in patients undergoing chemo-radio therapy.

- April 2025: ImmunityBio reported 71% complete response and 84% cystectomy avoidance at 36 months for ANKTIVA + BCG in non-muscle invasive bladder cancer.

- February 2025: INmune Bio announced plans to file a Biologics License Application for CORDStrom, a mesenchymal stromal cell therapy for paediatric Recessive Dystrophic Epidermolysis Bullosa, following positive MissionEB data.

Global Immunocytokines Market Report Scope

| IL-2-based Immunocytokines |

| IL-12-based Immunocytokines |

| IL-15-based Immunocytokines |

| IFN-α-based Immunocytokines |

| TNF-α-based Immunocytokines |

| Others (IL-21, GM-CSF, Combo) |

| Oncology |

| Autoimmune & Inflammatory Diseases |

| Infectious Diseases |

| Others (Fibrosis, Ophthalmology) |

| Systemic IV |

| Intratumoral Injection |

| Gene / Vector-encoded (e.g., mRNA, Viral) |

| Oncolytic-virus Delivered |

| Pharmaceutical & Biotech Companies |

| Academic & Research Institutes |

| Contract Manufacturing Organizations |

| Hospitals / Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Cytokine Type | IL-2-based Immunocytokines | |

| IL-12-based Immunocytokines | ||

| IL-15-based Immunocytokines | ||

| IFN-α-based Immunocytokines | ||

| TNF-α-based Immunocytokines | ||

| Others (IL-21, GM-CSF, Combo) | ||

| By Therapeutic Area | Oncology | |

| Autoimmune & Inflammatory Diseases | ||

| Infectious Diseases | ||

| Others (Fibrosis, Ophthalmology) | ||

| By Delivery Modality | Systemic IV | |

| Intratumoral Injection | ||

| Gene / Vector-encoded (e.g., mRNA, Viral) | ||

| Oncolytic-virus Delivered | ||

| By End-user | Pharmaceutical & Biotech Companies | |

| Academic & Research Institutes | ||

| Contract Manufacturing Organizations | ||

| Hospitals / Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is an immunocytokine and how does it work?

An immunocytokine is a fusion protein that links an immune-stimulating cytokine to a targeting moiety (often an antibody fragment) so the cytokine is delivered directly to diseased tissue, boosting local immune activity while limiting systemic toxicity.

How large was the immunocytokines market size in 2025?

The market generated USD 1.03 billion in 2025 and is projected to rise to USD 1.84 billion by 2030 on a 12.24% CAGR.

Which cytokine class currently drives the most revenue?

IL-2 fusion constructs led with 39.24% share in 2024, validated by ANKTIVA’s first-in-class approval in bladder cancer.

Why is Asia-Pacific showing the fastest growth?

Faster regulatory reviews, expanding clinical trial capacity in Australia, Japan, China and India, and strategic manufacturing partnerships are lifting the region at a 14.26% CAGR through 2030.

What safety risks must developers mitigate?

Cytokine-release syndrome remains the primary concern; developers employ dose titration, biomarker monitoring and activity-on-demand designs to limit severe immune reactions.

Page last updated on: