Antibody Fragments Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

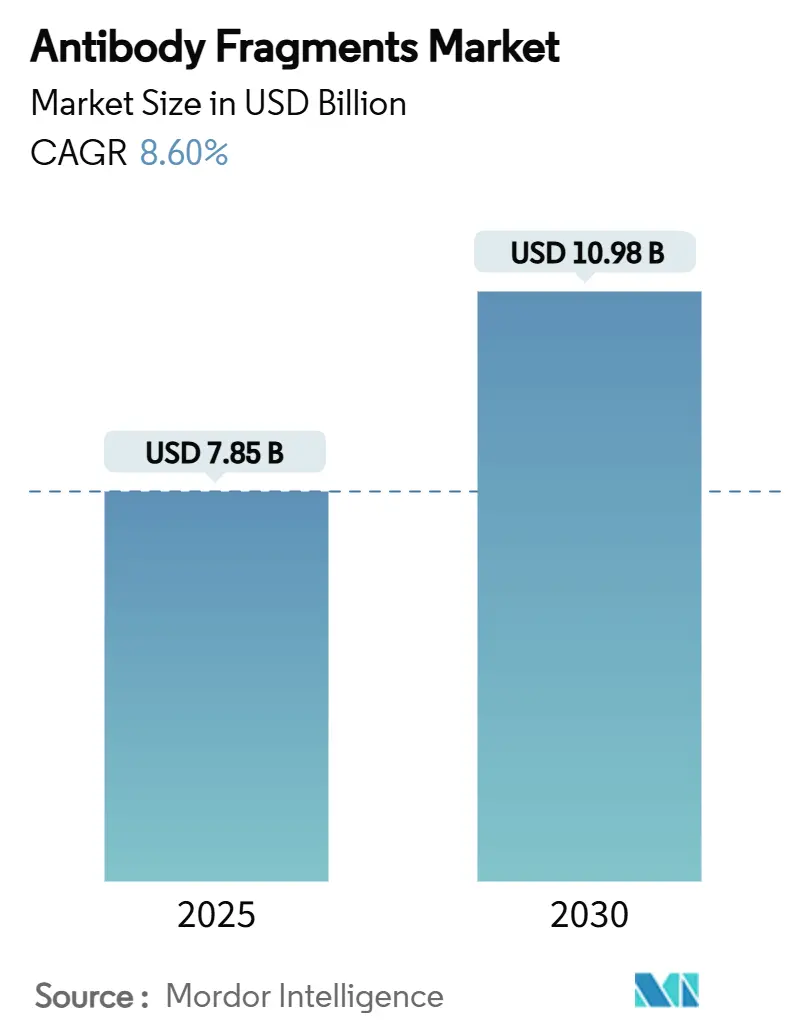

| Market Size (2025) | USD 7.85 Billion |

| Market Size (2030) | USD 10.98 Billion |

| Growth Rate (2025 - 2030) | 8.60% CAGR |

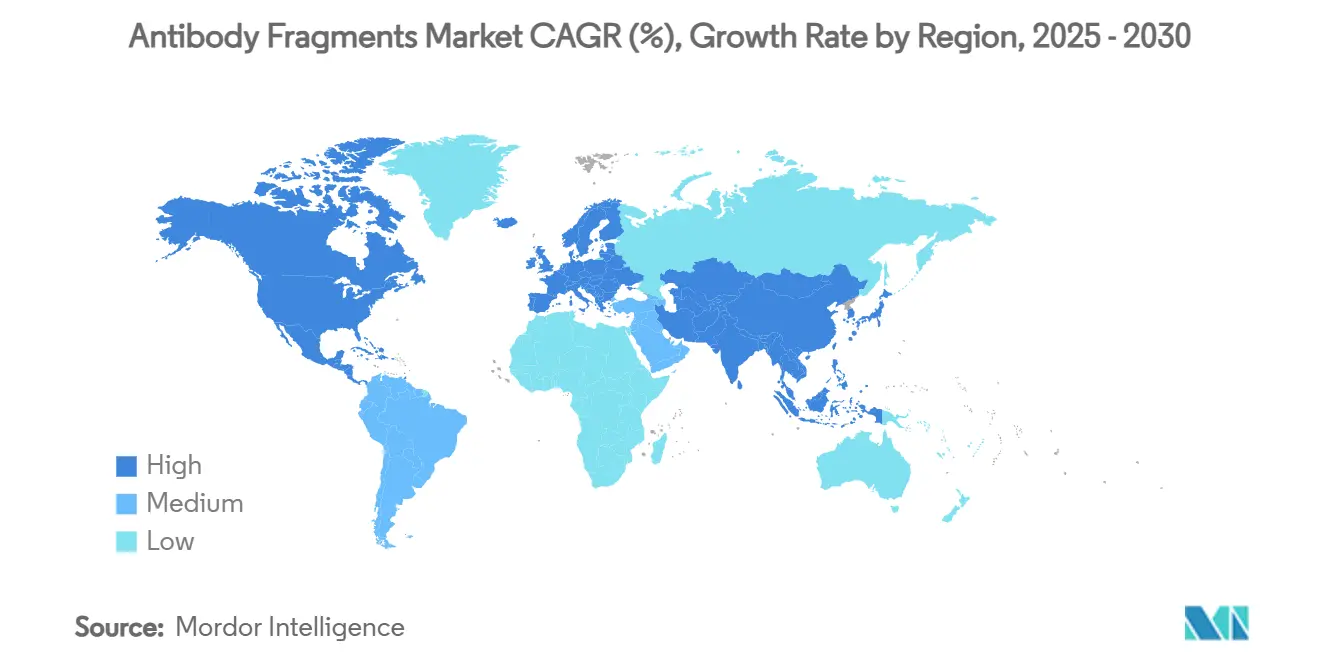

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antibody Fragments Market Analysis by Mordor Intelligence

The antibody fragments market size stands at USD 7.85 billion in 2025 and is forecast to reach USD 10.98 billion by 2030, translating into an 8.6% CAGR for the period. Demand is amplified by the superior tissue penetration and lower immunogenicity of fragments versus full-length antibodies, the rapid progress of AI-directed phage display and cell-free synthesis, and a widening clinical pipeline that targets oncology, autoimmune, and metabolic disorders. Investment in fragment-specific manufacturing, particularly in Asia-Pacific, is creating fresh supply capacity, while regulatory guidance from the FDA on bispecific and fragment-drug conjugates is cutting approval risk and speeding development. Competitive momentum is visible in the strong M&A cycle that has placed fragmented platforms at the center of portfolio defense as major biopharma firms confront looming patent expiries and look for differentiation. White-space opportunities arise at the intersection of fragments and real-time molecular imaging, where same-day diagnostics and theragnostic pairings can lift patient outcomes and expand reimbursement potential.

Key Report Takeaways

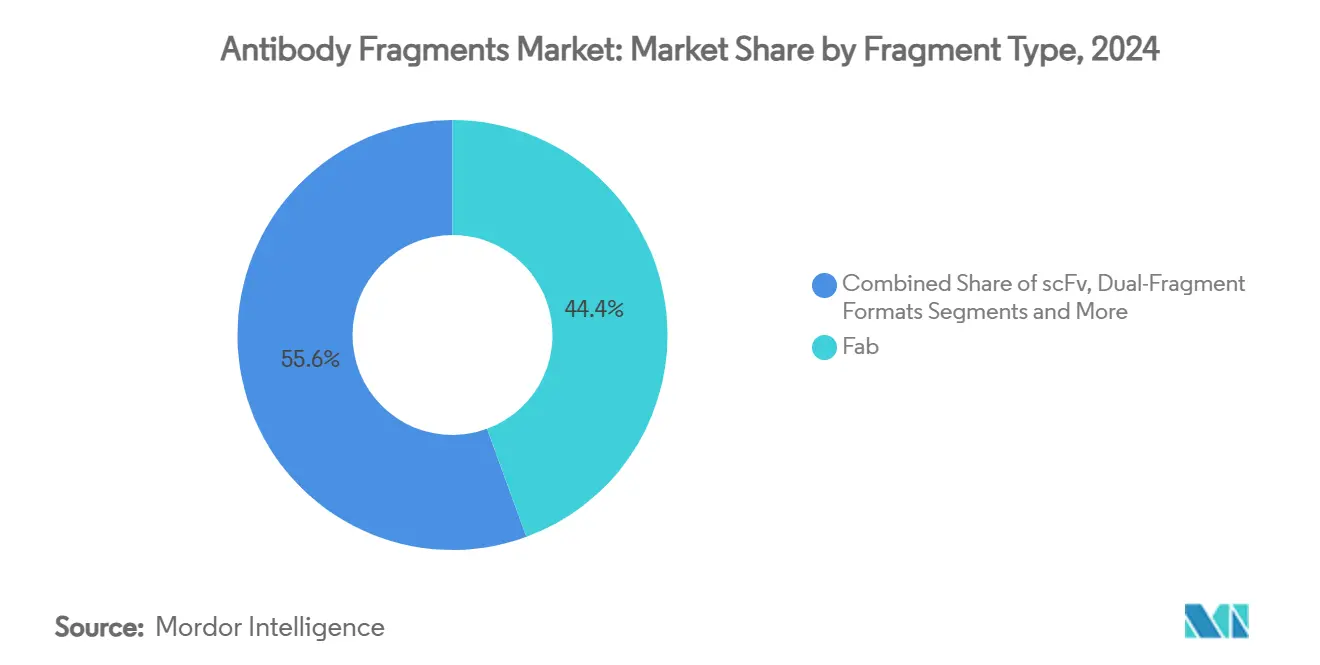

- By fragment type, Fab fragments led with 44.4% revenue share in 2024, whereas nanobody formats are advancing at an 11.65% CAGR through 2030.

- By application, therapeutics captured 69.5% of the antibody fragments market share in 2024, while diagnostics and imaging are set to grow the fastest at 9.98% CAGR up to 2030.

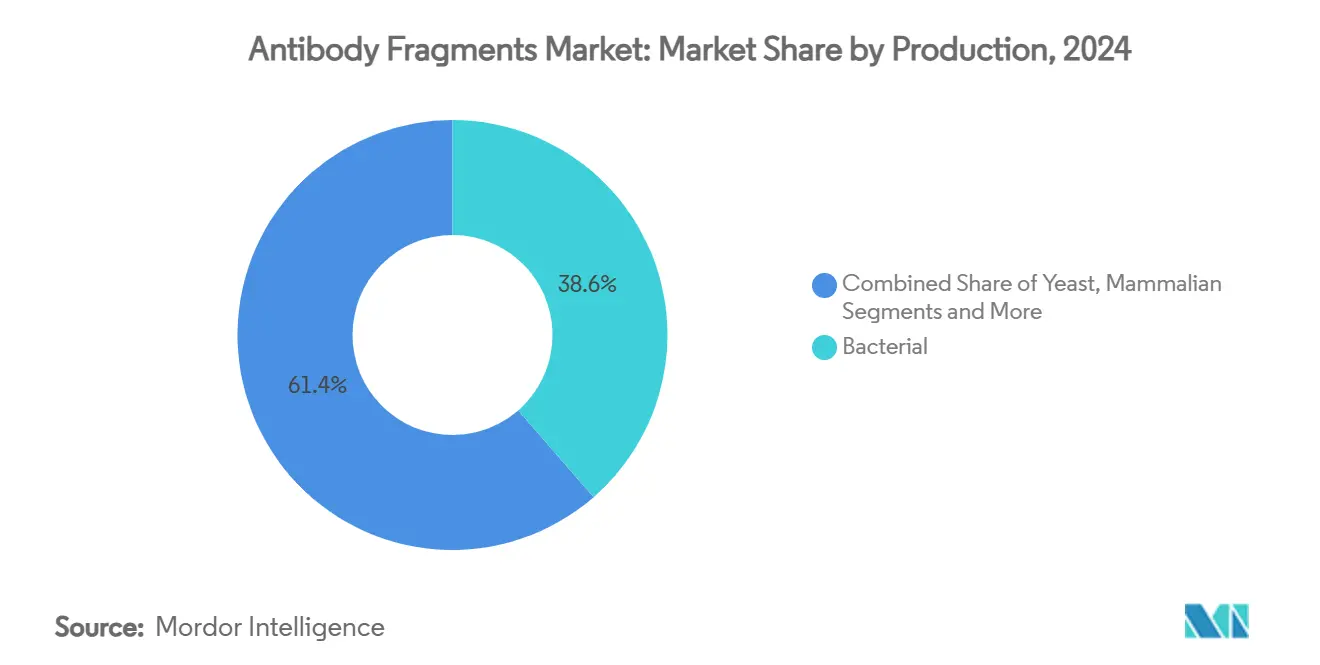

- By production method, bacterial expression systems accounted for 38.6% share of the antibody fragments market size in 2024, yet phage display and cell-free platforms are projected to climb at 12.50% CAGR over the forecast window.

- By end user, biopharmaceutical companies held 61.5% share in 2024, whereas CRO / CMO demand is expanding at 9.05% CAGR to 2030.

- By geography, North America dominated with 46.2% revenue share in 2024, while Asia-Pacific is on track for an 8.3% CAGR through 2030 on the back of large-scale plant build-outs and regulatory harmonization.

Global Antibody Fragments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of chronic diseases driving demand for targeted biologics | +2.10% | Global, high in North America and Europe | Long term (≥ 4 years) |

| Advantages of fragments: superior tissue penetration and reduced immunogenicity | +1.80% | Global, especially emerging APAC markets | Medium term (2-4 years) |

| Growing approvals and robust pipeline of fragment-based therapeutics | +1.20% | North America and EU leadership | Short term (≤ 2 years) |

| Emergence of fragment-drug conjugates for solid-tumour penetration | +0.90% | Oncology hubs in US and Germany | Medium term (2-4 years) |

| Convergence with advanced molecular imaging for in-vivo diagnostics | +0.70% | North America and EU | Long term (≥ 4 years) |

| AI-directed phage display and cell-free synthesis shorten R&D cycles | +0.60% | US, UK and Singapore biotech hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Prevalence of Chronic Diseases Driving Demand for Targeted Biologics

Cancer incidence is projected to rise by 47% by 2040, intensifying the need for therapies that can infiltrate solid tumors and spare healthy tissue.[1]U.S. Food and Drug Administration, “Clinical Pharmacology Considerations for Antibody-Drug Conjugates,” fda.govAntibody fragments meet this requirement through deeper tissue penetration and the ability to hit hidden epitopes that full-length antibodies overlook. Stronger demand also surfaces in autoimmune indications, where fragment-based immunomodulators achieve efficacy with fewer systemic side effects. Ageing demographics and lifestyle shifts in both industrialized and developing regions add steady volume to the therapeutic funnel. Major payers now reward targeted biologics that curb hospitalization costs, reinforcing market pull. Collectively, these factors give the antibody fragments market durable growth headroom.

Advantages of Fragments: Superior Tissue Penetration & Reduced Immunogenicity

Fragments are one-tenth the size of conventional IgG molecules and therefore navigate dense extracellular matrices more readily, with single-chain variable fragments reaching up to triple the tumour penetration of intact antibodies.[2]MDPI Editorial Board, “Anti-Drug Antibody Response to Therapeutic Antibodies and Potential Mitigation Strategies,” mdpi.com Fc-domain omission lowers complement activation, cutting the risk of infusion reactions. Nanobody formats reveal markedly lower anti-drug antibody formation, extending dosing intervals, and improving adherence. These pharmacological benefits translate into better risk-benefit ratios in chronic therapy settings. Precision medicine initiatives favor low-immunogenic scaffolds that can be re-dosed without neutralizing responses, further supporting adoption.

Growing Approvals & Robust Pipeline of Fragment-Based Therapeutics

The US FDA green-lighted teclistamab-cqyv for multiple myeloma, setting a precedent for bispecific T-cell engagers built on fragment backbones. Over 100 fragment candidates are now in clinical phases across oncology, rheumatology, and ophthalmology. Regulatory pathways have grown clearer as agencies release indication-specific guidance, trimming time-to-market. Venture and strategic funding surged in 2024, with landmark acquisitions signalling confidence in the modality. This pipeline breadth ensures a stable influx of launches that keep the antibody fragments market on its CAGR trajectory.

Emergence of Fragment-Drug Conjugates (FDCs) for Solid-Tumour Penetration

FDCs marry the small-format reach of fragments with potent warheads tuned for controlled intracellular release. Linker chemistries have been re-engineered to match fragment pharmacokinetics, enabling deeper tumour saturation at lower systemic exposure. Early clinical results show superior tumour-to-blood ratios versus classic ADCs. Site-specific conjugation improves product homogeneity and simplifies CMC dossiers, supporting faster regulatory review. As solid tumours account for the bulk of oncology incidence, FDCs can unlock substantial incremental market value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short serum half-life requiring costly half-life-extension technologies | -1.40% | Emerging markets most sensitive to cost | Medium term (2-4 years) |

| Purification and manufacturing complexity without Fc binding to Protein A | -0.80% | Global manufacturing hubs, strong in Asia-Pacific | Short term (≤ 2 years) |

| Regulatory ambiguity around novel bispecific and nano-format fragments | -0.60% | US, EU regulators with APAC spillover | Medium term (2-4 years) |

| Competition from alternative scaffolds in similar niches | -0.40% | Specialised research markets worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Short Serum Half-Life Requiring Costly Half-Life-Extension Technologies

Most fragment scaffolds circulate for only hours, forcing frequent dosing that erodes patient convenience and raises payer spend. PEGylation, albumin-binding tags, and Fc fusions double or even triple COGS, squeezing margins in price-sensitive indications. Albumin-binder conjugates can provoke immune responses, adding clinical risk. These hurdles are most acute in emerging economies, where health budgets struggle with chronic dosing regimens. Innovation in polymer conjugation is underway, but it will take several years to attain regulatory traction and cost parity.

Purification & Manufacturing Complexity Without Fc Binding to Protein A

Removing the Fc domain nullifies the high-capacity Protein A workflow that powers monoclonal antibody economics. Multi-step ion exchange and HIC alternatives cut yields and lift the cost of goods by up to 60%. Custom protocols per fragment format hinder scale and complicate tech transfer, especially for CMOs juggling diverse client portfolios. Continuous processing and single-use chromatography skids promise relief but demand upfront validation spend, impeding near-term cost downs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fragment Type: Nanobodies Drive Innovation Despite Fab Dominance

Fab fragments generated the largest revenue share in 2024, at 44.4%, in the antibody fragments market. Nanobodies, though smaller in value today, post an 11.65% CAGR, making them the prime innovation engine. Adoption reflects nanobodies' ability to exploit hidden grooves on GPCRs, ion channels, and intracellular antigens unreachable by bigger scaffolds. Their thermal stability and efficient bacterial expression can cut manufacturing costs by 50%, an attractive lever for biosimilars and emerging-market launches.

AI-assisted affinity maturation has recently overcome historical specificity gaps, making nanobodies viable for high-affinity therapeutics. Clinical precedents in oncology and autoimmunity calm regulatory concerns, while robust IP coverage in Europe and China confers defensible positions to first movers. Over the forecast horizon, nanobodies are expected to chip away at Fab share, especially in indications requiring blood–brain barrier transit and rapid renal elimination.

By Application: Diagnostics Accelerate While Therapeutics Dominate

Therapeutics held 69.5% of the 2024 revenue share, while diagnostics and imaging, although smaller, expanded at 9.98% CAGR and will add meaningful incremental revenue through 2030. Growth in imaging stems from the same-day scan capability that halves clinical workflow time versus full-length antibody tracers. Hospitals see faster bed turnover and better scheduling, while payers benefit from reduced inpatient costs.

Fragment-drug conjugates amplify therapeutic impact in solid tumours, fuelling a virtuous cycle where diagnostic success informs targeted treatment. Biosensors and point-of-care devices adopt fragments for their rapid on-off kinetics, supporting infectious-disease panels that demand quick turnaround. Research reagent demand plateaus but remains essential, as academic labs continue to seed the discovery funnel for commercial programs. Overall, therapeutics will stay the revenue anchor, but diagnostics will widen total addressable markets and diversify use cases.

By Production Method: Cell-Free Systems Challenge Bacterial Dominance

Bacterial systems supplied 38.6% of global value shared in 2024, underpinned by low-cost fermenters and established downstream modules. Cell-free and phage display platforms, however, race ahead at 12.50% CAGR thanks to rapid prototyping capability. Cell-free reactions remove cellular bottlenecks and allow direct incorporation of non-canonical amino acids, vital for site-specific payload conjugation. Early-stage yields now exceed 1 g/L, narrowing the cost gap versus bacteria. Yeast provides a halfway house, supplying glycosylated fragments at a moderate cost for ophthalmology and inflammatory targets.

Mammalian lines stay relevant for Fc-fusion fragments that need human-like glycosylation, even though higher overhead limits them to premium indications. Plant-based expression garners pilot-scale interest for pandemic surge capacity but awaits downstream economic proof. Over the forecast, a hybrid manufacturing network is expected, with bacterial lines handling volume and cell-free hubs delivering high-complexity molecules on demand.

By End User: CROs Expand as Biopharma Leads

Biopharmaceutical companies held a 61.5% market share in the antibody fragments market in 2024. CRO / CMO demand grew at a 9.05% CAGR because sponsors outsourced to access specialized fragment know-how and capex-heavy purification lines. Asia-Pacific CMOs such as WuXi Biologics erect dedicated fragment suites, pulling projects from Western firms that look to contain cost and shorten lead times. Academic centres stay pivotal for discovery; roughly one-third of INDs filed in 2024 originated from university spin-offs.

Diagnostic laboratories boost orders for fragment-based PET tracers, particularly in Europe where health systems aim for same-day discharge. A cadre of specialist service providers has emerged to offer AI-enabled affinity maturation and cell-free screening, carving a niche in early discovery. The outsourcing wave should persist as regulatory standards tighten, encouraging even large pharmas to tap external GMP expertise rather than retrofit legacy plants.

Geography Analysis

North America held 46.2% of global revenue in 2024, reflecting the region’s concentration of biotech capital, FDA leadership, and deep clinical-trial infrastructure. Accelerated approval pathways for breakthrough therapies remove uncertainty and pull in global development programmes. Canada leverages generous tax credits and evolving rare-disease frameworks to attract early-phase trials, while Mexico positions itself as a cost-efficient fill-and-finish node for export supply. Venture funding in Boston, the Bay Area, and Toronto remains robust, underpinning discovery at academic–industry interfaces.

Asia-Pacific is the fastest compounder at 8.3% CAGR, fueled by large-scale GMP suites under construction in China, South Korea, and Singapore. Government grants and cluster policies encourage technology transfer, while regulators harmonize review timelines to global standards. Japan continues to pioneer bispecific approvals, offering reference cohorts for Western regulators. Australia complements this with strong translational research and an R&D tax incentive that reimburses up to 43.5% of eligible spending, drawing early clinical studies southward.

Europe remains sizeable through 2030, anchored by Germany’s antibody engineering legacy and the United Kingdom’s robust VC ecosystem.[3]Nature Communications Editors, “Broadly Potent Spike-Specific Human Monoclonal Antibodies,” nature.com Harmonized EU guidelines reduce duplication, yet Brexit introduces extra administrative layers for UK dossiers. France scales fragment production via public–private consortia, whereas Italy and Spain focus on biosimilar pathways to tame healthcare budgets. Eastern European countries court contract manufacturing with competitive labor rates but face skills gaps. Overall, Europe benefits from precision-medicine reimbursement frameworks that reward targeted biologics, reinforcing demand for high-value fragments.

Competitive Landscape

Competition is moderate-to-high as global pharmaceutical majors compete with agile biotech challengers for leadership in the antibody fragments market. Roche, AbbVie, and Novartis channel capital into bispecific and conjugate platforms, often using acquisitions to plug technology gaps rather than build internally. The Novartis purchase of Dren Bio for USD 3 billion exemplifies the premium placed on fragment portfolios that can differentiate oncology pipelines.

Licensing is another strategic lever, with AbbVie securing trispecific rights from Ichnos Glenmark for USD 700 million to broaden its immunotherapy suite. Smaller innovators focus on highly specialized domains such as blood–brain barrier transit or intracellular antigen targeting, frequently partnering once proof-of-concept is established. IP positions are increasingly complex, with broad patent families around humanization, conjugation, and half-life extension creating cross-licensing webs that favor incumbents with strong legal resources.

Manufacturing capability is a sharp differentiator because fragment purification lacks a one-size-fits-all workflow. Firms that master high-yield, multi-step downstream operations gain cost and schedule advantages that translate into pricing power. AI-augmented discovery platforms add another competitive axis; players integrating machine learning report lead-optimization cycles of six weeks versus twelve months under classical protocols. Overall, sustained M&A, strategic alliances and technology integration point to a dynamic market where leadership will rest on the capacity to industrialize innovation at scale.

Antibody Fragments Industry Leaders

F. Hoffmann-La Roche AG

AbbVie Inc.

Novartis

Amgen

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Johnson & Johnson presented 84-week nipocalimab data showing 45% steroid reduction in gMG patients.

- January 2025: Novartis closed a USD 3 billion deal for Dren Bio’s anti-myeloid bispecific platform to strengthen solid-tumour programs.

- December 2024: AstraZeneca committed USD 1.5 billion to a Singapore plant dedicated to antibody-drug conjugate and fragment-drug conjugate production.

- August 2024: BioNTech bought Biotheus for USD 800 million to acquire bispecific fragment expertise for pipeline diversification.

Global Antibody Fragments Market Report Scope

| Fab Fragments |

| Single-chain Variable Fragment (scFv) |

| Dual-Fragment Formats |

| Single-domain / Nanobody |

| Other Novel Formats (Bispecific Fragments) |

| Therapeutics |

| Diagnostics & Imaging |

| Research Reagents |

| Drug Delivery & Conjugates |

| Biosensors |

| Bacterial Expression Systems |

| Yeast Expression Systems |

| Mammalian Expression Systems |

| Phage Display / Cell-Free Systems |

| Plant-based & Other Systems |

| Biopharmaceutical & Biotechnology Companies |

| Contract Research & Manufacturing Organizations (CROs/CMOs) |

| Academic & Research Institutes |

| Diagnostic Laboratories |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Fragment Type | Fab Fragments | |

| Single-chain Variable Fragment (scFv) | ||

| Dual-Fragment Formats | ||

| Single-domain / Nanobody | ||

| Other Novel Formats (Bispecific Fragments) | ||

| By Application | Therapeutics | |

| Diagnostics & Imaging | ||

| Research Reagents | ||

| Drug Delivery & Conjugates | ||

| Biosensors | ||

| By Production Method | Bacterial Expression Systems | |

| Yeast Expression Systems | ||

| Mammalian Expression Systems | ||

| Phage Display / Cell-Free Systems | ||

| Plant-based & Other Systems | ||

| By End User | Biopharmaceutical & Biotechnology Companies | |

| Contract Research & Manufacturing Organizations (CROs/CMOs) | ||

| Academic & Research Institutes | ||

| Diagnostic Laboratories | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the antibody fragments market in 2025?

The antibody fragments market size reaches USD 7.85 billion in 2025 and is projected to hit USD 10.98 billion by 2030.

Which fragment type grows the fastest?

Nanobody / single-domain formats post the highest CAGR at 11.65%, reflecting strong performance in tumour penetration and stability.

What region will expand most quickly through 2030?

Asia-Pacific rises at an 8.3% CAGR as China, South Korea and Singapore build large fragment-dedicated manufacturing plants.

Which application currently dominates revenue?

Therapeutic use commands 69.5% of 2024 sales due to rising approvals in oncology and autoimmune diseases.

Why are cell-free systems important now?

Cell-free synthesis supports rapid prototyping and site-specific conjugation, driving a 12.50% CAGR in production methodologies.

What is the main barrier to lower cost production?

The lack of Protein A affinity for fragments forces multi-step purification that can raise manufacturing costs by up to 60%.

Page last updated on: