Immunoassay Analyzers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

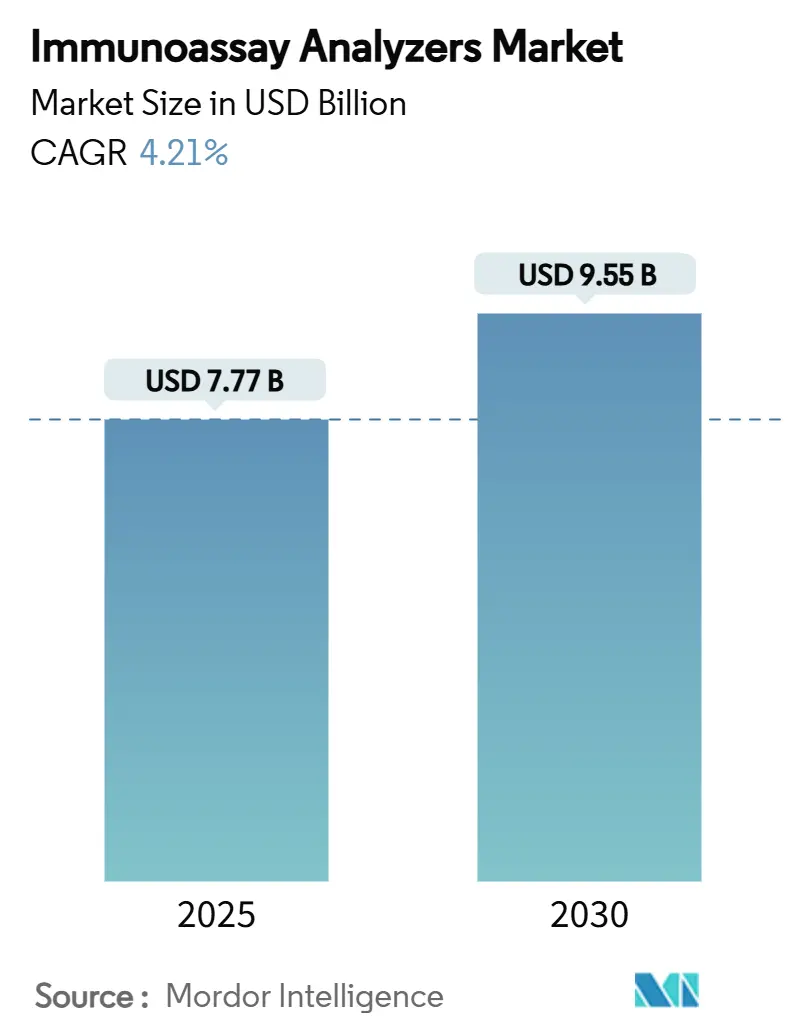

| Market Size (2025) | USD 7.77 Billion |

| Market Size (2030) | USD 9.55 Billion |

| Growth Rate (2025 - 2030) | 4.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

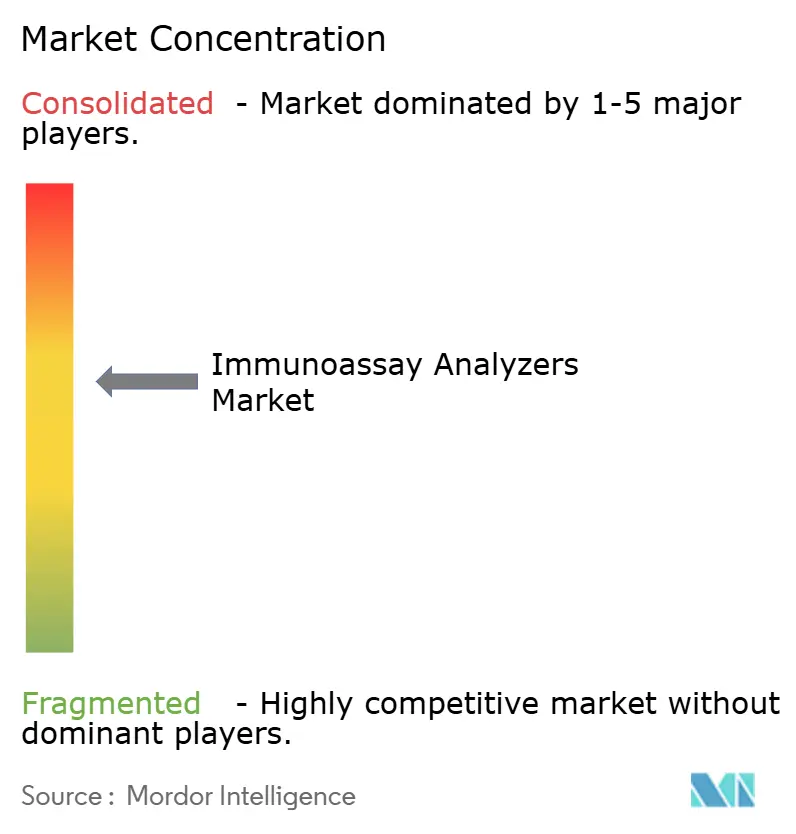

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Immunoassay Analyzers Market Analysis by Mordor Intelligence

The immunoassay analyzers market size reached USD 7.77 billion in 2025 and is forecast to climb to USD 9.55 billion by 2030, advancing at a 4.21% CAGR. This measured expansion reflects rising demand for laboratory automation, artificial-intelligence–enabled quality controls and a shift toward decentralized, point-of-care (POC) workflows rather than sheer test-volume growth. Vendors are responding to vacancy rates that have reached 25% in United States hospital laboratories by delivering compact, AI-driven platforms that keep output stable even when technologist staffing falls short. At the same time, multiplex and microfluidic technologies support broader test menus for oncology and fertility, while veterinary diagnostics open a fast-growing adjacent revenue stream. Regulatory tightening in the United States and European Union is raising compliance costs, yet it also favors companies with established quality-management systems and encourages strategic acquisitions aimed at bridging automation, reagent and software gaps.

Key Report Takeaways

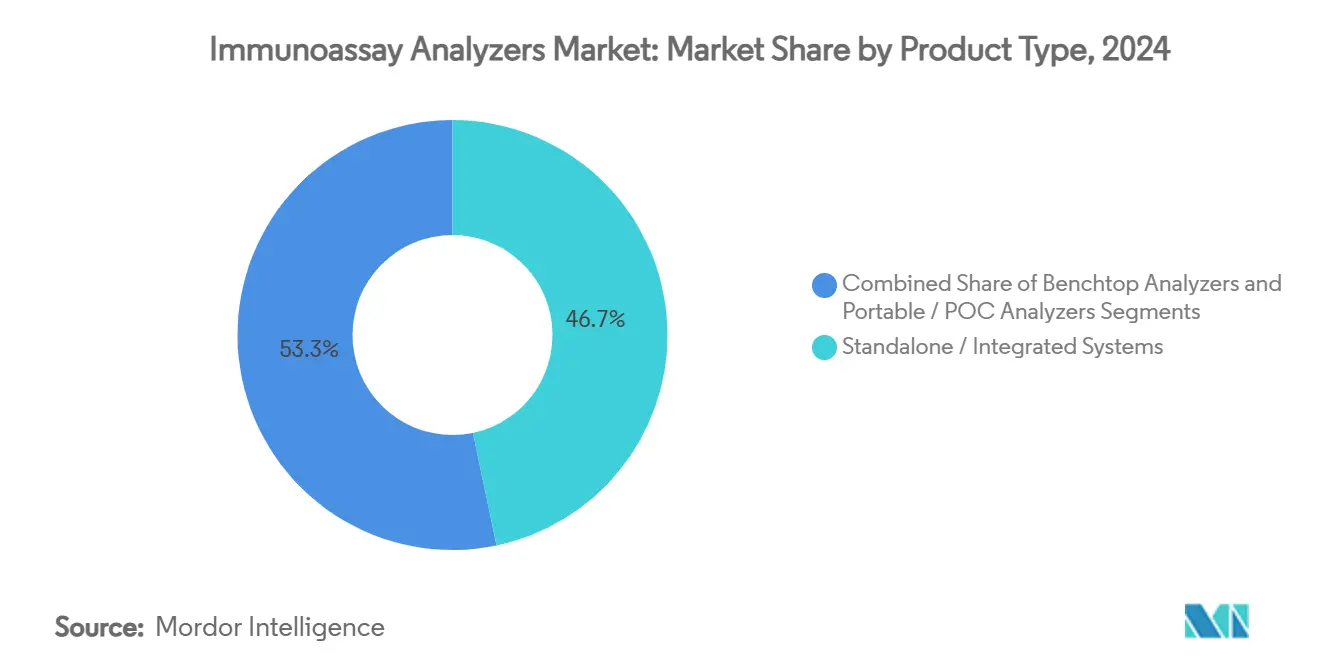

- Standalone and integrated instruments captured 46.72% immunoassay analyzers market share in 2024. Portable and POC analyzers are projected to post the fastest 8.67% CAGR through 2030.

- ELISA accounted for 63.42% of the immunoassay analyzers market size in 2024, while multiplex and microfluidic platforms are set to expand at a 7.25% CAGR.

- Hospital laboratories held 51.33% of the immunoassay analyzers market share in 2024; veterinary clinics and labs are on track for a 7.05% CAGR.

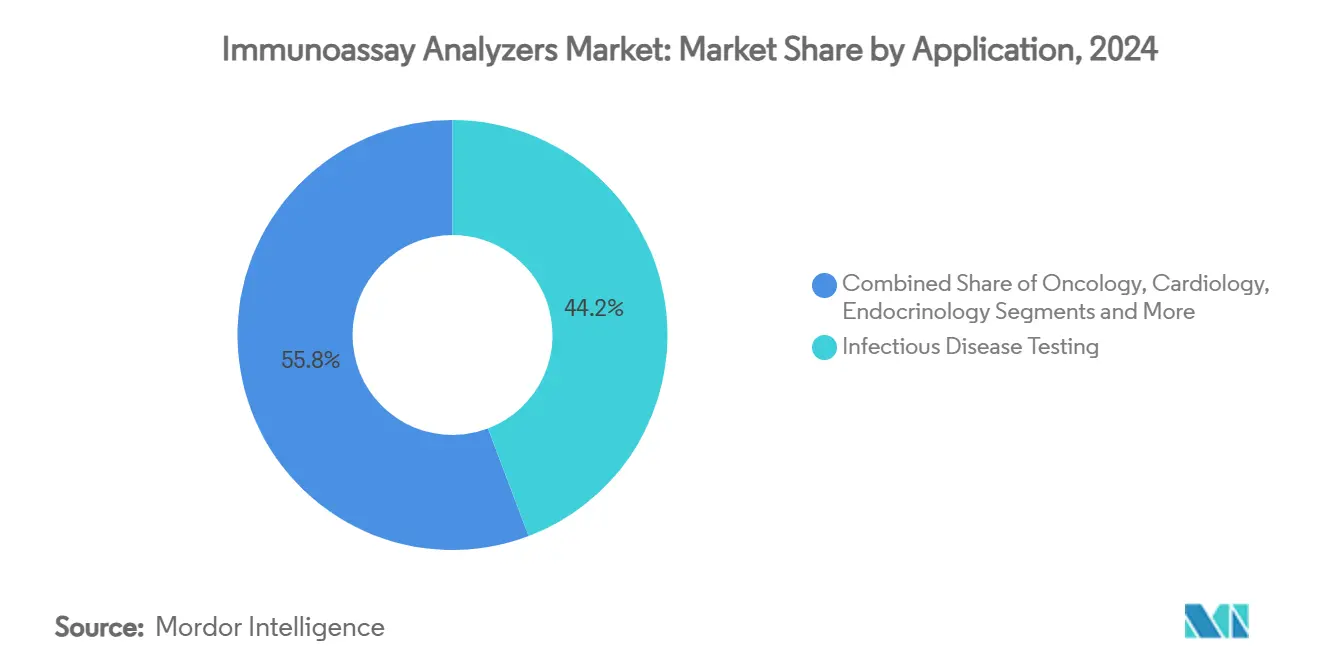

- Infectious-disease testing represented 44.23% of the immunoassay analyzers market size in 2024, but oncology testing is projected to grow at 8.84% CAGR.

- Mid-range systems (101–300 tests/h) covered 44.85% of the installed base in 2024, while low-throughput models (≤100 tests/h) are poised for 6.68% CAGR.

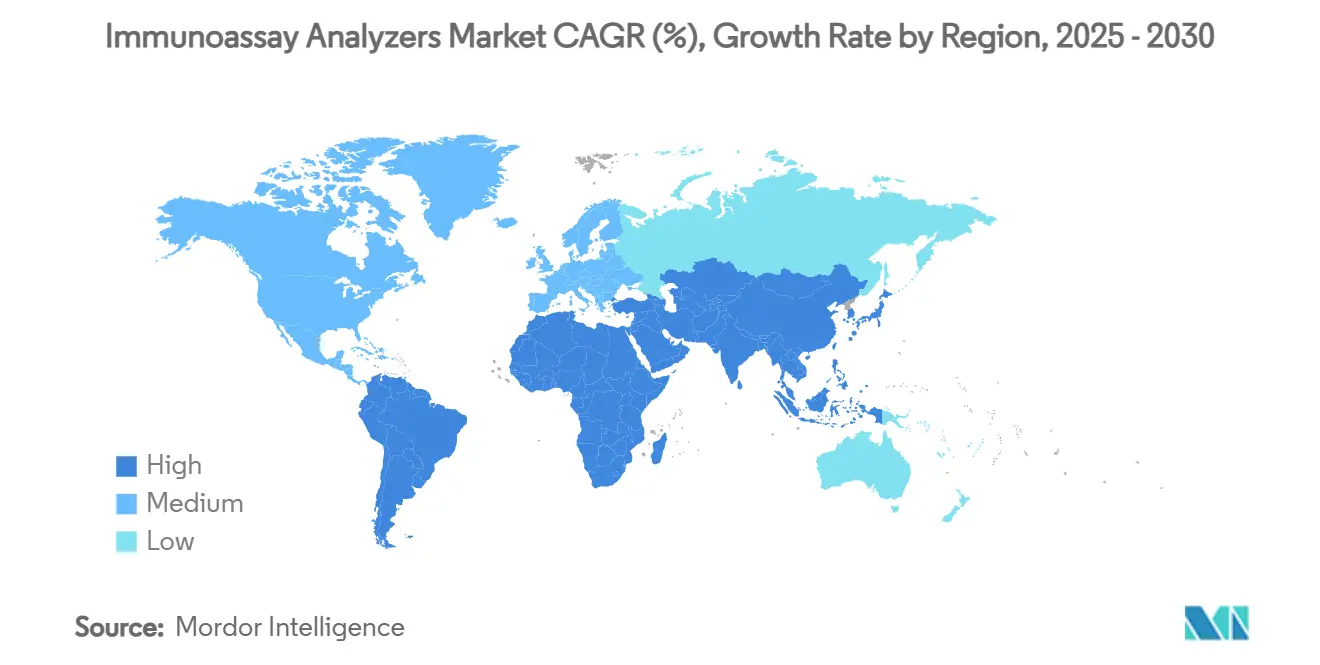

- North America dominated with 36.52% revenue in 2024; Asia-Pacific is forecast to register the fastest 6.26% CAGR.

Global Immunoassay Analyzers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of chronic & infectious diseases | +1.2% | Global; strongest in aging populations of North America & Europe | Long term (≥ 4 years) |

| Automation & high-throughput platform advances | +0.8% | North America & EU lead; Asia-Pacific adoption accelerating | Medium term (2–4 years) |

| Growing adoption of POC & rapid testing | +0.6% | Global; rural and resource-limited settings drive demand | Medium term (2–4 years) |

| AI-driven calibration cutting QC downtime | +0.4% | North America & EU early adopters; selective Asia-Pacific markets | Short term (≤ 2 years) |

| Companion-animal diagnostics demand surge | +0.3% | North America & Western Europe primary markets | Medium term (2–4 years) |

| Broadening test menus in oncology, cardiac & fertility | +0.5% | Global; developed markets spearhead adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising incidence of chronic & infectious diseases

Higher prevalence of cardiovascular, metabolic and neurodegenerative disorders is translating into routine use of high-sensitivity troponin, NT-proBNP and novel neuro-biomarkers in emergency and outpatient settings. Beckman Coulter’s 2025 research-use-only assays for p-Tau217, GFAP and NfL illustrate how immunoassay platforms are moving into neurology to replace invasive sampling techniques. Infectious-disease menus remain robust even after the pandemic, and multiplex cartridges now deliver simultaneous pathogen identification that limits empirical antibiotic use. Hospitals are also adding cardiotoxicity panels to oncology pathways, using immunoassay data to prevent therapy-induced heart failure.[1]Lisa B. Leypoldt, “Cardiac Biomarkers for Risk Stratification in Newly Diagnosed High-Risk Multiple Myeloma in the GMMG-CONCEPT Trial,” Cardio-Oncology, bmconcology.biomedcentral.com As preventive screening gains policy support, payers increasingly reimburse biomarker panels that detect disease earlier and ultimately lower long-term treatment costs.

Automation & high-throughput platform advances

Vacancy rates exceeding 25% have turned staffing shortfalls into a systemic bottleneck for clinical laboratories.[2]Siemens Healthineers, “New Survey Reveals Burnout in Clinical Labs Impacts Patient Care, Staff Safety; Optimism That Automation, AI Will Help Tackle Challenges,” Siemens Healthineers, siemens-healthineers.com Siemens Healthineers’ Atellica Solution processes up to 440 tests per hour while predictive algorithms schedule maintenance automatically, allowing “dark lab” operations that require minimal technologist oversight. Industry surveys show 89% of laboratory professionals now regard full automation as essential for sustaining quality under rising workloads. Modern track systems integrate immunoassay and chemistry modules with vision-guided robotic sample handling, ensuring continuous flow and freeing senior staff for complex troubleshooting. Vendors capable of bundling hardware, middleware and cybersecurity features are gaining an edge as laboratories rationalize supplier bases.

Growing adoption of POC & rapid testing

Health-system strategies are shifting care closer to the patient, triggering rapid uptake of handheld and benchtop POCT analyzers that deliver results within 10 minutes. bioMérieux’s 2024 purchase of SpinChip Diagnostics brings a microfluidic cartridge that produces central-lab–grade immunoassay data from whole blood at the bedside. The FDA’s clearance of Pathfast as the first U.S. point-of-care high-sensitivity cardiac troponin assay removes a regulatory barrier that had long restricted such testing to core labs. In low-resource regions, paper-based chips able to detect multiple pathogens on a single strip are reducing per-test reagent spend and cold-chain dependence. Integrated cloud connectivity means POC devices now upload results directly to electronic health records, closing data gaps and supporting antibiotic-stewardship dashboards.

AI-driven calibration cutting QC downtime

Machine-learning models embedded in modern analyzers track drift in real time, adapt calibration intervals dynamically and alert engineers before performance falls outside allowable limits. Continuous quality-monitoring modules already adjust for reagent lot changes and ambient-temperature swings without interrupting workflow.[3]Miguel A. Santos-Silva, “Artificial Intelligence in Routine Blood Tests,” Frontiers in Medical Engineering, frontiersin.org Early data show handwriting-recognition engines convert paper requisitions into orders with 99.9% accuracy after human verification, eliminating a previously manual bottleneck. Predictive service dashboards prioritize field visits based on component-failure probability, reducing unplanned downtime in multisite lab networks. This AI layer is particularly valuable for consolidated reference labs running mixed specialty menus where each minute of downtime results in thousands of delayed reports.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & reagent costs | –0.7% | Global; particularly restrictive in cost-sensitive markets | Long term (≥ 4 years) |

| Stringent regulatory approvals & compliance | –0.5% | North America & EU feel strongest effects; global trickle-down | Medium term (2–4 years) |

| Geo-political reagent-supply volatility | –0.4% | Global supply chains; risk magnified where single-source inputs | Short term (≤ 2 years) |

| Acute laboratory workforce shortage | –0.6% | North America & EU acute; Asia-Pacific trending upward | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High capital & reagent costs

Acquiring a high-throughput analyzer can exceed USD 500,000, while reagent and service contracts create ongoing financial commitments that deter small laboratories. Recent shortages of BD blood-culture bottles underscore how a single reagent disruption can ripple across clinical workflows, forcing rationing or test deferrals. Laboratories also carry the risk of lot-to-lot variability in critical antibodies; if a lot fails verification, repeat studies consume staff hours and materials. Platforms such as Bio-Techne’s Ella demonstrate that microfluidic cartridge designs can lower per-reportable costs by USD 2.78 and cut sample volume requirements by nearly 90%, but widespread migration is slow because legacy ELISA readers remain fully depreciated.

Stringent regulatory approvals & compliance

The FDA’s Laboratory Developed Tests (LDT) rule shifts thousands of assays into the medical-device framework by 2028, elevating documentation, performance-verification and post-market-surveillance requirements. Europe’s IVDR adds a similar compliance load, with early adopters warning that validation and post-market oversight exceed original resource estimates. China’s new device law also tightens import registration and quality-system audits, increasing the cost of regional launches. Although these regimes strengthen patient safety, they disproportionately burden start-ups that lack dedicated regulatory staff and funding.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Portable Platforms Challenge Traditional Dominance

Standalone and integrated systems anchored 46.72% immunoassay analyzers market share in 2024, a position built on broad menus and consolidated purchasing by hospital groups. Vendors continue to refresh these flagships with bidirectional middleware links and automated maintenance features that keep cost-per-test competitive. Portable and POC analyzers, however, are projected to post an 8.67% CAGR, outpacing all other product classes as emergency departments, ambulatory centers and rural clinics pivot toward immediate decision-support models. The immunoassay analyzers market size for POC platforms is therefore forecast to close the decade at more than double its 2024 level. bioMérieux’s SpinChip buyout demonstrates how microfluidic cartridges and smartphone readouts can bring laboratory-grade precision to handheld devices while enabling connectivity to cloud-based informatics hubs.

Benchtop analyzers remain the middle ground, finding favor in community hospitals and private labs that require daily throughput below 150 samples yet need the flexibility of 50-plus reagent positions. Vendors now offer modular add-ons—such as chilled reagent rings and auto-dilution modules—that extend menu depth without pushing facilities into full-scale floor-standing footprints. As a result, the immunoassay analyzers market continues to diversify, with purchasing decisions driven less by instrument class and more by a site’s strategic emphasis on decentralization, staffing and capital constraints.

By Technology: ELISA Dominance Faces Multiplex Disruption

ELISA accounted for 63.42% of the immunoassay analyzers market size in 2024 because laboratories trust its well-documented performance characteristics and reimbursement coding. Yet growth shifts toward multiplex and microfluidic systems, projected at 7.25% CAGR, as payers increasingly reward panels that deliver comprehensive answers from a single draw. Immunoassay analyzers market share for multiplex platforms could therefore reach low-double-digit territory by 2030. Chemiluminescent systems keep traction in core labs that prize speed and sub-pg/mL sensitivity for sepsis and cardiac panels, while fluorescence readers cater to neonatal and allergen testing where minute sample volumes are mandatory.

Microfluidic breakthroughs such as paper-in-polymer-pond plates push detection limits below 0.3 ng/mL for cancer markers, eclipsing standard ELISA kits on both sensitivity and turnaround. Machine-learning code natively embedded in assay cartridges now self-corrects for lot variance and temperature drift, meaning operators no longer recalibrate after each batch. These advances signal a gradual, rather than sudden, hand-off: ELISA remains the workhorse, but multiplex systems are carving out high-value niches and laying groundwork for eventual mainstream adoption.

By End User: Veterinary Segment Emerges as Growth Driver

Hospital laboratories retained 51.33% share in 2024 thanks to consolidated purchasing under integrated-delivery networks and stable reimbursement for inpatient diagnostics. Reference centers likewise expand footprints as smaller clinics outsource specialized assays that local staff cannot validate under new regulatory rules. Yet veterinary clinics register the highest 7.05% CAGR through 2030, propelled by rising pet-care spending and regulatory moves that tighten quality expectations for companion-animal testing. Immunoassay analyzers market size gains here are amplified because veterinary clinics previously relied on send-out models; each in-house placement represents incremental capital and reagent revenue.

POC devices appeal to urgent-care centers and outpatient specialists aiming to cut admission-to-treatment cycles, while pharmaceutical R&D groups deploy high-sensitivity systems for pharmacokinetic readouts. The breadth of end-user adoption illustrates how the immunoassay analyzers market adapts to divergent workflow needs without diluting core performance standards.

By Application: Oncology Applications Accelerate Beyond Traditional Testing

Infectious-disease assays generated 44.23% revenue in 2024, anchored by hospital stewardship programs and mandatory surveillance for viral hepatitis, HIV and respiratory pathogens. However, oncology panels are on track for an 8.84% CAGR, surpassing every other application segment. This acceleration stems from precision-therapy protocols that require pre-treatment stratification and on-treatment toxicity monitoring. Immunoassay analyzers market size for oncology is therefore projected to outpace that of cardiology, which nonetheless remains a mainstay because guidelines mandate troponin testing for chest-pain triage.

Endocrinology, autoimmune and allergy panels grow steadily as primary-care models embrace preventative hormone and allergen screens. Meanwhile, multi-analyte reflex algorithms bundle cardiac and inflammatory markers to improve rule-out accuracy for coronary syndromes. This convergence further broadens the addressable reagent pool and keeps analyzer utilizations high, reinforcing vendor recurring-revenue streams.

By Throughput Capacity: Low-Volume Systems Gain Traction

Mid-range instruments, delivering 101-300 tests per hour, held 44.85% of 2024 placements due to their suitability for regional hospitals that balance scale with staffing limits. High-throughput architectures continue to dominate mega-labs but face slowing incremental demand because most consolidation projects already replaced legacy analyzers. Low-throughput platforms are predicted to expand at 6.68% CAGR as POC and satellite labs prioritize rapid answers over bulk capacity. Revvity’s FDA-cleared free-testosterone analyzer processes 60 tests per hour yet offers 48-minute results, proving that specialized, low-volume devices can justify investment when clinical impact is clear.

The immunoassay analyzers market share mix is thus tilting toward a bimodal distribution: very high-volume core sites and widely distributed low-throughput nodes, both feeding data back into unified laboratory-information systems.

Geography Analysis

North America accounted for 36.52% revenue in 2024, underpinned by entrenched reimbursement pathways, rapid AI adoption and recent government funding to bolster domestic diagnostic production. The United States Laboratory Developed Tests rule, effective July 2024, introduces short-term compliance costs but ultimately stabilizes quality expectations, benefiting vendors with mature regulatory affairs departments. Canada and Mexico support regional demand through health-system modernization and expanded insurance coverage, although capital spending cycles differ.

Asia-Pacific is set to deliver the fastest 6.26% CAGR through 2030. China’s updated device law and “Made in China 2025” priorities encourage local manufacturing, even as higher validation thresholds lengthen time-to-market for foreign OEMs. Japan continues to pilot blood-based Alzheimer’s assays, demonstrating regional appetite for high-innovation products. India’s new marketing code formalizes ethical promotion and boosts confidence among clinicians adopting immunoassay platforms for tertiary care. The immunoassay analyzers market size for Asia-Pacific is therefore expected to close the forecast period approaching North American levels, albeit with different product-mix characteristics favoring compact analyzers.

Europe maintains steady growth despite IVDR-related paperwork peaks that momentarily stretched laboratory resources. Aging demographics sustain chronic-disease testing volumes, and public payers increasingly fund multiplex oncology panels to limit downstream treatment costs. South America and the Middle East & Africa remain nascent, but economic-development programs and private-sector hospital chains create footholds for vendors offering tiered-pricing models.

Competitive Landscape

The immunoassay analyzers market is moderately consolidated: the top five suppliers control just under two-thirds of global revenue, yet niche entrants specializing in robotics, reagent innovation or AI software are eroding legacy moats. Incumbents hedge by acquiring capability: BD will merge with Waters in a USD 17.5 billion deal that unites chemistry, mass-spectrometry and immunoassay strength. Roche has already folded LumiraDx’s point-of-care technology into its cobas ecosystem to address decentralized testing limits. bioMérieux’s SpinChip purchase highlights a willingness to pay premium multiples for disruptive microfluidics that compress result times to under 10 minutes.

Strategic themes center on integrating middleware, cybersecurity and predictive-maintenance dashboards into bundled offerings. Supply-chain resilience is another differentiator: firms investing in dual-sourcing and regional reagent plants won market share during 2024 shortages. Veterinary diagnostics offer a comparatively greenfield opportunity with lower competitor density and faster assay-approval cycles. Differentiation now hinges on menu depth, workflow automation and software analytics rather than raw analytical sensitivity alone.

Immunoassay Analyzers Industry Leaders

bioMérieux

Danaher

Siemens Healthineers

Abbott Laboratories

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- 2025: Zoetis opened a reference laboratory in Louisville, Kentucky, adding real-time specimen tracking and broad test menus to its U.S. network.

- April 2025: Thermo Fisher Scientific committed USD 2 billion to expand domestic manufacturing and R&D focused on high-impact innovation.

- March 2025: The FDA cleared Beckman Coulter’s DxC 500i Clinical Analyzer, broadening access to its integrated chemistry-immunoassay platform.

- January 2025: Anbio Biotechnology launched the ADL-1000 dry-chemiluminescence analyzer, targeting faster, cost-efficient workflows.

Global Immunoassay Analyzers Market Report Scope

| Standalone / Integrated Systems |

| Benchtop Analyzers |

| Portable / POC Analyzers |

| ELISA |

| CLIA |

| FIA |

| RIA |

| Multiplex / Microfluidic |

| Hospital Laboratories |

| Reference & Diagnostic Centers |

| Point-of-Care Settings |

| Veterinary Clinics & Labs |

| Pharma & Biotech R&D |

| Infectious Disease Testing |

| Oncology |

| Cardiology |

| Endocrinology |

| Autoimmune & Allergy |

| Low (≤100 tests/hr) |

| Mid (101–300 tests/hr) |

| High (>300 tests/hr) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Standalone / Integrated Systems | |

| Benchtop Analyzers | ||

| Portable / POC Analyzers | ||

| By Technology | ELISA | |

| CLIA | ||

| FIA | ||

| RIA | ||

| Multiplex / Microfluidic | ||

| By End User | Hospital Laboratories | |

| Reference & Diagnostic Centers | ||

| Point-of-Care Settings | ||

| Veterinary Clinics & Labs | ||

| Pharma & Biotech R&D | ||

| By Application | Infectious Disease Testing | |

| Oncology | ||

| Cardiology | ||

| Endocrinology | ||

| Autoimmune & Allergy | ||

| By Throughput Capacity | Low (≤100 tests/hr) | |

| Mid (101–300 tests/hr) | ||

| High (>300 tests/hr) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current size of the immunoassay analyzers market?

The immunoassay analyzers market size reached USD 7.77 billion in 2025.

2. How fast is the immunoassay analyzers market expected to grow?

It is forecast to expand at a 4.21% CAGR, reaching USD 9.55 billion by 2030.

3. Which product segment is growing the quickest?

Portable and point-of-care analyzers are projected to record the fastest 8.67% CAGR through 2030.

4. Why are oncology applications gaining momentum?

Precision-medicine protocols require multiplex biomarker panels, driving an 8.84% CAGR in oncology immunoassay testing demand.

5. What regions are likely to see the strongest growth?

Asia-Pacific is expected to post the highest 6.26% CAGR thanks to expanding healthcare infrastructure and supportive regulatory reforms.

Page last updated on: