Subcutaneous Immunoglobulin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

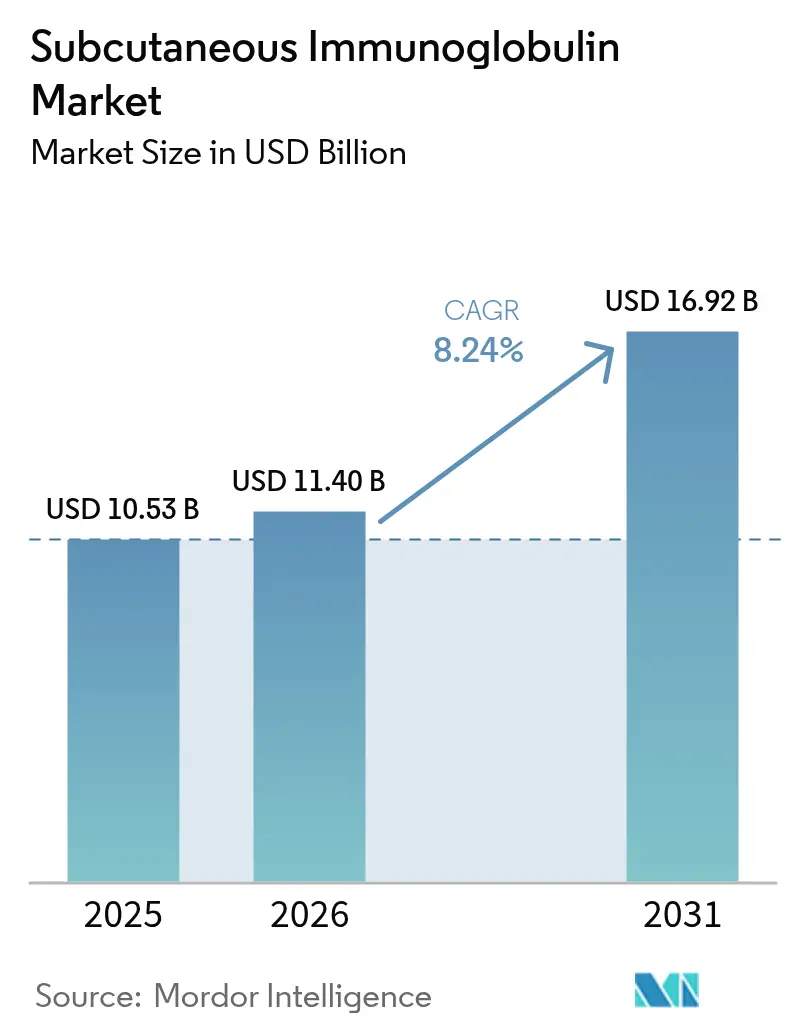

| Market Size (2026) | USD 11.4 Billion |

| Market Size (2031) | USD 16.92 Billion |

| Growth Rate (2026 - 2031) | 8.24% CAGR |

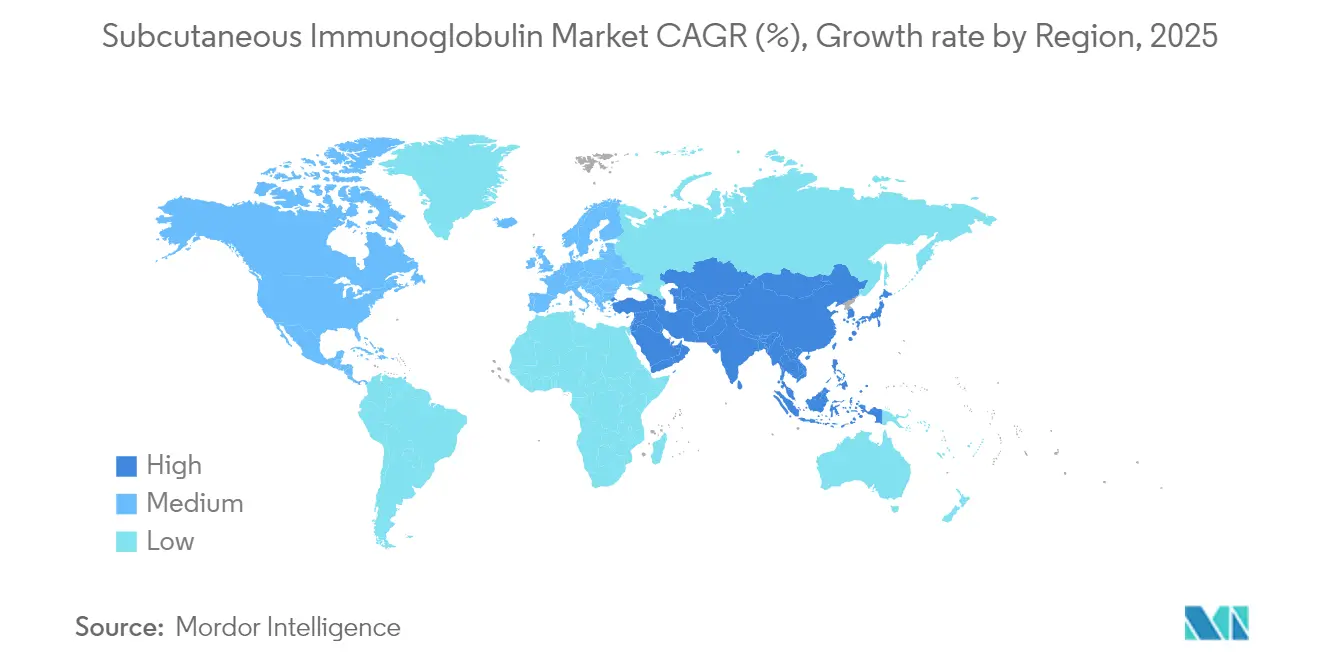

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Subcutaneous Immunoglobulin Market Analysis by Mordor Intelligence

The subcutaneous immunoglobulin market size was valued at USD 10.53 billion in 2025 and estimated to grow from USD 11.4 billion in 2026 to reach USD 16.92 billion by 2031, at a CAGR of 8.24% during the forecast period (2026-2031). Patient preference for self-managed therapy, improved infusion technologies, and payer support for home care together sustain a demand curve that remains comfortably above global plasma-collection capacity. Primary immunodeficiency continues to anchor demand because earlier diagnosis broadens the treated population, while neurological and hematologic conditions steadily push beyond niche status. Facilitated formulations extend the addressable base by compressing a month of therapy into one session, a feature that improves adherence and reduces indirect costs. Geographically, North America retains consumption leadership, yet the Asia–Pacific trajectory rises more steeply as Japan, China, and Australia clear new products and streamline reimbursement pathways. Manufacturers respond to chronic plasma scarcity with yield-enhancement processes, fractionation expansion, and partnerships that shorten supply chains.

Key Report Takeaways

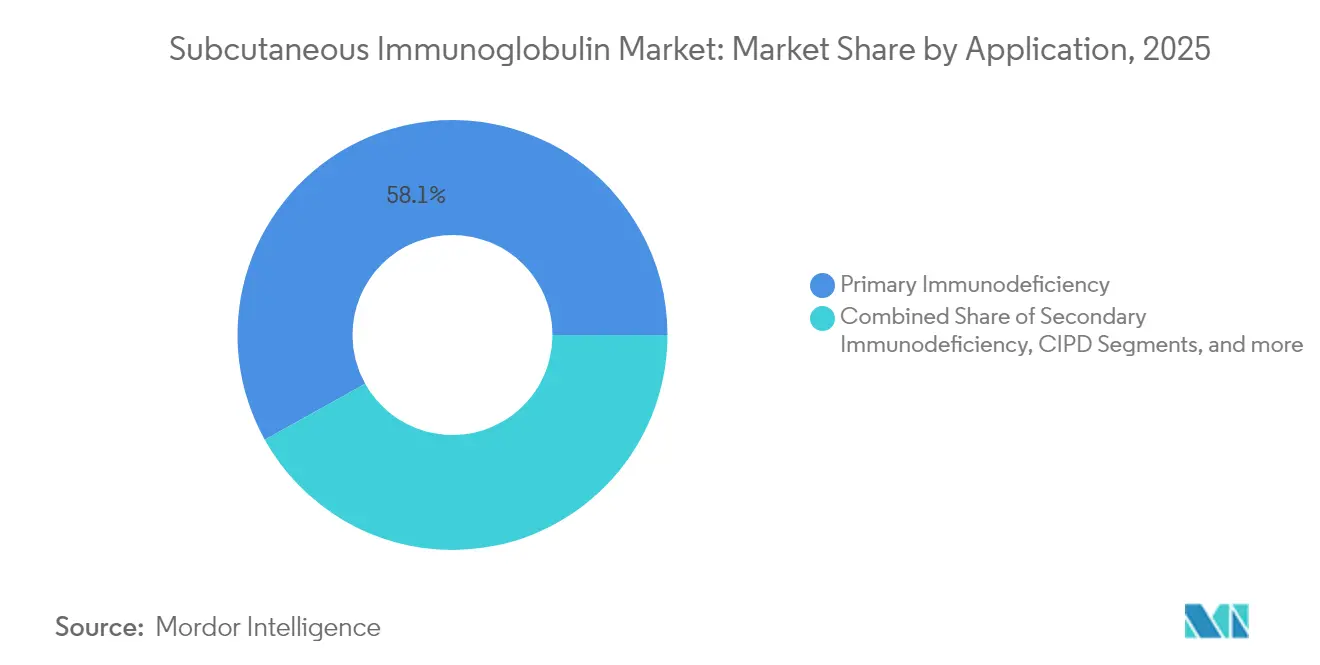

- By application, primary immunodeficiency held 58.10% of subcutaneous immunoglobulin market share in 2025 and is expanding at an 8.86% CAGR through 2031.

- By administration technique, conventional pump delivery led with 48.05% revenue share in 2025, while facilitated therapy is advancing at an 8.76% CAGR to 2031.

- By geography, North America captured 40.85% revenue in 2025; Asia–Pacific is forecast to grow at a 8.98% CAGR through 2031.

- By distribution channel, hospital pharmacies accounted for 39.30% share of the subcutaneous immunoglobulin market size in 2025 and are growing at an 8.79% CAGR.

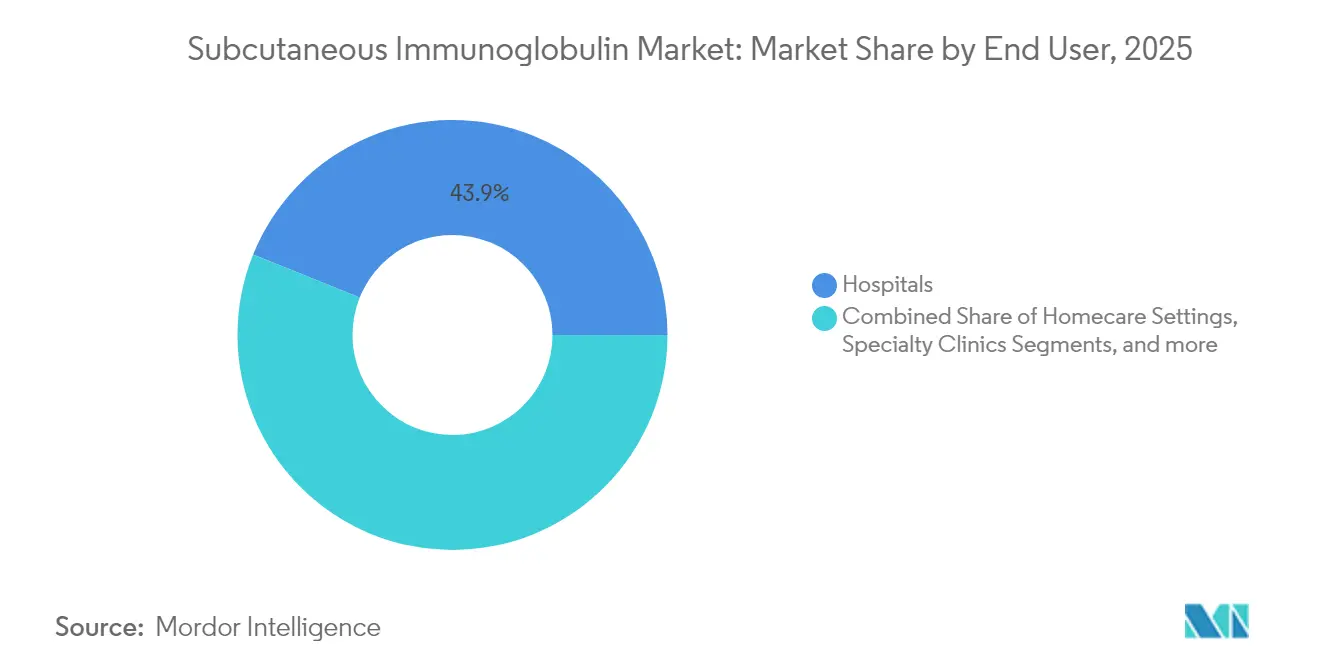

- By end user, hospitals retained 43.90% revenue share in 2025, while homecare settings show the highest projected growth at 8.47% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Subcutaneous Immunoglobulin Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of primary immunodeficiency disorders (PID) | +1.8% | Global, with higher impact in developed markets | Long term (≥ 4 years) |

| Shift from IVIG to home-based SCIG administration | +2.1% | North America & EU leading, APAC following | Medium term (2-4 years) |

| Aging population & rising chronic disease burden | +1.5% | Global, concentrated in developed economies | Long term (≥ 4 years) |

| Expanding reimbursement & plasma-collection programs | +1.2% | Regional, with UK and US initiatives | Medium term (2-4 years) |

| Hyaluronidase-facilitated high-volume fSCIG adoption | +0.9% | North America & EU primarily | Short term (≤ 2 years) |

| Decentralised plasma sourcing initiatives | +0.8% | UK, Australia, select EU markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Primary Immunodeficiency Disorders Drives Market Expansion

Improved screening algorithms embedded in large electronic-health-record systems now identify 6 in 10,000 individuals with inborn errors of immunity, well above earlier assumptions. More accurate epidemiology means physicians prescribe replacement therapy earlier, which lengthens a patient’s lifetime exposure to subcutaneous products. Hospital data place the average cost of admission for severe infections at USD 122,739, a level that persuades insurers to fund preventive immunoglobulin therapy. Parallel discoveries of immune deficits in Down syndrome and other syndromic conditions widen the treated population. COVID-19 experience further supports prophylactic IgG use for vulnerable groups as they transition from pandemic to endemic risk. Together these factors elevate baseline demand and stabilize year-on-year volume growth for the subcutaneous immunoglobulin market.

Patient Preference Accelerates IVIG-to-SCIG Migration

Survey data show that 82% of patients prefer subcutaneous delivery and 84% favor home administration, citing autonomy and reduced travel burden. Real-world studies confirm equal efficacy alongside fewer systemic reactions, particularly in chronic neuromuscular conditions. Health-economic analyses reveal that nurses spend 35 hours per patient annually on subcutaneous support versus significantly higher labor for intravenous regimens. Pre-filled syringes, manual push options, and small portable pumps remove the technical hurdles that once confined therapy to infusion suites. These combined conveniences channel a steady stream of new starters directly into the subcutaneous immunoglobulin market.

Aging Demographics and Chronic Disease Burden Expand Treatment Population

The number of adults living past 65 years rises every year, and with age comes secondary hypogammaglobulinemia triggered by hematologic malignancies or immunosuppressive therapies. Infection-related hospitalizations fall from 2.3 to 0.9 per person-year once subcutaneous therapy begins, a clinical outcome that speaks directly to payers focused on avoidable admissions. Chronic inflammatory demyelinating polyneuropathy joins the reimbursement list in many countries after regulators cleared immunoglobulin for long-term maintenance. As similar neurological conditions gain evidence packages, cumulative volume requirements for immunoglobulin replacement expand. The demographic swell therefore embeds structural growth inside the subcutaneous immunoglobulin market well beyond the primary immunodeficiency core.

Hyaluronidase-Facilitated Therapy Transforms Administration Paradigms

HYQVIA combines recombinant human hyaluronidase with 10% immunoglobulin to enable 300-600 mg/kg monthly dosing in a single two-hour session. Phase 3 evidence shows serum IgG trough levels match weekly conventional therapy, while reduced infusion frequency improves adherence metrics. Japan’s approval in December 2024 signals Asia–Pacific alignment with US and EU practice, and local training modules now standardize the dual-component infusion process. Economic models indicate that fewer visits offset higher drug acquisition costs when indirect patient productivity gains are counted. As additional countries authorize facilitated formulations, monthly schedules become a mainstream expectation rather than a niche option.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory & quality requirements | -1.1% | Global, with varying intensity by region | Long term (≥ 4 years) |

| High therapy cost & reimbursement friction | -0.9% | US primarily, selective EU markets | Medium term (2-4 years) |

| Global plasma supply constraints | -1.3% | Global, acute in developing markets | Short term (≤ 2 years) |

| Emerging FcRn-inhibitor biologics as substitutes | -0.7% | Developed markets initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Plasma Supply Constraints Challenge Market Growth Sustainability

Every liter of plasma requires 7-12 months of fractionation before a dose reaches the patient, so even modest demand increments strain inventories. Governments act: the United Kingdom moved from 0% to 25% plasma self-sufficiency by 2025 and targets 30-35% by 2031. Manufacturers upgrade processes, and ADMA Biologics filed for a 20% yield enhancement that uses optimized chromatography and virus-filtration steps. Yet collection policy changes in major donor countries still cap growth, and regional shortfalls appear first in developing economies with limited fractionation capacity. The subcutaneous immunoglobulin market therefore relies on continuous innovation to stretch each liter of plasma further.

FcRn-Inhibitor Biologics Emerge as Competitive Threat

Efgartigimod, batoclimab, rozanolixizumab, and nipocalimab block the neonatal Fc receptor, accelerating pathogenic IgG catabolism without wholesale IgG replacement. Early trials in myasthenia gravis and immune thrombocytopenia show rapid disease-score improvements with subcutaneous self-injection schedules. If larger studies confirm safety and durability, these agents could substitute immunoglobulin in more than 100 IgG-mediated conditions. Their targeted mechanism may lower infusion volume and cost, factors that resonate with both patients and payers. Consequently, innovators inside the subcutaneous immunoglobulin market monitor FcRn pipelines closely when shaping long-term capacity plans.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Expanding Immunodeficiency and Neurology Portfolio Fuels Growth

Primary immunodeficiency held 58.10% revenue in 2025 and is advancing at an 8.86% CAGR, underpinning the largest slice of the subcutaneous immunoglobulin market. Greater physician awareness, newborn screening pilots, and genomic testing converge to catch patients earlier, which extends therapy lifespan. Secondary immunodeficiency linked to chemotherapy, stem-cell transplant, and antirheumatic medications adds a sizeable cohort that previously relied on hospital IVIG infusions. Neurological applications are rising fastest because chronic inflammatory demyelinating polyneuropathy and multifocal motor neuropathy have secured guideline support for maintenance dosing. Regulatory clearance of GAMMAGARD LIQUID for CIDP in adults widened payer recognition in 2025. Emerging research on autoimmune encephalitis and stiff-person syndrome further enlarges the potential pool. Precision-medicine initiatives use serum biomarker panels and machine-learning algorithms to stratify patients for subcutaneous versus intravenous routes. This data-guided matching optimizes resource allocation and improves adherence, ensuring that subcutaneous immunoglobulin market growth remains patient-centric.

Segment diversity secures resilience. When plasma scarcity limits volume allocation, manufacturers can redistribute supply toward high-value neurology segments without abandoning core immunodeficiency users. Hospitals, clinics, and home-care services align educational content to reflect the broader indication mix, reducing mis-administration risks. As the treated base widens, real-world evidence networks collect safety, efficacy, and quality-of-life outcomes that feed back into payer dossiers. The feedback loop strengthens contract negotiations and secures formulary placement. Overall, application breadth transforms the subcutaneous immunoglobulin industry into a versatile treatment platform rather than a single-use product line.

By Administration Technique: Facilitated Therapy Reshapes User Expectations

Conventional pump infusion retained 48.05% revenue share in 2025 on the strength of entrenched clinical protocols and broad device availability. The method remains favored for children and patients with limited manual dexterity because programmable flow rates minimize infusion-site discomfort. That said, facilitated therapy is scaling quickly at an 8.76% CAGR on the back of hyaluronidase-enabled monthly dosing. Patients who struggled with weekly schedules migrate to one-day-per-month regimens, freeing time and cutting peripheral-catheter consumables. Rapid push, a syringe-driven manual technique, appeals to adults who prefer complete control and minimalist equipment. Comparative studies report non-inferior pharmacokinetics across these techniques, empowering physicians to tailor choices to patient lifestyle.

Device firms innovate in parallel. Wearable on-body injectors under clinical evaluation aim to combine large-volume capacity with discreet form factors. Smart-phone apps log infusion data and push reminders that support adherence. Training modules delivered through augmented reality reduce the initial learning curve and shorten hospital chair time at initiation. Regional practice patterns differ: North America deploys the full menu of techniques, Europe increasingly favors facilitated therapy for adults, and Asia–Pacific installs new-generation pumps capable of high-volume, low-pressure infusions following HYQVIA approval. Collectively, technique diversity underpins sustained depth in the subcutaneous immunoglobulin market.

By End User: Homecare Expansion Rebalances Channel Dynamics

Hospitals still commanded 43.90% revenue in 2025 because complex initiation protocols, dose titration, and comorbidity management often begin in tertiary centers. However, once dosing is stabilized, homecare settings register the highest growth at 8.47% CAGR as payers reimburse nursing visits and remote monitoring kits. Specialty neurology and immunology clinics benefit from dedicated infusion suites that accommodate both pump and facilitated sessions, capturing volume displaced from busy hospital wards. Long-term care facilities adopt subcutaneous protocols to lower infection-control risks tied to peripheral access devices. Telemedicine platforms integrate video checks and electronic symptom diaries, which reassure prescribers that remote patients maintain safety standards.

This shift redistributes logistics. Specialty distributors deliver temperature-controlled product directly to patients, while digital tools schedule nurse visits during induction and periodic follow-up. Hospitals respond by partnering with home-infusion firms rather than losing the revenue entirely. The result is a hybrid ecosystem where initial prescribing authority stays with the physician, but day-to-day administration migrates outside institutional walls. That hybrid structure broadens the subcutaneous immunoglobulin market by removing distance and scheduling barriers that once deterred therapy uptake.

By Distribution Channel: Hospital Pharmacies Retain Volume Leadership

Hospital pharmacies held 39.30% of total sales in 2025 and are growing fastest at 8.79% CAGR because they govern formulary access, manage prior-authorization workflows, and negotiate bulk contracts that guarantee supply stability. Retail chains invest in dedicated biologic hubs, yet limited shelf life and cold-chain demands restrict wide-scale rollout. Online pharmacies attract tech-savvy, stable patients, but variable state regulations and shipping constraints limit penetration.

Specialty pharmacies fill the gap. For example, KabaFusion secured a limited distribution deal for ALYGLO in 2024, offering tailored nurse support and 24-hour adverse-event hotlines. These providers build inventory management algorithms that forecast needs based on refill cadence, thus minimizing waste. Whichever channel ships the product, end-to-end traceability is mandatory under new drug-supply-chain-security rules in the United States and European Union. Compliance pushes smaller outlets to partner with larger wholesalers, enhancing the resilience of the subcutaneous immunoglobulin market supply network.

Geography Analysis

North America owns 40.85% revenue because the United States diagnoses roughly 150,000-200,000 primary immunodeficiency patients and maintains extensive home-infusion benefits under both commercial plans and Medicare. Canada reimburses therapy through provincial formularies and delivers product via hospital or community programs, while Mexico’s public-sector tenders are enlarging to include subcutaneous options. Recent Medicare rule changes that reimburse nursing time for home infusions further strengthen adoption. Robust plasma-collection infrastructure, predominantly in the United States, guarantees local supply and buffers international shocks.

Europe positions itself as a self-sufficient producer: the United Kingdom reached 25% domestic plasma self-sufficiency in 2025 and targets 30-35% by 2031. Germany operates the largest fractionation capacity, while France, Italy, and Spain prioritize national plasma-collection drives. The European Medicines Agency supports accelerated reviews for facilitated formulations, as evidenced by HYQVIA’s centralized authorization and XEMBIFY’s pan-EU label expansion. COVID-19 supply disruptions prompted investment in strategic plasma reserves, synchronizing public health and industrial policy.

Asia–Pacific is the fastest-growing region at 8.98% CAGR, prompted by Japan’s 2024 HYQVIA approval and widening reimbursement in urban China. Australia’s National Blood Authority supplies product for home administration every two months, embedding subcutaneous formulations into standard care. South Korea leverages its biopharmaceutical ecosystem to push local fractionation projects, while Indonesia attracted inward investment for a first-of-its-kind plasma facility. Challenges include fragmented regulatory frameworks and limited donor networks in emerging markets, but multilateral health-security programs supply technical assistance. The expanding base of qualified fractionation plants lays a durable foundation for the long-term growth of the subcutaneous immunoglobulin market.

Regulatory Landscape

Regulatory Landscape EU and US frameworks continue to shape SCIG commercialization through harmonized quality and clinical evidence requirements. In the EU, the EMA updated its framework in 2026 by adopting Revision 2 of the guideline on clinical investigation of human normal immunoglobulin for subcutaneous and/or intramuscular administration, and publishing the updated core SmPC guideline for SCIg/IMIg (Revision 2), which tightens expectations for study design, labeling, and comparability for lifecycle changes.

In the US, payer policies and FDA precedents influence access beyond approvals. UnitedHealthcare issued a Community Plan medical benefit policy effective July 2026 covering subcutaneous immune globulin, with emphasis on home administration pathways, and Florida Blue updated its immune globulin medical coverage guideline in July 2026. Together, these updates keep formulary positioning, documentation requirements, and site-of-care rules at the center of commercialization strategies for manufacturers pursuing home-based regimens.

Value Chain Analysis

Value Chain Analysis The SCIG value chain starts with plasma collection, testing and fractionation into immunoglobulin, formulation (including high-concentration and facilitated formats), fill-finish, and release testing under rigorous quality systems. A central constraint is the conversion cycle from donation to finished-product release, commonly around 7 to 12 months, which limits how quickly supply can respond to demand shifts. Manufacturers mitigate raw material risk through vertical integration of plasma collection and by pursuing yield-enhancement and process-optimization initiatives.

Downstream, cold-chain logistics, specialty distribution, and clinical support services (training, nursing, remote monitoring) are important for home-use models, while hospitals and specialty pharmacies manage prior authorization and maintain refill cadence. Lifecycle management actions also ripple across the chain. For example, FDA approval of Takeda's GAMMAGARD LIQUID ERC in June 2025 (IV or subcutaneous use) adds a new product to be commercialized starting in 2026, increasing incremental needs for fill-finish capacity, distribution readiness, and payer contracting. In Europe, EMA CHMP activity such as the April 2026 positive opinion on a variation to Privigen highlights how regulatory-controlled manufacturing changes affect supply continuity for immunoglobulin portfolios.

Competitive Landscape

The market exhibits moderate concentration, with Takeda, CSL Behring, Grifols, Octapharma, and Kedrion controlling most volume. Takeda differentiates through HYQVIA, the only monthly dose option, and defends share with post-marketing data that highlight stable IgG troughs and low systemic reaction rates. CSL Behring anchors its portfolio with HIZENTRA, a 20% room-temperature formulation that simplifies travel logistics. Grifols broadened access in 2024 when the FDA cleared XEMBIFY for treatment-naïve patients and biweekly dosing, thereby meeting a gap between weekly conventional and monthly facilitated schedules.

Plasma scarcity shapes strategic moves. ADMA Biologics filed an FDA supplement documenting a 20% yield gain, essentially increasing effective capacity without building new plants. Grifols’ Biotest unit secured FDA approval for YIMMUGO, a facility-sized milestone that lifts group output. Governments push for local fractionation, and manufacturers comply via joint ventures in Asia and Latin America, diversifying risk and defusing export restrictions.

Innovation outside plasma threatens incumbents. FcRn inhibitors led by efgartigimod and batoclimab promise subcutaneous self-injection and disease-specific modulation, bypassing full IgG replacement. Patent filings show cross-license activity in chromatographic purification, virus removal, and stabilizer chemistry. One recent disclosure described a bathophenanthroline-based process that reaches 95% purity and 90% yield, which could undercut established cost structures[4]MDPI Editorial Office, “High-purity immunoglobulin production methods,” MDPI Antibodies, mdpi.com. Collectively these dynamics keep the subcutaneous immunoglobulin market highly active on both technological and policy fronts.

Subcutaneous Immunoglobulin Industry Leaders

Takeda Pharmaceutical Company Limited

Biotest AG

CSL Behring

Grifols, S.A.

Octapharma AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Market Opportunities and Future Outlook Opportunities are closely tied to supply-side investments and process innovations, since plasma availability and fractionation throughput determine product availability. In March 2026, CSL Limited broke ground on a USD 1.5 billion expansion of its Kankakee, Illinois plasma-derived therapies facility, incorporating Horizon 2 yield-enhancing technology, which underscores industry focus on extraction gains and capacity expansion. Grifols then invested EUR 160 million in July 2025 for a new plasma fractionation facility in Lliça de Vall, Spain, aimed at expanding European capacity and resilience.

On the demand and product-differentiation side, facilitated and home-friendly SCIG regimens are widening adoption pathways through less frequent dosing and simpler administration, supported by new devices and advancing pipelines. Takeda introduced HyHub and HyHub Duo infusion devices in the United States in October 2025 for HYQVIA, reinforcing device-enabled adherence and training in homecare settings. A Phase 3 primary immunodeficiency study listing for BP-SCIG 20% (NCT07346859) posted in January 2026 also adds breadth for higher-concentration and facilitated formats, with payer and provider interest connected to portfolio scale and supply reliability.

Recent Industry Developments

- April 2026: Takeda announced a strategic collaboration with a leading contract manufacturing organization to augment fill-finish capacity for subcutaneous immunoglobulin products. The agreement is designed to increase production readiness and support home-based regimens across regions.

- October 2025: Takeda launched HyHub and HyHub Duo infusion devices in the United States for patients prescribed HYQVIA. By expanding device availability for facilitated subcutaneous administration, the company reinforced usability and standardized home-dosing workflows.

- December 2024: Takeda received regulatory approval in Japan for the HYQVIA 10% S.C. Injection Set for patients with agammaglobulinemia or hypogammaglobulinemia. The approval established facilitated subcutaneous immunoglobulin therapy in Japan and expanded access to less frequent, higher-volume subcutaneous dosing. This supported Asia-Pacific market development through a regulator-backed pathway for monthly-style regimens and associated clinical education.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues from commercially licensed human immunoglobulin therapies that are administered through the subcutaneous route, including conventional pump, rapid push, and hyaluronidase-facilitated subcutaneous infusion, across key clinical uses.

Scope exclusions: intravenous or intramuscular immunoglobulins, hyper-immune specialty globulins, and hospital-level compounding are excluded from this sizing.

Segmentation Overview

- By Application

- Primary Immunodeficiency

- Secondary Immunodeficiency

- Chronic Inflammatory Demyelinating Polyneuropathy (CIDP)

- Multifocal Motor Neuropathy (MMN)

- Other Applications

- By Administration Technique

- Conventional Pump

- Rapid Push

- Facilitated (fSCIG) Therapy

- By End User

- Hospitals

- Homecare Settings

- Specialty Clinics & Infusion Centers

- Others

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to anchor the demand pool and to keep the model tied to real world treatment patterns. We reviewed public health and regulatory sources, including US FDA labeling and safety updates, US CDC disease statistics where relevant, NIH PubMed clinical literature for dosing and switching trends, and WHO health system indicators for access signals.

To keep the country picture consistent, pricing and volume assumptions were checked using national reimbursement and health technology assessment publications where available, national statistics offices for demographics, and customs or trade statistics where plasma fractionation flows could be directionally inferred. Company filings, investor presentations, and reputable press were also used to verify therapy focus areas and route of administration priorities, supported by subscriptions that help with company financials, news screening, and patent searches. These examples are not exhaustive, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were run with stakeholders across the SCIG value chain, including manufacturer commercial and medical teams, plasma and fractionation linked experts, distributors, and clinicians or pharmacy leaders involved in immunoglobulin therapy administration. We used these conversations to validate treated patient counts, typical grams per patient per month, shifts toward home care, and how access and reimbursement shape adoption across major regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 16% | APAC: 48% |

| Mid tier: 55% | Functional/Unit leaders: 27% | EMEA: 32% |

| Smaller Players: 19% | Managers: 57% | Americas: 20% |

Market-Sizing & Forecasting

The core model uses a top-down, treated-cohort build up where epidemiology signals for primary and secondary immunodeficiency are translated into diagnosed and treated patients by region, then converted to value using average grams and realized pricing. When the steps are filled in, the market total falls out at the end, rather than being forced at the start.

Key inputs used in the sizing include the share of immunoglobulin patients managed through the subcutaneous route, average grams per patient driven by indication mix, uptake of hyaluronidase-facilitated SCIG versus conventional delivery, home care versus hospital administration split, and regional access factors such as reimbursement coverage and infusion capacity. Selective bottom-up checks corroborate totals, including sanity checks against supplier-level portfolios, sampled country price corridors, and distribution channel mix, while gaps are handled by using proxy adoption curves from comparable markets followed by interview rechecks.

For forecasting, we rely mainly on scenario analysis supported by multivariate regression on a few stable drivers, including diagnosed patient growth, route switching rates, and price progression assumptions in local currency. The final growth path is adjusted only after we reconcile it with what experts expect for supply availability, guideline usage, and payer behavior.

Data Validation & Update Cycle

Outputs are validated through multiple passes that look for mismatches between implied treated patient counts, grams consumed, and country level pricing logic. We also compare regional totals against independent signals such as therapy adoption narratives, regulatory milestones, and the expected direction of home care penetration, and then investigate outliers before sign-off.

Reviews are completed in steps, where assumptions are rechecked, calculations are replicated, and conclusions are reviewed for internal consistency before release. The study is refreshed on an annual cycle, and interim updates are triggered when material events occur, such as major label changes or meaningful access shifts. Before delivery, a final analyst pass is completed so the client receives the latest view available at that time.

Mordor Intelligence's Subcutaneous Immunoglobulin Market Size Compared With Other Published Estimates

Published market sizes for subcutaneous immunoglobulin often do not match because the underlying patient pool, route of administration rules, and what is counted as SCIG revenue can vary across publishers. Differences can also come from the starting year, currency conversion timing, and whether adoption is assumed to accelerate in a straight line or in steps.

The main gap comes from whether adjacent immunoglobulin categories are blended into SCIG and whether non-therapy items are included, where Mordor Intelligence counts only commercially licensed human immunoglobulin delivered subcutaneously (including pump, rapid push, and hyaluronidase-facilitated SCIG) and keeps IV or intramuscular immunoglobulins, hyper-immune globulins, and hospital compounding out of scope.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.40 B (2026) | |

| Global Consultancy A | USD 11.22 B (2024) | Uses an earlier base year and typically applies a broad therapy definition without clearly separating hyaluronidase-facilitated SCIG, which can shift the effective mix and the implied price per gram. |

| Industry Publisher B | USD 11.99 B (2024) | Often treats the market as a wider immunoglobulin replacement pool and may rely on higher treated-patient expansion assumptions over time, with less transparency on grams-per-patient and route switching inputs. |

The table shows that the spread is mostly explained by scope handling and by how demand is translated from patients to grams and then into value. By keeping the sizing steps traceable to treated cohorts, dosing intensity, and administration adoption, we can explain each assumption plainly and adjust it when new evidence shows up.

Key Questions Answered in the Report

What is the current size of the subcutaneous immunoglobulin market?

The market stands at USD 11.4 billion in 2026 and is forecast to reach USD 16.92 billion by 2031.

Which application segment holds the largest share?

Primary immunodeficiency leads with 58.10% revenue in 2025 and remains the fastest-growing segment.

Why is facilitated SCIG therapy gaining popularity?

Hyaluronidase-enhanced formulations enable monthly dosing, lowering infusion frequency and improving adherence without compromising serum IgG levels.

How are plasma supply constraints being addressed?

Manufacturers deploy yield-enhancement technologies and governments invest in local fractionation to increase output and diversify sourcing.

Could FcRn-inhibitor biologics replace immunoglobulin therapy?

Early data show promise for disease-specific autoimmune applications, but large-scale substitution depends on long-term safety, cost, and regulatory acceptance.

Which region is expected to grow fastest through 2031?

Asia–Pacific is projected to expand at a 8.98% CAGR due to recent product approvals and improving reimbursement frameworks.

Page last updated on: