Atherectomy Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

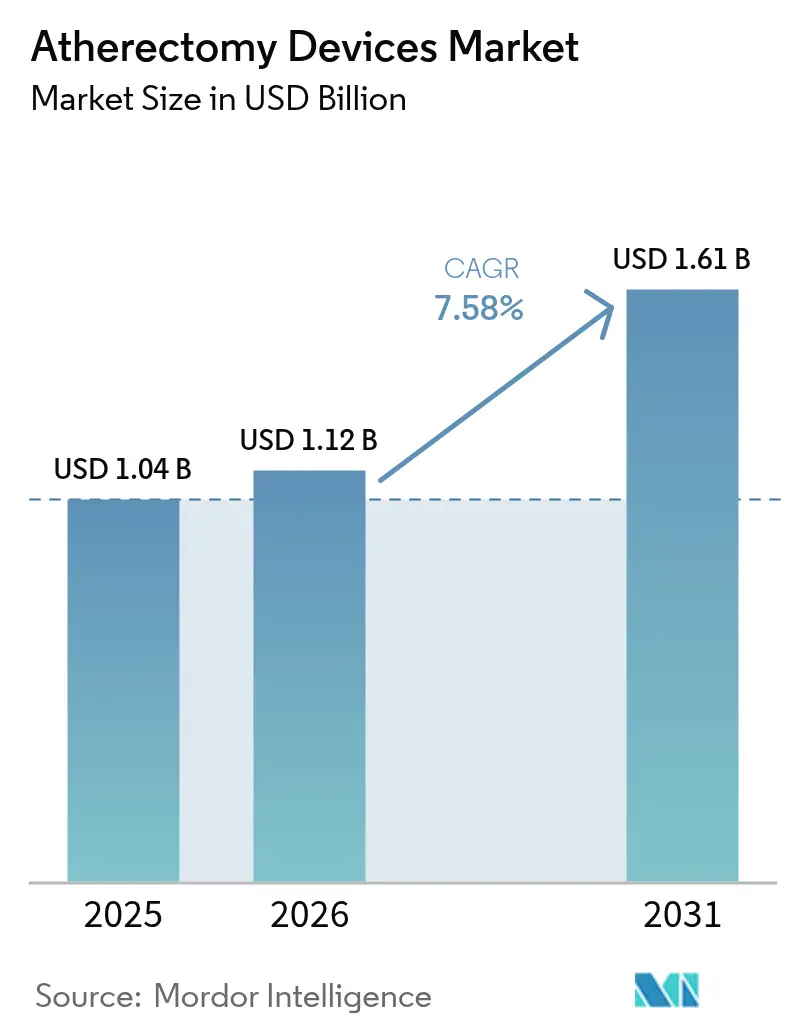

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.61 Billion |

| Growth Rate (2026 - 2031) | 7.58% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Atherectomy Devices Market Analysis by Mordor Intelligence

The atherectomy devices market size was valued at USD 1.04 billion in 2025 and estimated to grow from USD 1.12 billion in 2026 to reach USD 1.61 billion by 2031, at a CAGR of 7.58% during the forecast period (2026-2031). Growing acceptance of minimally invasive plaque-modification techniques, broader clinical use in complex calcified lesions, and favorable reimbursement for office-based laboratory (OBL) procedures in the United States underpin near-term demand. Device makers continue to pair atherectomy systems with drug-coated balloons to improve long-term patency, strengthening the therapy’s value proposition in peripheral vascular disease. Strategic acquisitions by multinational suppliers are consolidating intellectual property and global distribution, while Asia-Pacific localization programs are driving cost efficiencies that could accelerate regional adoption. Nonetheless, mixed evidence on long-term outcome superiority over plain balloon angioplasty, coupled with supply-chain tightness for diamond-coated burrs, tempers the five-year outlook.

Key Report Takeaways

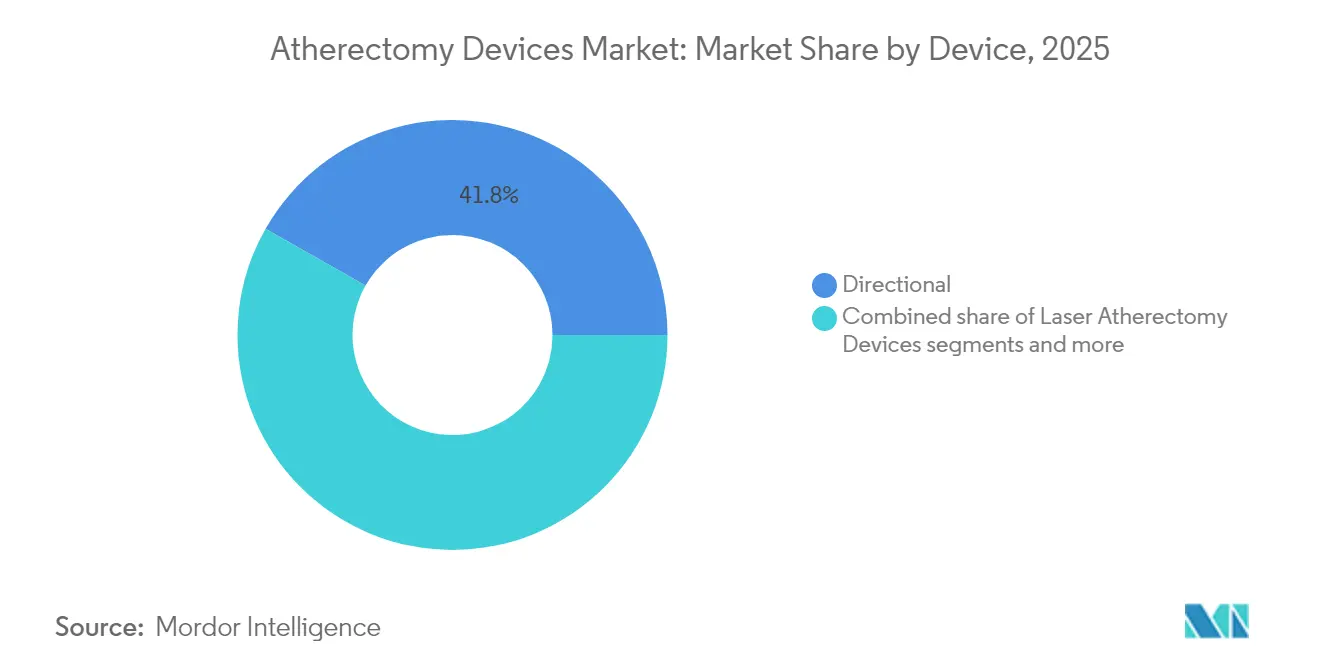

- By device type, directional systems led with 41.78% revenue share of the atherectomy devices market in 2025.

- By application, peripheral vascular disease accounted for 57.45% share of the atherectomy devices market size in 2025, whereas neurovascular procedures are projected to advance at a 7.86% CAGR through 2031.

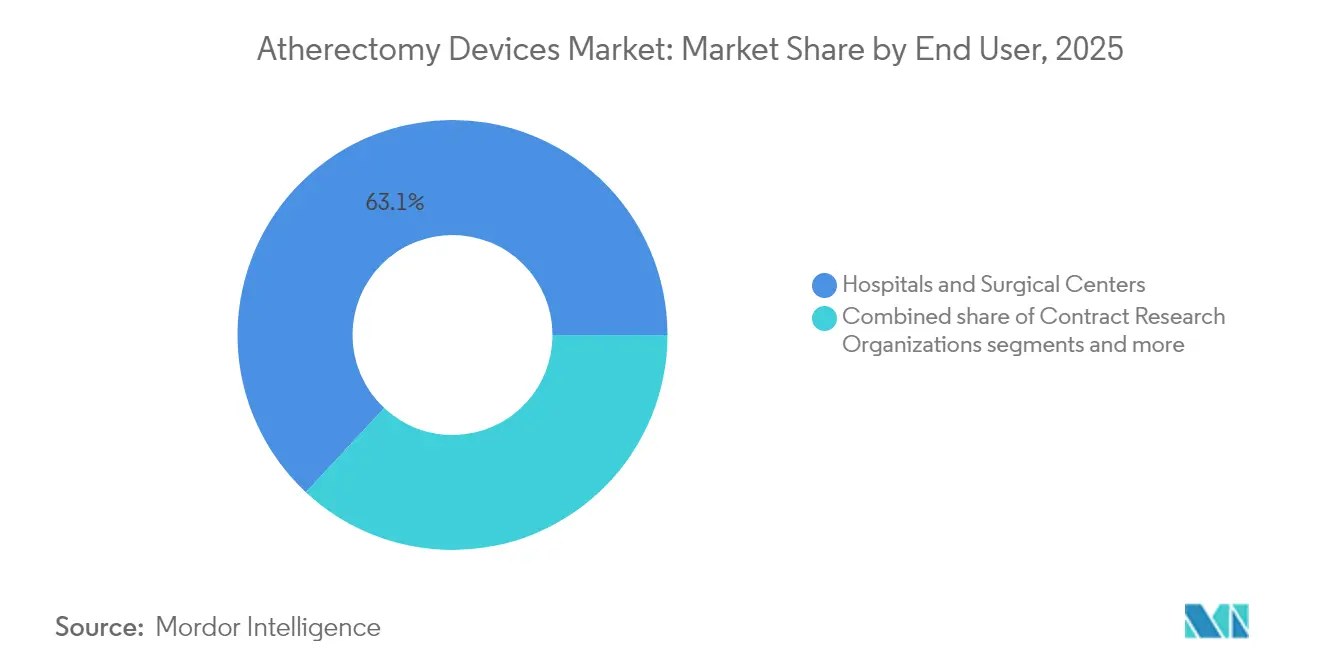

- By end user, hospitals and surgical centers held 63.05% of the atherectomy devices market share in 2025; ambulatory surgical centers are the fastest-growing setting at an 7.93% CAGR to 2031.

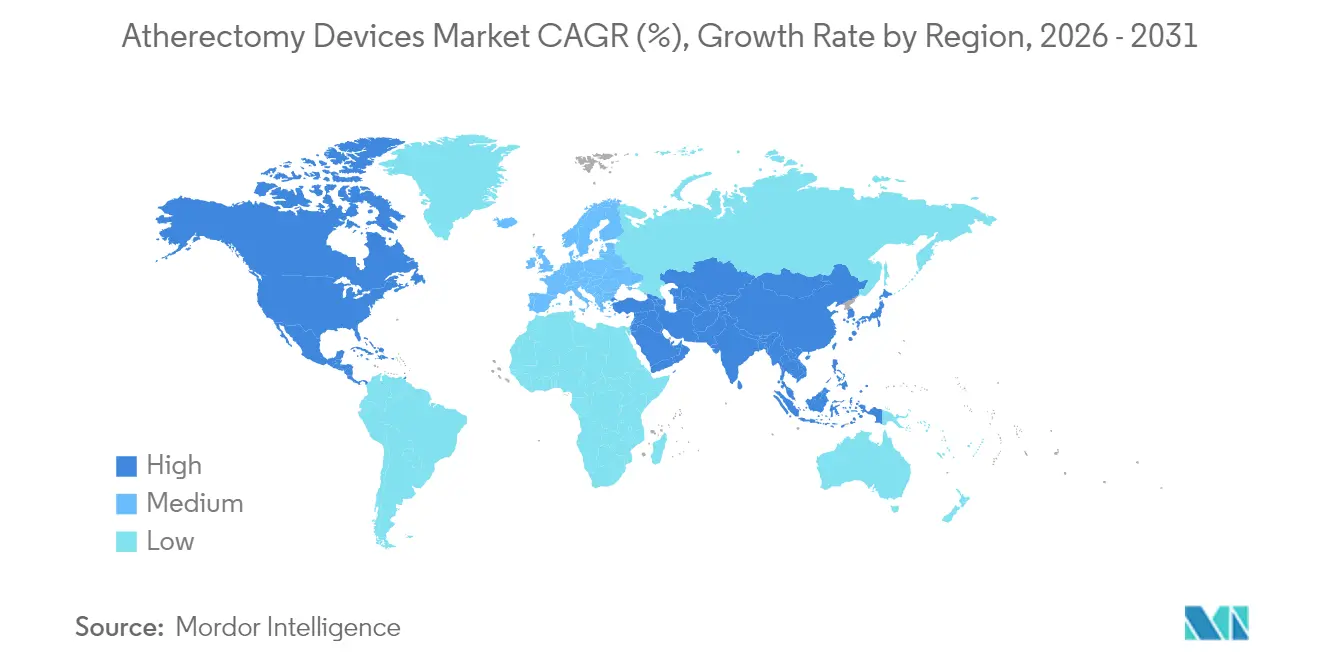

- By geography, North America dominated with 38.74% share in 2025, while Asia-Pacific is forecast to expand at an 8.08% CAGR between 2026 and 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Atherectomy Devices Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of peripheral & coronary artery disease | +2.1% | North America, Europe, global spill-over | Long term (≥ 4 years) |

| Growing adoption of minimally invasive endovascular procedures | +1.8% | Global, strongest in developed economies | Medium term (2-4 years) |

| Favorable reimbursement incentives for U.S. office-based labs | +1.2% | United States | Short term (≤ 2 years) |

| Laser systems with active aspiration lower distal-embolization risk | +0.9% | North America, Europe | Medium term (2-4 years) |

| Domestic manufacturing push in Asia-Pacific | +0.8% | Asia-Pacific | Long term (≥ 4 years) |

| Synergistic outcomes of atherectomy plus drug-coated balloons | +0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Peripheral & Coronary Artery Disease

Peripheral artery disease affects more than 200 million people worldwide, most acutely in aging populations with diabetes and metabolic syndrome. The expanding burden raises procedural complexity because heavily calcified lesions respond poorly to plain balloon angioplasty. Current U.S. and European guidelines now recommend endovascular interventions for infra-inguinal lesions under 25 cm, opening a larger pool of candidates for atherectomy. Hospitals report that older patients present with longer, more complex occlusions that require vessel-preparation techniques to achieve acceptable luminal gain. Consequently, device makers emphasize systems able to debulk eccentric calcium while minimizing embolic events. The long-term demographic tailwind supports double-digit growth in procedure volumes for at least the next decade.

Growing Adoption of Minimally Invasive Endovascular Procedures

Hospitals and outpatient centers prefer shorter stays and quicker ambulation, pushing physicians to select techniques that reduce anesthesia time and wound complications. Medicare reimbursements for OBL interventions reached USD 6.8 billion across 6,308 facilities in 2023. Atherectomy fits this shift because most systems are compatible with 6Fr sheaths, allowing same-day discharge. Ambulatory surgical centers have posted an 8.06% CAGR in atherectomy procedure counts as vascular surgeons and advanced practice providers gain proficiency. Rising comfort among payors with OBL safety metrics further lifts utilization, reinforcing a feedback loop that sustains capital purchases of new systems. Comparable trends in Europe and advanced Asia-Pacific economies are visible albeit at lower absolute volumes.

Favorable Reimbursement Incentives for Office-Based Labs (U.S.)

Historically, CMS set higher relative value units for peripheral atherectomy in OBLs than in hospital outpatient departments, creating a financial tailwind for community-based vascular practices. While the 2024 Physician Fee Schedule reduced payment for over 300 OBL codes, atherectomy still commands sufficient margin for practices operating at moderate volume. Recent code assignments for intravascular lithotripsy, which often complements atherectomy, boosted average payments by USD 8,000, signaling that innovative vessel-preparation modalities can secure premium coverage when backed by robust evidence. The interplay between reimbursement revisions and clinical guidelines will determine whether OBLs maintain their current share of the atherectomy devices market.

Laser Systems with Active Aspiration Lower Distal-Embolization Risk

Second-generation laser catheters integrate aspiration ports proximal to the ablation window, removing particulate debris before it migrates downstream. In a 402-patient registry, the Phoenix system achieved procedural success exceeding 99%, with embolization rates of only 2%. These safety gains are critical as operators tackle longer chronic total occlusions and severely calcified in-stent restenosis that previously required open bypass. Reduced complication risk expands eligibility among frail patients and those with limited runoff vessels, thereby widening the addressable base for laser-enabled atherectomy.

Restraints Impact Analysis of Atherectomy Devices Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited long-term evidence of superiority versus PTA/stenting | −1.4% | United States, Europe | Medium term (2-4 years) |

| High device and capital costs | −1.1% | Global | Short term (≤ 2 years) |

| Imminent reimbursement cuts tied to utilization reviews | −0.8% | United States, developed markets | Short term (≤ 2 years) |

| Supply-chain risk for diamond-coated burr materials | −0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Long-Term Evidence of Superiority vs. PTA/Stenting

The 2,005-patient ECLIPSE trial reported no statistical advantage for orbital atherectomy over plain balloon angioplasty in preventing target vessel failure before drug-eluting stent implantation00450-7/abstract). This neutral outcome echoes prior peripheral registries in which atherectomy reduced amputation risk yet increased repeat intervention rates. Evidence-based payors may therefore restrict reimbursement to subgroups with demonstrated benefit, constraining volume growth in regions that prioritize randomized data over operator preference.

High Device & Capital Costs for Providers

Rotational atherectomy consoles can exceed USD 150,000 and require single-use burrs priced above USD 2,000. OBL operators already face CMS payment that covers barely one-fifth of thrombectomy procedural costs, forcing careful case selection. Capital intensity favors integrated health systems capable of amortizing equipment across multiple sites, potentially squeezing smaller vascular practices out of the atherectomy devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Atherectomy Devices Market Segment Analysis

By Device Type:

Directional Systems Anchor Market LeadershipDirectional systems generated 41.78% of atherectomy devices market revenue in 2025, reflecting surgeon preference for precise plaque excision and compatibility with post-dilation balloons. The atherectomy devices market size for directional platforms is projected to grow at a steady 7.08% CAGR to 2031 as new cutter-head geometries improve crossing profile without sacrificing debulking capacity. Laser catheters represent the fastest-rising modality at 7.74% CAGR because aspiration-assisted designs significantly lower embolic risk. Rotational and orbital devices remain essential for densely calcified coronary and iliac lesions yet face scrutiny following neutral ECLIPSE outcomes.

Competitive positioning hinges on differentiated burr coatings, real-time feedback algorithms, and bundled service contracts. Abbott’s Diamondback 360 leverages a diamond-embedded crown that orbits eccentrically to sand down calcium, whereas Boston Scientific’s Jetstream incorporates front-cutting blades plus aspiration for in-stent restenosis. University-industry projects such as milli-scale robotics foreshadow next-generation systems capable of remote navigation through tortuous neurovascular beds. FDA guidance on Predetermined Change Control Plans allows manufacturers to pre-specify software updates, shortening iteration cycles and accelerating innovation cadence.

By Application:

Peripheral Vascular Disease Dominates, Neurovascular SurgesPeripheral vascular disease interventions captured 57.45% of atherectomy devices market share in 2025 as femoropopliteal and below-the-knee lesions make up the bulk of global endovascular workload. The segment benefits from rising diabetes incidence and wider screening programs that detect occlusive disease earlier. Neurovascular procedures, however, will post the fastest expansion at 7.86% CAGR, propelled by growth in middle meningeal artery embolization for chronic subdural hematomas. Combination therapy strategies that unite clot retrieval, mechanical debulking, and pharmacologic lysis promise to broaden atherectomy’s role in stroke-adjacent care pathways. Coronary artery disease remains a steady but slower-growing application, with adoption tempered by neutral trial data and abundant stent options.

By End User:

Outpatient Migration Reshapes DemandHospitals and tertiary surgical centers accounted for 63.05% of atherectomy devices market revenue in 2025 thanks to comprehensive imaging and standby surgical backup. Yet ambulatory surgical centers are scaling faster—an 7.93% CAGR—because payors reward same-day discharge and lower facility fees. The atherectomy devices market size tied to ambulatory volumes could surpass USD 668.3 million by 2031 if reimbursement remains favorable. OBLs occupy a middle ground; they thrived on 2018-2023 payment levels but now face margin compression. Quality-focused OBL operators respond by integrating outcomes registries and strict appropriateness criteria to safeguard payer confidence.

Geography Analysis

North America and APAC Atherectomy Devices Market

North America generated 38.74% of atherectomy devices market revenue in 2025 on the back of high procedural density, entrenched reimbursement, and robust clinical research infrastructure. The region’s growth moderates to mid-single-digit rates as volume shifts from hospital inpatient to outpatient venues. The atherectomy devices market size in Asia-Pacific will expand at an 8.08% CAGR through 2031, underpinned by domestic manufacturing incentives and accelerating cardiovascular disease prevalence. China’s Fourteenth Five-Year Plan calls for local production of high-end interventional devices, positioning regional firms to undercut imports without compromising quality. Japan and South Korea, meanwhile, leverage mature reimbursement systems that now recognize vessel-preparation codes, stimulating early adoption.

EMEA and LATAM Atherectomy Devices Market

Europe remains the third-largest regional segment, characterized by evidence-oriented purchasing committees influenced by the Medical Device Regulation. Hospitals emphasize long-term safety registries; therefore, suppliers that document reduced reintervention rates achieve preferred-vendor status. Innovation uptake is fastest in Germany and the Netherlands where OBL equivalents—practice-based cath labs—operate under bundled diagnosis-related group payments. Latin America and Middle East & Africa collectively account for less than 10% of global sales but show high-single-digit growth as private insurers expand coverage for peripheral vascular procedures.

Regulatory Landscape

In the United States, atherectomy systems are regulated as cardiovascular devices through the FDA 510(k) pathway. The Auryon Atherectomy System clearance (K260244), issued on April 10, 2026, points to continued regulatory throughput for system updates and configuration changes. In Europe, MDR (EU) 2017/745 classification and technical documentation requirements apply. In April 2026, the European Commission endorsed updated MDCG 2021-24 Rev. 1 classification guidance and released Version 5 of the Manual on borderline and classification, which can affect intended-use positioning, the scope of clinical evaluation, and recertification planning for legacy platforms.

Value Chain Analysis

The atherectomy value chain includes upstream inputs such as diamond-coated components for rotational and orbital systems, precision cutter assemblies for directional devices, and laser diodes plus optical fibers for laser platforms. Downstream, the flow covers device OEM manufacturing, sterilization and packaging, and distribution through direct hospital and IDN contracting as well as regional distributors that enable capital equipment placement and recurring single-use catheter sales. For laser atherectomy, the supply chain is more vertically integrated and concentrated, with a smaller set of global manufacturers combining laser source design, fiber-optic delivery, and catheter engineering into proprietary console-and-consumable ecosystems that support installed-base lock-in and service-driven revenue.

Competitive Landscape

The atherectomy devices market is moderately consolidated, with the top five suppliers controlling significant global revenue. Boston Scientific, Medtronic, Abbott, Teleflex, and Stryker employ mergers to fill technology gaps and extend channel reach. In January 2025, Stryker closed a USD 4.9 billion purchase of Inari Medical, securing thrombectomy know-how that complements its existing Jetstream franchise. Teleflex followed by acquiring Biotronik’s vascular intervention unit for €760 million in July 2025, securing a European manufacturing foothold.

Product differentiation has shifted from raw cutting efficiency to integrated therapy platforms combining vessel-preparation, antiproliferative drug delivery, and intelligent data capture. Vendors roll out cloud-connected consoles that log run time, cutter torque, and aspiration flow, feeding predictive maintenance algorithms that lower downtime. Smaller innovators target niche neurovascular or robotic niches, betting that faster FDA software iteration pathways will level the playing field.

Third-party service organizations offering per-click pricing on capital equipment are emerging, especially in low-volume community hospitals. Such models lower upfront cost but lock customers into proprietary consumables, reinforcing brand stickiness. Competitive intensity is expected to rise as Asian OEMs secure CE and FDA clearances by 2027, introducing price competition in value-sensitive markets.

Atherectomy Devices Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Medtronic

Becton, Dickinson and Company

Koninklijke Philips N.V.

- *Disclaimer: Major Players sorted in no particular order

Atherectomy Devices Market Companies Covered in this Report

- Abbott Laboratories

- Medtronic

- Boston Scientific

- Koninklijke Philips

- AngioDynamics

- Beckton Dickinson

- Straub Medical

- Avinger Inc.

- Terumo

- Shockwave Medical Inc.

- Cook Group

- Merit Medical Systems

- Penumbra

- BIOTRONIK

- Rex Medical LP

- Ra Medical Systems Inc.

- Cardiovascular Systems Inc. (CSI)

Market Opportunities and Future Outlook

Ongoing FDA 510(k) activity across atherectomy modalities reflects product-cycle momentum in peripheral and complex lesion workflows, and it creates room for suppliers that can simplify vessel preparation while lowering complication risk and reducing capital pressure on outpatient sites. The current clearance anchors include Eximo Medical’s Auryon Atherectomy System (FDA 510(k) K260244, April 10, 2026), Bard Peripheral Vascular’s Rotarex Atherectomy System (FDA 510(k) K242757, January 30, 2025), and Cardio Flow’s FreedomFlow Orbital Circumferential Atherectomy System configuration (FDA 510(k) K250723, April 25, 2025). Alongside the shift toward 6Fr compatibility and same-day discharge pathways, these clearances support opportunities for vendors that package capital placement, training, and consumable logistics for hospitals, ASCs, and office-based labs.

Clinical practice is converging around combination strategies for severe calcification, with integrated treatment protocols and bundled offerings pairing atherectomy with other plaque-modification technologies. Evidence also highlights where patient selection remains important. The Dual-Prep Registry (2026) reported 7.6% 1-year major adverse cardiovascular events when atherectomy was followed by intravascular lithotripsy in severely calcified coronary lesions, while the 2025 ECLIPSE randomized trial reported neutral differentiation for routine orbital atherectomy versus a balloon-first strategy in eligible lesions. Differentiation is increasingly tied to data-backed indication focus (calcified subsets, bifurcations, complex anatomy), device-plus-therapy pathways (atherectomy plus drug-coated balloons or lithotripsy), and workflow enablers such as cloud-connected consoles that capture procedural parameters for quality reporting in outpatient settings.

Recent Industry Developments in Atherectomy Devices Market

- April 2026: Eximo Medical received FDA 510(k) clearance (K260244) for the Auryon Atherectomy System. The clearance expands the pool of commercially available atherectomy platforms in the United States and supports competitive bidding as providers refresh consoles and consumables. It also reinforces the pace of iteration through the 510(k) route for device configurations and line extensions.

- March 2025: Abbott announced FDA approval of an IDE for its Coronary Intravascular Lithotripsy System clinical trial program in severe coronary calcification. The move signals continued investment in adjunct plaque-modification capabilities that influence integration with atherectomy workflows and may affect treatment planning for calcified lesions.

- July 2024: BD announced FDA 510(k) clearance of expanded indications for the Rotarex Atherectomy System. Broader labeled use can accelerate standardization of case selection and training across hospital and outpatient settings where thrombus and complex peripheral disease overlap with atherectomy use. The update also strengthens the competitive set in mechanical debulking as payors and providers emphasize indication clarity.

Atherectomy Devices Market Report Scope and Research Methodology

Market Definition and Coverage

This market is defined as the revenue generated from atherectomy systems and their related components that are used to remove or modify plaque in blood vessels during minimally invasive vascular procedures, across the full chain from manufacturer sales through clinical use.

Scope exclusions: We exclude diagnostic imaging-only tools, standalone balloons and stents not sold as part of atherectomy therapy, and general catheter lab capital equipment that is not specific to atherectomy.

Segments Covered in This Report

- By Device Type (Value)

- Directional Atherectomy Devices

- Rotational Atherectomy Devices

- Orbital Atherectomy Devices

- Laser Atherectomy Devices

- By Application (Value)

- Peripheral Vascular Disease

- Coronary Artery Disease

- Neurovascular Disease

- By End User (Value)

- Hospitals & Surgical Centers

- Ambulatory Surgical Centers

- Office-Based Labs

- by Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clinical and regulatory boundary so the count stays focused on atherectomy therapy and not the wider interventional device basket. We review public sources such as the US FDA device databases and safety communications, the US Centers for Medicare and Medicaid Services reimbursement files, and the US CDC and WHO cardiovascular and peripheral artery disease burden statistics to size the patient and procedure pool.

To translate demand into dollars, we also reference sources such as OECD health statistics, peer reviewed journals that discuss lesion complexity and atherectomy utilization, and trade association or government health system publications that indicate cath lab and outpatient growth. Alongside these, we scan company filings, investor presentations, and reputable press for product mix changes and pricing commentary, and we use an approved paid subscription for company financials and patent activity where it helps validate timelines and innovation intensity. These examples are not exhaustive, and many other public sources were also used for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work is used to stress-test the desk assumptions with people who see procedure patterns and purchasing behavior in real settings. We speak with a mix of manufacturers, distributors, interventional clinicians, and hospital and ASC procurement teams across major regions so pricing corridors, utilization rates, and adoption constraints can be confirmed and adjusted.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 15% | APAC: 41% |

| Mid tier: 49% | Functional/Unit leaders: 34% | EMEA: 33% |

| Smaller Players: 16% | Managers: 51% | Americas: 26% |

Market-Sizing & Forecasting

The main build uses a top-down approach where disease prevalence and treated population signals are converted into an addressable procedure pool, which is then mapped to atherectomy penetration and spending per case. For atherectomy devices, the inputs we lean on include peripheral artery disease and coronary disease case load trends, the share of complex and calcified lesions, shifts toward outpatient sites of care (including ASCs and office-based labs), average selling price ranges by device type, and regional reimbursement and tender behavior.

Once the demand pool is formed, totals are corroborated using selective bottom-up approximations, such as rolling up a sample of supplier revenues, distributor channel checks, and a volume times ASP cross-check for high-adoption countries. When a country has limited public procedure data, gaps are handled through proxy indicators like angioplasty volumes, interventional cardiology capacity, and clinician feedback on typical atherectomy use rates, before being normalized back to regional totals.

For forecasting, we use scenario analysis supported by a short list of variables that can be refreshed consistently each year, such as procedure growth, outpatient migration, and price erosion or premium retention by technology class. The scenarios are then aligned to what experts expect for adoption pace and reimbursement stability, and the final track is chosen after reconciling outliers.

Data Validation & Update Cycle

Outputs are checked against independent signals, including procedure growth markers, reimbursement changes, and reported business performance for the category, before any numbers are finalized. Variances are reviewed in steps, first at the model-input level and then at the regional roll-up level, and any sharp jumps trigger a re-check of currency conversion, pricing assumptions, and timing of product mix changes.

Reports are refreshed annually, and interim updates are made when material events occur, such as policy changes, major launches, or meaningful pricing resets in large markets. Before delivery, a final analyst pass is completed so the view reflects the latest available public data and the most recent expert feedback.

Mordor Intelligence's Atherectomy Devices Market Size Measured Against Other Published Estimates

It is common to see different market sizes for atherectomy devices because publishers do not always line up on timing, currency, and what exactly is counted as atherectomy spending. Small choices, such as whether a value is reported in constant or current dollars, or whether single-use components are bundled with capital, can move the total in a visible way.

In this study, year-to-year pricing is kept realistic by rechecking ASP ranges and currency conversion timing during each refresh cycle, and those checks are then reconciled back to procedure and adoption signals gathered from interviews, which is where Mordor Intelligence tends to land closer to the true purchasing pattern instead of a simple CAGR projection.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.12 B (2026) | |

| Global Publisher A | USD 1.03 B (2024) | Uses an earlier base year and a different forecast window, and the value can shift based on whether pricing is carried forward as a fixed average or adjusted for device-mix changes across peripheral and coronary use. |

| Industry Research Group B | USD 1.07 B (2025) | Applies a longer forecast horizon with a higher growth curve, and it is less clear how currency timing and annual ASP movement are revalidated when technology mix and site-of-care shift toward outpatient settings. |

The spread in the table is mainly explained by calendar alignment and how pricing is updated as the therapy mix changes. When scope stays limited to atherectomy therapy and the model is repeatedly tied back to procedures, adoption, and refreshed ASP corridors, the resulting market size becomes easier to replicate and interpret across regions.

Key Questions Answered in the Report

What is the projected value of the atherectomy devices market in 2031?

The market is expected to reach USD 1.61 billion by 2031 at a 7.58% CAGR.

Which device category currently holds the largest share?

Directional systems command 41.78% of 2025 revenue due to precise plaque excision capabilities.

Which regional segment will grow fastest through 2031?

Asia-Pacific is forecast to expand at an 8.08% CAGR, supported by domestic manufacturing initiatives.

How is reimbursement influencing outpatient utilization?

Despite recent CMS cuts, atherectomy still yields positive margins in many OBLs, sustaining outpatient migration.

What evidence challenges routine use in coronary lesions?

The ECLIPSE trial found no target vessel failure advantage for orbital atherectomy over balloon-first strategies, questioning its routine application.

Page last updated on: