Gynecological Examination Chairs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

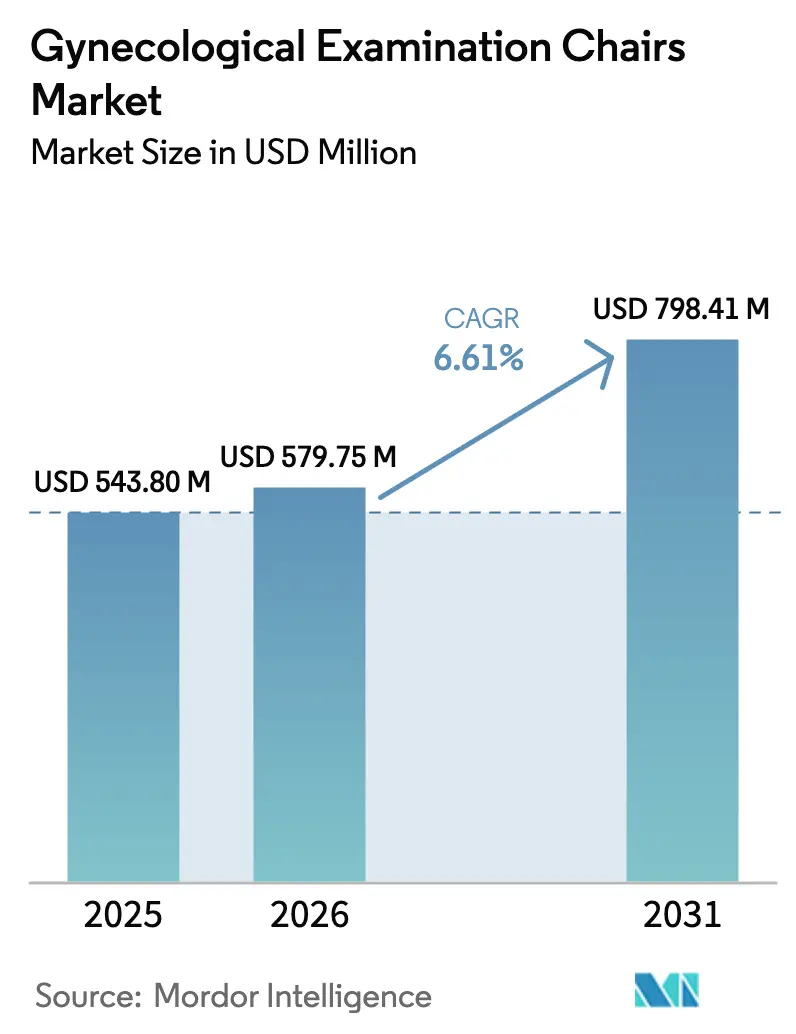

| Market Size (2026) | USD 579.75 Million |

| Market Size (2031) | USD 798.41 Million |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

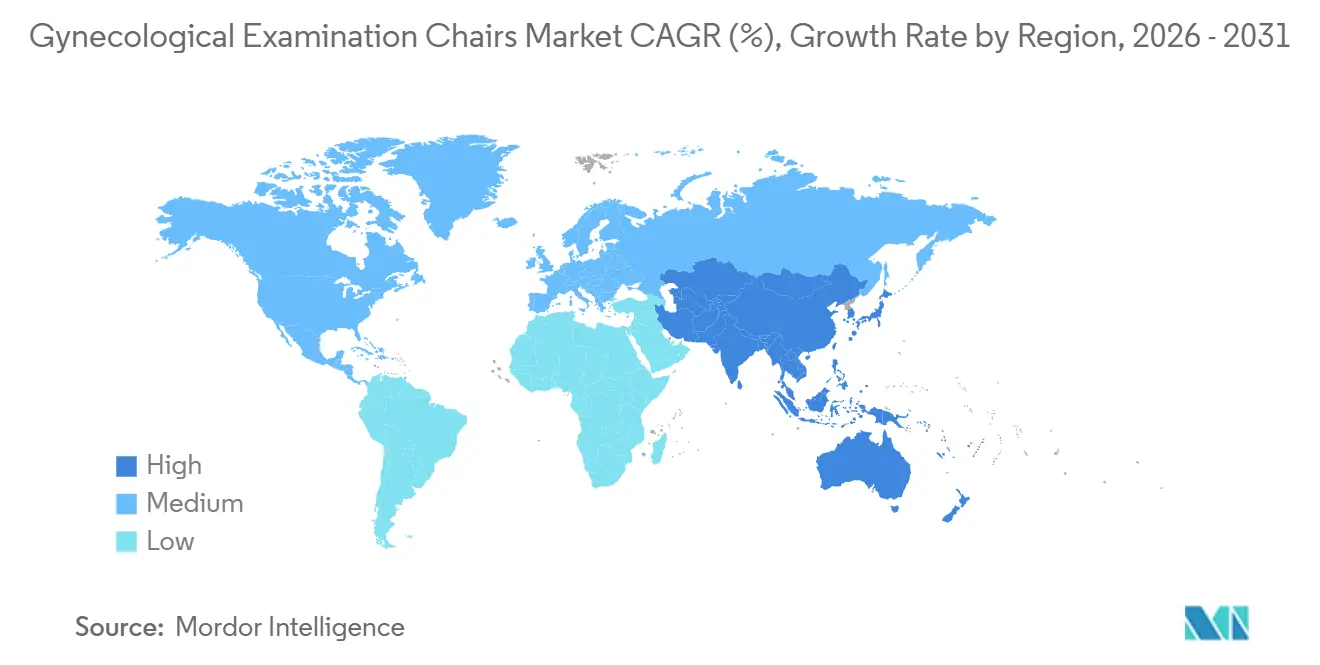

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gynecological Examination Chairs Market Analysis by Mordor Intelligence

The Gynecological Examination Chairs Market size was valued at USD 543.80 million in 2025 and is estimated to grow from USD 579.75 million in 2026 to reach USD 798.41 million by 2031, at a CAGR of 6.61% during the forecast period (2026-2031).

The increasing prevalence of 1.21 billion gynecological disorders, coupled with aggressive hospital-bed expansions in the Asia-Pacific region and a payer-driven shift toward ambulatory care, is driving demand for advanced, high-throughput equipment. Electric motorized models now account for nearly 50% of global unit sales, with their rapid adoption supported by digital health initiatives that incentivize connected devices capable of transmitting utilization, positioning, and preventive maintenance data directly to Electronic Health Records (EHRs). Additionally, the expansion of retail clinics and mobile women’s health vans is broadening the customer base, with a focus on compact designs, antimicrobial upholstery, and subscription-based pricing models that transition costs from capital expenditure (capex) to operational expenditure (opex). However, these growth drivers are tempered by significant upfront price premiums compared to manual tables and the potential for increased redesign and validation costs due to anticipated EPA restrictions on ethylene oxide sterilization.

Key Report Takeaways

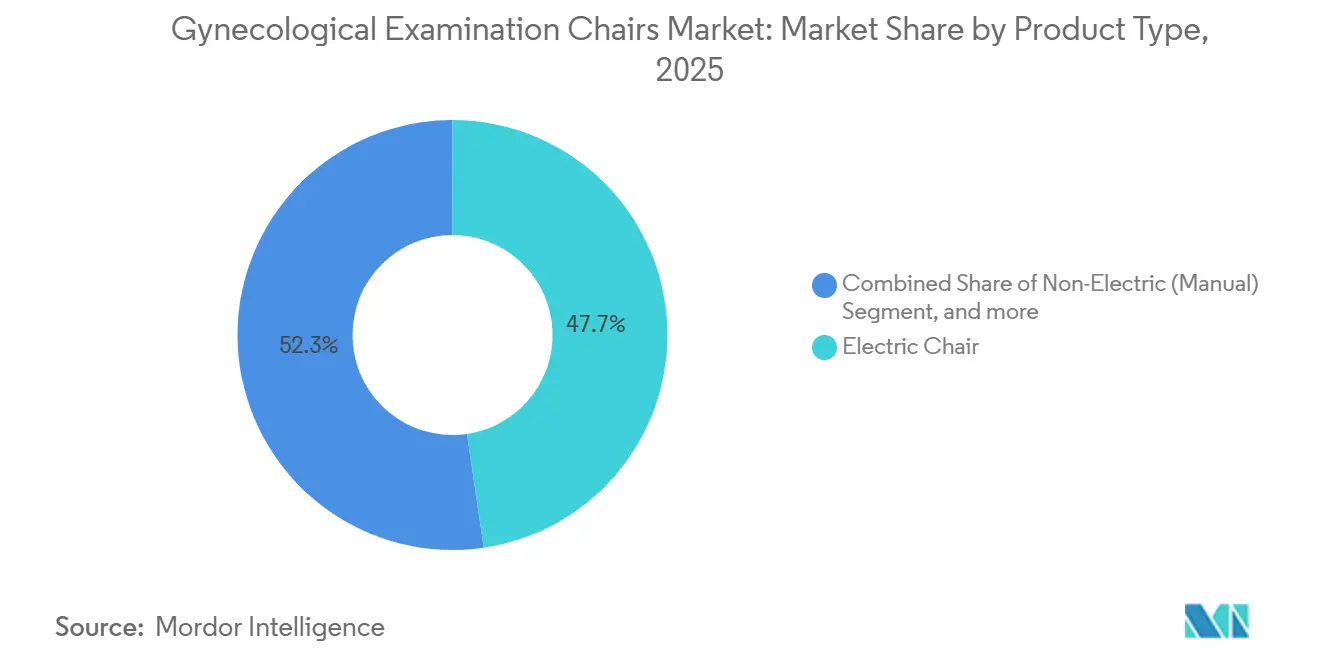

- By product type, electric motorized chairs held 47.67% of the gynecological examination chairs market share in 2025 and are advancing at an 8.54% CAGR through 2031.

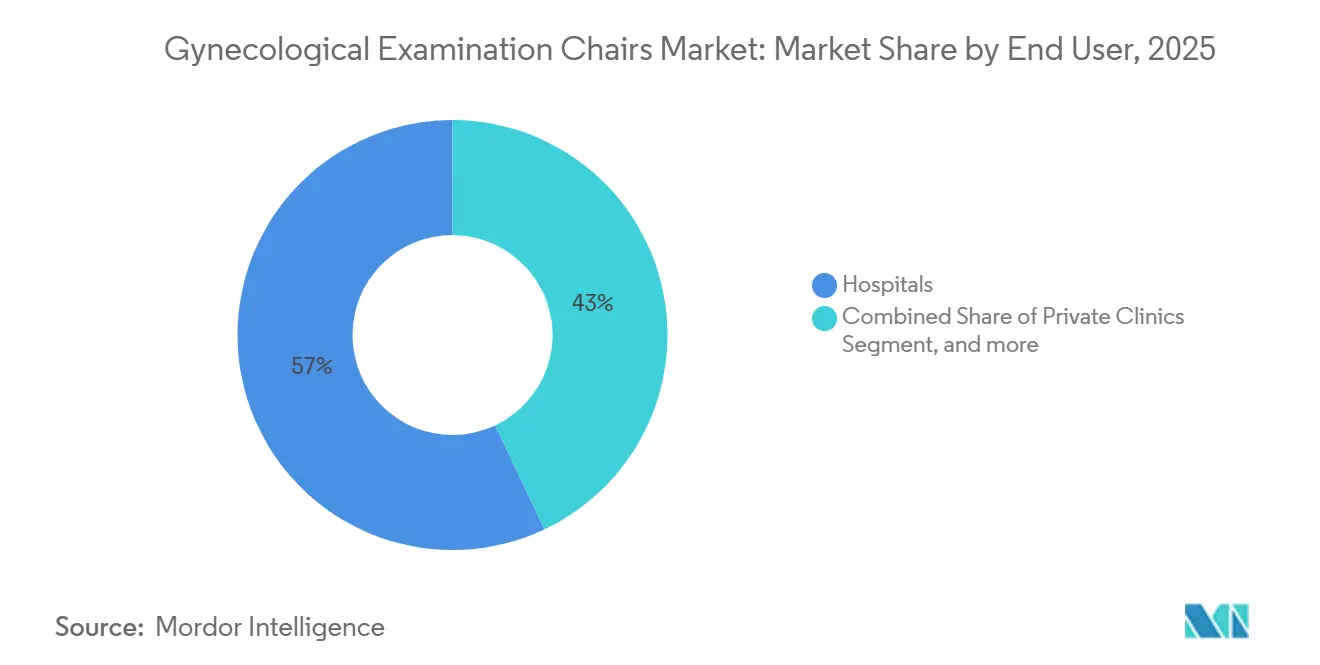

- By end user, ambulatory surgical centers are forecast to expand at an 8.87% CAGR to 2031, outpacing hospitals despite the latter’s 57.03% revenue lead in 2025.

- By geography, Asia-Pacific is projected to register a 7.54% CAGR over 2026-2031, rising faster than North America’s otherwise dominant 41.56% revenue contribution in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gynecological Examination Chairs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of women's health disorders | +1.8% | Global, with acute pressure in South Asia, Sub-Saharan Africa, and Latin America | Medium term (2-4 years) |

| Expansion of global healthcare infrastructure | +1.5% | Asia-Pacific core (India, China, Indonesia), spill-over to Middle East & Africa | Long term (≥ 4 years) |

| Technological advancements in examination chairs | +1.3% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Increasing focus on patient comfort and safety | +0.9% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Integration of digital health and IoT solutions | +0.7% | North America, Europe, early adopters in Asia-Pacific metros | Medium term (2-4 years) |

| Shift toward decentralized and outpatient care delivery | +0.4% | United States, Canada, Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Women's Health Disorders

The 2021 Global Burden of Disease update reported 1.21 billion prevalent reproductive-system conditions, a figure that continues to rise as screening programs expand in key markets such as India, China, and Indonesia. This increasing diagnostic coverage is driving higher patient revisit rates and prompting clinics to replace outdated fixed-height tables with advanced multi-position electric chairs. These chairs, designed to optimize space, support multiple functions, including pelvic exams, colposcopy, and prenatal monitoring. Furthermore, national mandates for universal cervical-cancer screening are fueling demand for chairs equipped with imaging mounts and ADA-compliant transfer surfaces, aligning with evolving regulatory and operational requirements[1]World Health Organization, “Global Strategy for Cervical Cancer Elimination,” who.int.

Expansion of Global Healthcare Infrastructure

Health-care expenditure in the Asia-Pacific region is projected to reach USD 5 trillion by 2030, fueled by key initiatives such as India's Ayushman Bharat insurance program, China's 14th Five-Year Plan commitment to establish 1,000 county-level hospitals for women and children, and multilateral funding aimed at expanding clinic networks in Indonesia. With new facilities adhering to modern WHO ergonomic and infection-control standards, there is a growing preference for advanced electric or electro-hydraulic chairs over traditional low-cost manual tables, driving a significant shift in medical equipment adoption.

Technological Advancements in Examination Chairs

Modern electric chairs use IP66-sealed linear actuators capable of 12,000 N push force, delivering smooth height changes from 17 to 36 inches plus Trendelenburg tilt via hand or foot controls. Self-locking mechanisms comply with IEC 60601-1 safety standards and maintain position during power loss. Peer-reviewed trials show that motorized systems can cut clinician muscle loading by up to 47%, a finding now referenced in many procurement scorecards. Hybrid electro-hydraulic designs bridge affordability and performance for cash-strapped public hospitals, while modular accessories extend a single chair across gynecology, urology, and minor surgery workflows.

Increasing Focus on Patient Comfort and Safety

Antimicrobial vinyl embedded with silver or copper reduces surface bioburden by 99.9% within 2 hours and trims terminal-cleaning time by nearly one-fifth. Transfer supports, low-height ranges, and 28-inch supine surfaces align with U.S. Medical Diagnostic Equipment standards, yet only 8.4% of surveyed primary-care sites met these specs in 2025. Chairs that meet these requirements sharply decrease staff lift-assist injuries, a top driver of workers' comp costs and malpractice claims.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure requirements | -1.2% | Global, acute in price-sensitive emerging markets (India, Indonesia, Sub-Saharan Africa) and independent clinics | Short term (≤ 2 years) |

| Stringent regulatory and compliance standards | -0.8% | North America, Europe, with spillover to Asia-Pacific as harmonization advances (China, Japan, South Korea) | Medium term (2-4 years) |

| Limited space and workflow constraints in clinics | -0.5% | Urban Asia-Pacific (Tokyo, Mumbai, Shanghai), dense European cities, and legacy U.S. community clinics | Short term (≤ 2 years) |

| Environmental sustainability and lifecycle considerations | -0.3% | Europe (carbon-footprint mandates), North America (EPA EtO restrictions), early pressure in Australia and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure Requirements

Electric gynecological chairs list at USD 2,950-7,500, compared with USD 1,050-2,400 for manual models, a 2-3× differential that strains ASC and rural-clinic budgets[2]U.S. Access Board, “Medical Diagnostic Equipment Standards,” access-board.gov. Add 10-15% for installation and USD 500-1,100 for accessories and the outlay becomes formidable; a 10-room women’s center can spend USD 50-75 thousand on chairs alone. Refurbished or subscription-priced offerings lower entry barriers, but uptake remains modest amid concerns about warranties and residual value.

Stringent Regulatory and Compliance Standards

Manufacturers must clear FDA 510(k), earn CE marks under EU MDR, and document ISO 13485 QMS plus IEC 60601 electrical safety, extending launches by up to two years and adding USD 0.5-2 million in pre-market costs[3]U.S. Food & Drug Administration, “Cybersecurity in Medical Devices,” fda.gov. Impending U.S. enforcement of accessibility rules and EPA toxics curbs may force redesigns or alternate sterilization validation, challenges that favor larger OEMs with dedicated regulatory teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electric Chairs Dominate on Workflow and Ergonomic Gains

In 2025, electric motorized units accounted for 47.67% of the gynecological examination chairs market share and are projected to grow at a CAGR of 8.54%. This growth is driven by programmable memory presets, which reduce patient setup time by nearly 40%. Hospitals increasingly favor these units due to their IoT telemetry capabilities, which integrate directly with asset-management software. As a result, electric motorized units are becoming the standard choice in high-income regions. While hydraulic and electro-hydraulic hybrids remain prevalent in cost-sensitive markets, demand for powered height adjustments is rising to meet forthcoming accessibility regulations. Although smart, fully connected chairs currently represent less than 5% of shipments, they have demonstrated a nearly one-third reduction in downtime during North American pilot programs. This positions the segment for significant growth as cybersecurity frameworks mature.

Regulatory and sustainability pressures are further driving the adoption of powered models. Compliance with EPA sterilant regulations is simplified when detachable components are reprocessed with hydrogen peroxide or radiation rather than ethylene oxide. In 2024, OEM reprocessing programs recovered 5 million pounds of equipment, resulting in USD 239 million in customer savings. These lifecycle-cost advantages align with the priorities of value-based procurement committees. Meanwhile, manual tables are increasingly non-compliant with ADA height-adjustment standards and are expected to be relegated to ultra-low-budget or humanitarian applications.

By End User: Hospitals Lead, ASCs Surge on Cost and Convenience

In 2025, hospitals accounted for a 57.03% revenue share, driven by enterprise-wide contracts bundling gynecological chairs with imaging carts and EHR integration at 15-20% below retail prices. These contracts align with replacement cycles that emphasize antimicrobial upholstery and actuator designs aimed at reducing caregiver injury claims. In contrast, ambulatory surgical centers (ASCs) are experiencing the fastest growth, with an 8.87% CAGR, as payers increasingly shift procedures away from hospitals to control costs. Each new ASC, supported by 6,300 Medicare-certified sites, typically establishes three to eight multipurpose procedure rooms, creating substantial demand for high-throughput chairs and contributing to significant cumulative volume.

Retail clinics represent another growth avenue, with major operators like CVS and Walgreens investing billions to expand locations offering well-woman exams. These clinics require compact, electrically adjustable chairs designed for 120-square-foot bays. Private OB/GYN offices and diagnostic centers continue to prefer electro-hydraulic hybrids that balance cost efficiency with functionality. Meanwhile, mobile care startups are adopting foldable, battery-powered chairs, optimized for deployment in curbside settings or community centers.

Geography Analysis

In 2025, North America contributed 41.56% of the total revenue, driven by over 6,300 Ambulatory Surgical Centers (ASCs), ongoing hospital refresh cycles, and the enforcement of accessibility regulations disqualifying many fixed-height tables. The expansion of retail clinics in the U.S. is attracting new non-hospital buyers, while Canadian provincial mandates are fueling demand for ISO-certified equipment with bilingual support.

Asia-Pacific is positioned as the fastest-growing region, with a projected 7.54% CAGR through 2031. Key drivers include India's Ayushman Bharat initiative, China's plan to establish 1,000 county-level hospitals for women and children, and AIIB-funded clinic modernizations in Indonesia. These developments are generating significant demand for electric and hybrid chairs that comply with WHO ergonomic standards. Local manufacturers are maintaining competitive pricing below USD 2,000, enabling widespread adoption even in tier-two cities.

In Europe, single-payer procurement systems ensure stable volumes but exert pressure on margins. Sustainability clauses in procurement contracts are increasingly favoring vendors offering circular-economy solutions. The Middle East market is bifurcated, with high-end Gulf hospital chains contrasting with donor-funded initiatives in Sub-Saharan regions, which primarily procure manual or cost-effective hybrid solutions. In Latin America, currency fluctuations moderate growth; however, Brazil and Argentina continue to drive steady public tender activity aligned with national women's health programs.

Competitive Landscape

In 2024, Stryker, Hill-Rom-Baxter, Midmark, and ArjoHuntleigh, all holding ISO 13485 certifications and multi-jurisdictional approvals, collectively accounted for 40-50% of global revenue. Stryker reinforced its market leadership with USD 22.6 billion in sales and completed seven strategic acquisitions to expand its installed base, capitalizing on scale advantages. The mid-tier market is driven by players such as LINET and Malvestio, along with several Chinese and Indian firms focusing on localized electro-hydraulic hybrids for national tenders. New entrants are addressing IoT gaps, as less than 5% of chairs are currently network-ready despite evidence of 30% downtime savings. Component suppliers like TiMOTION are lowering entry barriers for niche assemblers by offering turnkey EN 60601-certified actuator kits.

Retail-clinic giants are reshaping the competitive landscape: CVS controls 63% of U.S. retail outlets, while Walgreens is investing USD 5.2 billion to add 600 new sites. This consolidation allows both chains to influence market dynamics by driving demand for proprietary chair formats and subscription-based pricing models. Meanwhile, EPA sterilant restrictions and U.S. accessibility mandates are expected to pressure smaller competitors, creating opportunities for capital-rich multinationals to gain a competitive edge through rapid redesigns and compliance financing.

Gynecological Examination Chairs Industry Leaders

Stryker Corporation

Hill-Rom Holdings Inc. (Baxter)

Schmitz u. Söhne GmbH & Co. KG

Medifa-Hesse GmbH & Co. KG

Midmark Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Midmark Corp., one of the leading medical solutions providers focused on the design of the clinical environment to improve the delivery of care, launched the Midmark 631 procedure chair. Developed to better meet the accessibility needs of today’s patients, the Midmark 631 Procedure Chair is the first and only U.S. Access Board (USAB) compliant procedure chair.

- March 2024: German manufacturer SCHMITZ launched an advanced medi-matic gynaecological examination chair, emphasizing ergonomic and hygienic standards. It sets a new benchmark in medical, examination, and surgical chairs.

Global Gynecological Examination Chairs Market Report Scope

As per the scope of the report, gynecological examination chairs are used for the diagnosis and treatment procedures of gynaecology as these chairs reduce the examination and operating time.

The Gynecological Examination Chairs market is segmented by product type (electric chair, non-electric chair, and hydraulic chair), application type (gynecological cancer, menstrual disorder, menstrual disorder, hysterectomy, pregnancy complications, and other applications), end users (gynecological surgical centers, hospitals & clinics, and other end users) and geography (North America, Europe, Asia-Pacific, Middle East and Africa and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Non-Electric (Manual) |

| Electric (Motorised) |

| Hydraulic |

| Electro-Hydraulic Hybrid |

| Smart / IoT-Integrated Models |

| Hospitals |

| Private Clinics |

| Diagnostic Centres |

| Ambulatory Surgical Centres |

| Retail / Minute Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Non-Electric (Manual) | |

| Electric (Motorised) | ||

| Hydraulic | ||

| Electro-Hydraulic Hybrid | ||

| Smart / IoT-Integrated Models | ||

| By End User | Hospitals | |

| Private Clinics | ||

| Diagnostic Centres | ||

| Ambulatory Surgical Centres | ||

| Retail / Minute Clinics | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the gynecological examination chairs market by 2031?

The market is forecast to reach USD 798.41 million by 2031.

Which product type is growing fastest?

Electric motorized chairs are rising at an 8.54% CAGR thanks to ergonomic and digital-health advantages.

Why are ambulatory surgical centers important buyers?

ASCs seek cost-efficient, same-day care settings and are growing chair purchases at an 8.87% CAGR.

Which region will post the highest growth through 2031?

Asia-Pacific leads with a projected 7.54% CAGR as governments expand hospital and clinic capacity.

How are EPA sterilant rules affecting suppliers?

OEMs must validate hydrogen-peroxide or radiation methods or redesign components, adding compliance costs and favoring larger players.

Page last updated on: