Bowel Management Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

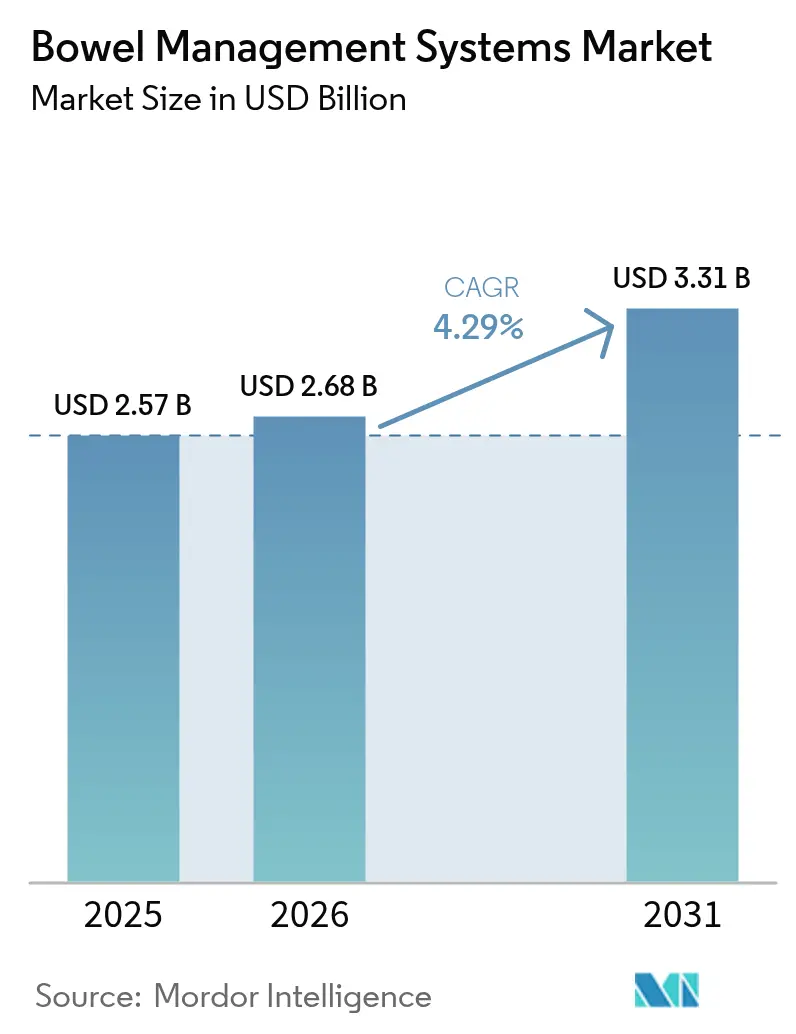

| Market Size (2026) | USD 2.68 Billion |

| Market Size (2031) | USD 3.31 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

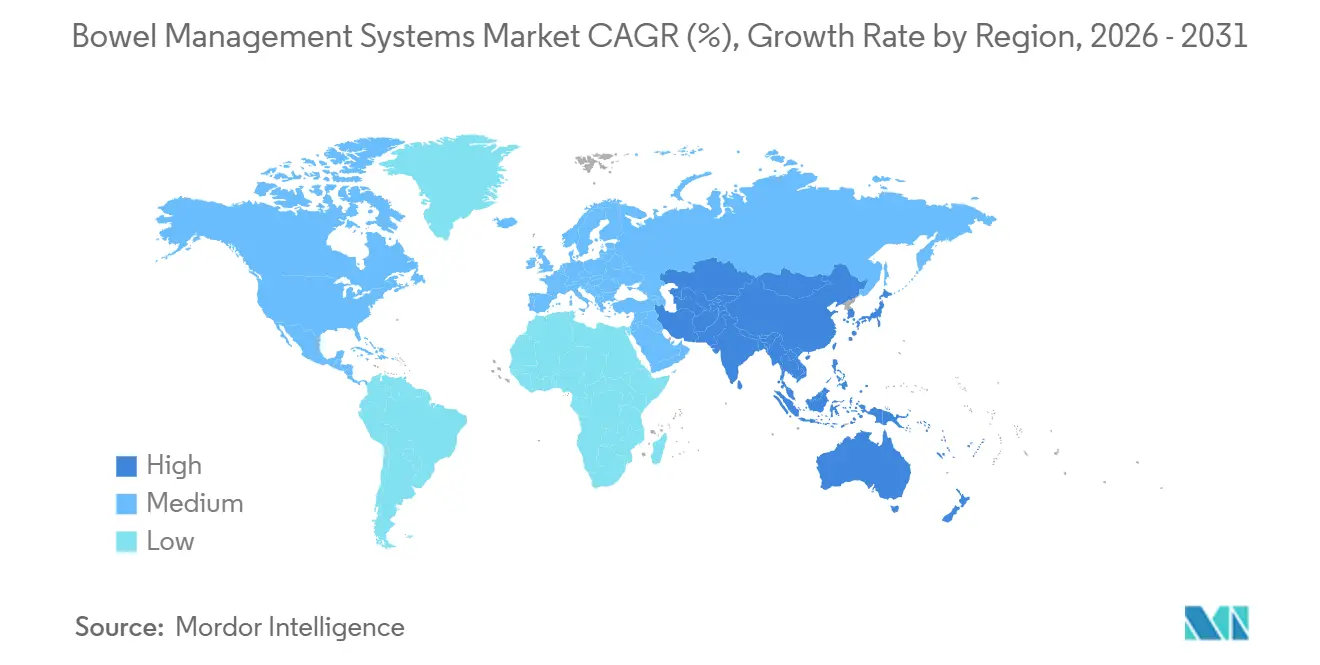

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

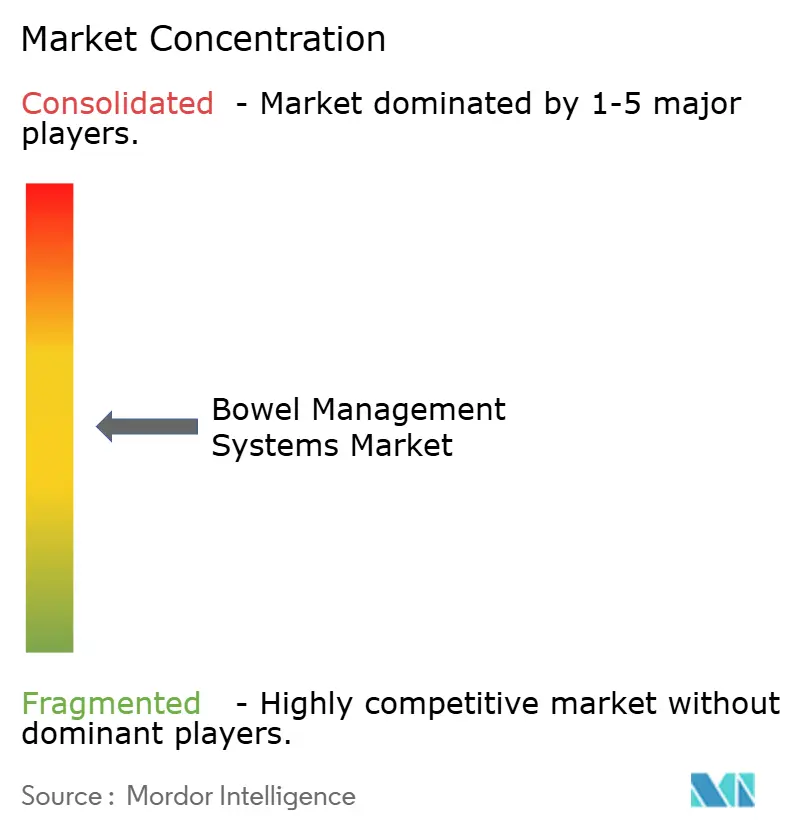

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bowel Management Systems Market Analysis by Mordor Intelligence

The bowel management systems market size is expected to grow from USD 2.57 billion in 2025 to USD 2.68 billion in 2026 and is forecast to reach USD 3.31 billion by 2031 at 4.29% CAGR over 2026-2031. Growth reflects a pivot toward neuromodulation therapies that restore continence without permanent stomas, stronger reimbursement for premium implants, and rising adoption of smart-sensor pouches that let clinicians monitor output remotely. Suppliers are investing in recyclable pouch films to comply with extended-producer-responsibility rules in the European Union, while policymakers in North America and Asia-Pacific expand coverage for sacral and tibial nerve stimulation, accelerating therapy uptake among Medicare and Ayushman Bharat beneficiaries. Competitive intensity is rising as smaller entrants pair Bluetooth-enabled accessories with telehealth platforms, giving hospitals a path to cut readmissions linked to leakage and skin complications. Collectively, these shifts strengthen pricing power in the bowel management systems market and widen the total addressable pool of high-acuity fecal-incontinence patients.

Key Report Takeaways

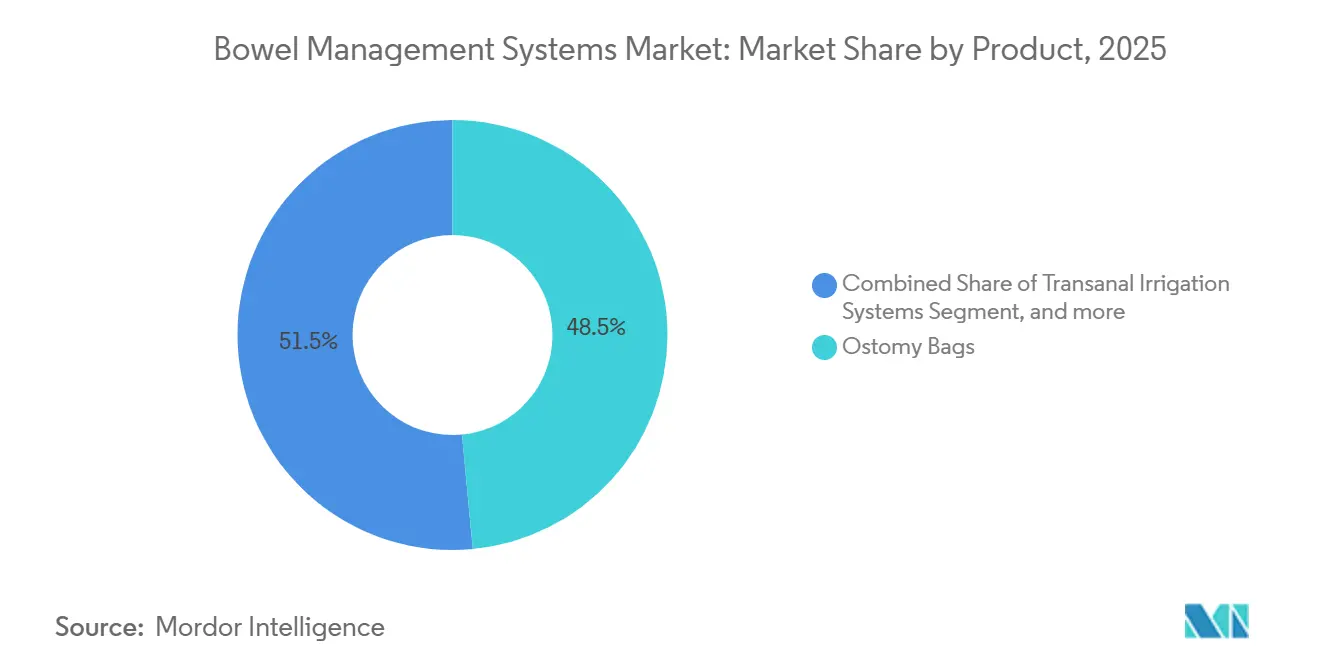

- By product type, ostomy bags commanded 48.54% of the bowel management systems market share in 2025, while nerve modulation devices posted the fastest 6.25% CAGR through 2031.

- By patient type, adult patients aged 18-64 accounted for 65.54% of the bowel management systems market size in 2025, yet the geriatric segment is advancing at 7.65% CAGR.

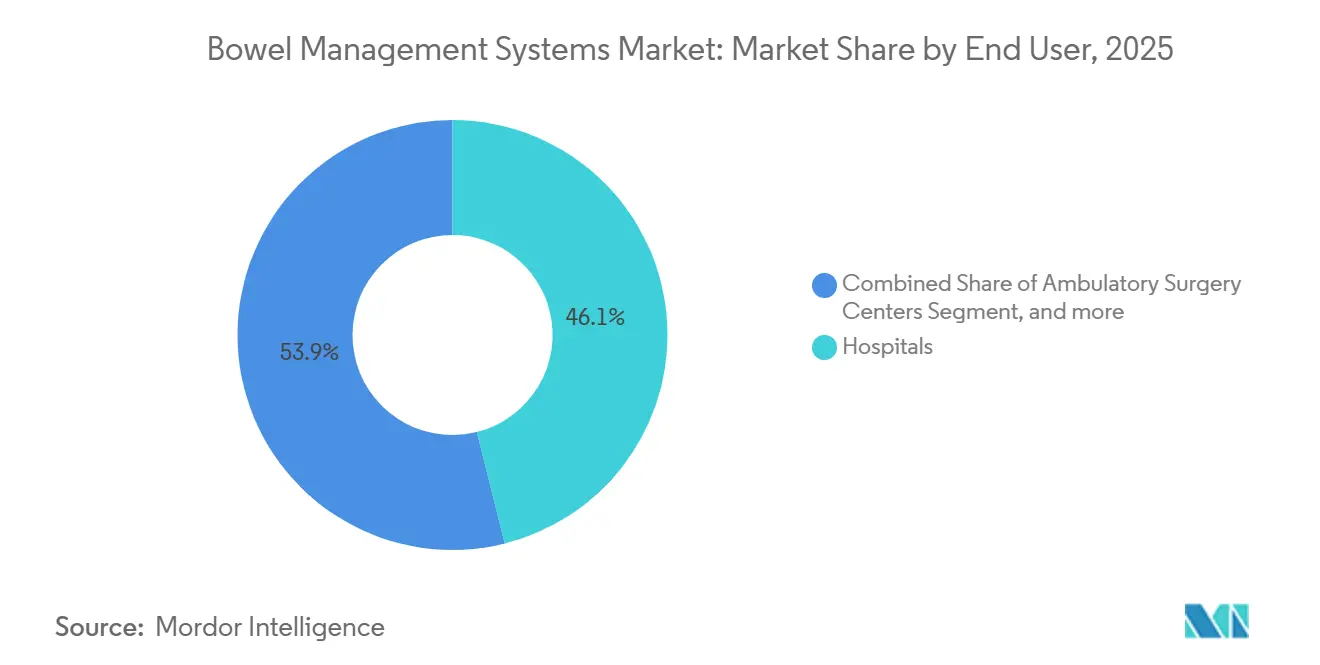

- By end user, hospitals held 46.15% revenue share of the bowel management systems market in 2025, whereas home-care settings are projected to expand at 7.82% CAGR to 2031.

- By geography, North America led with 38.23% of the bowel management systems market size in 2025, but Asia-Pacific is the fastest geography at 6.62% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bowel Management Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High incidence of inflammatory bowel disease | +0.9% | Global, elevated in North America and Europe | Medium term (2-4 years) |

| Rapidly growing geriatric population | +1.2% | Global, APAC and Europe | Long term (≥ 4 years) |

| Reimbursement expansion in high-income markets | +0.8% | North America, Western Europe, Japan | Short term (≤ 2 years) |

| Smart-sensor ostomy pouches | +0.6% | North America, EU core, urban APAC | Medium term (2-4 years) |

| ESG-driven shift to bio-based materials | +0.4% | EU, North America, select APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Incidence of Inflammatory Bowel Disease

Inflammatory bowel disease affects 3.1 million U.S. adults, while incidence climbs in industrializing economies, sustaining demand for ostomy supplies[1]Centers for Disease Control and Prevention, “IBD Surveillance,” CDC, cdc.gov. Earlier surgical intervention among biologic-therapy non-responders reduces the window from diagnosis to stoma creation, driving sales of high-output pouches with convex barriers that fit complex abdomens. Device makers respond with deeper filters that tame odor during active flares, an attribute valued by younger Crohn’s patients returning to school or work. Clinicians increasingly pair temporary ileostomies with restorative proctocolectomy, ensuring continued ostomy-bag replacement cycles. These patterns keep the bowel management systems market on a stable volume trajectory even if biologics delay some surgeries.

Rapidly Growing Geriatric Population

Adults aged 65 and over will reach 1.5 billion by 2050, with fecal-incontinence prevalence at 14.1% among community dwellers and up to 70% in nursing homes[2]United Nations Department of Economic and Social Affairs, “World Population Ageing,” UN, un.org . Aging magnifies pelvic-floor weakness, polypharmacy, and neurogenic bowel, expanding the candidate base for disposable pouches and neuromodulation implants. Japan’s long-term-care insurance now reimburses electronic irrigation and sacral nerve evaluation, signaling payer willingness to fund high-ticket devices that keep seniors at home. Chinese provinces include ostomy supplies on essential-drug lists, and Germany finances tibial nerve stimulation, boosting therapy penetration. Suppliers are redesigning closure clips, finger tabs, and color coding to suit arthritic hands and low vision, further embedding geriatric loyalty in the bowel management systems market.

Reimbursement Expansion in High-Income Markets

CMS lifted prior-authorization barriers for sacral neuromodulation in 2024, widening eligibility by about 120,000 Medicare beneficiaries annually. NHS England bundled a year of ostomy products into colorectal episodes, incentivizing hospitals to shift from bargain pouches to longer-wear convex barriers that cut emergency visits. Germany’s inclusion of tibial nerve stimulation delivers up to 12 reimbursed sessions, offering a step between conservative care and implant. Coverage lifts out-of-pocket shock—implant and programming can run USD 20,000—expanding uptake among fixed-income seniors. The bowel management systems market therefore sees faster revenue conversion in geographies that align reimbursement with total-cost-of-care savings.

Smart-Sensor Ostomy Pouches Enable Remote Monitoring

The FDA cleared 11Health’s Bluetooth sensor strip in 2024, giving patients a phone alert when output reaches 70% pouch capacity. Remote monitoring codes pay providers USD 50-65 per month for chronic-condition oversight, funding telehealth-nurse encounters that catch dehydration early. ConvaTec’s digital platform links wearables to its nursing network, a model that aligns with U.S. value-based contracts penalizing readmissions. Hospitals pilot sensor pouches to shorten inpatient education and off-load follow-up to virtual teams. Data generated by smart pouches also inform payer analytics on leakage rates, bolstering evidence that premium convex barriers lower peristomal dermatitis. These dynamics drive premiumization inside the bowel management systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patient preference for conservative care | -0.7% | Global, stronger in emerging markets | Short term (≤ 2 years) |

| Post-operative infections & device recalls | -0.5% | Global, heightened in North America and EU | Medium term (2-4 years) |

| High cost of neuromodulation implants | -0.4% | Emerging markets, uninsured in high-income countries | Long term (≥ 4 years) |

| Regulatory scrutiny on single-use plastic | -0.3% | EU, North America, select APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patient Preference for Conservative/Non-Invasive Care

A 2024 survey showed 68% of fecal-incontinence patients favor diet or physiotherapy over stoma formation, delaying conversion to pouch use. Cultural stigma around visible appliances amplifies hesitation in Asia, Latin America, and the Middle East. Tibial nerve stimulation offers a lower-invasiveness bridge, yet 30-40% of sessions fail to deliver durable control, leaving patients oscillating between suboptimal symptom relief and reluctance to pursue permanent diversion. Injectable bulking agents and magnetic sphincters also absorb candidates who might otherwise adopt ostomy systems. This conservatism tempers early-stage demand in the bowel management systems market.

Post-Operative Infections & Device-Recall Headwinds

The MAUDE database logged 47 ostomy-pouch adverse events in H1-2024, including 12 peristomal infections tied to adhesive delamination. Hollister’s June 2024 Class II recall of a two-piece colostomy system disrupted hospital formularies and triggered defensive stocking with rival brands. Sacral-neuromodulation implant infection rates at 5-8% often necessitate explant, souring both surgeons and payers on repeat procedures. Under EU Medical Device Regulation, Class IIb ostomy bags now require post-market clinical-follow-up, adding compliance cost and stretching launch cycles. Recalls and vigilance tighten margins while hospitals pressure vendors for more rigorous quality guarantees in the bowel management systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Nerve Modulation Outpaces Traditional Ostomy

Nerve-modulation devices logged the highest 6.25% CAGR between 2026 and 2031, benefiting from policy coverage and miniaturized leads that simplify implantation. Ostomy bags, though still 48.54% of the bowel management systems market size in 2025, are ceding share as colorectal surgeons adopt sphincter-sparing protocols. Within pouches, colostomy variants dominate due to left-sided resections, but ileostomy lines grow faster on rising IBD surgeries. Transanal irrigation systems, especially programmable electronic types, gain reimbursement in Germany and the U.K., offering an alternative for sigmoid stomas. Anal implants and magnetic sphincters open a small but high-margin niche after the FDA’s humanitarian approval of Implantica’s device in 2024. Accessory demand scales with pouch rotation; hydrocolloid rings designed for seven-day wear sell briskly to athletes who value discretion.

Suppliers hedge by bundling barriers, vent filters, and deodorizer sachets with baseplates, raising average selling price per patient episode. Recyclable pouch films bolster EU tenders, and electronic pumps with warmed saline broaden adhesion for chronic-constipation management.

By Patient Type: Geriatric Surge Reshapes Product Design

Adults aged 65+ will drive 37% of bowel management systems market growth through 2031. The segment’s 7.65% CAGR eclipses the adult-working group because polypharmacy and neurogenic bowel inflate incidence. Manufacturers add large finger grips, pre-cut apertures, and pastel color coding that contrasts against fragile skin. Japan’s insurance now underwrites electronic irrigation for chronic constipation, spurring demand for battery-operated pumps among home-bound elders[3]Ministry of Health, Labour and Welfare, “Long-Term Care Insurance Amendments,” MHLW, mhlw.go.jp. Pediatric demand stays niche yet stable, linked to congenital malformations.

Adult patients remain the core volume engine, supplying 65.54% of 2025 revenue, but geriatric-oriented upgrades lift average price. Suppliers co-design with occupational therapists to embed visual cues that simplify bag changes under tremor or cognitive decline, a differentiator at long-term-care facilities.

By End User: Home Care Gains as Hospitals Optimize Length-of-Stay

Home-care settings will post the fastest 7.82% CAGR to 2031 as CMS home-health codes finance up to 12 skilled-nursing visits for new ostomates. Hospitals, still 46.15% of 2025 revenue, compress colorectal discharge to 3-5 days, then shift education to telehealth wound-ostomy-continence nurses. Smart sensor pouches suit domiciliary oversight, providing leak alerts and volume graphs that flag dehydration earlier than self-report.

Ambulatory surgery centers leverage Medicare’s 2024 outpatient reclassification for ostomy reversal and nerve-stimulator implantation, undercutting hospital-facility fees by 30-40%. Skilled-nursing facilities buy standardized two-piece systems in bulk, trading premium sensors for cost containment. Direct-to-consumer platforms from Coloplast and ConvaTec ship subscription bundles, with courier delivery circumventing store-shelf constraints in rural zones. These logistics innovations reinforce the home-centric tilt of the bowel management systems market.

Geography Analysis

North America accounted for 38.23% of bowel management systems market size in 2025 thanks to Medicare coverage for sacral nerve stimulation and a dense network of certified wound-ostomy-continence nurses. The 2024 National Coverage Determination removed prior-authorization lag, adding roughly 120,000 fecal-incontinence beneficiaries per year. Eleven Health’s Bluetooth pouch system is live at 15 integrated delivery networks earning USD 50-65 monthly remote-monitoring fees. Canada broadened essential-benefit lists in Ontario and British Columbia, trimming patient copay. Mexico’s growth sits mostly in private clinics treating medical tourists, with government hospitals buying basic two-piece systems.

Asia-Pacific posts the fastest 6.62% CAGR, propelled by China’s 297 million seniors and India’s Ayushman Bharat package that now funds ostomy bags and irrigation. Shanghai and Guangdong pilot reimbursement for tibial nerve stimulation, while Japan’s long-term-care insurance subsidizes electronic irrigation. Australia’s Pharmaceutical Benefits Scheme added sacral nerve stimulation in 2024, reimbursing the AUD 25,000 implant. South Korea pilots bundled colorectal episodes including a year of pouch supply, signaling payer migration to value contracting across the region.

Europe’s bowel management systems market grows modestly amid MDR recertification bottlenecks that forced 30% of accessory SKUs off shelves in 2024. Germany’s statutory insurance covers tibial nerve stimulation, adding 80,000 eligible patients. NHS England bundled ostomy products into colorectal surgery tariffs, steering purchasing toward higher-quality convex barriers that curb readmissions. France and Italy test circular-economy pouch take-back modeled on Coloplast’s Dutch program. The Middle East and Africa stay nascent, with GCC private hospitals importing premium systems for expatriates, while South Africa’s public sector buys volume packs of two-piece bags. In South America, Brazil’s private insurers fund neuromodulation, but public shortages persist, keeping penetration low outside affluent metros.

Regulatory Landscape

Bowel management systems and related therapeutic devices are regulated as medical devices across major markets, with Class II pathways common for stool management kits and irrigation sets in the United States under FDA oversight. US suppliers must maintain core compliance across registration and listing (21 CFR Part 807), labeling (21 CFR Part 801), quality systems (21 CFR Part 820), and medical device reporting (21 CFR Part 803), which affects the readiness of ostomy and fecal management product lines for post-market surveillance.

In Europe, products fall under the Medical Device Regulation (EU) 2017/745 (MDR), which expanded clinical and post-market requirements versus legacy directives and tightened controls for higher-risk devices, including more structured post-market clinical follow-up for certain classes. For drug-device combinations and devices incorporating medicinal substances, MDR consultation routes can involve the European Medicines Agency (EMA) or national competent authorities, adding documentation and review steps that influence launch timing and design-control rigor. Standards updates also affect evaluation protocols, with ISO 15621:2026 providing an updated framework for assessing absorbent incontinence products for urine and feces, relevant to suppliers that span bowel and incontinence adjacencies.

Competitive Landscape

The bowel management systems market features moderate fragmentation. Coloplast, ConvaTec, and Becton, Dickinson and Company hold a notable share of the ostomy-bag slice, leveraging broad catalogs and nurse-education services. Medtronic and Boston Scientific dominate sacral neuromodulation with InterStim and Axonics-licensed platforms. Axonics’ r15 device cleared by the FDA in 2024 carries a rechargeable battery lasting 15 years, giving it a replacement-surgery cost edge. 11Health raised USD 6 million Series A to commercialize its Bluetooth sensor, creating a data-subscription annuity under U.S. remote-patient-monitoring codes.

Strategically, incumbents bolt on digital startups to add telehealth capacity; ConvaTec’s 2024 Ostomy Care portal pairs wearables with specialist nurses to lock in product loyalty. Patent filings in 2025 cluster around miniaturized leads, biodegradable substrates, and hydrocolloid blends extending wear to seven days. EU MDR’s burdens tilt advantage to capital-rich firms that can bankroll multi-year post-market studies, sidelining small suppliers. Quality lapses, such as Hollister’s 2024 flange-lock recall, prompt hospitals to shorten vendor lists to mitigate liability.

Sustainability offers a differentiation avenue: Coloplast pledges 50% bio-based polymers by 2030, while Hollister’s take-back pilot curbs landfill volumes. Implantica’s FDA-cleared magnetic sphincter fills a high-acuity gap for end-stage incontinence, but uptake depends on surgeon training and evidence of superiority over nerve stimulation. Overall, the bowel management systems market rewards portfolios that balance disposable volume with implant annuity and digital services.

Bowel Management Systems Industry Leaders

Becton, Dickinson and Company

ConvaTec Group plc

B Braun SE

Medtronic

Coloplast A/S

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Acute-care fecal management and critical-care drainage remain a focus area, supported by product innovation aimed at improving seal integrity, patient comfort, and continuous drainage performance in high-acuity settings. The May 2026 launch of Stryker's hygh-tec drainage fecal management system highlights ongoing investment in rectal catheter-based solutions for acute fecal incontinence, with hospitals prioritizing devices that reduce skin breakdown, contamination risk, and nursing workload in ICUs.

In chronic care, whitespace persists around simplified, portable transanal irrigation (TAI) and digitally enabled bowel-care pathways that fit home-care workflows and remote follow-up. Coloplast's Peristeen Light launch in 2024 reflects continued movement toward lower-volume, more portable TAI to support adherence, while clinical research activity around smart TAI systems and digital biofeedback is sharpening the evidence base for premium positioning and reimbursement discussions. Separately, consolidation and channel build-out in home-care oriented bowel management, including UK-focused vertical integration and portfolio acquisitions, is creating room for integrated product-plus-service models that bundle consumables, education, and monitoring to reduce leakage-related complications and avoidable care utilization.

Recent Industry Developments

- June 2026: Galmed Pharmaceuticals completed the acquisition of Colospan Ltd., adding the CG-100 intraluminal bypass device used in colorectal surgery. The acquisition broadens access to technologies intended to reduce post-surgical complications and potentially decrease the need for diversion, while bringing adjacent colorectal procedural tools closer to bowel management pathways.

- August 2025: Clinisupplies acquired the Renew Inserts portfolio from Renew Medical Inc. and Renew Medical UK Limited, expanding its bowel management offering in chronic care. The transaction increases portfolio depth for home-delivery and long-term management programs, where product breadth and dispensing capability can influence patient retention.

- February 2024: Coloplast launched Peristeen Light, a low-volume transanal irrigation device aimed at people with bowel disorders. The launch reinforces the shift toward more portable and simpler irrigation approaches that support self-management and can broaden adoption beyond specialist centers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the bowel management systems market covers medical devices and related consumables used to manage fecal incontinence and support safe stool collection, diversion, or controlled evacuation across care settings.

Scope exclusions: We exclude pharmaceuticals, general wound dressings not designed for bowel care, and clinical services that are billed separately from device supply.

Segmentation Overview

- By Product

- Ostomy Bags

- Colostomy Bags

- Ileostomy Bags

- Urostomy Bags

- Transanal Irrigation Systems

- Manual Pump-based Irrigation

- Electronic Smart Irrigation

- Nerve Modulation Devices

- Sacral Nerve Stimulation Systems

- Tibial Nerve Stimulation Systems

- Anal Implants & Artificial Sphincters

- Hydraulic Artificial Sphincters

- Magnetic Sphincters

- Skin Barriers & Accessories

- Skin Barrier Sheets & Rings

- Deodorizing Filters & Pouch Accessories

- Ostomy Bags

- By Patient Type

- Pediatric (<18 yrs)

- Adult (18-64 yrs)

- Geriatric (65+ yrs)

- By End User

- Hospitals

- Ambulatory Surgery Centers

- Home Care Settings

- Skilled Nursing Facilities

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary and pick demand and supply signals that can be tracked each year. We mainly reviewed public health statistics and care-delivery indicators from sources such as the US CDC, the WHO, and OECD health data, followed by medical device safety and registration information from agencies such as the US FDA and the European Commission medical device resources.

To translate these signals into a workable sizing model, we also used evidence from peer reviewed clinical literature (such as studies on fecal incontinence burden and management pathways), government procurement and reimbursement references where available, and manufacturer public documents like annual reports and investor presentations. For extra checks, we used paid subscriptions for company financials and intelligence, plus patent databases to understand product pipeline timing. The specific desk sources listed above are illustrative only and are not exhaustive, and other public references were also used for collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how bowel management products are used in hospitals, ambulatory centers, and home care, and on confirming price bands, utilization patterns, and replacement frequency for key device categories. Interviews and surveys were split across manufacturers, distributors, clinicians, and procurement stakeholders across major regions so our assumptions could be corrected where secondary information was thin.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 18% | APAC: 46% |

| Mid tier: 52% | Functional/Unit leaders: 33% | EMEA: 29% |

| Smaller Players: 19% | Managers: 49% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts from a top-down view where treated patient pools and care-setting usage patterns are reconstructed using prevalence signals, procedure volumes, and the typical care pathway for bowel control and diversion. Once that demand pool is set, annual consumption is built using practical inputs such as device adoption by setting, replacement frequency for consumables, average selling price ranges by product group, and the share of cases managed with irrigation or neuromodulation options.

The total is then corroborated through selective bottom-up approximations, including sampled revenue ranges for key suppliers, distributor channel checks, and volume times ASP spot checks for high-velocity consumables, which helps us adjust for gaps where public disclosure is limited. For forecasting, scenario analysis is used because uptake is influenced by reimbursement changes, hospital protocol updates, and the speed at which newer nerve modulation and remote monitoring enabled solutions enter routine use. Assumptions are finalized only after outputs align with the quantitative signals and the feedback heard in primary discussions.

Data Validation & Update Cycle

Model outputs are checked against independent signals such as regional healthcare spending direction, facility expansion trends, and the pace of relevant procedure and device adoption, and then outliers are investigated before numbers are finalized. When a variance cannot be explained by scope or timing, the inputs are reworked and, if needed, respondents are re-contacted to verify the assumption that caused the gap.

Each report goes through multi-step analyst review, where definitions, conversions, and year mapping are rechecked to avoid accidental double counting across product categories and settings. Updates are done annually, and interim refreshes are triggered when material regulatory, reimbursement, or demand events occur. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Bowel Management Systems Market Estimate Compared With Other Published Estimates

Published values for this market can look far apart because different studies choose different product inclusions and different base years, and then they apply different adoption and pricing assumptions across hospital and home care settings.

Procedure utilization signals and care-setting usage checks, supported by price band validation from distributor and hospital purchasing conversations, help keep Mordor Intelligence tied to bowel-management specific device and consumable demand rather than adjacent ostomy and general continence items.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.68 B (2026) | |

| Global Consultancy A | USD 1.79 B (2024) | Uses an earlier base year and a tighter product list focused on core device types, which can undercount accessories and some setting-level utilization captured in broader pathway builds. |

| Regional Consultancy B | USD 2.80 B (2024) | Anchors on a 2024 base with different ASP progression assumptions, and the scope may bundle adjacent continence and accessory revenues that are not always directly linked to bowel management use. |

The comparison shows that most of the spread comes from year alignment and what is treated as in-scope device and accessory revenue. By separating care settings clearly, using repeatable demand indicators, and then checking totals with pricing and utilization feedback, the number stays traceable to inputs that can be revisited during updates.

Key Questions Answered in the Report

What is the current value of the bowel management systems market?

The bowel management systems market size stood at USD 2.68 billion in 2026.

How fast will demand for nerve-modulation devices grow?

Nerve-modulation devices are advancing at a 6.25% CAGR between 2026 and 2031.

Which region delivers the fastest growth?

Asia-Pacific leads with a projected 6.62% CAGR through 2031, propelled by aging demographics and expanding reimbursement.

Why are smart-sensor pouches gaining traction?

Bluetooth-enabled pouches support remote monitoring codes that pay providers USD 50-65 per month, cutting leak-related readmissions.

How are ESG rules influencing product design?

EU extended-producer-responsibility fees push manufacturers toward bio-based films, reducing carbon footprints by up to 40%.

Page last updated on: