Hyperpigmentation Treatment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

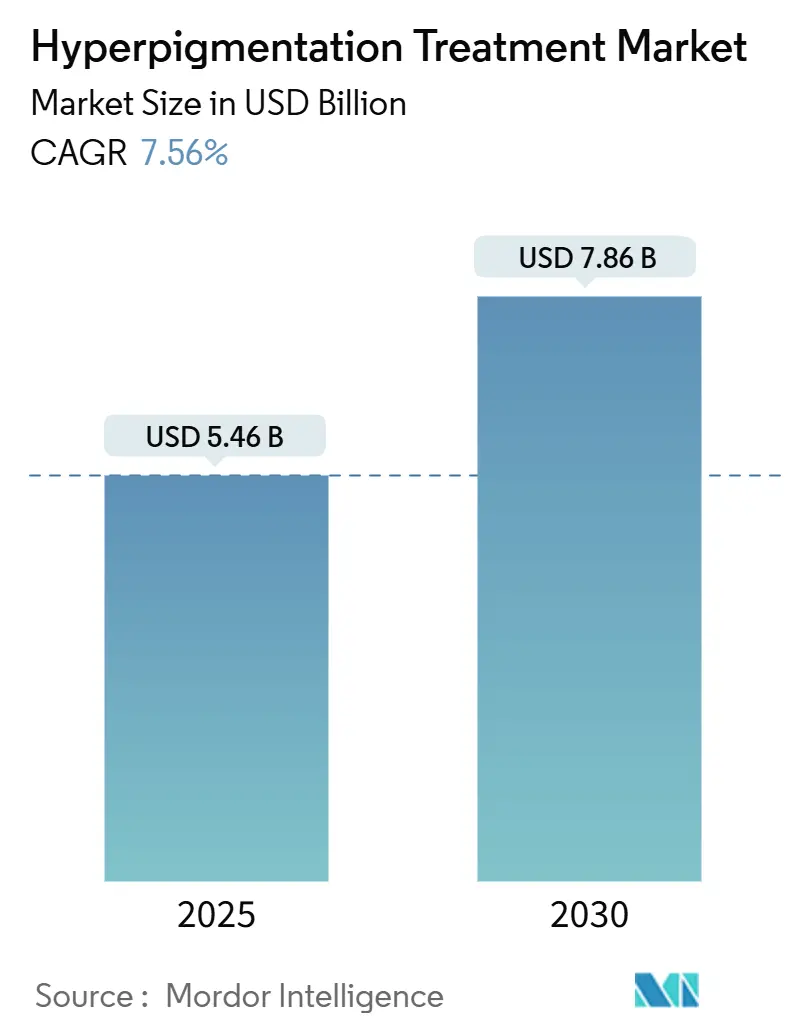

| Market Size (2025) | USD 5.46 Billion |

| Market Size (2030) | USD 7.86 Billion |

| Growth Rate (2025 - 2030) | 7.56% CAGR |

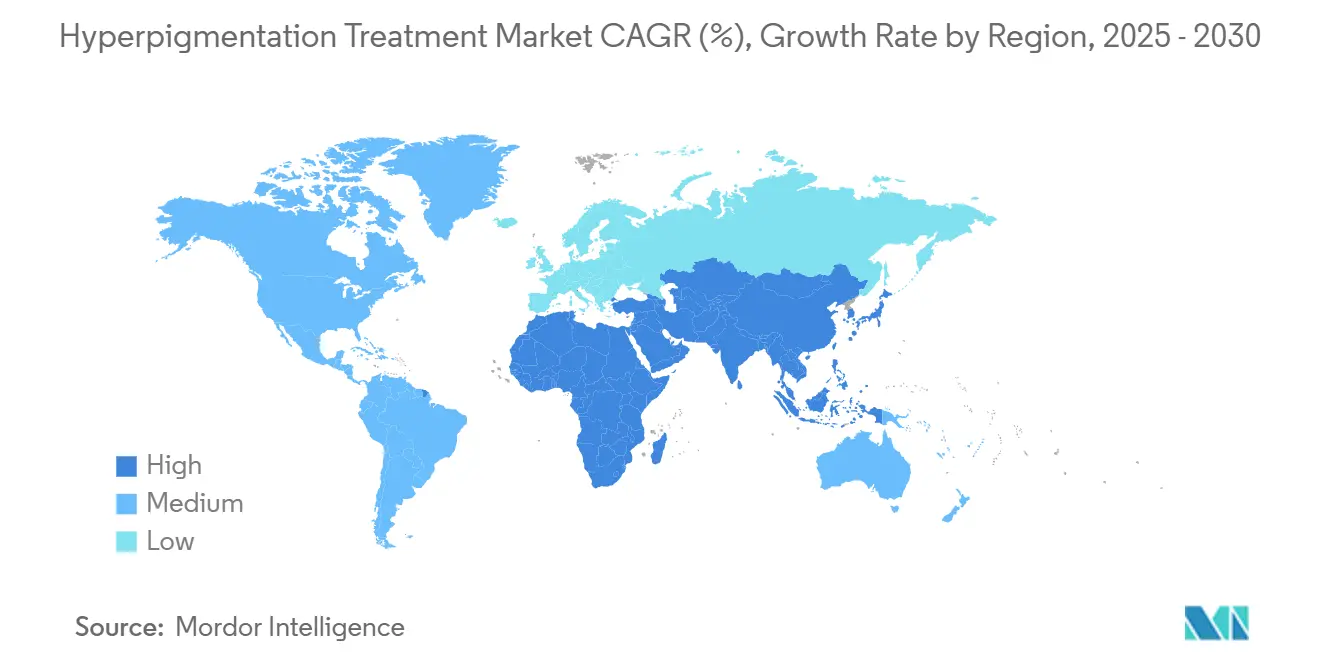

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hyperpigmentation Treatment Market Analysis by Mordor Intelligence

The hyperpigmentation treatment market size stood at USD 5.46 billion in 2025 and is projected to reach USD 7.86 billion by 2030, advancing at a 7.56% CAGR. Demand is expanding as consumers increasingly pursue skin-tone correction within preventive wellness regimens, prompting repeat clinic visits and at-home maintenance purchases. Breakthroughs in picosecond, 675-nm and focal-point laser platforms shorten downtime and cut post-inflammatory risks, broadening eligibility across darker Fitzpatrick types. Tele-dermatology further lifts the hyperpigmentation treatment market by connecting underserved patients to specialists, while AI-driven imaging tools refine treatment selection and adherence. Melasma and post-inflammatory hyperpigmentation (PIH) remain core revenue drivers, yet safer tranexamic-acid topicals are drawing preventive users into the over-the-counter channel. Regionally, North America leads on procedure volumes, whereas Asia-Pacific posts the fastest growth as medical-tourism hubs and rising incomes converge.

Key Reprot Takeaways

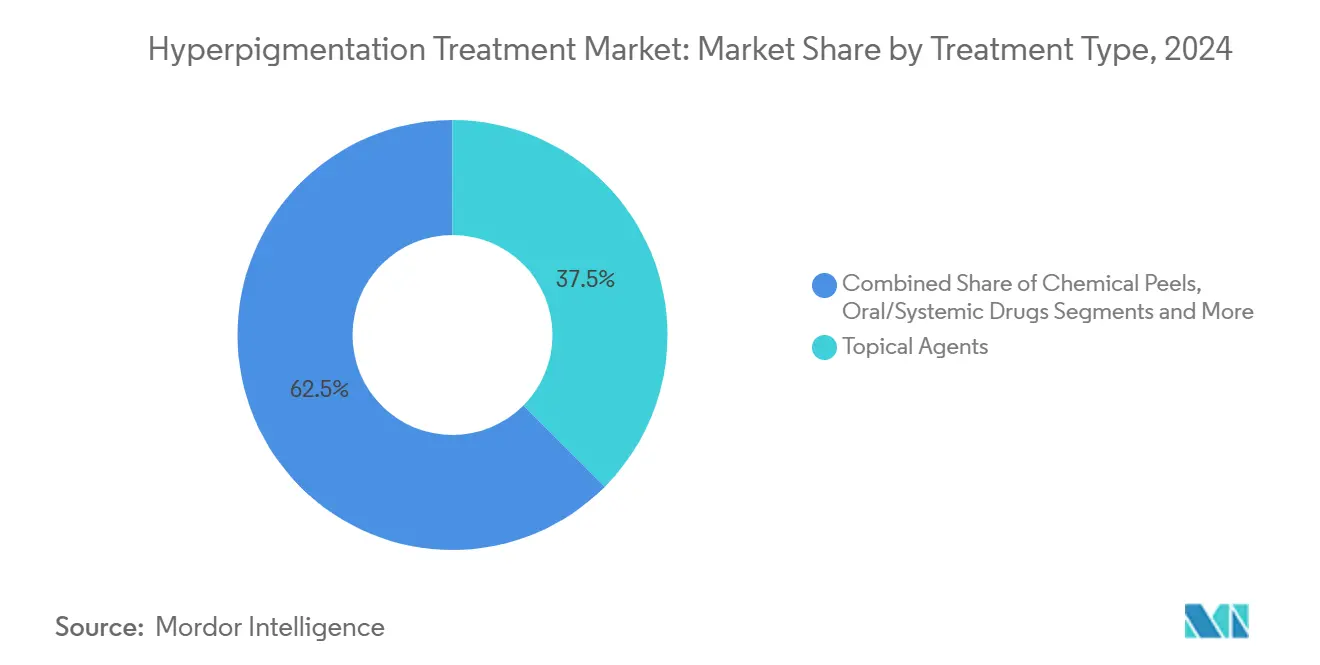

- By treatment type, topical agents captured 37.46% of the hyperpigmentation treatment market share in 2024. Laser and light-based therapy is expanding at an 11.47% CAGR, the quickest among all modalities.

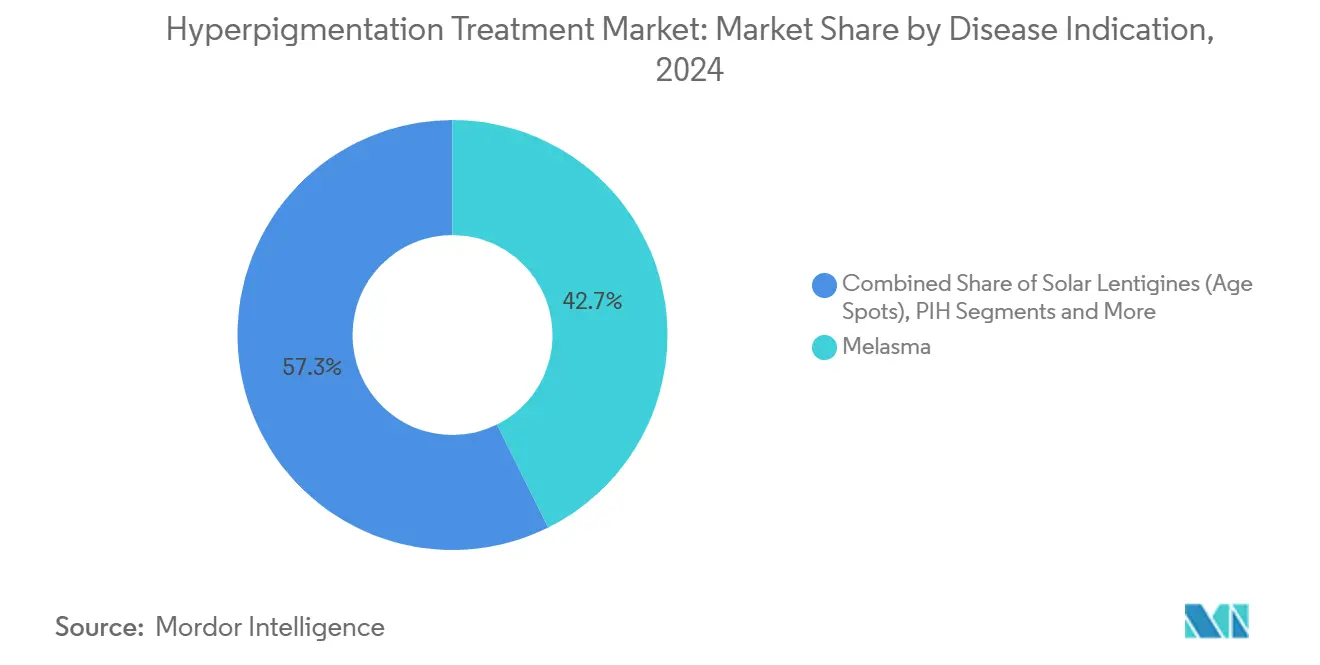

- By disease indication, melasma led with 42.66% revenue in 2024, while post-inflammatory hyperpigmentation is forecast to grow at 11.36% CAGR through 2030.

- By end-user, dermatology clinics held 45.28% of the hyperpigmentation treatment market size in 2024; med-spa centers are advancing at a 10.13% CAGR.

- By Geography, north america commanded 41.24% revenue in 2024, while Asia-Pacific is on track for the highest regional growth at a 9.33% CAGR

Global Hyperpigmentation Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand For Aesthetic Dermatology Procedures | + 2.1% | Global, strongest in North America & Asia-Pacific | Medium term (2-4 years) |

| Rising Incidence Of Melasma & PIH In Populations Of Color | + 1.8% | Global, concentrated in Asia-Pacific & Africa | Long term (≥ 4 years) |

| Technology Advances In Energy-Based Devices & Lasers | + 1.5% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| OTC Adoption Of Safer Tranexamic-Acid-Based Topicals | + 1.2% | Global, early gains in developed markets | Medium term (2-4 years) |

| Tele-Dermatology Enabling Remote Regimen Monitoring | + 0.8% | Global, accelerated in underserved regions | Short term (≤ 2 years) |

| Expanding E-Commerce & Social-Commerce Channels | + 0.7% | Global, led by Asia-Pacific digital adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Aesthetic Dermatology Procedures

Aesthetic medicine clinics report sustained double-digit appointment growth as pigment correction shifts from vanity to self-care, motivating earlier intervention among millennials and rising male participation. Social platforms magnify awareness of uneven skin tone, and financing plans reduce upfront cost barriers. The hyperpigmentation treatment market benefits because pigment-removal sessions often bundle with complementary rejuvenation services, lifting average spend per visit. Med-spas translate demand into geographic reach, establishing satellite sites that bring procedures closer to suburban consumers. Scalability of these outlets produces steady pipeline volume for topical maintenance products, closing the loop between in-clinic and at-home care.

Rising Incidence of Melasma & PIH in Populations of Color

Clinical audits show melasma and PIH prevalence rising in darker skin tones, where traditional retinoids yield partial relief for 85% of patients.[1]Touraj Khosravi-Hafshejani, “Treatment of Post-Inflammatory Hyperpigmentation in Skin of Colour: A Systematic Review,” SAGE Journals, journals.sagepub.com New diagnostic scores such as PIDASI and PIHASI, each holding inter-rater reliability above 0.93, standardize outcome tracking for diverse epidermal phenotypes.[2]Jayant Bhawalkar, “Focal Point Technology: Controlling Treatment Depth and Pattern of Skin Injury,” Journal of the American Academy of Dermatology, jaad.org Awareness programs underscore sunscreen’s 100% prevention efficacy for PIH when applied consistently. Research initiatives like the University of Basel’s PASSION database, which houses 4,200+ images of pigmented lesions in dark skin, enable AI-assisted triage and accelerate guideline refinement. These developments collectively channel higher patient volumes toward evidence-based interventions, lifting procedure counts within the hyperpigmentation treatment market.

Technology Advances in Energy-Based Devices and Lasers

Continuous upgrades in focal-point, 675-nm and picosecond platforms have pushed laser precision to the micron level, sparing the epidermis and slashing post-inflammatory risk for Fitzpatrick IV–VI patients. Multimodal consoles now layer fractional, Q-switched and non-ablative modes in a single hand-piece, reducing session counts and elevating satisfaction scores recorded across diverse skin tones. Capital investment pays back quickly for clinics because pigment correction packages often bundle with rejuvenation add-ons, lifting overall ticket value. The April 2024 combination of Cynosure and Lutronic gathered more than 470 active patents under one roof, accelerating next-generation roadmap execution across 130 countries. These structural gains funnel new-release devices into the hyperpigmentation treatment market at a faster cadence, intensifying upgrade cycles and broadening practitioner toolkits.

Over-the-Counter Adoption of Safer Tranexamic-Acid-Based Topicals

Regulators continue to scrutinize hydroquinone, nudging physicians and consumers toward alternative bleaching chemistry. Peer-reviewed trials on 3% tranexamic-acid creams report 13% color-intensity decline and 6% dark-spot-size reduction within eight weeks, paired with 95% patient-reported hydration gains. Encapsulation in liposomal and PLGA carriers enhances dermal permeation and lengthens drug residence time, allowing once-daily regimens that improve adherence. Retail giants now allocate dedicated shelf space to pigment correctors, expanding discovery beyond dermatology offices. As a result, entry-level consumers join the hyperpigmentation treatment market earlier in their skin-care journey, creating annuity-style revenue streams for manufacturers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Bans & Safety Concerns Around Hydroquinone | -1.4% | EU, Japan, Australia; proposed US restrictions | Short term (≤ 2 years) |

| High Procedure Cost & Limited Reimbursement | -1.1% | Global, acute in developing markets | Long term (≥ 4 years) |

| Shortage Of Trained Aesthetic Dermatologists In LMICs | -0.9% | Africa, South Asia, rural regions globally | Long term (≥ 4 years) |

| Counterfeit/Lightening-Cream Grey Market Eroding Trust | -0.7% | Africa, Southeast Asia, unregulated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Bans and Safety Concerns Around Hydroquinone

The European Union, Japan and Australia prohibit hydroquinone in cosmetics, and the U.S. Food and Drug Administration now classifies over-the-counter formats as unapproved drugs, citing ochronosis and carcinogenicity signals. Dose-dependent liver-injury pathways mapped through SCD1–AMPK signaling further reinforce toxic-risk profiles.[3]Lijun Zou, “Dose-Dependent Effects of Hydroquinone on Liver Injury,” PubMed, pubmed.ncbi.nlm.nih.gov Fragmented regulations complicate global brand labeling and add compliance overhead, delaying new-product rollouts inside the hyperpigmentation treatment market.

High Procedure Cost and Limited Reimbursement

Energy-based pigment removal demands multiple passes priced in the low-four-figure range, expenses rarely covered by insurers that classify the service as cosmetic. Out-of-pocket burden suppresses adoption among middle-income groups, especially in countries where disposable income trails global averages. Inflation-driven wage pressure on clinic staffing pushes session fees higher, widening the affordability gap and tempering growth momentum for the hyperpigmentation treatment market size in cost-sensitive territories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Topical Innovation Drives Market Leadership

Topical agents accounted for 37.46% of the hyperpigmentation treatment market share in 2024, retaining the lead as safer tranexamic-acid creams displaced hydroquinone in many physician protocols. Liposomal and poly-lactic-co-glycolic carriers now boost skin permeation and let users maintain results between in-clinic sessions. Chemical peels built around mandelic-acid or gluconolactone combinations add steady revenue because they double as hydration boosters that increase procedure adherence. Laser and light-based therapy posted the quickest advance at an 11.47% CAGR as multimodal consoles folded picosecond, fractional and Q-switched wavelengths into single hand-pieces, cutting session counts while widening skin-tone eligibility.

R&D pipelines emphasize pigment-modulating peptides and botanicals that sidestep regulatory scrutiny tied to traditional bleaching agents. Evidence shows 3% tranexamic-acid serums deliver 13% color-intensity decline within eight weeks with minimal irritation across Fitzpatrick types I–VI. Market leaders bundle these actives with niacinamide or azelaic acid to create multi-mechanism regimens that anchor patient loyalty. The hyperpigmentation treatment market benefits because topical continuity drives repeat purchase even after in-office clearance, creating an annuity stream that cushions seasonal demand swings.

By Disease Indication: PIH Acceleration Reflects Demographic Shifts

Melasma retained 42.66% revenue leadership in 2024, but post-inflammatory hyperpigmentation logged an 11.36% CAGR, the sharpest among indications tracked within the hyperpigmentation treatment market size forecast to 2030. Rising acne incidence and aesthetic-procedure uptake in skin-of-color cohorts elevate PIH caseloads that demand longer-term pigment control strategies. Newly validated scoring tools such as PIDASI and PIHASI—with inter-rater reliability above 0.93—let clinicians benchmark progress objectively, encouraging guideline-based care that often combines laser passes with topical maintenance.

Solar lentigines stay prominent among aging populations seeking photo-damage reversal, and complete lesion removal in a single 675-nm pass has been documented with vasculature-sparing laser surgery systems. Freckles, ephelides and other localized disorders now gain access to cosmetic-grade inhibitors such as thiamidol, whose tyrosinase suppression surpasses traditional kojic-acid benchmarks without safety flags. Combination protocols pairing low-fluence Q-switched Nd:YAG pulses with oral or topical tranexamic acid show synergistic clearance in recalcitrant entities like Riehl melanosis, expanding therapeutic optimism for difficult pigmentary conditions.

By End-User: Med-Spa Expansion Reshapes Treatment Delivery

Dermatology clinics commanded 45.28% of revenue in 2024 by managing complex or refractory cases requiring biopsy, dermoscopy or systemic therapy oversight. Yet med-spa centers are scaling fastest at a 10.13% CAGR, riding a footprint jump from 8,899 to 10,488 locations between 2022 and 2023 in the United States alone. Consumers gravitate to these outlets for bundled pigment correction and rejuvenation packages presented in wellness-oriented environments.

Hospital outpatient wings and specialty clinics preserve share by integrating dermatology with endocrinology or obstetrics where hormonal triggers underlie melasma. Meanwhile, at-home device makers target maintenance phases with low-energy LEDs and digital coaching apps that sync to dermatologist dashboards, fortifying adherence and bringing fresh users into the hyperpigmentation treatment market. This tiered delivery model diffuses capacity constraints, widening geographic reach without eroding clinical quality.

Geography Analysis

North America retained 41.24% revenue share in 2024 on the back of high procedure volumes, strong specialist density and clear post-marketing surveillance rules that speed device approvals. Proposed U.S. restrictions on hydroquinone are prompting formulators to pivot toward peptide and tranexamic-acid complexes, reshaping the regional hyperpigmentation treatment market outlook. Canada’s health authorities intensified seizures of illegal mercury creams, fostering consumer trust in regulated channels and nudging latent demand toward certified clinics.

Asia-Pacific is advancing at a 9.33% CAGR through 2030, making it the fastest-growing node inside the global hyperpigmentation treatment market. Rising disposable incomes intersect with high melasma prevalence to pull laser consoles and premium topicals into urban dermatology corridors. Medical-tourism clusters in South Korea and Thailand advertise pigment packages bundled with recovery stays, while China’s cross-border e-commerce corridors speed product imports that comply with evolving ingredient caps. Regional researchers also lead AI image-library creation for darker skin tones, closing diagnostic gaps and funneling more cases into evidence-based care pathways.

Europe maintains steady growth despite stringent ingredient curbs, including an April 2025 limit that caps kojic acid at 1% and places alpha-arbutin on the restricted list, a move pushing brands to reformulate flagship serums. These guardrails stimulate R&D around azelaic-acid, niacinamide and thiamidol alternatives, preserving momentum in the hyperpigmentation treatment market size across the region. Middle East and Africa grapple with counterfeit-cream crackdowns but see opportunity in tech-enabled tele-dermatology rollouts, while South America’s private-clinic networks invest in 675-nm and picosecond systems to meet growing aesthetic tourism inflows.

Competitive Landscape

Heightened deal activity is reshaping the hyperpigmentation treatment market as private-equity backed Hahn & Co. merged Cynosure and Lutronic in April 2024, pooling 470 patents and a 130-country sales footprint to speed next-generation laser rollouts. Galderma followed with record USD 1.129 billion Q1 2025 revenue on the strength of Relfydess neuromodulator and an expanded co-development pact with L'Oréal, reinforcing the value of proprietary pipelines inside the hyperpigmentation treatment market. Collectively, these moves intensify competition on device efficacy, treatment safety and brand reach.

Artificial-intelligence adoption is becoming a strategic differentiator within the hyperpigmentation treatment market, with VISIA-based melanin indexing and 3-D facial mapping enabling clinics to promise measurable outcomes and thus justify premium pricing. L'Oréal's launch of Melasyl™, supported by 121 peer-reviewed studies, illustrates how ingredient exclusivity can secure shelf space across mass, dermocosmetic and professional channels simultaneously. Device manufacturers are also bundling software updates that unlock new pulse parameters, creating recurring-revenue models that lift lifetime customer value.

Financial resilience is gaining weight in vendor selection criteria as Cutera's March 2025 Chapter 11 plan shaved USD 400 million in debt while preserving R&D investment, signaling that balance-sheet health underpins sustained innovation cycles in the hyperpigmentation treatment market. Smaller specialty formulators are targeting white-space niches such as pregnancy-safe serums, but elevated clinical-evidence thresholds and tightening ingredient rules in Europe raise barriers to entry. With the top five players holding a substantial share of 2025 revenue, competitive intensity remains moderate, rewarding differentiated science and omni-channel execution.

Hyperpigmentation Treatment Industry Leaders

AbbVie

Galderma S.A.

Bayer AG

L’Oréal Group

Candela Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Alkem Laboratories introduced Kojiglo serum in India, the first domestic liposomal pigment-corrector using Duo-Lipo technology.

- January 2025: Allergan Aesthetics unveiled the AA Signature Program at IMCAS 2025, combining personalized facial-mapping protocols with its injectable and topical lines.

- December 2024: Koru Pharma released the three-product Mesoheal Glow Series—Pink Glow, Amber Glow and Orchid Glow—to address distinct pigmentation concerns.

Global Hyperpigmentation Treatment Market Report Scope

| Topical Agents |

| Chemical Peels |

| Laser / Light-based Therapy |

| Microdermabrasion & Dermabrasion |

| Oral/Systemic Drugs |

| Melasma |

| Solar Lentigines (Age Spots) |

| Post-Inflammatory Hyperpigmentation (PIH) |

| Freckles, Ephelides & Others |

| Dermatology Clinics |

| Aesthetic / Med-Spa Centers |

| Hospitals & Specialty Clinics |

| Home-use / OTC Consumers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Topical Agents | |

| Chemical Peels | ||

| Laser / Light-based Therapy | ||

| Microdermabrasion & Dermabrasion | ||

| Oral/Systemic Drugs | ||

| By Disease Indication | Melasma | |

| Solar Lentigines (Age Spots) | ||

| Post-Inflammatory Hyperpigmentation (PIH) | ||

| Freckles, Ephelides & Others | ||

| By End-User | Dermatology Clinics | |

| Aesthetic / Med-Spa Centers | ||

| Hospitals & Specialty Clinics | ||

| Home-use / OTC Consumers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the hyperpigmentation treatment market?

The market was valued at USD 5.46 billion in 2025 and is forecast to hit USD 7.86 billion by 2030.

Which treatment modality is growing fastest?

Laser and light-based therapy is registering an 11.47% CAGR through 2030, the highest among all modalities.

Why is post-inflammatory hyperpigmentation attracting attention?

PIH cases are climbing in skin-of-colour populations and are projected to expand at an 11.36% CAGR, outpacing melasma.

Which region shows the strongest growth outlook?

Asia-Pacific is set to advance at a 9.33% CAGR, supported by rising incomes and a robust medical-tourism ecosystem.

How are safety regulations affecting product pipelines?

Ingredient bans on hydroquinone and kojic acid in several regions are accelerating R&D into tranexamic-acid, thiamidol and peptide alternatives.

Who are the key players shaping innovation?

Multinationals such as Galderma, L’Oréal, Cynosure-Lutronic and Allergan Aesthetics lead device and topical breakthroughs while smaller firms focus on niche formulations.

Page last updated on: