Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

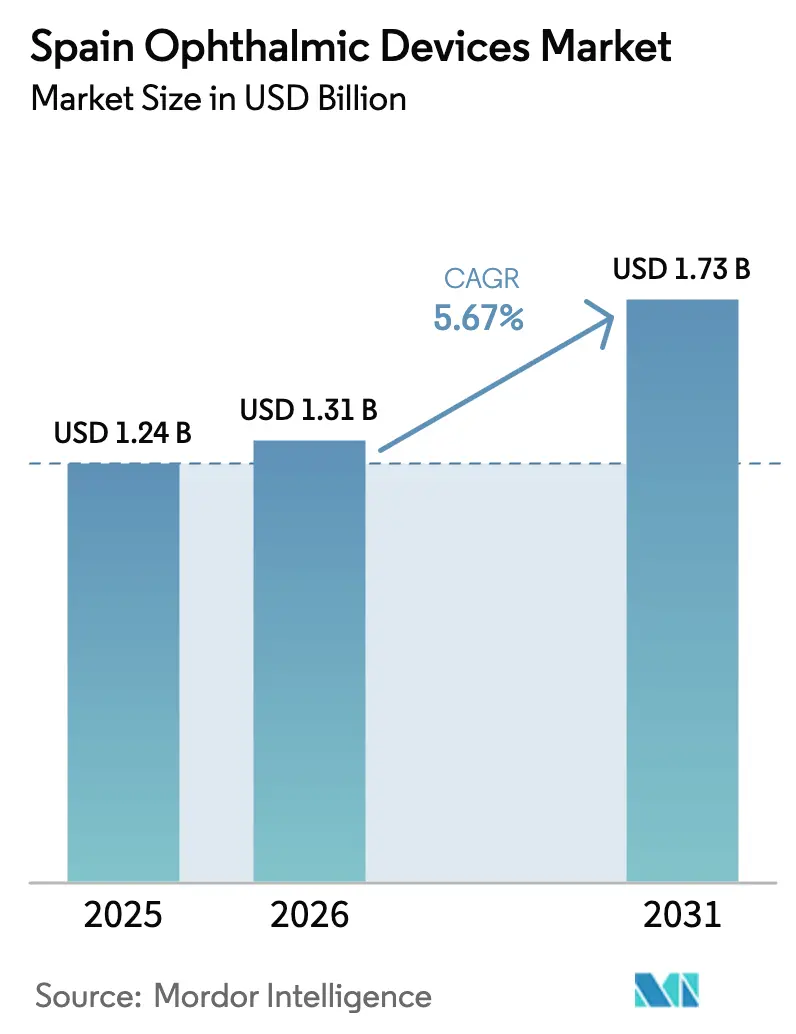

| Base Year Market Size (2025) | USD 1.24 Billion |

| Market Size (2026) | USD 1.31 Billion |

| Market Size (2031) | USD 1.73 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Ophthalmic Devices Market Analysis by Mordor Intelligence

The Spain Ophthalmic Devices Market size is projected to expand from USD 1.24 billion in 2025 and USD 1.31 billion in 2026 to USD 1.73 billion by 2031, registering a CAGR of 5.67% between 2026 to 2031.

Spain’s rapid demographic shift toward an older population is expanding demand for cataract, glaucoma, and age-related macular degeneration care. Public-sector stimulus under the Recovery, Transformation and Resilience Plan is shortening replacement cycles for surgical microscopes, optical coherence tomography (OCT) scanners, and phacoemulsification consoles. Artificial intelligence in fundus cameras and OCT systems is easing physician workload and accelerating diabetic-retinopathy screening, while inbound medical tourism sustains premium refractive demand along the Mediterranean coast. At the same time, hospital sustainability targets are nudging buyers toward bio-based single-use instruments, adding a green dimension to procurement criteria.

Key Report Takeaways

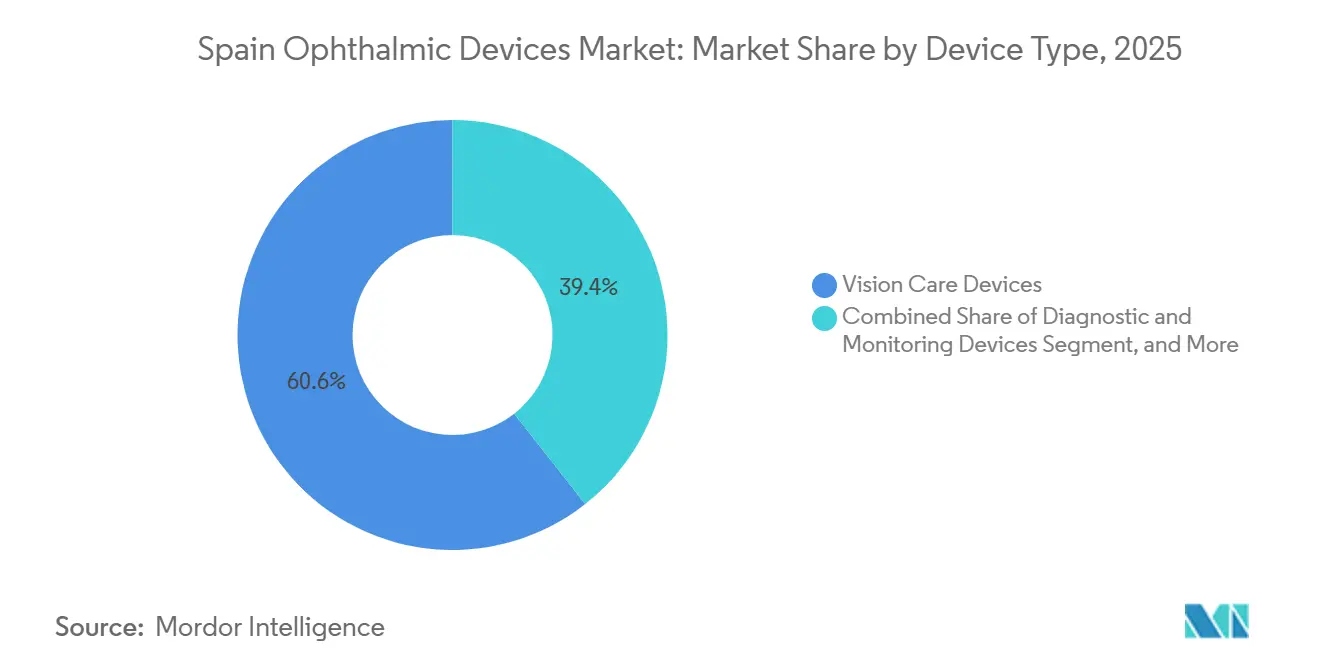

- By device type, vision-care products led the Spain ophthalmic devices market with 60.59% market share in 2025, whereas diagnostic and monitoring devices are forecast to log a 7.64% CAGR through 2031.

- By disease indication, cataract accounted for 37.66% of the Spain ophthalmic devices market in 2025, while diabetic retinopathy devices are expected to expand at a 6.98% CAGR between 2026 and 2031.

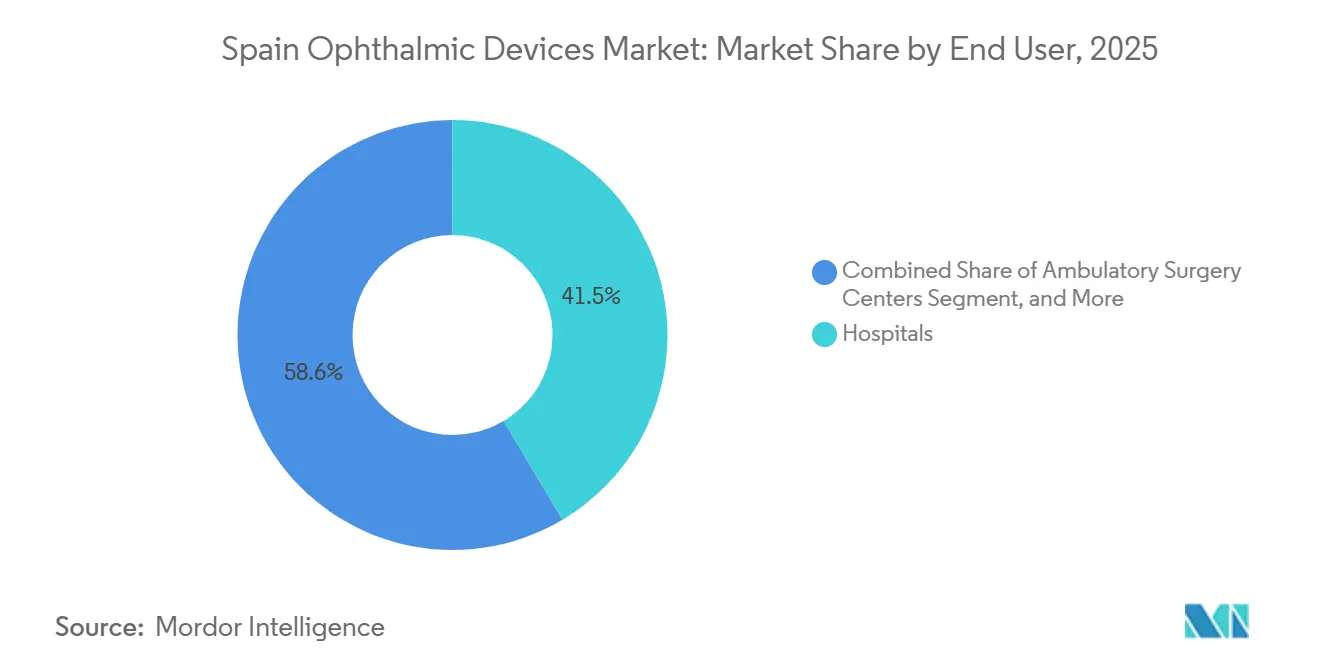

- By end user, hospitals accounted for 41.45% of the Spain ophthalmic devices market in 2025; ambulatory surgery centers are projected to post a 9.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Ophthalmic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly ageing population driving cataract, AMD and glaucoma procedures | +1.2% | Galicia, Castilla y León, Asturias | Long term (≥ 4 years) |

| AI-enabled OCT and fundus imaging adoption across hospitals | +0.8% | Catalonia, Madrid, Navarre | Medium term (2-4 years) |

| Government recovery-plan funding for ophthalmic equipment | +1.0% | Nationwide underserved areas | Short term (≤ 2 years) |

| Expansion of private ophthalmology chains | +0.9% | Madrid, Barcelona, Valencia | Medium term (2-4 years) |

| Inbound medical tourism for refractive and cataract surgery | +0.5% | Costa del Sol, Balearic Islands | Medium term (2-4 years) |

| Hospital sustainability targets favoring bio-based instruments | +0.3% | Catalonia, Basque Country | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapidly Ageing Population Driving Cataract, AMD & Glaucoma Procedures

Life expectancy reached 83.2 years in 2024, and the share of citizens aged 65 or above rose to 20.4% in 2025, trends projected to accelerate through 2050.[1]Instituto Nacional de Estadística, “Population Projections 2024-2050,” ine.es Cataract prevalence now exceeds 60% among Spaniards older than 70, generating roughly 450,000 surgeries each year. Regions with the oldest populations are refreshing their phaco systems and premium intraocular-lens inventories to meet demand. Universal insurance coverage stabilizes procedure volumes, yet rural dispersion steers interest to portable OCT scanners and smartphone fundus cameras for primary-care triage.

AI-Enabled OCT & Fundus Imaging Adoption Across Spanish Hospitals

Navarre’s NaIA-RD platform screened 78,000 diabetic patients in 2024 with 94% sensitivity, and Catalonia’s MIRA network processed more than 100,000 images in the same year.[2]Ministerio de Sanidad, “Recovery Plan Component 18 Equipment Renewal,” sanidad.gob.es These pilots relieve specialist bottlenecks, important because Spain has one ophthalmologist for every 4,200 residents. Vendors now embed AI into device firmware; Heidelberg Engineering’s SPECTRALIS update trims image-interpretation time to two minutes. Regulatory backing is solid, with 12 CE marks for ophthalmic AI software granted in 2024.

Government Recovery-Plan Funding for Ophthalmic Equipment

Component 18 of the national plan earmarked EUR 1.2 billion (USD 1.3 billion) for the installation of 750 high-tech devices by December 2025. Extremadura and Castilla-La Mancha allocated more than EUR 40 million to OCT and femtosecond platforms. Replacement cycles are shrinking; the average age of phaco consoles fell from 9.2 years in 2023 to 7.4 years in 2025.

Expansion of Private Ophthalmology Chains Boosting Device Procurement

Clínica Baviera operates 83 clinics and spent EUR 12 million in 2024 to deploy 15 new femtosecond lasers. Miranza, now part of Veonet, posts annual revenue of EUR 83 million and standardizes its equipment fleet to secure volume rebates. Waiting times in public hospitals average 112 days for cataract surgery, compared with 18 days in private clinics, accelerating patient migration and device uptake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost and restricted reimbursement for premium devices | −0.7% | Budget-constrained regions | Short term (≤ 2 years) |

| Stringent EU MDR and AEMPS approval timelines | −0.5% | Nationwide | Medium term (2-4 years) |

| Shortage of skilled ophthalmic technicians | −0.4% | Rural provinces | Medium term (2-4 years) |

| Budget disparities between autonomous communities | −0.6% | Low-income regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost & Restricted Reimbursement for Premium Devices

Femtosecond lasers cost between EUR 400,000 and EUR 600,000, yet public reimbursement per cataract case is EUR 1,850, unchanged since 2019. Private insurers cover upgrades only in high-tier plans, limiting access to 18% of privately insured citizens. Hospitals, therefore, favor durable, high-throughput systems over premium platforms, bifurcating the Spanish ophthalmic devices market into cost-focused public tenders and technology-driven private clinics.

Stringent EU MDR / AEMPS Approval Timelines

EU MDR extended regulatory clearance from 6 to 18 months, cutting Spain’s ophthalmic submissions by 28% in 2024. Fourteen niche suppliers exited Europe amid compliance costs, leading to short-term shortages of pediatric lenses and toric implants.[3]MedTech Europe, “Industry Survey 2024,” medtecheurope.org Hospitals now face nine-to-twelve-month lead times for newly certified devices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Vision Care Dominates, Diagnostics Accelerate

Vision Care Devices held 60.59% of Spain ophthalmic devices market share in 2025, anchored by 1,200 optical stores run by EssilorLuxottica’s GrandVision and Multiópticas, while CooperVision lenses secured about 28% of contact-lens revenue. Diagnostic & Monitoring Devices will post a 7.64% CAGR to 2031, the fastest among categories, because hospitals invest in swept-source OCT and AI-ready fundus cameras. OCT scanners alone account for 37% of diagnostic revenue, and Carl Zeiss Meditec and Heidelberg Engineering units are present in roughly 65% of public hospitals.

Spain ophthalmic devices market size for surgical platforms is rising as femtosecond lasers replace manual capsulotomy, and micro-invasive glaucoma implants see wider pairing with cataract procedures. Vitreoretinal tools are shifting to 27-gauge instrumentation for faster recovery, and robotic prototypes are slated for commercial launch after 2026.

By Disease Indication: Cataract Leads, Diabetic Retinopathy Surges

Cataract captured 37.66% of 2025 revenue. More than 1.2 million Spaniards qualify clinically for surgery, but capacity limits keep annual volumes at 450,000. Spain's ophthalmic devices market for diabetic retinopathy is expanding at a 6.98% CAGR, driven by 14.8% of adults living with diabetes and AI screening that detects the disease earlier.

MIGS implants allow pressure control in outpatient settings, raising demand for single-use stents. Anti-VEGF regimens dominate AMD management, creating recurring sales for injection kits and imaging follow-up.

By End-User: Hospitals Anchor, ASCs Gain Momentum

Hospitals retained 41.45% of end-user spending in 2025, performing 70% of cataract and 85% of vitreoretinal work under centralized purchasing that bundles service and consumables. Spain's ophthalmic devices market, driven by ambulatory surgery centers, is expected to grow 9.41% per year through 2031, as they cut cataract costs to EUR 1,200 per case and secure licenses in 9 months.

Specialty clinics such as Clínica Baviera and Miranza operate high-utilization theaters and digital booking systems. Optical retailers expand in-store triage, pushing handheld autorefractors and tonometers into primary-care workflows.

Geography Analysis

Madrid, Catalonia, and Andalucía account for 45% of the national population and have dense hospital networks. Madrid alone houses 28% of femtosecond lasers and 35% of swept-source OCT units, underscoring the capital region's purchasing power. Catalonia leads tele-retina adoption with 47 portable fundus cameras and 68% screening coverage among its diabetic community.

Andalucía wrestles with 16.2% adult diabetes prevalence and lower health outlays, resulting in 138-day cataract wait times despite EUR 1.8 billion in EU cohesion funding for 85 new OCT scanners and 12 femtosecond systems. Smaller regions such as Navarre and País Vasco punch above their weight; Navarre achieved 94% AI screening sensitivity, and País Vasco has the highest per-capita surgical device density.

Competitive Landscape

The top five suppliers held a significant share of the Spain ophthalmic devices market through direct sales and exclusive distributors. Alcon dominates cataract platforms with Centurion and PanOptix, while Carl Zeiss Meditec owns two-thirds of the installed OCT base. EssilorLuxottica controls retail channels after adding 900 Spanish stores via GrandVision, enabling lens-to-consumer vertical integration.

White-space pockets in Castilla-La Mancha, Extremadura, and Murcia tempt challengers that bundle installation, training, and per-procedure pricing to overcome fiscal constraints. STAAR Surgical’s EVO+ lens captured 18% of refractive-lens exchange in 2024, and Ziemer sells a femtosecond laser priced 25% below incumbents, appealing to cost-sensitive clinics.

Technology differentiation is decisive. Topcon’s Harmony platform integrates an AI layer segmentation that cuts review time by 75%, and Alcon filed 14 Spanish patents in 2024 for fluidics, IOL materials, and visualization algorithms. Smaller firms focus on niche tools to avoid premium-portfolio head-to-heads.

Spain Ophthalmic Devices Industry Leaders

Alcon Inc.

Carl Zeiss Meditec AG

Essilor International SA

Johnson & Johnson Vision Care

Bausch + Lomb Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Alcon obtained CE-mark approval for its Clareon Vivity IOL, with Spanish commercialization slated for Q3 2025.

- March 2025: AEMPS cleared Zeiss’s latest OCT platform with integrated AI for DR screening, enabling Spanish hospitals to fast-track early detection.

- March 2025: Alcon announced a USD 430 million deal to acquire Lensar, adding femtosecond-laser technology to its cataract and refractive lineup.

- September 2024: Rayner introduced the RayOne Galaxy spiral IOL, designed via AI, during the ESCRS Congress in Barcelona, reinforcing the city’s innovation stature.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study frames the Spain ophthalmic devices market as the sale of diagnostic and surgical equipment, vision-care aids, and ophthalmic imaging systems that are formally approved for human eye health in Spain's public and private settings.

Scope Exclusion: Veterinary eye devices and over-the-counter cosmetics are outside this assessment.

Segmentation Overview

- By Device Type

- Diagnostic & Monitoring Devices

- OCT Scanners

- Fundus & Retinal Cameras

- Corneal Topography Systems

- Ultrasound Imaging Systems

- Other Diagnostic & Monitoring Devices

- Surgical Devices

- Cataract Surgical Devices

- Vitreoretinal Surgical Devices

- Glaucoma Surgical Devices

- Other Surgical Devices

- Vision Care Devices

- Spectacles Frames & Lenses

- Contact Lenses

- Diagnostic & Monitoring Devices

- By Disease Indication

- Cataract

- Glaucoma

- Diabetic Retinopathy

- Other Disease Indications

- By End-user

- Hospitals

- Specialty Ophthalmic Clinics

- Ambulatory Surgery Centers (ASCs)

- Other End-users

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts completed structured interviews with Spanish ophthalmologists, hospital procurement chiefs, and local distributors, then validated assumptions with device regulators and insurance administrators across Madrid, Catalonia, Andalusia, and Valencia. These conversations clarified procedure volumes, average selling prices, and upcoming reimbursement tweaks that are rarely published.

Desk Research

We gathered baseline statistics from open sources such as the Spanish Ministry of Health, Eurostat's medical technology files, OECD health expenditure dashboards, and the International Agency for the Prevention of Blindness. Annual import-export values from Agencia Tributaria, peer-reviewed articles in journals like Ophthalmology, and company 10-K filings offered device mix, pricing clues, and replacement cycles. Subscription datasets, including D&B Hoovers for manufacturer revenues, Dow Jones Factiva for transaction news, and Questel for patent pulse, helped map competitive intensity. This list is illustrative; analysts pulled many other secondary materials to cross-check figures and fill contextual gaps.

Market-Sizing & Forecasting

Our model starts with a top-down reconstruction of Spain's cataract, refractive, retinal, and glaucoma surgery counts, aligned with population aging, diabetes prevalence, and public waiting-list trends, before translating those procedures into device demand pools. Select bottom-up checks, such as sampled distributor volume multiplied by median ASP and capacity utilization at four large contract manufacturers, balance the totals. Key variables include per-capita surgical rate, contact-lens wearer penetration, public-private payor mix, euro-dollar exchange path, and average device replacement life. We forecast through 2030 using multivariate regression that links these drivers to historical sales, and we scenario-test shifts in public funding and technology adoption to bracket uncertainty.

Data Validation & Update Cycle

Intermediate outputs pass anomaly flags, variance thresholds, and multi-analyst reviews. Final numbers are compared with shipment data snapshots and patent filing momentum. We refresh the model every twelve months and trigger interim updates after policy changes or major product launches; an analyst reruns quick checks just before report release so buyers see the latest view.

Why Our Spain Ophthalmology Devices Baseline Commands Dependability

Published estimates often diverge because firms select different device lists, apply varied euro-to-dollar conversions, or bake in contrasting adoption curves.

Key gap drivers usually trace back to whether contact lenses are fully counted, how each source treats refurbished systems, and the frequency with which assumptions are revisited. Mordor reports only new devices, converts revenue at annual average ECB rates, and updates inputs yearly, which keeps our baseline stable yet responsive.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.53 B (2025) | Mordor Intelligence | - |

| USD 0.62 B (2025) | Global Consultancy A | Includes refurbished systems and retailer mark-ups |

| USD 0.58 B (2024) | Trade Journal B | Uses list prices without volume-weighted ASP checks |

| USD 0.47 B (2024) | Industry Association C | Excludes diagnostic imaging devices from scope |

In sum, while headline numbers differ, our disciplined scope selection, live primary validations, and annual refresh cadence give decision-makers a balanced, repeatable baseline they can trust.

Key Questions Answered in the Report

How big is the Spain ophthalmic devices market in 2026?

The Spain ophthalmic devices market size is valued at USD 1.31 billion in 2026.

What is the projected CAGR for Spanish ophthalmic devices through 2031?

Revenue is forecast to rise at a 5.76% CAGR between 2026 and 2031.

Which device category is expanding fastest in Spain?

Diagnostic & Monitoring Devices are expected to grow at a 7.64% CAGR through 2031.

Why are ambulatory surgery centers gaining share?

They deliver cataract and refractive procedures at lower cost and faster scheduling, driving a 9.41% CAGR for ASC equipment demand.

Which regions lead in premium device adoption?

Madrid and Catalonia host the highest densities of femtosecond lasers and swept-source OCT systems.

Page last updated on: