Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

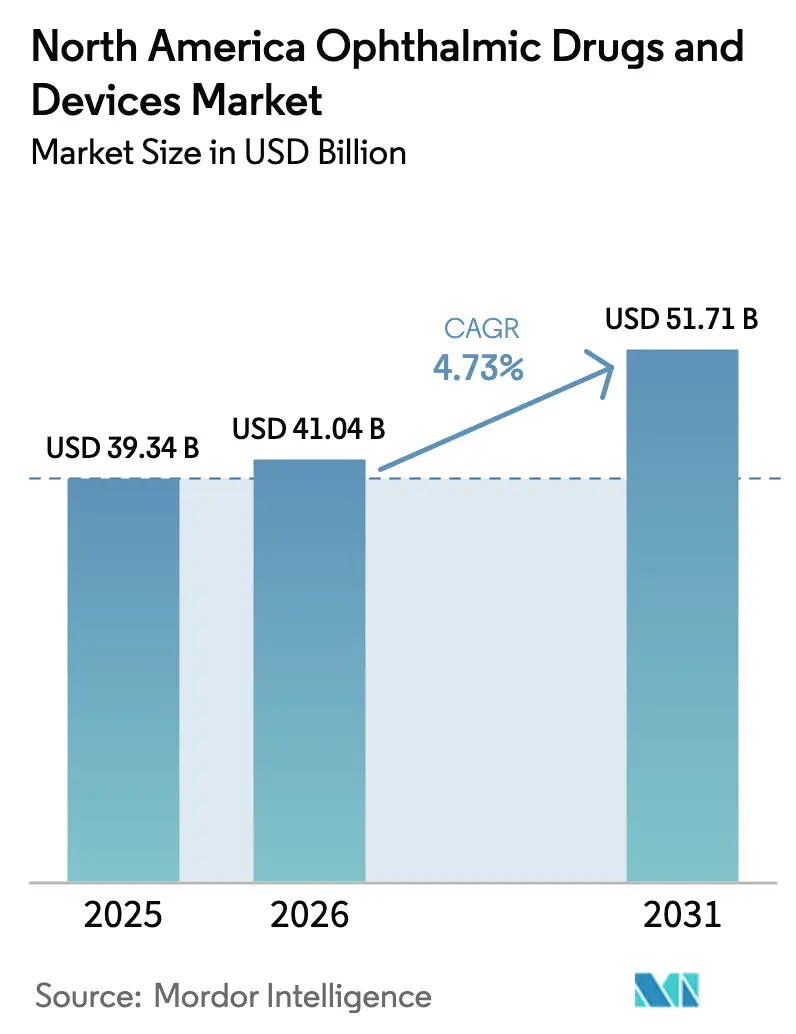

| Base Year Market Size (2025) | USD 39.34 Billion |

| Market Size (2026) | USD 41.04 Billion |

| Market Size (2031) | USD 51.71 Billion |

| Growth Rate (2026 - 2031) | 4.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Ophthalmic Drugs And Devices Market Analysis by Mordor Intelligence

The North America Ophthalmic Drugs And Devices Market size is expected to grow from USD 39.34 billion in 2025 to USD 41.04 billion in 2026 and is forecast to reach USD 51.71 billion by 2031 at 4.73% CAGR over 2026-2031.

Diagnostic and monitoring devices generated the highest revenue, with optical coherence tomography, fundus cameras, and tonometers remaining routine equipment in 14,800 U.S. ophthalmology practices. Aging demographics reinforce volume: by 2030, roughly 73 million Americans will be older than 65, and this cohort already drives 70% of cataract surgeries and 80% of glaucoma diagnoses. Ambulatory surgery centers gain share because Medicare’s site-neutral rules now equalize payments for 67 low-complexity ophthalmic procedures, cutting hospital margins while lifting ASC reimbursement for complex cataract cases by 12% in the 2025 Physician Fee Schedule. Venture capital worth USD 230 million flowed into robotics and digital ophthalmic platforms during 2024-2025, underscoring investor conviction that autonomous surgery, AI imaging, and drug-eluting implants will reshape competitive dynamics.

Key Report Takeaways

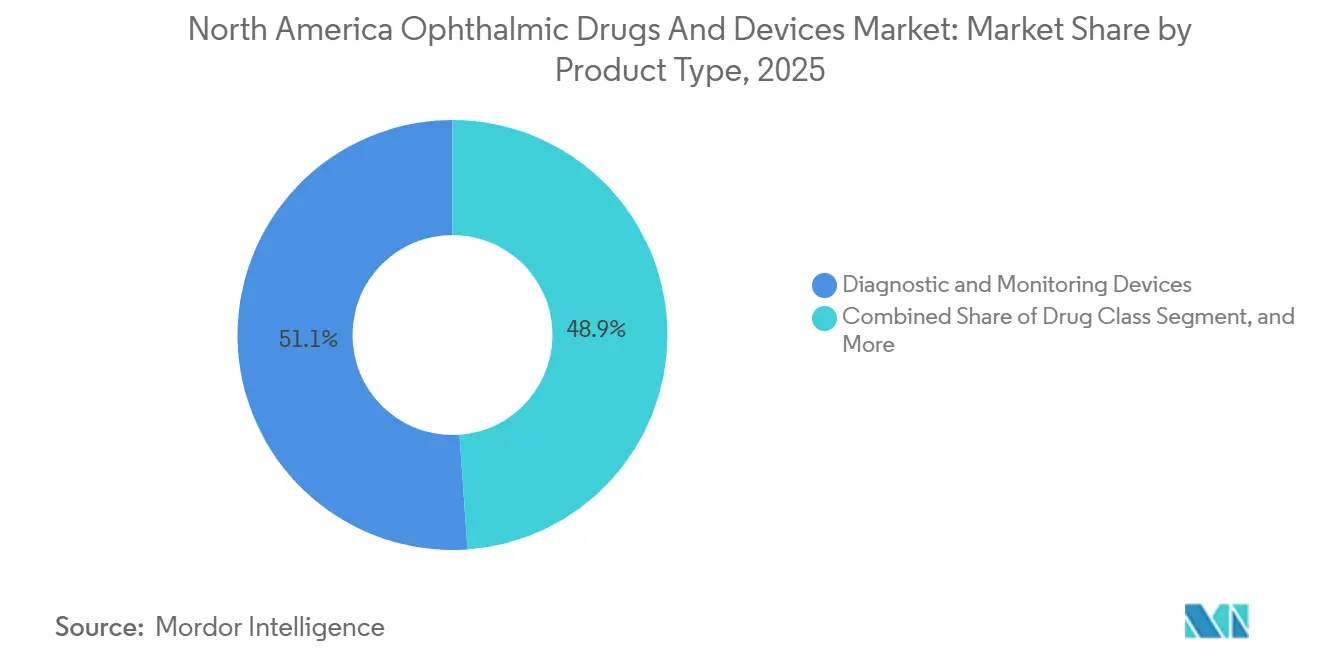

- By product type, diagnostic and monitoring devices led with 51.12% of North America ophthalmic devices and drugs market share in 2025. Drug class revenue is forecast to expand at a 6.33% CAGR through 2031, the fastest among product categories.

- By application, glaucoma applications are projected to grow at an 8.63% CAGR, outpacing cataract despite cataract’s 32.05% 2025 revenue lead.

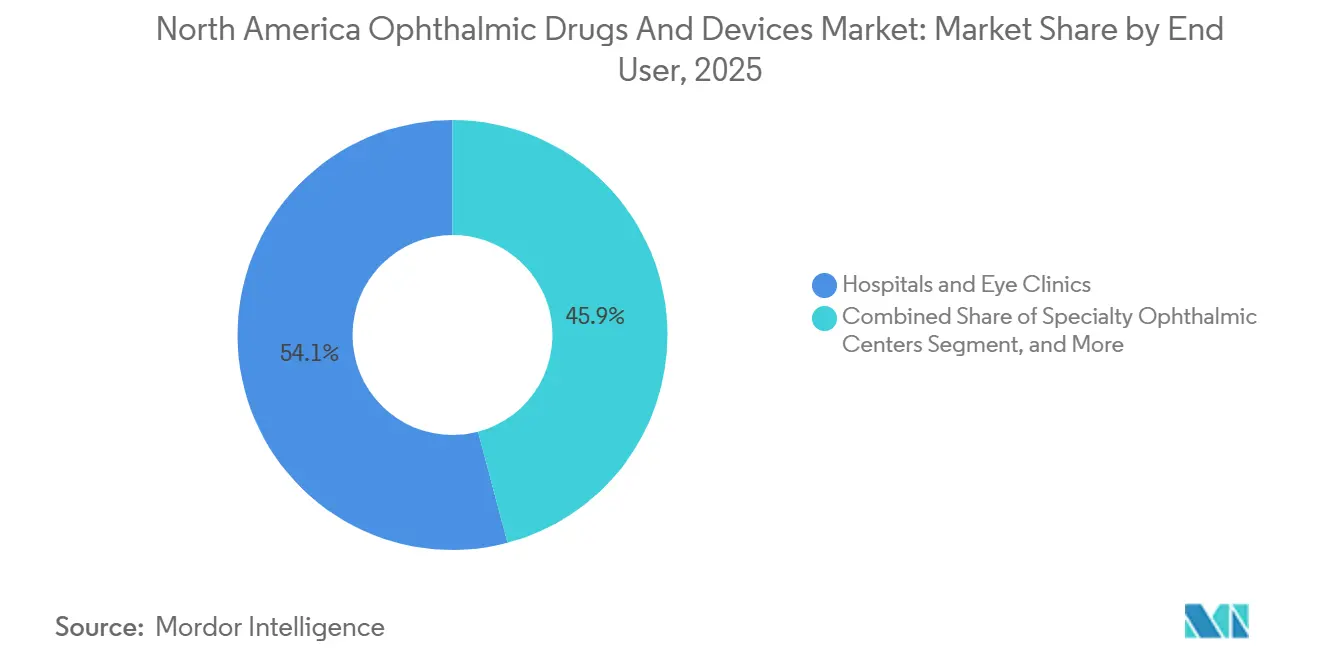

- By end user, specialty ophthalmic centers will register the highest end-user growth at 10.11% through 2031, while hospitals and eye clinics will hold 54.12% market share in 2025.

- By country, the United States led the North American ophthalmic devices and drugs market with 81.78% market share in 2025. Mexico is estimated to post the quickest country-level expansion at 8.26% through 2031 as medical tourism and private insurance adoption climb.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of North America Ophthalmic Drugs And Devices Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population and Cataract–Glaucoma Burden | +1.2% | United States, Canada, Mexico (Sunbelt states most intense) | Long term (≥ 4 years) |

| Technological Advances in Minimally Invasive Surgery | +0.9% | United States and Canada metropolitan ASCs | Medium term (2-4 years) |

| AI Powered Diagnostic Imaging Adoption | +0.7% | U.S. primary-care networks, Canadian provincial programs | Medium term (2-4 years) |

| Outpatient ASC Procedure Growth | +0.8% | U.S. Medicare regions, select Canadian provinces | Short term (≤ 2 years) |

| VC Funding in Robotics and Digital Platforms | +0.4% | U.S. innovation hubs | Long term (≥ 4 years) |

| Smart Drug-Delivery Implants | +0.5% | United States and Canada, spillover to Mexico private hospitals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Cataract–Glaucoma Burden

By 2030, the 65-plus population in North America will total 83 million, representing a 35% jump from 2020 and accounting for 92% of age-related macular degeneration cases and 78% of primary open-angle glaucoma cases.[1]U.S. Census Bureau, “Projected Age Demographics,” census.gov Cataract prevalence among Americans older than 75 climbed to 68% in 2024, up from 61% five years earlier, reflecting longer life expectancy and higher diabetes incidence. Canada’s National Institute on Ageing projects that seniors will make up one-quarter of the population by 2030, a shift already stretching cataract wait-lists that average 6.2 months in Ontario and British Columbia. Mexico’s aging curve lags but accelerates after 2028, prompting cross-border demand for U.S. procedures as the 60-plus cohort grows at 4.1% annually. This demographic momentum sustains steady cataract and glaucoma procedure pipelines that, in turn, support equipment upgrades and sustained drug dispensing.

Technological Advances in Minimally Invasive Surgery

Femtosecond laser-assisted cataract surgery penetrated 38% of U.S. premium cases in 2025 because blade-free capsulotomies cut posterior capsule rupture risk to 0.14% versus 0.92% for manual techniques. The iStent Infinite, cleared in 2024, places three micro-bypass stents through one injector and achieved an 18 mmHg mean intraocular pressure drop at 12 months in the APEX study. Lensar’s ALLY system overlays augmented-reality guidance on real-time OCT and was adopted by 127 U.S. ASCs in ten months. Canada reimburses FLACS only with premium IOLs, so 62% of 2025 cases were private-pay.

AI Powered Diagnostic Imaging Adoption

The FDA cleared 14 autonomous ophthalmic AI algorithms between January 2024 and December 2025, including EyeArt for diabetic retinopathy screening in primary care offices.[2]U.S. Food and Drug Administration, “De Novo and 510(k) Decisions 2024-2025,” fda.gov Notal Vision’s Home OCT lets AMD patients scan weekly at home, reducing clinic visits by 40% in a Veterans Affairs pilot involving 890 participants. By mid-2025, autonomous DR screening operated in 2,300 U.S. clinics, delivering 1.8 million scans and tripling referral rates compared with manual fundus review. Ontario integrated IDx-DR at 89 remote Indigenous health centers, diagnosing referable disease in 11.3% of adults and saving CAD 4.2 million in travel outlays. The FDA draft SaMD guidance issued in 2025 now requires post-market monitoring for algorithm drift when real-world demographics diverge from training data by more than 15%.

Outpatient ASC Procedure Growth

Ophthalmic cases performed in ASCs accounted for 21% of total U.S. volume in 2024, up from 16% in 2020, because site-neutral payments made lower-overhead facilities more profitable. The 2025 Physician Fee Schedule raised ASC reimbursement for complex cataract by 12% while hospital outpatient rates stayed flat.[3]Centers for Medicare & Medicaid Services, “2025 Physician Fee Schedule Final Rule,” cms.gov Sg2 forecasts ASC ophthalmic demand will climb another 21% through 2029, helped by Medicare Advantage plans that steer beneficiaries toward contracted ASCs. Alberta, British Columbia, and Quebec now allow private ASCs for cataract, yet fee schedules pay only 78% of hospital tariffs, limiting penetration to 18%. Mexico licensed 23 new ophthalmic ASCs in 2024, mostly in Monterrey, Guadalajara, and Tijuana, to serve inbound medical tourists.

Restraints Impact Analysis of North America Ophthalmic Drugs And Devices Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Advanced Equipment | -0.6% | U.S. independent ASCs, Canadian public hospitals, Mexico private clinics | Medium term (2-4 years) |

| Stringent FDA Approval Timelines | -0.4% | U.S. device makers, cross-border suppliers to Canada and Mexico | Long term (≥ 4 years) |

| Shortage of Skilled Ophthalmic Technicians | -0.3% | U.S. rural regions, Canadian provinces | Short term (≤ 2 years) |

| Sustainability Push Against Single-Use Devices | -0.2% | United States and Canada, initial rules in California and British Columbia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Devices & Limited Procedure Reimbursement

A fully equipped ophthalmic ASC requires USD 1.2-2.5 million for a femtosecond laser, swept-source OCT, phaco system, and microscope, making entry into the market tough for independents. Alcon’s Centurion system is listed at USD 135,000 in 2025, whereas J&J’s Catalys laser costs USD 650,000 or USD 9,500 monthly under a seven-year lease. Independent ASCs doing fewer than 800 cataract cases a year face payback periods of more than 4 years. Canadian capital budgets fell 8% in real terms from 2020-2024, forcing hospitals to stretch equipment cycles to 15 years. Mexico’s clinics pay 12-18% import tariffs on U.S. devices, raising landed costs outside major metros.

Stringent FDA Approval Timelines

Median 510(k) ophthalmic review duration extended to 187 days in 2024 as CDRH requested more AI evidence. Class III PMA devices averaged 18.3 months, and 34% drew major deficiency letters. Smaller firms shoulder USD 1.2-3.5 million per filing, a burden that narrows disruptive pipelines. Health Canada mirrors FDA data requirements and adds separate provincial reimbursement dossiers, which can lengthen launches by up to 14 months. COFEPRIS adopted a 90-day fast track for Class II but still requires 12-18 months for implants, widening diagnostic–surgical asymmetry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

North America Ophthalmic Drugs And Devices Market Segment Analysis

By Product Type:

Diagnostics Lead, Drugs AccelerateDiagnostics commanded 51.12% of 2025 revenue as swept-source OCT, fundus cameras and rebound tonometers became standard equipment in 92% of new office installations. The drug class will grow at 6.33% through 2031, overtaking hardware, as anti-VEGF biosimilars and novel dry-eye agents expand therapeutic volumes. Surgical devices grew 4.1% in 2024-2025 as premium toric and EDOF lenses lifted procedure revenue despite saturated monofocal demand. Vision care products face refractive-surgery headwinds, yet gain from myopia-control offerings aimed at children.

Swept-source OCT platforms such as Zeiss Cirrus 6000 displaced time-domain systems largely because 1050 nm wavelengths penetrate dense cataracts and capture 100,000 A-scans per second, a leap that enables widefield angiography. Fundus cameras integrating AI diabetic retinopathy software reached 41% of U.S. primary care deployments by mid-2025. Intraocular lens innovation is anchored by light-adjustable materials; RxSight’s LAL secured 12% of U.S. premium placements in 2025.

By Application:

Glaucoma Surges as MIGS Reshapes TreatmentCataract retained 32.05% of application revenue in 2025 on 4.2 million U.S. surgeries and remains the volume anchor through 2031. Glaucoma, however, will climb at an 8.63% CAGR as MIGS shifts surgery earlier; 32% of glaucoma operations used MIGS in 2025 compared with 18% in 2021. Retinal disorders generated 19% of revenue, with injection counts rising to 7.8 million annually. Refractive procedures have shifted from LASIK to SMILE, which now accounts for 28% of cases.

ASC economics favor cataract migration, with Medicare paying USD 1,138 per routine phaco case in ASCs versus USD 1,847 in hospitals. Premium lenses command USD 1,200-2,500 out-of-pocket per eye, bolstering surgeon income. MIGS devices lower mean IOP by roughly 25% and carry a lower complication risk than trabeculectomy, widening candidacy. Retinal reimbursement compression accelerates the adoption of longer-acting agents that stretch dosing to 12-16 weeks.

By End User:

Specialty Centers Gain as Consolidation AcceleratesHospitals and eye clinics delivered 54.12% of 2025 revenue but will cede share as specialty ophthalmic centers grow 10.11% through 2031 under private-equity ownership models that unify workflows and centralize purchasing. ASCs already perform 21% of ophthalmic procedures and gain a cost advantage from lower overhead, with operating costs averaging 42% of hospital outpatient equivalents.

Leasing has become the capital strategy of choice; 64% of ASCs opened in 2024-2025 leased lasers and OCT under 7-year agreements, slashing upfront spend to USD 12,000-15,000 per month. Medicare sequestration and nursing wage inflation shrink hospital cataract margins, hastening volume flight. Canadian formularies constrain private differentiation, while Mexico’s online pharmacy market remains nascent due to COFEPRIS script-verification rules.

Geography Analysis

United States Ophthalmic Drugs And Devices Market

The United States accounted for 81.78% of regional revenue in 2025, driven by 14,800 practices, 4.2 million cataract surgeries, and 7.8 million anti-VEGF injections. Premium segments drive U.S. upside as toric and multifocal lenses generated USD 1.9 billion in out-of-pocket spend, and femtosecond cataract technology added USD 680 million. Medicare Advantage enrollment hit 54% and steers two-thirds of beneficiaries to contracted ASCs, deepening consolidation. FDA granted 11 Breakthrough Device designations to ophthalmic innovations during 2024-2025, reinforcing the country’s launch primacy.

Canada Ophthalmic Drugs And Devices Market

Biosimilar ranibizumab reduced injection costs by 38% yet specialist wait times still exceed eight weeks in major provinces. Private clinics account for 34% of cataract cases with premium lenses, as public queues average 6.2 months. Device launches lag U.S. time-lines by up to 14 months due to separate CADTH health-technology assessments.

Mexico Ophthalmic Drugs And Devices Market

Mexico is poised for 8.26% CAGR, the region’s fastest, propelled by medical tourism that drew 42,000 U.S. patients in 2024 and expanding private insurance that now covers 29% of citizens. COFEPRIS licensed 23 new ophthalmic ASCs in 2024. LASIK prices remain 40-55% below U.S. levels, pulling cross-border volume. Class II device approvals were harmonized with FDA to 90 days, yet Class III implants still wait up to 18 months. IMSS public hospital backlogs push middle-income patients toward private options, accelerating demand for premium technology.

Competitive Landscape

The top five suppliers, Alcon, Johnson & Johnson Vision, Bausch + Lomb, Carl Zeiss Meditec, and EssilorLuxottica, held a significant share of the North America ophthalmic devices and drugs market revenue in 2025, reflecting moderate concentration. Alcon acquired a surgical planning software platform in 2024 and launched the Clareon Vivity lens in 2025, deepening ecosystem integration. Bausch + Lomb bought Elios Vision for USD 385 million, adding a femtosecond platform that pairs with Stellaris phaco and enVista lenses. Biosimilar ranibizumab captured 22% of U.S. volume by 2025, trimming Regeneron’s Eylea share to 54%.

Emerging players use AI and robotics to carve niches. EyeArt autonomous screening now operates in 2,300 clinics and accounts for 14% of diabetic retinopathy scans. ForSight Robotics targets a 2026 FDA filing for its autonomous femtosecond cataract unit that could shift labor economics. RxSight’s Light Adjustable Lens achieved 12% of premium IOL placements in 2025 after securing U.S. and EU approvals. Carl Zeiss Meditec’s digital ARTEVO microscope captured 18% of premium scope sales inside its first U.S. year.

Private-equity-backed provider chains alter purchasing leverage. EyeCare Partners grew to 340 locations and negotiated 15-22% device discounts otherwise unavailable to standalone practices. Sustainability mandates spur product redesign; Alcon’s EnVision reusable handpiece entered the market in 2025 to comply with California and British Columbia rules. Patent strategy remains key Glaukos filed 14 new patents in 2024-2025 to extend iDose TR coverage through 2037.

North America Ophthalmic Drugs And Devices Industry Leaders

Alcon Inc.

Carl Zeiss Meditec AG

Haag-Streit Group

Johnson & Johnson

Bausch Health Companies Inc. (Bausch + Lomb)

- *Disclaimer: Major Players sorted in no particular order

North America Ophthalmic Drugs And Devices Market Companies Covered in this Report

- Alcon

- Bausch Health

- BVI Medical

- Canon

- Carl Zeiss

- The Cooper Companies

- EssilorLuxottica

- Glaukos Corp.

- HOYA

- HAAG-Streit

- Iridex

- Johnson & Johnson

- Lensar Inc.

- Lumenis

- Nidek

- Optovue (a Zeiss company)

- RxSight Inc.

- Santen Pharmaceutical

- STAAR Surgical

- Topcon

- Ziemer Group

Read Analysis of North America Ophthalmic Drugs And Devices Companies

Recent Industry Developments in North America Ophthalmic Drugs And Devices Market

- January 2025: FDA approved the ENCELTO implant by Neurotech Pharmaceuticals, the first surgical device for macular telangiectasia type 2 with exploratory glaucoma and AMD applications

- May 2025: Genentech gained FDA clearance for Susvimo as a nine-month refill treatment for diabetic retinopathy, reducing the injection burden to two per year.

- May 2025: Alcon introduced the Clareon PanOptix Pro trifocal IOL in the United States, achieving 94% light utilization and lower scatter than prior models.

- May 2025: FDA authorized Alcon’s Tryptyr, the first TRPM8 agonist for dry-eye disease, with expected peak sales between USD 250-400 million

- April 2025: Orasis Pharmaceuticals launched Qlosi preservative-free pilocarpine drops for presbyopia, offering flexible once- or twice-daily dosing.

North America Ophthalmic Drugs And Devices Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the North American ophthalmic drugs and devices market as all prescription and over-the-counter ocular pharmaceuticals plus every diagnostic, surgical, and vision-care device that detects, treats, or corrects diseases of the eye. Revenue is captured at manufacturer selling price in USD, covering the United States, Canada, and Mexico.

Scope Exclusions: Cosmetic-only contact lenses, optometry service fees, and vision-insurance premiums are outside scope.

Segments Covered in This Report

- By Product Type

- Diagnostic & Monitoring Devices

- Optical Coherence Tomography Scanners

- Fundus Cameras

- Tonometers

- Other Diagnostic Devices

- Surgical Devices

- Intra-ocular Lenses

- Ophthalmic Lasers

- Phacoemulsification Systems

- Other Surgical Devices

- Vision Care Products

- Drug Class

- Anti-VEGF Agents

- Anti-inflammatory/Ocular NSAIDs

- Glaucoma Therapeutics (Prostaglandin Analogues, β-Blockers, Others)

- Anti-infectives

- Dry-Eye Therapies

- Diagnostic & Monitoring Devices

- By Application

- Cataract

- Glaucoma

- Refractive Errors

- Retinal Disorders

- Dry-Eye & Ocular Surface

- By End User

- Hospitals & Eye Clinics

- Ambulatory Surgery Centers (ASCs)

- Specialty Ophthalmic Centers

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Primary Research

We interview ophthalmic surgeons, procurement managers at ambulatory surgery centers, retail-chain optometrists, pharmacy buyers, and payer medical-policy leads across the United States, Canada, and Mexico. Their insights validate procedure growth, average selling prices, and emergent technology adoption that secondary data alone cannot reveal.

Desk Research

Mordor analysts start with authoritative public sources such as the Centers for Disease Control and Prevention, National Eye Institute, Medicare Part B reimbursement files, Statistics Canada health tables, United States International Trade Commission shipment data, and peer-reviewed journals indexed on PubMed. These provide prevalence curves, procedure counts, import volumes, and benchmark prices that ground early estimates.

To refine company-level shares and price dispersion, we mine D&B Hoovers financials and Dow Jones Factiva news archives, then cross-check with annual reports, patent filings, and trade-association white papers from bodies like Prevent Blindness and the American Academy of Ophthalmology. The sources listed are illustrative; many other datasets and publications inform our desk analysis.

Market-Sizing & Forecasting

The model pairs a top-down prevalence-to-treated-cohort build with selective bottom-up supplier roll-ups to cross-verify totals. Incidence of cataract, glaucoma, diabetic retinopathy, refractive error surgery volumes, AI-enabled diagnostic unit installs, average premium-IOL price shifts, and generic penetration rates are among the keystone variables. Forecasts rely on multivariate regression supplemented by scenario analysis when reimbursement or regulatory changes are probable; parameter ranges are stress-tested with our interview panel before values are finalized.

Data Validation & Update Cycle

Outputs pass three-step variance checks; anomalies trigger analyst peer review, and discrepancies above two standard deviations prompt fresh calls to key respondents. Reports refresh annually, and material events, such as FDA clearances, Medicare fee updates, and supply-chain shocks, initiate interim revisions.

How Mordor Intelligence's North America Ophthalmic Drugs And Devices Market Size Compares to Other Published Estimates

Published figures often diverge because firms slice the market differently, convert currencies on separate dates, or update models infrequently.

Key gap drivers include narrower product scopes that omit drugs, discounting of premium device pricing, aggressive or conservative procedure forecasts, and less frequent refresh cadences. Our study, which blends drugs with devices and reflects the 2025 pricing landscape, naturally arrives at a larger value.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 39.34 B (2025) | Mordor Intelligence | - |

| USD 31.77 B (2024) | Regional Consultancy A | Excludes online pharmacies and Mexico; uses 2023 exchange rates |

| USD 19.84 B (2024) | Global Consultancy B | Covers devices only; omits drug revenues and vision-care consumables |

| USD 12.31 B (2024) | Global Consultancy C | Surgical devices focus; applies factory-gate pricing without distributor mark-ups |

The comparison shows that when scope breadth, pricing tiers, and refresh timing are harmonized, Mordor's balanced approach delivers the most dependable baseline for strategic planning.

Key Questions Answered in the Report

How large will spending on ophthalmic devices and drugs be in North America by 2031?

Spending is forecast to reach USD 51.71 billion by 2031, reflecting a 4.73% CAGR from 2026.

Which application is expected to grow fastest to 2031?

Glaucoma treatment and management are projected to advance at an 8.63% CAGR, driven by early adoption of micro-invasive glaucoma surgery devices.

Why are ambulatory surgery centers gaining ophthalmic volume in the United States?

Medicare site-neutral payments and a 12% 2025 reimbursement boost for complex cataract procedures make ASCs more cost-effective than hospital outpatient departments.

What technology trends drive upgrades to diagnostic equipment?

AI-enabled swept-source OCT, autonomous diabetic-retinopathy screening, and home OCT for AMD monitoring push practices to replace legacy imaging systems.

How are sustainability rules influencing product design?

California and British Columbia regulations on single-use instruments led suppliers like Alcon to introduce reusable phaco handpieces that can be sterilized for 500 cycle.

Page last updated on: