Non-invasive Aesthetic Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

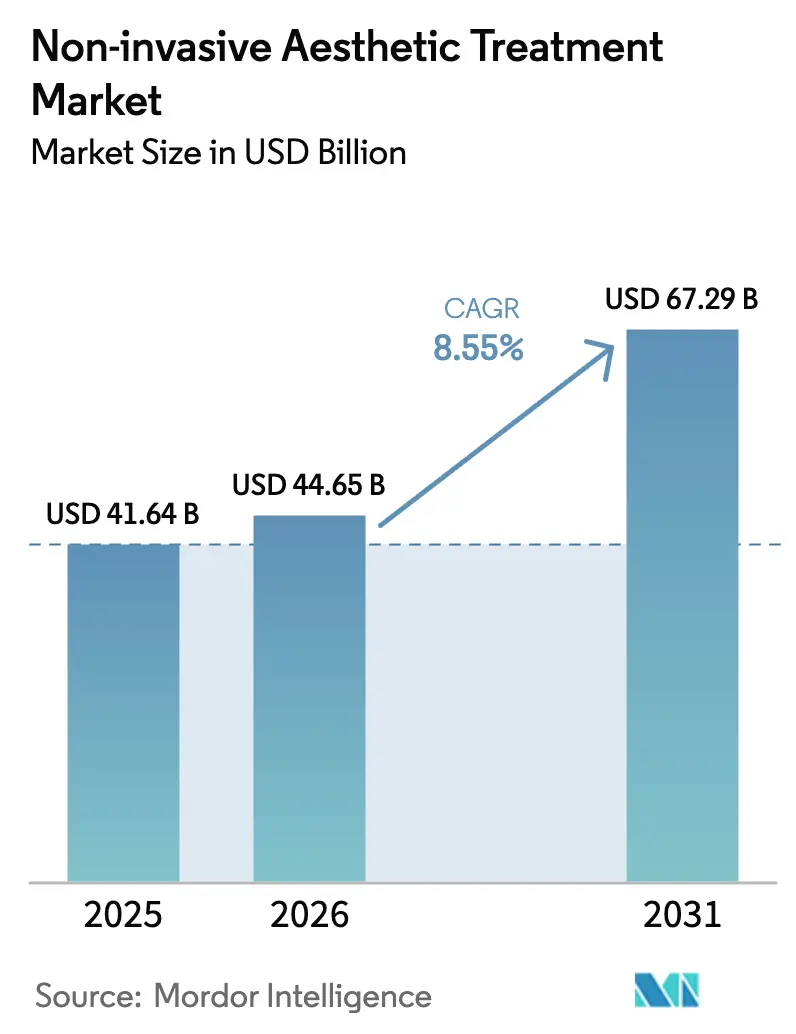

| Market Size (2026) | USD 44.65 Billion |

| Market Size (2031) | USD 67.29 Billion |

| Growth Rate (2026 - 2031) | 8.55% CAGR |

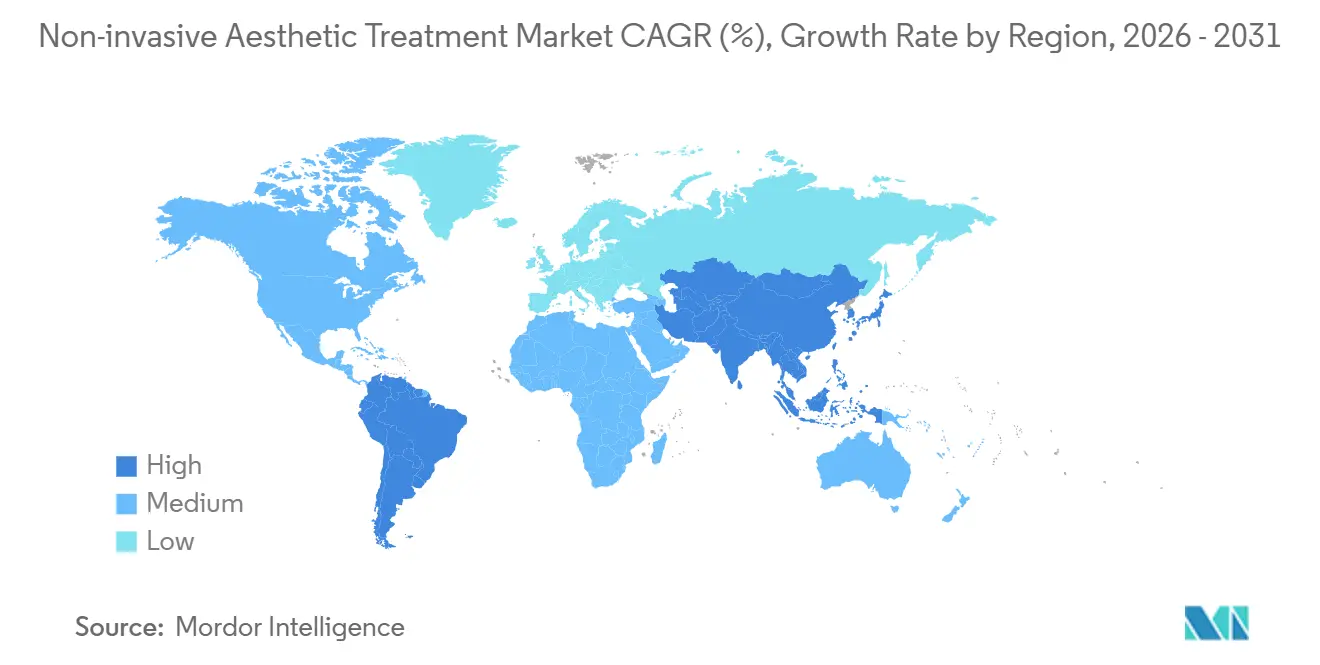

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

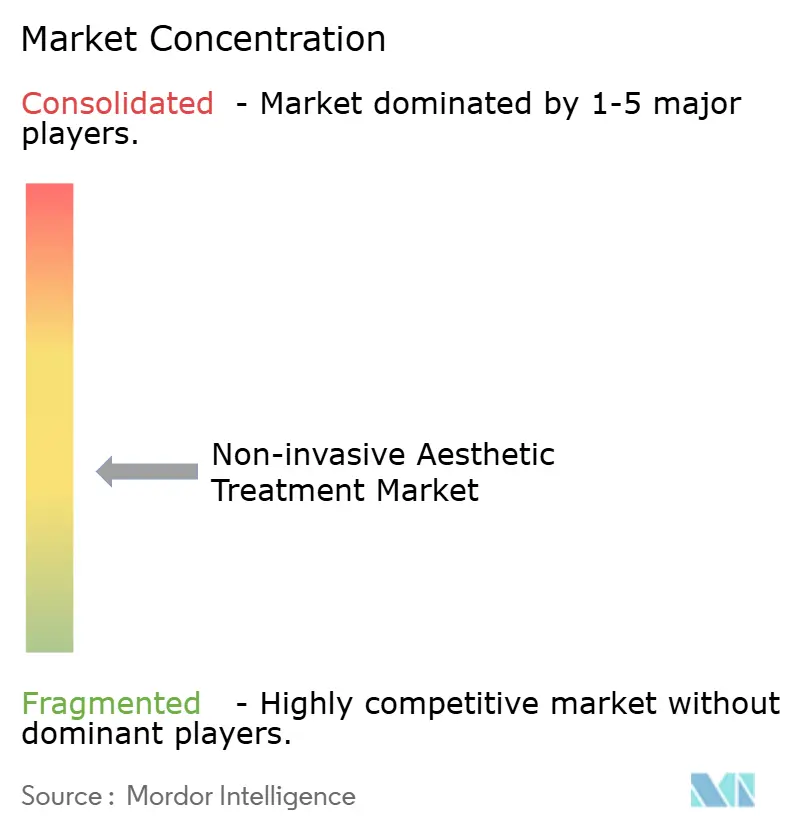

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-invasive Aesthetic Treatment Market Analysis by Mordor Intelligence

The Non-invasive Aesthetic Treatment Market size was valued at USD 41.64 billion in 2025 and is estimated to grow from USD 44.65 billion in 2026 to reach USD 67.29 billion by 2031, at a CAGR of 8.55% during the forecast period (2026-2031).

Consumer preference is tilting toward procedures that deliver surgical-level outcomes without incisions or downtime, and this structural change has accelerated as post-pandemic elective volumes normalize. Subscription-based med-spa programs are turning episodic visits into recurring revenue, supporting higher clinic utilization and stronger cash flow. AI-enabled facial-mapping engines now individualize energy and injectable protocols, raising patient satisfaction and shrinking revision rates.[1]Chaoyu Lei, “AI-Assisted Facial Analysis in Healthcare: From Disease Detection to Comprehensive Management,” Patterns, ncbi.nlm.nih.gov The emergence of semaglutide-driven weight loss has opened an unexpected corridor for body-contouring devices that tighten lax skin after dramatic fat loss. Competitive pressure remains intense as incumbents defend neurotoxin and filler franchises while energy-platform innovators differentiate through multimodal clearances and faster treatment cycles.

Key Report Takeaways

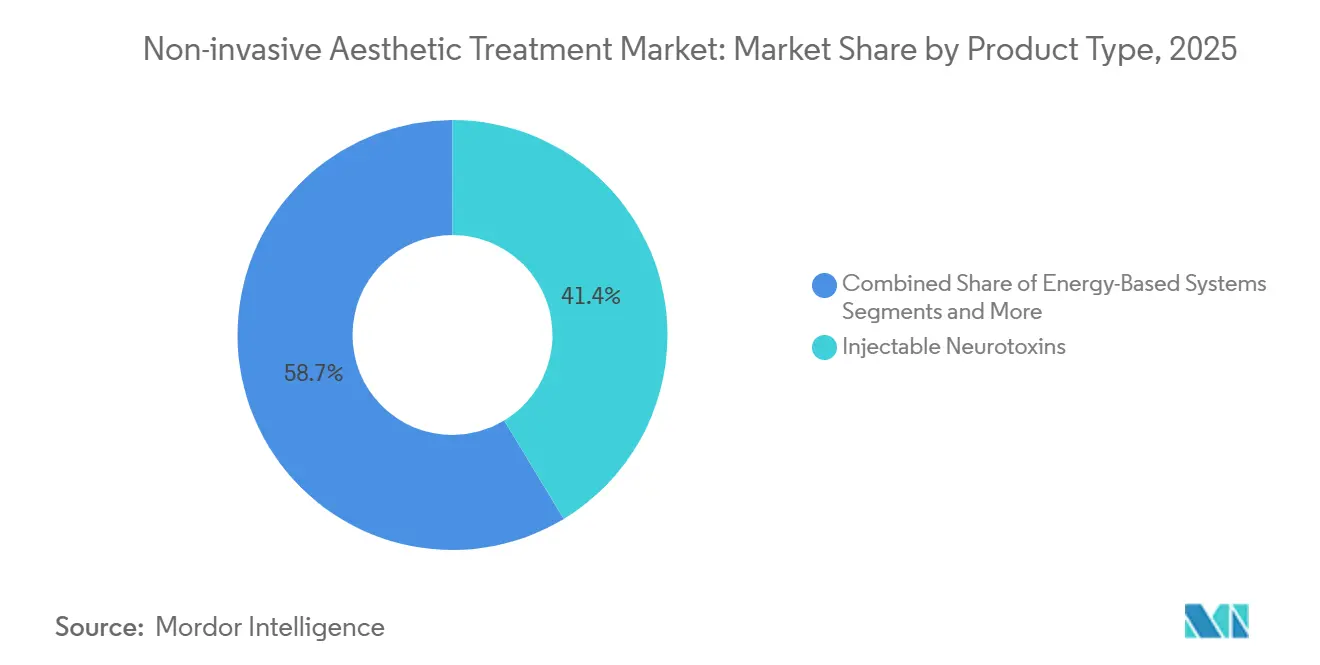

- Injectable neurotoxins led with 41.35% of the non-invasive aesthetic treatment market share in 2025, while energy-based systems are forecast to post the fastest 12.56% CAGR through 2031.

- Dermatology and plastic-surgery clinics captured 44.23% of end-user revenue in 2025, yet medical spas are projected to expand at an 11.57% CAGR to 2031.

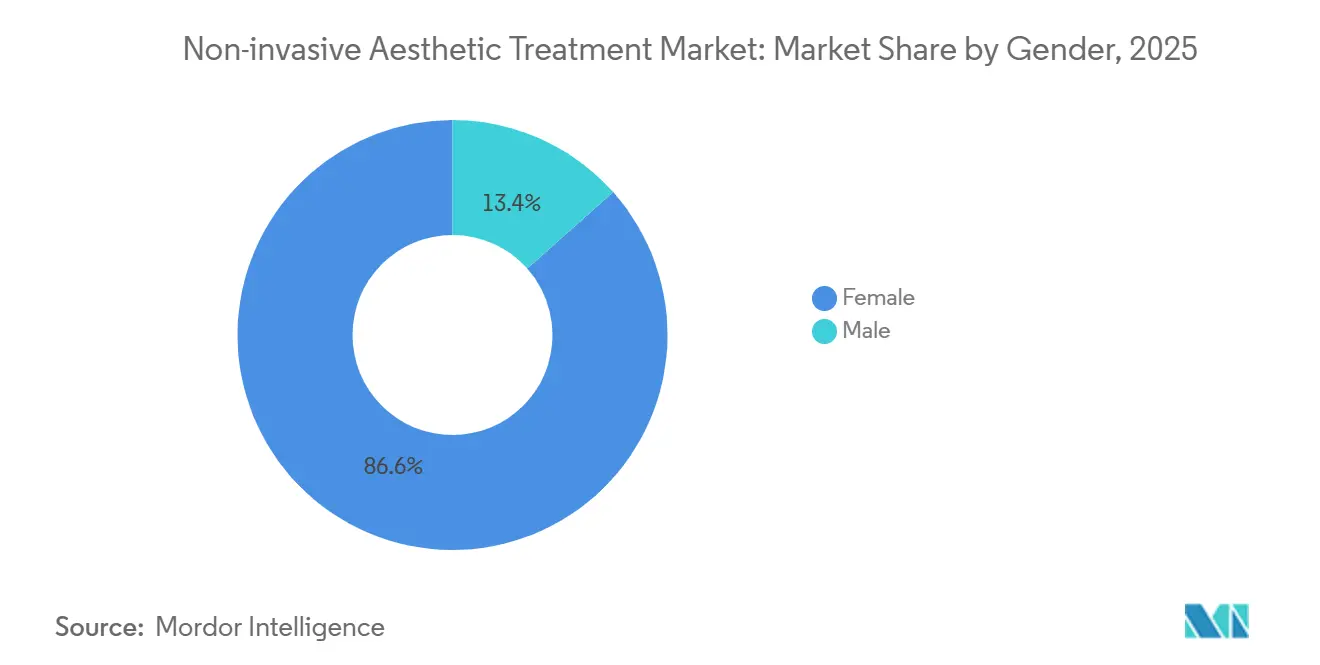

- Female patients accounted for 86.57% of global procedures in 2025, whereas male volumes are projected to climb at a 9.78% CAGR through 2031.

- The 40-54 age cohort represented 42.56% of procedure volume in 2025, while the 13-39 group is set to rise at a 10.47% CAGR between 2026-2031.

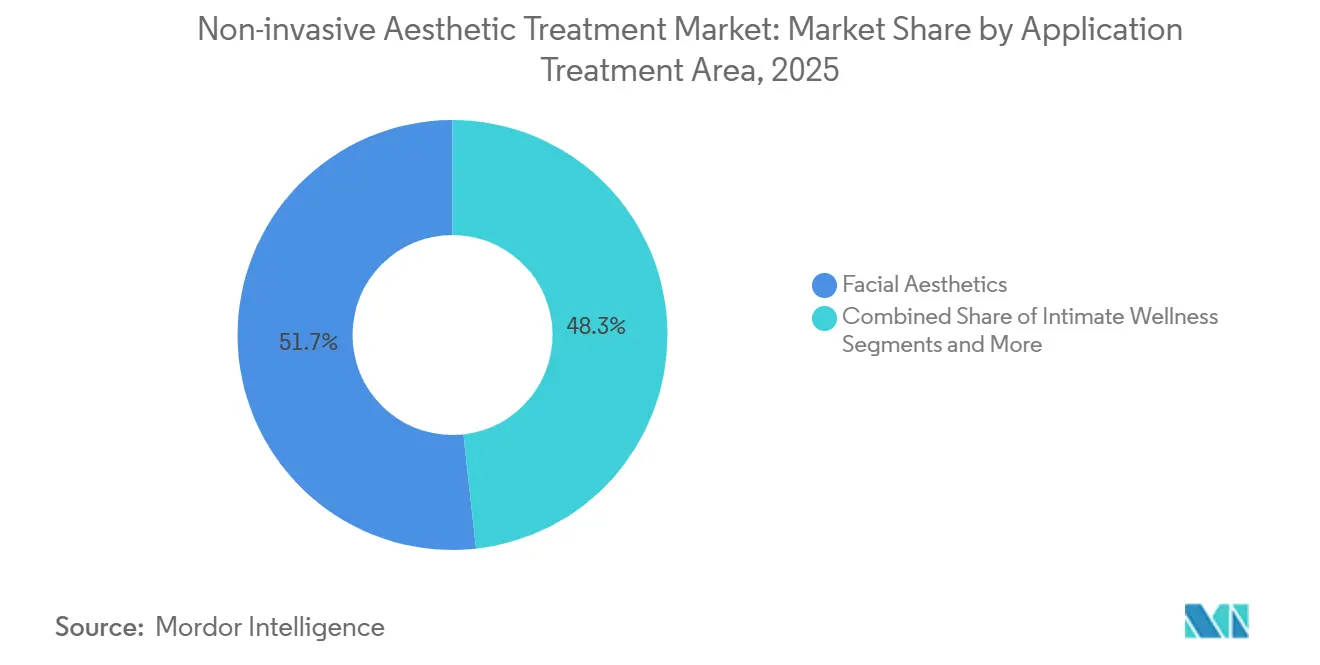

- Facial aesthetics held 51.75% of application revenue in 2025, but body-contouring procedures are forecast to register an 11.23% CAGR through 2031.

- North America retained 36.38% of global revenue in 2025, whereas Asia-Pacific is expected to lead regional growth at a 10.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Non-invasive Aesthetic Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging procedure volumes of neuromodulators & HA fillers post-pandemic | 1.8% | Global, strongest in North America & Europe | Short term (≤ 2 years) |

| Continuous device innovation in multi-modal energy platforms | 2.1% | Global, early adoption in North America & APAC | Medium term (2-4 years) |

| Rising disposable income & beauty consciousness in emerging APAC | 1.5% | APAC core (China, India, South Korea), spill-over to Southeast Asia | Long term (≥ 4 years) |

| AI-driven facial mapping enabling hyper-personalised protocols | 1.0% | North America & Europe, gradual APAC uptake | Medium term (2-4 years) |

| Subscription-based med-spa programmes boosting repeat utilisation | 1.2% | North America, expanding to Europe & APAC urban centers | Short term (≤ 2 years) |

| Post-semaglutide body-contouring demand spike | 0.9% | North America & Europe, emerging in APAC affluent segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Procedure Volumes of Neuromodulators & HA Fillers Post-Pandemic

The rebound of elective aesthetics after pandemic shutdowns has driven neuromodulator and hyaluronic acid (HA) filler sessions to record levels, evidenced by AbbVie’s Allergan Aesthetics unit booking USD 1.1 billion in Q3 2024 revenue, an 8.6% year-over-year increase.[2]AbbVie, “AbbVie Reports Third-Quarter 2024 Financial Results,” AbbVie News Center, news.abbvie.com This upswing is more than pent-up demand; remote work keeps faces on camera, prompting patients to pursue wrinkle prevention earlier in life. According to the International Society of Aesthetic Plastic Surgery (ISAPS) 2024 global survey, the number of hyaluronic acid procedures reached 6,338,184, marking a 5.2% rise from 2023 figures worldwide.[3] International Society of Aesthetic Plastic Surgery, “ISAPS Global Survey 2024,” ISAPS, isaps.org Concurrently, new cross-linking chemistries in HA fillers increase persistence and reduce post-injection inflammation, and dual-product protocols—utilizing neurotoxin for dynamic lines and filler for volume loss—are now routine in high-volume practices. The U.S. Food and Drug Administration has heightened surveillance of counterfeit injectables, issuing multiple warning letters in 2024 to unlicensed distributors, a move that safeguards patient safety and maintains clinician confidence.

Continuous Device Innovation In Multi-Modal Energy Platforms

Manufacturers are migrating from single-purpose lasers to systems that blend radiofrequency, ultrasound, and electromagnetic muscle stimulation in one handpiece. InMode’s Morpheus8 gained 2024 clearance for RF microneedling plus body-contouring modules, letting practitioners tighten skin and debulk fat in the same appointment. BTL’s EmSculpt Neo fuses RF heating with high-intensity focused electromagnetic pulses to cut fat and build muscle simultaneously, expanding cleared indications to abdomen, buttocks, and thighs. These platforms command premium pricing yet shorten chair time, improving clinic throughput and revenue per hour. Single-modality lasers now face commoditization risk unless vendors add software planning tools or flexible financing for smaller sites.

Rising Disposable Income And Beauty Consciousness In Emerging Asia-Pacific

The non-invasive aesthetic treatment market is set for double-digit expansion in Asia-Pacific as rising wages intersect with cultural acceptance of cosmetic upgrades. China and South Korea cleared multiple RF and ultrasound devices in 2024, showing regulatory alignment with global norms. Tier-2 Chinese cities now host more trained injectors, broadening access beyond Beijing and Shanghai, though clinician scarcity still caps volumes. India combines a swelling middle class with a surge of dermatology graduates, creating strong entry-level demand for injectables even as price sensitivity hampers premium device uptake. Japan’s aging population favors non-ablative lasers and collagen-stimulating fillers that yield subtle yet cumulative improvement.

AI-Driven Facial Mapping Enabling Personalized Protocols

Three-dimensional imaging is evolving into treatment-planning software that predicts post-procedure outcomes and guides injection depth, laser energy, and sequence order. North American surgeons using AI-guided systems report higher conversion rates for multi-session packages and fewer touch-ups. Cloud delivery models are lowering capital barriers for medical spas, yet integration complexity slows adoption. Regulatory frameworks still lag; if adverse events arise from algorithmic guidance, the FDA may impose software-as-a-medical-device audits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device & treatment costs limit access | -1.3% | Global, most acute in emerging APAC & South America | Long term (≥ 4 years) |

| Stringent, patchwork regulations delay launches | -0.9% | Global, particularly Europe (MDR) & China (NMPA) | Medium term (2-4 years) |

| Counterfeit injectables eroding clinician & patient trust | -0.7% | Global, concentrated in unregulated med-spa chains | Short term (≤ 2 years) |

| Shortage of trained practitioners outside tier-1 cities | -0.8% | APAC, Middle East & Africa, South America tier-2/3 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Device And Treatment Costs Limit Access

Premium energy platforms cost USD 100,000-300,000, putting them beyond reach for many independent clinics in emerging economies. Session fees of USD 500-1,500 restrict demand to high-income groups where household income exceeds USD 20,000. Leasing models ease some burden yet remain hindered by credit constraints. Manufacturers are releasing entry-level devices with fewer modes to gain volume, even at lower margins. Injectable pricing is comparatively manageable, but gray-market supply cuts margins and threatens R&D investment.

Stringent, Patch-Work Regulations Delay Launches

Europe’s Medical Device Regulation imposes extensive post-market evidence, slowing novel device approvals and favoring incumbents with strong regulatory arms. The FDA’s 510(k) route remains quicker for predicate devices, but De Novo submissions for novel energy mechanisms still stretch timelines. China’s NMPA has quickened approvals, yet foreign manufacturers endure multi-year documentation drills. Fragmentation burdens smaller innovators and raises development costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biostimulators Challenge HA Filler Dominance

Injectable neurotoxins commanded 41.35% of the non-invasive aesthetic treatment market share in 2025, underscoring entrenched brand equity for formulations such as Botox and Xeomin. Energy-based platforms, however, will post a 12.56% CAGR through 2031, the fastest among all categories, as bundled radiofrequency and ultrasound heads help clinicians address skin laxity and adipose reduction in a single visit. Hyaluronic acid fillers remain the revenue anchor because of reversibility and safety, yet polycaprolactone and poly-L-lactic acid products offer up to 24-month persistence, drawing share from HA. Galderma’s Sculptra and Merz’s Radiesse are marketed as collagen stimulators for post-weight-loss skin quality, resonating with GLP-1 patients. Laser and intense pulsed light units still dominate energy sales by installed base, but radiofrequency devices are closing fast as consumers seek non-ablative tightening without pigment risk. Electromagnetic muscle stimulators, epitomized by EmSculpt, created a fresh indication by building muscle mass and trimming overlying fat. Cryolipolysis growth is moderating as pharmaceutical weight loss shrinks treatable fat pockets, pushing vendors toward adjunctive skin-tightening features.

Energy vendors now bundle software subscriptions that unlock new protocols over Wi-Fi, turning hardware sales into recurring revenue streams. Consumable microneedle tips and single-use RF cartridges create razor-razor-blade economics, cushioning the margin impact of hardware price erosion. The non-invasive aesthetic treatment market size for energy platforms is projected to climb steadily as Asian clinics adopt multimodal towers to maximize floor space and procedure range. Competition will heighten when Chinese device makers scale exports after clearing U.S. and EU audits. Intellectual-property litigation is expected to rise, especially around proprietary pulse algorithms that claim superior tissue selectivity.

By End User: Med-Spas Capture Share From Traditional Clinics

Board-certified dermatology and plastic-surgery clinics held 44.23% of the non-invasive aesthetic treatment market size in 2025, leveraging hospital affiliations and complex case-handling capability. Yet medical spas are expanding at an 11.57% CAGR to 2031 by offering lounge-style environments and subscription pricing that spreads costs over twelve months. Relaxed U.S. state supervision rules permit nurse practitioners to inject under physician oversight, widening labor supply and lowering wage expenses. Hospitals and ambulatory centers sit at the low end of share because higher facility fees deter price-sensitive clients, although they attract post-bariatric body-contouring cases requiring anesthesia and multidisciplinary care.

Traditional clinics are fighting back by adopting luxury interiors, online scheduling, and membership programs to retain patients who might defect to spas. Some med-spas, in turn, recruit board-certified dermatologists to boost credibility and qualify for advanced procedure insurance. The competitive line is blurring as each model borrows elements from the other, yet pricing gaps persist: average neurotoxin vial costs USD 10-12 per unit in spas versus USD 14-16 in physician-owned clinics. The non-invasive aesthetic treatment market will likely stabilize with a hybrid model where core medical acts remain physician-led while high-volume maintenance treatments sit in spa settings.

By Gender: Male Aesthetics Destigmatizes Rapidly

Women represented 86.57% of global procedure counts in 2025, reflecting decades of targeted marketing and social acceptance. Male demand, though from a lower baseline, is rising at a 9.78% CAGR on the back of workplace competition and influencer-led normalization. Neurotoxin remains the gateway for men, focusing on forehead lines and masseter slimming without altering masculine facial contours. Fillers for jawline definition and tear-trough correction are gaining ground as product viscosity improves. Laser hair removal and RF skin tightening also resonate with male patients seeking minimal downtime.

Regional nuances matter: South Korea leads male penetration, while Middle Eastern markets are early in the adoption curve. Device makers now print male-specific protocols that adjust needle depth and energy fluence for thicker skin. Marketing materials emphasize discreet, natural outcomes to avoid the stigma of overt cosmetic intervention. The non-invasive aesthetic treatment market sees an opportunity in preventive regimens for men aged 25-40, aiming to lock in lifelong revenue before deeper rhytids form.

By Age Group: Preventive Treatments Drive Youth Segment

The 40-54 cohort generated 42.56% of 2025 procedure volume, targeting established photoaging, volume loss, and laxity. However, the 13-39 group is on track for the fastest CAGR at 10.47%, driven by preventive neurotoxin micro-dosing nicknamed “Baby Botox”. Social platforms amplify before-and-after visuals, encouraging early adoption. This younger audience values affordability, squeezes appointments between work and travel, and gravitates toward non-ablative lasers and light chemical peels. Practices lure them with loyalty apps and influencer referrals, banking on upsell potential as they age into higher-value filler and energy treatments.

The 55-69 segment remains steady, favoring combination packages that mix neuromodulators, fillers, and resurfacing for comprehensive rejuvenation. Patients over 70 represent a niche due to comorbidities and lower aesthetic prioritization, yet selective uptake occurs for minimally invasive treatments that improve quality of life without anesthesia risk. Regulators are focusing on informed consent for younger patients influenced by social media filters, ensuring realistic outcome expectations.

By Application: Intimate Wellness Emerges As High-Growth Niche

Facial aesthetics absorbed 51.75% of revenue in 2025, anchored by the dominance of neuromodulators and fillers. Body-contouring procedures will climb at an 11.23% CAGR as post-semaglutide patients seek skin tightening, and electromagnetic muscle stimulation adds sculpture to leaner frames. Skin-rejuvenation treatments—pigment, texture, vascular—benefit from versatile laser and IPL platforms, though topical growth-factor serums add competition at lower price points.

Hair and scalp therapies such as platelet-rich plasma injections are niche but expanding, propelled by destigmatization of male and female hair loss. Intimate wellness—RF or laser vaginal rejuvenation, penile aesthetic fillers—is the fastest-growing segment, catalyzed by new FDA clearances and broader cultural discourse around sexual health. Clinics market these services to postpartum and menopausal women as well as men seeking non-surgical enhancement. Regulatory vigilance over efficacy claims is tightening, yet first movers enjoy limited competition and attractive pricing.

Geography Analysis

North America generated 36.38% of global revenue in 2025 and remains the highest per-capita spender on aesthetic services. A dense network of trained practitioners and access to flexible patient financing enable rapid uptake of new technologies. GLP-1 prescriptions are fueling a surge in post-weight-loss body-contouring referrals, bringing endocrinology and primary-care physicians into the aesthetic funnel. Med-spa subscription models thrive in cities such as New York and Los Angeles, where patient acquisition costs are steep and consumers accept membership billing. Regulatory oversight is favorable but increasingly targets unlicensed operators selling counterfeit injectables.

Europe maintains a mature installed base of laser and RF devices, yet the Medical Device Regulation has lengthened approval pathways, giving incumbents a compliance advantage. Germany, France, and the United Kingdom lead procedure volumes, while Italy and Spain post robust filler demand due to cultural emphasis on facial aesthetics. Eastern Europe is emerging, aided by rising household incomes and cross-border practitioner training, although price sensitivity remains high. The strategic challenge is balancing patient-safety rigor with innovation speed so that Europe does not cede technology leadership to Asia or the United States.

Asia-Pacific will deliver the fastest regional CAGR of 10.45% through 2031, propelled by expanding middle classes in China, India, and Southeast Asia alongside regulatory harmonization that speeds device clearance. South Korea continues to top global procedure density, bolstered by government-supported medical-tourism programs. China’s National Medical Products Administration issued multiple RF and ultrasound approvals in 2024, signaling an openness that should shorten market entry for foreign brands. India’s tier-2 cities form the next frontier, though practitioner shortages and price sensitivity temper high-end device adoption. Japan sees steady demand for non-ablative lasers among an aging population seeking subtle rejuvenation. Australia rounds out the developed cohort with strict regulatory standards and high uptake of body-contouring technologies. The Middle East and Africa are nascent but benefit from Dubai’s push to become the Beverly Hills of the Gulf, attracting international surgeons and investment. South America, led by Brazil and Argentina, rides cultural acceptance of cosmetic enhancement yet remains vulnerable to currency swings.

Competitive Landscape

Market concentration is moderate. AbbVie, Galderma, and Merz collectively dominate injectables through well-established neurotoxin and filler portfolios and extensive KOL engagement. AbbVie’s Allergan Aesthetics booked USD 1.1 billion in Q3 2024, reflecting steady Botox demand despite biosimilar entries. Galderma’s USD 2.6 billion IPO in 2024 equips it with fresh capital for biostimulator R&D and tuck-in acquisitions. Merz focuses on Xeomin’s purity positioning to guard against neutralizing antibodies.

Energy-device specialists—InMode, BTL Industries, Candela, Cutera—compete by layering new applicators and software updates onto installed towers, defending margins as hardware ASPs slide. InMode secured 2024 clearances for Morpheus8 microneedle RF and new body-contouring modules, illustrating iterative innovation that extends platform life. BTL’s EmSculpt Neo differentiates with combined RF and electromagnetic pulses, delivering muscle hypertrophy metrics that appeal to fitness-oriented demographics.

Disruptors include Korean toxin producers Hugel and Daewoong, which leverage cost advantages and local K-beauty clout to seize Asia-Pacific share. Subscription med-spa chains are consolidating fragmented practices, unlocking bulk buying power and unified training programs but also drawing regulatory scrutiny over supervision standards. Intellectual-property disputes are rising around RF pulse shapes and cooling algorithms. Counterfeit injectables remain a systemic threat, prompting brands to pilot blockchain traceability and QR-based authentication that clinics and patients can verify via smartphone.

Non-invasive Aesthetic Treatment Industry Leaders

AbbVie

Galderma SA

Merz Aesthetics

Hologic

Candela Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Galderma gained FDA approval for Restylane Lyft with Lidocaine for chin augmentation in adults, expanding its HA filler indication.

- September 2025: The FDA cleared Obagi Saypha MagIQ injectable HA gel, the first intradermal filler in Obagi’s U.S. portfolio, with commercial launch planned for 2026.

- February 2025: Evolus received FDA approval for Evolysse Form and Evolysse Smooth HA gels, marking the firm’s entry into the U.S. dermal-filler segment.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we define the non-invasive aesthetic treatment market as the spending captured when certified physicians or licensed medical spas deliver injectable fillers and toxins, energy-based skin rejuvenation, non-surgical fat reduction, vascular or sclerotherapy sessions, laser hair removal, and allied office-based procedures that refresh appearance without cutting the skin or inserting instruments. Values are expressed at provider revenue level, inclusive of procedure fees and consumables, in constant 2024 US dollars.

Scope exclusions include invasive plastic surgeries, over-the-counter beauty topicals, purely home-use gadgets, and unlicensed service outlets that are not counted.

Segmentation Overview

- By Product Type

- Injectables – Neurotoxins

- Botulinum Toxin Type A

- Botulinum Toxin Type B

- Injectables – Dermal Fillers

- Hyaluronic Acid

- Calcium Hydroxylapatite

- Poly-L-Lactic Acid

- Collagen & PMMA Microspheres

- Polycaprolactone / Other Biostimulators

- Energy-Based Systems

- Laser / IPL Platforms

- Radiofrequency Devices

- Ultrasound / HIFU Platforms

- Cryolipolysis Systems

- Electro-Magnetic Muscle Stimulators

- Topical & Skin Booster Products

- Injectables – Neurotoxins

- By End User

- Dermatology & Plastic-Surgery Clinics

- Medical Spas

- Hospitals & Ambulatory Centers

- By Gender

- Female

- Male

- By Age Group

- 13 – 39 Years

- 40 – 54 Years

- 55 – 69 Years

- 70+ Years

- By Application / Treatment Area

- Facial Aesthetics

- Body Contouring & Fat Reduction

- Skin Rejuvenation / Pigment & Texture

- Hair & Scalp Treatments

- Intimate Wellness (Vaginal / Penile)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with board-certified dermatologists, plastic surgeons, med-spa owners, and regional distributors across North America, Europe, Asia-Pacific, Latin America, and the Gulf validate utilization patterns, typical session prices, patient mix, and upgrade intentions that secondary sources alone cannot surface. Follow-up surveys help refine assumption ranges and flag sudden demand shocks.

Desk Research

Our analysts review public datasets that ground the market baseline: regulatory filings from the US FDA MAUDE and EU Eudamed, annual treatment tallies from the American Society for Dermatologic Surgery, ISAPS and J-Cosme, UN Comtrade trade codes for aesthetic lasers, patent trends mined through Questel, and macro indicators such as age-band population from the UN DESA. Company 10-Ks, health ministry price ceilings, and peer-reviewed journals add clinical outcome and pricing context. This listing is illustrative; many additional open sources underpin the dataset creation.

Market-Sizing & Forecasting

We start with a top-down reconstruction that multiplies country-level procedure volumes published by professional societies by region-specific average session prices, then adjust for cash-pay discounting and repeat-treatment rates. Targeted bottom-up checks, sampled clinic revenue roll-ups, laser platform installed-base audits, and injectable unit shipments anchor the totals. Five fingerprints steer the model: 1) botulinum toxin unit price drift, 2) fractional laser platform park, 3) count of operating med spas, 4) disposable income growth within the 30-64 female cohort, and 5) consumer sentiment on appearance. Forecasts rely on multivariate regression blended with scenario analysis to capture technology adoption curves and macro resilience. Gaps in facility data are bridged by ratio analysis against national derm clinic registries before the final numbers are frozen.

Data Validation & Update Cycle

Sequential analyst reviews flag variance beyond +/-8% versus historical run rates. Outliers trigger re-contact with expert respondents, and models are stress tested against device vendor earnings and import duty receipts. Reports refresh each year, while material regulatory or reimbursement events prompt an interim update.

Why Our Non-invasive Aesthetic Treatment Baseline Commands Confidence

Published estimates often diverge because firms pick different service scopes, pricing ladders, geographies, and refresh cadences. When buyers line these studies up side by side, gaps can look baffling.

Key gap drivers here include whether invasive surgery and home-use gadgets sneak into the totals, how aggressively average selling prices are escalated across regions, and if country-level procedure volumes are validated beyond press releases. Mordor's disciplined reliance on audited society data, region-specific ASPs, and annual primary checks produces a balanced figure that decision-makers can trace back to clear variables.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.57 B (2024) | Mordor Intelligence | |

| USD 69.9 B (2023) | Global Consultancy A | Includes invasive surgery, OTC beauty products, and device hardware; uniform ASP applied globally |

| USD 25.7 B (2024) | Trade Journal B | Counts consumer skincare services and home-use devices; relies mainly on press releases |

| USD 21.01 B (2024) | Industry Research Group C | Derives totals from device vendor revenue mark-ups with limited provider-side validation |

The comparison shows that once scope creep and pricing shortcuts are filtered out, Mordor's lean yet diligently triangulated baseline offers the most transparent, reproducible starting point for strategy and investment planning.

Key Questions Answered in the Report

How big is the non-invasive aesthetic treatment market today?

The non-invasive aesthetic treatment market size reached USD 44.65 billion in 2026 and is set to climb to USD 67.29 billion by 2031.

Which segment leads by product type?

Injectable neurotoxins held 41.35% of global share in 2025, maintaining the lead despite rapid growth in energy-based systems.

What is the fastest-growing application area?

Body-contouring procedures are forecast to advance at an 11.23% CAGR through 2031, driven by demand from post-weight-loss patients.

Which region will grow the quickest?

Asia-Pacific is projected to post the highest regional CAGR at 10.45% through 2031, fueled by rising disposable income and faster device approvals.

Why are medical spas gaining share?

Subscription models, lower overhead, and relaxed supervision rules let medical spas expand patient volumes at an 11.57% CAGR to 2031.

What risks does the industry face?

High device costs, fragmented regulations, counterfeit injectables, and practitioner shortages in second-tier cities all restrain growth.

Page last updated on: