Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

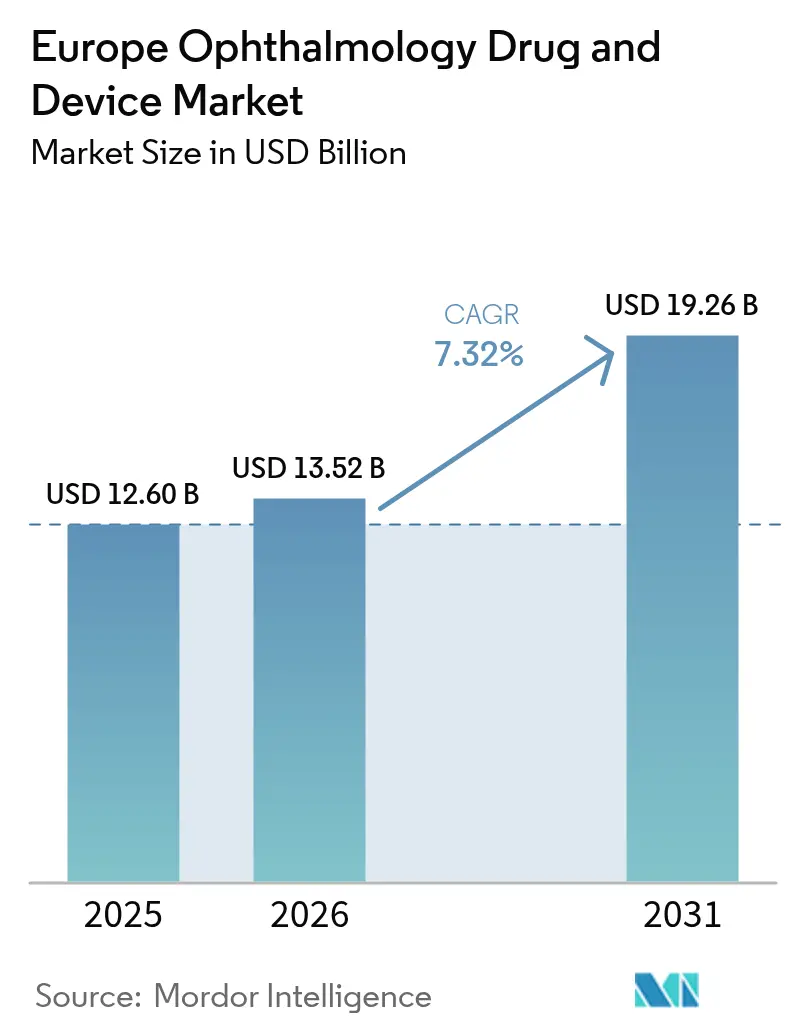

| Base Year Market Size (2025) | USD 12.6 Billion |

| Market Size (2026) | USD 13.52 Billion |

| Market Size (2031) | USD 19.26 Billion |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Ophthalmology Drug And Device Market Analysis by Mordor Intelligence

The Europe ophthalmic devices and drugs market size is expected to grow from USD 12.6 billion in 2025 to USD 13.52 billion in 2026 and is forecast to reach USD 19.26 billion by 2031 at 7.32% CAGR over 2026-2031. Demographic aging, rising incidence of chronic eye conditions, and steady migration toward minimally invasive surgery sustain this expansion. Hospitals continue to dominate procedure volumes, yet outpatient facilities are capturing the incremental growth as payers encourage cost-efficient care models. AI-enabled diagnostic platforms are improving screening throughput in Germany and the UK, while regulatory actions such as the EMA’s 2024 Durysta withdrawal are redirecting R&D toward safer sustained-release implants. Consolidation among leading manufacturers and new vertical integration moves by EssilorLuxottica underscore the sector’s shift toward end-to-end eye-care ecosystems.

Key Report Takeaways

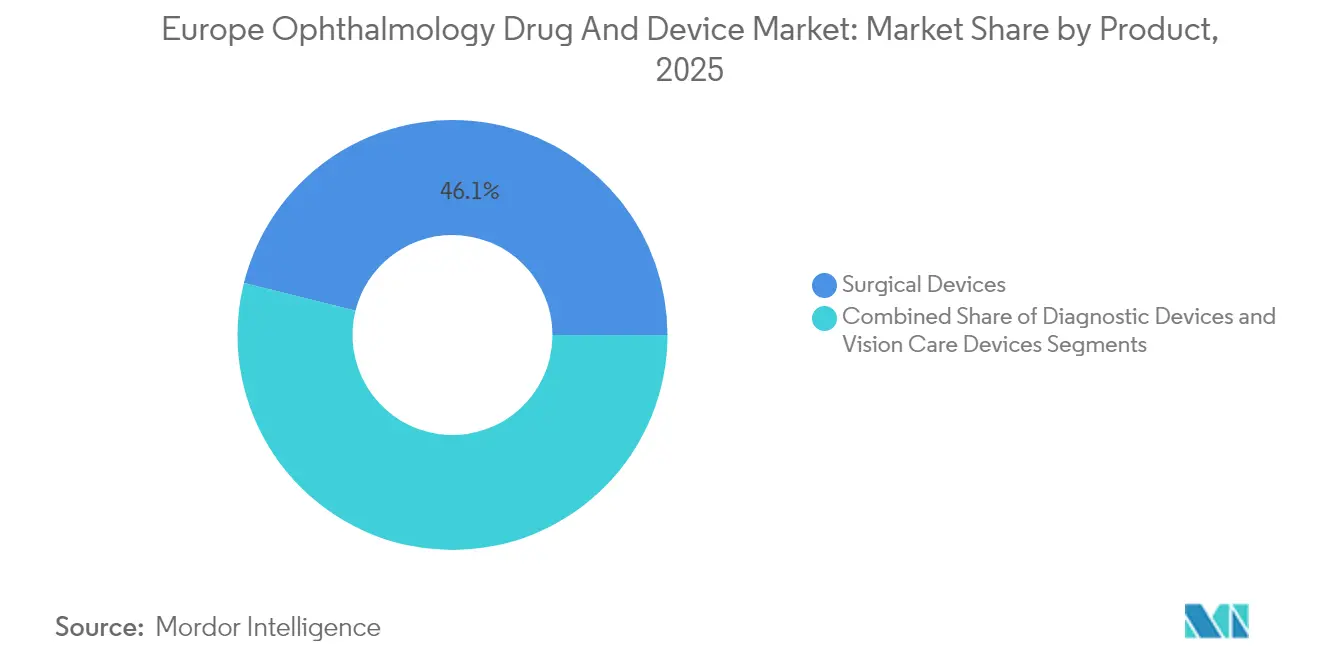

- By product, surgical devices led with 46.12% revenue share in 2025; drugs are projected to post the quickest 4.42% CAGR through 2031.

- By disease, cataract treatments captured 29.03% of Europe ophthalmic devices and drugs market share in 2025, while glaucoma therapeutics are set to grow at 6.54% CAGR to 2031.

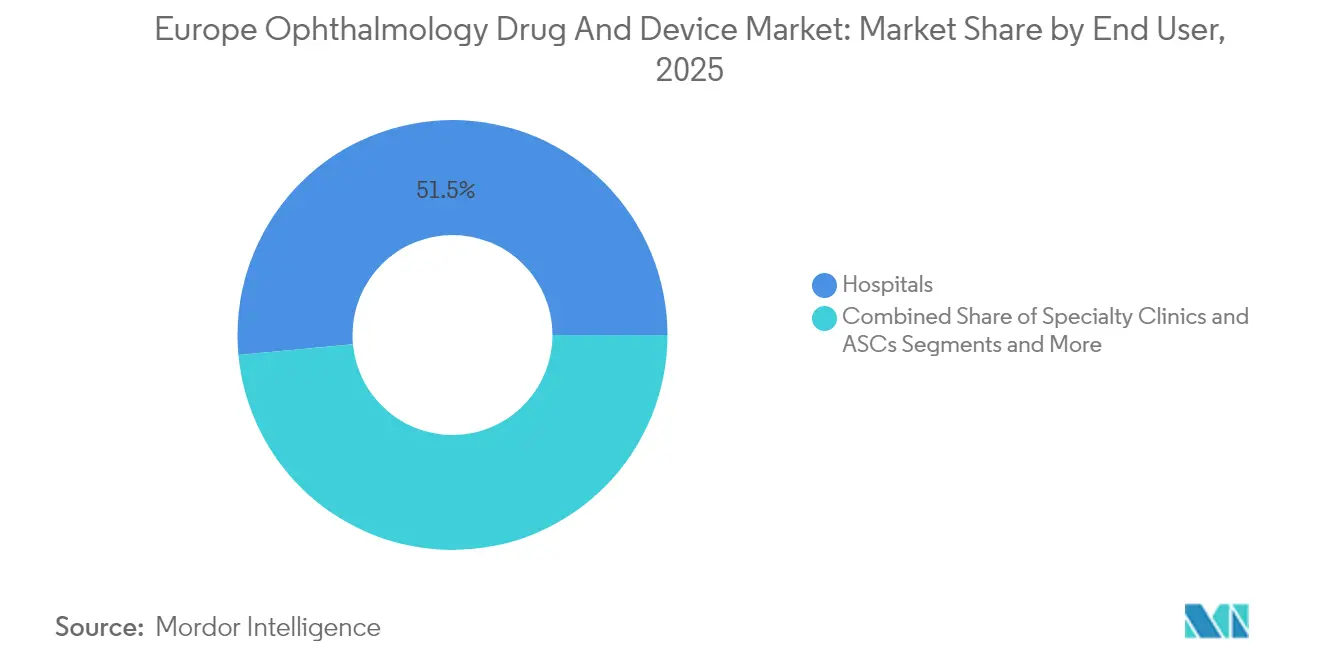

- By end user, hospitals held 51.48% of the Europe ophthalmic devices and drugs market size in 2025; ambulatory surgery centers are expanding at a 6.27% CAGR through 2031.

- By geography, Germany commanded 20.63% revenue share in 2025; the UK is forecast to be the fastest-growing market with a 5.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Ophthalmology Drug And Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence Of Chronic Eye Diseases | +2.10% | EU-wide, concentrated in Germany, France, Italy | Long term (≥ 4 years) |

| Expanding Geriatric Population Base | +1.80% | EU-wide, particularly Northern Europe | Long term (≥ 4 years) |

| Rapid Adoption Of Minimally-Invasive Glaucoma Surgery (MIGS) | +1.50% | Germany, UK, France, Spain | Medium term (2-4 years) |

| AI-Enabled Diagnostic Imaging & Remote Screening Rollout | +1.20% | Germany, UK, Scandinavia | Short term (≤ 2 years) |

| Surge In Sustained-Release Ocular Drug-Delivery Approvals | +0.90% | EU-wide, regulatory harmonization | Medium term (2-4 years) |

| EU Funding Programs For Ophthalmic R&D And Start-Ups | +0.40% | EU-wide, concentrated in research hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Chronic Eye Diseases

The incidence of age-related macular degeneration and diabetic retinopathy is climbing as Europe’s population ages, generating a durable demand base for both surgical and pharmaceutical interventions.[1]Nature Editors, “Economic Burden of Retinal Disorders to 2030,” nature.com Health systems are embedding ophthalmic screening into routine primary care, and German pilots using AI achieved 100% sensitivity for diabetic-retinopathy detection, catalyzing wider adoption. The economic burden of retinal disorders is estimated to hit EUR 99.8 billion by 2030, bolstering procurement budgets for advanced diagnostic equipment and sustained-release injectables.

Expanding Geriatric Population Base

Individuals aged 65 years or older constitute Europe’s fastest-growing cohort and exhibit the highest prevalence of cataract, glaucoma, and AMD. National services are tackling surgical backlogs by contracting private providers, a model that raised UK cataract procedure volumes 40% over pre-pandemic levels.[2]The Guardian Health Desk, “Private Providers Perform Majority of NHS Cataract Surgeries,” theguardian.com A larger elderly population simultaneously fuels premium IOL demand, reflecting patient preference for spectacle independence and rapid visual recovery.

Rapid Adoption of Minimally Invasive Glaucoma Surgery

German registry data show glaucoma procedures climbing 75% between 2006 and 2018, with MIGS devices now exceeding 11% of total surgeries. Devices such as the XEN Gel Stent deliver 75.9% success rates in European trials and render 55.2% of patients medication-free within six months. Combination cataract-MIGS procedures are becoming routine, creating bundled device revenue streams and shorter recovery windows.

AI-Enabled Diagnostic Imaging & Remote Screening Rollout

Validated algorithms reach sensitivities above 90% for key retinal conditions, and Aireen secured CE-MDR IIb clearance for an autonomous cloud-based system in 2024.[3]Aireen Communications Team, “Aireen – CE-MDR IIb Certified Autonomous Eye-Screening Platform,” Aireen, aireen.com Hospitals integrate AI triage with tele-ophthalmology to stretch specialist capacity, particularly in rural Scandinavia, thereby accelerating early disease detection and reducing avoidable vision loss.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost & Reimbursement Gaps For Premium Lenses/MIGS | -1.40% | Germany, France, UK, Netherlands | Medium term (2-4 years) |

| Stringent EU MDR Compliance Burden On SMEs | -0.80% | EU-wide, particularly affecting smaller companies | Short term (≤ 2 years) |

| Sub-Optimal Patient Adherence To Multi-Dose Eyedrop Regimens | -0.60% | EU-wide, elderly population focus | Long term (≥ 4 years) |

| Supply-Chain-Driven API Shortages For Sterile Ophthalmic Drugs | -0.40% | EU-wide, manufacturing concentration risk | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost and Reimbursement Gaps for Premium Lenses/MIGS

Cataract surgery tariff disparities range from EUR 432.5 (USD 507.1) in Poland to EUR 3,411.96 (USD 4,001.21) in Portugal, causing uneven patient access to premium IOLs. Co-payment requirements depress uptake in social-insurance markets, while MIGS reimbursement remains procedure-specific, creating friction for innovators and clinicians alike. Germany’s 2025 abolition of fixed prices for visual aids illustrates the fluid reimbursement landscape.

Stringent EU MDR Compliance Burden on SMEs

Certification costs have risen to 30%, and smaller manufacturers face resource diversion from R&D to documentation and surveillance, slowing product pipelines. Master UDI-DI obligations for contact lenses from November 2025 further heighten administrative overhead, though temporary exceptions aim to prevent supply bottlenecks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Surgical Devices Extend Premium Leadership

Surgical devices generated 46.12% of total 2025 revenue within the Europe ophthalmic devices and drugs market and continue to command premium pricing due to constant innovation. Alcon holds about 60% global share in presbyopia-correcting IOLs and has replicated similar penetration across major EU economies. Phaco platforms and femtosecond lasers secure attractive service contracts, while the fastest-expanding sub-segment is MIGS. The segment’s value proposition rises as bundled cataract-plus-MIGS procedures reduce overall care episodes.

Meanwhile, new hydrogel implants and refillable ocular reservoirs target adherence gaps. Vision-care devices retain stable revenue streams via contact-lens material upgrades and blue-light-filter spectacles. Alcon’s 2025 Clareon PanOptix Pro IOL, boasting 94% light utilization, exemplifies engineering efforts that sustain price premiums. Across all modalities, companies intensify R&D to capture an ageing demographic seeking spectacle independence and rapid recovery.

By Disease: Cataract Dominance, Glaucoma Momentum

Cataract therapies contributed 29.03% of 2025 revenue, underpinning the Europe ophthalmic devices and drugs market size due to universal reimbursement and high procedure volumes. Premium IOLs drive upsell opportunities, improving manufacturer margins. Glaucoma therapeutics lead growth at a 6.54% CAGR through 2031 on the back of MIGS and polymer-based sustained-release implants that eliminate drop fatigue.

AMD, diabetic retinopathy, and uveitis remain important, with Roche re-launching Susvimo in 2024 to offer a six-month anti-VEGF interval. Gene therapies in early trials signal longer-term disruption potential. Disease-level segmentation guides product-launch prioritization and informs payer negotiation strategies across Europe’s heterogeneous health systems.

By End User: ASC Uptake Quickens

Hospitals retained 51.48% revenue in 2025 thanks to installed capital equipment and complex case management. Yet ambulatory surgery centers posted a 6.27% CAGR. They will capture a growing share of the Europe ophthalmic devices and drugs market by 2031 as regulators push day-case pathways and operators expand capacity. The UK showcases the trend, with 60% of NHS cataract surgeries now performed in private clinics.

Retail optics and online pharmacies benefit from contact-lens subscriptions and dry-eye product lines. Specialty clinics leverage focused expertise to market premium vision-correction packages, while tele-ophthalmology broadens rural reach.

Geography Analysis

Germany generated 20.63% of 2025 revenue, reflecting substantial insurer reimbursement and early adoption of premium technologies. Carl Zeiss Meditec reported 14.1% EMEA revenue growth in H1 2024/25, buoyed by robust German demand. The country functions as a launchpad for MIGS and AI diagnostics, with clinical evidence and pricing benchmarks that ripple across neighboring markets.

The United Kingdom is projected to grow at 5.98% CAGR to 2031, the fastest in Western Europe, as NHS outsourcing expanded procedure counts by 40% versus pre-pandemic baselines. Post-Brexit regulatory divergence remains limited, allowing manufacturers to expedite parallel approvals through the UK MHRA and EU MDR pathways. Investments in Moorfields Eye Hospital’s electronic records and Optometrists-Ophthalmologists shared-care schemes solidify systemic capacity.

France, Italy, and Spain combine sizable populations with differing payment models. France relies heavily on ophthalmologists for primary eye care, intensifying capacity constraints. Italy’s regional financing disparities call for tailored pricing, whereas Spain harnesses medical tourism and private insurance to accelerate premium adoption. Emerging EU members in Eastern Europe are modernizing surgical theaters via cohesion funds and represent white space for mid-tier suppliers.

Collectively, these dynamics ensure that the Europe ophthalmic devices and drugs market remains anchored in its Big-5 economies while offering growth corridors in both North-Western innovation hubs and South-Eastern catch-up regions.

Competitive Landscape

Competition is moderate, with the top five vendors controlling roughly 55% of 2024 revenue. Alcon dominates cataract capital equipment and contact lenses, whereas Johnson & Johnson Vision leverages Acuvue and Tecnis franchises to retain share. EssilorLuxottica’s 2025 acquisition of Optegra clinics and Heidelberg Engineering illustrates vertical integration into diagnostics and surgical services.

Carl Zeiss Meditec amplified its vitreoretinal surgery footprint through the 2025 purchase of DORC and continues to merge optics with software to lock in workflow ecosystems. In pharmaceuticals, Novartis and Roche lead anti-VEGF therapies, while Bausch + Lomb expanded MIGS options via Elios Vision in 2024. Start-ups in AI and gene therapy are attracting EU Horizon grants and venture funding, compelling incumbents to pursue licensing and minority stakes.

Pricing power concentrates around premium IOLs, femto lasers, and sustained-release implants, yet EU tender cycles and MDR compliance costs challenge margins. Players with global supply chains are also mitigating API shortages by dual-sourcing sterile ingredients.

Europe Ophthalmology Drug And Device Industry Leaders

Topcon Corporation

Johnson & Johnson

Carl Zeiss Meditec AG

Pfizer

Nidek Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: EssilorLuxottica acquired Optegra clinics to deepen its presence in surgical eye care.

- April 2025: Carl Zeiss Meditec finalized the DORC acquisition, integrating the EVA NEXUS platform .

- March 2025: Alcon secured majority control of Aurion Biotech and its corneal-cell therapy AURN001.

- February 2025: EssilorLuxottica’s Nuance Audio hearing-aid glasses gained FDA and CE approvals.

Europe Ophthalmology Drug And Device Market Report Scope

As per the scope of the report, ophthalmic drugs are administered to the eyes, most typically as an eye drop formulation. These topical formulations are used to combat a multitude of diseased states of the eye and ophthalmic devices are medical equipment designed for diagnosis, surgery, and vision correction. These devices gain increased importance and adoption due to the high prevalence of various ophthalmic diseases such as glaucoma, cataract, and other vision-related issues. The Europe Ophthalmology Drug and Devices Market is Segmented by Product (Devices (Surgical Devices (Intraocular Lenses, Ophthalmic Lasers, Other Surgical Devices), Diagnostic Devices), Drugs (Glaucoma Drugs, Retinal Disorder Drugs, Dry Eye Drugs, Allergic Conjunctivitis, and Inflammation Drugs, and Other Drugs)), Disease (Glaucoma, Cataract, Age-related Macular Degeneration, Inflammatory Diseases, Refractive Disorders, and Other Diseases) and Geography (Germany, United Kingdom, France, Italy, Spain and the Rest of Europe). The report offers the value (in USD million) for the above segments.

By Product

| Devices | Surgical Devices | Intra-ocular Lenses |

| Ophthalmic Lasers | ||

| Phacoemulsification Systems | ||

| Other Surgical Devices | ||

| Diagnostic Devices | Optical Coherence Tomography Scanners | |

| Fundus Cameras | ||

| Tonometers | ||

| Other Diagnostic Devices | ||

| Vision Care Devices | Contact Lenses | |

| Spectacle Lenses | ||

| Drugs | Glaucoma Drugs | |

| Retinal Disorder Drugs | ||

| Dry-Eye Therapies | ||

| Anti-Allergy / Anti-Inflammatory Drugs | ||

| Anti-Infective Drugs | ||

| Other Drugs | ||

By Disease

| Glaucoma |

| Cataract |

| Age-related Macular Degeneration |

| Diabetic Retinopathy |

| Inflammatory Diseases |

| Refractive Disorders |

| Other Diseases |

By End User

| Hospitals |

| Specialty Clinics & ASCs |

| Retail Pharmacies & Optical Stores |

| Online Pharmacies |

Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Product | Devices | Surgical Devices | Intra-ocular Lenses |

| Ophthalmic Lasers | |||

| Phacoemulsification Systems | |||

| Other Surgical Devices | |||

| Diagnostic Devices | Optical Coherence Tomography Scanners | ||

| Fundus Cameras | |||

| Tonometers | |||

| Other Diagnostic Devices | |||

| Vision Care Devices | Contact Lenses | ||

| Spectacle Lenses | |||

| Drugs | Glaucoma Drugs | ||

| Retinal Disorder Drugs | |||

| Dry-Eye Therapies | |||

| Anti-Allergy / Anti-Inflammatory Drugs | |||

| Anti-Infective Drugs | |||

| Other Drugs | |||

| By Disease | Glaucoma | ||

| Cataract | |||

| Age-related Macular Degeneration | |||

| Diabetic Retinopathy | |||

| Inflammatory Diseases | |||

| Refractive Disorders | |||

| Other Diseases | |||

| By End User | Hospitals | ||

| Specialty Clinics & ASCs | |||

| Retail Pharmacies & Optical Stores | |||

| Online Pharmacies | |||

| Geography | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

Key Questions Answered in the Report

What is the current Europe Ophthalmology Drug and Device Market size?

The Europe Ophthalmology Drug and Device Market is projected to register a CAGR of 7.32% during the forecast period (2026-2031)

Who are the key players in Europe Ophthalmology Drug and Device Market?

Topcon Corporation, Johnson & Johnson, Carl Zeiss Meditec AG, Pfizer and Nidek Co. Ltd are the major companies operating in the Europe Ophthalmology Drug and Device Market.

What years does this Europe Ophthalmology Drug and Device Market cover?

The report covers the Europe Ophthalmology Drug and Device Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Europe Ophthalmology Drug and Device Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: