Transdermal Skin Patches Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 9.8 Billion |

| Market Size (2031) | USD 12.4 Billion |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Transdermal Skin Patches Market Analysis by Mordor Intelligence

The Transdermal Skin Patches Market size was valued at USD 9.35 billion in 2025 and estimated to grow from USD 9.8 billion in 2026 to reach USD 12.4 billion by 2031, at a CAGR of 4.82% during the forecast period (2026-2031). Sustained growth is underpinned by patent-cliff pressures that push pharmaceutical companies toward reformulating blockbuster drugs into patches, the expanding pool of self-administered chronic-care therapies, and rapid progress in microneedle technology that widens the range of molecules suitable for dermal delivery. Manufacturers also benefit from clearer U.S. FDA combination-product guidance, accelerating development timelines and spurring investment in next-generation systems. Meanwhile, online pharmacies gain traction as patients gravitate toward discreet, subscription-based purchasing models that align with the modality’s convenience advantages.

Key Report Takeaways

By therapeutic area, smoking cessation led with 64.53% of the transdermal skin patches market share in 2024, whereas neurological disorders are advancing at a 5.38% CAGR through 2030.

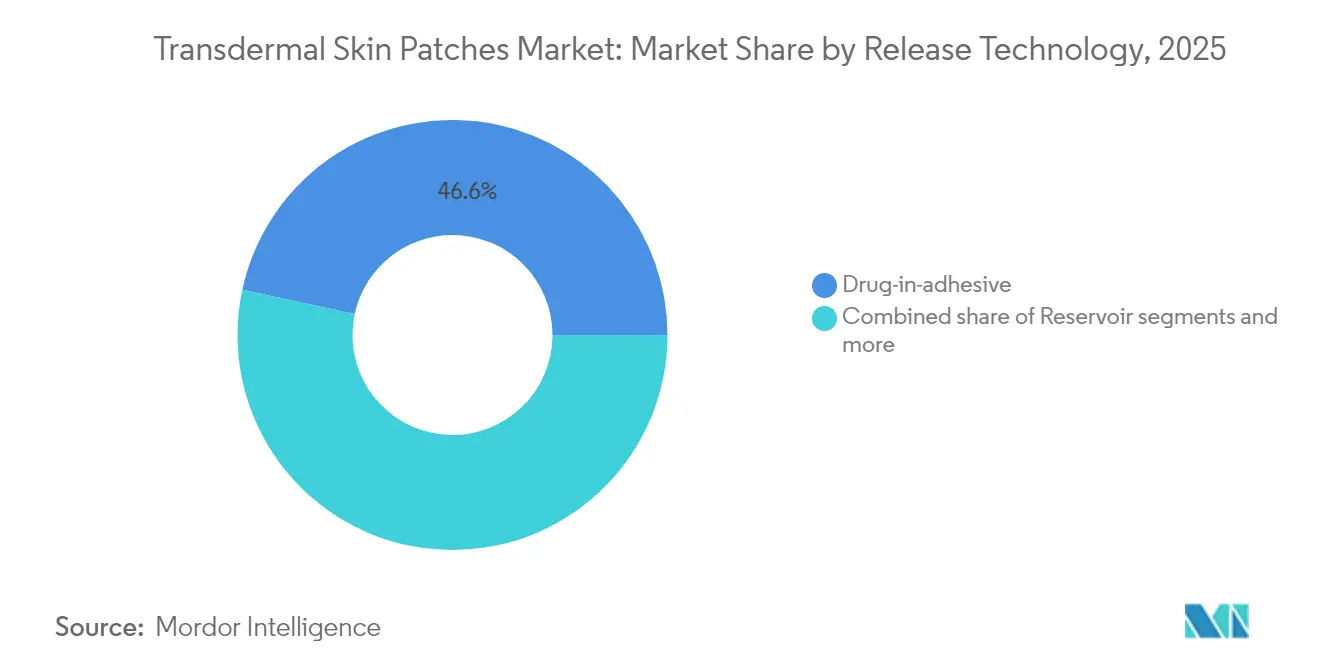

By release technology, drug-in-adhesive systems captured 47.13% of the transdermal skin patches market size in 2024, while microneedle-assisted formats are expanding at 4.91% CAGR between 2025-2030.

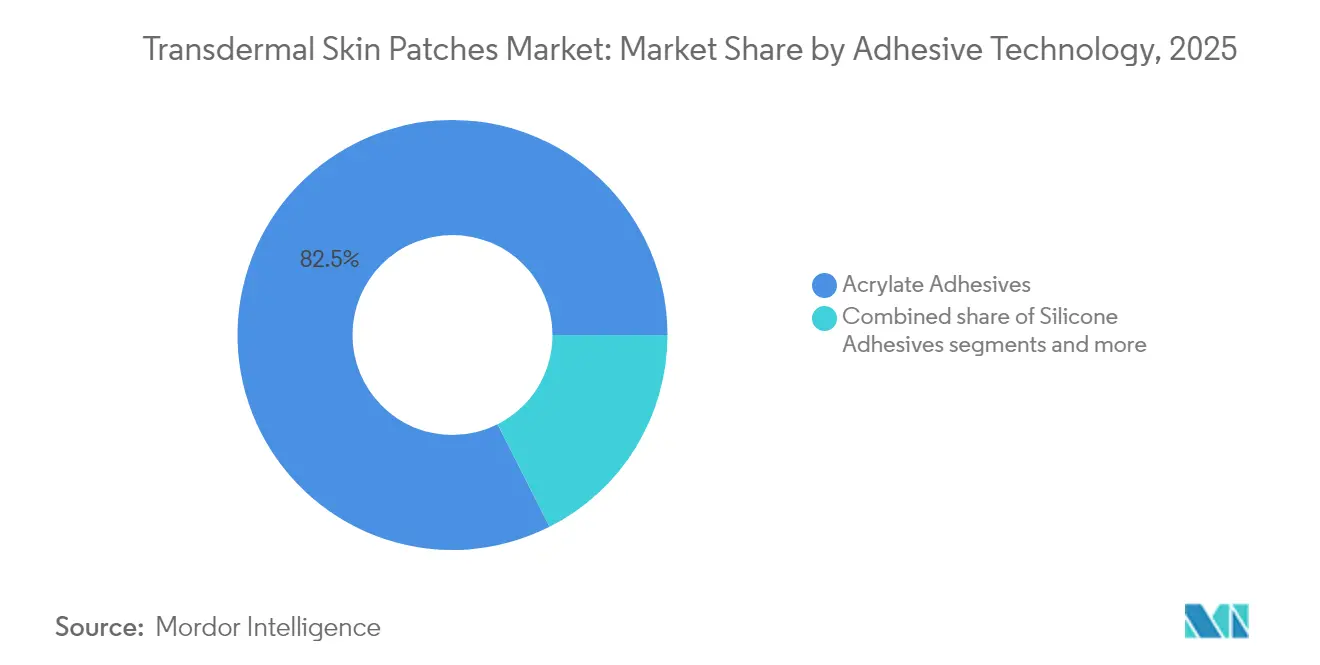

By adhesive technology, acrylate platforms dominated with 83.12% revenue share in 2024; hydrogel formulations are projected to grow at 5.78% CAGR to 2030.

By distribution channel, retail pharmacies held 71.23% share of the transdermal skin patches market in 2024, yet online pharmacies exhibit the fastest growth at 5.96% CAGR during the forecast horizon.

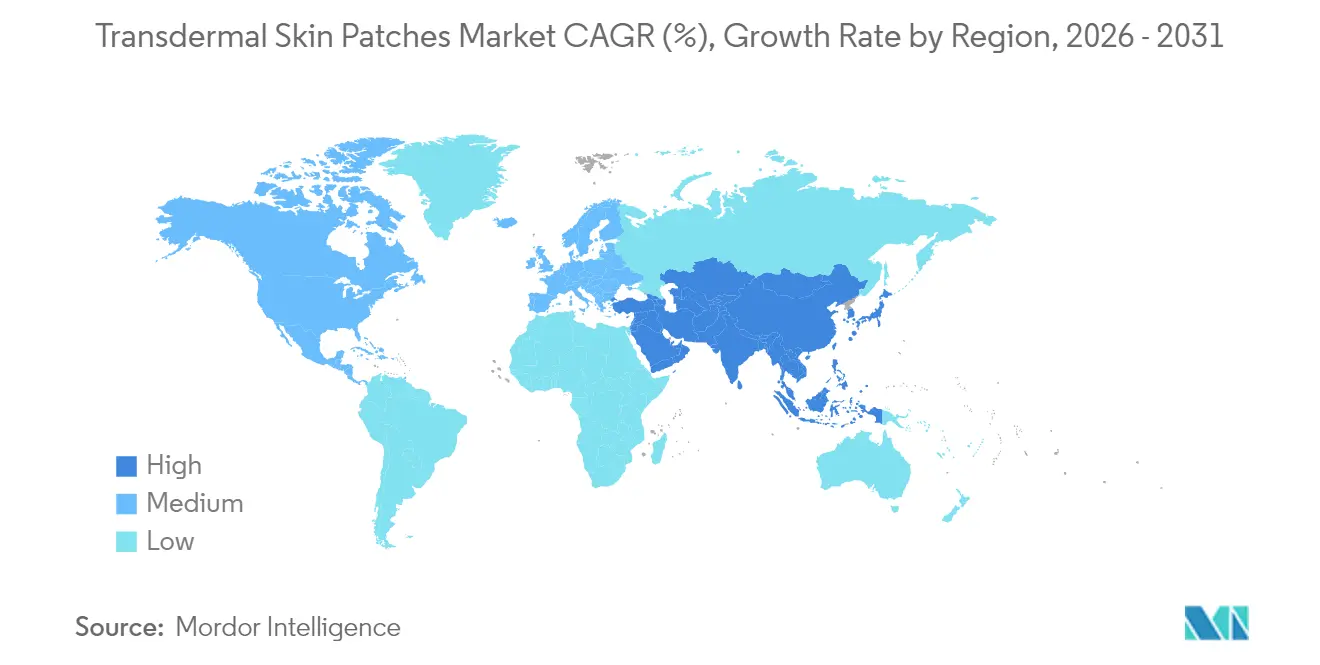

North America commanded 39.23% of the transdermal skin patches market in 2024, whereas Asia-Pacific represents the fastest-growing region with a 5.19% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Transdermal Skin Patches Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent cliff–driven switch to novel delivery formats | +1.2% | North America & Europe | Medium term (2-4 years) |

| Rapid rise of self-administered chronic-care therapies | +0.9% | APAC & North America | Long term (≥ 4 years) |

| Reimbursement expansion for smoking-cessation aids | +0.7% | North America & EU | Short term (≤ 2 years) |

| Microneedle/ionic-poration hybrids entering Phase III | +0.6% | United States & Japan | Long term (≥ 4 years) |

| AI-enabled adhesive design lowering skin-irritation rates | +0.4% | Developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patent Cliff–Driven Switch to Novel Delivery Formats

Pharmaceutical companies face USD 200 billion worth of patent expirations between 2025-2030, prompting reformulations that extend exclusivity while improving patient adherence. This pivot is pronounced in chronic pain and neurological therapies where patches circumvent hepatic first-pass metabolism, enabling lower dosing with steadier plasma levels. FDA guidance released in June 2024 clarified “Essential Drug Delivery Outputs,” reducing regulatory uncertainty and cutting pre-approval timelines by up to 12 months. Companies therefore treat transdermal delivery as both a life-cycle management tool and a compliance-boosting strategy for lifestyle medications.

Rapid Rise of Self-Administered Chronic-Care Therapies

Rising global prevalence of diabetes, hypertension, and hormone-related conditions elevates demand for home-based treatment that minimizes clinic visits. Transdermal insulin systems achieved 35% higher patient-satisfaction scores than subcutaneous injections in recent trials. APAC markets adopt patches quickly due to aging populations and rural care gaps, while elderly cohorts worldwide value the simple “apply-and-go” format that aids cognitive decline-related adherence issues.

Rapid Rise of Self-Administered Chronic-Care Therapies

Rising global prevalence of diabetes, hypertension, and hormone-related conditions elevates demand for home-based treatment that minimizes clinic visits. Transdermal insulin systems achieved 35% higher patient-satisfaction scores than subcutaneous injections in recent trials. APAC markets adopt patches quickly due to aging populations and rural care gaps, while elderly cohorts worldwide value the simple “apply-and-go” format that aids cognitive decline-related adherence issues.

Reimbursement Expansion for Smoking-Cessation Aids

Twenty U.S. states now provide comprehensive insurance coverage for nicotine patches. North Dakota Medicaid dropped prior authorization in 2025, mirroring private-insurer trends that see a 40% rise in patient completion of cessation programs when costs are fully covered. Because smoking cessation already holds the largest therapeutic share, broader reimbursement materially lifts revenue visibility for patch suppliers.

Restraints Impact Analysis of Transdermal Skin Patches Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High development cost vs. oral generics | -0.8% | Global, particularly impacting emerging markets | Medium term (2-4 years) |

| Skin-sensitivity litigation risks | -0.5% | North America & EU, with regulatory scrutiny | Long term (≥ 4 years) |

| Regulatory ambiguity on combination-device pathway (U.S. & EU) | -0.4% | North America & EU, affecting global development | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Development Cost vs. Oral Generics

Novel transdermal patches can cost USD 50 million to bring to market compared with USD 5-10 million for oral generics, largely due to specialized manufacturing and bioequivalence studies. In low-income settings, payers emphasize volume over innovation, challenging patch adoption despite clinical benefits. Combination-product regulations further raise costs with added device-testing requirements, squeezing smaller entrants.

Skin-Sensitivity Litigation Risks

Medical adhesive-related skin injury affects around 1.5% of users and has triggered multimillion-dollar settlements in the United States. Heightened FDA scrutiny now mandates extensive dermatology datasets, elongating approval and inflating insurance premiums. As a result, some firms restrict innovation to known acrylate systems, slowing the shift toward more biocompatible platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Transdermal Skin Patches Market Segment Analysis

By Release Technology:

Microneedles Challenge Traditional DominanceDrug-in-adhesive systems held 46.62% of the transdermal skin patches market share in 2025, reflecting process maturity, proven safety, and cost efficiency. Yet microneedle-assisted formats show the highest forecast CAGR at 4.88%, propelled by their ability to deliver peptides, vaccines, and even GLP-1 agonists with bioavailability above 50%. Reservoir and matrix patches maintain niche roles in controlled-release analgesia and generic pain management, respectively.

Microneedle advances resonate with pharmaceutical pipelines that now feature larger biologic molecules. Start-ups such as Anodyne Nanotech report room-temperature-stable patches that bypass cold-chain costs, opening emerging-market opportunities. As clinical data accumulate, the technology is expected to reallocate a portion of the transdermal skin patches market size away from injections, particularly in chronic metabolic and autoimmune care.

By Therapeutic Area:

Neurological Applications Drive Growth Beyond Smoking CessationSmoking-cessation patches continue to dominate with 64.01% share in 2025, anchored by public-health funding and strong clinical evidence. However, neurological disorders register the fastest growth at 5.14% CAGR on the back of steady-state drug delivery advantages for Parkinson’s and ADHD therapies. Hormone-replacement and pain-management segments remain stable, while cardiovascular and contraception patches serve targeted populations.

Continuous dermal release mitigates peak-trough fluctuations critical in central-nervous-system treatment. Rotigotine and methylphenidate patches exemplify the model, demonstrating improved motor control and attentional stability, respectively. Payers increasingly recognize reduced hospitalization and enhanced quality-of-life outcomes, bolstering formulary inclusion.

By Adhesive Technology:

Hydrogel Innovation Challenges Acrylate DominanceAcrylate adhesives comprised 82.45% of 2025 revenues, valued for robust stickiness and established safety profiles. Hydrogel variants, though only a minor slice of the transdermal skin patches market size today, are forecast to grow at 5.46% CAGR as bio-friendly polymers ease skin stress and enable moisture-regulated drug dispersion. Silicone options cater to geriatric and pediatric skin sensitivity, while eco-based adhesives remain nascent.

Hydrogels’ ability to host nanoparticles and buffer pH positions them for high-dose biologic patches. Alpha-tocopherol-infused liposomal hydrogels, for instance, deliver retinaldehyde without irritation over 24 hours, proving promise for long-wear dermatological therapies. As manufacturing costs decline, the technology is expected to erode acrylate’s lead, especially in premium therapy areas.

By Distribution Channel:

Digital Transformation Accelerates Online GrowthRetail pharmacies accounted for 70.55% of sales in 2025, buoyed by pharmacist counseling and immediate pick-up convenience. Yet the online segment is expanding fastest at 5.62% CAGR, powered by telehealth integration, discrete delivery, and subscription models that synchronize refills. Hospital pharmacies dominate complex, multi-patch regimens, while direct-to-consumer channels serve cosmetic and lifestyle products.

Regulators now allow remote verification for prescription patches following 2024 FDA digital-health guidance, fostering app-linked adherence platforms and automated shipping. For chronic smokers and menopausal women, e-commerce mitigates stigma and encourages sustained therapy, further lifting the overall transdermal skin patches market.

Geography Analysis

North America Transdermal Skin Patches Market

North America led the transdermal skin patches market with 38.77% share in 2025, lifted by broad reimbursement for nicotine therapy, favorable IP protection, and streamlined FDA combination-product pathways. Medicare’s inclusion of patches for vasomotor symptom management in 2025 further widens uptake, while domestic manufacturing expansions, such as LGM Pharma’s USD 6 million facility upgrade, bolster supply resilience. U.S. demographic aging also raises demand for patch-based pain and hormone therapies requiring minimal dexterity.

Europe Transdermal Skin Patches Market

Europe follows with mature yet regulation-dense adoption. Implementation of MDR raises compliance costs, yet the European Medicines Agency’s 2024 Q&A clarifies device-drug integration requirements, reducing ambiguity. Hormone-replacement patches enjoy strong traction, though recent estradiol shortages underline the need for regional manufacturing redundancy. Additionally, smoking-cessation reimbursement across leading EU economies sustains steady volume despite fierce generic competition.

APAC Transdermal Skin Patches Market

Asia-Pacific represents the fastest-growing region, advancing at 5.06% CAGR through 2031. Aging populations in China and Japan, coupled with rising diabetes prevalence, create fertile ground for patch adoption. Regulatory harmonization across ASEAN, alongside local production investments, lowers market-entry barriers. China’s menopausal-therapy market illustrates the opportunity; clinicians increasingly recommend patches over oral estrogen due to lower thrombotic risk. Expanding e-commerce ecosystems also address rural accessibility challenges, propelling online patch sales.

Competitive Landscape

The transdermal skin patches market shows moderate concentration. Legacy firms such as Johnson & Johnson and Novartis leverage scale and regulatory expertise, but growth hinges on innovation rather than portfolio breadth. Emerging players—Anodyne Nanotech with HeroPatch and Medherant’s TEPI Patch—attract capital by targeting biologic delivery gaps. CordenPharma’s USD 980 million GLP-1 capacity expansion underscores industry belief in peptide-patch potential.

Partnerships dominate strategy. Big pharma pairs with specialist CMOs for microneedle fabrication, while consumer-health brands collaborate with AI adhesive developers to differentiate on comfort. Competitive intensity increases as FDA approves the first generic lidocaine 1.8% patch in 2025, signaling an emerging off-patent wave. Nevertheless, experience navigating device-drug regulations provides incumbents an edge, balancing disruptive threats with collaboration prospects.

Transdermal Skin Patches Industry Leaders

Teva Pharmaceuticals USA Inc.

Novartis AG

Teikoku Pharma USA, Inc.

Viatris, Inc.

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Transdermal Skin Patches Market Companies Covered in this Report

- 3M

- Abbott Laboratories

- Johnson & Johnson

- Novartis

- Teva Pharmaceutical Industries

- Hisamitsu Pharmaceutical

- GlaxoSmithKline

- Bayer

- Viatris

- LTS Lohmann Therapie-Systeme

- Nitto Denko

- Corium LLC

- Agile Therapeutics Inc.

- UCB

- Luye Pharma Group Ltd.

- Zydus Lifesciences Ltd.

- Sparsha Pharma International Pvt Ltd

- Tapemark Inc.

- AdhexPharma

Recent Industry Developments in Transdermal Skin Patches Market

- March 2025: LGM Pharma invested USD 6 million in U.S. semi-solid and transdermal production

- March 2025: FDA approved Aveva’s first generic lidocaine 1.8% patch

Global Transdermal Skin Patches Market Report Scope

As per the report's scope, the transdermal patch is a medicated adhesive patch placed on the skin to deliver a precise dose of medication. These patches deliver medicine dosage through the skin using a diffusion technique, which gets released into the bloodstream over a long period. The transdermal skin patches market is segmented by type, application, and geography. The market is segmented into single-layer drug-in-adhesive, multi-layer drug-in-adhesive, matrix, and other types. By application, the market is segmented into pain relief, smoking reduction and cessation aid, overactive bladder, hormonal therapy, and other applications. The market is segmented by geography into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value in USD for the above segments.

Segmentation Overview

| Drug-in-adhesive |

| Reservoir |

| Matrix |

| Microneedle-assisted |

| Others |

| Smoking Cessation |

| Hormone Replacement Therapy |

| Pain Management |

| Neurological Disorders |

| Cardiovascular Disorders |

| Contraception |

| Others |

| Acrylate Adhesives |

| Silicone Adhesives |

| Hydrogel Adhesives |

| Other Adhesives |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Release Technology (Value) | Drug-in-adhesive | |

| Reservoir | ||

| Matrix | ||

| Microneedle-assisted | ||

| Others | ||

| By Therapeutic Area (Value) | Smoking Cessation | |

| Hormone Replacement Therapy | ||

| Pain Management | ||

| Neurological Disorders | ||

| Cardiovascular Disorders | ||

| Contraception | ||

| Others | ||

| By Adhesive Technology (Value) | Acrylate Adhesives | |

| Silicone Adhesives | ||

| Hydrogel Adhesives | ||

| Other Adhesives | ||

| By Distribution Channel (Value) | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Others | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Transdermal Skin Patches Market?

The Transdermal Skin Patches Market size is expected to reach USD 9.8 billion in 2026 and grow at a CAGR of 4.82% to reach USD 12.4 billion by 2031.

What is the current Transdermal Skin Patches Market size?

In 2026, the Transdermal Skin Patches Market size is expected to reach USD 9.8 billion.

Who are the key players in Transdermal Skin Patches Market?

Teva Pharmaceuticals USA Inc., Novartis AG, Teikoku Pharma USA, Inc., Viatris, Inc. and Johnson & Johnson are the major companies operating in the Transdermal Skin Patches Market.

Which is the fastest growing region in Transdermal Skin Patches Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Transdermal Skin Patches Market?

In 2026, the North America accounts for the largest market share in Transdermal Skin Patches Market.

What years does this Transdermal Skin Patches Market cover, and what was the market size in 2025?

In 2025, the Transdermal Skin Patches Market size was estimated at USD 9.8 billion. The report covers the Transdermal Skin Patches Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Transdermal Skin Patches Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: