Hyperbaric Oxygen Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.88 Billion |

| Market Size (2031) | USD 10.55 Billion |

| Growth Rate (2026 - 2031) | 6.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hyperbaric Oxygen Therapy Market Analysis by Mordor Intelligence

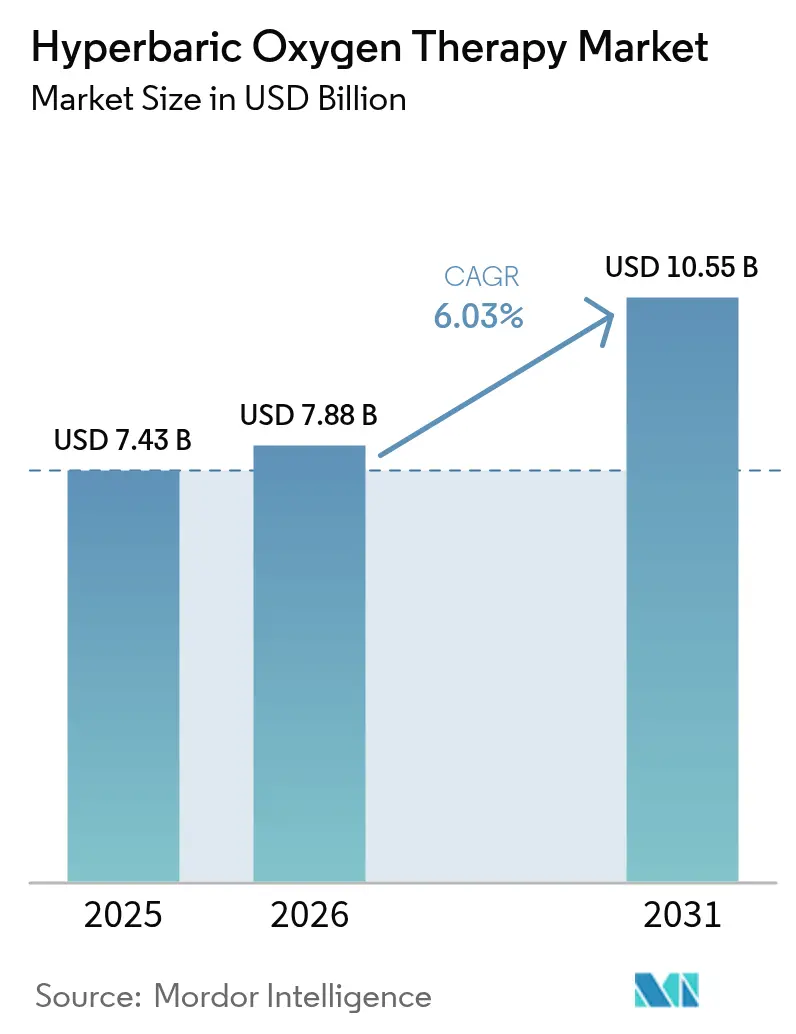

The hyperbaric oxygen therapy market size was valued at USD 7.43 billion in 2025 and estimated to grow from USD 7.88 billion in 2026 to reach USD 10.55 billion by 2031, at a CAGR of 6.03% during the forecast period (2026-2031). Continuous publication of positive clinical data in wound care, diabetic-foot management and emerging post-viral indications underpins this expansion. Providers view the therapy as a cost-effective way to prevent amputations, shorten inpatient stays and improve quality scores, which sustains hospital demand even as portable systems open new care pathways. Asia-Pacific captures growing capital flows thanks to government-funded chamber hubs in tourist zones and aggressive medical-tourism marketing, while North America remains the clinical-research anchor that validates new indications. Device makers add digital sensors, AI-guided oxygen dosing and remote-monitoring software, raising clinician confidence and reducing adverse-event risk, which in turn reinforces the hyperbaric oxygen therapy market growth outlook.

Key Report Takeaways

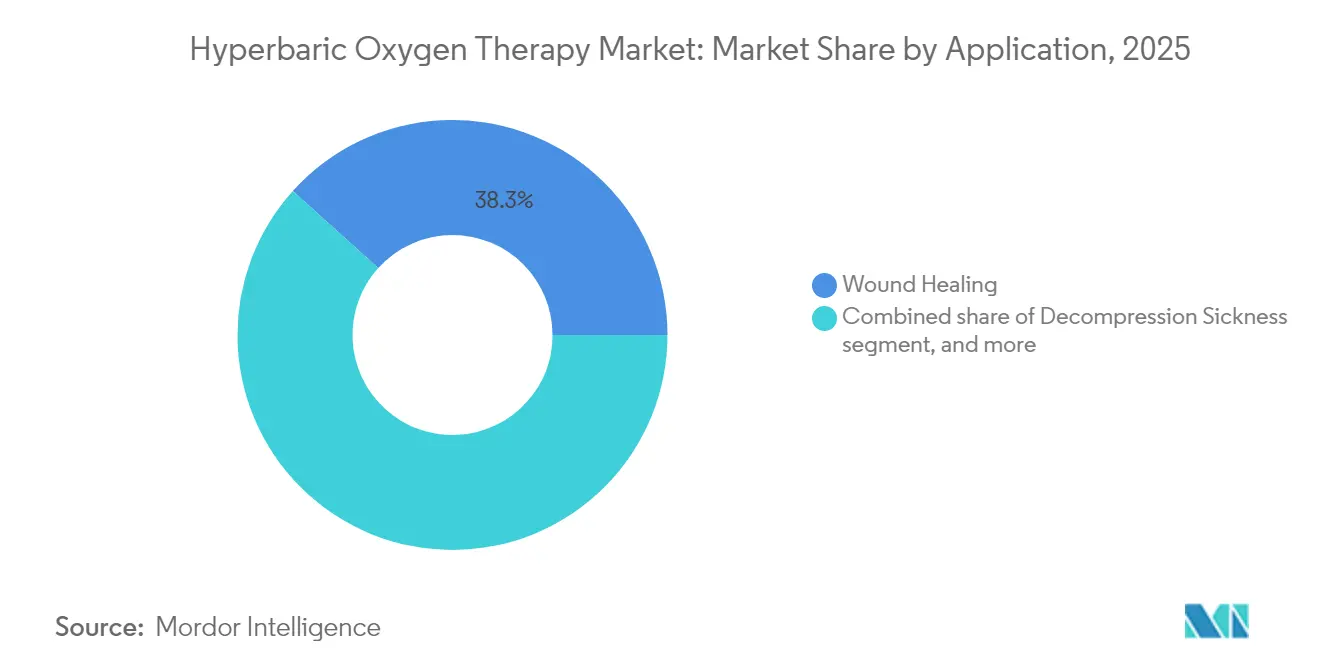

- By application, wound healing led with 38.32% of hyperbaric oxygen therapy market share in 2025, while diabetic-foot ulcers are projected to expand at an 8.52% CAGR through 2031.

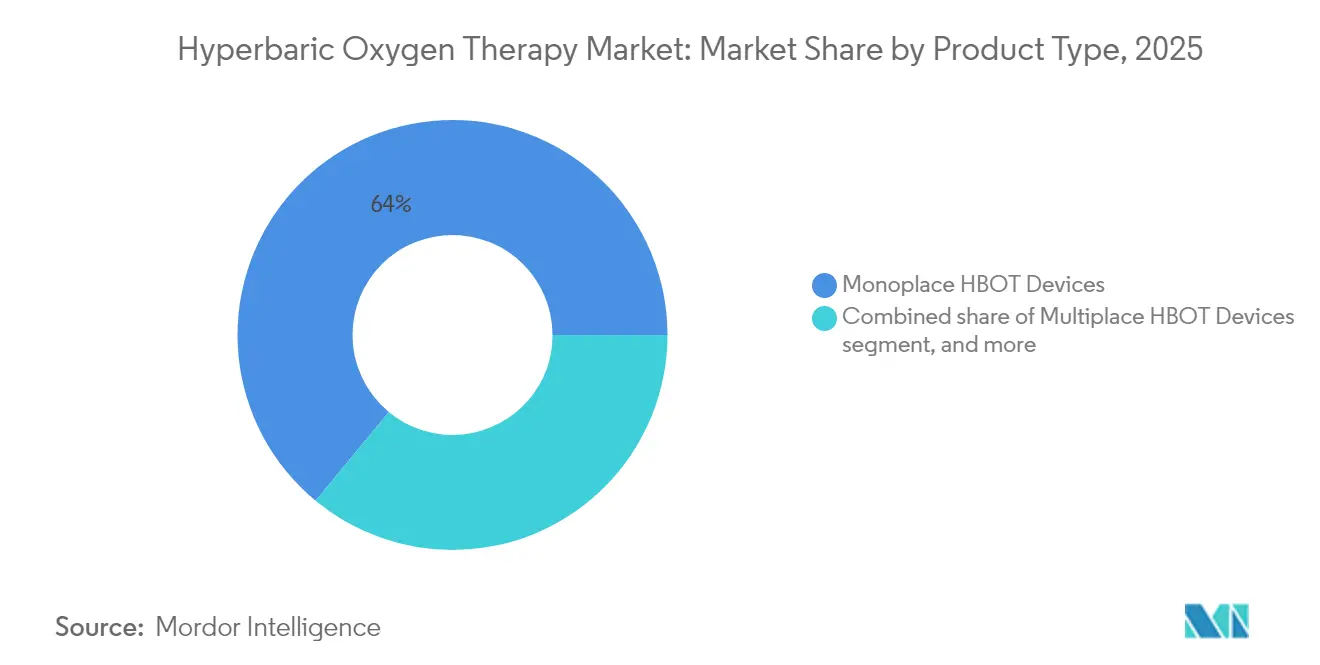

- By product type, monoplace chambers held 64.01% revenue in 2025; portable and topical systems are forecast to grow at an 8.71% CAGR to 2031.

- By end user, hospitals retained 54.85% of the hyperbaric oxygen therapy market size in 2025, yet the home-care channel is advancing at a 9.42% CAGR to 2031.

- By geography, North America accounted for 42.08% revenue in 2025, whereas Asia-Pacific is set to grow the fastest with a 7.32% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Hyperbaric Oxygen Therapy Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of acute & chronic wounds | +1.2% | North America & Europe | Medium term (2-4 years) |

| Growing prevalence of diabetes & diabetic-foot ulcers | +1.8% | Asia-Pacific & North America | Long term (≥4 years) |

| Technological advances (portable, digital & hybrid chambers) | +1.1% | North America, EU, accelerating APAC | Short term (≤2 years) |

| Expanding use in cosmetic & sports-medicine procedures | +0.7% | North America, Europe, select APAC | Medium term (2-4 years) |

| AI-driven oxygen-dosing & remote-monitoring platforms | +0.4% | Developed markets first | Long term (≥4 years) |

| Repurposing surplus industrial pressure vessels in EMS | +0.3% | Cost-sensitive regions | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Acute & Chronic Wounds

Diabetic-foot ulcers affect 15% of the global diabetes population and account for a disproportionate share of inpatient costs. Hyperbaric sessions elevate tissue oxygen levels, support angiogenesis and achieve a 44-fold improvement in reaching the first 30% wound-size reduction milestone compared with standard care[1]Prosiding Gunabangsa, “HBOT in Chronic Wounds,” gbg.or.id. Payers respond by broadening coverage for chronic-wound protocols, while hospital wound centers allocate capital for additional monoplace chambers to meet referral demand.

Growing Prevalence of Diabetes & Diabetic-Foot Ulcers

Meta-analyses show significant gains in hematological and inflammatory markers and higher closure percentages when diabetic wounds receive hyperbaric oxygen therapy. Clinicians also record faster peripheral-neuropathy recovery, which positions HBOT as a multi-benefit intervention in endocrine clinics. Asia-Pacific’s accelerating diabetes incidence drives chamber installations in regional hospitals that seek to curb future amputation rates.

Technological Advances in Portable, Digital & Hybrid Chambers

Sechrist Industries’ 2024 launch of software-integrated chambers provides real-time gas, temperature and humidity tracking, allowing responsive oxygen adjustments that refine outcomes. OxyRevo’s Apex36 portable unit delivers 1.5 ATA therapy in outpatient or residential settings, expanding access where hospital capacity is constrained. Academic studies confirm sensor accuracy improvements at varied pressures, and VR-based training simulators close the skills gap for new operators.

Expanding Use in Cosmetic & Sports-Medicine Procedures

A 296-patient study in aesthetic surgery showed faster recovery and shorter work absences when hyperbaric sessions followed liposuction or facial work. Sports-medicine physicians add sessions to accelerate muscle repair and reduce inflammation, driving chamber adoption in private orthopedic clinics. These elective-care markets bring premium reimbursement rates that offset capital costs for providers.

Restraints Impact Analysis of Hyperbaric Oxygen Therapy Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex & opex of HBOT installations | -1.5% | Global, cost-sensitive markets | Medium term (2-4 years) |

| FDA-approved vs. off-label indication gap | -0.8% | North America, spillover globally | Long term (≥4 years) |

| Escalating fire-safety insurance premiums for centers | -0.6% | North America, Europe, price-sensitive APAC | Short term (≤2 years) |

| Shortage of certified hyperbaric clinicians & technicians | -0.4% | Global, acute in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex & Opex of HBOT Installations

Even an entry-level monoplace unit can cost USD 40,000 to USD 200,000, and complete facility build-outs range from USD 250,000 to USD 750,000 once specialized ventilation, fire suppression and accreditation fees are added. Annual service contracts and operator training push total ownership higher, curbing adoption in smaller clinics. Leasing trims upfront expense but extends payback periods beyond five years for low-volume sites.

FDA-Approved Vs. Off-Label Indication Gap

The United States restricts reimbursement to 14 established indications, leaving post-COVID cognitive complaints and several neurological disorders ineligible despite encouraging pilot data[2]U.S. Food & Drug Administration, “Hyperbaric Chamber Device Classification,” fda.gov. Providers must absorb costs or ask patients to self-pay, which slows diffusion into promising areas until larger trials conclude and regulators update labeling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Hyperbaric Oxygen Therapy Market Segment Analysis

By Application:

Diabetic Complications Drive Growth AccelerationThe hyperbaric oxygen therapy market size for wound-healing indications reached USD 2.85 billion in 2025 and maintained leadership with a 38.32% revenue share. Integrated wound-care centers rely on HBOT to lower infection risk and speed closure for pressure ulcers, venous ulcers and complex surgical wounds. The diabetic-foot-ulcer sub-segment grows fastest at an 8.52% CAGR due to rising global diabetes prevalence and systematic-review evidence showing 67.5% full-healing rates with only 17.5% recurrence within 12 months. Decompression-sickness demand stays stable among commercial dive and tourism hubs, supported by centers in Thailand that treat up to 500,000 visiting divers each year.

Diversification continues as clinicians test HBOT in radiation-induced cystitis and hemorrhagic complications, reporting promising symptoms relief even in elderly patients who exhausted standard measures. Long-COVID patient cohorts also benefit from improved cognition and reduced fatigue after individualized hyperbaric regimens, broadening the therapy’s neurologic footprint. Together, these applications anchor a demand profile that keeps equipment utilization high across multidisciplinary hospital programs.

By Product Type:

Portable Innovation Challenges Monoplace DominanceMonoplace chambers commanded 64.01% revenue in 2025, helped by established clinical protocols and streamlined infection control that support quick patient throughput. Multiplace systems find niche roles in critical-care units where medical staff must enter the chamber to deliver interventions without compromising treatment pressure.

Portable and topical devices grow at an 8.71% CAGR, fueled by lighter composite materials, wheelchair-friendly entry doors and Bluetooth-enabled sensor suites that push real-time data to supervising physicians. Hybrid low-pressure models create incremental demand in community hospitals that cannot justify high-ATA infrastructure. Regulators meanwhile tighten safety checks following recent incidents, and accredited vendors that bundle operator-training modules into purchase contracts emerge as preferred partners.

By End User:

Home Care Disrupts the Hospital-Centric ModelHospitals captured 54.85% of the hyperbaric oxygen therapy market share in 2025 thanks to integrated vascular-surgery and emergency-medicine lines that feed a steady pipeline of reimbursable cases. Stand-alone wound-care clinics proliferate where outpatient payment rules favor day-case management. Specialized dive-medicine centers cluster along coastal tourism corridors, offering rapid decompression-sickness treatment for visiting divers.

The home-care channel shows a 9.42% CAGR as FDA-classified portable units enter the residential segment under physician prescription. Telehealth dashboards monitor session times, chamber pressure and oxygen concentration, allowing clinicians to intervene remotely if needed. Pay-for-performance insurers support home-based regimens to prevent costly readmissions linked to chronic wounds. Training videos, safety drills and standardized patient-selection criteria help mitigate residential-fire and oxygen-toxicity risks, unlocking a consumer-centric growth path for suppliers.

Geography Analysis

North America Hyperbaric Oxygen Therapy Market

North America held 42.08% revenue in 2025 and remains the research and reimbursement leader. Academic centers such as Duke and Mayo Clinic publish peer-reviewed outcome studies that influence global clinical-guideline writers. Insurers reimburse FDA-approved indications, which underpins steady chamber utilization. The 2025 Oakland County explosion renewed focus on accreditation, prompting regulators to intensify on-site inspections and raising the compliance bar for new entrants. Established manufacturers that offer turnkey safety packages are well positioned to benefit.

APAC, EMEA and South America Hyperbaric Oxygen Therapy Market

Asia-Pacific records the highest growth at a 7.32% CAGR up to 2031. The Philippines earmarked PHP 50 million to create hyperbaric hubs in key dive islands, a strategy expected to lift tourism revenue and improve diver safety. Thailand’s Bangkok Hospital markets international packages priced 50% to 90% below United States equivalents, attracting self-pay patients seeking wound-care or sports-recovery treatments. China still hosts the world’s largest installed base but faces a replacement wave as aging steel chambers approach end-of-life certification, creating a retrofit opportunity for suppliers. Europe is a mature yet innovation-oriented arena where national health services fund HBOT for approved oncologic and reconstructive applications. Germany’s stringent equipment-testing regime favors premium vendors with CE-marked pressure vessels, while the United Kingdom directs new spending toward community-based wound-care centers that include hyperbaric suites inside outpatient clinics. Middle East and Africa markets grow from a smaller base as Gulf state hospitals add HBOT to burn-unit protocols. South America sees moderate uptake, led by Brazil’s private orthopedic chains bundling post-surgery hyperbaric sessions into rehab packages.

Regulatory Landscape

Regulation for hyperbaric oxygen therapy devices and facilities is split between medical-device controls and pressure-vessel and facility safety regimes, which makes compliance a dual-track requirement for manufacturers and providers. In the United States, hyperbaric chambers are regulated by the FDA as Class II devices under 21 CFR 868.5470, with clearance pathways such as 510(k) and operational expectations that align with facility standards used by hospitals. The FDA formally recognized the 2024 edition of NFPA 99 (Health Care Facilities Code) in April 2025, and in August 2025 issued a Letter to Health Care Providers emphasizing adherence to manufacturer instructions to reduce electrical and static hazards during use, reinforcing scrutiny after safety incidents.

In Europe, chambers are governed by the EU Medical Devices Regulation (MDR) 2017/745 (commonly treated as Class IIb), while professional bodies support operational consistency through frameworks such as the European Code of Good Practice for Hyperbaric Oxygen Therapy referenced by European hyperbaric organizations. In Canada, hyperbaric chambers are licensed as Class III medical devices, and compliance guidance points to standards such as CSA Z275.1:23 for hyperbaric operations with alignment to ASME PVHO-1 for pressure vessels; a June 2026 compliance guidance update reiterated CSA Z275.1:23 as the current reference point. Across regions, regulators and associations also distinguish medical-grade HBOT from low-pressure, non-medical wellness devices, tightening the acceptance bar for facilities, procurement, and reimbursement-linked documentation.

Competitive Landscape

The hyperbaric oxygen therapy market is moderately concentrated, with a handful of players leveraging large installed fleets and comprehensive service offers. Sechrist Industries operates more than 2,800 monoplace systems in the United States, surpassing all competitors combined and ensuring dense parts-supply coverage. Its 2024 software upgrade added predictive-maintenance analytics that alert technicians ahead of component failure, cutting downtime and strengthening customer loyalty. Perry Baromedical capitalizes on a dual-portfolio strategy, supplying both monoplace and multiplace chambers that share modular subassemblies to streamline manufacturing costs.

Safety credentials now rank second only to price. The Undersea and Hyperbaric Medical Society’s 2025 guidance urges clinics to limit chamber installation to vendors offering NFPA-compliant construction and operator-training curricula[3]Undersea and Hyperbaric Medical Society, “2025 Safety Update,” uhms.org. Portable-device specialists partner with telehealth platforms to link home-care sessions to supervising physicians, targeting diabetic-foot patients who require long treatment series. Regional manufacturers explore refurbishing industrial pressure vessels for emergency-medical-service fleets, but market acceptance depends on demonstrating equivalent safety and regulatory compliance.

Strategic moves highlight a shift from equipment sales to full-lifecycle support. Sechrist University expanded its virtual-reality curriculum, giving customers access to competency badges recognized by leading insurers. Perry Baromedical introduced a trade-in rebate that discounts new units when clients retire legacy chambers, locking in long-term service contracts. OxyRevo co-brands recovery suites with private hospitals in Malaysia and Indonesia to access self-pay sports and cosmetic-surgery segments. Competitive intensity therefore moves beyond price toward integrated ecosystems covering equipment, training, digital analytics and ongoing accreditation assistance, reinforcing the hyperbaric oxygen therapy market trajectory.

Hyperbaric Oxygen Therapy Industry Leaders

Environmental Tectonics Corporation

HAUX-LIFE-SUPPORT GmbH

Sechrist Industries Inc.

Perry Baromedical Corp.

- *Disclaimer: Major Players sorted in no particular order

Hyperbaric Oxygen Therapy Market Companies Covered in this Report

- Environmental Tectonics

- HAUX-LIFE-SUPPORT

- Sechrist Industries

- Perry Baromedical Corp.

- Fink Engineering

- Hearmec

- Hyperbaric SAC

- Hyperbaric Modular Systems Inc. (HMS)

- Pan America Hyperbarics Inc.

- OxyHeal Health Group

- IHC Hytech B.V.

- BioBarica

- BAROKS Hyperbaric

- AHA Hyperbarics

- Tekna Manufacturing

- Gulf Coast Hyperbarics

- Submarine Mfg & Products Ltd

- Eternalhealth Medical Equip.

- OxyVal Hyperbaric

- Hyperbaric Medical Solutions

Market Opportunities and Future Outlook

Coverage and reimbursement boundaries continue to shape near-term whitespace, especially where providers can standardize around reimbursable wound-care pathways while building evidence for emerging indications. In the United States, CMS Medicare Part B covers HBOT for defined conditions, including diabetic wounds of the lower extremities (Wagner grade III or higher) that have not responded to standard wound therapy, along with indications such as carbon monoxide poisoning, decompression illness, gas embolism, and gas gangrene. This supports a clear commercialization corridor for hospital wound centers and affiliated outpatient programs that can document eligibility and outcomes, which in turn supports purchases of additional monoplace capacity and associated digital monitoring upgrades.

Technology and safety compliance are converging into a procurement opportunity for vendors that bundle device clearance, facility-code alignment, and operational training into a single offering. The FDA focus on safe-use practices, alongside facility standards such as NFPA 99 and pressure-vessel requirements like ASME PVHO-1, increases the value of integrated systems designed to reduce operator error and improve traceability of treatment parameters. On the clinical-technology front, published research on AI-enabled decision support, registries, and digital-twin style simulations indicates an active roadmap for more patient-tailored dosing and protocol selection. This can help providers justify utilization, support quality reporting, and expand the addressable pool as evidence and payer policies broaden beyond the current indication set.

Recent Industry Developments in Hyperbaric Oxygen Therapy Market

- April 2026: Environmental Tectonics Corporation (ETC) announced the award of contracts totaling about USD 37 million across its Aerospace and Commercial/Industrial units, spanning simulation and sterilization systems alongside its hyperbaric-related capabilities. The scale of awards supports investment capacity in engineering, manufacturing, and lifecycle services that intersect with hospital and institutional hyperbaric infrastructure procurement.

- August 2025: HAUX-LIFE-SUPPORT GmbH completed installation and commissioning of a HAUX-STARMED-QUADRO pressure chamber system at Pasteur II Hospital in Nice, France. The project reflects continued investment in large, clinical-grade multi-chamber systems that can support both routine HBOT throughput and higher-acuity pressure medicine needs within hospital settings.

- December 2024: HAUX-LIFE-SUPPORT GmbH installed and commissioned a HAUX-QUADRO 2700-2200 pressure chamber at Ostrava City Hospital in the Czech Republic. Deliveries of modern, high-capacity systems reinforce replacement and modernization cycles in mature European hospital networks, shaping competitive positioning for vendors with turnkey installation and commissioning expertise.

Hyperbaric Oxygen Therapy Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the hyperbaric oxygen therapy market is defined as revenue generated from medically used hyperbaric chambers and related systems that deliver 100% oxygen at elevated pressure for therapeutic use in clinical settings, along with the associated installed-base driven upgrade and replacement demand.

Scope exclusions: Non-medical wellness pods, portable normobaric canisters, and recreational use cases are excluded from the market.

Segments Covered in This Report

- By Application

- Decompression Sickness

- Diabetic Foot Ulcers

- Gas Embolism

- Infection Treatment

- Wound Healing

- Other Applications

- By Product Type

- Monoplace HBOT Devices

- Multiplace HBOT Devices

- Topical / Portable HBOT Devices

- Hybrid Low-Pressure Chambers

- By End User

- Hospitals

- Ambulatory Surgical & Specialty Clinics

- Stand-alone Hyperbaric Treatment Centers

- Home-Care Settings

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by aligning the market definition to how hyperbaric therapy is regulated and procured, then mapping demand signals to the clinical conditions most commonly treated in practice. Public sources were used to ground initial assumptions, including hospital and outpatient activity indicators, along with safety and utilization norms for pressurized chambers.

We referenced non-paywalled sources such as the US FDA for device and safety context, the US CDC for decompression related public health references, the WHO for broader health burden framing, and clinical literature indexed in PubMed for indications and treatment patterns. Trade and shipment direction was cross-checked using national customs statistics and an import/export shipment-level database where relevant, and company filings and investor presentations were used to validate product focus and geographic exposure. This list is not exhaustive, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs came from interviews and short surveys with chamber manufacturers and their channel partners, hospital biomedical teams, wound care center operators, and clinicians who regularly prescribe therapy. Since this is a global market, we also ensured coverage across the major regions, so the model assumptions on utilization, pricing, and replacement cycles could be checked against real buying and operating behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 14% | APAC: 48% |

| Mid tier: 48% | Functional/Unit leaders: 39% | EMEA: 29% |

| Smaller Players: 14% | Managers: 47% | Americas: 23% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up logic together, but the main total is reconstructed top-down from the addressable care pool and how therapy is delivered in real settings. Where evidence was needed, selective bottom-up checks were run using sampled average selling prices and estimated unit volumes, along with channel feedback, and then totals were adjusted to keep them realistic.

Key inputs used in the model included the installed base of chambers by care setting, average sessions per chamber per day, typical treatment course length by major indication, replacement and refurbishment cycles, and pricing differences between monoplace and multiplace systems. Regional weighting was influenced by where hospital infrastructure is higher and where reimbursed wound care pathways are more established, then refined through interview feedback.

For forecasting, scenario analysis was used so that adoption and utilization could be flexed around practical constraints, such as staffing, facility certification, and capex budget cycles. In each region, smoothing was also applied to utilization and pricing series so one-time ordering spikes did not overstate the run-rate, which helped keep year-to-year movement understandable and repeatable.

Data Validation & Update Cycle

Outputs were validated through multiple checks, starting with comparing implied unit counts and utilization to what practitioners said was feasible, then reviewing whether the revenue split by region matched independent signals such as hospital investment cycles and trade direction. When a value looked off, the inputs behind it were traced back and re-tested, and follow-up calls were triggered when assumptions could not be supported consistently.

Before sign-off, the model and written insights go through step-by-step analyst reviews so that definitions, arithmetic, and logic stay consistent across chapters. Reports are refreshed annually, and interim updates are made when material events occur, such as reimbursement changes or major supply shifts. Right before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Hyperbaric Oxygen Therapy Market Size Compared Against Other Published Estimates

Market values for hyperbaric oxygen therapy can differ across publications because the counting boundary is not always the same, and because utilization and pricing assumptions are handled differently. The spread is usually explained by what is included (devices only versus broader therapy revenues), the base year used, and how the forecast path is shaped.

By tracking utilization per installed chamber, refreshing price progression by chamber type, and then stress-checking currency timing and regional weights, Mordor Intelligence keeps the estimate aligned to medical-grade chamber demand rather than adjacent wellness or loosely defined service revenues.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.88 B (2026) | |

| Global Consultancy A | USD 4.22 B (2026) | Often scoped as a narrower devices-only pool with limited upgrade and refurbishment capture, and the utilization assumptions can stay conservative across care settings, which compresses the implied demand base. |

| Industry Publisher B | USD 4.67 B (2026) | May blend equipment and service revenues unevenly across regions and apply a faster growth curve without fully reconciling installed-base capacity, reimbursement readiness, and feasible session throughput. |

The table shows that the main differences come from what is counted as market revenue and how the care capacity constraint is applied year by year. When utilization, replacement timing, and price mix are tied back to observable operating patterns, the resulting number is easier to explain and to re-create, which is what decision-makers usually need.

Key Questions Answered in the Report

What is the current value of the hyperbaric oxygen therapy market?

The market generated USD 7.88 billion in 2026 and is projected to reach USD 10.55 billion by 2031.

Which application segment is expanding the fastest?

Diabetic-foot-ulcer therapy is the quickest-growing application, advancing at an 8.52% CAGR through 2031.

Why are portable hyperbaric chambers becoming popular?

Advances in lightweight materials and digital monitoring make portable units suitable for outpatient clinics and even home care, widening access while meeting safety requirements.

How significant is Asia-Pacific to future growth?

Asia-Pacific is the fastest-growing region at a 7.32% CAGR, driven by government investments and competitive medical-tourism pricing.

What are the main barriers to wider adoption?

High capital and operating costs, plus a regulatory gap between FDA-approved and emerging off-label indications, remain the primary hurdles.

How is safety addressed after recent incidents?

Updated guidelines from the Undersea and Hyperbaric Medical Society emphasize accreditation, structured operator training and real-time chamber monitoring to prevent future accidents.

Page last updated on: