Hemostats Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

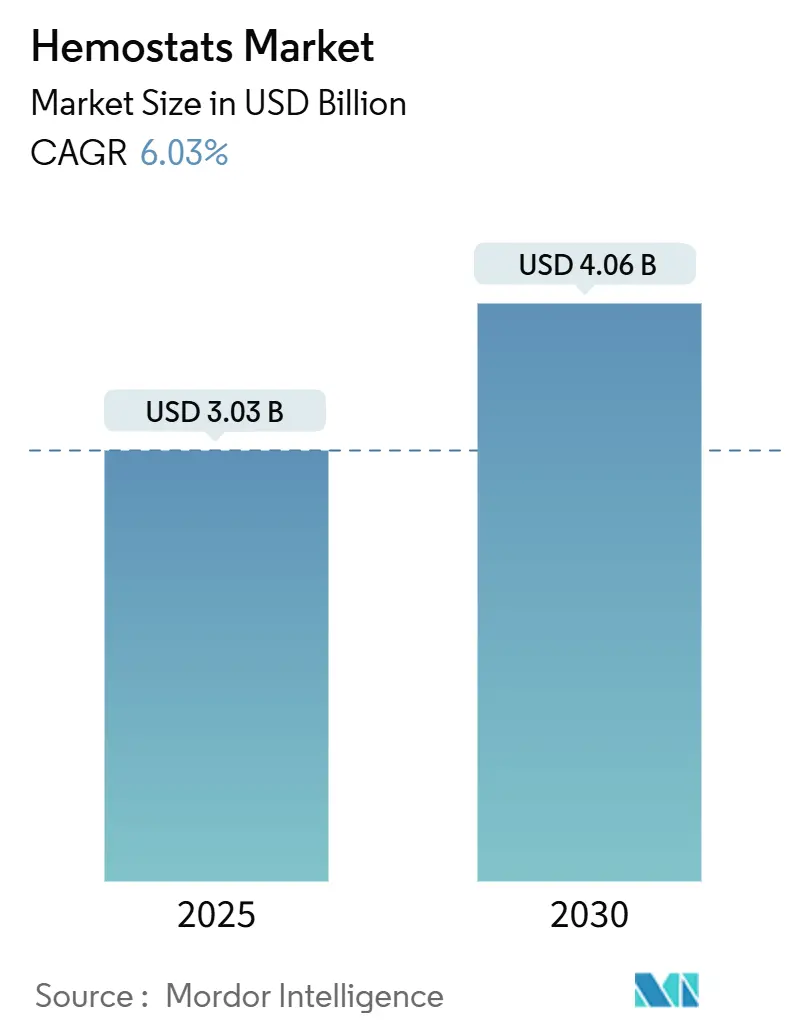

| Market Size (2025) | USD 3.03 Billion |

| Market Size (2030) | USD 4.06 Billion |

| Growth Rate (2025 - 2030) | 6.03% CAGR |

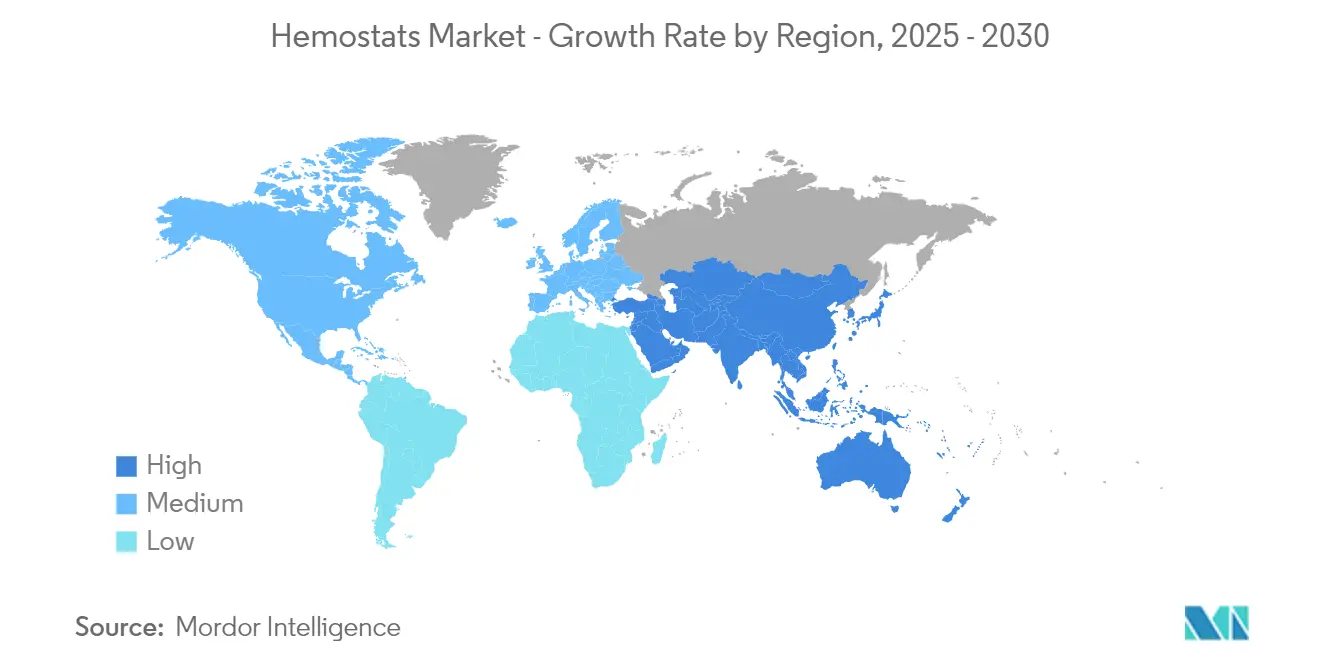

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hemostats Market Analysis by Mordor Intelligence

The Hemostats Market size is estimated at USD 3.03 billion in 2025, and is expected to reach USD 4.06 billion by 2030, at a CAGR of 6.03% during the forecast period (2025-2030).

The hemostats industry is experiencing significant transformation driven by broader healthcare infrastructure modernization and technological advancement. Healthcare facilities worldwide are increasingly investing in state-of-the-art surgical facilities and advanced medical technologies. An increase in surgical procedures creates a demand for innovative hemostats. For instance, in December 2024, the Australian Institute of Health and Welfare (AIHW) reported a 5% rise in public hospital elective surgery admissions, jumping to 771,600 in 2023-24 (excluding Northern Territory) from 735,500 in 2022-23. This increase in surgical procedures highlights a growing demand for medical consumables, including hemostats, which are critical in controlling bleeding during surgeries. The rising number of admissions directly correlates with the heightened need for such products, presenting significant growth opportunities for manufacturers and suppliers in the hemostat market.

The integration of digital health technologies and smart surgical solutions is reshaping traditional surgical practices, leading to improved patient outcomes and reduced recovery times. This evolution is particularly evident in developed regions where healthcare systems are actively adopting value-based care models and investing in cutting-edge surgical infrastructure.

The market is witnessing a notable shift toward innovative biomaterial technologies and next-generation hemostatic solutions. The emergence of biopolymer-based hemostats represents a significant advancement, offering improved biocompatibility and enhanced absorption characteristics. These materials are available in various forms including particles, powder, sponges, sheets, and hydrogels, providing surgeons with greater flexibility in addressing different surgical scenarios. For instance, as per the article published in April 2024 in the International Journal of Biological Macromolecules, the researchers showed that, wounds treated with sodium alginate experienced a limited blood loss compared to the control group. This underscores sodium alginate's inherent hemostatic activity, highlighting its potential to meet the growing demand for effective hemostatic materials in the market. Such advancements are critical as the demand for innovative wound care solutions continues to rise, driven by increasing surgical procedures and trauma cases globally.

A remarkable trend in the industry is the growing adoption of minimally invasive surgical techniques, particularly in aesthetic and reconstructive procedures. Surgeons in the United States conducted approximately 24.44 million cosmetic minimally invasive procedures in 2023, marking a 7% rise from 2022, as reported by the American Society of Plastic Surgeons. This increase in procedures reflects a growing demand for advanced surgical tools and materials, including hemostats, which are critical in ensuring precision and efficiency during such procedures. The rising adoption of minimally invasive techniques is expected to drive the demand for hemostats, as they play a vital role in controlling bleeding and enhancing patient outcomes. This shift has catalyzed the development of specialized hemostatic products designed specifically for minimally invasive applications, featuring improved precision and ease of application in confined surgical spaces.

The industry landscape is being reshaped by strategic collaborations and product innovations from key market players. For instance, Ethicon launched an ETHIZIA hemostatic sealing patch in November 2023, and Baxter introduced PERCLOT Absorbable Hemostatic Powder in July 2023. These innovations focus on dual-action hemostatic technology, combining mechanical hemostasis with biological clotting mechanisms. The trend toward ready-to-use formulations and preloaded applicators is gaining momentum, addressing the growing demand for efficient and user-friendly solutions in both hospital and ambulatory surgical settings.

Global Hemostats Market Trends and Insights

Increasing Volume of Surgical Procedures and Rising Healthcare Spending

The growing volume of surgical procedures worldwide represents a primary driver for the hemostats market. For instance, as per the German Heart Surgery Report 2023, heart surgical procedures totaled 100 thousand in 2023, marking an uptick from the 93,913 recorded in 2022 in Germany. This increase in surgical volumes directly correlates with a growing demand for hemostats, as these products play a critical role in managing bleeding during complex cardiovascular surgeries. The rising number of procedures underscores the expanding market opportunities for hemostat manufacturers to cater to the evolving needs of healthcare providers. This substantial surgical volume creates a consistent demand for effective hemostatic agents to control bleeding during procedures. The increasing complexity of surgical interventions, particularly in specialties like orthopedics, cardiovascular surgery, and general surgery, has heightened the need for advanced hemostatic solutions.

The healthcare sector has witnessed significant increases in spending, particularly in developing economies, which has enabled healthcare facilities to invest in advanced surgical technologies and hemostatic products. This increased healthcare expenditure has facilitated the adoption of premium hemostatic agents that offer superior bleeding control and reduced operative time. The rise in both elective and emergency surgical procedures, coupled with the growing number of ambulatory surgical centers, has created a robust demand for various hemostatic products. The American Society of Plastic Surgeons reported 1 million reconstructive surgeries in 2023, indicating the substantial volume of elective procedures that require effective hemostasis management.

Technological Innovation in Hemostatic Agents

The hemostats market is experiencing significant growth driven by continuous technological innovations in hemostatic agents and delivery systems. Recent developments have focused on creating more effective, biocompatible products that offer faster hemostasis and reduced complications. The emergence of biopolymer-based hemostats represents a major advancement, offering improved biocompatibility and absorption characteristics while maintaining effective bleeding control. These innovations have expanded the application scope of hemostatic agents across various surgical specialties and have enhanced their effectiveness in challenging surgical scenarios requiring precise bleeding management.

The development of dual-action hemostatic technology has revolutionized bleeding management in surgical procedures. These advanced products combine multiple mechanisms of action, such as mechanical barrier formation and coagulation cascade activation, to achieve more effective hemostasis. The integration of novel materials and delivery systems has resulted in products that offer improved handling characteristics and more precise application in difficult-to-reach surgical sites. Manufacturers are increasingly focusing on developing ready-to-use formulations and preloaded applicators that simplify product usage and reduce preparation time in critical situations, making these advanced hemostatic solutions more accessible and practical for surgical teams.

Hemostats Market Application Segment Analysis

Absorbable Hemostats Segment in Hemostats Market

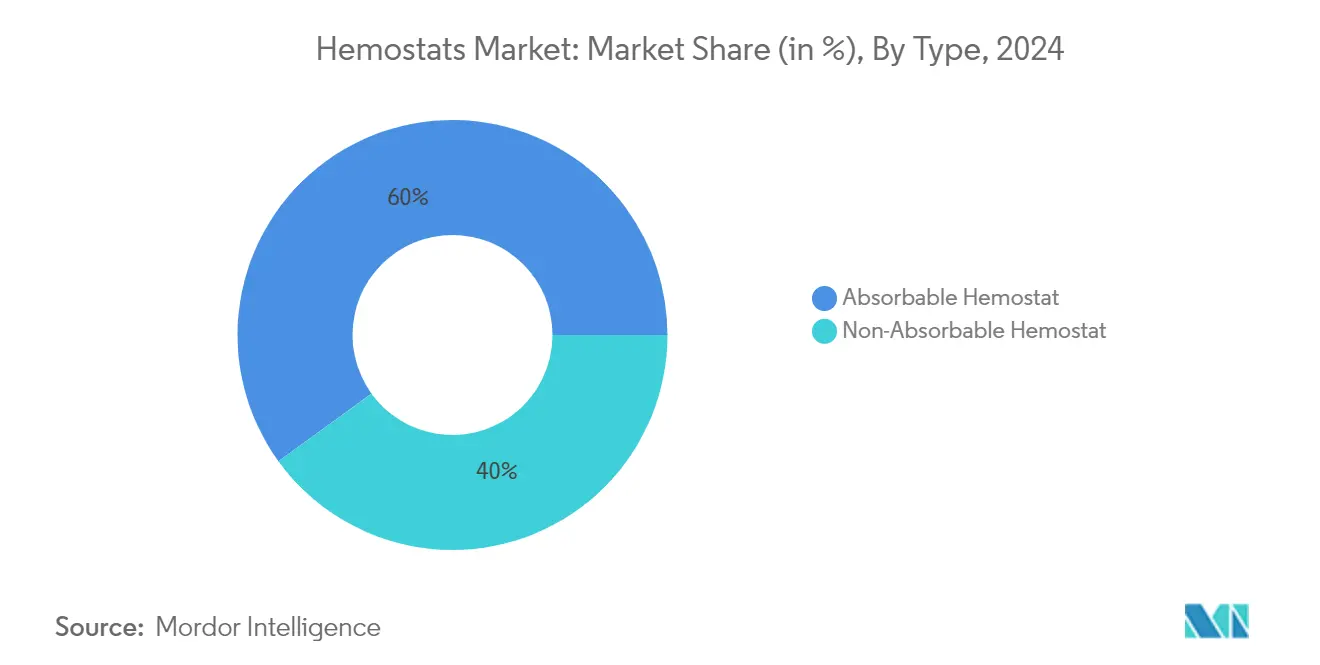

The absorbable hemostats segment maintains its dominant position in the global hemostats market, commanding approximately 60% of the market share in 2024. This substantial market presence is primarily driven by the increasing adoption of minimally invasive surgical procedures and the segment's superior biocompatibility characteristics. The segment's success is further reinforced by the widespread use of gelatin-based and collagen-based hemostats in various surgical applications, particularly in orthopedic and cardiovascular procedures. Healthcare providers consistently prefer absorbable hemostats due to their natural absorption properties, which eliminate the need for removal and reduce the risk of foreign body reactions. The segment's strong performance is also attributed to continuous product innovations, particularly in oxidized regenerated cellulose-based hemostats, which offer improved hemostatic efficacy and tissue compatibility. Recent regulatory approvals and the expansion of applications in emerging surgical fields have further consolidated the segment's market leadership.

Non-Absorbable Hemostats Segment in Hemostats Market

The non-absorbable hemostats segment is experiencing remarkable growth, emerging as the fastest-growing segment in the hemostats market. This accelerated growth is primarily fueled by technological advancements in fibrin sealants and synthetic sealants, which offer enhanced hemostatic properties and longer shelf life. The segment's rapid expansion is further supported by increasing demand in emergency care settings and trauma centers, where immediate and reliable hemostasis is crucial. Innovations in hemostatic gauze and forceps design have significantly improved their efficacy and ease of use, contributing to wider adoption among healthcare professionals. The development of next-generation synthetic sealants with improved adhesion properties and reduced immunogenic responses has opened new opportunities in various surgical applications. Additionally, the growing preference for these products in military medicine and pre-hospital care settings has created substantial growth opportunities for manufacturers.

Hemostats Market Formulation Segment Analysis

Matrix and Gel Segment in Hemostats Market

The matrix and gel segment maintains its dominant position in the global hemostats market. This leadership position is primarily attributed to the segment's superior versatility in various surgical applications and ease of use in both open and minimally invasive procedures. The segment's success is further bolstered by recent technological advancements in biopolymer-based formulations, which have significantly improved their hemostatic efficacy. Healthcare providers increasingly prefer matrix and gel formulations due to their precise application capabilities and reduced risk of displacement during surgical procedures. The segment's growth is also supported by the rising adoption of advanced surgical techniques and the increasing number of complex surgical procedures globally. Additionally, the segment benefits from continuous product innovations, including the development of dual-action formulations that combine hemostatic properties with antimicrobial features.

Powder Segment in Hemostats Market

The powder segment emerges as the fastest-growing category in the hemostats market, driven by the increasing adoption of minimally invasive surgical procedures and the segment's superior ability to reach difficult surgical sites. Powder formulations are gaining significant traction due to their enhanced surface coverage capabilities and rapid absorption properties, making them particularly effective in controlling diffuse bleeding. The segment's growth is further accelerated by ongoing innovations in powder delivery systems and the development of next-generation hemostatic agents. Recent technological advancements have led to the introduction of smart powder formulations that offer improved adhesion and faster hemostasis. The segment also benefits from the growing preference for powder-based hemostats in emergency medicine and trauma care, where quick application and effectiveness are crucial.

Hemostats Market Application Segment Analysis

Orthopedic Surgery Segment in Hemostats Market

The orthopedic surgery segment dominates the global hemostats market, primarily driven by the increasing volume of orthopedic surgical procedures, including Hip and knee replacements, shoulder replacements, surgeries, etc, among others. The segment's prominence is further reinforced by the growth in the adoption of minimally invasive surgical techniques, which require specialized hemostatic solutions. The aging global population and rising prevalence of orthopedic diseases necessitating surgical interventions have significantly contributed to this segment's dominance. Additionally, technological innovations in surgical hemostats, particularly in absorbable variants, have enhanced their efficacy and safety profile, making them indispensable in modern surgical settings. The segment's strong performance is also supported by the expanding healthcare infrastructure and increasing healthcare spending worldwide.

Trauma Management Segment in Hemostats Market

The trauma management injury segment is emerging as the fastest-growing segment in the hemostats market, primarily attributed to the rising incidence of trauma cases globally, including road accidents, sports injuries, and workplace accidents. The segment's rapid expansion is further fueled by increasing awareness about the critical importance of immediate hemorrhage control in trauma cases. Technological advancements in portable and easy-to-use hemostatic products specifically designed for emergency trauma care have significantly contributed to this growth. The segment is also benefiting from enhanced emergency response systems and the growing adoption of advanced hemostatic agents by first responders and emergency medical services. Moreover, the development of novel hemostatic formulations with improved efficacy and faster action times is expected to sustain this growth momentum throughout the forecast period.

Hemostats Market End User Segment Analysis

Hospitals & Clinics Segment in Hemostats Market

The hospitals & clinics segment dominated the global hemostats market in 2024. This substantial market presence is primarily attributed to the high volume of surgical procedures performed in hospital settings and their comprehensive emergency care capabilities. The segment's leadership position is further strengthened by hospitals' advanced infrastructure, which supports complex surgical interventions requiring sophisticated hemostatic agents. The presence of skilled healthcare professionals and the ability to handle both routine and emergency procedures contributes significantly to this segment's dominance. Additionally, hospitals' established procurement systems and bulk purchasing power enable them to maintain substantial inventories of various hemostatic products. The segment's growth is also supported by increasing healthcare spending and the rising adoption of advanced hemostatic technologies in hospital settings. Moreover, the growing number of hospital-based trauma centers and specialized surgical units continues to drive the demand for diverse hemostatic solutions.

Ambulatory Surgical Centers Segment in Hemostats Market

The ambulatory surgical centers (ASCs) segment is projected to exhibit the highest growth rate in the hemostats market, which is primarily driven by the increasing shift towards outpatient surgical procedures and the cost-effectiveness of ASC-based treatments. The segment's expansion is further fueled by technological advancements in minimally invasive surgical techniques, which align perfectly with the ASC care delivery model. Rising patient preference for same-day surgical procedures and shorter recovery times has significantly contributed to the segment's growth momentum. The adoption of advanced hemostatic agents in ASCs is also increasing due to their improved efficiency in managing surgical bleeding and reducing procedure times. Additionally, favorable reimbursement policies and the growing number of ASC facilities worldwide are creating substantial growth opportunities. The segment's growth is further supported by the increasing range of surgical procedures being approved for outpatient settings and the rising focus on reducing healthcare costs.

Hemostats Market Geography Segment Analysis

Hemostats Market in North America

North America represents the most established regional market for hemostats, characterized by advanced healthcare infrastructure, high surgical procedure volumes, and a strong presence of major market players. The region benefits from the widespread adoption of advanced hemostatic technologies, well-developed reimbursement frameworks, and an increasing focus on minimally invasive surgical procedures. Both the United States and Canada demonstrate robust demand for hemostatic products, driven by rising geriatric populations requiring surgical interventions and the growing prevalence of chronic conditions necessitating surgical treatments.

Hemostats Market in United States

The United States dominates the North American hemostats market, accounting a notable share in the regional market. The country's leadership position is attributed to its sophisticated healthcare system, extensive network of surgical centers, and high healthcare expenditure. The presence of leading manufacturers, continuous product innovations, and favorable regulatory environment further strengthen the market. The US market also benefits from increasing adoption of advanced hemostatic agents in specialized surgical procedures, growing demand for minimally invasive surgeries, and rising prevalence of cardiovascular and orthopedic conditions requiring surgical interventions.

Hemostats Market in Canada

Canada emerges as the fastest-growing market in North America, projected to grow at a notable pace. The growth is driven by increasing healthcare investments, rising surgical procedures, and growing adoption of advanced hemostatic technologies. Canadian healthcare facilities are increasingly incorporating innovative hemostatic products in various surgical specialties, particularly in cardiovascular and orthopedic procedures. The country's universal healthcare system, combined with growing emphasis on reducing surgical complications and improving patient outcomes, continues to drive market expansion.

Hemostats Market in Europe

Europe represents a significant market for hemostats, characterized by sophisticated healthcare systems, high surgical procedure volumes, and strong emphasis on medical innovation. The region encompasses diverse healthcare markets including Germany, France, UK, Italy, Spain, Switzerland, and Netherlands, each contributing uniquely to the overall market landscape. The European market benefits from well-established healthcare infrastructure, increasing adoption of advanced surgical technologies, and growing focus on reducing surgical complications through effective hemostatic management.

Hemostats Market in Germany

Germany stands as the largest hemostats market in Europe, commanding approximately 25% of the European market share in 2024. The country's market leadership is supported by its robust healthcare system, high surgical procedure volumes, and strong presence of medical device manufacturers. German healthcare facilities demonstrate high adoption rates of advanced hemostatic products, particularly in complex surgical procedures. The market is further strengthened by comprehensive healthcare coverage and significant investments in healthcare infrastructure.

Hemostats Market in France

France emerges as the fastest-growing market in Europe, with a notable growth rate. The French market demonstrates increasing adoption of innovative hemostatic solutions, particularly in minimally invasive surgeries. The country's healthcare system strongly emphasizes surgical excellence and patient safety, driving demand for advanced hemostatic products. Growing investments in healthcare infrastructure and rising surgical procedure volumes, particularly in cardiovascular and orthopedic specialties, contribute to market expansion.

Hemostats Market in Asia-Pacific

The Asia-Pacific region represents a rapidly evolving market for hemostats, characterized by improving healthcare infrastructure, increasing surgical procedure volumes, and growing adoption of advanced medical technologies. Countries including Japan, China, India, Australia, and South Korea are witnessing significant market development, driven by rising healthcare expenditure and growing awareness about advanced surgical solutions. The region demonstrates substantial potential for market expansion, supported by large patient populations and increasing access to surgical care.

Hemostats Market in China

China emerges as the largest hemostats market in Asia-Pacific, driven by its extensive healthcare system modernization initiatives and large patient population. The country's market leadership is supported by increasing investments in healthcare infrastructure, rising number of surgical procedures, and growing adoption of advanced medical technologies. Chinese healthcare facilities are increasingly incorporating sophisticated hemostatic solutions across various surgical specialties, particularly in urban centers.

Hemostats Market in India

India represents the fastest-growing market in the Asia-Pacific region, driven by rapidly expanding healthcare infrastructure and increasing access to surgical care. The country's market growth is supported by rising surgical procedure volumes, growing medical tourism, and increasing adoption of advanced surgical technologies. Indian healthcare providers are increasingly recognizing the importance of effective hemostatic management in improving surgical outcomes, particularly in tertiary care centers and specialized surgical facilities.

Hemostats Market in Middle East and Africa

The Middle East and Africa region shows promising growth in the hemostats market, with countries including South Africa, Saudi Arabia, UAE, and Kuwait driving market development. The region's market is characterized by rapid healthcare infrastructure development, increasing healthcare spending, and growing adoption of advanced surgical technologies. Saudi Arabia emerges as the largest market in the region, while the UAE demonstrates the fastest growth potential, supported by significant healthcare investments and growing medical tourism. The region's market expansion is further driven by improving access to surgical care and increasing awareness about advanced hemostatic solutions.

Hemostats Market in South America

South America demonstrates growing potential in the global hemostats market, with Brazil and Argentina emerging as key markets. The region's market development is driven by improving healthcare infrastructure, increasing surgical procedure volumes, and growing adoption of advanced medical technologies. Brazil emerges as the largest market in the region, while Argentina shows the fastest growth potential, supported by healthcare system modernization and increasing access to surgical care. The region's market expansion is further supported by rising healthcare expenditure and growing awareness about advanced surgical solutions.

Competitive Landscape

Top Companies in Hemostats Market

The global hemostats market is led by prominent players, including Aegis Lifesciences, Artivion, Inc, B Braun SE, Baxter International, Becton, Dickinson and Company, Integra LifeSciences Corporation, Johnson & Johnson, Medtronic, Pfizer Inc.and Terumo Corporation. These companies demonstrate a consistent focus on product innovation through the development of next-generation hemostatic agents incorporating advanced biomaterials and dual-action technologies. Operational agility is evidenced through flexible manufacturing capabilities and robust supply chain networks ensuring product availability across regions. Strategic initiatives commonly pursued include licensing agreements for novel technologies, distribution partnerships to enhance market reach, and investments in R&D facilities. Geographic expansion, particularly in emerging markets, remains a key priority with companies establishing local manufacturing units and strengthening distribution networks while also pursuing strategic acquisitions to gain quick market access.

Consolidated Market Led By Global Players

The hemostats market exhibits moderate to high consolidation with the top 5-6 global players accounting for nearly half of the market share. These dominant players are largely diversified medical device and pharmaceutical conglomerates with extensive product portfolios spanning multiple therapeutic areas. Their competitive advantage stems from established brand equity, extensive distribution networks, and significant R&D capabilities. Regional and local players typically focus on specific product segments or geographic markets, competing through cost leadership and local market knowledge.

The market has witnessed steady M&A activity aimed at portfolio expansion and geographic penetration. Large companies actively pursue acquisitions of innovative startups and regional players to access novel technologies and establish presence in high-growth markets. Strategic partnerships and licensing agreements are common, particularly for accessing proprietary technologies or establishing manufacturing and distribution capabilities in new markets. The trend towards consolidation is expected to continue as companies seek economies of scale and expanded market presence.

Innovation and Market Access Drive Success

For established players, maintaining market leadership requires continuous investment in product innovation, particularly in advanced biomaterials and combination products. Success factors include developing cost-effective manufacturing processes, building strong relationships with healthcare providers, and expanding presence in emerging markets. Companies must also focus on clinical evidence generation to demonstrate product efficacy and safety, while maintaining compliance with evolving regulatory requirements. Strategic partnerships with research institutions and technology companies can accelerate innovation and market access.

New entrants and smaller players can gain market share by focusing on underserved market segments or geographic regions, developing specialized products for specific surgical applications, and establishing strong distribution partnerships. Success requires understanding local market dynamics, regulatory requirements, and healthcare delivery systems. Companies must also consider the increasing influence of healthcare providers and payers in product selection, while addressing potential substitution risks from alternative hemostatic technologies. Building relationships with key opinion leaders and healthcare institutions remains crucial for market penetration and growth.

Hemostats Industry Leaders

B Braun SE

Baxter International

Becton, Dickinson and Company

Integra LifeSciences Corporation

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Cresilon Inc., unveiled TRAUMAGEL, a groundbreaking plant-derived hemostatic gel, in the United States market. This innovative gel swiftly halts bleeding upon application to a wound, making it a game-changer for point-of-care treatments.

- September 2024: Medcura, Inc., a prominent leader in the development of advanced hemostasis solutions leveraging patented biopolymer technologies to effectively manage surgical bleeding, was honored with the prestigious 2024/2025 Best Technology in Spine Award for its innovative product, LifeGel Absorbable Hemostatic Gel. This recognition underscores the company's commitment to delivering cutting-edge solutions that address critical needs in the surgical and medical fields.

- April 2024: LifeScience PLUS unveiled its latest innovation, DonorSeal at the 56th Annual American Burn Association (ABA) Meeting in Chicago. This 100% natural, plant-based cellulose matrix is specifically engineered to address the critical needs of donor site treatment. DonorSeal delivers significant value by enabling rapid hemorrhage control, effectively reducing blood loss, and accelerating wound healing. This breakthrough product underscores the company's commitment to advancing medical solutions and addressing key challenges in wound care management.

- March 2023: Axio Biosolutions received FDA clearance under the 510(k) regulatory pathway for its Ax-Surgi Surgical Hemostat, an innovative chitosan-based hemostatic product engineered for managing severe bleeding during surgical procedures.

Global Hemostats Market Report Scope

As per the scope of the report, hemostats are essential surgical tools widely utilized to control bleeding during medical procedures. With a design that combines features of pliers and scissors, these instruments are specifically engineered to clamp exposed blood vessels effectively. Hemostats are part of a broader category of pivoting instruments, where the structural design of the tip determines their precise functionality, making them indispensable in achieving surgical precision and efficiency.

Hemostats market is segmented by type, formulation, application, end user, and geography. By type, the market is segmented into absorbable and non-absorbable hemostats. By absorbable hemostat the market is segmented into gelatin-based hemostats, collagen-based hemostats, oxidized regenerated cellulose-based hemostats and other absorbable agents. By nonabsorbable hemostat, the market is segmented into fibrin sealants, synthetic sealants, hemostatic gauze and hemostatic forceps. By formulation, the market is segmented into matrix and gel, sheets and pads, sponges, powders and others. By application, the market is segmented into orthopedic surgery, general surgery, cardiovascular surgery, gynecological surgery, dental treatments. trauma management and other applications. By end user, the market is segmented into hospitals & clinics, ambulatory surgical centers, nursing homes and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (in USD) for the above segments.

| Absorbable Hemostats | Gelatin-based Hemostats |

| Collagen-based Hemostats | |

| Oxidized Regenerated Cellulose-based Hemostats | |

| Other Absorbable Agents | |

| Non-Absorbable Hemostats | Fibrin Sealants |

| Synthetic Sealants | |

| Hemostatic Gauze | |

| Hemostatic Forceps |

| Matrix and Gel |

| Sheets and Pads |

| Sponges |

| Powders |

| Others |

| Orthopedic Surgery |

| General Surgery |

| Cardiovascular Surgery |

| Gynecological Surgery |

| Dental Treatments |

| Trauma Management |

| Other Applications |

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Nursing Homes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Absorbable Hemostats | Gelatin-based Hemostats |

| Collagen-based Hemostats | ||

| Oxidized Regenerated Cellulose-based Hemostats | ||

| Other Absorbable Agents | ||

| Non-Absorbable Hemostats | Fibrin Sealants | |

| Synthetic Sealants | ||

| Hemostatic Gauze | ||

| Hemostatic Forceps | ||

| By Formulation | Matrix and Gel | |

| Sheets and Pads | ||

| Sponges | ||

| Powders | ||

| Others | ||

| By Application | Orthopedic Surgery | |

| General Surgery | ||

| Cardiovascular Surgery | ||

| Gynecological Surgery | ||

| Dental Treatments | ||

| Trauma Management | ||

| Other Applications | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Nursing Homes | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Hemostats Market?

The Hemostats Market size is expected to reach USD 3.03 billion in 2025 and grow at a CAGR of 6.03% to reach USD 4.06 billion by 2030.

What is the current Hemostats Market size?

In 2025, the Hemostats Market size is expected to reach USD 3.03 billion.

Which is the fastest growing region in Hemostats Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Hemostats Market?

In 2025, the North America accounts for the largest market share in Hemostats Market.

What years does this Hemostats Market cover, and what was the market size in 2024?

In 2024, the Hemostats Market size was estimated at USD 2.85 billion. The report covers the Hemostats Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Hemostats Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: