Oxygenators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

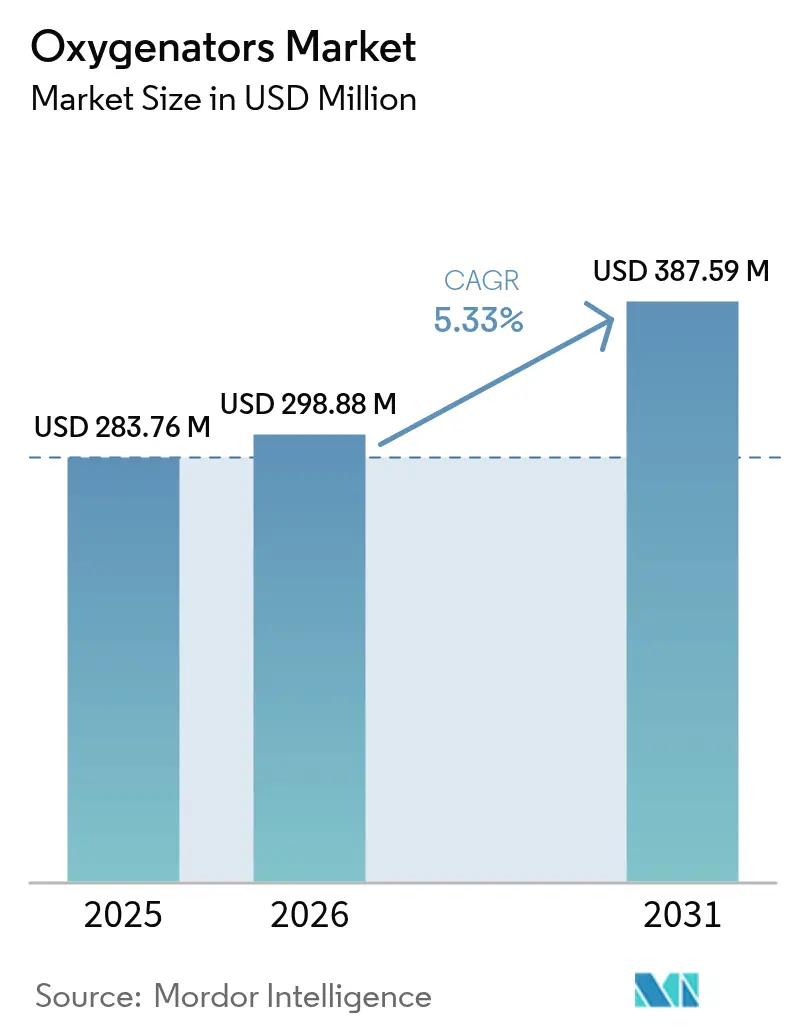

| Market Size (2026) | USD 298.88 Million |

| Market Size (2031) | USD 387.59 Million |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

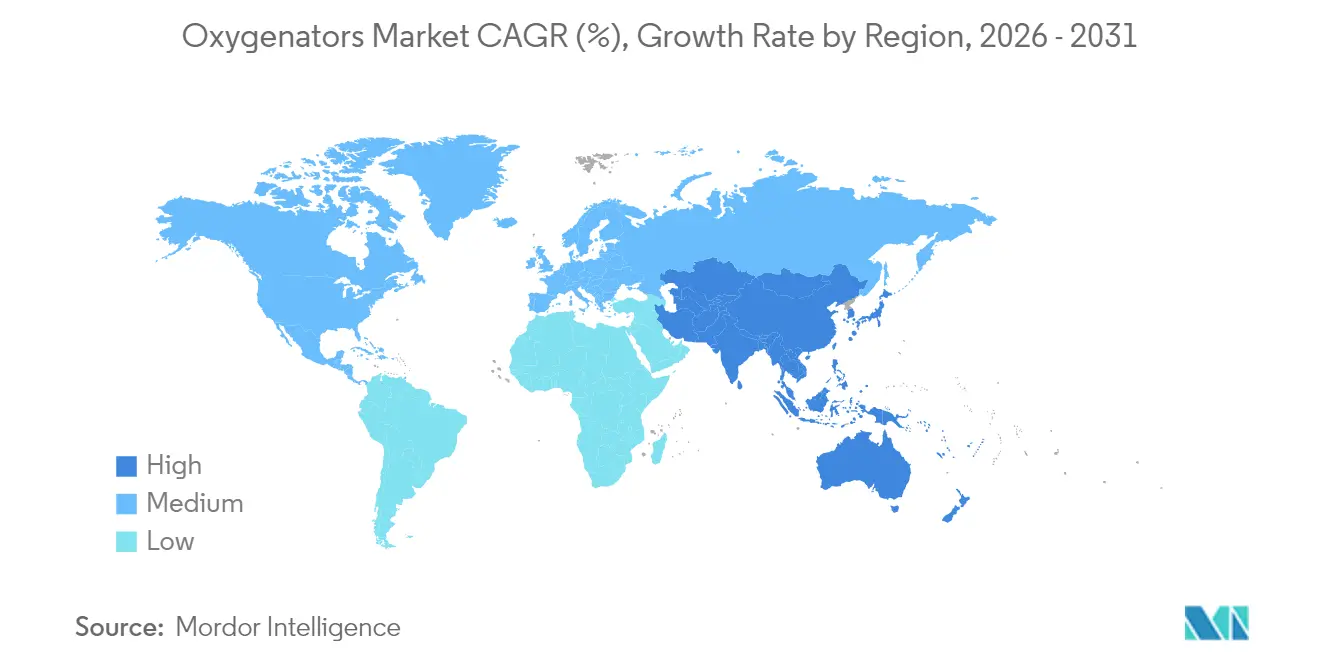

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

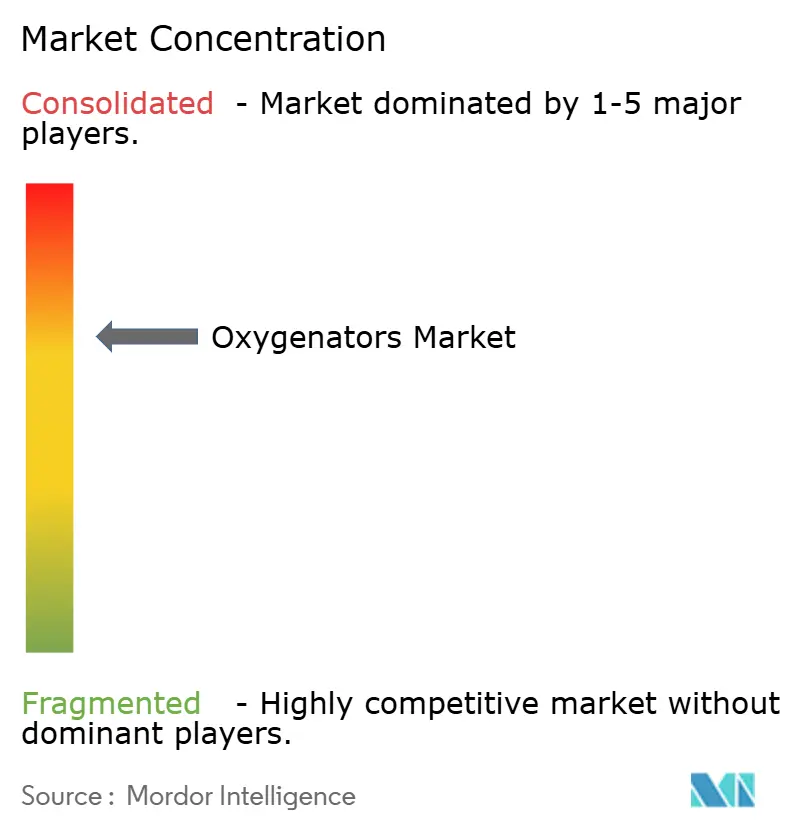

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oxygenators Market Analysis by Mordor Intelligence

The oxygenators market size is expected to grow from USD 283.76 million in 2025 to USD 298.88 million in 2026 and is forecast to reach USD 387.59 million by 2031 at 5.33% CAGR over 2026-2031. This controlled advance conceals brisk shifts in product preference, care-delivery settings, and regional demand. Portable extracorporeal membrane oxygenation (ECMO) platforms compatible with membrane oxygenators are expanding procedure volumes outside the operating room. At the same time, aging populations require longer-duration extracorporeal support amid a rising cardiopulmonary disease burden. Device makers are bundling AI-enabled monitoring software with disposables to lock in service revenue and differentiate themselves on outcomes rather than relying solely on hardware. Meanwhile, policy changes in the United States, Europe, and China are broadening reimbursement for pre-hospital initiation and hybrid interventional-surgical protocols, creating new replacement cycles for legacy bubble systems. Supply-chain volatility for polymethylpentene (PMP) hollow fibers remains the principal cost threat; yet, the scale advantages enjoyed by Chinese manufacturers are compressing price dispersion, forcing incumbents to defend their premium positioning with biocompatibility upgrades and longer, validated use-life. Overall, the oxygenators market is poised to reward companies that combine material science innovation, software analytics, and training ecosystems to ease perfusionist bottlenecks.

Key Report Takeaways

- By product type, bubble oxygenators led the oxygenators market share with 60.78% of 2025 revenue, whereas membrane variants are projected to grow at a 7.32% CAGR through 2031.

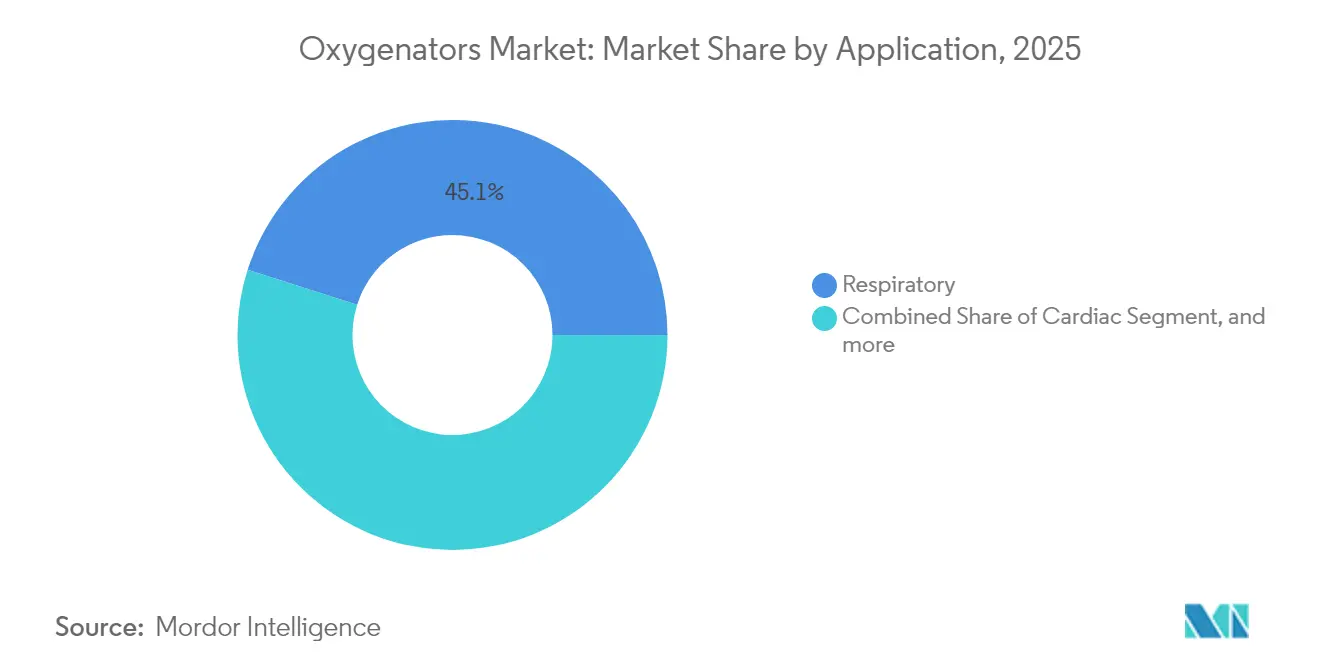

- By application, respiratory support accounted for a 45.10% slice of the oxygenators market size in 2025, while cardiac use cases are advancing at a 7.61% CAGR through 2031.

- By geography, North America accounted for a 42.35% slice of the oxygenators market size in 2025, while Asia-Pacific is projected to grow at a CAGR of 6.41% over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oxygenators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in global prevalence of cardiopulmonary disorders | +1.8% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Increasing geriatric population | +1.5% | Japan, Germany, Italy, coastal China | Long term (≥ 4 years) |

| Availability of technologically advanced oxygenators and reimbursement policies | +1.0% | United States, Germany, United Kingdom, China | Medium term (2-4 years) |

| Adoption of portable ECMO systems in pre-hospital emergency transport | +1.2% | North America, Western Europe, GCC, Australia | Medium term (2-4 years) |

| AI-enabled real-time monitoring reducing complication rates | +0.9% | North America, select European centers, South Korea, Japan | Medium term (2-4 years) |

| Expansion of low-cost manufacturing capacity in emerging markets | +0.7% | China, India, Southeast Asia, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Global Prevalence of Cardiopulmonary Disorders

Cardiovascular disease claimed 19.8 million lives in 2022, and chronic obstructive pulmonary disease (COPD) affects 391.9 million people, driving sustained demand for veno-venous ECMO circuits[1]World Health Organization, “The Top 10 Causes of Death,” who.int. Acute respiratory distress syndrome accounts for 10% of intensive-care admissions and 23% of mechanically ventilated patients, making oxygenators a frontline consumable. Heart-failure prevalence now tops 64.3 million worldwide, and decompensated cases are increasingly bridged with ECMO while definitive interventions are arranged. Hospitals that built ECMO capacity during the COVID-19 surge have repurposed infrastructure for non-viral ARDS and cardiogenic shock, keeping utilization above pre-pandemic baselines. Together, these epidemiologic pressures are broadening the candidate pool across elective, urgent, and emergent pathways, anchoring a resilient growth spine for the oxygenators market.

Increasing Geriatric Population

The global population aged 65 and older will climb from 771 million in 2022 to 994 million by 2030, with the steepest gains in East Asia and Southern Europe[2]United Nations Department of Economic and Social Affairs, “World Population Prospects 2022,” un.org. Octogenarians are now routinely offered complex cardiac surgery, supported by updated Japanese Circulation Society guidelines endorsing ECMO in elderly cardiogenic-shock patients. Older patients present compounded pulmonary dysfunction, necessitating oxygenators with higher gas-exchange efficiencies and anti-inflammatory surface coatings to mitigate prolonged bypass. Because absolute procedure counts track demographic expansion, geriatric demand introduces a multi-decade structural tailwind that outweighs cyclical swings in elective surgery.

Adoption of Portable ECMO Systems in Pre-Hospital Emergency Transport

MicroPort’s 2-kg MOBYBOX and Getinge’s Cardiohelp allow cannulation at the scene of cardiac arrest, shortening low-flow time and elevating neurologically intact survival above 40% in early case series. The Centers for Medicare & Medicaid Services began reimbursing pre-hospital ECMO in March 2025, removing a payment barricade that had constrained adoption in the United States[3]Centers for Medicare & Medicaid Services, “Medicare Advantage Pre-Hospital ECMO Coverage Decision Memo,” cms.gov. Air-ambulance fleets in Western Europe and Australia are following suit, positioning portable oxygenators as essential trauma inventory. As EMS crews master standardized algorithms, pre-hospital penetration is expected to spread to metropolitan fire departments by 2027, giving the oxygenators market another high-margin niche.

AI-Enabled Real-Time Monitoring Reducing Complication Rates

Machine-learning models such as ECMO PAL now flag thrombotic or hemorrhagic events 4–6 hours before clinical manifestation, cutting major-bleed episodes by 20% in validation studies. Continuous analytics incorporating pump flow, membrane pressure gradient, and plasma-free hemoglobin feed audible alerts that let perfusionists fine-tune anticoagulation or schedule oxygenator change-outs proactively. Manufacturers bundling these predictive licenses with disposables gain recurring revenue and stickier account relationships, nudging the oxygenators market toward a hardware-plus-software model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of minimally invasive cardiac procedures reducing CPB usage | -1.3% | North America, Western Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Stringent regulatory and biocompatibility compliance requirements | -1.0% | Global | Long term (≥ 4 years) |

| Acute perfusionist workforce shortage limiting ECMO program expansion | -0.8% | North America, Australia, United Kingdom, Netherlands | Medium term (2-4 years) |

| Raw-material supply-chain volatility for medical-grade polymers | -0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adoption of Minimally Invasive Cardiac Procedures Reducing CPB Usage

Global transcatheter aortic valve replacement (TAVR) volumes reached 332,000 in 2023 and are projected to climb 15% annually, eliminating the need for cardiopulmonary bypass (CPB) circuits and disposable oxygenators in converted cases. Transcatheter mitral solutions are following a similar trajectory, further squeezing surgical case counts. Although manufacturers are pivoting toward ECMO and extracorporeal life support applications, volumes are asymmetric—one high-volume cardiac center can forfeit hundreds of CPB circuits each year, while adding only dozens of ECMO runs. Until ECMO usage expands beyond critical-care salvage, minimally invasive cardiology will limit overall oxygenator market growth.

Acute Perfusionist Workforce Shortage Limiting ECMO Program Expansion

Approximately 5,000 certified perfusionists serve the entire United States, and burnout-driven attrition following the COVID-19 surge has hindered the launch of new programs in community hospitals. Training pipelines remain congested, and accrediting bodies require 24/7 coverage, creating a staffing gate that is either all or nothing. Tele-perfusion pilots offer remote oversight but face uneven regulatory acceptance and liability ambiguity. The shortfall most directly caps ECMO growth, but ripple effects spill into CPB scheduling, forcing hospitals to cancel elective cases when vacancies arise. This talent bottleneck limits the oxygenators market below its theoretical ceiling, despite robust demand for devices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Membrane Variants Gain on Biocompatibility Edge

Bubble oxygenators contributed 60.78% of 2025 revenue, solidifying their position in the oxygenators market due to their low upfront cost and simple priming. Membrane designs, however, are advancing at a 7.32% CAGR through 2031, double the pace of bubble counterparts, and are forecast to widen their position in the overall oxygenators market size by mid-decade. Hollow-fiber polymethylpentene (PMP) membranes slash hemolysis and platelet activation during ECMO runs exceeding 14 days, a decisive benefit in prolonged cardiogenic-shock support. Integrated heat exchangers and arterial filters, as seen in Getinge’s PLS line, shorten circuit assembly time and reduce contamination risk. Updated ISO 7199 protocols emphasize long-term thrombogenicity benchmarks that bubble units struggle to meet, accelerating regulatory tilt toward membranes. Bubble devices will persist in short procedures and pediatric repairs where cost sensitivity eclipses biocompatibility demands, but rising quality thresholds will keep incremental value flowing to membranes within the oxygenators market.

Extracorporeal cardiopulmonary resuscitation (ECPR) has emerged as a distinct product niche that prioritizes rapid deployment kits marrying membrane oxygenators, centrifugal pumps, and cannulae in sealed sterile packs. The Extracorporeal Life Support Organization reports 29.5% survival in adult ECPR, rising above 40% when cannulation occurs inside 60 minutes of arrest. This application commands premium disposable pricing and is spurring introduction of single-use circuits that aim to eliminate infection risk, though payers remain cautious. As reimbursement clarity improves, ECPR will add incremental lift to the oxygenators market share for membrane systems, even as bubble designs retreat into legacy cardiac-surgery indications.

By Application: Cardiac Segment Accelerates on Interventional Synergies

Respiratory support captured 45.10% of 2025 revenue, sustaining the oxygenators market size through veno-venous ECMO for ARDS and bridge-to-transplant. Cardiac indications, however, are expanding at a 7.61% CAGR to 2031 as interventional cardiologists combine veno-arterial ECMO with percutaneous ventricular assist devices to unload the left ventricle during acute myocardial infarction. The September 2025 EACTS/STS/AATS joint guidelines formally endorsed the “ECPELLA” strategy, unlocking reimbursement across 27 EU states. Shorter support times—median 3-5 days—cut ICU and consumable costs, enabling more institutions to adopt ECMO without dedicated long-term resources. This synergy positions cardiac use as the fastest-growing slice of the oxygenators market, even if volume trails the larger respiratory cohort.

ECPR, while the smallest application by case count, yields the highest per-run revenue and sits at the intersection of EMS, emergency medicine, and critical-care markets. NICE is scheduled to publish guidance on veno-arterial ECMO for ECPR in October 2025, likely green-lighting National Health Service coverage and cascading into broader European adoption. Conversely, respiratory growth faces a tempered outlook as advances in prone positioning and protective ventilation reduce progression to ECMO candidacy. Consequently, cardiac and ECPR applications will represent disproportionate incremental gains in oxygenators market share through the decade, even if respiratory support retains the largest absolute spend.

Geography Analysis

North America generated 42.35% of 2025 revenue and is forecast to advance at 4.72% annually to 2031, sustained by Medicare reimbursement for pre-hospital ECMO and concentrated trauma-center networks. Twelve metropolitan fire departments now field Cardiohelp systems under public-private partnerships, widening the oxygenators market footprint beyond tertiary hospitals. Regional imbalances linger—coastal academic centers often carry excess perfusion capacity while rural facilities struggle to recruit staff, shaping uneven access but steady aggregate demand. Stringent FDA 510(k) requirements deter many Asian entrants, preserving premium pricing for established U.S. suppliers and reinforcing the region’s status as the most profitable slice of the oxygenators market.

Asia-Pacific is the fastest-growing geography at 6.41% CAGR through 2031, powered by China’s surge from 2,826 ECMO cases in 2017 to 10,656 in 2021. The National Medical Products Administration cleared Hengrui’s maglev-pump platform in January 2025, the second domestic system to reach market, priced 35% below Western comparators. Local price competition is compressing margins for multinationals, prompting joint ventures and localized manufacturing. Japan shows high per-capita ECMO utilization but slower unit growth due to flat demographics and spending caps, while India’s nascent network of 16 centers logged survival rates above 40%, signaling clinical competence but still modest oxygenators market size.

Europe accounted for roughly 27.85% of 2025 sales, with Germany, the United Kingdom, and France leading installed base and innovation. The European Health Insurance Card now reimburses cross-border ECMO transfers, and Germany’s InEK NUB funding supports novel technology premiums for three years post-launch. Workforce constraints mirror North America—United Kingdom perfusionist shortages have forced triage protocols prioritizing younger, reversible cases. Pending NICE guidance on ECPR and VA-ECMO for heart failure is expected to unlock National Health Service coverage, spreading demand to secondary hospitals and giving oxygenators market vendors fresh tender opportunities by late 2026.

Regulatory Landscape

Oxygenators used in CPB and ECMO circuits are blood-contacting cardiovascular devices and are subject to biocompatibility and performance verification requirements. In the United States, the FDA regulates CPB oxygenators under 21 CFR 870.4350, typically via the 510(k) pathway, where predicate-based substantial equivalence supports market entry; Lifemotion Disposable Membrane Oxygenator received FDA 510(k) clearance (K253838) on 16 March 2026.

In Europe, oxygenators fall under MDR (Regulation (EU) 2017/745), with clinical evidence expectations and post-market surveillance shaping timing and lifecycle costs. The Clinical Evaluation Consultation Procedure (CECP) introduces independent expert-panel scrutiny for high-risk devices, while mandatory use of four EUDAMED modules became effective on 28 May 2026. Commission Delegated Regulation (EU) 2026/1451 (dated 20 March 2026) further clarifies device lists and clinical investigation obligations under MDR Article 61.

Value Chain Analysis

The oxygenator value chain starts with medical-grade polymers and other blood-contact materials, notably polymethylpentene (PMP) hollow fibers. Precision manufacturing follows, including fiber spinning, membrane bundle assembly, heat-exchanger integration, and sterile packaging under tightly controlled quality systems. Because oxygenators are consumables embedded in CPB and ECLS workflows, manufacturers often pair disposables with compatible consoles, sensors, and software, and then support adoption through clinical education and service agreements to reduce perfusion workflow friction.

Midstream and downstream, distribution typically relies on direct sales to large hospitals and group purchasing structures in mature markets, while national distributors handle tenders and public procurement in other regions. Supply continuity has become a more prominent procurement criterion as device makers and regulators emphasize medical device supply-chain vulnerabilities. As a result, buyers increasingly consolidate suppliers, diversify sourcing, and hold additional safety stock rather than relying on just-in-time models. In Europe, the January 2025 shortage-reporting mandate for medical devices reinforces early-warning expectations across the chain, and FDA discussions around expanding shortage reporting beyond emergencies increase documentation and risk-management demands that flow down to critical component suppliers.

Competitive Landscape

Getinge, LivaNova, Medtronic, and Terumo together control an estimated 60-65% of revenue, giving the oxygenators market a moderate concentration profile. Incumbents are layering value through proprietary surface coatings, integrated heat exchangers, and AI analytics to stave off price erosion. LivaNova’s 2024 buyout of Caisson Interventional unlocked bundled selling to hybrid cath-lab theaters, melding transcatheter valve repairs with ECMO back-up in a single capital package. Getinge continues to miniaturize its Cardiohelp line, while Terumo has lengthened validated oxygenator run times to 30 days, appealing to centers deploying ECMO as bridge-to-decision support.

Chinese challengers Chinabridge and Hengrui have secured NMPA clearances and are fast-tracking CE Mark applications, leveraging 30-40% list-price discounts and insourcing of PMP fibers to erode Western gross margins. MicroPort’s 2024 acquisition of Hemovent positions the MOBYBOX platform as the lightest portable ECMO on the market, targeting air-ambulance and military medevac users. Emerging disruptors employ maglev pumps that eliminate bearings, slashing hemolysis and permitting oxygenator change-out intervals beyond 30 days, a key metric for bridge-to-transplant candidates.

Regulatory rigors under ISO 7199 and ISO 10993 create high fixed costs for biocompatibility testing, but also serve as validation currency for Chinese systems seeking Western entry. The NMPA’s March 2025 clinical-evaluation guidance, requiring 30-patient samples and stringent bench gas-exchange tests, effectively screens out under-resourced startups, leaving scaled domestic suppliers as credible export contenders. As performance parity converges, competition will hinge on bundled analytics, perfusionist training support, and service contracts rather than standalone hardware, nudging the oxygenators market toward a solution-selling model.

Oxygenators Industry Leaders

Getinge AB

Livanova Plc

Medtronic

Terumo Medical Corporation

EUROSETS SRL

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is growing around connected ECLS ecosystems that pair membrane oxygenators with portable consoles, monitoring, and decision support, particularly as ECMO programs expand outside the operating room into emergency transport and broader critical-care pathways. The most tangible commercial proof points are regulatory milestones for next-generation platforms and disposables, including Getinge receiving a CE mark for Cardiohelp II in March 2026 with added monitoring and integrated functionality, and Lifemotion Medical Technology receiving FDA 510(k) clearance (K253838) in March 2026 for a disposable membrane oxygenator. Together, these approvals support differentiation through integrated features rather than disposable pricing alone.

Localization of complex cardiopulmonary device production is another opportunity area, since it can reduce import dependence and improve supply resilience while shifting the competitive set available to hospitals and tendering bodies. Mediyant Technologies securing USFDA 510(k) clearance and a CDSCO Class C license in July 2026 for an Indian-manufactured heart-lung machine illustrates that regulatory maturity for locally produced systems is advancing, and these systems can be paired with oxygenator consumables. On the technology side, published work on hemocompatible surface coatings and design optimization using computational fluid dynamics and reduced-order models aligns with the market emphasis on longer validated run times and fewer change-outs, targeting thrombosis and hemolysis constraints that drive clinical and economic adoption decisions.

Recent Industry Developments

- March 2026: Lifemotion Medical Technology received FDA 510(k) clearance (K253838) for a disposable membrane oxygenator, expanding access to U.S. hospital systems for CPB and ECMO disposables. The clearance signals a ramp in U.S. market presence for disposables and could influence competitive dynamics in CPB and ECMO programs.

- June 2025: Medtronic secured CE Mark for the VitalFlow ECMO system in Europe, leveraging technology from its MC3 Cardiopulmonary business. The clearance strengthens Medtronic's ability to offer an integrated ECMO platform proposition to European critical-care centers where device standardization and bundled procurement influence oxygenator pull-through.

- April 2024: Getinge announced it would acquire Paragonix Technologies, broadening its footprint in adjacent cardiothoracic and transplant-support workflows. The portfolio expansion supports broader solution selling to hospitals that run high-acuity programs, complementing Getinge offerings around perfusion and extracorporeal support.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers oxygenators used in extracorporeal circulation, where blood is oxygenated outside the body during cardiac, respiratory support, and emergency resuscitation use cases. The market sizing reflects revenues from oxygenator devices across the covered regions in the study period.

Scope exclusions: We exclude general hospital oxygen supply equipment and respiratory oxygen therapy devices that do not perform extracorporeal blood oxygenation.

Segmentation Overview

- By Product Type

- Bubble Oxygenator

- Membrane Oxygenator

- By Application

- Respiratory

- Cardiac

- Extracorporeal Cardiopulmonary Resuscitation (ECPR)

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with mapping the demand and procedure context that oxygenators depend on, then narrowing it to the extracorporeal setting. For procedure and care-access context, we use public sources such as the US FDA device and safety information, the US CDC health statistics, OECD health data, and WHO health system indicators, to estimate procedure volumes and care access patterns.

On the supply side, we review company annual reports, investor presentations, product brochures, and reputable press to understand product positioning and likely price bands. When useful, patent databases are used to confirm technology direction, for example membrane materials and monitoring integration. We also use an import and export shipment level database to sanity check cross-border supply flows in key hubs. These examples are not exhaustive, and we review additional public and paid sources to support data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to validate the real purchase unit (per device, per procedure pack, or tender lot), typical replacement cycles, and how pricing differs between cardiac and respiratory use. We also interviewed stakeholders across manufacturers, distributors, perfusion and ECMO user settings, and procurement roles across APAC, EMEA, and the Americas, so assumptions could be adjusted where local practice patterns differ.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 17% | APAC: 48% |

| Mid tier: 46% | Functional/Unit leaders: 32% | EMEA: 34% |

| Smaller Players: 19% | Managers: 51% | Americas: 18% |

Market-Sizing & Forecasting

Our core model uses a top-down build that reconstructs the addressable oxygenator demand pool from extracorporeal procedure activity and care capacity, then converts it into revenues using price and mix assumptions. The largest inputs include cardiopulmonary bypass procedure volumes, ECMO and ECPR adoption intensity, hospital and ICU capacity signals, technology mix between bubble and membrane oxygenators, and average selling price movement by region and application.

We cross-check the totals with selective bottom-up approximations, such as sampling supplier revenues where public disclosures exist, channel checks on tender activity, and simple volume times ASP checks in representative countries. In smaller markets where bottom-up visibility is limited, we fill gaps by proxying from similar healthcare systems, then rebalance back to regional totals after expert review.

For forecasting, we use scenario analysis supported by short-run trend smoothing. Demand is sensitive to procedure growth, critical care capacity expansion, and adoption decisions that can shift after guideline and reimbursement changes. We stress test assumptions against what interviewees expect for the next 12 to 24 months in utilization, pricing pressure, and mix change.

Data Validation & Update Cycle

Validation uses multiple checks so outputs remain tied to real-world signals and do not drift due to a single strong assumption. We compare results against independent indicators such as procedure growth rates, regional hospital capacity trends, and observed price bands, then investigate large variances before final sign-off.

Before publishing, the model and narrative go through stepwise analyst review. We trigger callbacks when an estimate conflicts with procurement feedback or supply availability signals. The study is refreshed annually, and interim updates are made when major regulatory, reimbursement, or supply chain events materially change pricing or adoption. Right before delivery, we run a final update pass so clients receive the most current view.

Mordor Intelligence's Oxygenators Market Estimate Compared With Other Published Estimates

Published market sizes for oxygenators do not always match, even when they appear to cover the same device category. Differences typically come from the base year chosen, how procedure-driven demand is translated into revenue, and whether adjacent extracorporeal items are counted together with oxygenators.

Some external estimates group oxygenators with a wider extracorporeal consumables spend or rely on broader "ECMO systems" style reporting, which can lift the total even if the growth rate looks reasonable. In Mordor Intelligence sizing, revenue is counted for oxygenator devices only, kept separate from adjacent disposables and console components. The estimate is then refreshed with updated procedure and adoption inputs before forecasting forward.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 298.88 M (2026) | |

| Global Consultancy A | USD 302.01 M (2025) | Uses a different base year and longer horizon, and the published highlight does not clearly explain how regional price and technology mix are updated between years, which can shift the starting value. |

| Industry Publisher B | USD 295.20 M (2026) | Base year is stated as 2025 but the 2025 value is not shown in the summary, and scope notes in the public view are limited, which makes it harder to confirm if oxygenator only revenues are separated from broader ECMO related items. |

Across the three figures, most of the spread is explained by base year choice and how tightly oxygenator device revenue is separated from nearby extracorporeal product spending. By keeping inputs tied to procedure activity, mix, and realistic ASP bands, the final number remains traceable and can be re-created with the same steps when new data points are available.

Key Questions Answered in the Report

How large is the global oxygenators market in 2026?

The oxygenators market size is USD 298.88 million in 2026 and is forecast to reach USD 387.59 million by 2031.

Which product segment is growing fastest within oxygenators?

Membrane oxygenators lead growth, expanding at a 7.32% CAGR through 2031 due to superior biocompatibility and compatibility with portable ECMO.

What geographic region is expanding most quickly?

Asia-Pacific is the fastest-growing region, advancing at 6.41% annually, propelled by rapid ECMO adoption and domestic manufacturing in China.

How are portable systems influencing oxygenator demand?

Sub-3 kg ECMO platforms allow pre-hospital deployment, opening new high-margin niches and accelerating procedure volumes outside traditional OR environments.

What is the main workforce challenge affecting oxygenator uptake?

A static pool of about 5,000 certified perfusionists in the United States limits the pace at which hospitals can launch or expand ECMO programs.

Which companies dominate the oxygenators competitive landscape?

Getinge, LivaNova, Medtronic, and Terumo collectively hold roughly 60-65% market share, though Chinese suppliers are rapidly gaining ground.

Page last updated on: