Compression Therapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.52 Billion |

| Market Size (2031) | USD 5.76 Billion |

| Growth Rate (2026 - 2031) | 4.96% CAGR |

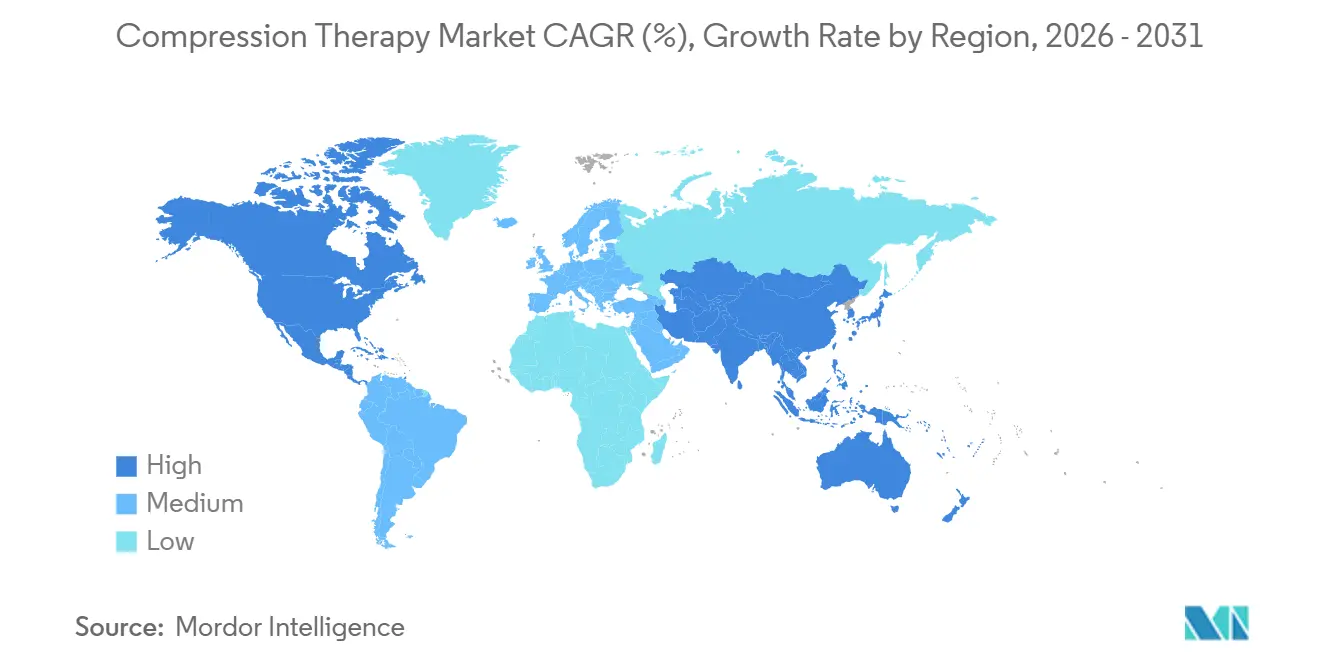

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Compression Therapy Market Analysis by Mordor Intelligence

The compression therapy market size in 2026 is estimated at USD 4.52 billion, growing from 2025 value of USD 4.31 billion with 2031 projections showing USD 5.76 billion, growing at 4.96% CAGR over 2026-2031. Sustained demand originates from aging societies, the rising prevalence of venous disorders, and broader acceptance of compression garments in preventive wellness. Institutional confidence is building after Medicare expanded lymphedema coverage in 2024, while elite-sport recovery protocols have given the therapy consumer appeal [1]Centers for Medicare & Medicaid Services, “Lymphedema Compression Treatment Coverage,” cms.gov . Device makers are shifting toward data-enabled products that combine static and dynamic pressure cycles, elevating clinical outcomes and unit prices. Competitive strategies now hinge on regulatory readiness under the European Medical Device Regulation, geographic expansion into Asia-Pacific, and portfolio upgrades that integrate smart textiles and remote monitoring.

Key Report Takeaways

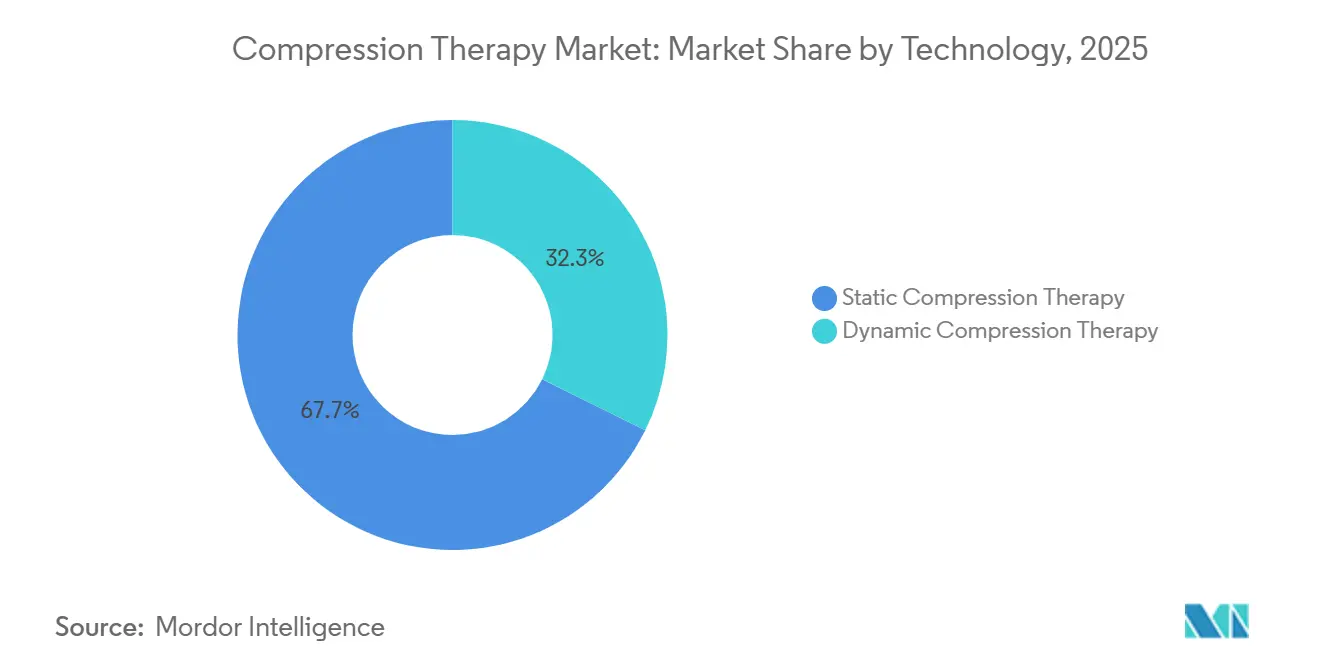

- By technology, static systems led with a 67.74% compression therapy market share in 2025, while dynamic systems are projected to register a 5.68% CAGR through 2031.

- By product, compression garments accounted for 52.02% of the compression therapy market size in 2025 and compression pumps are set to expand at a 5.52% CAGR to 2031.

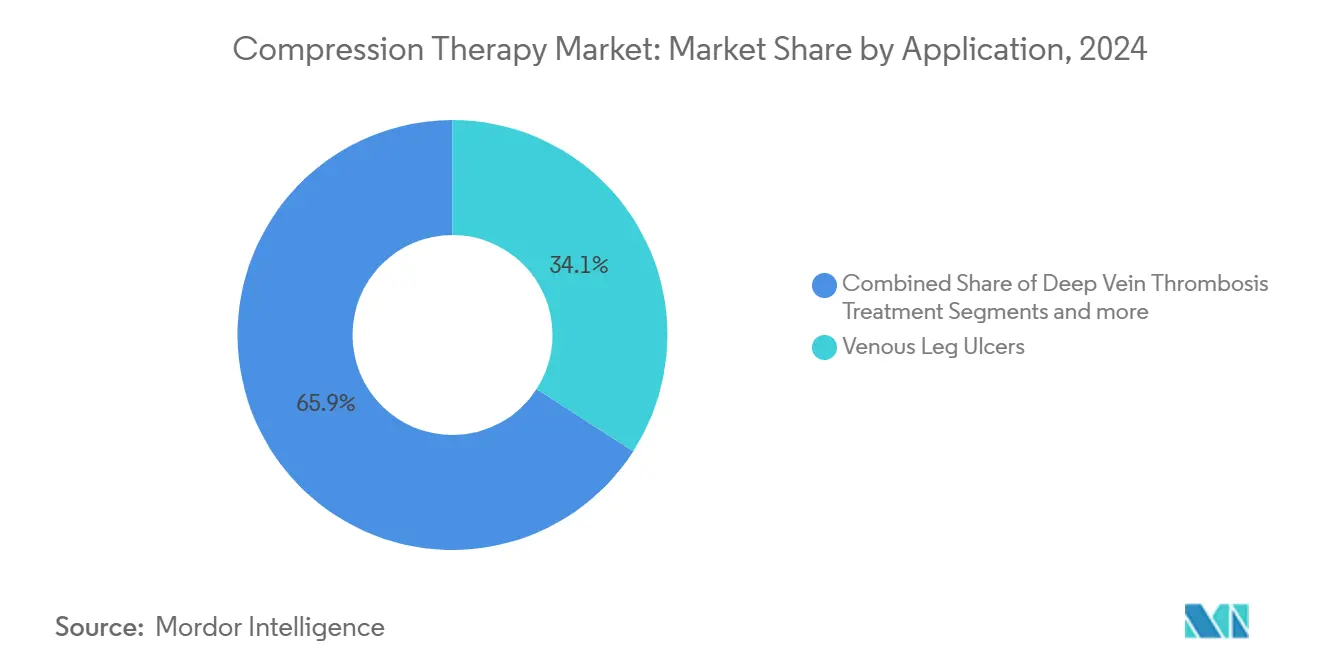

- By application, venous leg ulcers commanded 34.05% of 2025 revenue; lymphedema treatment is advancing at a 5.63% CAGR to 2031.

- By end user, hospitals held 41.02% of the compression therapy market size in 2025; home healthcare is pacing the field at a 5.86% CAGR through 2031.

- By geography, North America contributed 40.55% of 2025 revenue, whereas Asia-Pacific is forecast to grow at a 5.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Compression Therapy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of venous disorders and lymphedema | +1.2% | North America and Europe | Long term (≥ 4 years) |

| Growing geriatric population | +0.9% | Asia-Pacific and North America | Long term (≥ 4 years) |

| Increasing awareness about compression therapy benefits | +0.8% | Asia-Pacific, MEA | Medium term (2-4 years) |

| Advancements in compression garments | +0.7% | North America & EU | Medium term (2-4 years) |

| Expanding use in sports and fitness recovery | +0.6% | Global | Short term (≤ 2 years) |

| Favorable reimbursement policies in developed markets | +0.5% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of venous disorders and lymphedema

Chronic venous insufficiency affects 25 million adults in the United States, creating continuous demand for compression therapy as a first-line intervention [2]American Heart Association, “Chronic Venous Insufficiency Statistics,” heart.org. High-pressure graduated stockings prevent post-thrombotic syndrome, and 2025 SCAI clinical guidelines strongly endorse their use for venous ulcers [3]Robert R. Attaran, "2025 SCAI Clinical Practice Guidelines for the Management of Chronic Venous Disease: This statement was endorsed by the Society for Vascular Medicine (SVM)," JSCAI, sciencedirect.com. This formal backing stabilizes procurement plans for hospitals and payers. Persistent therapeutic need produces predictable replacement cycles, allowing manufacturers to plan capacity and sustain the compression therapy market over the long term.

Growing geriatric population

Population aging places structural pressure on vascular health, especially in Asia-Pacific where the 65+ cohort is climbing at 4% annually. Clinical trials show 87.5% of older adults report improved quality of life with pneumatic compression devices. Medicare’s 2024 lymphedema benefit removes cost barriers in the United States. Together, demographic inevitability and policy support ensure expanding uptake of compression solutions for chronic swelling and mobility limitations.

Increasing awareness about compression therapy benefits

Sports-science publications confirm pneumatic compression reduces muscle soreness and accelerates recovery. Recreation athletes and wellness consumers are adopting similar practices, widening the customer base beyond patients. Manufacturers such as SIGVARIS promote all-day comfort lines, while endorsements from professional teams sparkle interest across fitness communities. Awareness campaigns convert compression therapy from solely curative to preventive, enlarging the compression therapy market.

Advancements in compression garments

Smart textiles equipped with embedded sensors now modulate pressure in response to real-time limb circumference changes. MIT’s fiber-computer concept enables garments that collect biomechanical data while delivering therapy. LYCRA ADAPTIV fibers alter stretch properties under load, balancing comfort and therapeutic pressure. Nanocoated radiative-cooling fabrics lower skin temperature, raising adherence levels in warm climates. Premium pricing attached to these innovations boosts revenue per unit and heightens product differentiation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of patient compliance and discomfort during use | -0.8% | Global | Medium term (2-4 years) |

| Limited reimbursement in developing markets | -0.6% | Asia-Pacific, MEA, Latin America | Long term (≥ 4 years) |

| Availability of alternative therapies | -0.4% | North America & Europe | Medium term (2-4 years) |

| High cost of advanced products | -0.5% | Asia-Pacific, MEA, Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lack of patient compliance and discomfort during use

Non-adherence remains a clinical hurdle; surveys show many patients discontinue stockings within weeks due to heat and difficulty donning. SIGVARIS counters with moisture-wicking yarns and temperature-regulating finishes that improve wearer experience. Digital companions now track usage and alert clinicians when wear time falls below prescription. As material science advances, the compliance barrier is expected to recede, tempering the negative CAGR impact.

Limited reimbursement in developing markets

In emerging economies, public insurers seldom cover medical compression, and out-of-pocket costs deter regular use. Tiered product lines with basic cotton blends at lower price points are helping manufacturers seed brand presence. Governments in Southeast Asia are piloting chronic-wound reimbursement initiatives, suggesting gradual relief of this restraint over the long term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Dynamic Systems Drive Innovation

Static systems accounted for 67.74% of 2025 revenue, giving them the largest compression therapy market share among technologies. Dynamic pumps, though smaller, are charting a 5.68% CAGR as hospitals and home-care providers migrate to devices that tailor pressure cycles. The Kendall SCD SmartFlow platform delivers vascular refill detection to personalize therapy and cut session times. The compression therapy industry is experiencing a technological convergence where smart textiles interface with pneumatic controllers, signaling future hybrid solutions.

Dynamic devices earn premium pricing because clinical studies cite superior edema reduction and patient comfort. Hospital wound centers frequently adopt pneumatic sleeves following ulcer debridement, while home-care agencies lease portable pumps to chronic-swelling patients. Static wraps remain prevalent for their low cost and ease of training, ensuring they retain core demand within the compression therapy market.

By Product: Garments Lead, Pumps Accelerate

Compression garments generated 52.02% of 2025 revenue, cementing their role as the most popular modality for daily use. Graduated stockings constitute the bulk of volume, although torso and arm sleeves are gaining attention among lymphedema patients. Pumps are forecast to post the highest 5.52% CAGR; Tactile Medical’s Nimbl system achieved meaningful limb-volume reductions in 52-week trials. The compression therapy market size for pumps is expanding as payers approve rental reimbursement and remote monitoring assures adherence.

Braces and wraps hold discreet niches, especially within sports orthopedics. Manufacturers often bundle braces with moisture-managing fabrics to attract athletes seeking stabilization and compression in one product. As consumer literacy on prophylactic care rises, product lines diversify to include fashion-oriented compression socks, fueling incremental growth and reinforcing garments’ dominance in the compression therapy market.

By Application: Lymphedema Treatment Gains Momentum

Venous leg ulcers retained 34.05% of revenue in 2025, reflecting chronic wound burdens in aging populations. The compression therapy market size for venous ulcers is supported by guideline mandates that position multi-layer bandaging as gold standard. Lymphedema is the fastest-growing application at a 5.63% CAGR, catalyzed by Medicare’s coverage of garment supplies and enhanced pump algorithms. Clinics report higher follow-through rates after stocking multi-pressure kits with educational materials, strengthening therapy outcomes.

Deep vein thrombosis aftercare remains a substantial opportunity, with stockings recommended to prevent post-thrombotic syndrome. Colleges and gyms increasingly use compression sleeves to expedite recovery, representing an emerging wellness subsegment. This application plurality cushions revenue volatility, ensuring the compression therapy market remains diverse across pathologies.

By End User: Home Healthcare Transformation

Hospitals held 41.02% of 2025 sales, justified by broad inpatient indications and bundled procurement contracts. Most Level-1 trauma centers maintain in-house pump fleets for perioperative thromboprophylaxis, grounding a stable demand floor. Home healthcare, however, is rising at a 5.86% CAGR, forming a new frontline for chronic swelling care as patients prefer at-home regimens supported by telehealth. Device makers now preconfigure Bluetooth modules that transmit adherence data to nurses, lifting therapy transparency.

Specialty wound clinics deploy higher-intensity pressure regimens and trial next-gen fabrics featuring conductive yarns. Physical therapy offices have integrated compression sleeves into recovery packages, expanding the compression therapy industry’s relationship with rehabilitative services. The pivot toward decentralized care favors compact, user-friendly devices and subscription supply models, broadening income streams.

Geography Analysis

North America contributed 40.55% of 2025 revenue due to Medicare reimbursement, broad clinical literacy, and well-developed distributor networks. Hospitals replenish stockings every six months, supporting recurring orders that stabilize the compression therapy market. Europe follows with consistent adoption under public health systems; Germany’s statutory funds reimburse two pairs of medical stockings per year, ensuring predictable volume.

Asia-Pacific is forecast for a 5.72% CAGR through 2031. Aging demographics intersect with rising diabetes prevalence, elevating venous and lymphatic complications. Urban hospitals in China now pilot smart-textile stockings, while Japanese home-care providers integrate pneumatic pumps for aged residents. These shifts attract foreign direct investment and spur local manufacturing clusters.

In South America and the Middle East & Africa, growth is tempered by limited reimbursement and import duties. Nonetheless, physician education programs and modular pumps priced for emerging markets are gradually elevating penetration. As these regions upgrade vascular-care infrastructure, the compression therapy market is expected to capture incremental volume gains.

Competitive Landscape

Moderate concentration characterizes the field. Solventum and Essity AB leverage multi-brand portfolios and extensive hospital ties, medi GmbH excels with German engineering and CE-mark expertise, and SIGVARIS owns a strong consumer retail footprint. Market entry barriers rose with Europe’s 2024 Medical Device Regulation, favoring firms able to fund comprehensive clinical dossiers.

Technology disruption is reshaping rivalries. Hyperice’s Normatec Premier integrates mobile apps and AI-guided recovery plans, challenging legacy pump providers. Smart garment pioneers partner with sports-science labs to validate performance claims, opening flank positions in the compression therapy market. Digital-health tie-ins differentiate offerings and build data streams for predictive maintenance and refill prompts.

Consolidation activity persists. Teleflex acquired BIOTRONIK’s vascular intervention unit for EUR 760 million to expand end-to-end clot-management solutions. Cross-border deals provide regional footprints and regulatory files that shorten market-entry timelines. As hybrid systems proliferate, alliances between textile specialists, sensor makers, and pump manufacturers are likely to intensify, emphasizing the convergence narrative.

Compression Therapy Industry Leaders

-

Essity AB (BSN medical)

-

SIGVARIS Group

-

Tactile Systems Technology, Inc.

-

medi GmbH & Co. KG

-

Solventum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: AIROS Medical, Inc., announced the launch of the U.S. Food and Drug Administration (FDA) 510(k)-cleared ARTAIRA Arterial Compression Device. ARTAIRA is a non-invasive intermittent pneumatic compression device that increases blood flow and circulation to the lower extremities to treat patients with some symptoms of peripheral arterial disease (PAD) in the comfort of their own homes.

- November 2024: Heriot-Watt University researchers unveiled a flexible pressure-sensing polymer patch fit for sub-bandage placement to verify correct pressure in real time.

- October 2024: Tactile Systems Technology commenced U.S. sales of the Nimbl pneumatic platform for upper-extremity lymphedema.

- October 2024: Hyperice began European rollout of Normatec Premier following CE certification and integrated multilingual app support.

Global Compression Therapy Market Report Scope

As per the scope of the report, compression therapy is a simple and effective means of increasing blood flow activity in the lower limbs through strengthening vein support. It's a form of wound care that aims to gently apply pressure to the ankles and legs by wearing specifically designed stockings. It is used to treat edema and other venous and lymphatic disorders of the lower limb.

The compression therapy market is segmented by technology, product, application, end user, and geography. By technology, the market is segmented into static compression therapy and dynamic compression therapy. By product the market is segmented into compression garments, compression pumps, and compression braces. By application segment includes venous leg ulcers, deep vein thrombosis treatment, lymphedema treatment, and other applications. By end user the market is segmented into hospitals, specialty clinics, home care, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. For each segment, the market sizing and forecasts have been done based on value (USD).

| Static Compression Therapy |

| Dynamic Compression Therapy |

| Compression Garments |

| Compression Pumps |

| Compression Braces |

| Venous Leg Ulcers |

| Deep Vein Thrombosis Treatment |

| Lymphedema Treatment |

| Other Applications |

| Hospitals |

| Specialty Clinics |

| Home Care |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Static Compression Therapy | |

| Dynamic Compression Therapy | ||

| By Product | Compression Garments | |

| Compression Pumps | ||

| Compression Braces | ||

| By Application | Venous Leg Ulcers | |

| Deep Vein Thrombosis Treatment | ||

| Lymphedema Treatment | ||

| Other Applications | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Home Care | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the compression therapy market in 2026?

The compression therapy market size is USD 4.52 billion in 2026.

What is the growth outlook for compression devices used at home?

Home-healthcare purchases of compression systems are projected to rise at a 5.86% CAGR through 2031 as care shifts outside hospitals.

Which product segment is growing quickest?

Compression pumps are expanding at a 5.52% CAGR, the fastest among product categories.

Why is Asia-Pacific viewed as the most attractive expansion region?

Rapid population aging, increasing vascular-disease prevalence, and improving healthcare infrastructure drive a 5.72% CAGR in Asia-Pacific.

What technological trend is reshaping competitive dynamics?

Smart textiles combining real-time pressure sensing with adaptive fabrics are redefining product performance and pricing tiers.

How do reimbursement policies influence adoption?

Medicare and several EU payers cover medical stockings and certain pumps, lowering patient costs and stabilizing recurring demand.

Page last updated on: