Recreational Oxygen Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

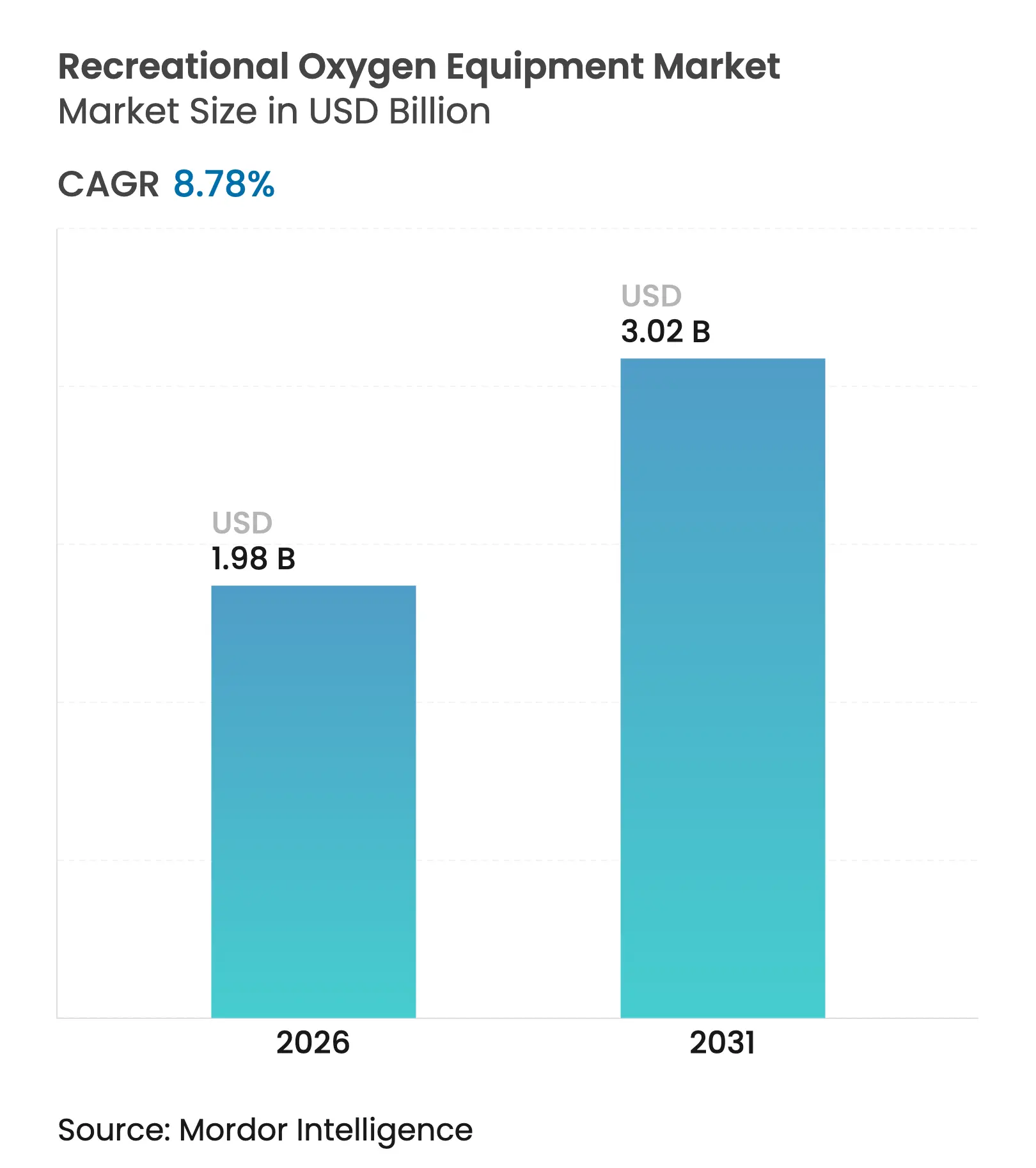

| Market Size (2026) | USD 1.98 Billion |

| Market Size (2031) | USD 3.02 Billion |

| Growth Rate (2026 - 2031) | 8.78 % CAGR |

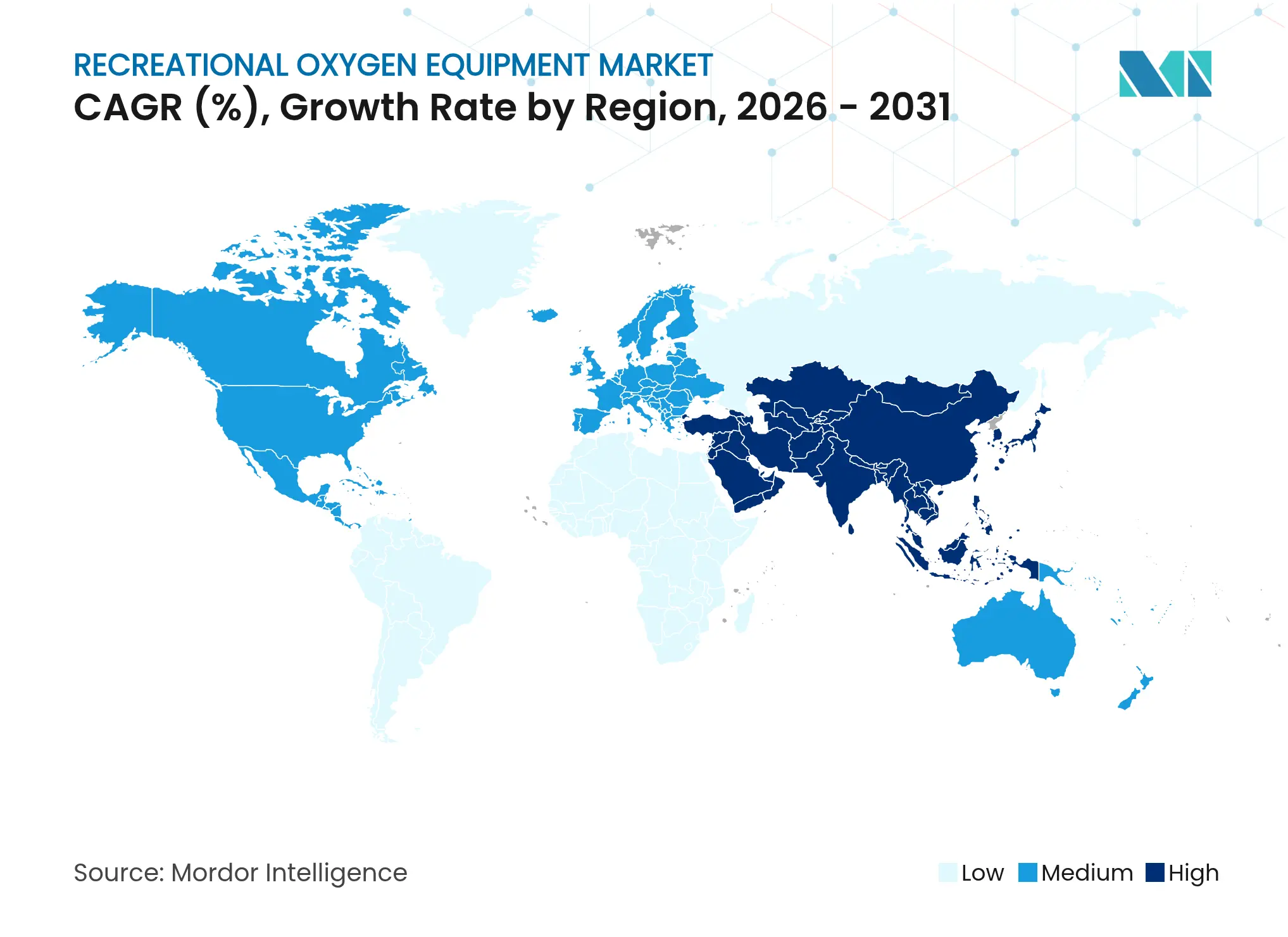

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

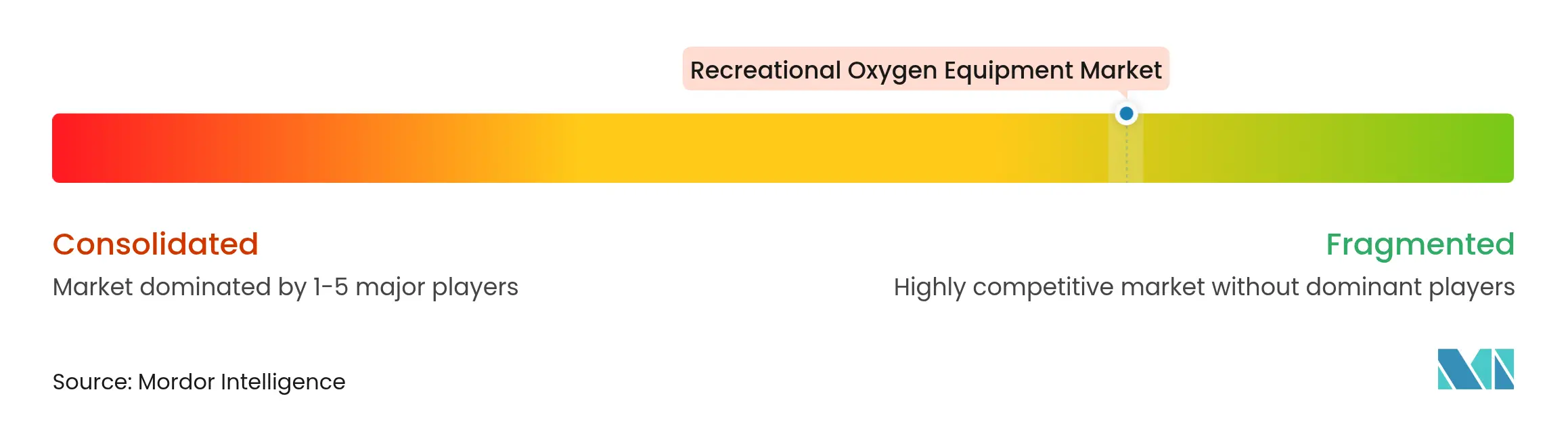

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Recreational Oxygen Equipment Market Analysis by Mordor Intelligence

The recreational oxygen equipment market size is expected to grow from USD 1.82 billion in 2025 to USD 1.98 billion in 2026 and is forecast to reach USD 3.02 billion by 2031 at 8.78% CAGR over 2026-2031. Demand growth is underpinned by rising interest in high-altitude travel, home-based fitness recovery, and biohacking practices that position oxygen supplementation as an everyday performance enhancer. Intensifying product innovation around lighter batteries, higher oxygen purity, and Bluetooth-enabled monitoring empowers users to integrate oxygen routines seamlessly into daily life. Major retailers and pharmacy chains now merchandise portable concentrators and oxygen cans beside vitamins, signaling mainstream acceptance while lowering customer acquisition costs for manufacturers. Meanwhile, strategic acquisitions by larger medical-supply groups broaden distribution and service footprints, accelerating professionalization of a category once limited to niche sports stores.

Key Report Takeaways

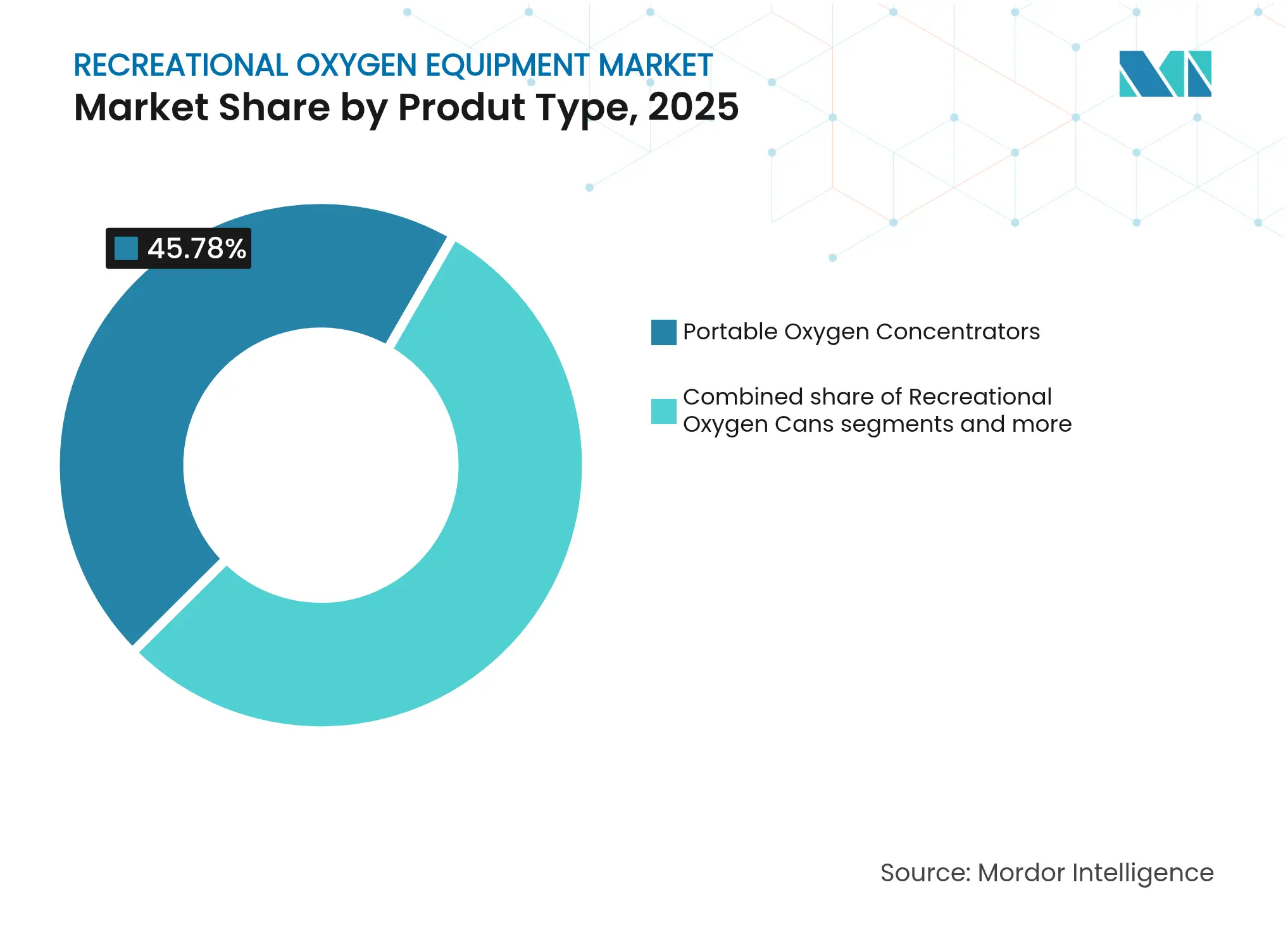

- By product type, portable oxygen concentrators captured 45.78% of recreational oxygen equipment market share in 2025.

- Hyperbaric oxygen chambers for personal use are projected to advance at a 9.01% CAGR between 2026 and 2031.

- By application, sports and fitness recovery commanded 40.71% share of the recreational oxygen equipment market size in 2025.

- Wellness and spa applications are expected to grow at a 9.62% CAGR through 2031.

- By geography, North America led with 41.85% revenue share in 2025, while Asia-Pacific is forecast to post the fastest 9.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Recreational Oxygen Equipment Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing use of portable oxygen cans by endurance athletes Growing use of portable oxygen cans by endurance athletes | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Global, with concentration in North America & Europe | Impact Timeline:Medium term (2-4 years) |

Rising consumer-health focus on respiratory wellness Rising consumer-health focus on respiratory wellness | +1.8% | Global, accelerated in developed markets | Long term (≥ 4 years) | |||

Expansion of high-altitude tourism destinations Expansion of high-altitude tourism destinations | +0.9% | APAC core, spill-over to South America | Long term (≥ 4 years) | |||

Retail rollout across pharmacy & sporting-goods chains Retail rollout across pharmacy & sporting-goods chains | +1.1% | North America & Europe, expanding to APAC | Medium term (2-4 years) | |||

Influencer-led "bio-hacking" communities boosting demand Influencer-led "bio-hacking" communities boosting demand | +0.7% | Global, concentrated in urban centers | Short term (≤ 2 years) | |||

Airport spa chains installing oxygen bars post-COVID Airport spa chains installing oxygen bars post-COVID | +0.5% | Global, focused on major international hubs | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Use of Portable Oxygen Cans by Endurance Athletes

Elite and recreational athletes increasingly integrate low-flow oxygen bursts between training intervals to accelerate lactate clearance and shorten recovery windows. Sports federations ranging from tennis to mixed martial arts allow supplemental oxygen provided it is free of performance-enhancing additives, removing regulatory friction to adoption. Major sporting goods stores now dedicate shelf space to oxygen cans beside electrolyte powders, giving the recreational oxygen equipment market fresh visibility in mainstream retail. Equipment manufacturers have responded with lightweight aluminum cylinders fitted with ergonomic masks, enabling runners to self-dose during altitude simulation workouts. Consumer reviews emphasize perceived stamina boosts and reduced muscle soreness, reinforcing word-of-mouth marketing effects. As endurance races resume post-pandemic, on-course oxygen kiosks are emerging as premium support services that bundle recovery stations with paid race entries.

Rising Consumer-Health Focus on Respiratory Wellness

COVID-19 underscored the fragility of lung function, encouraging consumers to seek daily routines that maintain high blood-oxygen saturation. Urban dwellers exposed to air-pollution alerts frequently purchase portable concentrators for home offices, combining oxygen sessions with guided breathing apps. Wellness centers report double-digit growth in demand for hyperbaric oxygen therapy (HBOT), citing per-session revenues of USD 60–USD 150 that recoup chamber costs within 18 months. Clinical studies on intermittent hypoxic–hyperoxic training for Long COVID have shown meaningful improvements in exercise capacity, lending scientific legitimacy to consumer adoption. Millennials and Gen Z consumers—already comfortable paying subscription fees for biometrics wearables—now view oxygen routines as another measurable health metric. This attitudinal shift lengthens product-replacement cycles because users increasingly demand multi-mode devices that handle continuous flow, pulse dose, and nebulization.

Expansion of High-Altitude Tourism Destinations

Adventure operators in Tibet, Patagonia, and the Himalayas have reopened at full capacity, welcoming travelers with limited acclimatization windows who rely on portable concentrators to offset acute mountain sickness risk. New stratospheric-balloon experiences—climbing beyond 30 km altitude—require cabin life-support systems that share components with consumer concentrators, creating downstream sourcing synergies for suppliers. Local governments near ski resorts offer tax rebates on oxygen-bar installations in hotels, positioning respiratory wellness as a differentiator for premium hospitality. Rising disposable incomes across Asia-Pacific unlock budget for experiential travel, ensuring sustained sales of lightweight concentrators bundled with expedition packages. Manufacturers also partner with tour companies to provide rental fleets, converting occasional users into future direct purchasers after their trips.

Retail Rollout Across Pharmacy & Sporting-Goods Chains

Pharmacy giants in the United States have added dedicated shelf space for portable oxygen products next to inhalers and pulse oximeters, normalizing oxygen supplementation for casual shoppers. Store-within-a-store concepts allow brands to conduct onsite oxygen saturation demos, enhancing customer education while increasing high-margin accessory sales. The expanded distribution network reduces shipping costs for manufacturers and provides consistent consumer-brand touchpoints, driving repeat purchases of single-use canisters. In Europe, sporting-goods chains pilot click-and-collect lockers that stock refillable cylinders, reinforcing sustainability narratives. Regional rollout schedules track air-quality indices and altitude clusters, ensuring that inventory aligns with localized demand triggers such as wildfire seasons or marathon events.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Regulatory grey zone between medical & consumer oxygen Regulatory grey zone between medical & consumer oxygen | -1.4% | Global, particularly stringent in Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-1.4% | Geographic Relevance:Global, particularly stringent in Europe | Impact Timeline:Long term (≥ 4 years) |

Safety concerns around incorrect high-flow usage Safety concerns around incorrect high-flow usage | -0.8% | Global, with focus on liability-conscious markets | Medium term (2-4 years) | |||

Rising environmental pushback on single-use aluminum cans Rising environmental pushback on single-use aluminum cans | -0.6% | Developed markets with strong environmental regulations | Long term (≥ 4 years) | |||

Smartphone-based oximetry reducing perceived need Smartphone-based oximetry reducing perceived need | -0.4% | Global, accelerated in tech-savvy demographics | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Regulatory Grey Zone Between Medical & Consumer Oxygen

Jurisdictions worldwide still debate whether high-purity oxygen sold without a prescription constitutes a medical device or a wellness accessory, creating compliance ambiguity for manufacturers. Differing classification regimes drive costs for parallel packaging, dual quality-management certifications, and multi-country product codes. In Europe, certain member states treat oxygen cans as medicinal gases, imposing pharmacy-only distribution, while others list them under general consumer products, resulting in patchwork market access. Logistics complexity discourages smaller entrants, potentially slowing innovation as firms weigh certification timelines against product-lifecycle horizons. A unified global standard would accelerate cross-border e-commerce, but consensus remains distant, prolonging uncertainty that suppresses long-term capital investment in the recreational oxygen equipment market.

Safety Concerns Around Incorrect High-Flow Usage

Although most recreational devices deliver low-flow oxygen, consumer misuse—such as continuous exposure above manufacturer limits—poses elevated fire and lung-toxicity risks[1]Source: PHMSA, “Safety Advisory Notice on Unsafe Cylinders,” phmsa.dot.gov . FDA adverse-event databases include portable concentrator malfunctions during air travel, underscoring the need for robust alarm systems and airline-approved batteries. Training gaps persist because many recreational buyers have no clinical background; they may inhale pure oxygen while smoking or exceed recommended flow rates during unsupervised sessions. Liability fears raise insurance premiums for gyms and spas, limiting commercial oxygen-bar rollouts. Manufacturers are responding with tamper-proof flow controls and app-based usage timers, but widespread adoption of safety-first designs will take several product cycles.

Segment Analysis

By Product Type: Concentrators Lead While Chambers Accelerate

Portable concentrators generated the largest revenue slice in 2025, securing 45.78% of recreational oxygen equipment market share owing to their lightweight design, FAA acceptance for in-flight use, and battery runtimes exceeding five hours. Feature sets now include Bluetooth telemetry that uploads oxygen-flow logs to coaching apps, blurring lines between medical compliance and fitness biometrics. At the opposite end, personal hyperbaric chambers represent the most dynamic niche, forecast to expand at a 9.01% CAGR through 2031. Wellness influencers document perceived gains in cognitive clarity and post-workout stamina, amplifying consumer curiosity and prompting spas to introduce single-person HBOT pods. Accessories ranging from antimicrobial masks to pulse-ox ring sensors bolster aftermarket revenue streams and lock customers into proprietary ecosystems.

Hyperbaric chamber manufacturers are redesigning pressure cycles to shorten sessions from 90 to 45 minutes, increasing daily throughput for commercial operators and strengthening the recreational oxygen equipment market size in premium service venues. Meanwhile, oxygen-bar equipment vendors shift toward modular rigs that can switch from 30% to 90% oxygen at the touch of a touchscreen, aligning experience levels with patron comfort. Single-use canister makers pursue refillable cartridges to counter environmental pushback and reduce aluminum waste. Collectively, these product-level innovations ensure that the recreational oxygen equipment market continues to diversify beyond its concentrator core, appealing to both entry-level users and high-spending biohackers.

Note: Segment shares of all individual segments available upon report purchase

By Application: Sports Recovery Dominates as Wellness Gains Speed

Sports and fitness recovery held 40.71% of the recreational oxygen equipment market size in 2025, reflecting entrenched use by endurance athletes who value rapid lactate metabolism and faster heart-rate normalization after intervals. Leading gym chains have integrated oxygen stations beside cryotherapy booths, bundling recovery subscriptions that lift average customer lifetime value. The wellness and spa category is projected to grow at a 9.62% CAGR as resorts incorporate oxygen cocktails and HBOT sessions into detox retreats. Such packages pair red-light therapy, pulsed-electromagnetic-field mats, and oxygen exercise, appealing to travelers looking for multidimensional rejuvenation.

Home-care adoption is another rising pillar, especially among older adults managing mild exertional dyspnea who prefer an over-the-counter solution rather than prescription oxygen. Manufacturers respond with voice-guided device tutorials and auto-humidification features that minimize nasal dryness. High-altitude tourism applications also spur demand; trekking agencies now include concentrator rentals in expedition fees, easing kit-weight burdens for climbers. As applications proliferate, cross-selling potential rises—an athlete who first buys a portable can for marathon recovery might later upgrade to a home concentrator, illustrating the strategic value of broad product portfolios within the recreational oxygen equipment market.

Geography Analysis

North America preserved its leadership position with 41.85% revenue share in 2025 owing to clear FDA guidance that differentiates recreational oxygen from prescription medical gases, allowing drugstores and outdoor retailers to sell devices without physician oversight. Pharmacy giants have now placed demo kiosks in more than 3,000 stores, giving shoppers hands-on exposure that converts browsers to buyers. Institutional investors signaled confidence when Owens & Minor acquired Rotech Healthcare for USD 1.36 billion, creating a vertically integrated platform that pairs equipment sales with nationwide servicing contracts. Airports from Atlanta to Los Angeles have installed oxygen bars in departure lounges, boosting impulse consumption by anxious flyers.

Asia-Pacific is projected to log a 9.84% CAGR through 2031, the fastest worldwide. China’s Everest gateway towns report more than 500,000 annual tourists who frequently purchase portable oxygen before ascending beyond 3,000 meters, turning pharmacies into critical last-mile outlets. Inogen’s USD 27.2 million alliance with Yuwell boosts localized production capacity, shaving tariffs and aligning product features with Chinese safety codes. Emerging trekking circuits in India’s Ladakh and Indonesia’s Papua provinces further widen the addressable base, while urban biohacking studios in Seoul and Tokyo provide high-margin retail channels.

Europe remains steady, fortified by a mature spa culture and government-funded research on HBOT for post-radiation tissue injury relief. Although classification rules differ between member states, the European Parliament’s acknowledgement of ozone therapy bolsters policymaker openness to broader oxygen-based wellness treatments. Environmental regulation drives interest in recyclable canisters and refill stations, spurring companies to pilot closed-loop supply chains in Germany and the Nordics. Retailers emphasize carbon-neutral shipping labels, appealing to eco-conscious consumers who nonetheless value portable oxygen for post-workout recovery and air-pollution mitigation.

Competitive Landscape

Market Concentration

The recreational oxygen equipment market is moderately concentrated, with about a dozen players controlling the lion’s share of branded revenues. Medical device firms such as Inogen and CAIRE leverage FDA clearances to market dual-use concentrators that span medical and recreational segments, giving them credibility with healthcare providers and insurers. Boutique brands like Boost Oxygen differentiate on flavor infusions and celebrity endorsements, seeding social-media buzz that drives impulse shelf purchases. Strategic consolidation accelerated in 2024 when Owens & Minor absorbed Rotech Healthcare, creating synergies in distribution warehousing and after-sales maintenance that smaller independents struggle to match.

Technological rivalry centers on purity levels, runtime per battery charge, and app-enabled coaching dashboards. Inogen’s Rove 4 delivers up to 840 ml/min while weighing less than 1.4 kg, responding to customer surveys that rank portability above maximum flow in purchase criteria[2]Source: Inogen, “Rove 4 Product Launch,” inogen.com . CAIRE’s forthcoming cloud-connected FreeStyle HiFi model promises predictive maintenance alerts, an advantage for rental fleets operated by adventure-tour agencies. Green engineering has become an innovation frontier; Chart Industries is testing interchangeable carbon-fiber cylinders that halve empty-can weight and slash logistic emissions.

Barriers to entry include certification lead times, warranty servicing networks, and the capital costs of precision oxygen-sensor manufacturing. Yet, the category remains open to disruptive entrants that harness direct-to-consumer e-commerce models. Social-media biohackers often partner with micro-brands to launch limited-edition oxygen kits bundled with wearable oximeters, tapping niche audiences but forcing incumbents to elevate influencer-marketing spend. Over the forecast period, competitive intensity is expected to pivot toward sustainability claims and software integration rather than raw oxygen-flow specifications, aligning with evolving consumer priorities.

Recreational Oxygen Equipment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Inogen announced a USD 27.2 million strategic collaboration with Yuwell to expand product portfolios and Chinese market reach

- December 2024: Inogen secured FDA 510(k) clearance for the Simeox 200 airway-clearance device, broadening its respiratory-care suite

Table of Contents for Recreational Oxygen Equipment Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing use of portable oxygen cans by endurance athletes

- 4.2.2Rising consumer-health focus on respiratory wellness

- 4.2.3Expansion of high-altitude tourism destinations

- 4.2.4Retail rollout across pharmacy & sporting-goods chains

- 4.2.5Influencer-led “bio-hacking” communities boosting demand

- 4.2.6Airport spa chains installing oxygen bars post-COVID

- 4.3Market Restraints

- 4.3.1Regulatory grey zone between medical & consumer oxygen

- 4.3.2Safety concerns around incorrect high-flow usage

- 4.3.3Rising environmental pushback on single-use aluminum cans

- 4.3.4Smartphone-based oximetry reducing perceived need

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product Type

- 5.1.1Recreational Oxygen Cans

- 5.1.2Portable Oxygen Concentrators

- 5.1.3Hyperbaric Oxygen Chambers (Personal)

- 5.1.4Oxygen Bar Equipment

- 5.1.5Accessories (Masks, Tubing)

- 5.2By Application

- 5.2.1Sports & Fitness Recovery

- 5.2.2High-Altitude & Adventure

- 5.2.3Wellness & Spa

- 5.2.4Home & Personal Care

- 5.2.5Others

- 5.3By Geography

- 5.3.1North America

- 5.3.1.1United States

- 5.3.1.2Canada

- 5.3.1.3Mexico

- 5.3.2Europe

- 5.3.2.1Germany

- 5.3.2.2United Kingdom

- 5.3.2.3France

- 5.3.2.4Italy

- 5.3.2.5Spain

- 5.3.2.6Rest of Europe

- 5.3.3Asia-Pacific

- 5.3.3.1China

- 5.3.3.2India

- 5.3.3.3Japan

- 5.3.3.4South Korea

- 5.3.3.5Australia

- 5.3.3.6Rest of Asia-Pacific

- 5.3.4South America

- 5.3.4.1Brazil

- 5.3.4.2Argentina

- 5.3.4.3Rest of South America

- 5.3.5Middle East and Africa

- 5.3.5.1GCC

- 5.3.5.2South Africa

- 5.3.5.3Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Boost Oxygen LLC

- 6.3.2Oxygen Plus Inc.

- 6.3.3CAIRE Inc. (AirSep)

- 6.3.4Philips Respironics

- 6.3.5Inogen Inc.

- 6.3.6Invacare Corporation

- 6.3.7Drive DeVilbiss Healthcare

- 6.3.8Chart Industries (SeQual)

- 6.3.9OxyGo LLC

- 6.3.10Xi’an Arooxy Technology

- 6.3.11OxyHealth LLC

- 6.3.12Environmental Tectonics Corp.

- 6.3.13Sechrist Industries

- 6.3.14O2 Grow

- 6.3.15Linde plc (BOC)

- 6.3.16ResMed Inc.

- 6.3.17GF Health Products

- 6.3.18Besco Medical

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Recreational Oxygen Equipment Market Report Scope

As per the scope of the report, recreational oxygen equipment is a supplemental oxygen commonly utilized in recreational situations or sports. It is different from medical oxygen as it does not require a prescription. Recreation oxygen boosts performance in sports, increases endurance, and promotes relaxation. The recreational oxygen equipment market is segmented by product type (oxygen bar, oxygen cans, and other product types) and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD million) for the above segments. The report offers the value (in USD million) for the above segments. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.