Hydroxychloroquine Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

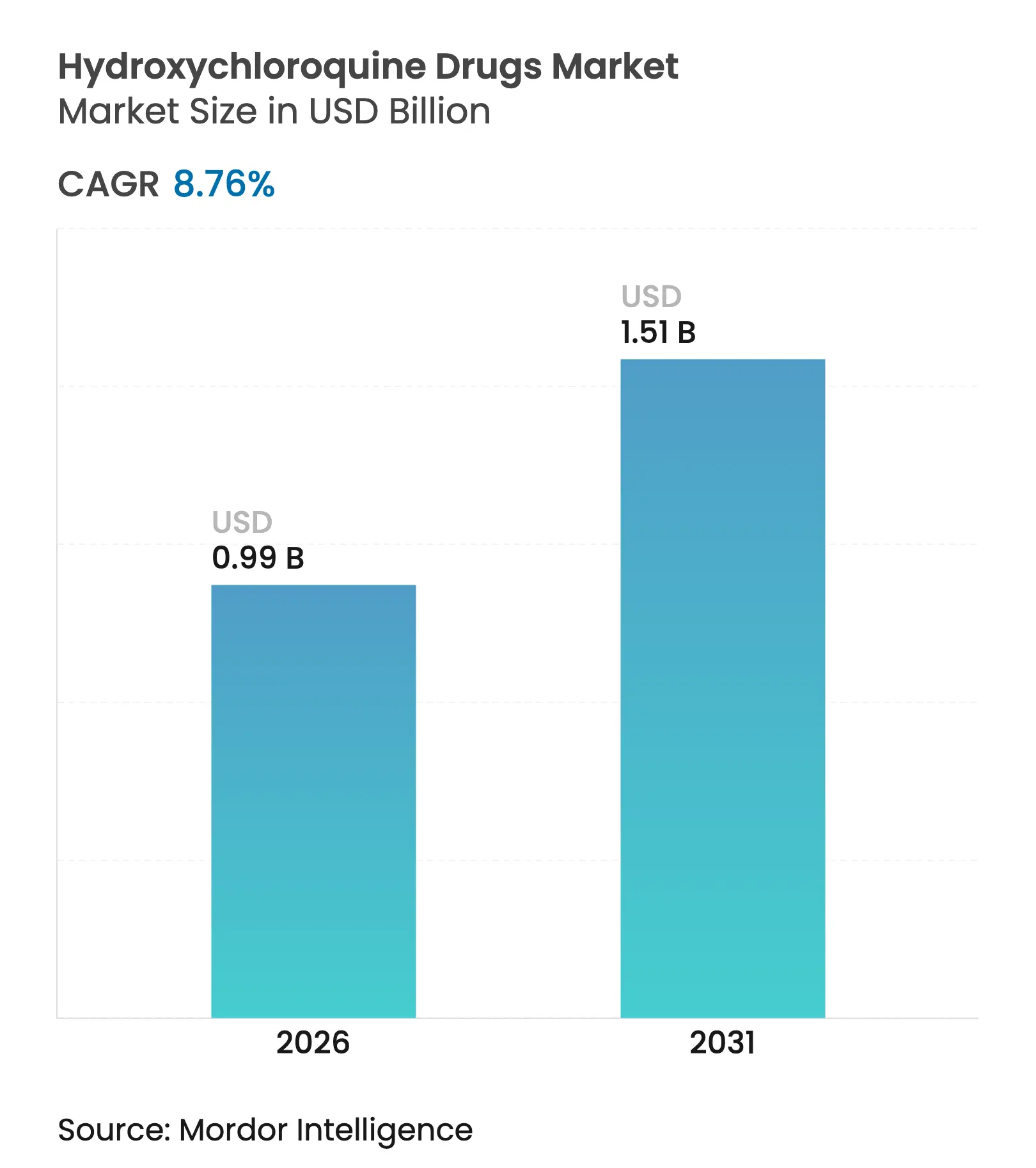

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 1.51 Billion |

| Growth Rate (2026 - 2031) | 8.76 % CAGR |

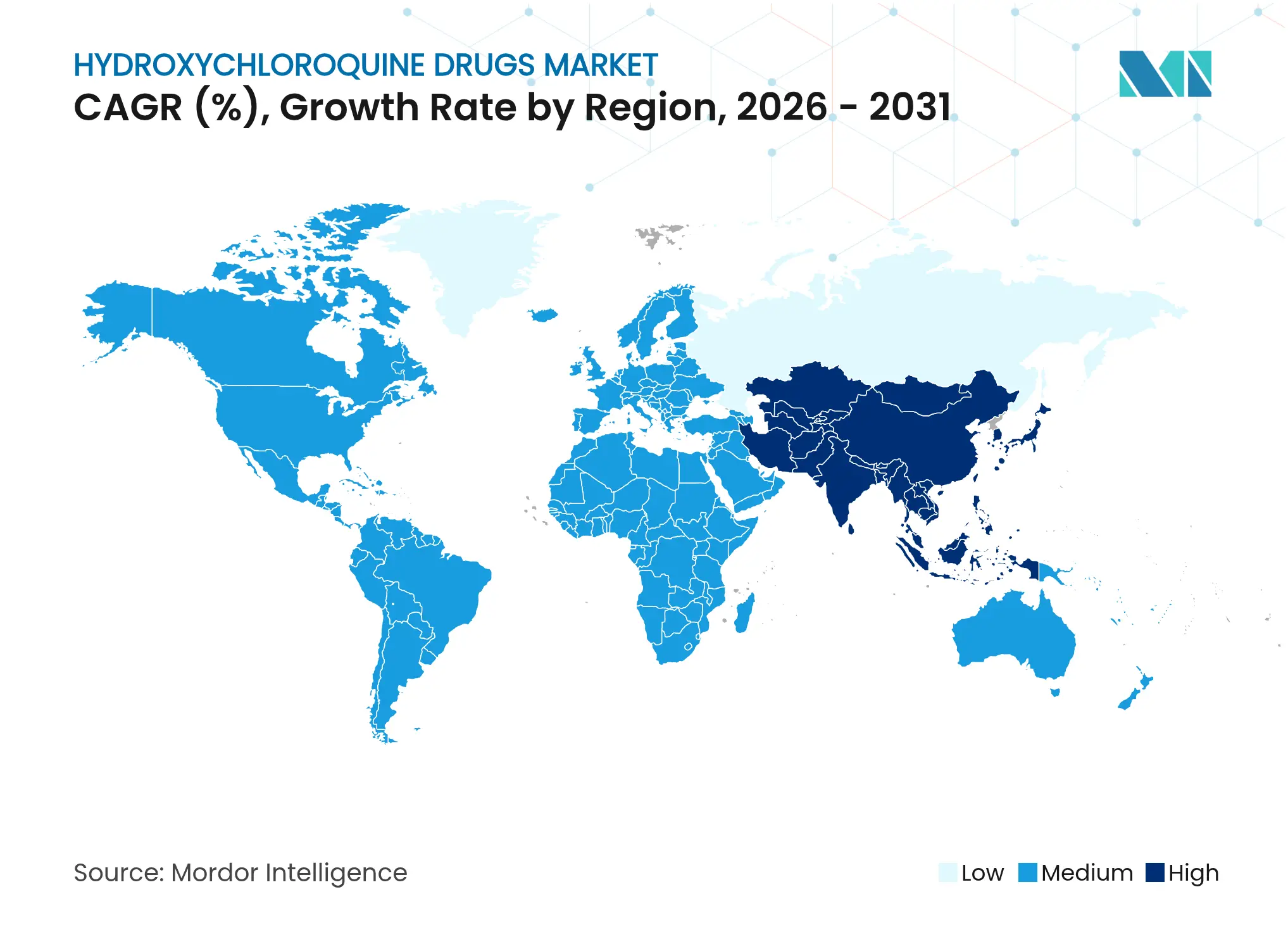

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Hydroxychloroquine Drugs Market Analysis by Mordor Intelligence

The hydroxychloroquine drugs market size was valued at USD 0.91 billion in 2025 and estimated to grow from USD 0.99 billion in 2026 to reach USD 1.51 billion by 2031, at a CAGR of 8.76% during the forecast period (2026-2031). India’s position as the source of 70% of global supply keeps manufacturing costs competitive and underpins reliable export flows to large-volume destinations such as the United States and Brazil. North America secures the largest regional position, benefiting from advanced reimbursement systems and a diversified network of branded-and-generic prescribers. Asia-Pacific registers the fastest growth, supported by rising healthcare spending, favorable production incentives, and bulk drug park investments that cut API import reliance. Malaria therapy remains the leading clinical use, although rapid uptake for rheumatoid arthritis widens the addressable patient base amid escalating autoimmune disease prevalence. Digitization in medicine purchasing is another catalyst, with online pharmacy penetration rising as consumers prioritize convenience and competitive pricing. Formulation innovation, especially pediatric-friendly oral suspensions, enlarges the user pool by improving adherence in age groups that struggle with standard tablets.

Key Report Takeaways

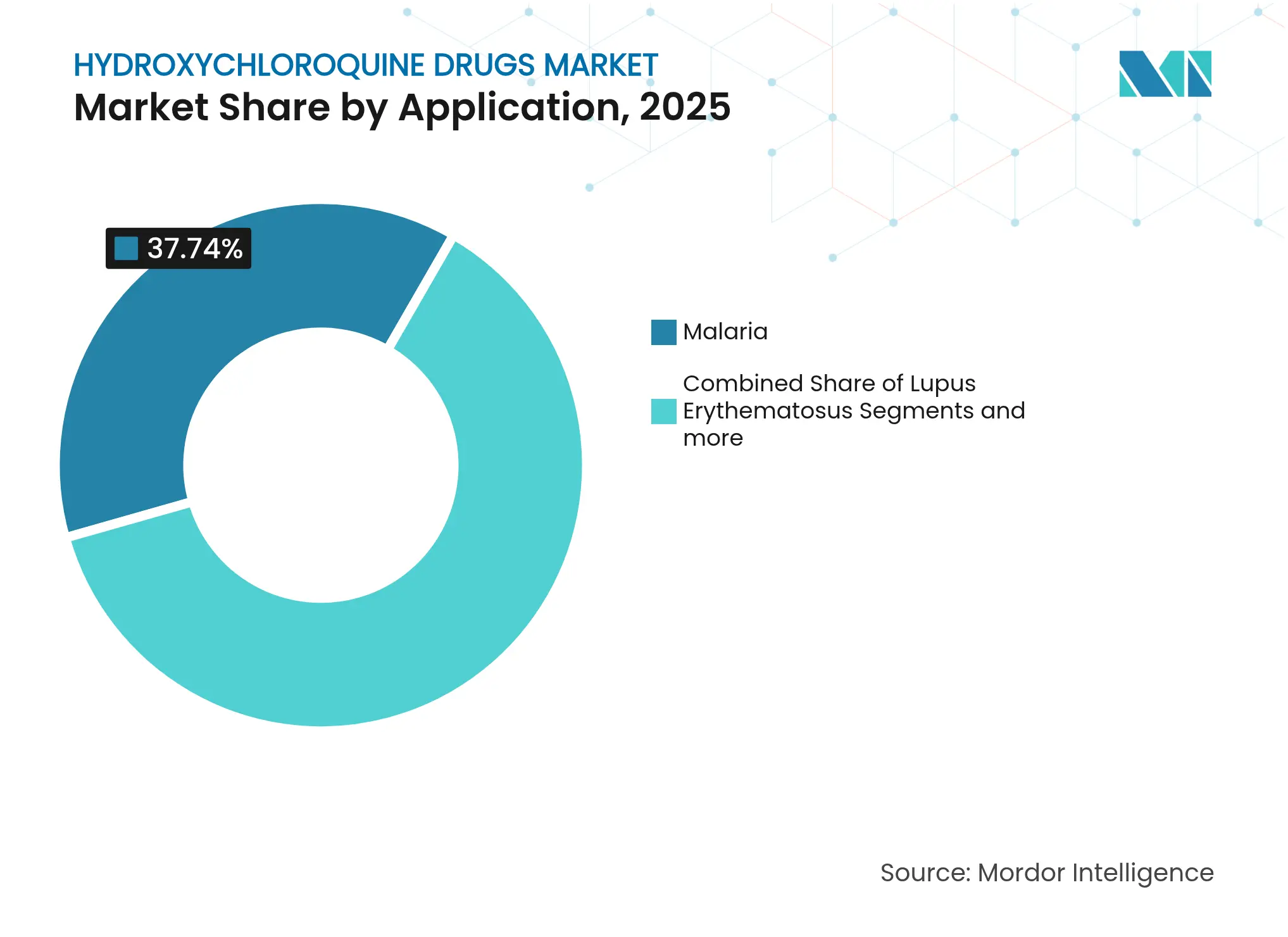

- By application, malaria retained 37.74% of the hydroxychloroquine drugs market share in 2025, while rheumatoid arthritis is projected to grow at 9.76% CAGR between 2026-2031.

- By distribution channel, hospital pharmacies controlled 45.58% revenue in 2025; online pharmacies are set to expand at 9.55% CAGR to 2031.

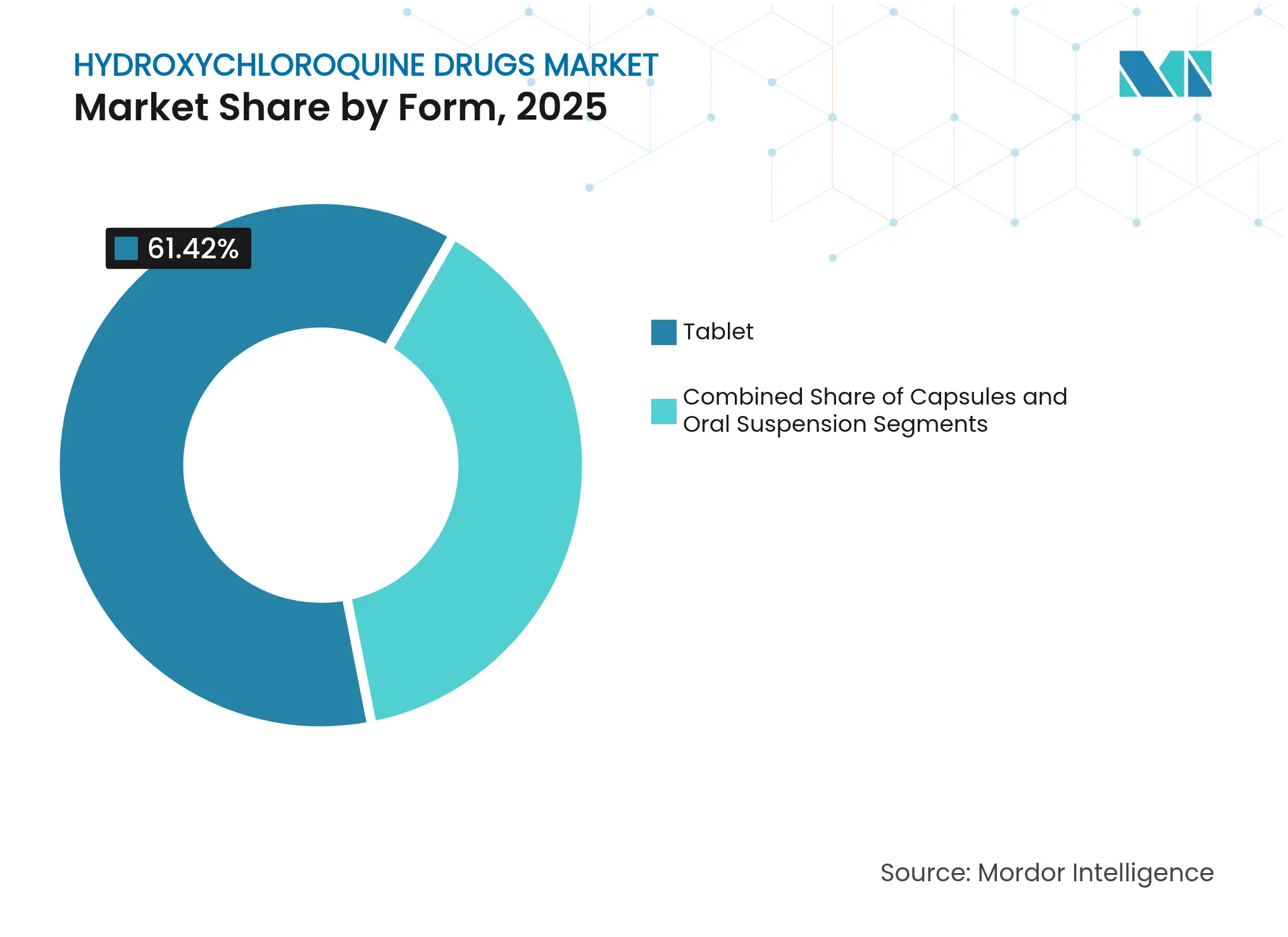

- By form, tablets commanded 61.42% share of the hydroxychloroquine drugs market size in 2025, whereas oral suspensions register the fastest 9.62% CAGR through 2031.

- By geography, North America led with 37.86% revenue share in 2025; Asia-Pacific posts the highest 9.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydroxychloroquine Drugs Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High malaria & rheumatoid arthritis prevalence

High malaria & rheumatoid arthritis prevalence

| +2.1% | Global; Sub-Saharan Africa & high-income regions | Long term (≥ 4 years) |

( ~ ) % Impact on CAGR Forecast

:

+2.1%

|

Geographic Relevance

:

Global; Sub-Saharan Africa & high-income regions

|

Impact Timeline

:

Long term (≥ 4 years)

|

Systemic lupus & other autoimmune burdens

Systemic lupus & other autoimmune burdens

| +1.8% | North America & EU; emerging in APAC | Medium term (2-4 years) | |||

Regulatory fast-tracking & generic approvals

Regulatory fast-tracking & generic approvals

| +1.4% | Global; led by FDA & EMA | Short term (≤ 2 years) | |||

Expanded global manufacturing capacity & lower prices

Expanded global manufacturing capacity & lower prices

| +1.2% | APAC core; spill-over global | Medium term (2-4 years) | |||

Adjunct therapy potential in PCOS & hypertensive

pregnancy

Adjunct therapy potential in PCOS & hypertensive

pregnancy

| +0.9% | Global; early in developed markets | Long term (≥ 4 years) | |||

Nano-delivery & formulation innovation

Nano-delivery & formulation innovation

| +0.7% | North America & EU; expanding to APAC | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Malaria & Rheumatoid Arthritis Prevalence

Persistent malaria transmission in climate-sensitive regions and a rising global rheumatoid arthritis burden sustain baseline demand for hydroxychloroquine. Temperature and rainfall shifts in Ethiopia’s Gambella province directly correlate with higher malaria cases, reinforcing the drug’s relevance in endemic zones [1]Geteneh Moges Assefa, "The Relationship of Climate Change and Malaria Incidence in the Gambella Region, Ethiopia," MDPI, mdpi.com. Simultaneously, rheumatoid arthritis incidence climbed from 10.4 to 11.8 per 100,000 between 1990 and 2021, creating a larger candidate population for disease-modifying antirheumatic regimens [2]BMJ RMD Open, “Global RA incidence 1990-2021,” rmdopen.bmj.com . World Health Organization guidelines continue to highlight antimalarial therapy as integral to malaria case management despite emerging resistance. Rheumatology guidelines likewise keep hydroxychloroquine central in early-stage combination protocols, reinforcing consistent prescription volumes.

Burden Of Systemic Lupus & Other Autoimmune Disorders

Hydroxychloroquine use intensifies in systemic lupus erythematosus, primary Sjögren syndrome, and emerging indications such as ANCA-associated vasculitis [3]Wei-Sheng Chen, "Hydroxychloroquine dose-dependently reduces the risk of incident diabetes in primary Sjögren syndrome patients on glucocorticoids: a nationwide population-based cohort study," Arthritis Research and Therapy, arthritis-research.biomedcentral.com. High-dose regimens lower diabetes risk among Sjögren patients on glucocorticoids, strengthening the drug’s metabolic value proposition. Yet surveys show that 50.2% of lupus patients never receive hydroxychloroquine, underlining the need for clinician education and toxicity-mitigation protocols. Broader cardiovascular and lipid benefits make the therapy attractive for long-term management across overlapping autoimmune conditions.

Regulatory Fast-Tracking & Generic Approvals

Accelerated pathways such as the FDA Commissioner’s National Priority Voucher compress review cycles to as little as 1-2 months for high-priority generics, potentially shortening time-to-market for new hydroxychloroquine entrants. Parallel Scientific Advice sessions between FDA and EMA help firms resolve complex chemistry questions simultaneously, trimming development redundancy and cost. Stable ANDA user fees at USD 321,920 uphold a predictable filing environment while encouraging multiple filers, increasing price competition that favors payers.

Expanded Global Manufacturing Capacity & Lower Prices

Monthly Indian output has risen sixfold to 200 million tablets, anchoring global availability and tempering cost escalation. China’s WuXi STA opened an additional 169-acre API site in 2024, adding 3,773 m³ of reactor volume to the regional supply chain. Nonetheless, API price spikes from INR 7,000 to INR 50,000/kg during peak demand episodes expose volatility that smaller firms struggle to hedge. European and North American reshoring programs seek to diversify sourcing, but most near-term capacity remains Asia-centric.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Chronic global API & finished-dose shortages

Chronic global API & finished-dose shortages

| -1.9% | Worldwide; smaller manufacturers hit hardest | Short term (≤ 2 years) |

( ~ ) % Impact on CAGR Forecast

:

-1.9%

|

Geographic Relevance

:

Worldwide; smaller manufacturers hit hardest

|

Impact Timeline

:

Short term (≤ 2 years)

|

Retinal / cardiac toxicity monitoring

Retinal / cardiac toxicity monitoring

| -1.3% | Global; stricter in developed markets | Long term (≥ 4 years) | |||

Competitive biologics & targeted DMARDs

Competitive biologics & targeted DMARDs

| -0.8% | North America & EU; spreading to APAC | Medium term (2-4 years) | |||

Post-COVID regulatory pushback

Post-COVID regulatory pushback

| -0.6% | Global; pronounced in high-income markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Chronic Global API & Finished-Dose Shortages

Persistent shortages of key starting materials jeopardize production continuity, particularly for price-sensitive generics that lack long-term supply contracts. India imports about 70% of its APIs from China, so any cross-border disruption directly affects export commitments. U.S. federal funding to onshore essential medicines aims to dilute this risk, but capacity build-out is a multi-year exercise.

Retinal / Cardiac Toxicity Limiting Long-Term Use

Swept-source OCT-angiography shows thinning and reduced vessel density in patients on therapy beyond five years, enforcing frequent ophthalmic checks that raise total treatment cost. Studies on cardiac conduction yield mixed findings, prompting caution in patients with pre-existing arrhythmic risk. These safety flags temper aggressive prescription growth, especially where monitoring infrastructure is scarce.

Segment Analysis

By Application: Broadening Demand Beyond Malaria

Malaria therapy retained 37.74% of hydroxychloroquine drugs market share in 2025, upheld by endemic transmission across tropical belts and reinforced by WHO policy continuity. Rheumatoid arthritis now registers the highest 9.76% CAGR to 2031 as combination DMARD protocols gain physician acceptance in both high- and middle-income countries. The hydroxychloroquine drugs market size for malaria is forecast to widen steadily yet may cede relative weight as autoimmune prescriptions mount. Systemic lupus and Sjögren syndrome sustain a stable mid-single-digit expansion, aided by fresh evidence of cardiometabolic protection.

Emerging women’s-health indications such as PCOS and hypertensive pregnancy broaden the clinical pipeline and can partly offset seasonal malaria swings. In PCOS, measurable gains in insulin sensitivity and lipid modulation distinguish hydroxychloroquine from metformin, offering an alternative for intolerant patients. Added pregnancy-safety data support off-label uptake despite the absence of formal label revisions, highlighting the drug’s versatility in multidisciplinary care. COVID-19 usage, once a major demand spike, has receded under mixed trial outcomes and tighter authorization rules, leaving a residual niche in small observational protocols.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Institutional Strength Meets E-Commerce Momentum

Hospital pharmacies controlled 45.58% of hydroxychloroquine drugs market revenue in 2025 through bulk purchasing, formulary influence, and mandatory inpatient dispensing procedures. Online pharmacies, however, record a 9.55% CAGR through 2031, reflecting accelerated e-health adoption and direct-to-patient fulfillment enabled by electronic prescriptions. The hydroxychloroquine drugs market size captured by digital vendors may exceed USD 350 billion across all medicines by 2032, signaling long-run disruptive potential.

Regulators demand robust authentication and serialization to counter substandard or falsified supplies, with multi-stakeholder verification programs emerging in the United States and the EU. Retail chains adapt by integrating click-and-collect models and medication counseling services to retain patient loyalty. Manufacturers increasingly negotiate omnichannel supply contracts, balancing the margin stability of institutional tenders with the volume upsides of e-commerce growth.

By Form: Tablets Remain Dominant While Suspensions Climb

Tablets accounted for 61.42% of the hydroxychloroquine drugs market in 2025, favored for cost-efficient mass production and patient familiarity. Yet oral suspensions outpace all other formats at 9.62% CAGR, propelled by pediatric dosing flexibility and geriatric swallowability advantages. The hydroxychloroquine drugs market size for oral liquids is projected to expand appreciably, albeit from a smaller base, as pediatric malaria and juvenile autoimmune therapies seek child-friendly delivery.

Capsules and modified-release microspheres hold niche relevance where taste masking or pharmacokinetic tailoring is essential. Nano-liposomal prototypes under evaluation in North America promise lower systemic exposure and may attract prescribers concerned about cumulative ocular toxicity. Formulation differentiation therefore offers a competitive lever in an otherwise commodity-leaning therapeutic class.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America held 37.86% of global revenue in 2025, reflecting insurance coverage breadth, entrenched generic penetration, and practice guidelines endorsing hydroxychloroquine across diverse autoimmune disorders. Post-pandemic scrutiny temporarily dampened prescription volumes in certain health systems, but FDA re-affirmation of a structured benefit-risk framework coupled with the 2025 priority voucher program sustains clinician confidence. Competitive pricing from Indian generics continues to temper brand premiums, keeping patient out-of-pocket exposure manageable.

Asia-Pacific prints the quickest 9.84% CAGR to 2031, leveraging favorable production economics, rising healthcare expenditure, and supportive industrial policies such as India’s Production Linked Incentive scheme and three new bulk drug parks. India supplies 70% of worldwide output, anchoring regional exports and domestic unmet need simultaneously. China’s National Reimbursement Drug List negotiations saw domestic firms secure 71% of listed innovations in 2024, although heavy price cuts averaging 63% illustrate ongoing affordability pressures. Harmonized regulatory adoption of PIC/S GMP and digital dossier submissions across Southeast Asian markets further lubricates cross-border trade.

Europe posts steady mid-single-digit expansion as synchronized EMA-FDA scientific advice for complex generics compresses filing timelines and costs. State-funded health systems deliver predictable baseline demand, particularly for systemic lupus and rheumatoid arthritis management. The Middle East and Africa, most notably Sub-Saharan zones, sustain antimalarial volume growth as climate change lengthens transmission seasons and intensifies caseloads. Latin America, with Brazil as a primary importer, strikes a balance between domestic production ambitions and reliance on Indian supply lines, cementing a moderate growth outlook through 2030.

Competitive Landscape

Market Concentration

Competition is moderately fragmented: global originators such as Sanofi coexist with high-volume Indian generics including Sun Pharmaceutical, Dr. Reddy’s Laboratories, and Cipla. Generic dispensing rates across therapeutics soared from 54% to 92% between 2002 and 2024, underscoring the commodity nature of the hydroxychloroquine drugs market. Price pressures intensify as multiple ANDA holders capitalize on low entry barriers and expedited approval windows, prompting firms to differentiate on formulation convenience, pharmacovigilance robustness, and supply reliability.

Quality oversight remains pivotal. A 2024 FDA warning letter to Sun Pharmaceutical highlighted CGMP lapses around equipment sanitation and contamination control, illustrating the reputational stakes tied to compliance. Producers demonstrating impeccable audit results can command preferred-supplier status among institutional buyers wary of recalls. Innovation pipelines explore nano-delivery and pediatric suspension variants; although still niche, such upgrades confer pricing headroom relative to standard tablets.

Strategic moves in 2025 include Sanofi partnering with a U.S. telehealth platform to bundle rheumatology consultations with home delivery, while Dr. Reddy’s invested in a blockchain-enabled track-and-trace system covering its entire hydroxychloroquine supply chain to enhance batch-level transparency. WuXi STA’s 2024 Chinese API expansion signals continued Asia-centric scale-based leadership, even as Western reshoring policy nudges attempt to chip away at concentration risk.

Hydroxychloroquine Drugs Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: FDA launched the Commissioner’s National Priority Voucher program, cutting review times to 1-2 months for products tied to U.S. health priorities.

- June 2024: FDA issued a warning letter to Sun Pharmaceutical Industries for significant CGMP infractions.

- February 2024: FDA and EMA opened a Parallel Scientific Advice pilot for complex generics, streamlining dual-agency feedback.

- February 2024: Florida received FDA approval to import prescription medicines from Canada, targeting USD 183 million first-year savings.

Table of Contents for Hydroxychloroquine Drugs Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1High Malaria & Rheumatoid?Arthritis Prevalence

- 4.2.2Burden Of Systemic Lupus & Other Autoimmune Disorders

- 4.2.3Regulatory Fast-Tracking & Generic Approvals

- 4.2.4Expanded Global Manufacturing Capacity & Lower Prices

- 4.2.5Adjunct Therapy Potential in PCOS & Hypertensive Pregnancy

- 4.2.6Nano-Delivery & Formulation Innovations Improving Safety

- 4.3Market Restraints

- 4.3.1Chronic Global API & Finished-Dose Shortages

- 4.3.2Retinal / Cardiac Toxicity Limiting Long-Term Use

- 4.3.3Competitive Biologics & Targeted DMARDs

- 4.3.4Post-COVID Regulatory Pushback & Prescriber Skepticism

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porters Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Application

- 5.1.1Coronavirus Disease (COVID-19)

- 5.1.2Malaria

- 5.1.3Lupus Erythematosus

- 5.1.4Rheumatoid Arthritis

- 5.1.5Polycystic Ovary Syndrome

- 5.1.6Others

- 5.2By Distribution Channel

- 5.2.1Hospital Pharmacy

- 5.2.2Retail Pharmacy

- 5.2.3Online Pharmacy

- 5.3By Form

- 5.3.1Tablet

- 5.3.2Capsules

- 5.3.3Oral Suspension

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East and Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East and Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1Sanofi SA

- 6.3.2Novartis International AG

- 6.3.3Teva Pharmaceutical Industries Ltd

- 6.3.4Viatris (Mylan)

- 6.3.5Sun Pharmaceutical Industries Ltd

- 6.3.6Dr. Reddy's Laboratories Ltd

- 6.3.7Lupin Ltd

- 6.3.8Zydus Lifesciences

- 6.3.9Cipla Ltd

- 6.3.10Laurus Labs Ltd

- 6.3.11IPCA Laboratories Ltd

- 6.3.12Amneal Pharmaceuticals Inc

- 6.3.13Hikma Pharmaceuticals PLC

- 6.3.14Accord Healthcare

- 6.3.15Aurobindo Pharma Ltd

- 6.3.16Jubilant Pharma Ltd

- 6.3.17Advanz Pharma Corp

- 6.3.18Hetero Labs Ltd

- 6.3.19Mangalam Drugs & Organics Ltd

- 6.3.20Cadila Pharmaceuticals Ltd

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Hydroxychloroquine Drugs Market Report Scope

This report forecasts revenue growth at global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2017 to 2025. For the purpose of this study, Mordor Intelligence has segmented the global hydroxychloroquine drugs market report on the basis of disease type, distribution channel, and region.