Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 204.91 Billion |

| Market Size (2031) | USD 256.18 Billion |

| Growth Rate (2026 - 2031) | 4.57% CAGR |

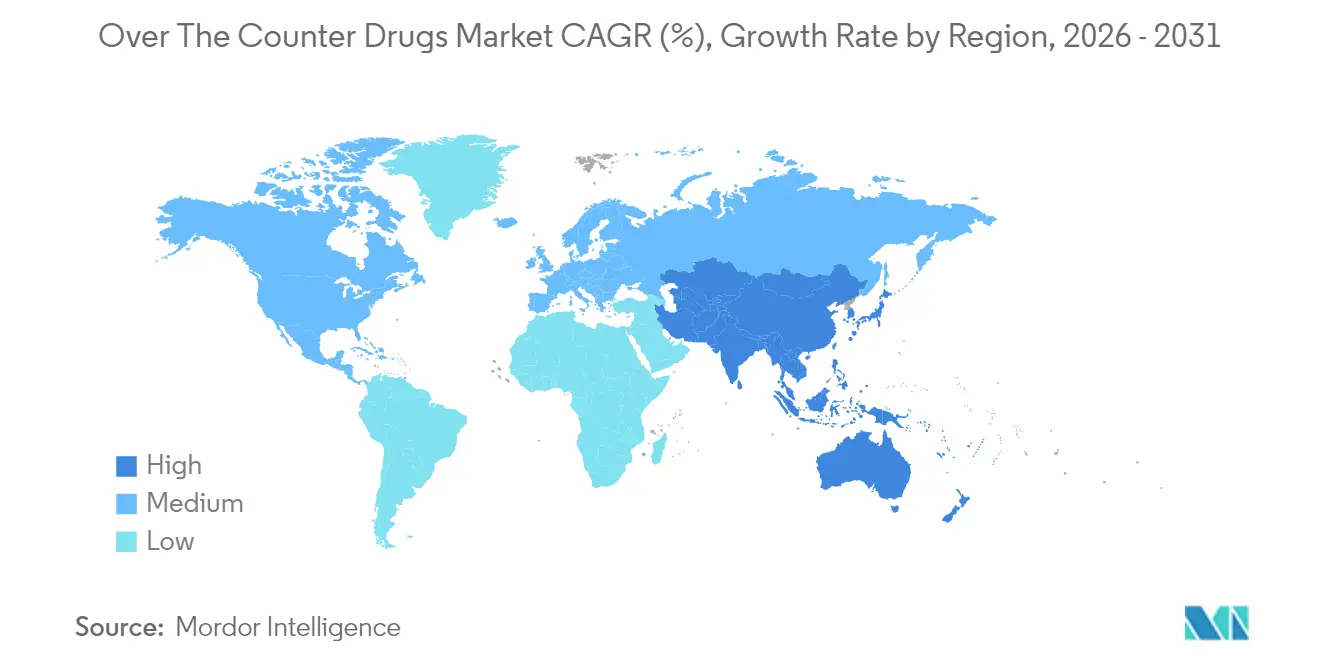

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

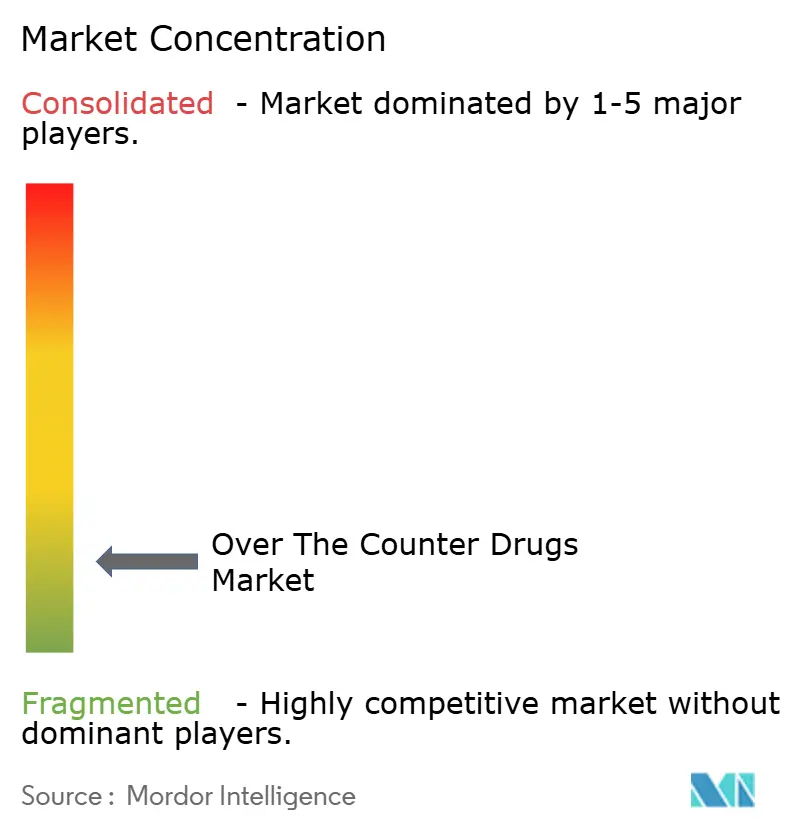

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Over The Counter Drugs Market Analysis by Mordor Intelligence

The over-the-counter (OTC) drugs market size was valued at USD 195.96 billion in 2025 and estimated to grow from USD 204.91 billion in 2026 to reach USD 256.18 billion by 2031, at a CAGR of 4.57% during the forecast period (2026-2031). Steady expansion rests on consumers’ increasing willingness to self-treat minor ailments, a trend that lightens the burden on primary-care systems and rewards companies able to simplify decision-making at the shelf. Regulatory agencies are continuing to relax rules that once kept complex molecules in prescription-only channels, inviting manufacturers to rethink end-of-life strategies for mature brands and to weave digital self-selection tools into product launches. Investment is also tilting toward dosage formats that feel more like daily wellness rituals, gummies, chewables, and patches, because taste and convenience now sit alongside efficacy when shoppers weigh options. With counterfeit risk still high in parts of Asia, brand owners are pairing track-and-trace technology with community education to protect trust, while retailers in North America and Europe fine-tune omnichannel models that merge doorstep delivery with real-time pharmacist guidance.

Key Report Takeaways

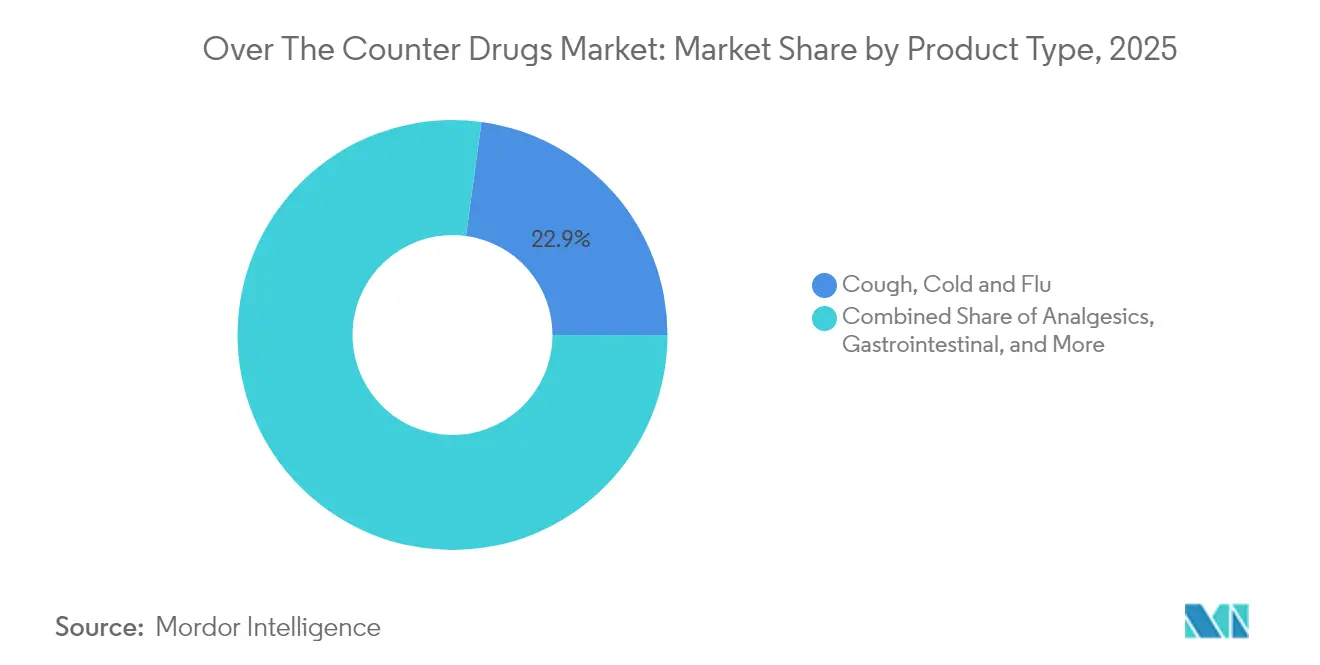

- By product type, cough, cold and flu remedies held a 22.85% revenue share in 2025, whereas vitamins, minerals and supplements are projected to advance at a 7.52% CAGR through 2031.

- By formulation type, tablets dominated with 38.25% of sales in 2025; gummies and chewables are the fastest-growing format at a 9.35% CAGR to 2031.

- By distribution channel, retail chain pharmacies captured 41.95% of turnover in 2025, while online pharmacies are expanding at a 9.95% CAGR over the forecast period.

- By age group, adults (15-64) accounted for 63.40% of over-the-counter drugs market size in 2025, and the geriatric segment (65+) is growing quickest at an 8.16% CAGR.

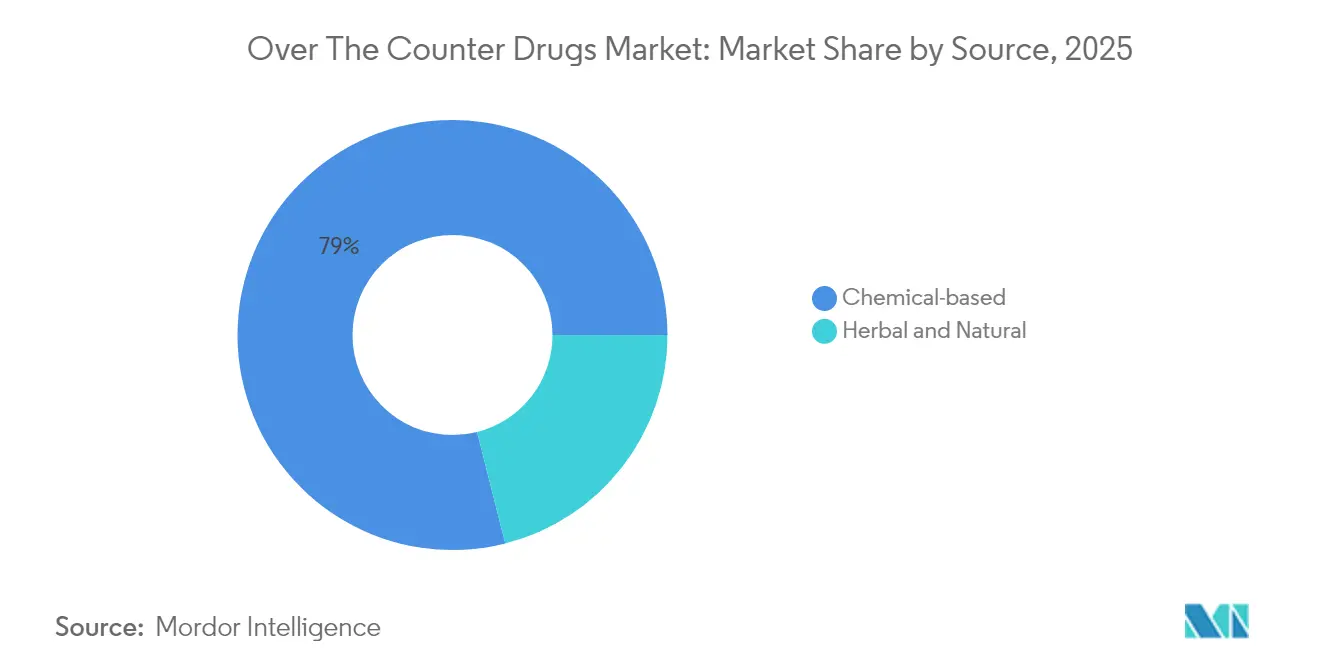

- By source, chemical-based products retained 78.95% over-the-counter (OTC) drugs market share in 2025; herbal and natural alternatives show the strongest momentum with a 8.88% CAGR through 2031.

- By geography, North America led with 34.55 % of global revenue in 2025, whereas Asia-Pacific is set to register the highest regional CAGR at 8.31 % to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Over The Counter Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Preference for Self-Care and Preventive Health | +1.8% | Global, with stronger effect in North America & Western Europe | Medium term (2-4 years) |

| Continued Rx-to-OTC Switches Across Multiple Therapeutic Classes | +1.2% | North America & EU, with delayed adoption in emerging markets | Long term (≥ 4 years) |

| Proliferation of Digital & Omnichannel Pharmacy Platforms | +0.9% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Liberalization of Pharmacy & Drug Retail Regulations in Developing Economies | +0.7% | APAC, Africa, and Latin America | Medium term (2-4 years) |

| Rapidly Ageing Population Elevating Demand for Chronic OTC Management | +1.0% | Japan, Western Europe, North America, China | Long term (≥ 4 years) |

| Post-Pandemic Focus on Respiratory & Immunity Products | +1.1% | Global, with higher intensity in regions with severe COVID-19 impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Preference For Self-Care And Preventive Health

81% of consumers now turn to an OTC product as the first response to minor ailments, according to Pfizer disclosures. The behavioral shift is large enough to reduce physician footfall for common conditions, which in turn changes prescribing habits: physicians increasingly frame OTC use as an essential component of step-therapy protocols to reserve prescription interventions for higher-acuity needs. An interesting derivative effect is that payers quietly welcome the trend, because every OTC dollar spent introduces a private out-of-pocket contribution that relieves reimbursement budgets, a dynamic that rebalances cost pressures without new legislation.

Continued Rx-to-OTC Switches

The United States Food and Drug Administration (FDA) codified the Additional Conditions for Nonprescription Use (ACNU) rule in January 2025, opening the gate for products with nuanced safety profiles to migrate into OTC status. More than 700 individual products have crossed the prescription wall, notes the Consumer Healthcare Products Association (CHPA). An under-appreciated consequence is that life-cycle management teams now view Rx-to-OTC migration as a mainstream strategic lever alongside patent-extension tactics, effectively lengthening commercial tailwinds for mature molecules without repurposing or reformulating them.

Digital and Omnichannel Pharmacy Proliferation

Academic research in Japan shows that although 89 % of consumers still purchase OTC medicines in stores, nearly one in ten buys online while consulting a smartphone for supplementary information. This hybrid pattern indicates that the “research online, purchase offline” model is morphing into a “research everywhere, purchase anywhere” reality. Retail chains are responding by embedding quick-response codes on shelf tags to integrate digital content at the point of sale, a move that quietly shifts the store from a transactional venue to a content-amplification node[1]Guyue Tang et al., “Analysis of Japanese Consumers' Attitudes Toward the Digital Transformation of OTC Medicine Purchase Behavior and eHealth Literacy,” Frontiers in Digital Health, frontiersin.org.

Liberalization of Pharmacy and Drug-retail Regulations in Developing Economies

India and China are rolling out reforms that allow non-pharmacy outlets to stock select OTC lines, a policy stance mirrored in South Korea where convenience-store availability has squeezed price points and dented traditional pharmacy revenue. For manufacturers, this regulatory looseness multiplies distribution nodes but also fragments inventory management, forcing investments in data-rich demand-sensing platforms. A counterintuitive upside emerges for smaller brands: wider channels reduce shelf-space barriers, letting agile entrants secure visibility in outlets historically reserved for legacy incumbents.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit & Substandard Products Undermining Brand Trust in Emerging Markets | -0.8% | APAC, Africa, and parts of Latin America | Medium term (2-4 years) |

| Price Erosion from Intensifying Retail Competition & Private-Label Expansion | -1.2% | Global, with stronger effect in mature markets | Medium term (2-4 years) |

| Safety Concerns over Misuse and Adverse Events Limiting Category Expansion | -0.6% | Global, with higher impact in regions with limited pharmacist access | Short term (≤ 2 years) |

| Tightening Regulatory Surveillance and Track-and-Trace Mandates Increasing Compliance Costs | -0.9% | Global, with earlier implementation in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Substandard Products Undermining Brand Trust

The National Association of Boards of Pharmacy estimates that 96% of online pharmacy sites operate out of compliance. This proliferation fuels a parallel market that erodes legitimate brand equity and, by extension, patient adherence. At a strategic level, the counterfeit threat propels legitimate players toward blockchain-based track-and-trace solutions, even when regulators have not yet mandated them. Early adopters may therefore secure a two-fold benefit: supply-chain integrity and marketing leverage built on verified authenticity.

Price Erosion from Intensifying Retail Competition and Private-label Expansion

Liberalized sales channels have triggered price compression, particularly where mass-merchandisers introduce private-label SKUs that replicate branded formulations. For national brands, the remedy increasingly lies in value-added differentiation—be it a quicker onset of action, a cleaner excipient profile, or app-linked adherence nudges. The implicit insight is that the OTC brand manager’s skill set now straddles classical FMCG tactics and med-tech fluency, a hybrid capability that was rare even five years ago.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: VMS Outpaces Traditional Categories

Cough, cold, and flu remedies retain the largest slice of market share at 22.85% in 2025, yet vitamins, minerals, and supplements (VMS) clock a 7.52% CAGR for 2026-2031, the fastest within the matrix. The trend reflects post-pandemic immunity consciousness and a broader pivot from treatment to prevention. A notable inference is that VMS branding increasingly centers on functional outcomes such as “sleep quality” or “stress balance,” mimicking the precision-messaging language long used in the tech sector to articulate user benefits rather than technical specs.

Manufacturers are increasingly focusing on condition-specific formulations that target emerging consumer concerns such as stress management, sleep quality, and cognitive performance, creating differentiated positioning in an increasingly crowded marketplace.

By Formulation Type: Tablets Remained the Dominant Dosage Format

Tablets still account for 38.25% of the market in 2025, but gummies and chewables expand at 9.35% CAGR. The adhesion of confectionery formats to healthcare illustrates how sensory experience can dislodge entrenched dosage forms. Manufacturers now invest in gelatin-free plant bases and reduced sugar profiles to appeal to health-conscious adults, not just children. This pivot underlines a strategic insight: taste and texture are becoming table-stakes product attributes, erasing the historical divide between therapeutic efficacy and consumer indulgence.

The innovation pipeline for OTC formulations continues to expand, with transdermal patches gaining traction for consistent drug delivery and orally disintegrating formats addressing swallowing difficulties in pediatric and geriatric populations.

By Age Group: Adults Aged 15-64 Accounted for Major Share

Adults aged 15-64 years hold 63.40% of consumption in 2025, but seniors expand fastest at 8.16% CAGR for 2026-2031. Various sources highlighted the polypharmacy drag that complicates OTC selection for older adults. In response, some retailers are piloting shelf placements that cluster geriatric-friendly SKUs, mimicking grocery “free-from” aisles that cluster allergen-safe products. This merchandising tweak not only improves navigation for seniors but also raises the category’s average ticket value thanks to bundled offerings.

The aging population presents unique challenges for OTC manufacturers, as approximately 80% of older adults have multiple chronic conditions, leading to complex medication regimens that increase the risk of adverse drug interactions.

By Source: Natural Products Gain Mainstream Traction

Natural products gain mainstream traction. Chemical-based OTC products dominate with 78.95% share in 2025, yet herbal and natural alternatives are sprinting ahead at 8.88% CAGR. The trend is creating integration challenges for healthcare systems, as 77.8% of consumers in some markets use herbal preparations, often alongside conventional medications, creating potential interaction risks.

Significant interactions have been identified with common herbal products like grapefruit, St. John's wort, and valerian, which can lead to serious adverse effects when combined with certain conventional medications. This underscores the need for enhanced consumer education and healthcare provider awareness regarding herbal-drug interactions, particularly for patients with chronic conditions who frequently use multiple medications.

By Distribution Channel: Digital Disruption Reshapes Access

Digital disruption reshapes access. Retail chain pharmacies commanded 41.95% market share in 2025. However, online players, growing at 9.95% CAGR, blur the channel demarcation. Traditional chains counter with same-day delivery and in-app counseling, effectively turning pharmacists into virtual care navigators. The secondary effect is that prescription units inside these chains experience cross-sell uplift when OTC shoppers engage digitally, validating omnichannel as a revenue amplifier rather than cannibalizing force.

Traditional pharmacy retailers are responding with omnichannel strategies that integrate digital and physical experiences, while pure-play online pharmacies are differentiating through competitive pricing, subscription models, and enhanced medication management tools.

Geography Analysis

Market share leadership at 34.55% in 2025 is underpinned by high out-of-pocket costs that foster self-medication, robust pharmacy chains, and a favorable regulatory climate for Rx-to-OTC switches. The FDA’s ACNU framework, operational since January 2025, allows digital tools to guide self-selection for more complex molecules, a policy shift that effectively converts software into a regulatory compliance mechanism. This dynamic nudges tech partners into the core of drug-commercialization strategies.

At an 8.31% CAGR, Asia-Pacific represents the fastest-growing regional chunk through 2031, driven by rising disposable income and growing middle-class aspirations. China’s National Medical Products Administration lists more than 5,000 registered OTC products, including over 800 switches from prescription status. The sharpening competitive stakes spur multinational firms to localize not just packaging language but also dose strengths aligned with regional clinical guidelines—an adaptation that historically lagged behind marketing localization.

Most jurisdictions permit online sales and refrain from price controls, yet many still restrict non-pharmacy retail to safeguard dispensing oversight. The fragmented rulebook obliges manufacturers to maintain country-specific SKU variants, which inflates inventory complexity but allows micro-targeted marketing claims attuned to local health concerns. A sophisticated takeaway emerges: agile supply chains that use postponement strategies, delaying final packaging until country allocation, is now a material competitive advantage in Europe.

Competitive Landscape

The top five companies in the market command around 16% of revenue. Such fragmentation means that brand equity, rather than scale, often decides shelf presence. Corporate maneuvering reinforces this view: GSK de-merged its Haleon consumer unit, and Johnson & Johnson spun off Kenvue, both actions designed to give consumer-health agendas strategic autonomy. Interestingly, the separation trend democratizes R&D budgets, because newly independent entities can allocate capital directly to OTC opportunities without competing for funding against high-margin prescription pipelines.

Petros Pharmaceuticals’ AI-enabled SaaS platform mines electronic health records to identify molecules fit for Rx-to-OTC transition, accelerating dossier preparation and regulatory engagement. The platform illustrates how software intellectual property can insert itself upstream in pharmaceutical value chains, not just in downstream marketing or adherence apps. Forward-looking firms treat such tools as acquisition targets rather than optional collaborators, portending a future where tech scouting becomes a core BD function.

The geriatric segment remains under-served, especially for polypharmacy management. Few OTC SKUs incorporate pill-splitting lines, large-font instructions, or blister packs with tactile cues. Companies that solve these ergonomic pain points can capture loyalty in a demographic that values reliability over novelty, converting what was once niche user-experience work into a measurable revenue stream.

Over The Counter Drugs Industry Leaders

Bayer AG

Haleon Group

Sanofi S.A.

Reckitt Benckiser Group plc

Kenvue Brands LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Glenmark Pharmaceuticals received FDA approval for olopatadine hydrochloride ophthalmic solution 0.2 % as an OTC product.

- May 2024: Amneal Pharmaceuticals began supplying OTC naloxone 4 mg nasal spray to U.S. retail chains, illustrating how public-health imperatives can accelerate market entry for harm-reduction products.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the over-the-counter drugs market as all non-prescription, regulator-approved pharmaceutical products that consumers may self-select for prevention or treatment of minor conditions through pharmacies, supermarkets, convenience stores, and licensed online platforms worldwide. Products span analgesics, cough and cold remedies, gastro-intestinal aids, dermatology preparations, vitamins, minerals, and supplements.

Scope exclusion: Herbal teas, homeopathic remedies, sports nutrition powders, and any product marketed solely as a cosmetic are left outside our sizing.

Segmentation Overview

- By Product Type

- Cough, Cold & Flu

- Analgesics

- Gastrointestinal

- Dermatology

- Vitamins, Minerals & Supplements (VMS)

- Weight Management

- Ophthalmic

- Sleep Aids

- Oral Care

- Smoking Cessation

- Antihistamines / Allergy

- Ear Care

- Wound Care

- Other Products

- By Formulation Type

- Tablets

- Capsules & Softgels

- Liquids & Syrups

- Powders & Granules

- Ointments & Creams

- Sprays & Inhalers

- Gummies & Chewables

- Transdermal Patches

- By Distribution Channel

- Hospital Pharmacies

- Retail Chain Pharmacies

- Independent Pharmacies & Drugstores

- Online Pharmacies

- Other Channels

- By Age Group

- Pediatrics (0-14 yrs)

- Adults (15-64 yrs)

- Geriatrics (65+ yrs)

- By Source

- Chemical-based

- Herbal & Natural

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with pharmacy chains, national regulators, ingredient suppliers, and consumer-health clinicians across North America, Europe, Asia-Pacific, Latin America, and the Middle East. These discussions validated pricing swings, online penetration, and the pace of Rx-to-OTC switches, while structured surveys in multiple languages clarified purchase frequency and typical basket spend.

Desk Research

We began with official statistics such as US FDA OTC Monograph databases, the European Medicines Agency's Union Register, and Japan's PMDA switch lists, which clarify how many active substances qualify for self-care use. Trade associations, including CHPA, AESGP, and Consumer Health Products Canada, supplied retail sales audits and policy updates. Additional insights came from public company filings, select press releases, and paid datasets inside D&B Hoovers and Dow Jones Factiva that flag brand revenues and channel splits. A wide range of other open-source and subscription references was reviewed to cross-check every datapoint.

Desktop sources outlined the historical demand arc, yet they seldom disclose net-of-rebate values or online pharmacy volumes, prompting us to lean on primary work for those gaps.

Market-Sizing & Forecasting

A top-down retail expenditure rebuild drew on country level per-capita OTC spend, number of pharmacy outlets, and average transaction values, followed by selective bottom-up checks using sampled SKU volumes multiplied by weighted average selling prices. Key variables feeding our multivariate regression include annual Rx-to-OTC switch count, e-pharmacy share, cold-and-flu incidence, consumer price index for medicines, and median household income. Where retailer data were missing, interpolation relied on three-year trend lines anchored to known switch events.

Data Validation & Update Cycle

Outputs run through variance scans versus import-export records, household survey signals, and listed company revenue guides. Senior reviewers sign off after reconciling anomalies. Reports refresh once a year, with interim updates triggered by significant regulatory or demand shocks so clients always receive the newest view.

Why Mordor's Over the Counter Drugs Baseline Numbers Merit Confidence

Published figures for this market often differ because firms pick dissimilar product baskets, channel mixes, and currency assumptions. We show in plain sight which segments count and apply one refresh cadence, thereby letting decision makers trace every step.

Key gap drivers include whether vitamins are bundled, if dietary supplements are merged, and how online pharmacy mark-ups are handled. Currency conversions and forecast horizons introduce extra divergence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 195.96 Bn (2025) | Mordor Intelligence | |

| USD 180.1 Bn (2024) | Global Consultancy A | Omits vitamins and minerals segment |

| USD 262.8 Bn (2024) | Research Publisher B | Combines OTC drugs with dietary supplements |

| USD 158.26 Bn (2024) | Industry Journal C | Tracks retail pharmacy sales only, excludes online and convenience stores |

Together, these contrasts show why our disciplined scope selection and annual renewal create a balanced, transparent baseline that clients can replicate and sensibly debate.

Key Questions Answered in the Report

What is the projected global OTC drugs market size by 2031?

The market is forecast to reach USD 256.18 billion by 2031, reflecting a 4.57 % CAGR from 2026 levels.

Which region is expected to grow fastest in the OTC sector through 2031?

Asia-Pacific, propelled by an 8.31 % CAGR, is poised to be the fastest-growing regional market due to rising middle-class purchasing power and regulatory openness.

How significant is the shift toward digital sales channels for OTC products?

Online pharmacies are expanding at a 9.95% CAGR, more than double traditional retail growth, signaling an irreversible pivot toward omnichannel consumer engagement.

Why are gummies and chewables gaining traction in OTC formulations?

Their 9.35 % forecast CAGR stems from improved palatability and convenience, which drive adherence, particularly in vitamins, minerals, and supplements.

What is the strategic importance of the FDA’s ACNU rule?

The rule enables complex prescription medicines to transition to OTC status by leveraging digital self-selection tools, effectively enlarging the addressable market without compromising safety.

How are counterfeit OTC products affecting the industry?

They erode consumer trust and compress margins for legitimate brands, prompting manufacturers to invest in blockchain-based verification and authenticated supply chains to preserve market integrity.

Page last updated on: