Global Barbiturate Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

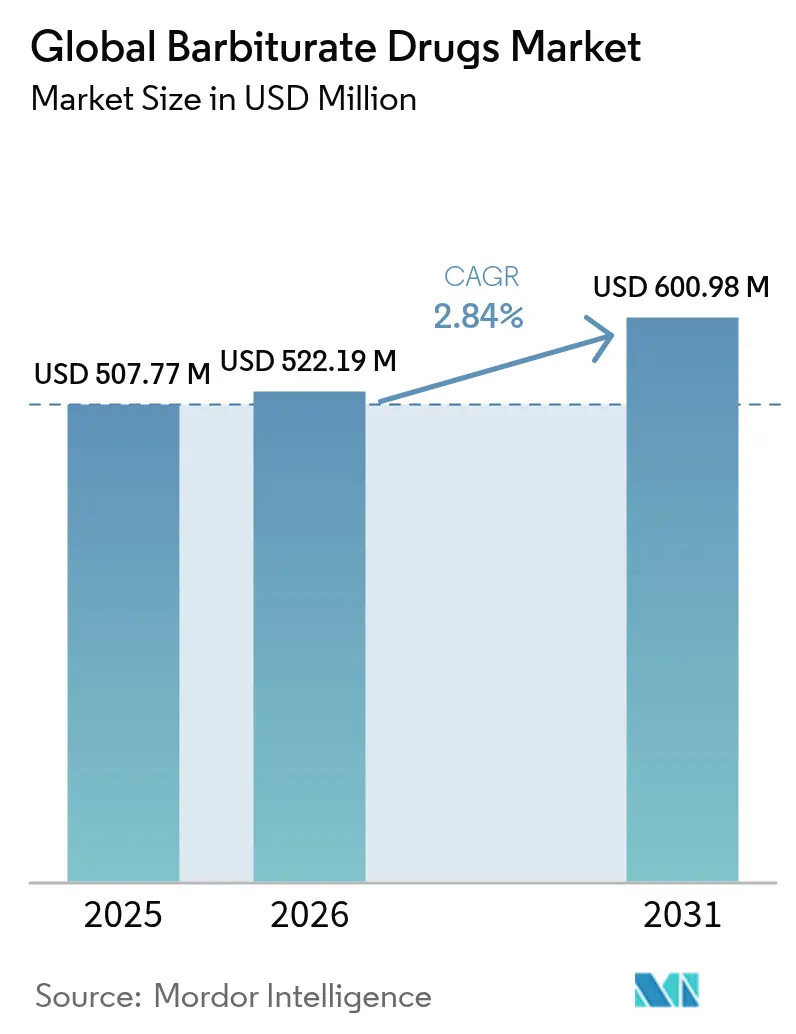

| Market Size (2026) | USD 522.19 Million |

| Market Size (2031) | USD 600.98 Million |

| Growth Rate (2026 - 2031) | 2.84% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Barbiturate Drugs Market Analysis by Mordor Intelligence

Barbiturate market size in 2026 is estimated at USD 522.19 million, growing from 2025 value of USD 507.77 million with 2031 projections showing USD 600.98 million, growing at 2.84% CAGR over 2026-2031. Ongoing demand for rapid-onset sedatives in critical care, widening generic production in Asia, and neonatal approvals such as Sun Pharma’s Sezaby continue to uphold global consumption despite intensifying regulatory pressures favoring benzodiazepine alternatives. Rapid-sequence intubation protocols, the resilience of phenobarbital in drug-resistant epilepsy, and targeted innovation in ultra-short-acting formulations sustain market relevance as healthcare systems prioritize proven, cost-effective therapies in high-acuity settings. Concurrently, intravenous delivery advances, AI-enabled dosing, and upgraded compounding rules create new operational lanes for manufacturers and hospital pharmacies.

Key Report Takeaways

- By application, epilepsy treatments held 46.15% of the barbiturate market share in 2025, while insomnia therapies are projected to clock the fastest 4.86% CAGR through 2031.

- By drug type, long-acting compounds commanded 38.75% of the barbiturate market size in 2025, whereas ultra-short-acting formulations will post the highest 4.12% CAGR to 2031.

- By route of administration, oral products dominated with a 58.20% share of the barbiturate market size in 2025, yet intravenous options will accelerate at 5.55% CAGR over 2026-2031.

- By distribution channel, hospital pharmacies retained 53.10% revenue share in 2025, and online pharmacies are poised for a 6.62% CAGR despite tight DEA oversight.

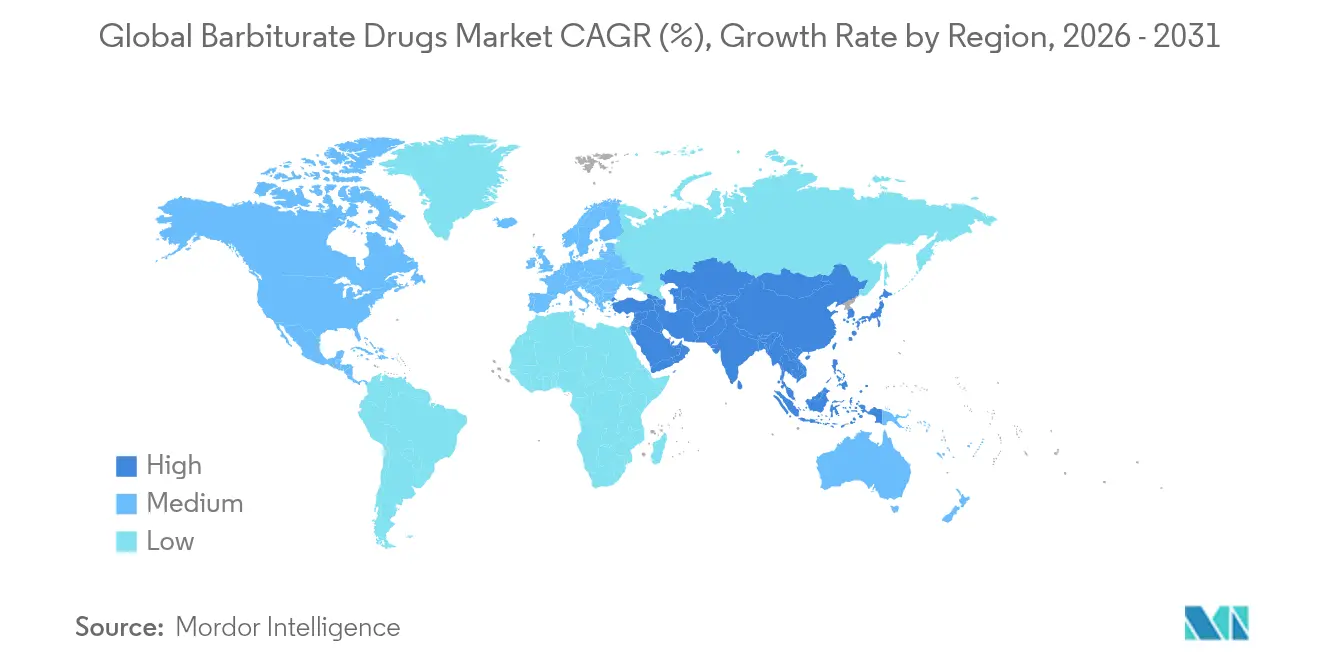

- By geography, North America led with 41.70% barbiturate market share in 2025; Asia-Pacific presents the quickest 7.75% CAGR to 2031 on the back of surging generic capacity in India and China.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Barbiturate Drugs Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of drug-resistant epilepsy | +0.8% | North America & Europe | Medium term (2-4 years) |

| Growing use of phenobarbital in neonatal care protocols | +1.2% | Developed health systems worldwide | Short term (≤ 2 years) |

| Demand for rapid-onset anesthetics in emergent surgeries | +0.6% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Uptick in medically-induced coma procedures for TBI | +0.4% | Global trauma centers | Long term (≥ 4 years) |

| Surging low-cost generic production in India & China | +0.3% | APAC core, global export reach | Long term (≥ 4 years) |

| AI-guided drug-screening panels boosting phenobarbital demand | +0.2% | North America & Europe first, global later | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Drug-Resistant Epilepsy

Roughly 30% of patients with epilepsy remain refractory to first-line antiepileptic drugs, sustaining a dependable demand pool for phenobarbital and related compounds. The International League Against Epilepsy reinforces phenobarbital’s role for refractory seizures, especially where cost containment steers formulary choices. Randomized trials show 24-hour seizure freedom in 80% of phenobarbital-treated refractory cases versus 28% for levetiracetam, sharpening clinicians’ focus on time-tested GABA-ergic agents in critical episodes. Precision medicine also favors the barbiturate market as genetic sub-groups with preferable response profiles are increasingly identified through next-generation sequencing. As treatment algorithms mature, barbiturates retain a solid footing in resource-limited health systems and tertiary epilepsy centers alike.

Growing Use of Phenobarbital in Neonatal Care Protocols

The 2024 FDA approval of Sezaby marked the first neonatal-specific phenobarbital formulation, cementing its primacy in treating neonatal seizures. Comparative trials show superior seizure control relative to levetiracetam despite elevated respiratory-monitoring requirements, prompting NICUs to formalize phenobarbital-centric algorithms. Cost advantages of generic phenobarbital further bolster adoption in middle-income countries where neonatal intensive care is scaling rapidly. As protocol adherence improves, hospital purchase orders for injectable phenobarbital have risen, supporting predictable barbiturate market demand. Real-world data are now integrated into AI-driven dosing dashboards, refining therapeutic windows in vulnerable newborns.

Demand for Rapid-Onset Anesthetics in Emergent Surgeries

Emergency rooms increasingly rely on ultra-short-acting barbiturates like methohexital for rapid sequence intubation amid global thiopental shortages, creating fresh growth niches. Trauma surgeons value barbiturates’ cardiovascular stability versus propofol in hypotensive patients, while anesthesiologists cite smoother emergence profiles essential for outpatient recovery. AI-backed perioperative systems model methohexital kinetics to finetune dose-response curves, reinforcing barbiturate utilization in protocol-driven surgical centers. These data-guided improvements continue to broaden acceptance across APAC where high-acuity surgical capacity is rising.

Uptick in Medically-Induced Coma Procedures for TBI

Pentobarbital remains the sedative of choice when intracranial pressure exceeds threshold after standard interventions fail, particularly in neurotrauma hubs worldwide. Evidence-based guidelines underscore barbiturates’ metabolic suppression benefits, sustaining procurement contracts in military and civilian trauma units. Enhanced multimodal neuromonitoring enables precise titration, reducing adverse event rates and extending barbiturate applications beyond legacy indications. The cumulative effect is a steady demand curve within the barbiturate market among tertiary care institutes.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push toward benzodiazepine substitution | -0.7% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Narrow therapeutic index driving malpractice premiums | -0.5% | North America & Europe primarily | Medium term (2-4 years) |

| Global thiopental API shortages after GMP plant closures | -0.4% | Global, acute impact in North America & Europe | Short term (≤ 2 years) |

| Growing payor restrictions on Schedule II sedatives | -0.6% | North America primarily, expanding to Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push Toward Benzodiazepine Substitution

DEA scheduling places most barbiturates in Schedule II, subjecting clinicians to stricter log-keeping and inventory audits than for Schedule IV benzodiazepines. Major insurers require prior authorizations, adding administrative overhead that dissuades routine barbiturate prescribing. Updated guidelines from anesthesiology and psychiatry societies further cement benzodiazepines as first-line, squeezing short-term barbiturate volume. Despite recognized niche value, administrative drag and shifting formularies temper near-term adoption rates.

Narrow Therapeutic Index Driving Malpractice Premiums

Barbiturates’ tight efficacy-toxicity range prompts higher malpractice premiums for heavy prescribers, driving cost-sensitive departments toward alternatives. Pharmacovigilance databases show elevated respiratory depression events relative to newer sedatives, reinforcing insurer caution. Coupled with training and monitoring requirements, these factors elevate total cost of care, moderating growth momentum for the barbiturate market in general hospital settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Ultra-Short-Acting Formulations Drive Innovation

Long-acting compounds retained 38.75% share of the barbiturate market size in 2025, reflecting their cornerstone role in epilepsy and chronic sedation. Yet ultra-short-acting versions are charting a 4.12% CAGR owing to their utility in emergent anesthesia and rapid sequence intubation. Methohexital’s swift onset and offset enable same-day discharge, reducing bed occupancy and improving cost metrics for ambulatory surgery centers. Growth is further lifted by process patents covering solubilizing excipients that improve stability and diminish pain on injection. Short-acting and intermediate-acting variants maintain mid-tier positions, servicing specific neurosurgical and psychiatric needs where duration balance matters.

Clinicians gravitate toward pharmacokinetic predictability, a trait amplified in ultra-short-acting iterations that dovetail with real-time anesthesia depth monitors. At the same time, the sustained demand for long-acting agents in refractory epilepsy ensures a resilient revenue base within the barbiturate market. Manufacturers therefore pursue portfolio breadth, producing both depot and flash-acting SKUs, hedging against therapeutic shifts while capturing emerging procedure-driven sales.

By Application: Epilepsy Dominance Faces Insomnia Growth Challenge

Epilepsy protocols anchored 46.15% of barbiturate market share in 2025, a testament to phenobarbital’s longevity in seizure control. However, insomnia accounts are beginning to swell at a 4.86% CAGR as sleep specialists revisit barbiturate efficacy for therapy-resistant cases. Renewed clinical interest is fed by real-world reports of improved sleep architecture in psychiatric comorbidity populations versus non-barbiturate hypnotics. Pre-operative sedation remains a dependable mid-volume segment, with surgeons valuing titratable depth under hemodynamically fragile conditions. Medically induced comas, though comparatively niche, deliver consistent high-value demand tied to neurocritical care centers where lives hinge on strict intracranial pressure management.

This pluralistic demand profile fortifies the barbiturate market against abrupt downturns, ensuring that pressure on one indication does not derail overall revenue trajectories. Insomnia-related uptake also spurs formulation R&D, with micro-granulated oral dispersible tablets entering late-stage development.

By Route of Administration: Intravenous Delivery Accelerates

Oral formulations dominated 58.20% of barbiturate market size in 2025, reflecting historical outpatient epilepsy use. Intravenous formats, however, will outpace at a 5.55% CAGR as critical care and emergency medicine lean on rapid bioavailability. Hospitals appreciate programmable syringe pumps that harmonize with closed-loop sedation algorithms, minimizing overshoot risks. Regulatory clarity around bulk compounding under Section 503B now permits outsourcing facilities to fill interim shortages of sterile barbiturate injectables.

The shift also dovetails with tele-ICU programs, where remote intensivists adjust infusion rates via integrated platforms. Manufacturers that provide tamper-evident, bar-coded vials gain bidding advantages in centralized procurement auctions, reinforcing intravenous product momentum inside the barbiturate market.

By Distribution Channel: Online Pharmacies Navigate Regulatory Complexity

Hospital pharmacies accounted for 53.10% revenue in 2025, anchored by inpatient utilization under strict stewardship protocols. Online pharmacies, although subject to Drug Enforcement Administration reporting, are advancing at 6.62% CAGR thanks to streamlined e-prescribing and direct-to-patient refill services. Digital platforms leverage two-factor authentication and real-time PDMP checks, assuring regulators of compliance. Retail outlets sustain moderate throughput, balancing chronic epilepsy scripts with rising prior-authorization workloads.

The widening omnichannel architecture brings convenience for stable outpatient populations while ensuring acute care facilities retain command over high-risk intravenous stock. This blended approach helps insulate the barbiturate market from single-channel supply disruptions and aligns with consumer expectations for integrated care pathways.

Geography Analysis

North America exerted 41.70% control of the global barbiturate market in 2025, bolstered by advanced neurotrauma centers, robust payer frameworks, and calibrated DEA production quotas that secure medicinal access while curtailing diversion. Hospitals routinely deploy barbiturate coma therapy in severe TBI, a practice embedded in Level I trauma guidelines. Canadian provinces similarly maintain phenobarbital on restricted formularies for cost-efficient epilepsy control, underpinning consistent regional procurement.

Asia-Pacific is slated for an 7.75% CAGR, driven by India’s active pharmaceutical ingredient dominance and China’s scale manufacturing prowess, both endorsed by successful USFDA audits that unlock Western market channels. Expanded health-insurance schemes across Southeast Asia further stimulate demand for economical seizure medication in rural clinics. Meanwhile, tertiary hospitals in Korea and Japan are incorporating ultra-short-acting barbiturates into anesthesia bundles, diversifying regional consumption drivers.

Europe shows measured expansion under unified EMA oversight that expedites mutual recognition of barbiturate dossiers, maintaining patient access within stringent pharmacovigilance frameworks. Germany and France display modest uptake in insomnia off-label uses under specialist supervision. South America and the Middle East & Africa trail but reveal upside as surgical capacity and neurocritical care capabilities mature; multilateral aid projects often include phenobarbital in essential-drug packages, laying foundations for broader barbiturate market penetration.

Competitive Landscape

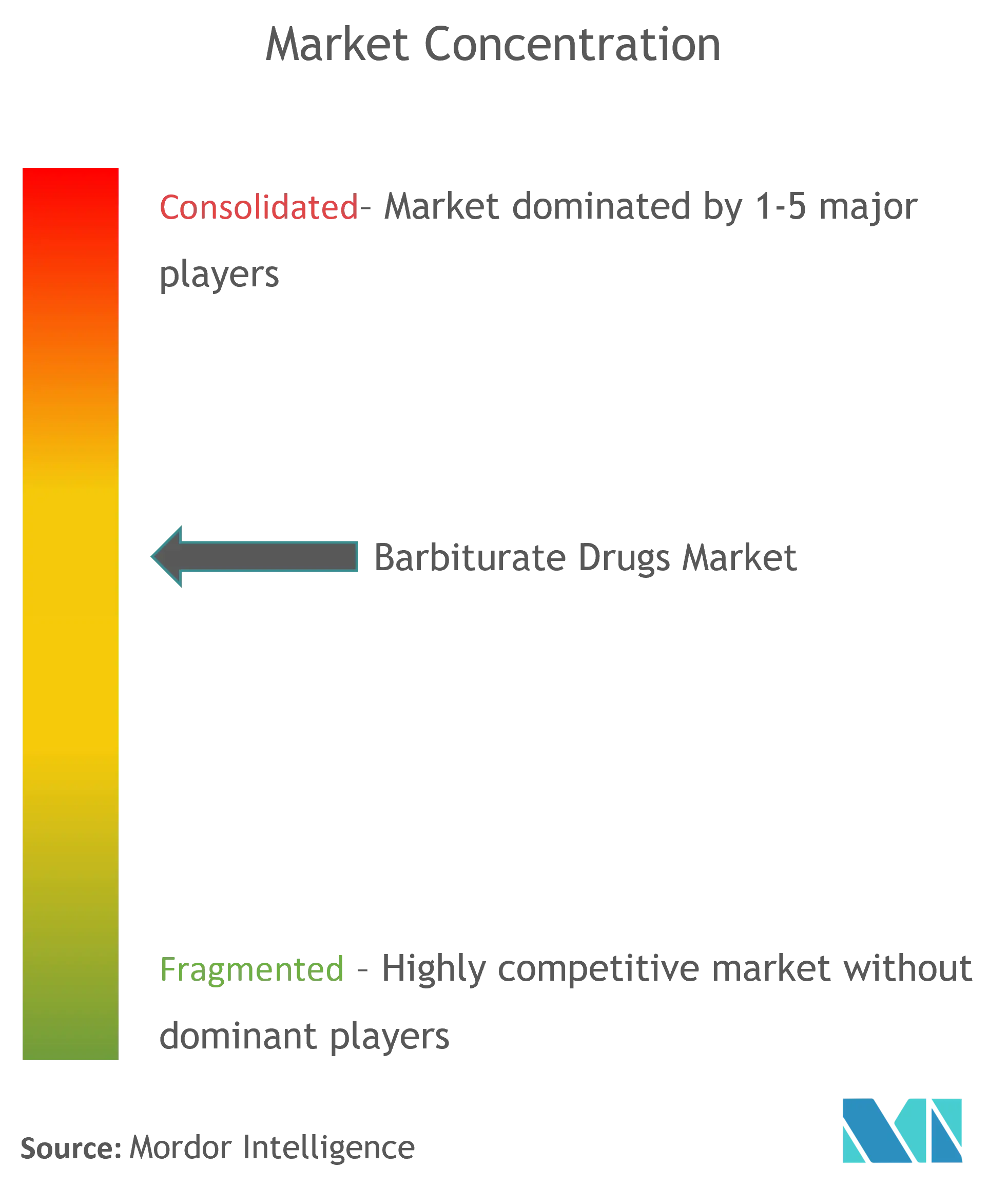

The barbiturate market portrays moderate fragmentation with multinational innovators sitting beside cost-focused generic houses. Pfizer, Eli Lilly, and Sanofi capitalize on legacy molecules and global distribution reach, whereas Teva, Hikma, and Dr. Reddy’s supply price-sensitive geographies with high-volume generics. Vertical integration is pronounced: manufacturers invest in upstream API plants to guard against supply shocks, a lesson underscored during recent thiopental shortages.

Competitive thrust now centers on sterile manufacturing excellence and data-rich post-marketing surveillance. Firms that align ESG targets with WHO environmental thresholds gain procurement leverage among hospital groups adopting sustainability scorecards. The advent of AI-directed dosing support tools offers another differentiator; vendors bundling software decision aids with drug supply enhance clinician confidence and secure formulary preference. Despite pricing headwinds, sustained clinical indispensability in select protocols keeps revenue floors intact for committed players within the barbiturate industry.

Global Barbiturate Drugs Industry Leaders

Par Pharmaceutical

Akorn Operating Company LLC

Samarth Life Science Pvt. Ltd

Ethypharm

Abbott

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: FDA finalized interim policies allowing 503B outsourcing facilities more flexibility in compounding injectable barbiturates during supply disruptions

- December 2024: DEA set 2025 aggregate production quotas for Schedule II substances, including barbiturates, balancing medical needs with diversion prevention

Global Barbiturate Drugs Market Report Scope

Barbiturates are a group of sedative-hypnotic medications used for the treatment of seizure disorder, neonatal withdrawal, insomnia, preoperative anxiety, and induction of coma for increased intracranial pressure. They are also useful for inducing anesthesia. The Barbiturate Drugs Market is segmented by Drug Type (Ultra-Short Acting Barbiturate, Short-Acting Barbiturate, Long-Acting Barbiturate, and Combination Drugs), Disease Type (Epilepsy, Insomnia, Sedation, and Other Disease Type), Distribution Channel (Retail Pharmacies, Hospital Pharmacies, and Other Pharmacies), and Geography (North America, Europe, Asia-Pacific, and Rest of the World). The report offers the value (in USD million) for the above-mentioned segments.

| Ultra-short-acting |

| Short-acting |

| Intermediate-acting |

| Long-acting |

| Epilepsy |

| Insomnia |

| Pre-operative Sedation |

| Medically-Induced Coma |

| Oral |

| Intravenous |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Drug Type (Value) | Ultra-short-acting | |

| Short-acting | ||

| Intermediate-acting | ||

| Long-acting | ||

| By Application (Value) | Epilepsy | |

| Insomnia | ||

| Pre-operative Sedation | ||

| Medically-Induced Coma | ||

| By Route of Administration (Value) | Oral | |

| Intravenous | ||

| By Distribution Channel (Value) | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the barbiturate market in 2031?

The barbiturate market is expected to be worth USD 600.98 million by 2031.

Which region is projected to grow fastest for barbiturates through 2031?

Asia-Pacific is projected to expand at an 7.75% CAGR, the quickest regional pace.

Which application currently leads barbiturate demand?

Epilepsy treatment leads, holding 46.15% of global share in 2025.

Why are ultra-short-acting barbiturates gaining traction?

They deliver rapid onset and predictable offset, ideal for emergency anesthesia and outpatient surgery.

How are online pharmacies influencing barbiturate distribution?

Enhanced e-prescribing compliance and DEA-aligned safeguards are enabling a 6.62% CAGR in online pharmacy sales.

Page last updated on: