Hydroxycarbamide Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

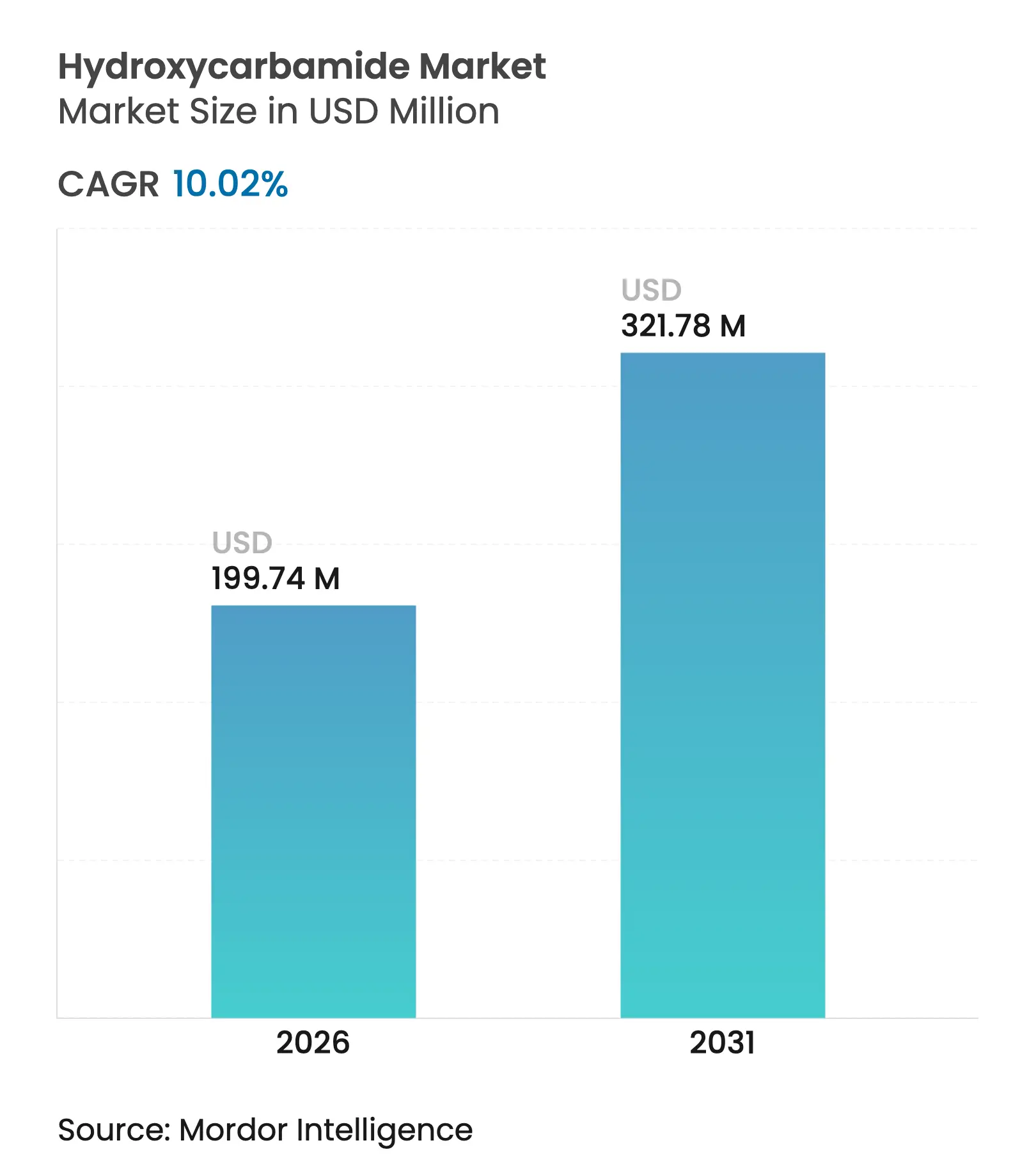

| Market Size (2026) | USD 199.74 Million |

| Market Size (2031) | USD 321.78 Million |

| Growth Rate (2026 - 2031) | 10.02 % CAGR |

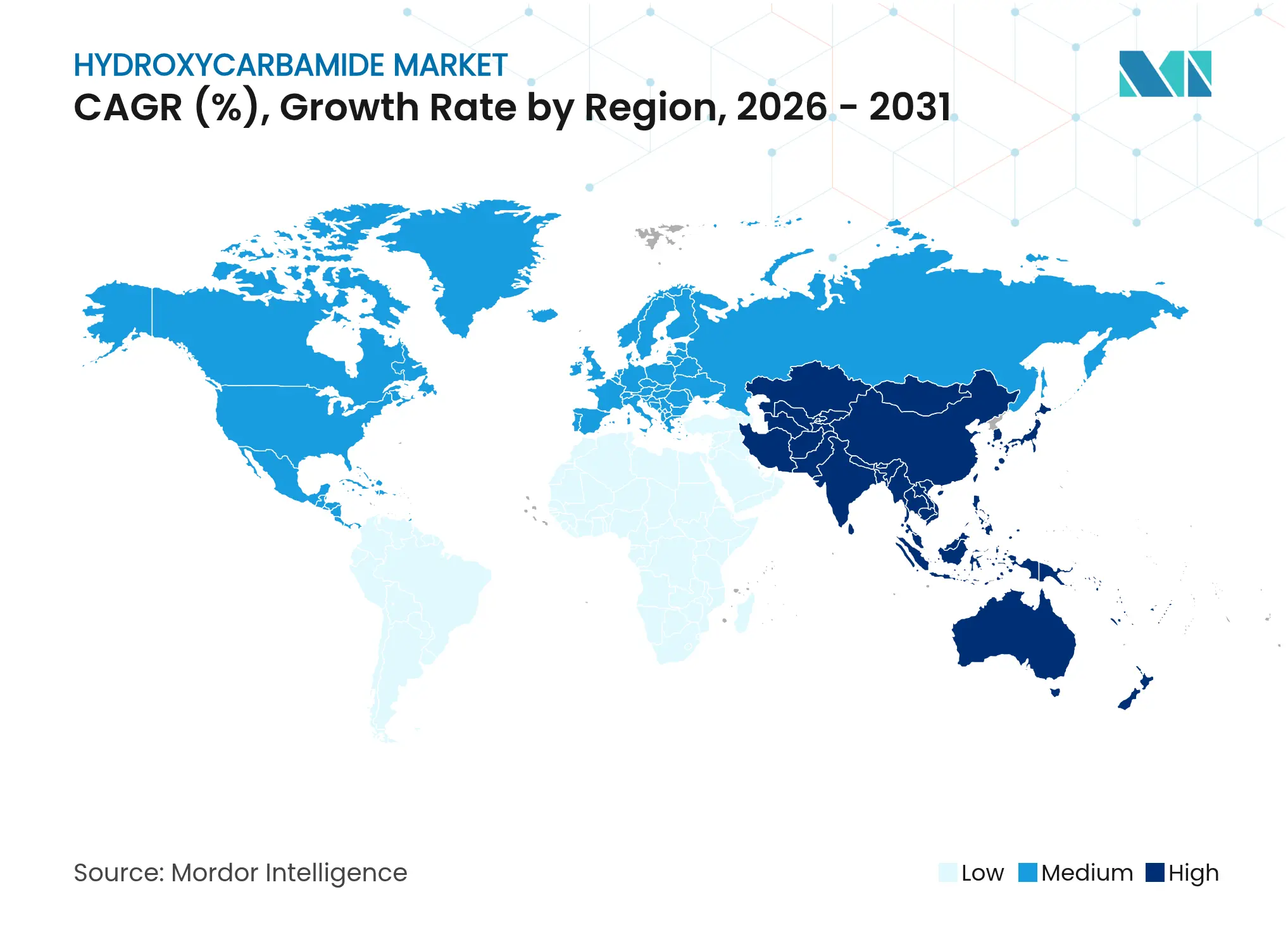

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Hydroxycarbamide Market Analysis by Mordor Intelligence

Hydroxycarbamide market size in 2026 is estimated at USD 199.74 million, growing from 2025 value of USD 181.54 million with 2031 projections showing USD 321.78 million, growing at 10.02% CAGR over 2026-2031. Growth is underpinned by the drug’s role as the gold-standard therapy for sickle cell disease, by expanding clinical protocols in myeloproliferative disorders and oncology, and by national public-health initiatives that widen screening and subsidize treatment. Strengthening regulatory support, notably WHO Africa’s 2024 guidance that embeds hydroxycarbamide into essential care packages, augments demand across low- and middle-income geographies. Large-scale newborn screening roll-outs, rising generic manufacturing capacity, and the introduction of infant-friendly liquid formulations further reinforce the hydroxycarbamide market’s upward trajectory. Competitive pressures from high-priced gene therapies inadvertently emphasize the treatment’s cost-effectiveness, while moderate fragmentation among generic suppliers maintains pricing discipline.

Key Report Takeaways

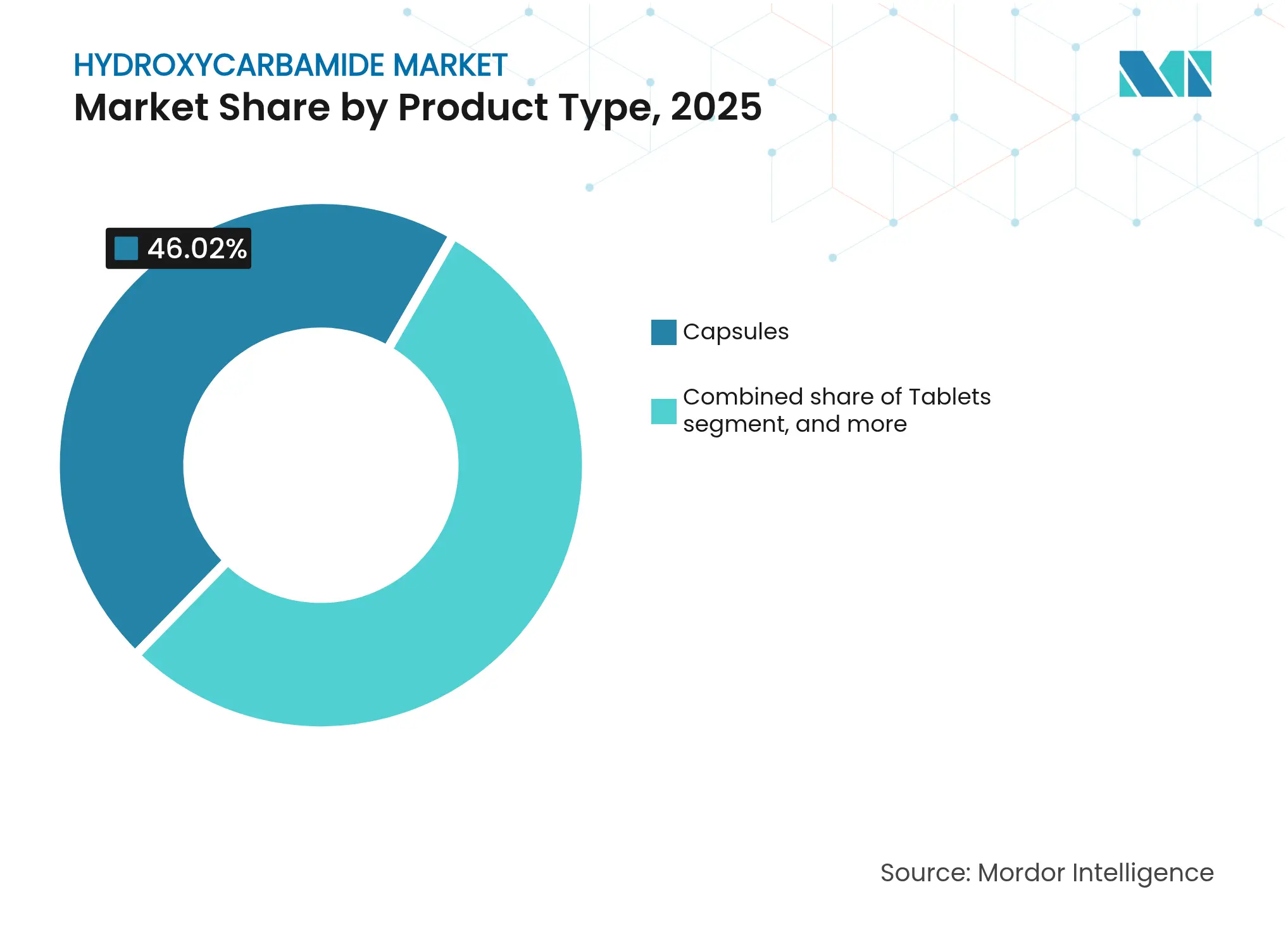

- By product type, capsules led with 46.02% of hydroxycarbamide market share in 2025, while oral solutions and suspensions are projected to post a 12.12% CAGR through 2031.

- By application, sickle-cell disease accounted for 57.92% of the hydroxycarbamide market size in 2025, whereas oncology indications are set to grow at 12.34% CAGR through 2031.

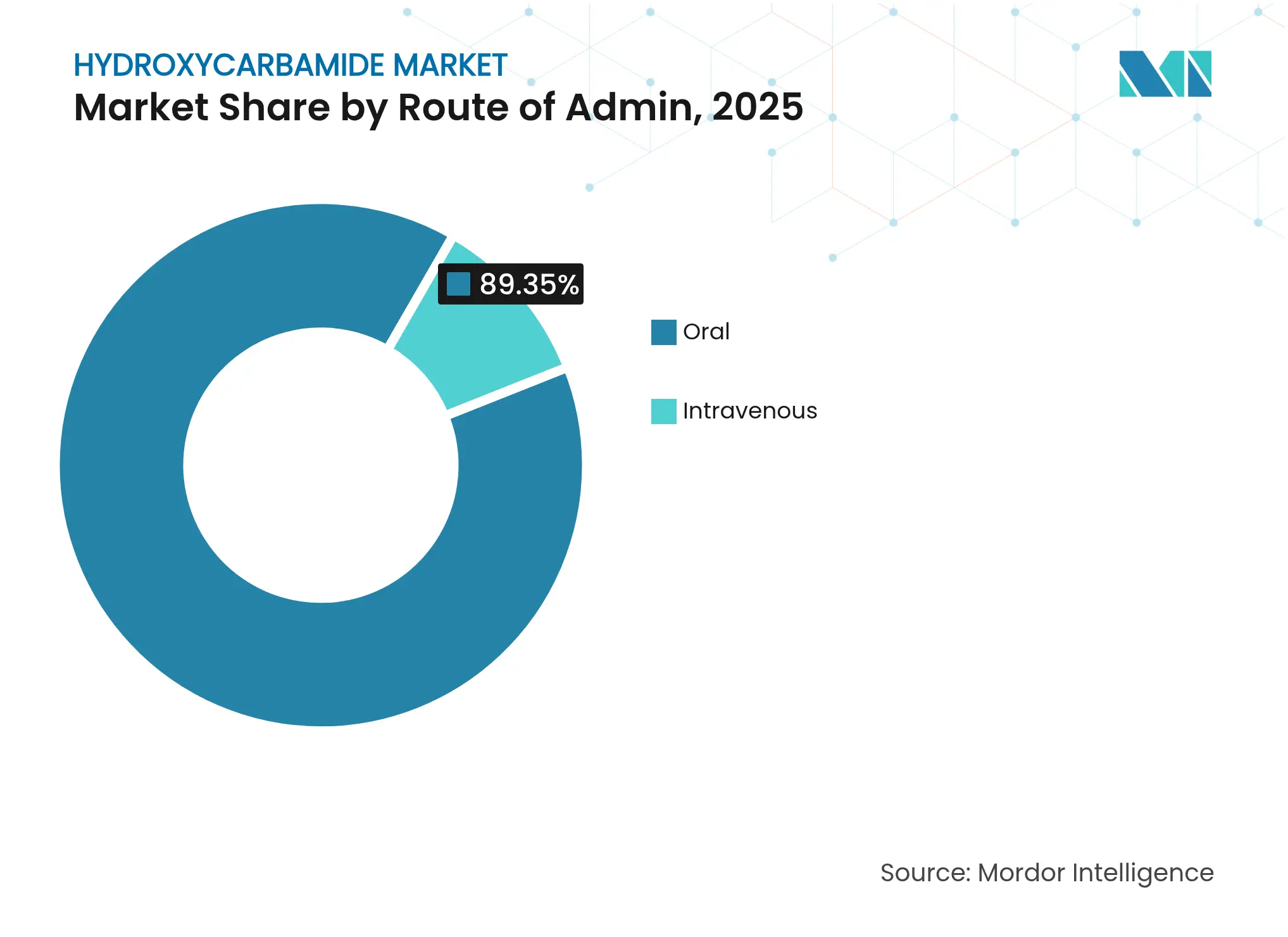

- By route of administration, oral formulations dominated with 89.35% share in 2025; intravenous administration will expand at a 12.95% CAGR to 2031.

- By distribution channel, hospital pharmacies dominated with 64.82% share in 2025. Digital and tender-based channels will expand at a 13.21% CAGR to 2031.

- By geography, North America held 40.98% of the hydroxycarbamide market in 2025; Asia-Pacific will register the fastest growth at 11.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydroxycarbamide Market Trends and Insights

Driver Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing global burden of hemoglobinopathies Growing global burden of hemoglobinopathies | +2.8% | Sub-Saharan Africa, India, Middle East | Long term (≥ 4 years) | % Impact on CAGR Forecast:+2.8% | Geographic Relevance:Sub-Saharan Africa, India, Middle East | Impact Timeline:Long term (≥ 4 years) |

Favorable regulatory approvals and reimbursement policies Favorable regulatory approvals and reimbursement policies | +2.1% | North America, Europe, expanding to Asia-Pacific | Medium term (2-4 years) | |||

Robust generic manufacturing capacity in emerging markets Robust generic manufacturing capacity in emerging markets | +1.9% | India, China with global supply impact | Medium term (2-4 years) | |||

Rising awareness and newborn screening programs Rising awareness and newborn screening programs | +1.7% | Global, with accelerated adoption in Asia-Pacific and Africa | Long term (≥ 4 years) | |||

Integration of hydroxyurea into public health supply chains Integration of hydroxyurea into public health supply chains | +1.4% | Africa, India, Latin America | Long term (≥ 4 years) | |||

Development of novel pediatric formulations Development of novel pediatric formulations | +0.8% | Global, with premium adoption in developed markets | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Global Burden of Hemoglobinopathies

More than 400,000 babies are born each year with sickle cell disease, and concentrated incidence in sub-Saharan Africa and India sustains inexorable demand for therapy[1]Augustine Odame, “Global Sickle Cell Burden and the Role of Therapy,” plosone.org. Nigeria’s national control program and parallel initiatives in East Africa translate epidemiologic urgency into systematic hydroxycarbamide adoption. India reports 15,000-25,000 new cases annually, while recent national surveys place overall prevalence at 1.17%, with tribal districts showing markedly higher rates. Government recognition of the disorder’s contribution to under-five mortality is pushing hydroxycarbamide toward routine use, enlarging the addressable pool for pharmaceutical suppliers. As birth cohorts age, cumulative patient numbers elevate long-run demand, reinforcing the hydroxycarbamide market’s expansion path.

Favorable Regulatory Approvals and Reimbursement Policies

The FDA’s April 2024 green light for Xromi oral solution extended approved use to infants as young as six months, broadening early-intervention protocols and catalyzing pediatric prescription growth[2]U.S. Food and Drug Administration, “FDA Approves Xromi,” fda.gov. EMA’s September 2024 suspension of voxelotor removed a direct competitor, indirectly solidifying hydroxycarbamide’s standing in European treatment algorithms[3]European Medicines Agency, “Questions and Answers on Voxelotor Suspension,” ema.europa.eu. Inclusion on WHO’s Essential Medicines List and expanding Medicaid preferential pricing in the United States align payer incentives with clinical guidelines, lowering out-of-pocket barriers for vulnerable populations. Orphan drug designations and fast-track reviews further accelerate formulation updates, shielding incumbents from disruptive entrants and supporting the hydroxycarbamide market’s sustained climb.

Robust Generic Manufacturing Capacity in Emerging Markets

Indian manufacturers supply over 50% of active pharmaceutical ingredients for United States prescriptions, anchoring global cost competitiveness in the hydroxycarbamide market. Cipla’s FY24 revenue of INR 25,455 crore, up 14%, underscores the profitability of scale production, while Zydus and Dr. Reddy’s bolster supply resilience across key export corridors. A looming USD 63.7 billion US patent cliff through 2029 diverts multinational focus toward specialty assets, creating room for aggressive generic expansion in hydroxycarbamide. Lower manufacturing costs allow tiered pricing in resource-constrained regions, unlocking previously latent segments of the hydroxycarbamide market.

Rising Awareness and Newborn Screening Programs

Systematic newborn screening rapidly converts undiagnosed neonates into treatment candidates. India’s national program plans to screen 70 million citizens, having already evaluated 58.5 million by early 2025, with free hydroxycarbamide dispensation across public facilities. In Namibia, point-of-care HemoTypeSC testing revealed 9.4% sickle cell trait prevalence, validating low-cost deployment models across Africa. Longitudinal pediatric data show hydroxycarbamide cuts emergency visits by 0.36 and hospital days by 0.84 per patient-year, reducing health-system strain. Early diagnosis coupled with subsidized therapy embeds the drug into lifelong management pathways, reinforcing forward demand across the hydroxycarbamide market.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Safety concerns regarding long-term myelosuppression Safety concerns regarding long-term myelosuppression | –1.8% | Global, with heightened scrutiny in developed markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:–1.8% | Geographic Relevance:Global, with heightened scrutiny in developed markets | Impact Timeline:Medium term (2-4 years) |

Suboptimal patient adherence and physician adoption Suboptimal patient adherence and physician adoption | –2.3% | Global, particularly acute in low- and middle-income countries and pediatric cohorts | Long term (≥ 4 years) | |||

Limited label indications in several low-income countries Limited label indications in several low-income countries | –1.1% | Sub-Saharan Africa and South Asia | Medium term (2-4 years) | |||

Supply constraints of pharma-grade active ingredient Supply constraints of pharma-grade active ingredient | –1.5% | Global, dependent on Chinese and Indian API supply chains | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Safety Concerns Regarding Long-Term Myelosuppression

Despite decades of favorable outcomes, hydroxycarbamide’s cytotoxic classification and potential for myelosuppression keep some providers hesitant. Regular blood count monitoring burdens clinics and unnerves caregivers, especially for pediatric patients confronting lifelong therapy commitments. Isolated case reports of late gastrointestinal ulcers and diverging data on fertility impacts sustain debate. Recent ASH data indicating no reduction in ovarian reserve lend reassurance but have yet to permeate all practice settings. Where specialist hematology services are scarce, cautious prescribers may delay initiation, tempering overall hydroxycarbamide market growth.

Suboptimal Patient Adherence and Physician Adoption

Adherence remains uneven; Tanzanian studies report only 23.8% of children achieving good compliance, with socioeconomic adversity, caregiver workload, and limited health-literacy driving lapses. Surveys across India, Malaysia, and Thailand highlight physician knowledge gaps that translate to variable prescription patterns despite guideline consensus. Daily dosing, ongoing laboratory monitoring, and pharmacy access costs compound attrition. Mobile directly observed therapy pilots show promise but require sustained funding. Suboptimal adherence depresses real-world effectiveness, dampens clinician confidence, and restrains potential hydroxycarbamide market expansion even in jurisdictions with drug availability.

Segment Analysis

By Product Type: Liquid Formulations Propel Pediatric Uptake

Liquid formulations amplify the hydroxycarbamide market size among infants and toddlers and hold a 12.12% CAGR through 2031, outpacing capsule growth. Capsules retain 46.02% share given entrenched adult use and efficient large-scale production. Tablets such as Siklos that disperse in water balance adult convenience with pediatric flexibility. With regulatory incentives for child-friendly medicines, multinational and generic manufacturers prioritize suspension and solution production lines, consolidating value around proprietary flavoring and stability technologies. Liquid manufacturing complexity and cold-chain requirements present moderate barriers, favoring incumbents with established capabilities and preserving elevated margins in this rapidly expanding tier of the hydroxycarbamide market.

Steady capsule demand anchors supply chains and underwrites price competitiveness for adult chronic care, while niche intravenous formulations service acute hospital settings. Hospitals in high-income markets increasingly stock injectable options for rapid intervention, yet volume remains modest, limiting direct impact on overall hydroxycarbamide market share.

Note: Segment shares of all individual segments available upon report purchase

By Application: Oncology Momentum Builds on Combination Therapy

Sickle-cell disease underpins 57.92% of hydroxycarbamide market share in 2025, reflecting mature clinical pathways and insurance coverage. By contrast, oncology use is forecast to scale 12.34% CAGR, leveraging the drug’s ribonucleotide reductase inhibition for cost-aware combination protocols in head-and-neck cancers and select leukemias. Clinical studies validating organ-protection benefits in chronic sickle cell management widen intra-indication dosing sophistication, while myeloproliferative disorders sustain steady baseline demand. Oncology’s faster growth diversifies revenue streams, mitigates reimbursement concentration risk, and offsets single-indication exposure, keeping the hydroxycarbamide market resilient against competitive shocks centered on hemoglobinopathies alone.

By Route of Administration: Intravenous Use Expands in Acute Care

Oral regimens constitute 89.35% of global volume owing to self-administration convenience and chronic disease management paradigms. The intravenous sub-segment’s 12.95% CAGR signals heightened hospital uptake during acute vaso-occlusive crises when enteral absorption is compromised. Tertiary centers in North America and Europe drive adoption, while teaching hospitals in India and Nigeria pilot rapid-infusion protocols. Manufacturing sterile injectables involves capital-intensive facilities and stringent validation, restricting supplier base and allowing modest premium pricing that modestly augments the hydroxycarbamide market size without eroding affordability for oral lines.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Procurement Gains Momentum

Hospital pharmacies absorb 64.82% of global volume, reflecting centralized care models for sickle cell disease. Retail chains sustain chronic refill convenience in developed markets. Digital and tender-based channels are rising 13.21% CAGR, propelled by national elimination missions leveraging e-procurement for bulk discounts and track-and-trace oversight. Online sales platforms in the United States and Europe support home delivery for adult maintenance therapy and integrate adherence apps, aligning with telehealth’s post-pandemic growth. Government tenders in Africa and Latin America anchor predictable demand, solidifying cash-flow visibility for manufacturers and cementing the hydroxycarbamide market’s long-term viability.

Geography Analysis

North America led with 40.98% share in 2025, due to established clinical guidelines, expansive insurance coverage, and early adoption of infant formulations. Medicaid and private payers routinely reimburse therapy, while ASH centers of excellence standardize dosing and lab-monitoring algorithms. Canada leverages universal coverage to ensure equitable access, and Mexico’s Seguro Popular includes hydroxycarbamide on essential formularies, sustaining contiguous regional demand.

Europe contributes steady volume through universal health systems and specialized rare-disease networks. The EMA’s suspension of voxelotor in 2024 reinforced physician trust in hydroxycarbamide, maintaining market penetration in Germany, France, Italy, Spain, and the United Kingdom. Cross-border treatment arrangements within the EU streamline patient referrals to hemoglobinopathy centers, preserving consistent utilization despite demographic variances.

Asia-Pacific is projected to post 11.12% CAGR, driven by India’s national elimination mission, which offers free drug supply across 278 districts and strong political commitment to reach 70 million citizens. China scales production for domestic and export use, while Japan and Australia refine clinical protocols through academic-industry collaboration. ASEAN states pilot screening programs with World Bank support, creating nascent but fast-moving demand clusters that integrate digital adherence tools and centralized procurement.

Africa registers accelerating uptake as WHO regional guidance spurs donor-funded supply chains. Nigeria, Kenya, and Ghana embed hydroxycarbamide within newborn screening pathways, and public tenders ensure stock availability. Demographic trends and high disease prevalence position the continent as a pivotal driver of long-run hydroxycarbamide market size growth.

Competitive Landscape

Market Concentration

The hydroxycarbamide market is moderately fragmented. Teva, Bristol Myers Squibb, Novartis (via Addmedica), and generics from Cipla, Zydus, Sun Pharma, and Dr. Reddy’s dominate global supply. Teva’s planned 2025 API divestiture may reshape cost structures, while Cipla’s double-digit revenue gains underscore emerging-market strength. Pediatric formulation specialization grants competitive leverage to Novartis partnerships that market Xromi and Siklos. Lonza’s manufacturing deal for Casgevy exemplifies collaboration between gene-therapy innovators and traditional contract manufacturers, indirectly validating hydroxycarbamide’s affordability advantage against multimillion-dollar one-time treatments.

Strategic moves focus on scale economics, differentiated dosing formats, and regional access programs rather than molecular novelty. Indian suppliers leverage government tenders to entrench share in Asia and Africa, while multinational players defend premium markets through brand recognition and hospital penetration. Cost–benefit comparisons versus gene therapies reinforce hydroxycarbamide’s first-line status, sustaining volume even amid high-profile curative options.

Hydroxycarbamide Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sanofi secures FDA approval of Qfitlia, illustrating continued innovation in rare hematologic disorders.

- February 2025: Bristol Myers Squibb reports Q4 2024 revenues of USD 12.3 billion, raises 2025 guidance to USD 45.8-46.8 billion.

- January 2025: Teva reports 2024 revenue of USD 16.54 billion and outlines seven-biosimilar US launch plan.

- May 2024: Cipla posts FY24 revenue of INR 25,455 crore and signals expansion in oncology generics.

- March 2024: Roche announces USD 50 billion US investment in pharma and diagnostics to 2030.

Table of Contents for Hydroxycarbamide Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope Of The Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing Global Burden of Hemoglobinopathies

- 4.2.2Favorable Regulatory Approvals and Reimbursement Policies

- 4.2.3Robust Generic Manufacturing Capacity in Emerging Markets

- 4.2.4Rising Awareness and Newborn Screening Programs

- 4.2.5Integration of Hydroxyurea Into Public Health Supply Chains

- 4.2.6Development of Novel Pediatric Formulations

- 4.3Market Restraints

- 4.3.1Safety Concerns Regarding Long-Term Myelosuppression

- 4.3.2Suboptimal Patient Adherence and Physician Adoption

- 4.3.3Limited Label Indications in Several Low-Income Countries

- 4.3.4Supply Constraints of Pharma-Grade Active Ingredient

- 4.4Regulatory Landscape

- 4.5Porter's Five Forces Analysis

- 4.5.1Threat Of New Entrants

- 4.5.2Bargaining Power Of Buyers / Consumers

- 4.5.3Bargaining Power Of Suppliers

- 4.5.4Threat Of Substitute Products

- 4.5.5Intensity Of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product Type

- 5.1.1Capsules

- 5.1.2Tablets

- 5.1.3Oral Solutions & Suspensions

- 5.1.4Intravenous Solutions

- 5.2By Application

- 5.2.1Sickle-Cell Disease

- 5.2.2Myeloproliferative Disorders (Polycythemia Vera, Essential Thrombocythemia)

- 5.2.3Oncology (Cml, Head & Neck Scc)

- 5.2.4Thalassemia & Other Indications

- 5.3By Route Of Administration

- 5.3.1Oral

- 5.3.2Intravenous

- 5.4By Distribution Channel

- 5.4.1Hospital Pharmacies

- 5.4.2Retail Pharmacies

- 5.4.3Online Pharmacies & Tender-Based Supply

- 5.5Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1Teva Pharmaceutical Industries

- 6.3.2Bristol Myers Squibb

- 6.3.3Novartis AG

- 6.3.4Cipla Ltd.

- 6.3.5Zydus Lifesciences

- 6.3.6Dr. Reddy�s Laboratories

- 6.3.7Sun Pharma

- 6.3.8Alkem Laboratories

- 6.3.9Aurobindo Pharma

- 6.3.10Lupin

- 6.3.11Glenmark Pharma

- 6.3.12Hikma Pharmaceuticals

- 6.3.13Intas Pharma

- 6.3.14Qilu Pharmaceutical

- 6.3.15Taj Pharma Group

- 6.3.16Samarth Life Sciences

- 6.3.17Akums Drugs & Pharmaceuticals

- 6.3.18Apotex

- 6.3.19Nova Laboratories

- 6.3.20Addmedica

7. Market Opportunities & Future Outlook

- 7.1White-Space & Unmet-Need Assessment

Global Hydroxycarbamide Market Report Scope

As per the scope of the report, hydroxycarbamide is a drug that is used to treat sickle-cell disease, chronic myelogenous leukemia, cervical cancer, and polycythemia vera.

The hydroxycarbamide market is segmented by product type, application, and geography. By product type, the market is segmented into capsules, tablets, and others. By application, the market is segmented into sickle cell disease, cancer, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (USD) for all the above segments.