Anti-Malarial Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 1.39 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle-East and Africa |

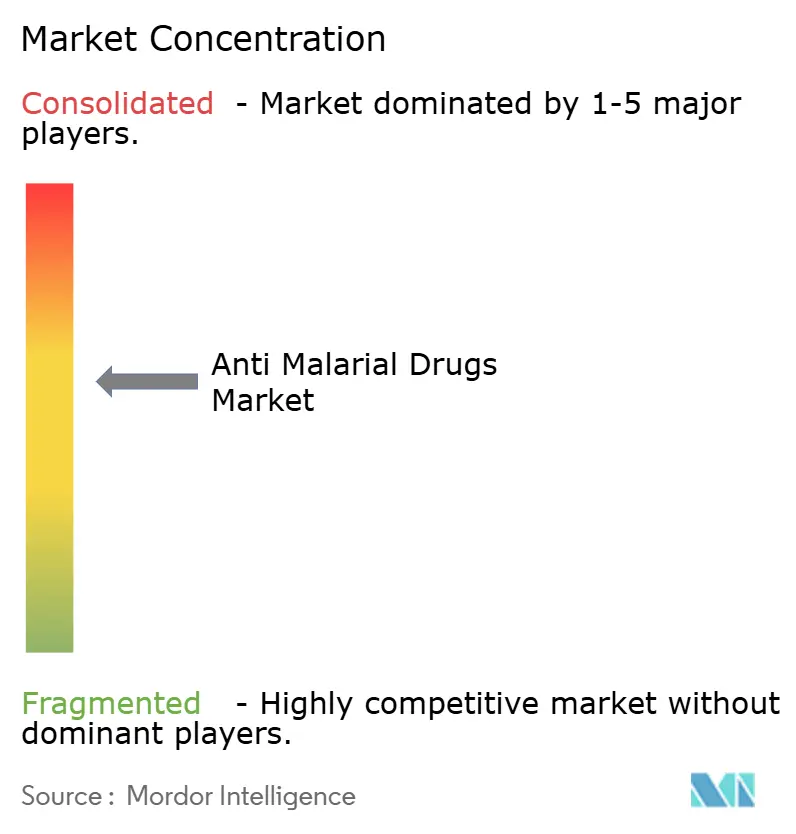

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-Malarial Drugs Market Analysis by Mordor Intelligence

The anti-malarial drugs market size is expected to grow from USD 1.08 billion in 2025 to USD 1.13 billion in 2026 and is forecast to reach USD 1.39 billion by 2031 at 4.26% CAGR over 2026-2031. This progression shows a shift from volume-led growth to value-driven innovation as companies introduce next-generation compounds that fight emerging resistance while preserving affordability for endemic countries. Artemisinin resistance spreading through East Africa is forcing portfolio diversification, spurring research into spiroindolone and endoperoxide analogues. Plasmodium falciparum continues to dominate clinical demand, yet improved diagnostics are revealing a larger burden from P. knowlesi. Geographic revenue still favors high-income regions where prophylaxis and R&D spending drive premium pricing. Inside endemic areas, digital procurement platforms and radical cure therapies are reshaping supply chains and treatment choices.

Key Report Takeaways

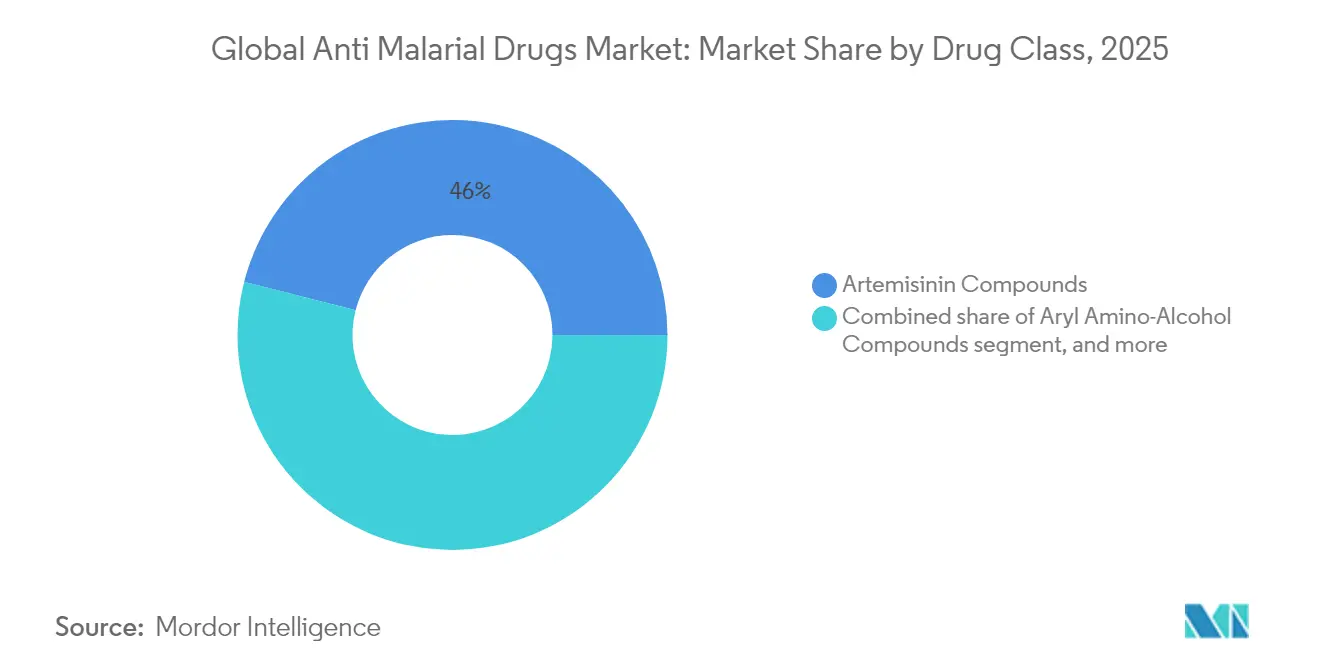

- By drug class, artemisinin compounds retained 46.02% of the anti-malarial drugs market share in 2025, while spiroindolones recorded the top CAGR at 6.23% through 2031.

- By malaria type, Plasmodium falciparum accounted for 62.55% share of the anti-malarial drugs market size in 2025; Plasmodium knowlesi is projected to advance at a 6.62% CAGR to 2031.

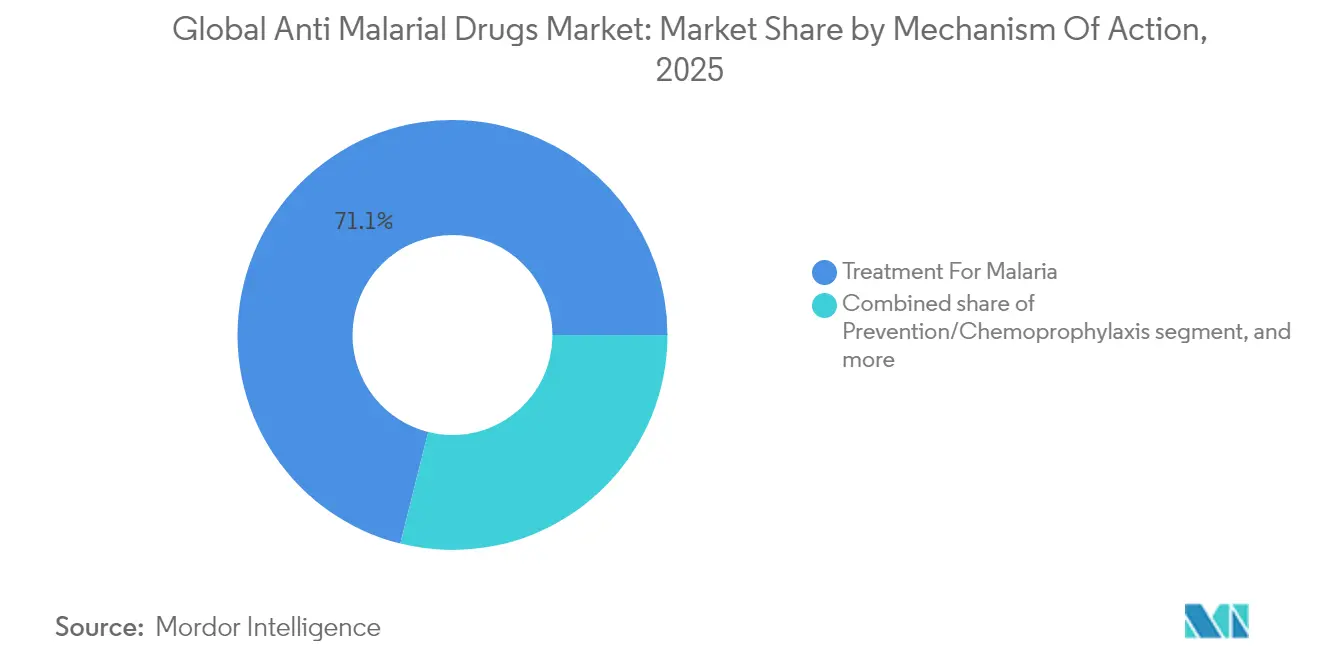

- By mechanism of action, treatment applications held 71.10% revenue share in 2025; radical cure formulations are expanding at a 7.15% CAGR.

- By distribution channel, public procurement agencies managed 53.88% share of the anti-malarial drugs market size in 2025, while online pharmacies are growing at a 7.09% CAGR.

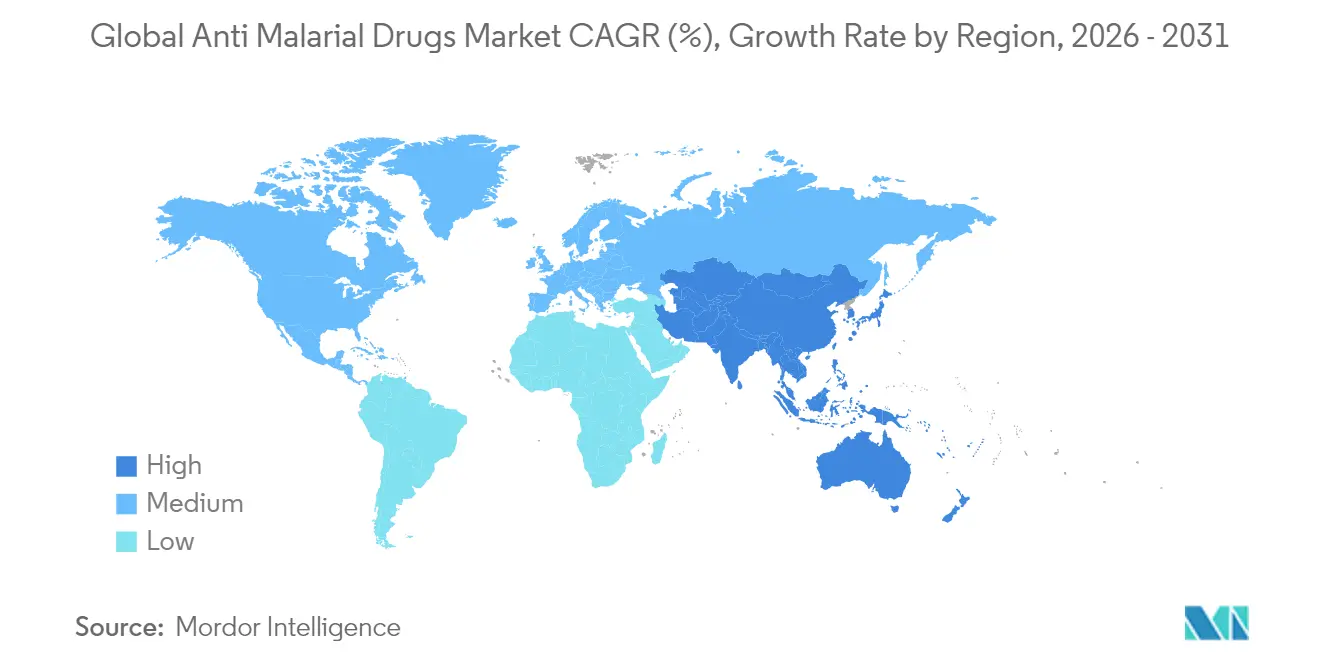

- By geography, North America led with 39.12% of anti-malarial drugs market share in 2025; Asia-Pacific posts the fastest regional CAGR at 5.18% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anti-Malarial Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Endemic disease burden in tropical regions | +1.2% | Sub-Saharan Africa, Southeast Asia | Long term (≥ 4 years) |

| Government-led malaria control initiatives and funding | +0.8% | Global, concentration in Africa | Medium term (2-4 years) |

| Advancements in artemisinin-based combination therapies | +0.6% | Global | Short term (≤ 2 years) |

| Expansion of global health financing mechanisms | +0.5% | Low- and middle-income countries | Medium term (2-4 years) |

| Integration of digital health tools in case management | +0.4% | Asia-Pacific, Sub-Saharan Africa | Medium term (2-4 years) |

| Growing private-sector investment in novel antimalarials | +0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Endemic Disease Burden In Tropical Regions

Persistent transmission in tropical climates sustains baseline demand even when purchasing power is low. Sub-Saharan Africa recorded 597,000 malaria deaths in 2023, equal to 94% of the global total, yet contributed a smaller share of revenue because pricing relies on donor procurement[1]World Health Organization, “World Malaria Report 2024,” who.int. Ethiopia logged 7.3 million cases and 1,157 deaths in 2024 during supply chain disruptions that limited medicine availability. Urban invasion by Anopheles stephensi is altering transmission patterns, requiring new therapeutic strategies that go beyond rural programs. This concentrated burden assures continuous consumption in endemic countries, but revenue growth remains capped by affordability frameworks.

Government-Led Malaria Control Initiatives And Funding

National plans such as Indonesia’s 2030 elimination roadmap and India’s 2023-27 strategic plan translate policy ambition into predictable drug tenders[2]Asia Pacific Leaders Malaria Alliance, “Indonesia Malaria Elimination Roadmap,” aplma.org. Cross-border surveillance along India-Bhutan and India-Nepal corridors aggregates procurement volumes and lowers unit costs. Yet WHO cautions that projected aid reductions in 2025 could affect services across 64 endemic countries, disrupting supply chains and destabilizing the anti-malarial drugs market. Funding swings therefore create cyclic demand, benefiting suppliers able to flex production in line with donor cycles.

Advancements In Artemisinin-Based Combination Therapies

Multiple first-line therapy guidelines promote a rotation of ACTs to slow resistance. Novartis showed strong efficacy for Coartem Baby in infants under 5 kg, expanding clinical reach into a previously undersupplied cohort. Triple ACTs layer two partner drugs with an artemisinin derivative to delay resistance, but higher complexity raises manufacturing and regulatory costs that suppliers must absorb or offset through premium markets.

Expansion Of Global Health Financing Mechanisms

The Global Fund approved USD 9.2 billion in malaria-inclusive grants for 2024-2025, directing 32% of the first USD 12 billion to antimalarial programs[3]The Global Fund, “Grant Cycle 7 Funding Decisions,” theglobalfund.org. Gavi’s roll-out of malaria vaccines across 15 African countries in 2024 accelerates market penetration for follow-on drugs used in breakthrough cases. At the same time, a USD 4.3 billion gap identified in 2023 emphasizes the ceiling on near-term expansion of the anti-malarial drugs industry. As nations graduate from donor eligibility, manufacturers will need tiered-pricing models that sustain commercial margins.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing drug resistance in endemic areas | -1.0% | East Africa, Southeast Asia | Short term (≤ 2 years) |

| Proliferation of counterfeit and substandard medications | -0.8% | Sub-Saharan Africa, South Asia | Medium term (2-4 years) |

| Limited commercial incentives for novel chemistries | -0.6% | Global | Long term (≥ 4 years) |

| Supply-chain vulnerability to raw-material shortages | -0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Drug Resistance In Endemic Areas

Kelch-13 469Y mutations now identified in Uganda, Tanzania, Rwanda, and the Democratic Republic of Congo confirm partial artemisinin resistance beyond its Southeast Asian origin. Rising resistance shortens product lifecycles, compels costly reformulation, and may sideline smaller producers unable to fund R&D. WHO’s new recommendation for multiple first-line therapies raises the logistical burden on health systems that must stock several options simultaneously.

Proliferation Of Counterfeit And Substandard Medications

About 19% of antimalarials sampled in Sub-Saharan Africa are substandard or falsified, causing between 40,000 and 160,000 deaths each year. East African reviews show 24% failure rates, notably 73% for chloroquine. In Kenya, 52.1% of medicine-quality complaints tracked by regulators involve defects. Counterfeits erode public trust, dampen legitimate demand, and create extra pharmacovigilance costs for compliant manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Spiroindolones Lead Innovation Shift

Artemisinin derivatives controlled 46.02% of anti-malarial drugs market share in 2025, anchored by global treatment guidelines. Spiroindolones, represented by Novartis’s cipargamin, are advancing at a 6.23% CAGR because they retain potency against artemisinin-resistant strains. Antifolates and aryl amino-alcohols keep niche relevance in combinations and prevention. Endoperoxide analogues are in early pipelines that aim to mimic peroxide-based activity without cross-resistance.

The transition indicates strategic hedging against single-mechanism failure. Other drug types such as FIKK kinase inhibitors and chromatin remodelers are under exploration, offering new pathways to disrupt parasite biology [SCiencedaily.com]. Regulatory lead times remain long, so larger firms with deeper capital are best placed to carry these assets through approval.

By Malaria Type: Knowlesi Gains Recognition

Plasmodium falciparum accounted for 62.55% of the anti-malarial drugs market size in 2025. Improved PCR diagnostics are uncovering a faster rise in P. knowlesi, which now grows at a 6.62% CAGR, particularly in Malaysia and parts of Indonesia where human–macaque interface drives zoonotic spillover. Plasmodium vivax retains high demand because its liver hypnozoites necessitate radical cure regimens.

Species-tailored therapies are beginning to penetrate. Brazil’s and Thailand’s introduction of single-dose radical cure for vivax signals movement toward precision medicine in malaria care. Broader adoption hinges on diagnostic accuracy in primary care settings.

By Mechanism Of Action: Radical Cure Accelerates

Therapeutic dosing for active infection held 71.10% revenue share in 2025, yet radical cure products such as tafenoquine are expanding at 7.15% CAGR thanks to WHO prequalification of a single-dose regimen. Prevention through traveler prophylaxis and seasonal chemoprevention remains stable, serving distinct patient cohorts.

Radical cure simplifies care and prevents repeat episodes, but G6PD screening requirements add cost and operational complexity in rural clinics. Suppliers of point-of-care G6PD tests may capture adjunct revenues as radical cure uptake rises.

By Distribution Channel: Digital Transformation Emerges

Public procurement agencies bought 53.88% of volumes in 2025, underlining donor dominance. Online pharmacies, though still modest in absolute terms, are growing at 7.09% CAGR by courting urban consumers in Asia-Pacific who seek convenient access and verified supply chains. Hospital pharmacies preserve demand for severe malaria medicines, while retail outlets stay relevant in mixed public-private systems.

Regulatory clarity on e-pharmacy operations differs widely. Countries that digitize product registries, like Mali, speed approval cycles and improve counterfeit detection; slower adopters risk widened quality gaps.

Geography Analysis

North America’s dominant 39.12% share of the anti-malarial drugs market in 2025 came from premium prophylaxis sales to travelers, the military, and research institutions. Imported cases totaled 1,772 in 2024, confirming that non-endemic settings still require reliable treatments. Regulatory leadership by the FDA further anchors R&D investments. Yet reliance on discretionary travel exposes the segment to economic downturns that can quickly dampen pharmacy demand.

Asia-Pacific is forecast to grow at 5.18% CAGR through 2031 as expanding middle-income populations invest in healthcare infrastructure and governments boost case detection. The anti-malarial drugs market size here rises in tandem with integrated surveillance and elimination plans. Funding shortfalls of USD 478 million identified by the Global Fund illustrate ongoing dependency on blended finance. Resistance to artemisinin in the Greater Mekong Subregion drives interest in spiroindolones and triple ACTs. P. vivax dominance ensures radical cure uptake once G6PD testing barriers ease.

Europe, Middle East & Africa, and South America remain heterogeneous. European demand orbits around traveler prophylaxis and basic research, contributing stable but low-growth revenue. Sub-Saharan Africa’s disease load secures steady procurement yet caps pricing. African vaccine deployments will coexist with drugs for breakthrough and mixed infections, potentially increasing combination therapy use. South America’s Amazon basin is nearing elimination, shifting drug procurement toward follow-up care and imported case management.

Competitive Landscape

The anti-malarial drugs market displays moderate fragmentation. GlaxoSmithKline, Novartis, and Cipla jointly held 41% revenue in 2024 as they field both legacy ACTs and new assets such as tafenoquine and cipargamin. These firms leverage large-scale manufacturing and global regulatory teams to meet donor and private orders.

Competitive positioning is moving from price-based bids to value differentiation through novel mechanisms, pediatric formulations, and digital adherence technologies. Novartis’s pledge to maintain production despite possible order cuts shows commitment to public-health obligations that reinforce brand reputation. Dr. Reddy’s collaborative development approach underscores how mid-cap players enter via risk-sharing partnerships.

Niche opportunities exist around P. knowlesi-targeted agents, AI-aligned compound discovery, and e-pharmacy distribution models. Emerging disruptors include monoclonal antibody developers and companies testing vector-control adjuncts such as nitisinone for mosquito population suppression. Overall, supplier success will hinge on balancing innovation costs with donor affordability thresholds.

Anti-Malarial Drugs Industry Leaders

Novartis AG

Strides Pharma Science Limited

Glenmark Pharmaceuticals

GlaxoSmithKline PLC

Cipla Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Novartis received approval for Coartem Baby, the first treatment designed for infants under 5 kg, filling a critical pediatric gap.

- June 2025: Oxford University and Recipharm widened their vaccine partnership to scale fill-finish for R78C and RH5.1 candidates, extending pipeline diversity.

- June 2025: Bharat Biotech and GSK committed to halve malaria vaccine prices by 2028 to broaden access while using volume efficiencies.

- March 2025: Merck partnered with the Walter and Eliza Hall Institute on multi-stage antimalarial agents with potential resistance-breaking properties.

- February 2025: 60 Degrees Pharmaceuticals secured FDA permission to import KODATEF to prevent domestic stock-outs.

Global Anti-Malarial Drugs Market Report Scope

As per the scope of the report, antimalarial drugs are drugs that are designed to treat malaria in individuals or prevent infection in individuals who have no immunity to the infection. Malaria is a disease caused due to the parasite known as Plasmodium, which belongs to the organism group Protozoa. Generally, malaria is treated by single drug therapy as first-line therapy, and sometimes the combination drug therapy is for the second line of infection. Anti-malarial drugs are available on the market in the form of tablets, injectables, and capsules. The Anti-Malarial Drugs Market is Segmented by Drug Class (Aryl amino alcohol compounds, Antifolate compounds, Artemisinin compounds, and Other Drug Types), Malaria Type ( Plasmodium Falciparum, Plasmodium Vivax, Plasmodium Malariae, Plasmodium Ovale) Mechanism of Action (Treatment for Malaria, Prevention from Malaria)and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Aryl Amino-Alcohol Compounds |

| Antifolate Compounds |

| Artemisinin Compounds |

| Endoperoxide Analogues |

| Spiroindolone Compounds |

| Other Drug Types |

| Plasmodium Falciparum |

| Plasmodium Vivax |

| Plasmodium Malariae |

| Plasmodium Ovale |

| Plasmodium Knowlesi |

| Treatment For Malaria |

| Prevention / Chemoprophylaxis |

| Radical Cure (Anti-Relapse) |

| Public Procurement Agencies |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Aryl Amino-Alcohol Compounds | |

| Antifolate Compounds | ||

| Artemisinin Compounds | ||

| Endoperoxide Analogues | ||

| Spiroindolone Compounds | ||

| Other Drug Types | ||

| By Malaria Type | Plasmodium Falciparum | |

| Plasmodium Vivax | ||

| Plasmodium Malariae | ||

| Plasmodium Ovale | ||

| Plasmodium Knowlesi | ||

| By Mechanism Of Action | Treatment For Malaria | |

| Prevention / Chemoprophylaxis | ||

| Radical Cure (Anti-Relapse) | ||

| By Distribution Channel | Public Procurement Agencies | |

| Hospital Pharmacies | ||

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the anti-malarial drugs market?

The anti-malarial drugs market size stood at USD 1.13 billion in 2026 and is forecast to reach USD 1.39 billion by 2031 at a 4.26% CAGR.

Which drug class is growing the fastest?

Spiroindolone compounds, led by cipargamin, are expanding at 6.23% CAGR through 2031, reflecting their ability to treat artemisinin-resistant infections.

Why does North America hold a large market share despite low malaria transmission?

High prophylaxis demand from travelers and the military, coupled with significant R&D investment, gives North America 39.12% revenue share even with minimal endemic cases.

How is radical cure therapy changing malaria treatment?

WHO prequalification of single-dose tafenoquine is driving 7.15% CAGR in radical cure therapies, which eliminate dormant liver stages and prevent relapse.

What are the main risks limiting market growth?

Rising drug resistance, widespread counterfeit medicines, and donor funding volatility are the leading restraints on the anti-malarial drugs market outlook.

Which region is projected to grow the fastest?

Asia-Pacific is expected to post the highest regional CAGR of 5.18% through 2031 thanks to expanding healthcare investment and improved diagnostic coverage.

Page last updated on: