Global Cephalosporin Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 21.24 Billion |

| Market Size (2031) | USD 24.59 Billion |

| Growth Rate (2026 - 2031) | 2.97% CAGR |

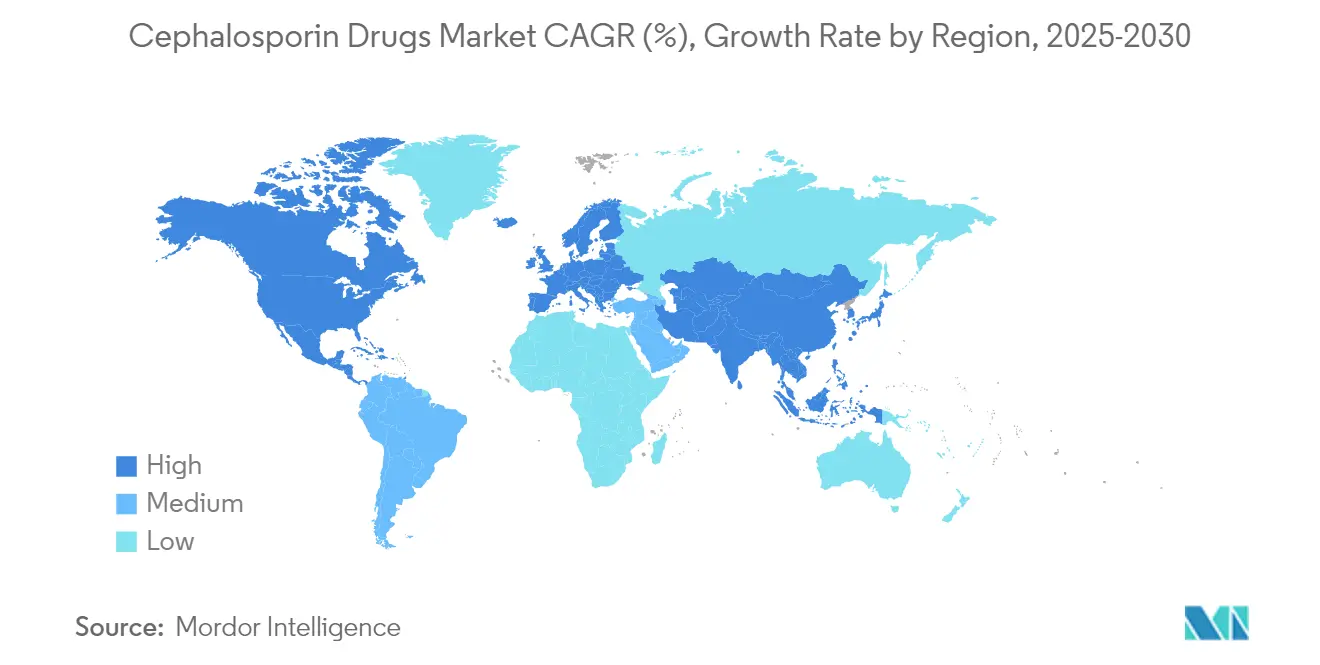

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Cephalosporin Drugs Market Analysis by Mordor Intelligence

Cephalosporin drugs market size in 2026 is estimated at USD 21.24 million, growing from 2025 value of USD 20.63 million with 2031 projections showing USD 24.59 million, growing at 2.97% CAGR over 2026-2031. Steady demand endures because cephalosporins remain first-line therapies for severe hospital infections, even as competitive generics and stewardship rules limit rapid expansion. Uptake of newer generations designed for multidrug-resistant pathogens, broader surgical volumes requiring prophylaxis, and the World Health Organization’s AWaRe framework, which encourages cephalosporin access in low- and middle-income countries, underpin growth.[1]World Health Organization, “2023 AWaRe Antibiotic Classification Update,” who.int On the other hand, tender-based procurement depresses prices, and the rise of non-antibiotic modalities such as phage therapy threatens long-term volumes. Competitive differentiation now hinges on beta-lactamase-inhibitor combinations, long-acting depot injections for outpatient therapy, and expedited regulatory pathways that add exclusivity for qualified infectious disease products.

Key Report Takeaways

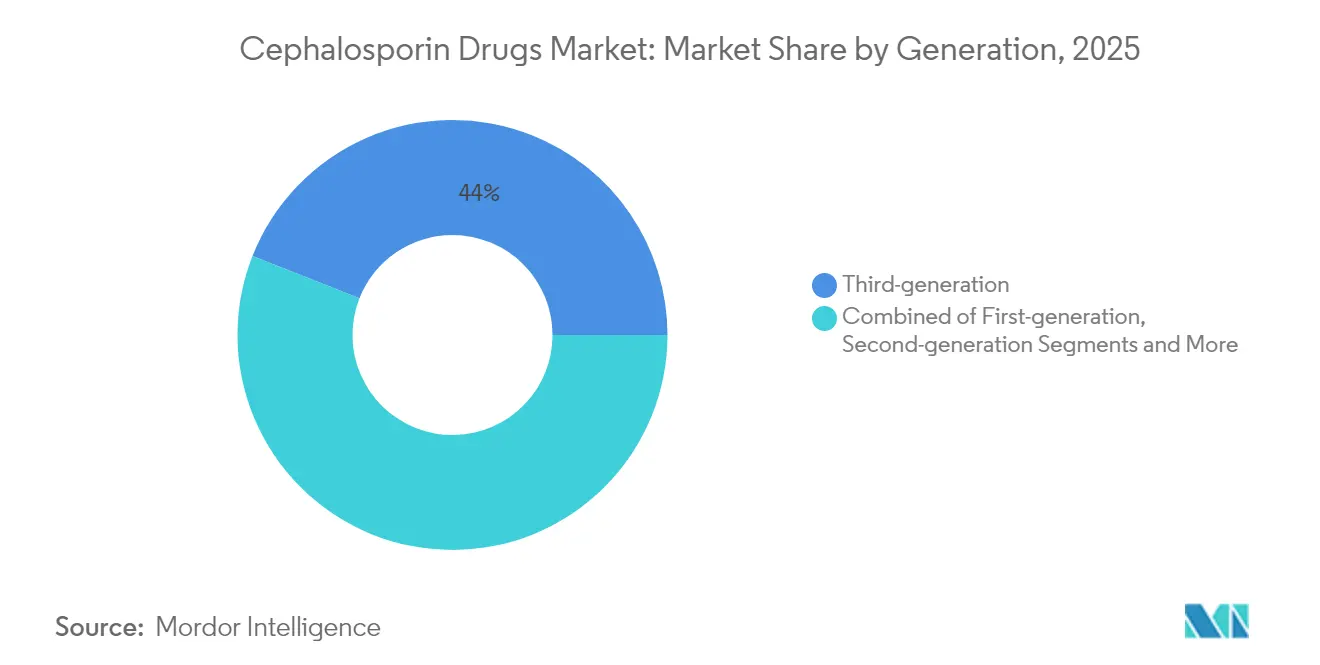

- By generation, third-generation agents led with 44.02% of the cephalosporin drugs market share in 2025, while fifth-generation products are projected to expand at a 8.68% CAGR through 2031.

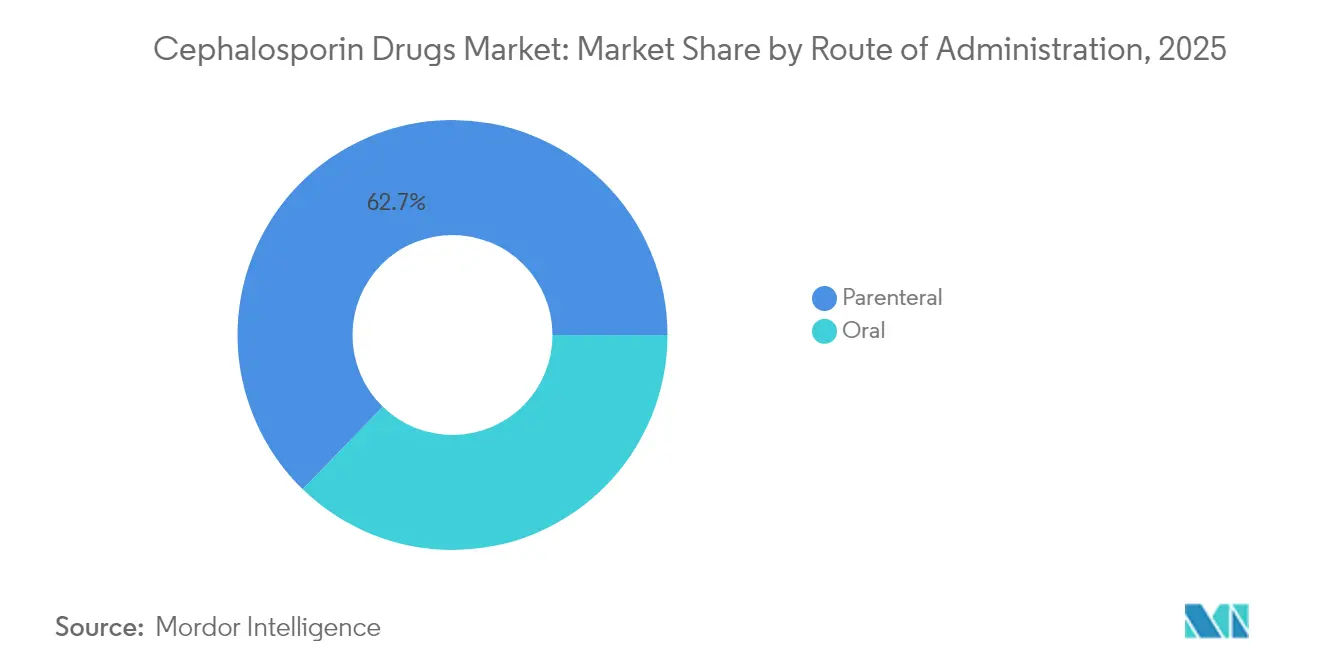

- By route of administration, parenteral formulations accounted for 62.74% of the cephalosporin drugs market size in 2025 and are growing at a 7.22% CAGR to 2031.

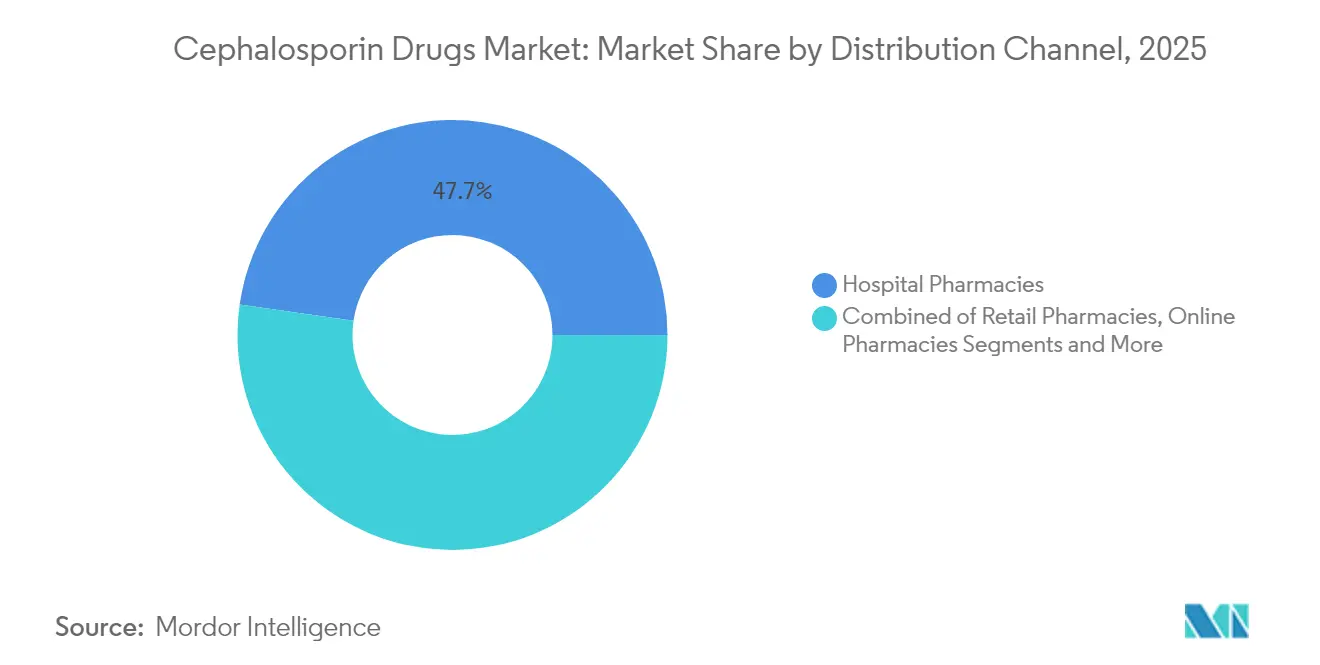

- By distribution channel, hospital pharmacies held 47.74% revenue share in 2025; online pharmacies record the highest forecast CAGR at 9.28% to 2031.

- By prescription type, prescription drugs dominated with an 79.65% share in 2025, yet OTC products are tracking a 6.12% CAGR to 2031.

- By indication, respiratory tract infections captured a 27.12% share of the cephalosporin drugs market size in 2025, while sepsis and meningitis surge at an 7.86% CAGR through 2031.

- By geography, North America commanded a 31.18% share in 2025, whereas Asia-Pacific is advancing at a 7.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cephalosporin Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Prevalence of MDR Gram-Negative Infections | +0.80% | Global, with highest impact in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Growth In Surgical Procedures & Hospital-Acquired Infections | +0.60% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Expedited QIDP & Antimicrobial Pull-Incentive Programs | +0.40% | United States, with spillover to regulatory-aligned markets | Short term (≤ 2 years) |

| WHO AWaRe Re-Classification Boosting LMIC Usage | +0.50% | Sub-Saharan Africa, South Asia, Latin America | Medium term (2-4 years) |

| Long-Acting Parenteral Depot Formulations for OPAT | +0.30% | North America & EU, early adoption in urban centers | Medium term (2-4 years) |

| Increasing Veterinary Approvals & Agri-Antibiotic Use | +0.20% | Global agricultural regions, concentrated in livestock-intensive areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Prevalence of MDR Gram-Negative Infections

Multidrug-resistant gram-negative pathogens now dominate hospital infection profiles, pushing clinicians toward fifth-generation cephalosporins that retain activity against ESBL-producing Enterobacterales. Klebsiella pneumoniae ST307 isolates show 85% resistance to third-generation agents, accelerating the adoption of ceftobiprole and cefepime-enmetazobactam combinations that remain effective. The Infectious Diseases Society of America’s 2024 guidance positions these advanced drugs as recommended therapy, enabling premium pricing despite generic competition. Hospitals also deploy combination regimens with beta-lactamase inhibitors, especially in intensive care units, creating long-run volume support for high-potency cephalosporin variants.

Growth in Surgical Procedures & Hospital-Acquired Infections

Increasing global surgical volumes correlate directly with cephalosporin prophylaxis demand. Guidelines endorse first- and second-generation agents for most interventions, achieving 3% infection rates when dozed within one hour before incision. Hospital-acquired pneumonia and sepsis protocols rely on early broad-spectrum coverage; studies demonstrate notable mortality reductions when cephalosporins are administered promptly. Outpatient surgery growth further expands need for short-acting formulations, while emerging economies add substantial new surgical capacity, sustaining the cephalosporin drugs market.

Expedited QIDP & Antimicrobial Pull-Incentive Programs

The U.S. FDA’s QIDP pathway grants five-year exclusivity extensions and priority review, materially improving cephalosporin R&D economics.[2]U.S. Food and Drug Administration, “Qualified Infectious Disease Product (QIDP) Designations,” fda.gov Since 2012, 147 designations have passed through the program, including Exblifep and Zevtera, both securing rapid approval and strategic pricing leeway. Although critics argue the policy favors incremental innovation, QIDP scaffolds investor confidence and channels R&D funds toward combination therapies that tackle resistance.

WHO AWaRe Re-Classification Boosting LMIC Usage

AWaRe guidance classifies many cephalosporins in the Access category, signalling governments in low- and middle-income countries to procure these agents for first-line treatment. The 2023 list directs funding toward ceftriaxone for pneumonia and sepsis, triggering higher tenders across South Asia and Sub-Saharan Africa. Aligning national formularies with AWaRe expands unit volumes, even under price-sensitive conditions, and anchors the cephalosporin drugs market in regions previously underserved by parenteral antibiotics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generic Price Erosion from Tender-Based Procurement | -0.70% | Global, particularly pronounced in emerging markets and public healthcare systems | Short term (≤ 2 years) |

| Global Antibiotic Stewardship Restrictions on Broad Use | -0.50% | North America & EU leading, expanding globally through WHO initiatives | Medium term (2-4 years) |

| Poor ROI Despite Pull Incentives Deterring R&D | -0.40% | Global pharmaceutical industry, concentrated in developed markets with high R&D costs | Long term (≥ 4 years) |

| Emerging Non-Antibiotic Modalities (Phage, CRISPR) | -0.30% | North America & EU early adoption, expanding to Asia-Pacific research centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Generic Price Erosion from Tender-Based Procurement

Patent expirations invite numerous generic entrants, and centralized tenders drive prices down swiftly, particularly for third-generation drugs. Hospitals that implemented strict restriction policies documented 46.2% spending drops after switching to the lowest-priced generics. Manufacturers must now lean on manufacturing scale or exit low-margin segments, intensifying consolidation within the cephalosporin drugs market.

Global Antibiotic Stewardship Restrictions on Broad Use

Mandatory stewardship programs curb empirical use of broad-spectrum antibiotics. The CDC notes that nearly 30% of in-hospital prescriptions are unwarranted, prompting decision-support systems and automatic stop orders. Such controls dampen cephalosporin volumes even where clinical need persists, underscoring the importance of targeted diagnostics and narrower formulations.[3]Centers for Disease Control and Prevention, “Core Elements of Hospital Antibiotic Stewardship,” cdc.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Generation: Fifth-Generation Innovation Drives Premium Growth

Third-generation molecules held 44.02% of the cephalosporin drugs market share in 2025, owing to dependable coverage across respiratory, urinary, and intra-abdominal infections. However, continuous resistance pressure propels fifth-generation agents, which are forecast to clock a 8.68% CAGR through 2031. Ceftobiprole’s 2024 approval illustrates how expanded gram-positive and gram-negative spectra elevate therapeutic value and sustain premium pricing. Fourth-generation cefepime, paired with modern beta-lactamase inhibitors, also gains traction because composite response rates top 79.1% in difficult urinary tract infections. The cephalosporin drugs market size for advanced generations is therefore widening faster than volumes indicate, as hospitals pay a premium for resistance-breaking efficacy.

Fiscal incentives embedded in QIDP statutes prolong exclusivity for novel combinations, encouraging firms to position fifth-generation drugs at the apex of formulary hierarchies. Nonetheless, cost-focused payers favor third-generation generics for routine cases, forcing manufacturers to balance high-margin innovation with high-volume legacy franchises. This dynamic generates a bifurcated competitive field where pricing strategy and antimicrobial performance co-determine adoption.

By Prescription Type: OTC Growth Signals Access Expansion

Prescription medicines commanded 79.65% of 2025 revenue because complex dosing regimens and resistance concerns require medical oversight. Yet the OTC sub-segment advances at a 6.12% CAGR as regulators in select Asia-Pacific markets permit pharmacist-guided supply for mild infections. This controlled liberalization lowers patient wait times and streamlines primary care burdens, broadening participation in the cephalosporin drugs market.

Growing digital pharmacies further bolsters OTC uptake by integrating virtual consultation modules that satisfy legal requisites for antibiotic sales. In contrast, high-income markets persist with prescription status, citing stewardship priorities. The resulting patchwork regulatory canvas leaves multinational firms tailoring SKU portfolios to disparate access models while maintaining vigilance on safety and resistance monitoring.

By Route of Administration: Parenteral Dominance Reflects Severity

Parenteral formats captured 62.74% of the cephalosporin drugs market size in 2025 because critical illnesses demand rapid therapeutic levels obtainable only by intravenous infusion. OPAT expansion, backed by wearables and elastomeric pumps, pushes parenteral CAGR to 7.22% as care migrates from inpatient wards to community settings. Subcutaneous innovation achieving 96% bioavailability could further convert certain oral regimens into injectable step-downs, consolidating parenteral primacy.

Oral dosages still cover uncomplicated respiratory and urinary tract infections but face adherence and absorption challenges. Manufacturers invest in palatable suspensions and sustained-release tablets to defend this niche. Nonetheless, payers widely accept higher costs for parenteral drugs when clinical guidelines mandate swift bacterial clearance, preserving their revenue dominance within the cephalosporin drugs market.

By Indication: Sepsis Emergence Drives Critical Care Focus

Respiratory tract infections retained the top spot with 27.12% market share in 2025, reflecting entrenched guideline support for ceftriaxone and similar agents. However, heightened awareness of sepsis pushes that segment to an 7.86% CAGR, outpacing all others as emergency departments implement early antibiotic bundles. Japanese and U.S. sepsis protocols specify cephalosporins as empirical cornerstones, raising demand for agents with robust gram-negative activity.

Incidence tracking shows that meningitis admissions also climb, especially in Sub-Saharan Africa, sustaining the need for high-penetrance cephalosporins. Skin-structure and urinary tract infections remain stable but are increasingly managed with cheaper generics, illustrating how clinical severity levels dictate therapeutic hierarchy in the cephalosporin drugs market.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Hospital pharmacies were responsible for 47.74% of sales in 2025 because they control parenteral inventory for acute admissions. Yet online channels grow swiftly at 9.28% CAGR as e-commerce platforms integrate e-prescription verification and cold-chain logistics. Expanded broadband access, mobile payments, and prescription-upload tools position virtual pharmacies as convenient portals, especially for chronic or recurrent infections.

Retail outlets preserve relevance for post-discharge oral step-downs, though margin pressures intensify as online rivals offer lower prices. Hospitals respond by partnering with logistics firms to extend infusion services to homes, blurring boundaries between institutional and community supply. This convergence validates omnichannel strategies to reach every touchpoint in the cephalosporin drugs market.

Geography Analysis

North America led with 31.18% revenue in 2025, due to advanced hospitals, high surgical throughput, and QIDP-driven innovation pipelines. U.S. antimicrobial stewardship rules ensure rational use without compromising timely access, and Canada’s provincial formularies prioritize cost-effectiveness while retaining broader-spectrum options for critical care. Large payer systems negotiate steep volume discounts, restraining headline growth but cementing baseline demand for both generic and premium cephalosporins across the cephalosporin drugs market.

Asia-Pacific registers the fastest 7.55% CAGR through 2031, underpinned by capacity expansions in China and India, rising health expenditures, and alarming resistance rates that necessitate advanced formulations. Partnerships such as Orchid Pharma–Cipla’s launch of cefepime-enmetazobactam underscore local manufacturing’s role in broadening access. Government tenders linked to universal health schemes stimulate large-volume purchases, although intense price competition requires firms to balance profitability with scale.

Europe maintains steady mid-single-digit growth as evidence-based prescribing and rapid diagnostics temper unnecessary usage. Harmonized EMA approvals allow simultaneous launches with the U.S., enabling companies to leverage unified marketing campaigns across major markets. The United Kingdom’s post-Brexit regulatory adjustments introduce moderate uncertainty, but overall adherence to WHO stewardship guidance creates predictable demand patterns that privilege newer combinations able to overcome endemic ESBL prevalence.

Regulatory Landscape

Regulatory Landscape: Antimicrobial resistance controls and expedited review tools for serious infections continue to shape how cephalosporin drugs are developed and authorized. In the United States, the FDA uses Qualified Infectious Disease Product (QIDP) designations to accelerate development and extend exclusivity for eligible antibacterial innovations, supporting approvals of newer cephalosporin combinations intended for resistant Gram-negative pathogens.

Across major markets, access and stewardship frameworks sit alongside conventional marketing authorization requirements. The European Union maintains centralized review and authorization through the EMA and the European Commission, as illustrated by the European Commission marketing authorization for Exblifep (cefepime/enmetazobactam) in March 2024. At a global policy level, the WHO Model List of Essential Medicines (24th list released in September 2025) and the AWaRe classification keep guiding national formulary inclusion and procurement priorities for widely used cephalosporins such as cefotaxime and ceftriaxone, especially in public-sector systems.

Value Chain Analysis

The cephalosporin drugs value chain starts with fermentation and chemical synthesis of core intermediates (notably 7-ACA and 7-ADCA), then moves to API production and sterile or oral finished-dosage manufacturing, followed by distribution into hospital, retail, and online pharmacy channels. Because beta-lactam production requires dedicated manufacturing lines and contamination-control systems, the number of qualified sites is limited, which makes supply reliability a key differentiator in tender-driven markets.

Quality and traceability expectations continue to tighten across the chain, increasing compliance workload for intermediate and API producers and influencing make-versus-buy decisions. In April 2026, the U.S. FDA issued a draft guidance on establishing impurity specifications for antibiotics, reinforcing scrutiny of impurity profiling in fermentation and semi-synthetic products. Separately, policy actions focused on manufacturing oversight and supply-chain visibility, including the FDA's July 2026 proposed rule for distributed manufacturing registration and clarification of foreign establishment obligations, raise documentation and operational-control requirements for companies supplying cephalosporin APIs and finished products globally.

Competitive Landscape

The cephalosporin drugs market is moderately consolidated. Pfizer, Roche, and Merck exploit global distribution networks and established brand equity, whereas Basilea Pharmaceutica, Venatorx Pharmaceuticals, and Allecra Therapeutics carve niches with beta-lactamase-inhibitor pairings that address specific resistance gaps. Strategic alliances proliferate: Venatorx teamed with Menarini for Europe-wide commercialization of cefepime-taniborbactam, while Shionogi’s acquisition of Qpex Biopharma strengthens its late-stage pipeline.

Artificial-intelligence-assisted discovery gains foothold; Eli Lilly collaborates with OpenAI to accelerate lead identification for next-gen antimicrobials. This technology convergence compresses development timelines and may offset historically low returns on antibiotic investment. Meanwhile, veterinary approvals for drugs such as pradofloxacin generate additional revenue streams yet raise stewardship debate, compelling firms to navigate divergent regulatory terrains.

Portfolio strategies now emphasize life-cycle management: once human indications lose exclusivity, companies file for pediatric, outpatient depot, or animal health extensions to sustain cash flows. Manufacturers also invest in vertically integrated supply chains to mitigate raw material shortages and differentiate on reliability—a decisive factor in tender awards. Collectively, these moves strengthen competitive moats while keeping acquisition prospects vibrant as larger players seek assets with validated resistance-breaking profiles.

Global Cephalosporin Drugs Industry Leaders

Baxter International

GlaxoSmithKline PLC

Lupin Pharmaceuticals Inc.

Pfizer Inc.

Teva Pharmaceutical Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are concentrated in next-generation combinations designed for multidrug-resistant Gram-negative infections, particularly where stewardship constraints still allow differentiated formulary positioning. A specific proof point is the U.S. FDA approval of Wockhardt's Zaynich (cefepime/zidebactam) in May 2026 for complicated urinary tract infections, which broadens the set of cephalosporin-based options aimed at difficult-to-treat hospital pathogens and supports launches that go beyond commodity third-generation injectables.

A second whitespace area is upstream resilience for key starting materials and intermediates, where regional capacity additions can reduce exposure to concentrated supply and contamination-related shutdown risks. India illustrates this direction, with Orchid Pharma's March 2026 groundbreaking for a fermentation-based 7-ACA facility in Kathua, which positions domestic intermediate supply closer to finished-dose manufacturing ecosystems. Alongside capacity, process innovation in strain engineering, including CRISPR/Cas9 approaches in industrial organisms used to produce cephalosporin precursors, supports improved yields and impurity profiles. This aligns manufacturing economics with stricter quality expectations while feeding large-volume, public-procurement demand influenced by WHO AWaRe and essential-medicines adoption.

Recent Industry Developments

- June 2026: Lupin Pharmaceuticals updated its US product catalog to include multiple cephalosporin antibiotics such as cefadroxil, cefdinir, and cefprozil, reflecting continued portfolio maintenance in a highly competitive generics landscape. The refresh supports commercial continuity across retail and outpatient channels where SKU breadth and reliable supply help maintain pharmacy placements and contract coverage.

- May 2025: Innoviva Specialty Therapeutics expanded Zevtera (ceftobiprole) availability in the United States following approval for bacteremia, skin infections, and pneumonia. This expansion enables broader hospital adoption and formulary consideration.

- June 2024: Orchid Pharma and Cipla introduced cefepime-enmetazobactam in India, expanding local access to a cephalosporin plus beta-lactamase inhibitor combination aimed at resistant hospital pathogens. The launch aligns with growing demand for advanced parenteral therapies in Asia-Pacific and reinforces the role of domestic manufacturing and partnerships in scaling availability under price-sensitive procurement.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the cephalosporin drugs market is defined as the global revenue generated from finished cephalosporin antibiotic medicines used in human therapy, across oral and injectable dosage forms, and sold through hospital and retail supply chains.

Scope exclusions: We exclude veterinary use, bulk cephalosporin API sales, and combination therapies where a cephalosporin is not the primary active ingredient.

Segmentation Overview

- By Generation

- First-generation

- Second-generation

- Third-generation

- Fourth-generation

- Fifth-generation

- By Prescription Type

- Prescription Drugs

- OTC Drugs

- By Route of Administration

- Oral

- Parenteral

- By Indication

- Respiratory Tract Infections

- Urinary Tract Infections

- Skin & Soft-Tissue Infections

- Sepsis & Meningitis

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the market boundaries, align drug class definitions, and build a first view of demand and supply signals. We referenced public health and surveillance outputs such as those from the World Health Organization, the US CDC, and ECDC, along with treatment guideline updates from bodies such as IDSA where they were available.

To ground the demand pool, we also reviewed official statistics and repositories such as the World Bank, OECD health data, and national health ministry publications, followed by peer reviewed journals for resistance trends and prescribing shifts across generations. On the supply side, company annual reports, investor presentations, and reputable press were reviewed to understand portfolio focus and manufacturing footprints. Where available, we also used paid subscriptions for company financials, news and financials, patent databases, and shipment level trade data to cross-check signals. These desk sources are illustrative only, and many other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating real use of cephalosporins by generation, the split between oral and injectable demand, and how pricing behaves under tenders and hospital protocols. We spoke with a mix of manufacturers, distributors, pharmacists, and clinicians across major regions so gaps from desk research could be filled. We then rechecked key assumptions before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 17% | APAC: 44% |

| Mid tier: 44% | Functional/Unit leaders: 35% | EMEA: 37% |

| Smaller Players: 20% | Managers: 48% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where epidemiology and treated-patient volumes are translated into therapy demand. That demand is then filtered through route of administration and care-setting mix to estimate sell-through value. In practice, the demand pool is shaped using inputs such as bacterial infection incidence patterns, inpatient versus outpatient treatment share, stewardship guidance like the WHO AWaRe framing, penetration of later-generation cephalosporins in severe cases, and tender-driven price corridors for key molecules.

The totals are then checked with selective bottom-up approximations so the result stays practical. These checks include sampled ASP times volume logic by dosage form, channel mix validation through distributor feedback, and supplier revenue signals where disclosure allows. Where direct splits are not available, gaps are handled using proxy weights from comparable countries.

For forecasting, scenario analysis is used as the main technique because uptake and pricing are sensitive to policy and resistance. Assumptions on infection burden, stewardship tightening, generic intensity, and hospital procurement behavior are stress-tested with primary inputs, and the final trajectory is kept consistent with observed price erosion and mix shift patterns across generations.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including treated patient logic, pricing checks by route and channel, and reconciliation against disclosed company performance cues. When an outlier appears, the drivers are decomposed, inputs are revisited, and follow-up calls are triggered to confirm whether the change is real or a data artifact.

Before sign-off, the model goes through a multi-step analyst review so assumptions, unit conversions, and currency treatments are consistent across regions. The report is refreshed annually, and interim updates are made when material events occur, such as major guideline changes, large tender resets, or new approvals that alter generation mix. Right before delivery, a final review pass is performed so the numbers reflect the latest available public and field inputs.

Mordor Intelligence's Cephalosporin Drugs Market Estimate Compared With Other Published Estimates

Published market values for cephalosporin drugs can differ even when they look like they are talking about the same thing, mainly because the scope boundary and the pricing logic are not handled the same way. The year used, the treatment of combination therapies, and the way hospital tenders are reflected in average selling prices can all move the final total.

By tracking dosage-form level demand signals and refreshing tender-linked ASP assumptions through primary validation, Mordor Intelligence keeps the estimate tied to finished human-use cephalosporin sales and avoids mixing in bulk API revenues or non-primary combinations, which is a common source of spread.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 21.24 B (2026) | |

| Global Research Publisher A | USD 20.65 B (2025) | Uses a different base year and forecast window, and the price progression appears to be smoothed at a broad regional level without explicitly reflecting hospital tender resets by molecule and dosage form. |

| Industry Research Publisher B | USD 19.38 B (2023) | Anchors the market on an earlier year and may understate later-generation mix shift effects, which can matter when injectable hospital demand is rising faster than retail oral volumes. |

The table highlights that timing and what is counted drive most of the gap. When the scope is limited to finished human-use products and pricing is checked against procurement behavior, the market size becomes easier to trace to real demand indicators and repeatable calculation steps.

Key Questions Answered in the Report

What is the current size of the cephalosporin drugs market?

The cephalosporin drugs market is valued at USD 21.24 million in 2026, with a forecast to reach USD 24.59 million by 2031 at a 2.97% CAGR.

Which cephalosporin generation is growing fastest?

Fifth-generation cephalosporins are projected to expand at a 8.68% CAGR through 2031 due to their activity against multidrug-resistant pathogens.

Why do parenteral formulations dominate the cephalosporin drugs market?

Severe infections require rapid serum concentrations that only intravenous delivery can provide, giving parenteral formats 62.74% revenue share in 2025 and a 7.22% growth rate.

Which region is expected to post the highest growth?

Asia-Pacific is the fastest-growing region, advancing at a 7.55% CAGR to 2031, driven by expanding healthcare access and high antimicrobial resistance rates.

How are stewardship programs affecting cephalosporin demand?

Stewardship initiatives reduce unnecessary broad-spectrum use, trimming volume growth; however, they also encourage adoption of newer, more targeted cephalosporins that deliver better clinical outcomes.

Page last updated on: