Hyoscine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

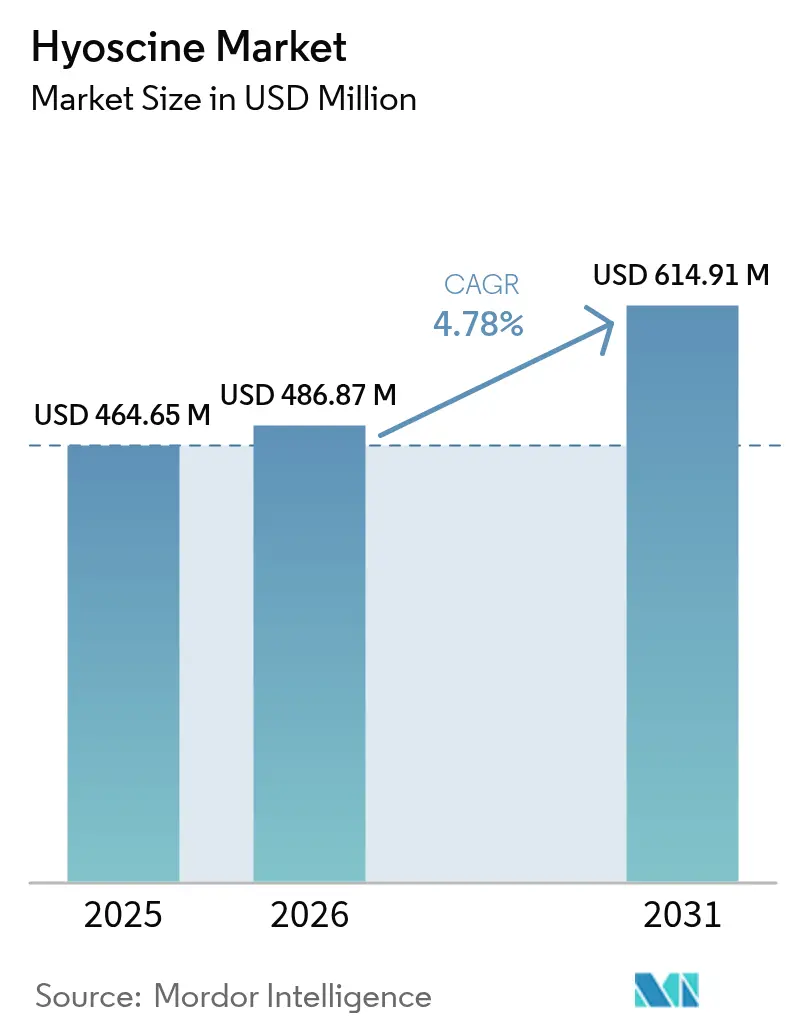

| Market Size (2026) | USD 486.87 Million |

| Market Size (2031) | USD 614.91 Million |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

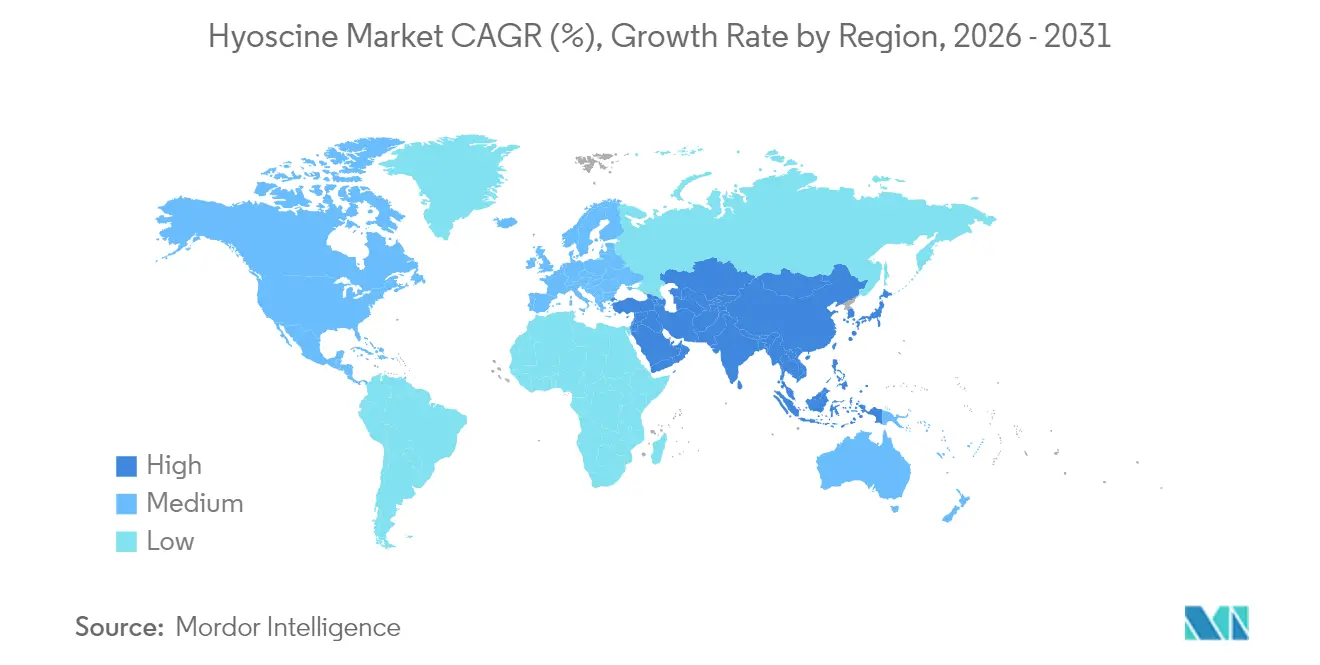

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hyoscine Market Analysis by Mordor Intelligence

The hyoscine market size was valued at USD 464.65 million in 2025 and estimated to grow from USD 486.87 million in 2026 to reach USD 614.91 million by 2031, at a CAGR of 4.78% during the forecast period (2026-2031). Momentum comes from wider recognition of the drug’s anticholinergic versatility, a growing body of clinical evidence in postoperative nausea and vomiting (PONV) protocols, and sustained investment in advanced transdermal platforms. Rising surgical volumes, increased global travel, and heightened diagnosis of functional gastrointestinal disorders all reinforce demand. Competition centres on differentiated delivery technologies that promise steady plasma levels while mitigating anticholinergic burden. Meanwhile, supply-side pressures tied to Duboisia cultivation spur vertical integration and bio-engineered alkaloid initiatives in Australia and India.

Key Report Takeaways

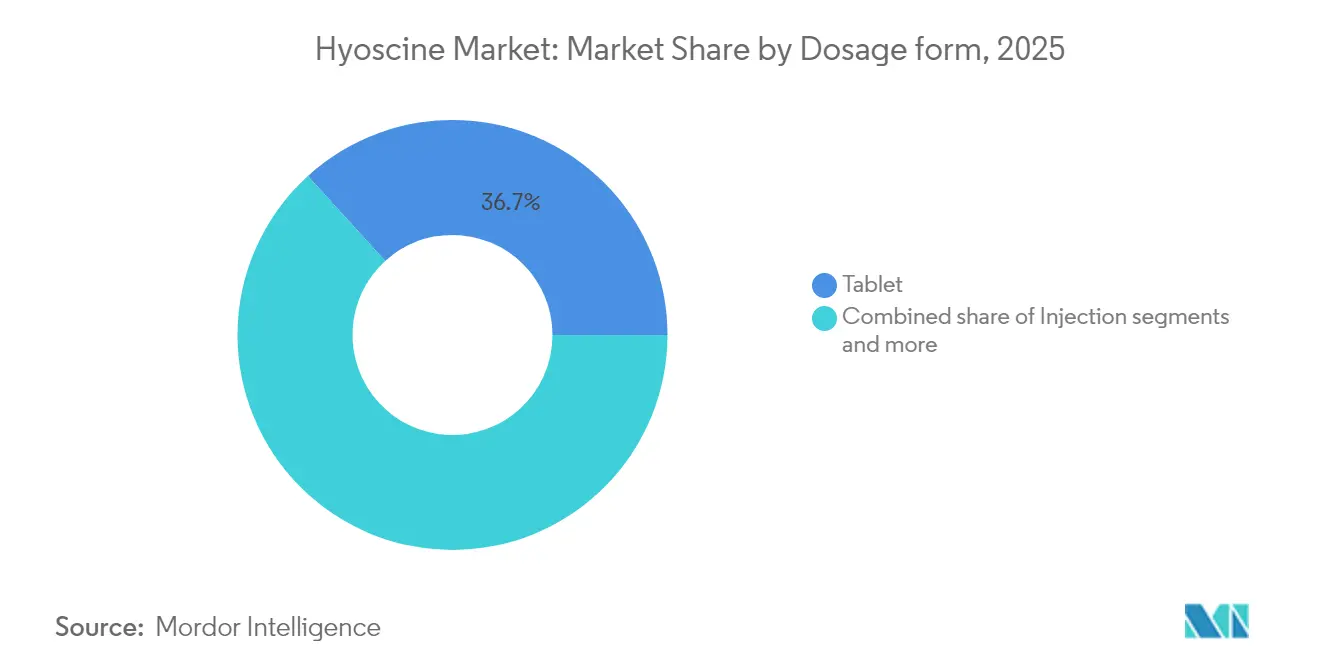

- By dosage form, tablets accounted for 36.74% of 2025 revenue, whereas transdermal patches are growing fastest at a 6.37% CAGR through 2031.

- By indication, motion sickness captured 38.35% of 2025 demand, while neurological disorders are projected to deliver the highest 6.8% CAGR to 2031.

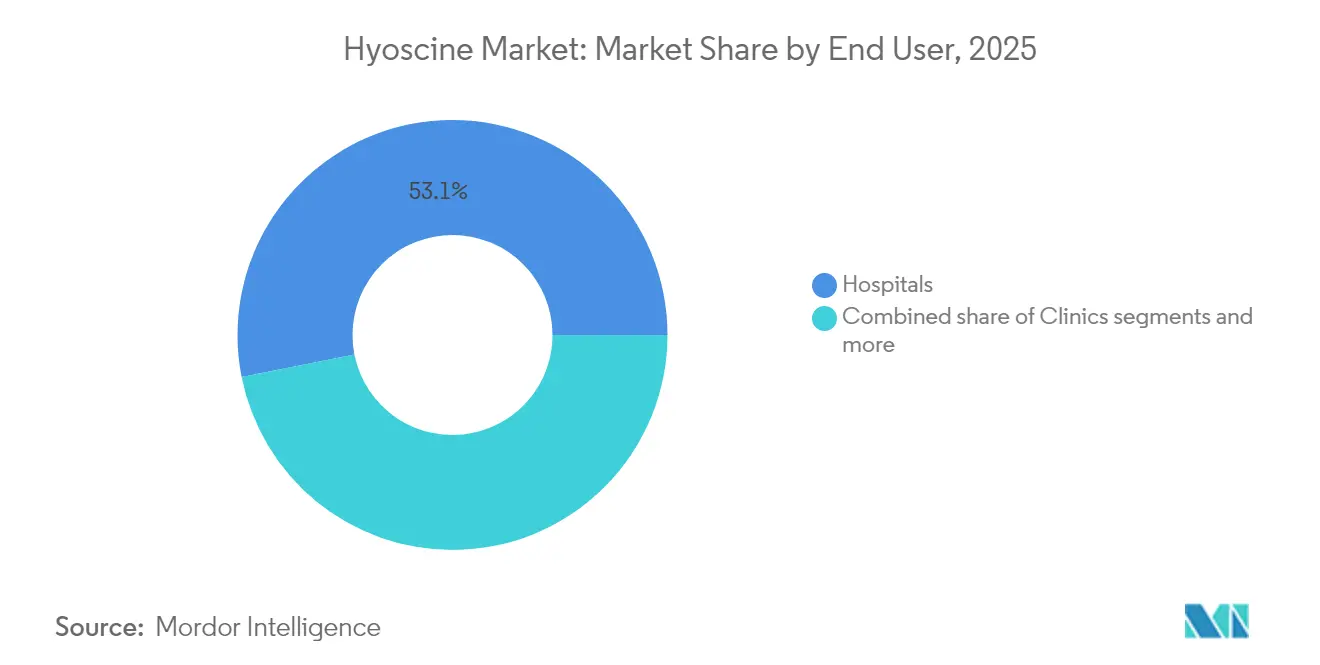

- By end user, hospitals held 53.12% of 2025 revenue, yet home-care settings are expanding at a 7.29% CAGR to 2031.

- By geography, North America commanded 41.68% of 2025 revenue; Asia-Pacific is on track for the quickest 7.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hyoscine Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of motion sickness | +0.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growing prevalence of gastrointestinal disorders | +1.2% | Global, particularly Asia-Pacific emerging markets | Long term (≥ 4 years) |

| Surge in surgical procedures leading to PONV | +1.0% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Adoption of advanced transdermal delivery systems | +0.9% | Developed markets, spill-over to emerging economies | Long term (≥ 4 years) |

| Experimental use in neuro-psychiatric disorders | +0.7% | North America & EU research centers | Long term (≥ 4 years) |

| Bio-engineered Duboisia cultivation boosting supply | +0.4% | Australia, with technology transfer to India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Motion Sickness

Growing passenger kilometres by air, sea, and autonomous vehicles heighten vestibular conflicts that precipitate motion sickness. Transdermal scopolamine delivers up to 72-hour prophylaxis, outperforming shorter-acting orals and supporting premium pricing in the hyoscine market. Military programs exploring intranasal formats underscore new mission-critical niches. With tourism rebounding and virtual reality headsets becoming mainstream, the addressable base widens further.

Growing Prevalence of Gastrointestinal Disorders

Irritable bowel syndrome rates are climbing on dietary shifts, urban stressors, and improved diagnostics in Asia-Pacific. Hyoscine butylbromide, a peripherally acting antispasmodic, increasingly features as first-line therapy in clinical guidelines. WHO’s essential-medicine listing shields demand from generic erosion, while paediatric safety reviews hint at label extensions that will augment the hyoscine market.

Surge in Surgical Procedures Leading to PONV

Minimally invasive and day-case surgeries are rising, yet PONV still affects up to 30% of general cases and over 50% of high-risk cohorts. Muscarinic blockade complements serotonin antagonists, delivering additive symptom control and shorter recovery stays. Evidence of safety in breastfeeding mothers following caesarean section broadens use in obstetric theatres.

Adoption of Advanced Transdermal Delivery Systems

Next-generation patches employ micro-reservoirs and stimulus-responsive polymers for predictable flux, addressing historical variability complaints. Real-time terahertz spectroscopy now validates in-vivo diffusion without biopsies, supporting quality-by-design manufacturing. Home-care uptake soars because patches reduce dosing frequency and caregiver oversight, a boon for the hyoscine market in ageing societies.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Anticholinergic side-effect profile | -0.8% | Global, particularly affecting geriatric populations | Short term (≤ 2 years) |

| Stringent prescription & regulatory controls | -0.6% | North America & EU, expanding to emerging markets | Medium term (2-4 years) |

| Duboisia crop volatility due to climate change | -0.4% | Australia & India cultivation regions | Long term (≥ 4 years) |

| Geriatric formulary exclusion trends | -0.3% | Developed markets with aging populations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Anticholinergic Side-Effect Profile

Dry mouth, blurred vision, delirium, and urinary retention limit dose escalation, especially in patients above 60 years where pneumonia and mortality risks rise. Recent FDA warnings on heat-related complications when patches interact with external warming sources accentuate caution[1]Source: U.S. Food and Drug Administration, “FDA Adds Warning About Serious Risk of Heat-Related Complications,” fda.gov. Hospitals now deploy stricter monitoring and risk-stratification algorithms, which may constrain near-term gains for the hyoscine market.

Stringent Prescription & Regulatory Controls

Misuse in criminal assaults and concerns over paediatric toxicity have tightened scheduling in several jurisdictions. Complete response letters for novel intranasal submissions underline lengthy approval cycles and elevated compliance costs[2]Source: Defender Pharmaceuticals, “Complete Response Letter for Intranasal Scopolamine,” defenderpharma.com . Smaller manufacturers struggle to fund the pharmacovigilance infrastructure now required, heightening entry barriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage Form: Transdermal Innovation Drives Growth

Tablets led 2025 revenue with 36.74% hyoscine market share following decades of physician familiarity and low unit cost. However, transdermal patches are projected to clock 6.37% CAGR and could capture a larger slice of the hyoscine market size as sustained-release formats gain favour among travellers and elderly users.

Injection formats retain relevance in emergency departments that value rapid onset, yet adoption outside hospital walls remains modest due to administration complexity. Oral solutions serve paediatric and dysphagic cohorts, while pipeline nasal gels target military and spaceflight settings. Overall, patch technology is propelling differentiation within the hyoscine market through longer dwell times and adherence-friendly designs.

By Indication: Neurological Applications Gain Momentum

Motion sickness prevailed with 38.35% of 2025 revenue, a testament to post-pandemic travel recovery. Nonetheless, neurological disorders are poised for the highest 6.8% CAGR as rapid-acting antidepressant trials progress. Early data show meaningful mood improvements within hours, positioning scopolamine toward unmet psychiatric needs.

Gastrointestinal use cases remain stable, anchored by rising IBS diagnostics in Asia-Pacific. PONV demand mirrors global surgical volumes, especially in laparoscopic and obstetric theatres. Respiratory indications represent a smaller but durable niche. The diversification of use cases reinforces the resilience of the hyoscine market.

By End User: Home Care Settings Accelerate

Hospitals controlled 53.12% of 2025 consumption because formulary inclusion and perioperative protocols rely on hyoscine for multimodal antiemesis. Yet home-care settings will expand fastest at 7.29% CAGR through 2031, thanks to telehealth supervision and user-friendly patches that limit dosing errors.

Clinics bridge acute hospital services and at-home therapy, benefiting from growth in day-case procedures. The COVID-19 hangover continues to push healthcare toward decentralised delivery, an environment in which hyoscine market participants offering tamper-evident packaging and e-label guidance stand to win share.

Geography Analysis

North America generated 41.68% of 2025 revenue due to entrenched reimbursement and early adoption of controlled-release formats. Europe follows closely, buoyed by older demographics and stringent PONV guidelines that specify anticholinergic combinations. North American suppliers also benefit from captive Duboisia plantations that buffer botanical supply risk.

Asia-Pacific is forecast to post the highest 7.81% CAGR, lifted by improving diagnostic penetration, rising medical tourism, and government drives to localise active pharmaceutical ingredient production. India’s regulatory overhauls, including fast-track plant clearances and pharmacovigilance digitisation, are fostering capacity additions and scale that can reshape the hyoscine market.

Latin America and Middle East & Africa offer longer-term optionality but remain sensitive to price ceilings and patch import tariffs. Multinationals leverage partnered distribution and tiered-pricing to maintain presence, yet supply interruptions from climatic Duboisia shocks can impede service levels. Geographic diversification of plantations is therefore a strategic hedge for the hyoscine market.

Competitive Landscape

The hyoscine market is moderately fragmented. Leading firms pair vertically integrated alkaloid farming with proprietary patch technologies that command premium margins. Recent consolidation talk—including Alkem Laboratories’ USD 3 billion pursuit of JB Chemicals—reflects a push for scale-based cost leverage.

Developers of electronic-enabled patches capable of personalised dose modulation have tightened their hold on high-value home-care channels. Generic manufacturers focus on tablets and injectables, banking on formulary price wins in emerging markets. Supply reliability remains a key differentiator: companies with diversified Duboisia farms in Australia and India mitigate climatic shocks, while others source alkaloids on the spot market and risk cost volatility.

Strategic moves include Baxter’s 2025 bundle-pricing initiative that tied Scopoderm with infusion pumps for ambulatory surgery centres, and Amneal’s payor agreements that widened neurological product coverage beyond 50% of US lives. Quality lapses, such as Viatris’ 2024 warning letter, highlight ongoing compliance challenges and reinforce the premium on cGMP track records for the hyoscine market.

Hyoscine Industry Leaders

Caleb Pharmaceuticals, Inc

Baxter International

Alchem International Pvt. Ltd

Perrigo

GSK plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: FDA issued enhanced safety warnings for Transderm Scōp patches regarding serious heat-related complications

- April 2025: Amneal Pharmaceuticals announced expanded insurance coverage for CREXONT.

Global Hyoscine Market Report Scope

As per the scope of the report, Hyoscine is an effective medicine for motion sickness and is used to treat postoperative nausea, gastrointestinal spasm, and vomiting. This medicine belongs to the antimuscarinic family and works by blocking some acetylcholine effects within the nervous system.

The hyoscine market is segmented by Type (Hyoscine Butyl Bromide, Hyoscine Hydrobromide), Mode of Administration (Oral, Patches, Injections), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value in USD million for the above segments.

| Tablets |

| Injection |

| Transdermal Patch |

| Oral Solutions |

| Others |

| Motion Sickness |

| Gastrointestinal Disorders |

| Post-operative Nausea & Vomiting (PONV) |

| Neurological Disorders |

| Respiratory Disorders |

| Others |

| Hospitals |

| Clinics |

| Home-care Settings |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Dosage Form (Value) | Tablets | |

| Injection | ||

| Transdermal Patch | ||

| Oral Solutions | ||

| Others | ||

| By Indication (Value) | Motion Sickness | |

| Gastrointestinal Disorders | ||

| Post-operative Nausea & Vomiting (PONV) | ||

| Neurological Disorders | ||

| Respiratory Disorders | ||

| Others | ||

| By End User (Value) | Hospitals | |

| Clinics | ||

| Home-care Settings | ||

| Others | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the hyoscine market by 2031?

The hyoscine market is forecast to reach USD 614.91 million by 2031, growing at a 4.78% CAGR.

Which dosage form is expanding fastest?

Transdermal patches are on course for a 6.37% CAGR, the quickest among all formats.

Why is Asia-Pacific viewed as the growth engine?

Better healthcare access, rising disposable income, and local API capacity are driving a 7.81% CAGR in Asia-Pacific.

What are the main restraints facing the hyoscine market?

Dose-limiting anticholinergic effects and increasingly strict global prescription controls are the primary brakes on growth.

Page last updated on: