Non-steroidal Anti-Inflammatory Drugs (NSAIDs) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.48 Billion |

| Market Size (2031) | USD 33.57 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-steroidal Anti-Inflammatory Drugs (NSAIDs) Market Analysis by Mordor Intelligence

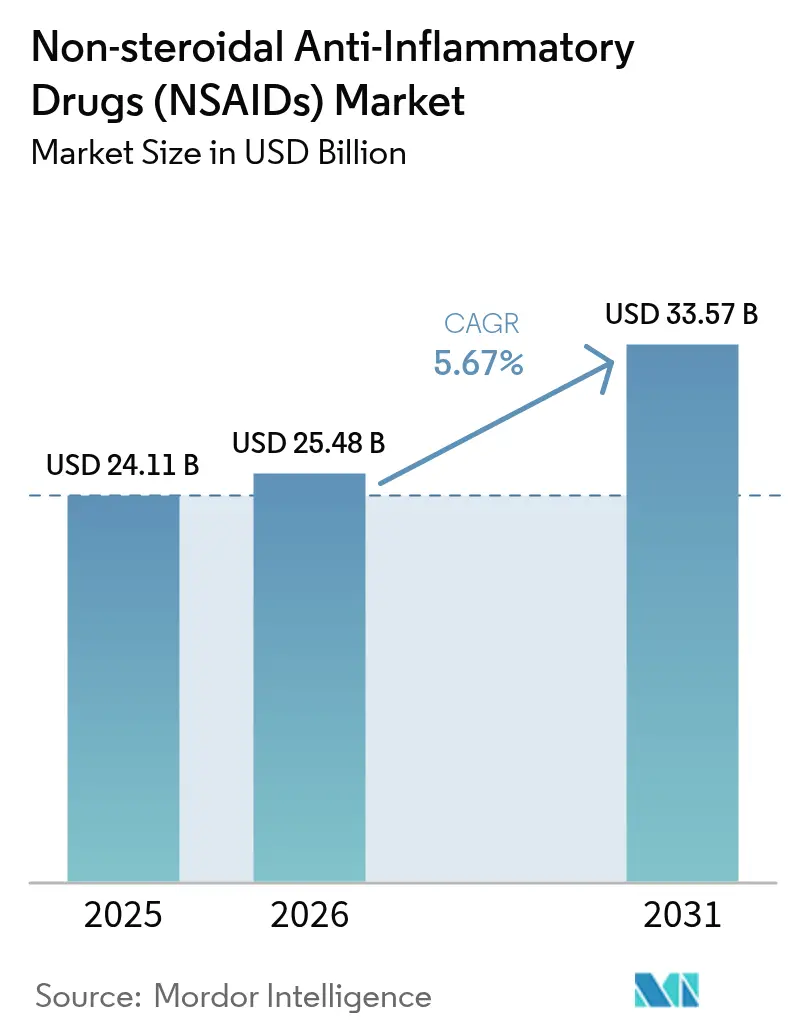

The NSAIDs market size was valued at USD 24.11 billion in 2025 and estimated to grow from USD 25.48 billion in 2026 to reach USD 33.57 billion by 2031, at a CAGR of 5.67% during the forecast period (2026-2031). Demand rises as health systems look for non-opioid pain options, aging populations grow, and over-the-counter (OTC) access expands. Volume gains are tempered by gastrointestinal (GI) and cardiovascular safety warnings, patent expirations, and heightened regulatory scrutiny. North America leads revenue today, yet Asia-Pacific grows fastest as wider insurance coverage and online pharmacies broaden access. Product strategy pivots toward topical gels that mitigate systemic risks, while AI-supported reformulation helps companies extend lifecycles in the NSAIDs market.

Key Report Takeaways

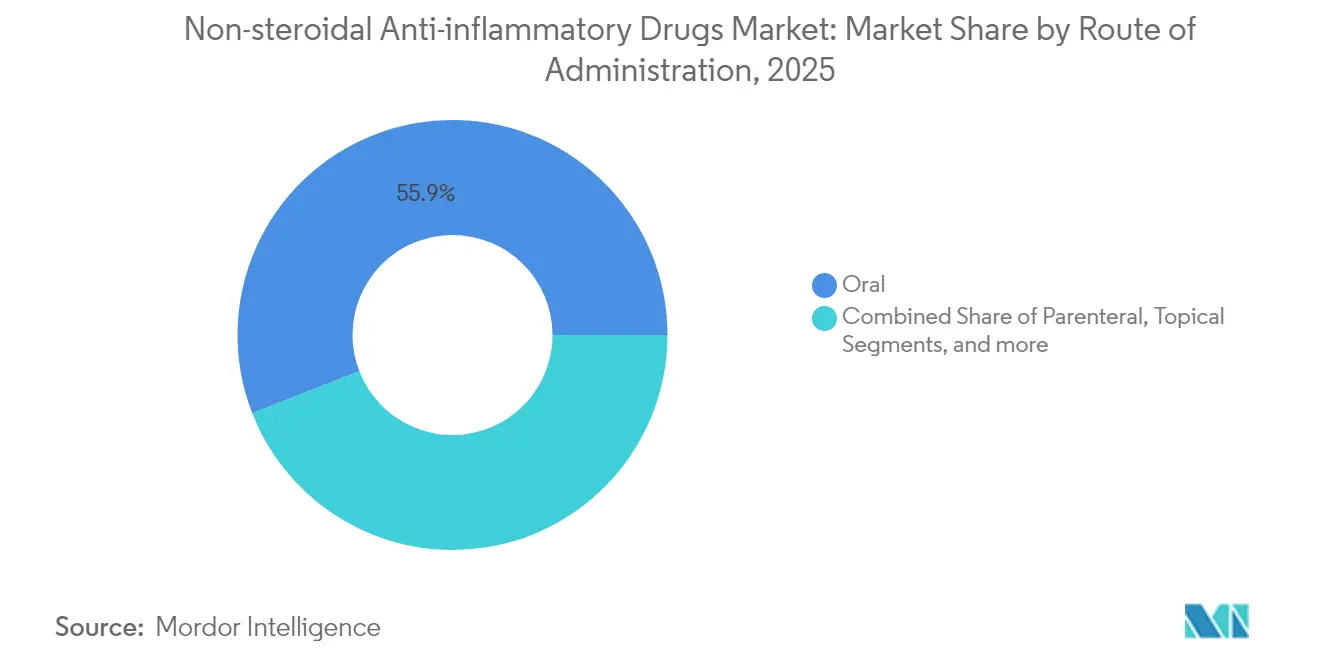

- By route of administration, oral delivery led with 55.92% of NSAIDs market share in 2025, while topical formulations are projected to expand at 6.18% CAGR to 2031.

- By drug class, non-selective COX inhibitors accounted for 61.77% share of the NSAIDs market size in 2025, whereas COX-2 selective drugs are set to grow at 6.32% CAGR through 2031.

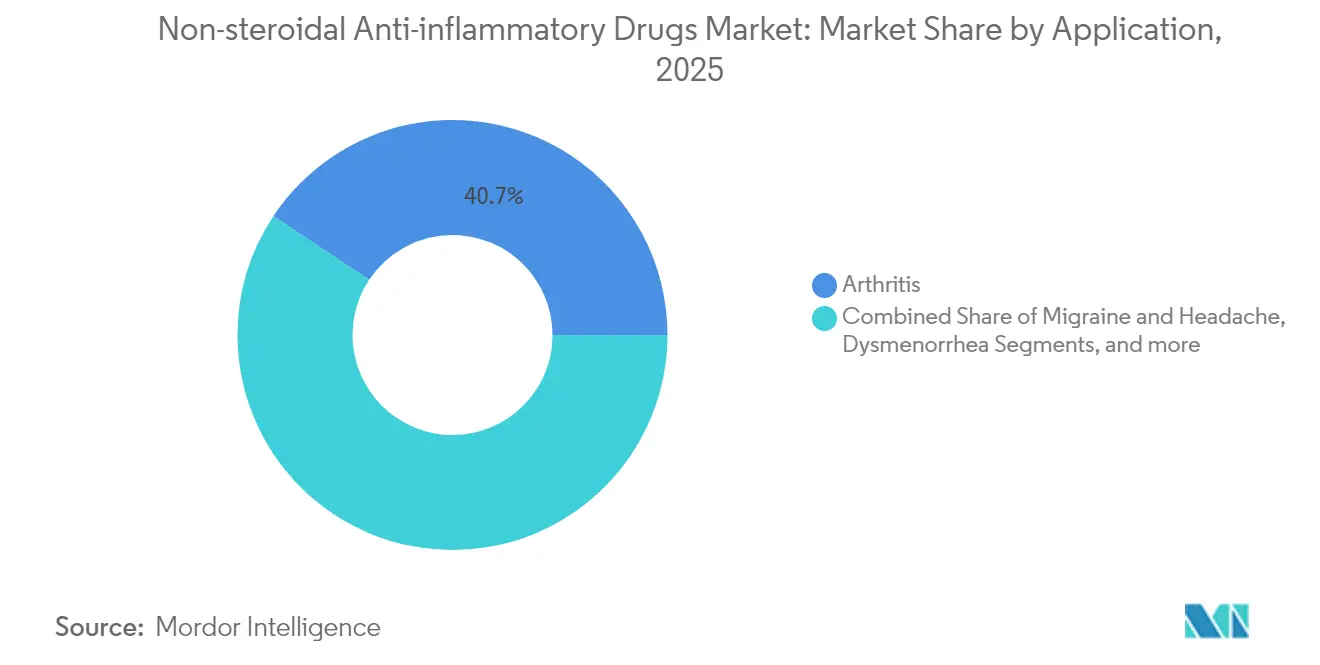

- By application, arthritis treatments captured 40.68% of NSAIDs market share in 2025; migraine therapies are forecast to advance at a 6.12% CAGR to 2031.

- By distribution channel, retail pharmacies controlled 45.98% of the NSAIDs market size in 2025, while e-commerce platforms are expected to rise at 6.41% CAGR.

- By geography, North America held 41.35% of NSAIDs market share in 2025; Asia-Pacific is positioned for the highest 6.29% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Non-steroidal Anti-Inflammatory Drugs (NSAIDs) Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global burden of chronic pain & inflammatory disorders | +1.8% | Global, with highest impact in aging populations of North America & Europe | Long term (≥ 4 years) |

| Preference for NSAIDs over opioids & acetaminophen | +1.2% | North America & Europe, expanding to APAC markets | Medium term (2-4 years) |

| Growing OTC availability & self-medication culture | +0.9% | Global, particularly strong in emerging markets of APAC & Latin America | Short term (≤ 2 years) |

| Emergence of fixed-dose-combination topical gels improving GI safety | +0.7% | North America & Europe initially, with gradual APAC adoption | Medium term (2-4 years) |

| AI-driven drug-repositioning accelerating low-cost reformulations | +0.4% | Global, led by innovation hubs in North America & Europe | Long term (≥ 4 years) |

| Expanding applications in specialized therapeutic areas | +0.3% | North America & Europe primarily, with selective APAC adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Burden of Chronic Pain & Inflammatory Disorders

Chronic pain affects more than 100 million adults worldwide, and osteoarthritis prevalence is set to climb sharply by 2050, reinforcing a structural need for anti-inflammatory drugs. Broader diagnostic capabilities in emerging economies widen the patient pool, while governments classify chronic pain as its own condition, supporting reimbursement for long-term NSAID therapy. Workforce productivity losses tied to untreated pain further justify coverage expansions. As a result, the NSAIDs market secures a stable demand base that transcends economic cycles.

Preference for NSAIDs Over Opioids & Acetaminophen

Clinical trials show an ibuprofen–acetaminophen regimen can equal hydrocodone’s pain relief with none of the addiction risk. US and EU prescribing guidelines now advise non-opioid first-line therapy, propelling formulary placement of NSAIDs. Because these products also treat inflammation, they out-perform acetaminophen in arthritis and sports injuries. Payers see cost savings versus opioid misuse expenses, reinforcing guideline adoption. This shift repositions the NSAIDs market as the cornerstone of moderate-pain management.

Growing OTC Availability & Self-Medication Culture

The FDA review of OTC Monograph M013 could widen non-prescription NSAID use in the United States[1]FDA, “Internal Analgesic, Antipyretic, and Antirheumatic Drug Products for Over-the-Counter Human Use; Monograph,” federalregister.gov. Emerging middle-class consumers in Asia and Latin America rely on pharmacy counters for primary care, boosting volumes. Digital symptom checkers support safe self-medication, while corporate wellness programs stock NSAID options to curb absenteeism. Together these factors funnel discretionary spending into the NSAIDs market.

Fixed-Dose-Combination Topical Gels Improving GI Safety

Topical diclofenac delivers pain relief comparable with oral tablets while reducing systemic exposure. New gels pair penetration enhancers with complementary actives, and real-world data covering 100,000 users show 70.8% buy only a single pack, suggesting rapid benefit and satisfaction (EFSM conference abstract). Payers and clinicians recommend these products for patients with cardiovascular or GI risks. The safety profile draws new users into the NSAIDs market and lengthens therapy duration for existing patients.

Restraints Impact Analysis of Non-steroidal Anti-Inflammatory Drugs (NSAIDs) Market*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GI & cardiovascular adverse events prompting regulatory warnings | -1.4% | Global, with strictest enforcement in North America & Europe | Short term (≤ 2 years) |

| Patent cliffs & price erosion for blockbuster brands | -0.8% | North America & Europe primarily, with spillover to global markets | Medium term (2-4 years) |

| Increasing healthcare cost pressures and generic competition | -0.6% | Global, with highest impact in cost-sensitive emerging markets | Short term (≤ 2 years) |

| Growing awareness of drug interactions and contraindications | -0.4% | North America & Europe primarily, expanding to APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GI & Cardiovascular Adverse Events Prompting Regulatory Warnings

The FDA and European Medicines Agency (EMA) now require boxed warnings covering cardiovascular, GI, and rare dermatologic events. High-dose NSAID courses in ankylosing spondylitis raise ischemic heart disease and stroke risk according to longitudinal cohort analyses. Clinicians screen patients more rigorously and limit duration, trimming prescription volumes. Added monitoring inflates treatment costs, weighing on the NSAIDs market despite unflagging underlying demand.

Patent Cliffs & Price Erosion for Blockbuster Brands

Prolensa lost exclusivity in 2024 after generic bromfenac approval, illustrating how niche ophthalmic NSAIDs also face erosion. Broader 2025 losses across the pharmaceutical sector intensify price competition, and payers leverage multiple suppliers to negotiate discounts. Brand owners pivot to novel delivery systems and combination products, yet generic alternatives squeeze revenue per unit in mature segments of the NSAIDs market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Non-steroidal Anti-Inflammatory Drugs (NSAIDs) Market Segment Analysis

By Route of Administration:

Topical Formulations Drive Safety RevolutionOral products kept 55.92% of NSAIDs market size in 2025 because of physician familiarity and patient convenience. Topical options, however, climb at 6.18% CAGR as risk-averse prescribers recommend localized therapy for osteoarthritis and soft-tissue injuries. Advanced hydrogels now match oral efficacy without increasing GI or cardiovascular events.

Fixed-dose combination patches embed permeation enhancers that sustain release for up to 12 hours, reducing dosing frequency and boosting adherence. Regulatory guidance encourages topical NSAIDs in older adults with comorbidities. Consequently, manufacturers expand plant capacity for gels and sprays to capture incremental volumes in the NSAIDs market.

By Drug Class:

COX-2 Selectivity Balances Efficacy and SafetyNon-selective inhibitors retained the largest 61.77% slice of NSAIDs market size in 2025 by virtue of cost and broad indication labeling. COX-2 agents escalate at 6.32% CAGR as new evidence refines cardiovascular risk assessments and highlights GI protection. Emerging candidates optimize selectivity ratios and half-lives to widen their therapeutic window.

Pipeline products also aim for dual-target inhibition, modulating prostaglandin and leukotriene pathways simultaneously to tackle inflammation with fewer side effects. If late-stage trials confirm benefit, non-selective dominance could erode, reshaping drug-class revenue mix within the NSAIDs market.

By Application:

Migraine Treatments Accelerate Through InnovationArthritis accounted for 40.68% of NSAIDs market size in 2025 on the back of large, chronic patient pools. Migraine formulations register the quickest 6.12% CAGR thanks to fixed-dose innovations such as meloxicam plus rizatriptan, which achieved 77% sustained pain freedom in phase 3 trials.

Broader neurology adoption follows updated treatment pathways that favor NSAID-triptan combinations for moderate attacks. Ophthalmic, dysmenorrhea, and fever-flu indications broaden the clinical footprint, ensuring diversified revenue streams for companies active in the NSAIDs market.

By Distribution Channel:

E-commerce Transforms Access PatternsRetail pharmacies commanded 45.98% of NSAIDs market share in 2025 through professional counseling and immediate fulfillment. Online pharmacies post the highest 6.41% CAGR as consumers embrace direct-to-door delivery, price transparency, and auto-refill features.

National chains blend digital platforms with local pickup to guard share, while pure-play e-pharmacies ramp marketing in underserved rural areas. Hospital outlets retain relevance for injectable and peri-operative needs, but omnichannel convenience is redefining demand capture strategies in the NSAIDs market.

Geography Analysis

North America Non-steroidal Anti-Inflammatory Drugs (NSAIDs) Market

North America held 41.35% of revenue in 2025, supported by high healthcare outlays and opioid-replacement policies that prioritize NSAID prescriptions. Regulatory frameworks are robust, and insurers push cost-effective generics, creating both stability and price pressure in this zone of the NSAIDs market.

APAC Non-steroidal Anti-Inflammatory Drugs (NSAIDs) Market

Asia-Pacific records the fastest 6.29% CAGR through 2031 as populations age and middle-class consumers seek affordable pain relief. Local manufacturers scale production, and governments integrate essential NSAIDs into reimbursement lists, accelerating access. OTC use is widespread, yet physician visits per capita are rising, bringing more diagnosed arthritis and migraine cases into formal care.

EMEA and South America Non-steroidal Anti-Inflammatory Drugs (NSAIDs) Market

Europe retains sizeable volume anchored by universal health systems, yet strict EMA evaluations slow new launches and emphasize pharmacovigilance. Emerging regions in the Middle East, Africa, and South America gain momentum as infrastructure improves. Multinationals partner with domestic distributors to navigate regulatory nuance and economic swings while unlocking incremental demand in the global NSAIDs market.

Competitive Landscape

The NSAIDs market is moderately fragmented. Leading firms such as Bayer, Pfizer, and Johnson & Johnson leverage legacy brands, broad portfolios, and global supply chains. Generic specialists like Lupin and Glenmark compete on price and regulatory agility, accelerating erosion after patent expiry for oral and ophthalmic products.

Top contenders invest in AI screening to find new indications or reformulate existing actives, compressing R&D timelines and cost. Novel topical devices, iontophoretic systems, and preservative-free eye drops create premium niches. Partnerships with digital health startups provide patient-support apps that differentiate offerings in a crowded NSAIDs market.

Consolidation prospects rise as mid-tier pipelines thin and scale advantages grow in sourcing active pharmaceutical ingredients (APIs) under tightened quality standards. Sustainability goals add another layer of competition, with firms marketing greener synthesis routes to hospital buyers seeking lower environmental footprints.

Non-steroidal Anti-Inflammatory Drugs (NSAIDs) Industry Leaders

Pfizer Inc.

Johnson & Johnson

Bayer AG

Sanofi S.A.

Haleon plc

- *Disclaimer: Major Players sorted in no particular order

Non-steroidal Anti-Inflammatory Drugs (NSAIDs) Market Companies Covered in this Report

- Pfizer

- Bayer

- Johnson & Johnson (McNeil)

- Haleon plc

- Reckitt Benckiser Group

- Sanofi

- Horizon Therapeutics

- Sun Pharmaceuticals Industries

- Assertio

- Perrigo Company

- Iroko Pharmaceuticals

- Viatris

- Novartis

- Dr. Reddy’s Laboratories Ltd

- Teva Pharmaceutical Industries

- Boehringer Ingelheim

- Abbvie

- Endo International

- Hikma Pharmaceuticals

- Orion

Read Analysis of Non-steroidal Anti-Inflammatory Drugs (NSAIDs) Companies

Recent Industry Developments in Non-steroidal Anti-Inflammatory Drugs (NSAIDs) Market

- January 2025: Axsome Therapeutics received FDA approval for Symbravo, a meloxicam–rizatriptan tablet for acute migraine in adults, achieving 77% sustained pain freedom

- January 2025: Vertex Pharmaceuticals won FDA clearance for Journavx (suzetrigine), a Na V 1.8 blocker for acute pain, raising competitive stakes for NSAID incumbents.

- April 2024: Glenmark Therapeutics secured approval for generic Advil Dual Action (ibuprofen 125 mg + acetaminophen 250 mg) in the United States.

- February 2024: The EMA recommended refusal of Ibuprofen NVT 400 mg soft capsules over bioequivalence issues with Nurofen Rapid 400 mg.

Non-steroidal Anti-Inflammatory Drugs (NSAIDs) Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the non-steroidal anti-inflammatory drugs (NSAIDs) market as the worldwide sales value of prescription and over-the-counter medicines whose main action is reversible inhibition of cyclo-oxygenase-1 and/or cyclo-oxygenase-2 enzymes, supplied in oral, topical, parenteral, or transdermal forms. According to Mordor Intelligence, this universe generated USD 24.11 billion in revenue in 2025 and is projected to expand steadily through 2030.

Scope Exclusions: Combination analgesics where the NSAID is not the primary active ingredient and veterinary-only products are left outside our frame.

Segments Covered in This Report

- By Route of Administration

- Oral

- Parenteral

- Topical

- Others

- By Drug Class

- Non-selective COX Inhibitors

- COX-2 Selective Inhibitors

- By Application

- Arthritis

- Migraine & Headache

- Ophthalmic Conditions

- Fever & Flu

- Dysmenorrhea

- Others

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- E-commerce

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia & New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts spoke with rheumatologists, hospital pharmacists, and large community-pharmacy buyers across North America, Europe, and Asia-Pacific, and we ran short online polls with chronic-pain patient advocates. These interactions clarified real-world generic adoption, topical switch rates, and willingness-to-pay thresholds that secondary data alone cannot reveal.

Desk Research

We began with authoritative public datasets such as the US FDA National Drug Code directory, European Medicines Agency sales notices, WHO Defined Daily Dose statistics, CDC ambulatory care surveys, and UN DESA aging population tables, which help us track volume baselines and dosing norms. Our team then layered in company filings, investor presentations, and shipment codes for ibuprofen, naproxen, and diclofenac extracted from UN Comtrade to verify cross-border flows. Paid utilities like D&B Hoovers provided revenue splits that tighten price corridors. The sources listed illustrate our approach; many additional outlets were reviewed, cross-checked, and archived for consistency.

Market-Sizing & Forecasting

We reconstruct the 2025 baseline through a top-down parse of prescription volumes and OTC unit shipments, multiplied by weighted average selling prices. We then corroborate totals with selective bottom-up supplier roll-ups. Key variables include population aged 65+, arthritis prevalence, NSAID defined-daily-doses per capita, COX-2 uptake, retail e-commerce share, and inflation-adjusted ASPs. A multivariate regression projects each driver to 2030; where gaps appear, results are stress-tested against expert consensus before finalization.

Data Validation & Update Cycle

Outputs pass automatic variance checks versus historical FDA recall counts, quarterly earnings, and IMS sell-in audits. Senior reviewers scrutinize anomalies before sign-off. Our model refreshes annually, with interim updates triggered by boxed warnings, major recalls, or currency shocks.

How Mordor Intelligence's Non-steroidal Anti-Inflammatory Drugs (NSAIDs) Market Size Compares to Other Published Estimates

Published estimates often diverge because firms adopt different inclusion rules, price stacks, and refresh cadences.

Key gap drivers include rival studies omitting OTC gels, locking exchange rates to a single year, or assuming flat generic erosion, whereas we apply dynamic ASP compression and topical migration trends validated in 2025 interviews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 24.11 Bn (2025) | Mordor Intelligence | - |

| USD 22.58 Bn (2024) | Global Consultancy A | Excludes OTC topical formats; single-step currency conversion |

| USD 25.84 Bn (2025) | Industry Journal B | Relies on shipment value extrapolation without parallel-trade adjustment |

Global Consultancy A pegs its narrower 2024 market at USD 22.58 billion, while Industry Journal B reports USD 25.84 billion for 2025.

These comparisons show that our disciplined scope selection, live data inputs, and yearly updates deliver a balanced, transparent baseline that decision-makers can trace and replicate.

Key Questions Answered in the Report

What is the current value of the NSAIDs market and its growth outlook?

The market is valued at USD 25.48 billion in 2026 and is projected to hit USD 33.57 billion by 2031 at a 5.67% CAGR.

Which region is growing fastest in the NSAIDs market?

Asia-Pacific is forecast to expand at 6.29% CAGR through 2031 due to wider insurance coverage, local manufacturing scale-ups, and strong OTC demand.

Why are topical NSAIDs gaining popularity?

Topical gels and patches offer comparable pain relief with fewer GI and cardiovascular side effects, making them the preferred option for high-risk patients.

How are patent expirations influencing NSAID prices?

Expired exclusivities invite generic competition, which presses down price points and shifts brand focus toward new delivery platforms or fixed-dose combinations.

What role does e-commerce play in NSAID distribution?

Online pharmacies are growing at 6.41% CAGR as consumers prioritize convenience, transparent pricing, and home delivery, prompting retailers to adopt omnichannel models.

Are NSAIDs replacing opioids in moderate pain management?

Yes, recent guidelines recommend NSAIDs as first-line therapy for many moderate pain conditions because they provide effective relief without addiction risk.

Page last updated on: