Alexipharmic Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.02 Billion |

| Market Size (2031) | USD 6.55 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

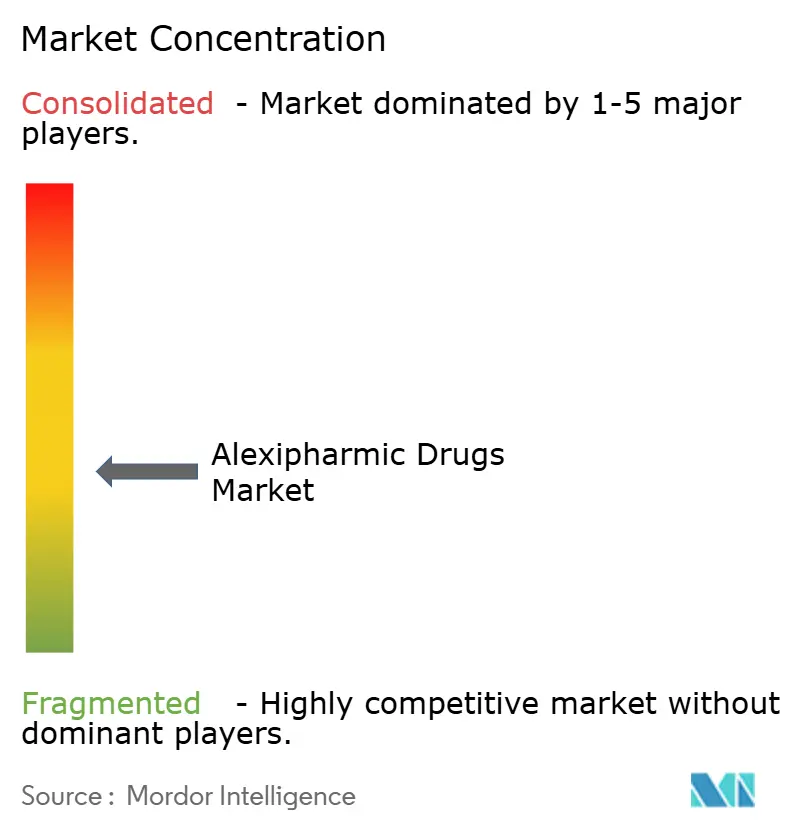

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Alexipharmic Drugs Market Analysis by Mordor Intelligence

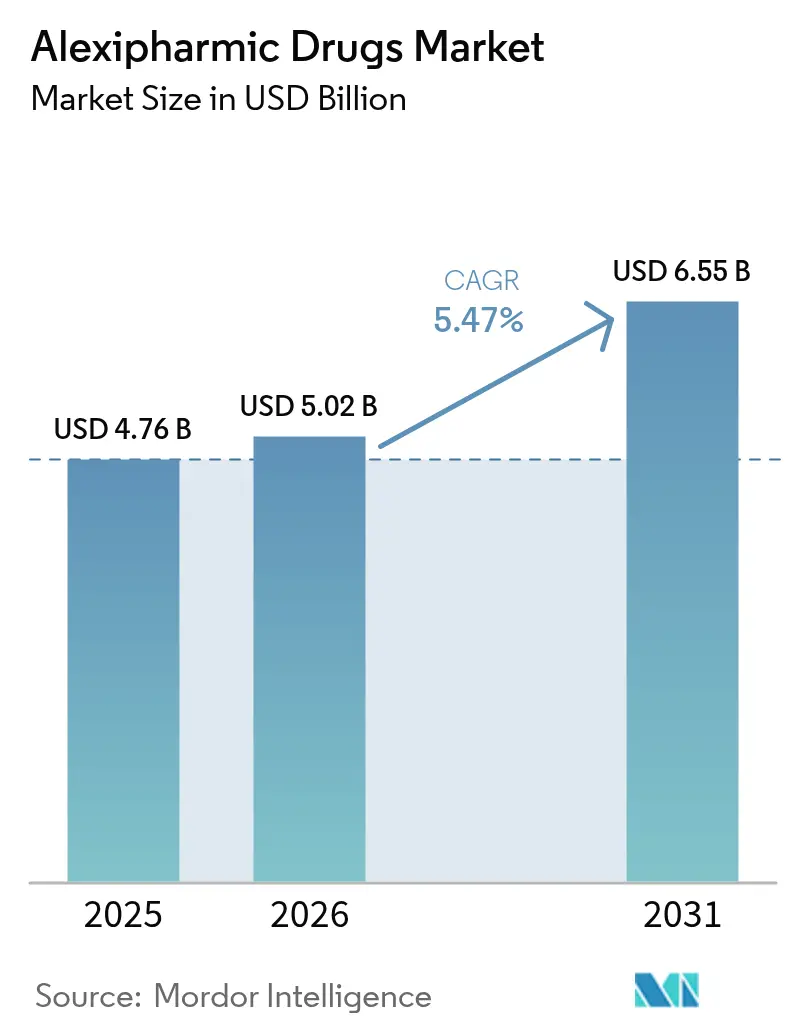

Alexipharmic Drugs market size in 2026 is estimated at USD 5.02 billion, growing from 2025 value of USD 4.76 billion with 2031 projections showing USD 6.55 billion, growing at 5.47% CAGR over 2026-2031.

Rising global overdose cases, heightened industrial exposure to toxic compounds, and supportive laws that mandate over-the-counter access to critical antidotes are the main growth engines. Government procurement of naloxone, increasing venture capital inflows into smart delivery devices, and the pharmaceutical sector’s emphasis on rapid-acting formulations extend the addressable patient pool. Demand is further reinforced by community harm-reduction programs and tighter employer liability standards that encourage stockpiling across non-hospital sites. Even so, reimbursement pressures and raw-material shocks add volatility to margins, compelling manufacturers to diversify sourcing and invest in lean production lines. Heightened counterfeit-drug incidents in developing economies also shift geographic priorities for new product launches.

Key Report Takeaways

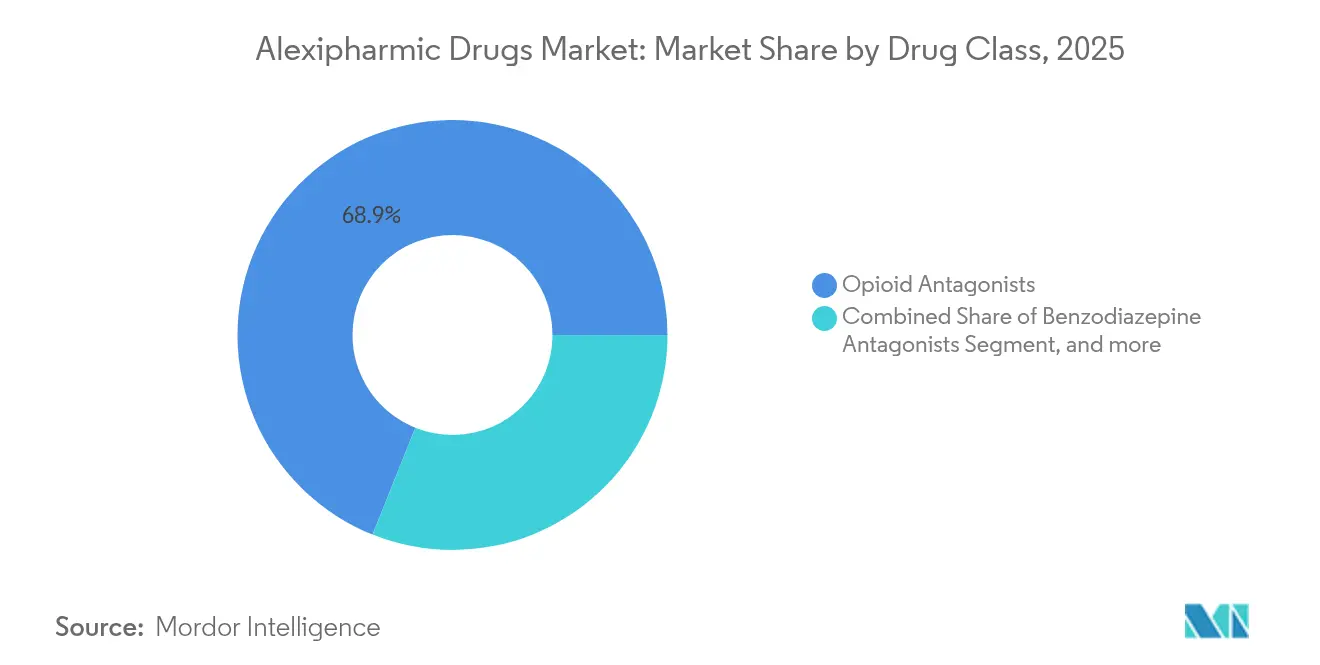

- By drug class, opioid antagonists led with 68.94% revenue share in 2025; cyanide antidotes are forecast to advance at an 8.33% CAGR through 2031.

- By route of administration, parenteral delivery accounted for 61.25% of the alexipharmic market share in 2025 while intranasal products record the highest projected CAGR at 7.55% to 2031.

- By formulation, solutions commanded 43.28% of the alexipharmic market size in 2025; nasal sprays are on track to expand at a 9.92% CAGR during the review period.

- By distribution channel, hospital pharmacies held 52.20% share of the alexipharmic market size in 2025 and retail or community outlets exhibit a 6.05% CAGR outlook.

- By geography, North America captured 38.92% of 2025 revenue, whereas Asia Pacific is climbing at a 8.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Alexipharmic Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising dependence on psychoactive & narcotic drugs | +1.2% | Global with focus on North America and Europe | Long term (≥ 4 years) |

| Regulatory backing for medication-assisted treatment | +0.8% | North America and EU, expanding into Asia Pacific | Medium term (2-4 years) |

| Escalating synthetic-opioid fatalities in lower-income regions | +0.9% | Asia Pacific core, spill-over to MEA and South America | Short term (≤ 2 years) |

| Surge in counterfeit-drug poisonings triggering naloxone demand | +0.7% | Global with hotspots in North America and Asia Pacific | Short term (≤ 2 years) |

| Government-funded community naloxone programs | +0.6% | North America and EU, pilot schemes in Asia Pacific | Medium term (2-4 years) |

| Venture funding in intranasal & auto-injector tech | +0.5% | Global with R&D clustering in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Dependence on Psychoactive & Narcotic Drugs

Synthetic opioids that exceed fentanyl potency now circulate in United States and European street markets, widening the overdose severity spectrum and prompting demand for higher-dose naloxone kits.[1]Damien Gayle, “Nitazenes: Potent New Synthetic Opioids Emerging in Europe,” theguardian.com Gaps in rapid detection technology amplify accidental exposure risks, pushing hospitals and first responders to maintain larger inventories. Distribution networks in Latin America and Southeast Asia are beginning to mirror North American consumption patterns, suggesting the upward trend in antidote volumes will persist. Pharmaceutical firms answer the need by co-developing concentrated formulations that overcome receptor saturation. Broader availability of test strips for new analogs is expected to support earlier intervention yet will not reduce naloxone demand in the short term.

Regulatory Backing for Medication-Assisted Treatment (MAT)

The 2024 FDA decision reclassifying Narcan nasal spray to over-the-counter status erased prescription barriers, allowing pharmacies, schools, and public venues to stock the antidote without clinician oversight. Medicare and Medicaid now reimburse naloxone with minimal copay in 42 states, embedding recurring purchase orders into public budgets. Europe follows similar cues with centralized EMA approvals that shorten lead times for new intranasal launches. These moves transform community harm-reduction initiatives from grant-funded pilots into permanent public health fixtures. As more countries embed naloxone coverage into national formularies, the alexipharmic market gains a predictable baseline of volume growth independent of broader economic cycles.

Escalating Synthetic-Opioid Fatalities in Lower-Income Regions

Industrializing pockets of Asia Pacific confront rising fentanyl and tramadol trafficking that outpaces enforcement capacity, driving double-digit spikes in overdose mortality across Vietnam, the Philippines, and central India. Lower insurance penetration compels families to rely on public hospitals, which now lobby governments for larger antidote budgets. Japan’s approval of diazepam nasal spray reflects regional momentum for innovative delivery beyond IV lines, indicating future cross-label expansions. Heavy manufacturing growth in Indonesia and Bangladesh also raises cyanide exposure incidents that create parallel demand for hydroxocobalamin and sodium nitrite kits. In combination, these pressures accelerate the alexipharmic market’s shift toward Asia Pacific.

Surge in Counterfeit-Drug Poisonings Triggering Naloxone Demand

Seizures of fentanyl-laced counterfeit tablets climbed to 115 million units in 2023, and hospital consultations for 15-34-year-olds spiked accordingly. Patients often believe they are ingesting legitimate oxycodone, forcing emergency departments to treat opioid toxicity among demographics traditionally outside substance-use surveillance. Pentobarbital admixtures complicate the clinical picture because naloxone alone is insufficient, spurring new interest in multi-component antidote regimens. Pharmaceutical distributors adapt by offering bundled overdose response packs with step-wise dosing guides. Localized hotspots, such as Arizona and British Columbia, experience inventory depletion cycles that test supply chain agility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy & hospitalization costs | -0.4% | Global with pronounced effect in North America | Medium term (2-4 years) |

| Rising popularity of abuse-deterrent opioid formulations | -0.3% | North America and EU, slow uptake in Asia Pacific | Long term (≥ 4 years) |

| Stigma limiting patient access & prescription fill rates | -0.5% | Global, concentrated in rural and underserved zones | Short term (≤ 2 years) |

| Supply-chain shocks for key antidotes’ APIs | -0.6% | Global with API manufacturing hub in Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Therapy & Hospitalization Costs

Out-of-pocket charges for a two-pack OTC naloxone carton average USD 44 in the United States, deterring purchase among uninsured households.[2]Centers for Medicare & Medicaid Services, “Out-of-Pocket Cost Analysis for OTC Naloxone,” cms.gov Hospital buyers weigh antidote restocking against high-volume generics and may under-order products with uncertain turnover. Specialized cyanide antidotes can exceed USD 1,200 per adult dose, discouraging rural facilities from keeping full treatment courses. Insurance reimbursement disparities across states deepen gaps, leaving clusters of counties without 24-hour antidote access. Varying co-payment levels under Medicaid further fragment purchasing power, reducing the uniformity of demand and dampening the alexipharmic market CAGR.

Rising Popularity of Abuse-Deterrent Opioid Formulations

Pharmaceutical innovations like Ensysce’s PF614 incorporate chemical barriers that resist crushing or heat extraction, aiming to curb misuse. The FDA expedited several such applications in 2025, reinforcing a prevention strategy that could taper naloxone volumes over time. Although determined users can defeat many barriers, initial evidence shows slower diversion rates for new brands. Payers encourage physicians to prescribe these formulations by offering lower deductibles, redirecting prescription patterns away from traditional opioids. Widespread adoption remains a decade away, but early momentum injects an element of demand uncertainty into the alexipharmic market forecast.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Opioid Antagonists Hold Structural Lead

Opioid antagonists commanded 68.94% of 2025 revenue, underscoring the synthetic opioid emergency that dominates clinical headlines across developed economies. Naloxone’s switch to OTC status multiplied consumer touchpoints, from gas stations to college campuses, cementing the segment’s lead. Cyanide antidotes, while niche, exhibit the fastest 8.33% CAGR because industrial regulators now require on-site kits at electroplating plants and chemical warehouses. Benzodiazepine reversal agents show mid-single-digit growth tied to elective surgery volumes. Heavy-metal chelators gain episodically during environmental incidents yet contribute steady baseline turnover. Competitive profiles vary: opioid antagonists face generic entrants that suppress price, whereas cyanide antidotes benefit from patent-protected formulations, enabling premium margins.

Product expansion into multi-dose blister packs and child-resistant nasal applicators illustrates how packaging innovation supports broader user adoption across home, workplace, and first-responder settings. Manufacturers differentiate through shelf-life extensions and tamper-evident seals that satisfy stringent procurement criteria.

By Route of Administration: Parenteral Dominance Faces Community-Led Shifts

Parenteral formats represent 61.25% of 2025 sales because emergency departments prioritize intravenous onset that achieves peak plasma levels within minutes. Intranasal products, however, log a 7.55% CAGR as regulators approve self-administered sprays for layperson use, especially in public venues lacking clinical staff. Oral and sublingual deliveries address maintenance therapy rather than acute reversal and thus carve a smaller but steady niche.

Hospitals continue to demand vial stability under variable refrigeration conditions, prompting R&D into heat-tolerant formulations. Meanwhile, community health programs evaluate spray devices that provide audible click confirmation, reducing training complexity and error risk. Manufacturers that align dose strengths with emerging high-potency opioid threats gain formulary preference.

By Formulation: Solutions Remain Workhorse Yet Sprays Accelerate

Solutions captured 43.28% of 2025 global revenue owing to their flexible use across IV, IM, and oral pathways. They require minimal re-validation when new strengths are introduced, keeping regulatory costs low. Nasal sprays record a superior 9.92% CAGR on the back of consumer preference and retailer logistics that favor compact, room-temperature products. Auto-injectors, once dominant, now grapple with high unit prices and battery disposal concerns, yet they sustain healthy volumes in school districts and factory sites where staff training time is limited.

The alexipharmic market size for solution formulations is set to outpace vials in multiple European countries by 2028 as centralized procurement bodies standardize publicly funded overdose kits. Continued advances in micro-dispensing pumps boost dose accuracy while lowering unit costs, strengthening the segment’s competitiveness.

By Distribution Channel: Hospitals Anchor Sales, Retail Outlets Surge

Hospital pharmacies retained 52.20% of 2025 revenue because antidote stocking is mandated under many accreditation standards. Bulk-purchase discounts and inventory management systems give hospitals leverage to negotiate favorable terms. Retail and community pharmacies, benefiting from OTC rules, rise at 6.05% CAGR through 2031 as chain drugstores devote entire shelf sections to emergency medication.

Employer-sponsored health stations and EMS fleets compose the smallest but rapidly diversifying group, reflecting broader workplace safety mandates. Distributors experiment with vending-machine pilots at transport terminals, illustrating inventive ways to extend reach without high operating overhead.

Geography Analysis

North America retains leadership with 38.92% of global sales in 2025. Federal investments such as BARDA’s five-year naloxone framework agreement deliver predictable offtake that stabilizes factory capacity planning. Harm-reduction strategies embed antidotes into police cruisers and public libraries, expanding non-clinical utilization points. Overdose mortality eased 27% from 2023 to 2024, signaling effectiveness of widespread distribution, yet the persistence of nitazenes sustains bulk ordering. Canada’s national plan funds free naloxone for high-risk prescriptions, and Mexico’s new industrial safety code mandates cyanide antidote kits in gold-mining districts, contributing incremental upticks.

Asia Pacific posts the fastest 8.76% CAGR and is poised to surpass Europe by 2031. Industrial build-out raises cyanide exposure in metal finishing, prompting local labor ministries to enforce on-site antidote inventory. Japan approved diazepam nasal spray in 2024, signaling broader acceptance of non-injectables, while China’s generics pipeline lowers price barriers for municipal emergency stockpiles. India’s role as API powerhouse positions domestic firms to backfill global shortages and capture value through export-linked incentives. Emerging economies in Southeast Asia face counterfeit-drug influxes that increase community naloxone demands, steering humanitarian aid budgets toward antidote procurement.

Europe maintains steady mid-single-digit growth anchored by EMA’s centralized procedure that eases cross-border circulation of new formulations. Post-Brexit recalibration diverted some volume from UK-centric hubs to continental warehouses, but also invited new entrants that leverage local fill-finish lines. Regional green-transition policies target reduction of cyanogenic emissions, indirectly boosting demand for detoxification agents during remediation projects. Abuse-deterrent opioid uptake is highest in Scandinavian markets, which could temper long-term naloxone volumes yet will take several years to materially influence totals.

Competitive Landscape

The alexipharmic market is moderately fragmented. Emergent BioSolutions faces OTC competitors that erode branded NARCAN margins, prompting the company to pitch educational value-add services to preserve contracts. Amphastar diversifies into biosimilar insulin to hedge exposure to price-sensitive emergency drugs, illustrating portfolio hedging strategies. ARS Pharmaceuticals leverages its intranasal technology platform across multiple acute therapies, using shared manufacturing assets to lower unit economics.

Technology-centric start-ups exploit gaps in user-friendly administration; Micron Biomedical’s microneedle patch targets layperson use in industrial sites where IV lines are impractical. Established players counter by filing incremental device patents and forging distribution alliances with national pharmacy chains to lock in shelf space. API security remains a differentiator firms that dual-source precursors or maintain captive synthesis capacity gain resilience that appeals to hospital group-purchasing organizations. Over the forecast period, the competitive landscape will likely experience selective consolidation as larger stakeholders purchase niche innovators to close delivery-technology gaps.

Alexipharmic Drugs Industry Leaders

Ethypharm S.A.

Bausch Health Companies Inc.

Fresenius Kabi

Mylan N.V. (Viatris)

Emergent BioSolutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Amphastar Pharmaceuticals reported mixed Q1 2025 financial results with revenue of USD 170.5 million, noting a 20% increase in Primatene Mist sales while facing competitive pressures in glucagon and epinephrine products. The FDA accepted the company's Biologics License Application for insulin aspart, marking expansion into biosimilar insulin offerings that complement their emergency medication portfolio.

- April 2025: Glenmark Pharmaceuticals and Alkem Laboratories launched generic versions of empagliflozin following patent expiry on March 11, 2025, with prices significantly lower than the original branded product, illustrating competitive dynamics in pharmaceutical markets that could extend to antidote categories.

- March 2025: Shionogi announced that ensitrelvir demonstrated a 67% reduction in COVID-19 risk in the Phase 3 SCORPIO-PEP trial for post-exposure prophylaxis, receiving FDA Fast Track designation and highlighting regulatory support for innovative antiviral approaches.

Global Alexipharmic Drugs Market Report Scope

Alexipharmic drugs are medications that act as an antidote used to reverse or reduce the effects of a drug overdose, and drug poisoning. These are employed in an emergency shot to save lives quickly and can be used to defend against various types of microbial infections. As per the scope of the report, various alexipharmic drugs used in drug overdose and poisoning cases were described in detail.

| Opioid Antagonists |

| Benzodiazepine Antagonists |

| Cyanide Antidotes |

| Heavy-Metal Chelators |

| Others |

| Parenteral |

| Intranasal |

| Oral & Sublingual |

| Solution |

| Auto-Injector |

| Nasal Spray |

| Tablets & Capsules |

| Hospital Pharmacies |

| Retail & Community Pharmacies |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Opioid Antagonists | |

| Benzodiazepine Antagonists | ||

| Cyanide Antidotes | ||

| Heavy-Metal Chelators | ||

| Others | ||

| By Route of Administration | Parenteral | |

| Intranasal | ||

| Oral & Sublingual | ||

| By Formulation | Solution | |

| Auto-Injector | ||

| Nasal Spray | ||

| Tablets & Capsules | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail & Community Pharmacies | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the alexipharmic market in 2026?

The alexipharmic market size is USD 5.02 billion in 2026 with a forecast value of USD 6.55 billion by 2031.

Which region is growing fastest for antidote demand?

Asia Pacific is registering a 8.76% CAGR, outpacing all other regions due to industrial expansion and synthetic drug exposure.

What drug class holds the highest revenue share?

Opioid antagonists lead at 68.94% of 2025 sales, driven by widespread naloxone adoption.

Why are intranasal antidotes gaining popularity?

Intranasal formats remove needle handling, allow OTC sales, and fit community distribution models, supporting a 7.55% CAGR through 2031.

What is the major restraint facing manufacturers?

Supply-chain shocks for critical APIs remain the most significant drag, subtracting an estimated 0.6 percentage points from forecast CAGR.

Page last updated on: